From the Reserve Bank (RBNZ) Dashboard data we can take a look at the overall balance of bank loan books.

Banks are essentially loan books. We can't look in them to see individual loans, but we can look broadly at what sectors banks lend to.

We have a lot riding on our banks being well structured, and financially stable.

The RBNZ regulates and reviews bank and financial system stability. They last did that on Wednesday, November 25. Their conclusion was that "the banking system has maintained strong buffers of capital and liquidity, and the insurance sector remains well capitalised."

But that Dashboard data allows us to inspect the balance of each bank's loan book.

It is not something the RBNZ does in its review. In fact, it has explicitly said they have no power to tell banks who to lend to or what sectors to target.

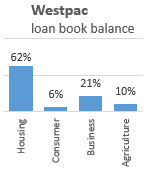

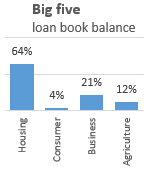

But we can see, for example, that 61.9% of all overall bank lending is for housing. That proportion is growing. A year ago it was 59.2%; two years ago it was 58.6%.

So that raises the question about whether this is a healthy concentration, whether it is heathy that it is getting more concentrated, and Dashboard data allows us to inspect which institutions have the greater or lesser concentation.

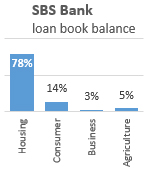

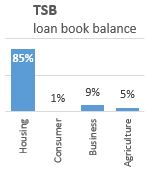

The big five

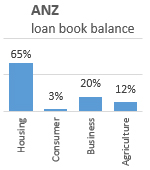

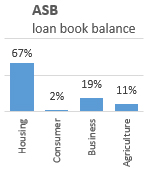

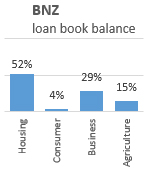

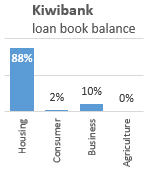

The overall New Zealand banking system is dominated by five large retail banks, and perhaps Kiwibank is little weight in this group. So four big banks dominate.

It used to be observed that we really only had one real trading bank, BNZ. The rest are in fact really just mortgage banks. But BNZ has now joined the pack with more than half its loan book in home lending.

Here is the share of lending to each broad sector in each of these banks:

As a set, it is one that dominates 95% of retail and business lending, the overall consolidation is like this:

Only BNZ has anything approaching a balance in the spread of lending across sectors.

And in the current economy, that is hurting it. The New Zealand economy is more of just a housing market than ever, and being light on housing exposure isn't a competitive advantage.

In a real economy, we should be encouraging banks to diversify their risks across sectors, but we are doing the opposite.

The RBNZ allows special advantages for lending for houses. It allows very low capital risk-weights for housing compared with other lending, and it is about to deliver very low cost funding, almost all of which will be directed to housing.

And the Government has started its own lending program for SMEs, businesses that make up more than 90% of New Zealand's commercial economy - and the attraction of that IRD-administered loan service is that it comes with zero interest cost, is unsecured, and the obligation to pay back the loan in part or full will be negotiable based on how well your SME business performs. If it struggles, there will be debt and payment relief on a basis no banker would ever contemplate. Banks need their loans repaid and they apply proper credit assessments about that, something the IRD/Government isn't doing. So why borrow from a bank?

And the overall bond market that has an excess of funds looking for opportunity at very low yields, is an attractive option for large corporates who are taking full advantage now. So business lending by banks is up against severe headwinds as well.

All these practical market signals leave banks little option than to target lending to housing.

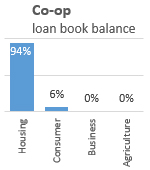

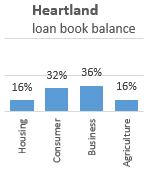

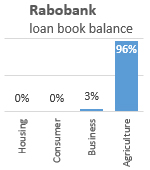

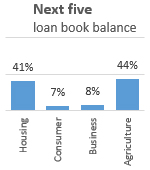

The next five

These banks generally are fighting for the scraps the big five miss. Specialist rural lender Rabobank is probably the exception. But these lenders, mainly locally owned, are in a tough spot, without the scale to effectively compete and no practical way to raise significant capital.

But some of them have built a commendable balance in their loan books, especially Heartland Bank which is a standout on this basis. But others are just as exposed to housing as the majors or even more so.

Rabobank and Heartland Bank give this disparate group some sort of rough balance.

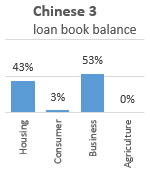

And then there are the three Chinese banks, Bank of China, China Construction Bank, and ICBC.

Together (and they don't really work together), they have a different sort of loan book balance than any other bank set.

That our banks are choosing or prevented from lending to our productive economy should be of concern. "All" eggs in the housing basket isn't likely to help the New Zealand economy grow and develop.

Sadly, everyone knows this - the borrowers, the banks, the regulators, and even the Government.

But still, those who can are setting the incentives to target housing ever more closely.

Yes, we need more housing, and especially housing for first home buyers, people with average incomes, and more social housing.

