By Geoff Simmons*

Our tax system needs reform, but the Green Party’s wealth tax isn’t it.

The problems with our tax system

One Tax Working Group report after another has pointed out the hole in our tax system – around the treatment of property. We pay some of the highest tax rates on most investments – businesses, Kiwisaver, bank deposits - in the Western World. But when it comes to property, we have some of the lowest taxes.

The difference is what drives us to invest more in property (and less in business) than any other country in the world. The sad fact is that it is easier to make money speculating on property than it is investing in businesses that actually create jobs and exports. Property prices are rising but we are restricting our ability to pay for those higher prices – our incomes.

Inland Revenue’s own data shows that half of our wealthiest citizens don’t even pay the top rate of income tax. The major loophole they exploit in order to amass their fortunes is property.

Our tax system has problems, that much is clear. But just as Labour’s flawed capital gains tax wasn’t the answer, neither is the Green Party’s wealth tax.

The Greens’ wealth tax will destroy the incentive to invest

There has been a lot of debate about whether wealth taxes have worked overseas. They have worked in Switzerland, but failed in France. The key difference between the two is the rest of the tax system. Switzerland’s company tax rate is 8%, so the wealth tax is doing the heavy lifting in terms of taxing the return from investments. In that context a wealth tax hits all assets reasonably evenly – including property. In France the company tax rate is 31%, so a 1.5% wealth tax on top of that really puts the squeeze on, hence it is avoided by shifting the fortune to another jurisdiction.

We need to take into consideration the rest of the tax system. Remember we already tax the returns from investment in business (profits, dividends) at one of the highest rates in the world. What happens when we add a wealth tax onto that?

Here are some rough and ready numbers on the Green Party wealth tax and why it would kill off productive investment:

The average real return on investment is 5% (that is probably generous these days). That is a nominal return of 7%. Remember it is the nominal return that gets taxed! Nominal return taxed at top marginal tax rate of 33% = 2.3% tax. So the existing 33% tax on profit already takes roughly half of the real return on investment. The Tax Working Group pointed that out. In real terms an investor is left with a 2.7% return after income tax. If someone has a $2m fortune, they would face a 2% tax on the marginal dollar invested. That leaves 0.7% real return on investment. Add in the 42% tax on income over $150,000 and your return would be 0.06%.

Why would you bother with the risk for a return of less than 1% on average? Almost half of investments will be going backwards in a given year. The answer is you wouldn't bother. You'd shift your fortune to Australia instead. The Greens’ wealth tax would kill off productive investment from high net worth individuals. This is at a time we need to invest $1b every year as a nation to achieve our emissions reductions targets. That is a bit of an own goal from the-Green Party.

TOP’s alternative

TOP’s proposal is that all significant assets (in practice it would be mainly property) should pay as much tax as a bank deposit. Assuming a bank deposit is earning 3% (yes, yes, I know it isn’t right now – who knows what the new “normal” brings) and you are paying 33% marginal tax rate that equates to a 1% tax on the equity held in property each and every year. Note that this tax is levied on the equity in an asset. In other words, the value of the asset minus the debt held against it.

The Tax Working Group called this the Risk Free Rate Method or RFRM. We prefer to call it a property tax. The big advantage of it is that it broadens the tax system. This is the ideal way to collect tax – tax everything a little bit.

It also plugs the tax loophole around property. It would end the desire to speculate on property – killing off capital gain. Instead of land-banking, people that own land would be incentivised to build and rent out their property to earn a return on their investment.

Because it is a minimum return, it doesn’t double tax productive assets like the wealth tax does. Instead it says if you are earning at least a 3% taxable return on this asset over time, you don’t need to pay any more tax.

Unlike the Greens’ proposal, TOP are not reliant on this tax change to raise revenue to pay for our spending promises. TOP want this to be tax neutral, so the revenue could be used to reduce the tax on other investments, in particular Kiwisaver. This also allows us to bargain with Establishment Parties who may not like a tax on the family home – for example there could be a threshold below which the tax doesn’t apply.

*Geoff Simmons is leader of The Opportunities Party.

127 Comments

If you want to introduce a land tax then call it a land tax and be done with it. All this nonsense about equality with a bank deposit interest ? So if bank rates rise to 10% you are going to tax properties at 3.3% ? Get real.

In our current world where rates are almost zero and returns on property are below 4% and declining this proposal has as much appeal as the Greens policy.

CGT is the way forward as it a small stamp duty. Why try and recreate the wheel ?

It does seem especially odd as nominal rates fall to zero and we consider a future with possible negative rates. What then?

Poorly thought out policies rarely consider actual scenarios.

Let's assume rather than negative rates we have zero rates. That means zero IRD revenue from property. How does that broaden the tax base ?

Yes, under the new 'normal' (which TOP is trying to say is uncertain yet) the only types of taxes that work are transaction taxes (of which GST is a type), death taxes and land taxes.

The new normal is that there isn't normal. It is a series of crisis increasing in freqency. The new normal is a trend.

well, capital gain tax, labour tax etc. all transactionl taxes. an annual tax on unrealised gain is not.

Add environmental taxes

- vehicle & industry air pollution tax proportionate to the health effects

- internalisation of full road crash costs by road users

- carbon tax

- waterway & nitrogen taxes on farmers not meeting national standards

I'm still on the fence between the use of environmental regulation versus environmental taxation as a means to an end (the end being a healthy atmosphere/environment). The problem with polluter-pays approaches (such as the ETS) is that those with the ability to pay, still pollute.

Take private vehicle use in Auckland for example. We could simply designate 50% of all dual carriage lanes as bus lanes only. The only cost associated with that is greater traffic congestion for private vehicle use (as well as the cost associated with improving the network)..

land tax = Rates - which goes up year after year -- and is not going down anytime soon

that's what happens when you let politicians defer maintenance and you get a population explosion. You end up having to pay for it sometime! Rates are actually bugger all in the grand scheme of things. People spend more on their telco bills than roads, water and waste.

Where the hell do you live? I pay about $4.3k per year on rates, my telco bill is about $1350. Hell, my power bill is only $2700 or so.

Yes, where do you live.. my major expense in Christchurch is rates. $8400 pa for a 240sqm home on a 550sqm section. Its an indirect tax

Why all assets must pay tax, even if they do not produce a return? do we expect everyone who does not work to pay tax, because labor has to pay tax? also why should we tax on "potential" as opposed to realised? it is like taxing a young 20 years old a lot more because their present value is much higher than a 60 years old CEO of a listed company.

when you can tax actual capital gains when they are actually realized (and you need to account for inflation) why you need all this madness?

NZ has a distortion that significantly favors houses over other forms of investment. A Good article worth reading https://www.newsroom.co.nz/as-safe-as-houses. However, we tax offshore equity investments punitively whether direct or via kiwisaver on an UNREALISED BASIS. We tax the FX movements on foreign denominated investments on an UNREALISED BASIS.

Could you imagine the outrage if the property investors in Auckland since 2011 paid tax based on the increment in value of the properties each year when they were not even sold. But the 3.3 million in kiwisaver are oblivious to this stealth tax that is having a major impact on how much they have for retirement.

1) I agree with your argument on unfair taxing of kiwisaver. It is so because the convenience of the tax man is given priority to taxation principals and the equitable treatment of all investments. It is too hard to actually monitor actual gains from investments, so we do it that way (absolute non-sense, specially relating to kiwi-saver investments, where every single transaction is duly recorded, accounted for etc to the cent).

2) As far as I know, capital gains are generally exempted from being taxed, regardless of the type of asset they are earned on (exception being the taxation of . E.g. if you invest in a business, grown it and then sell it for a significant gain, the gain is not taxed. So I do not see the significant distortion in favor of property here. The significant distortion in favour of property (in relation to other assets) in my humble opinion is not in taxation but in ability to access credit. The other much debated "advantage" is the imputed rent that a house owner earns over someone who rents. which is absolute non-sense. When you add up ownership costs (interest, rate, insurance, upfront gst paid on a house) the actual rental income is much smaller than often portrayed. My personal opinion is in agreement with the article you linked: i.e. there is an absolute lack of investment opportunities in NZ given its economic potential and limitations. The credit accessibility, coupled with lack of opportunity elsewhere, plus ability to leverage property, plus immigration and credit affordability (interest rate) plus subsidisation (accommodation supplement) have all come together to create a perfect storm for property. Tax is only a very small part of the story in my humble opinion.

The FIF regime changes bought in on 1 April 2007 were specifically to grab the tax from Kiwisaver funds that were starting on 2 July 2007. It enabled the government to get a guaranteed tax take of 28% on 5% income on all kiwisaver to the extent it was in offshore equities. Prior to this NZ did not tax investments in the FIF regime that were in the grey list: Australia, Britain, Canada, Germany, Japan, Norway and the United States. This was removed in 2011. Just before the regime was enacted a last minute exemption was given for Australian equities. So the reason for it is it was a great STEALTH TAX that Michael Cullen introduced to raise a lot of money. Some years the NZ Superfund pays $550m in FIF Tax on $550m in actual income received.

The negative tax consequences of investing in foreign shares instead of NZ & AU shares also significantly disadvantages investors saving for retirement.

Assuming I invested $100k in Nov 12 as follows and held them in the following two investments: Xero Limited. My gain is 1075%. Today my $100k has a market value of $1.075m. Xero pays no dividends so there has been no NZ tax payable. Berkshire Hathaway Class. My gain is 156%. Today my $100k has a market value of $256k. BRK B paid no dividends over this period. As BRK B is a foreign share I must pay FIF tax each year from 1 April 13 onwards. For simplicity assume the 5% FDR is used. For the BRK B investment I am paying approx. $2000 actual income tax on deemed income of approx. $6000 on 1 April 13. By 1 April 19 I am paying approx. $4000 income tax on deemed income of approx. $12000 per year. So, over the 7 income years I am paying $20,000 income tax on a completely unrealised basis. Spread this over 30 years until I retire the taxes are insane. All the while I have never received any money or REALISED GAIN.

Take on step further and assume I put it the 100k in a property and left it vacant since Nov 12 and over that time its gone up 156% I walk away with my gain tax free. So the distortion is massive between a house even kept vacant and buying shares in a one US company. The longer you hold the shares in the US company the greater it becomes.

FIF/FDR is not so bad when prices increase strongly like they have over the last few years.

It's terrible in a bear market though.

You say its not so bad but its unrealized i.e. you may never receive it and you cant claim it back if your investment makes a loss ultimately. The tax is greater than the actual dividends received. It robs you of the benefit of compounding. Happy to pay tax when realized but on an unrealized basis is BS.

All valid points. Effectively FIF/FDR disincentives investing in dividend paying value stocks and encourages investment into high beta stocks like tech, biotech, etc.

Of course no tax would be better still. But if the options are (i) 33% on realised capital gains or (ii) 33% on unrealised 5% deemed dividends (= 1.65% of portfolio value) then I would take option (ii)

If you hold the shares for 20 years say in the Vanguard S&P 500 index (which you can do for say kiwisaver) you would never take option (ii) . The loss of the benefit of compounding with the 1.65% tax each year under option (ii) makes you significantly worse off. Further you have fund the 1.65% somehow each year. As it grows you would have sell down the investment to pay the 1.65%.

Yes you would need to fund the 1.65% by selling or investing more cash. But now you have the opportunity to strategically sell at the beginning of corrections and buy back in during recoveries, rather than holding for 20 years. Assuming you're not in the business of trading. (I'm not a tax professional and this is not financial advice.)

Timing of selling and repurchasing can only be described as a fools game if you study the likelihood of being successful. That's the main reason the worlds best like Buffett, Munger, Druckenmiller, Russo and Icahn etc do not attempt to do so if you study them (i do this full time).

Yes that's the theory, but personally I think that only applies for large portfolios where there's a risk of moving the market.

Just think of it as portfolio rebalancing then. All you need is for your actions to get you a return slightly higher than a buy and hold strategy.

Have a read of Ground Rules a book. You can also listen to audio book on you tube. Might change your perspective.

I agree that FIF/FDR is not good for Kiwisaver/locked-in investments.

Forget 'returns' - forget 'growth'. We need to write a tax policy starting with these assumptions.

A significant chunk of the wealthy use Charitable Trusts to minimise tax also.

With these charitable trust donations to political parties, the biggest rort continues.

Interesting, could you kindly give an example please. Genuine question.

The tax issue no reporter wants to ask Robertson is kiwisaver. The Government is robbing kiwisavers with its FIF tax regime to the extent they are in international equities.

On 1 April 2020 they happily tax everyone on 5% of their kiwisaver balances even though the vast majority had gone down substantially. Further as they recover during 2020 they will tax them on 1 April 2021 on another 5%. So yes, we get taxed when kiwisaver makes losses and then get taxed again when the recover to pre-existing levels. So this Government is not doing any favours to kiwisavers. It’s a tax cash cow for the Government that nobody wants to talk about. The same applies to anyone invested in equities outside NZ and Australia. All the while gains in houses supported by Orr and Roberston remain tax free. Grow some kahunas Labour and bring in a CGT and tax kiwisaver and international equities on a realised basis.

IRD just needs to hire the former architects of these structured finance transactions and transfer pricing structures to understand them and attack them. This would raise more than this proposed 39% tax rate. The ATO in Australia has successfully done this now for a number of years with some big wins against multinationals. Some adjustments the ATO have achieved are AUD$600m. Instead our IRD focuses of dumbing down its skilled workers and transforming the business with very few skilled workers left.

Policy announcement 1: Accommodation Supplement is scrapped. 4 billion more in to pay down debt. Rents will fall as tenants wont have the money. Policy announcement 2: All REALLISED gains on houses, farms and shares are subject to CGT. Rollover relief if sale is going into another property. CPI indexing so not taxing inflation.

I'd be the first to support the removal of the accommodation supplement, except it would collapse the housing market.

No government is going to promote policies that collapse the housing market.

It would seem the only way forward is to wean our way off the drug (over a number of years), which is the accommodation supplement. As everyone recognises housing is overpriced, it would seem appropriate the government step up to fix the situation. Measures could include:

1. Large scale government (residential) building on their existing land holdings.

2. Become part of the materials supply chain.

3. Become part of the land supply chain, with covenants restricting residential builds to not more than 100 square metres; excluding outbuildings.

4. Provide some competition in banking; by capitalising Kiwibank to create economies of scale and giving them the government contract.

5. Regulate rentals during seasonal peak demand periods.

How can the government still bank with Westpac, when their head office has just had to pay $1.3 billion in fines. The only reason Simon Power is there is the loans he encouraged Solid Energy to take on; not to mention the renewal he signed.

Unfortunately the Government is not capable of doing most things in your list whether Labour or National and would just add regulation and when it failed talk about a RESET! Tried to build 10000 houses a year and LETS DO THIS ra ra and they built 336 and most of those were already being built anyway. J Adern then says we will have a RESET (code name for bury this failed policy) and then slowly never talk about it again.

I am not sure it will collapse it but rents will go down a lot possibly 20%.

In addition Councils refuse to free up land to allow building of new residential areas and put ridiculous minimum plot size designation on lots of areas to stop new developments and have urban design zealots telling you what to do based on their green ideals.

So the combination of the tax distortion and Council's actions has a lot to do with it I think.

Good things take time.

The market will reset given time, followed by a cleanout of useless politicians; hopefully to be replaced by an improved democracy.

Let us pray!

As or before it collapsed the housing market would it collapse a government?

Scenario likelihood - initially the rents would stay the same. The people unable to afford the rents would scrape, beg, and borrow - houses are in short supply - on mass, before they are homeless, they would vote for someone who says they will reinstate the subsidy. It will swing a government.

I think we are caught in a loop and the only way out is a catalyst or crisis that enables a step change. That is some sort of phased change maybe.

To create change we need to solve the GREAT NEW ZEALAND RIP OFF and make houses cheaper and in greater supply......houses prices also controlled by limiting land development and preventing imported building materials being used easily. Building materials are controlled by a few companies. Said companies have lobbied to have in legislation NZ durability testing via Branz or other for every product. Allowing sale of building materials for double Australia and even triple USA price making building extremely expensive for relatively poor quality. They also pay your friendly builder a kick back for you buying over priced materials in the form of rebates in cash or kind. If competitors manage to get in said companies use politically lobbying to get dumping tariffs put on imported products shutting them down. If NZ scrapped durability testing and accepted say testing that met standard in California then materials would plummet. The said companies would say the materials would not be of the same quality but the truth is the local products are cheap and nasty at exorbitant prices.

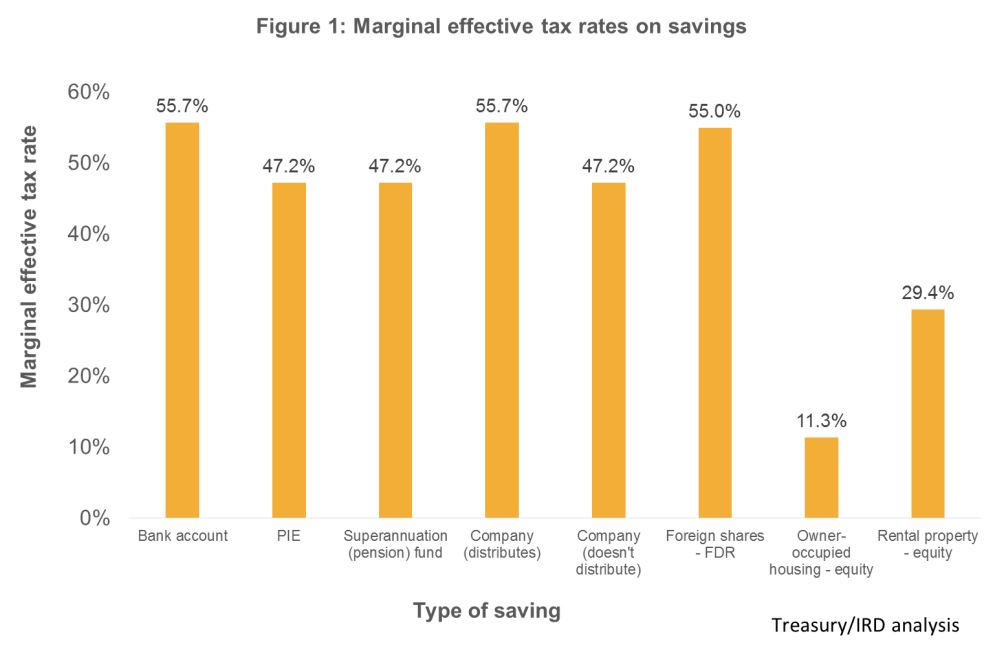

Geoff, that graph is nonsense. https://pimms.nzpif.org.nz/UserFiles/files/NZPIF%20-%20TWG%20Paper%20Re…

Is the tax shown for owner-occupied housing council rates? This is a tax disadvantage incurred by land that other assets don't incur. Owner occupied housing earns no income, it shouldn't even be on the graph.

Interesting how rates are a fee for services or a tax depending on the argument being espoused.

Also I wonder why they ignored both leverage and the whole FIF regime, I guess if you pay enough you get the answer you want.

Biggest problem with Councils is they have gone way beyond the core services they should be providing but are failing do like water, sewerage and rubbish collection etc. They have become another arm of the central Government. Instead of core services they are using rates to fund music festivals and all sorts of BS while growing bigger fiefdoms putting in place red tape to do anything. Further hiring offshore to bring so called "experts" to fill high paying CEO roles with people who know nothing about NZ. Total BS.

All true, but I would still like to see a "growth levy" line item in my rates to cover both replacement of existing infrastructure and expansion for future growth. I don't see why the $100's of millions that are being spent to replace the clapped out infrastructure in my inner city Auckland suburb are spread across all ratepayers but someone buying a newbuild on the city fringes is expected to pick up the tab. It's a bit rich when existing property owners rail against the cost of growth when their own infrastructure was almost certainly provided by central/local government.

Instead of a growth levy as you put it just fund it out of existing rates and stop pissing away current rates collected on non core services and pet projects of civil servants who are out of control.

Not to mention spending their depreciation on 3 waters infrastructure instead of saving it to replace it, then crawling to government asking for help with 3 waters

Thanks DD, that's exactly (actually, far in excess!) of what I've been looking for to explain that graph ever since I first saw it in the TWG report. It never passed the 'sniff test' for me and I had no idea how they came up with such high rates. The report you linked to is a far more reasonable interpretation of the situation, particularly that it identifies that housing is not so much tax advantaged but inflation advantaged.

Owner occupied housing earns no income, it shouldn't even be on the graph.

Yes it does! Imputed rental!

In the same way that a rental property provides 'accommodation services' which a tenant pays rent for (and then gets taxed), your family home provides 'accommodation services' (which then don't get taxed). The value of this is of course determined by the yield on similar properties to your family home. Simple really.

Btw this further tax incentive for owner-occupier over rental housing goes a bit of the way towards explaining why there are 190,000 empty houses (alot are baches, and thus owner occupier and tax exempt) and also why you hear stories like 'we're building the wrong type of houses' when expensive owner-occupier houses get supplied to a market that has a shortage at the bottom.

Imaginary income isn't income. A unicorn isn't a horse.

Oh, so you get zero benefit from using your family home? You're making a mistake here because you're assuming that a formal transaction has to take place for something to have value.

You use your house for accommodation.

You could just as easily rent that house out for someone else's accommodation.

Regardless of whether a transaction occurs, a service - accommodation - exists and has been utilised.

How is this so hard to understand?

I also get benefit from my bicycle, should I pay tax on imputed income for that too? How about the imputed income I get from blowing my own nose instead of paying someone to do it for me?

Unlike the tenant, I had to pay a million bucks for the house, so I get the benefit of not having to pay rent. The tenant has the benefit of not having to pay a million bucks for the house they live in. Should I be compensated because I incurred that cost that they didn't?

Also, the income I used to purchase the house was taxed.

Also, the income I used to purchase the house was taxed.

Was it? Because many people use untaxed capital gains from houses to buy other houses, or to trade up to their next house.

It was if it came out of his salary/wages

And so is the money I spend. That gets taxed with GST. It's the nature of money and taxation. When money circulates, it gets taxed at points throughout its circulation. The double tax whinge is a non-issue. Tax is the price of civilisation.

I think our current civilisation is over-priced

How about "imputed labour" to be introduced on people who work less than 40 hours a week? it will make the concept of "imputed" fair. After all you can be spending your ideal time making more money to pay to government.

Also, how you calculate "imputed rent"? if you assume 100% of money is borrowed to buy the house, then the so called "imputed" rent difference will be miniscule and can even be negative in some circumstances. It is the home owner savings (principals repaid and saved deposit) that reduces this. A renter has the exact same ability to invest the principle repayment he does not need to pay in something to earn capital gains.

That's an incorrect interpretation of the idea believer.

Imputed labour in this case would refer to a case where you work to provide something for yourself where no taxation occurs. I.e growing your own vegetables, brewing your own beer, squeezing your own juice etc... you've received a benefit which you've provided for yourself without any transaction occuring. Not to say that we should discourage people doing the above btw.

Imputed rent = rent you'd receive from the market if the house was rented out. It's that simple.

You have an asset, a house, were you can either use to live in, or earn income (rent it out). So sure, if you use it, you can be assumed to earn that equivalent in income even when you live in there. That applies to your home coffee machine, your personal car, your bike, etc. that is your imputed capital income.

Now, you have your time, another asset, you can put it in the market to earn income at your hourly market rate (minimum being the minimum wage) or you can spend it as you like. So if you go out fishing, read a book, play with your kids or hang out with your mates instead, you can be assumed to have earned of the equivalent market labour hourly rate*hours not worked. That is your imputed labour income. Imputed labour= labor income you'd receive from the market if your time was rented out to the market, it is that simple.

Also, you did not address my second point, how will you calculated rental income (that has to be net of all the costs). If you want to assume market income for any house, then you have to also assume market expenses for the same asset. The cost of owning a house is the cost of financing it, regardless of how individuals actually do that. The cost of ownership must assume a 100% and interest only mortgage which will accrue interest at your personal mortgage rate (and with zero equity, you will get a considerably higher interest rate) plus all other ownership costs (insurance, rates, maintenance and repair, etc). That should be taken into account as well, so the money you pay to live in your house, is the same money you would have paid if you rented it (more or less). So, your net imputed income is zero

Let's charge all vehicle owners the imputed rent that they're not paying taxi fares.

Unsure what point you're trying to make here NZdan, both of those groups already pay for their use of the roads. The point of imputed rental is that you don't pay tax on it but you do when you sell it to someone else

The point is he could be hiring his car out, so according to your/TOPs imputed rent logic, he should be taxed for the imaginary income his car is generating.

"Unlike the Greens’ proposal, TOP are not reliant on this tax change to raise revenue to pay for our spending promises"

So TOP don't understand the purpose of taxation either. IT DOESN'T FINANCE THE GOVERNMENT!

Study MMT, TOP.

Geoff advocates the MMT approach of RBNZ funding Treasury directly and writing off the debt, instead of using the banks as an intermediary through open market operations.

Currently Government (Treasury/coalition partners, as opposed to RBNZ) is funded through debt and tax.

Wrong, taxation and borrowing do not fund the government. What would be the source of money under your model? Taxpayers cannot create money as counterfeiting is illegal and the government cannot borrow back money before it has first created it through its spending.

I assure you, tax and borrowing fund the coalition's spending. This is simply a fact. I don't know who told you that RBNZ gifts money to the coalition to fund its spending. There is a very clear separation between RBNZ and the coalition/Treasury.

I am funded by my salary, investments and borrowing. The fact that the RBNZ "printed" that money does not mean that I am funded by RBNZ. Treasury/coalition is funded by tax and borrowing. The fact that the RBNZ "printed" that money does not mean that it is funded by RBNZ

The RBNZ is an arm of the government, it is not a separate entity, that is a ridiculous claim. An article here in Stuff today. https://www.stuff.co.nz/business/opinion-analysis/300116549/heres-a-fre…

RBNZ is independent. I can't explain it any simpler - Treasury is funded by tax and borrowing, not gifted money by RBNZ. A simple Google search can prove it. If Treasury didn't borrow or tax they would have no money to spend. By your logic everyone is funded by RBNZ because they print the money, but this isn't how it works in reality. Why don't you understand this? Listen to this interview between Geoff and his BFF Jenee -

https://www.interest.co.nz/news/106666/top-leader-geoff-simmons-why-rbn…

This taken from the RBNZs own website. The Reserve Bank of New Zealand is New Zealand's central bank. It was established in 1934, and although not a government department, has been wholly owned by the government of New Zealand since 1936. https://www.rbnz.govt.nz/about-us/what-is-the-reserve-bank

Politicians have made a commitment not to interfere in the banks daily operations that is all but that doesn't make it independent of government.

Reserve Bank of New Zealand Act 1989 affords RBNZ statutory independence, even though it is owned by government. But this aside, it does not gift money to Treasury. Treasury is funded through debt and tax - this is an undeniable fact.

https://www.interest.co.nz/news/98147/robertson-defends-independence-rb…

They also say this, "The Reserve Bank has the sole right to produce currency in New Zealand". As the bank is owned by the government, how can it be gifting money to itself?

You still have not explained where else you think that money (currency) comes from. Some study of sectoral balances would be helpful. Only the government can create net financial assets to finance our savings, we cannot save up bank debt. https://gimms.org.uk/fact-sheets/sectoral-balances/ also https://www.economicsjunkie.com/sectoral-balances-and-private-saving/

NZ currency is created by RBNZ.

RBNZ is not the same thing as Treasury.

Treasury/parliament/the coalition partners are NOT gifted money by RBNZ. RBNZ is a seperate independent entity. The money that Jacinda spends comes from tax and debt (bonds).

If I want new money I borrow it or work for it. I don’t get gifted it by RBNZ. You can acknowledge this. So why can’t you acknowledge that if Jacinda wants new money she needs to tax it or borrow it by selling bonds? RBNZ WILL NOT GIFT IT TO HER NO MATTER HOW MUCH SHE ASKS. She would need to sell bonds (take on debt).

Here you are younger generations, the only party who has a serious housing policy drawn up. Don't be persuaded by others who say it is a wasted vote - there is no such thing in a democratic country.

In facts the real wasted vote is to continue to vote for dumb shit that stopped working a long time ago.

TOP is a guaranteed wasted vote. Despite TOP’s attempts to differentiate themselves, they are really very similar to the Greens on economic and social matters, but the Greens aren’t necessarily a wasted vote as they stand a reasonable chance of getting 5%.

A very high proportion of TOP votes are poached from the Greens. The more votes TOP gets, the less likely the Greens are to get above the 5% threshold. This would be a good outcome, so I suppose TOP votes aren’t a waste in this respect.

Frankly the Greens don't deserve to get into Parliament because of this ludicrous wealth tax, which Labour has had the good sense to rule out.

i.e. don't vote for the Greens based on their wealth tax. t too would be a wasted vote whether they get in or not.

I'd like to see Geoff join ACT as finance spokesperson.

I think Geoff likes using the power of the state to provide better outcomes a little bit too much to join the Act party.

ACT and TOP are polar opposites on virtually all issues. ACT is a free market libertarian party. TOP's economic policy is highly interventionist and their other policies are heavily influenced by race and other social justice considerations.

The only wasted vote is voting for the two major parties and expecting improved economic and social outcomes from previous.

Any evidence to actually support this statement? I was considering voting Labour until I realised like national they weren't at all interested in addressing the major inequlities of our country.

Note that this tax is levied on the equity in an asset. In other words, the value of the asset minus the debt held against it.

would this not just encourage debt creation to the max, i.e borrowing funds from offshore most likely from a tax haven trust?

Seems a huge incentive to leverage up the family home and switch to interest only.

Why would people take out debt to avoid paying tax? It makes no sense.

1. Banks have to lend to you in the first place, if they don't think you can handle the debt, then your 'clever plan' is doomed at the outset.

2. You have to pay interest on your debt. The tax is set at a lower rate than the interest payments would be. It doesn't make sense to voluntarily pay $20,000 per year in interest costs so that you can avoid paying $15,000 in tax costs.

Keep the family home leveraged to avoid TOP's tax. That is a clear incentive. Take the money that would otherwise go into the mortgage and invest in some other interest/dividend bearing asset class that cancels out the interest that the bank is charging you on the mortgage.

Wait, so you owe $30k per annum on the mortgage. Your plan is to invest that $30K in some other asset that pays $3k in dividends before tax, and then used that taxed dividend stream to make the $30k payments on your mortgage each year?

Think you need to hit the calculator again.

The $30k in your example comprises interest as well as principal. You put the mortgage on interest only because the more you pay the mortgage down, the higher your tax bill is. Of that $30k, you continue to pay the interest component to the bank as you are legally obligated to. You put the remaining principal component of that $30k into an interest/dividend investment (e.g. mutual fund). The dividend earned from the mutual fund cancels out the additional interest that you are paying the bank by not paying down the principal.

It has always been the case mathematically that you are better off paying off a minimal amount of your mortgage, and investing the difference in shares. Historically the share market on average returns more than mortgage interest charges. I.e you should be better off investing a 7% share return via and index then paying off a 3% mortgage. Most people don't do this because of the inherent risk and inability to deal with market volatility. Now if you add in a equity tax on housing, it only strengthens the case to undertake an interest only strategy and investing the difference in shares.

Which is actually what this policy is trying to encourage - investment in productive enterprises (via the share market, or any other means), not houses.

WHat if those productive investment are in foreign companies? what is in it for NZ? you pay mortgage to Ausi banks and then pay it to a US company.

This is a silly way of looking at an obvious problem. NZ economy has very little to offer in form of viable economic investment. NZ is excellent in what it has traditionally been a world level player: primary products. That is so heavily invested in NZ, at least under the existing used business models.

As for other areas, the inputs of any business are very expensive in NZ, some being so because of NZ geographic location, some because NZ is socially and environmentally more responsible than many other countries, some because the very small size of the market and its vulnerability to lack of competition in supply (e.g. unlucrative local market unless you can create a monopoly). These means that comping up with a viable business case for doing anything in NZ (the first step before you go out and look for how to fund it) is very hard. As someone who has seen some business cases in NZ, all of them assumed a significant portion of their activities being done in Asia or Africa, and even then they were barely break even under very optimistic assumptions (i.e. we go and get the US market or the Ausi market or the Chinese market). Where there has been even a sliver of hope, money has flowed (e.g. Xero). No sign of "capital shortage" there.

Investment in productive enterprises will not be led by micro investors (such as people who put their money in housing) but by major credit providers (banks) and investment entities (fund managers the largest being the NZSF). Their leadership will bring the rest. Why they are not investing in NZ? nothing is being proposed that makes financial sense.

Serious question here - Geoff states that “TOP’s proposal is that all significant assets (in practice it would be mainly property) should pay as much tax as a bank deposit.“

Does this mean that they are still proposing to tax all major assets, like farm equipment, business assets etc? I was lead to believe that they abandoned this policy earlier this year? Geoff, what is going on????

I would have thought the part in parenthesis was pretty clear already?

Can you direct me to any policy document that clarifies this on their website or elsewhere?

This was definitely their policy last year (essentially a wealth tax very similar to the Greens despite their best efforts to claim it is hugely different). But earlier this year all of their communications changed to give the impression that had abandoned this and were only pursuing a real estate tax.

Third page: https://d3n8a8pro7vhmx.cloudfront.net/garethmorgan/pages/2959/attachmen…

They exclude some forms of land but otherwise it's stated as a property tax.

So you're right, saying "in practice it would mainly be property" is opening the door on a topic that their other publishings indicate is closed.

Edit: kind of embarrassing that link includes "garethmorgan" in it?

Very embarrassing about Gazza. Well spotted.

Certainly cant see anything in there about them wanting to tax other assets, so it is extremely interesting that Geoff is indicating they do actually propose to tax other assets in this article. TOP are a shambles.

Still waiting to hear how you're going to fund your UBI without using the revenue from this property tax, as the conclusion to this article doesn't allude to using this tax to fund a UBI at all.

Stop being lazy and do your research.... it's all tabulated on their website..

Hey Albert, can you show me where on their website they fund the UBI without using the revenue from this property tax? Since apparently I'm being lazy, even though I've already looked on their website and can't find any such thing? In fact their policy document Appendix Two shows they are using $8B in new revenue to fund the UBI? https://d3n8a8pro7vhmx.cloudfront.net/garethmorgan/pages/2692/attachmen…

And when I asked them on Facebook they said they didn't have a policy paper on it yet but were basing that on what Andrew Yang has proposed in the USA, in other words they haven't actually done any work on how that would work in a New Zealand setting.

Perhaps you shouldn't call people lazy when you don't know what research they've already done prior to asking the question.

They are funding the UBI by using the revenue generated by the property tax and combining that with all the additional savings (listed in the table you found and includes such things as scrapping paid parental leave, student allowances etc) made to provide a net postive ($421 million) fiscal position. Their goal is to make the policy tax neutral (give or take) so as to spread the tax revenue more evenly. Whether they can acheive that is another matter up for debate but that is how they propose to fund the UBI.

Right, so you've told me what I already know, and didn't answer my original question, because the end of the article above suggests they wouldn't use this money for UBI, but for cutting kiwisaver taxes.

On their face book page members from TOP have also said they don't need the property tax to fund the UBI, they can do the UBI independently. Which is what I am asking for more information about.

They've left out that link because this article is not a full overview of their policy, simply a focus on why the Greens are silly and need to listen to economists more often if they want to write good policy.

But the very end of the article says this:

Unlike the Greens’ proposal, TOP are not reliant on this tax change to raise revenue to pay for our spending promises. TOP want this to be tax neutral, so the revenue could be used to reduce the tax on other investments, in particular Kiwisaver.

It's not true. One of their spending promises is a UBI, and their UBI policy shows they're using $8B raised by this tax to pay for it.

Since 100% of the tax is being used to pay for their spending promise of the UBI, there would be $0 left over "to reduce the tax on other investments, in particular Kiwisaver".

They can't have it both ways, either this revenue is earmarked for the UBI, or it's not. The article suggests it isn't, and so I'm wanting more detail on how they can afford a UBI without using the revenue from this tax.

In fact their UBI policy says they're going to reduce government contributions to Kiwisaver to the tune of $900M per year. For those earning the least and putting the least into their Kiwisaver account, any reduction in kiwisaver taxes are likely to be dwarfed by the removal of government contributions.

Seriously, Land tax is a far better, simpler, graceful, effective solution to repairing our tax system.

If you are going to post rubbish at least attempt to back it up with some sort of rational argument.

Reason 1/1000 that this is rubbish - Land tax introduces a fundamental disconnect between requirement to pay and ability to pay.

If there is a rationalisation is it still rubbish?

If you're a landholder, and you're holding land that you can't afford to pay the tax on, you either increase your productive utilisation of that land or sell it to someone who can/will. Under utilisation of land and exhorbitant land costs/rents make so many business opportunities unviable, and is a significant factor in our uncompetitive productivity. It's a large part of why everything is so expensive in NZ.

https://commons.wikimedia.org/wiki/File:Everybody_works_but_the_vacant_…

.jpg){kind=link}

The government has no business meddling in how landowners are incentivised to use their own land. If they would like a lawn instead of an additional unit, that is their prerogative as the asset owner and absolutely nothing to do with anyone else. The profit motive is sufficient incentive for landowners to develop. Believe it or not, quadrupling council rates would not result in more productive use of land. Nor does land magically get used more productively when interest rates go up.

We (citizens, represented by our government) most certainly do have an interest in how our most important natural resource is utilised. There has been a massive issue with warped incentives, in recent history it's been very profitable to simply hoard as much land as possible. This has been due to the perverse incentives created by our tax system. Loopholing and eventually abolishing land tax in 1990 was the biggest economic crime this country has been victim to.

You're right... Quadrupling rates, would only work if the rating valuation system was changed to be levied against land values only. We've covered this ground recently.

https://www.interest.co.nz/property/105862/auckland-councils-economists…

It is not "our" resource, it is the owner's.

Well they don't need to get access to "our" public services either, then. They can build their own alternative health care, education and police systems if they don't want to contribute funding to our one in the manner that we think fit.

The whole point of a government is to trample on the rights of individuals, to as minor a degree as possible, to produce the best possible outcome for society at large, and provide goods and services that the individuals working by themselves couldn't provide. That takes money which means taxes which means you gotta pay somehow.

Paying a land tax seems fairer, easier to implement and harder to game than most alternatives, even if isn't "perfect" in all respects. Don't let the perfect be the enemy of the good.

Your logic leaves much to be desired. Let me charge you annual tax on your bicycle and if you object you don't need to get access to "our" public services either, then.

His bicycle isn't a natural resource. Neither is it fixed in supply. Neither is it a fundamental of economics. Neither is it a component of shelter, a basic human right. With great privilege comes great responsibility. It is a privilege to hold exclusive title to land, and with that should come an appropriate amount of responsibility.

The metal it is made out of is a natural resource. A resource that is fixed in supply in the same way that land is as there is only so much of it on earth.

Productive land (i.e. improved land) is not fixed in supply. Just like improved metal (e.g metal that has been turned into a bicycle) is not fixed in supply. Please don’t parrot Georgist talking points at me, I’ve heard and discredited all of them too many times before.

You can’t just declare things a human right willy nilly.

Land value tax does little but create a nation of tenants, serfs to the landlord government. We won’t stand for it here.

It's a natural resource when it's in the ground. When it's in bicycle form it's no longer a natural resource. And chances are it came from Australia's natural resources, which had the burden of royalties associated with it.

LVT reduces rents, land prices, and shifts burden from those who work and trade for a living onto the unearned land rents. It takes the banks foot off our throats. Here's a little ELI5 for you. https://np.reddit.com/r/newzealand/comments/6b6qy5/landlords_threaten_r…

If you could link me to some of your works where you disprove Georgism that would be appreciated. It sounds like I've got a lot to learn from you, since your economic knowledge is superior to that of a man whose work "Progress and Poverty" was second in popularity to only the bible at one stage, and considering it was an economics text, that's an amazing feat. Albert Einstein on George "Men like Henry George are rare unfortunately. One cannot imagine a more beautiful combination of intellectual keenness, artistic form and fervent love of justice."

If you prefer right wing economists. Here's Milton Friedman on the topic. https://www.youtube.com/watch?v=yS7Jb58hcsc

Please introduce me to any respected economist who disagrees with Henry George.

Here's some info about the relationship between housing and human rights in New Zealand: https://www.hrc.co.nz/files/4215/1363/5639/2017_07_25_-_Right_to_housin…

I prefer Milton’s son, David.

If all you can do is parrot me talking points from a fringe movement of the past, we’re done here.

I can parrot you talking points from the communist manifesto, wouldn’t that be productive?

Ahh, Friedman gave that talk at the height of his career. It wasn't simply dribblings during teen angst. You do know who Milton Friedman is don't you?

Do you know who Milton’s son, David, is? The intellect of the son far surpasses that of the father.

Yeah, he's an anarchocapitalist. Hahahahahahahahahaha... Hahahahahahhahaha.

I hear Somalia is rather balmy this time of year. Good luck, you'll be needing this. /̵͇̿̿/'̿'̿ ̿ ̿̿ ̿̿ ̿̿.

I just think it’s funny that you thought I might not know who Milton Friedman is. You’re clearly very proud of your high school economics knowledge.

Are you telling me I've found an anarcho-capitalist in the wild?! Wow. I mean, I believed anarcho-capitalism could work when I was a teenager, heck my first ever vote was for Act. But in the 2 decades since, my understanding progressed a little.

I shouldn't laugh, you really don't know... OK, start here. Look at all countries with regard to government spending as a percentage of GDP. Look at all successful economies and notice where they sit in the spectrum. https://en.wikipedia.org/wiki/List_of_countries_by_government_spending_…

Ask yourself why there are none that are even close to zero.

I’m not an ancap. I, along with the vast majority of kiwis, simply dismiss LVT as totally illogical and unacceptable.

Well why are you holding David Friedman up as your shining light in economics? https://en.wikipedia.org/wiki/David_D._Friedman

You did say that the intellect of the son far outshone that of the father... Now you're telling me you don't even agree with him.

Mate, you're a broken record. At this point I know your stance is purely emotional.

I agree with some ideas of many different economists. Friedman is one of them.

There's really not much more to David Friedman's economics than anarcho-capitalism and you don't agree with that. Milton has much more depth. And he was a Georgist.

At this point you're only fooling yourself.

You first learned of D Friedman 5 minutes ago sunshine, don’t pretend that you know his work.

I take it that you think that the natural resources of a nation belong only to the wealthy and privileged then? Why do you think there's rates associated with it?

I'd recommend a perusal of Thomas Paine's "Agrarian Justice". http://www.piketty.pse.ens.fr/files/Paine1795.pdf

DD, that is patently ludicrous. The government is constantly "meddling" with property rights, usually in favor of existing landowners and to the detriment of renters, first home buyers, productivity etc etc. What do you think zoning regulations are? How about the RMA? Rates? Need I go on?

Yes, we need to reform the RMA. Zoning and the RMA are the same issue. The RMA requires district plans to be prepared, and district plans specify zoning and accompanying development rules.

Rates should be reduced to only a flat fee for core council services.

Who says the leopard can't change its shorts?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.