But we also need more productive economy investment, investment in improved productivity, and more employment driven by tax-paying businesses. We will never get it when banks are effectively disincentivised from lending to these sectors.

216 Comments

Great to see we are now talking about the big 5, instead of the big 4.

I love David Chaston and his shocking report yesterday. It showed KiwiBank has 87.7% percent of its Loan Book in mortgages. Though KiwiBank's market share was low. The inverse was true of ANZ.

Hmmm, which segment of banks comes out the strongest during a housing crunch...

Banks with all their eggs in one basket, kiwis with all their eggs in the banks basket. Nothing could go wrong here though... listen to Orr, banks have great capital and liquidity... just ignore that he had to bail the banks out with $128billion QE & FLP to keep them going.

According, to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

Great article! The question about New Zealands economy having come to approximate a housing market, in the long term our fate will depend on how we deflate this bubble. We continue to accrue risk and it's completely obvious that will end badly if we don't take immediate, sustained action on housing affordability (which is driving household debt up rapidly from an already high base.) However it also appears the government are for some reason waiting for that crash, which either shows that they have a brilliant plan to deal with a deep and prolonged recession as the economy restructures afterwards (as happened in Ireland after the Celtic Tiger, New Zealand is now approaching similar levels of household debt) or they simply don't understand the level risk being accrued? I don't actually know which though but it might be a good question for Robertson and Ardern.

https://www.zerohedge.com/markets/how-much-space-300000-buys-cities-aro…

That is 300k American....but shows how we have been rooked in the Fair Isles of NZ.

Governments think in 3 year time slots. If it crashes they know it will be someone else’s problem so why even bother thinking about it?

There will be no plan for a crash. The expectation now because of what has happened this year is that we flood the market with even more money and anyone who can’t pay their mortgage just gets another ‘holiday’ until they can.

The incentives are for greed, incompetence, no care and laziness. Who even cares about productivity now?

Who even cares about productivity now?

China.

True - why China (probably now) is and will be the global power this century.

And NZ Chinese investors. Note in the charts above how most (50%+) of the loans made by the Chinese banks here are to businesses and (interestingly) NOT to agriculture. Seems the howling of some a few years ago (Messrs Little and Peters) was misplaced about Chinese buying up large tracts of productive farmland

There has been a retreat of Chinese investment in some sectors due to the overseas investment office. I know of some (Chinese companies) that setup here with the intention of buying up large, but have found it more restrictive than they expected.

Surely there is a high probability of a couple nore labour governments yet? New Zealanders seem happy to give governments a few rolls of the dice.

If we see a property crash and there is general misery out there...who knows. If housing becomes further out of reach for many surely people will grow tired of Aderns promises (as they did the National leadership)?

99.9% sure it's the second.

Money is plentiful

Crash will come with either (1) supply overshooting demand (2) demand falling away dramatically

IMO (1) not likely, (2) could happen, with immediate effects, with large reduction to immigration - political hot potato.

(2) could also happen if credit tightens dramatically for housing speculation and/or comparative investments are more attractive (risk/return profiles show possible arbitrage)

Didn’t realise kiwibank was so exposed to housing...should I be concerned or will government bail them out?

Theoretically, no, the depositors become bondholders. In reality this is often politically unpalatable and if they've bailed out AirNZ a few times I think they'd probably do Kiwibank as well because it would be a severe financial event for NZ super fund, ACC and NZPost as they are in up to their necks.

Yes that is interesting, and concerning.

Now might be a good time to change their name to Lame man Kiwi Bank or Merry Linch Kiwi Bank.

Kiwibank has top line growth similar to other banks and they often win awards for customer service. Their issues has just been that they have spent a few years sinking money into expensive "transformation" projects but it has yet to show any meaningful advantage from or return on the capital they've sunk (it's only investing if you one day get a return.) The long and the short of it being they've spent a lot of money, now it's time to show customers and shareholders the shiny new whizz bangs that will win them market share.

What government bail out??? It's not like NZ has a Savers Guarantee like the rest of the Western world.

cj099.. same type of bail out we gave them in the 1990s when BNZ nearly went under.

The fact that Arden thinks tinkering with home deposit subsidies for FHBs will actually benefit them shows how out of depth she is.

This is a universal problem in Washington Consensus infected nations.

When the moral code that requires service to the public good decays, the legitimacy of the state collapses. Here is a quote from the paper:

"Moral failure of the leadership in this social setting brings calamity because the state's lifeblood--its citizen-produced resource-base--is threatened when there is loss of confidence in the state, which brings in its wake social division, strife, flight, and a reduced motivation to comply with tax obligations.

In the resulting weakened fiscal economy, services that citizens have come to depend on fail, including public goods and administrative control of corruption.

To realize and sustain good government is especially difficult owing in large part to the importance of shared moral obligations between citizens and the state."

In other words, a strict moral code that requires elites to devote resources and leadership for the public good is the critical foundation of the entire social, economic and political order. When this moral code decays, the state and its elites both lose legitimacy and the consent of the governed. Link

We had a similar discussion about this on a different article during the week. If/when enough people realise this system is rigged against them why bother playing by the rules any longer? It’s not in human nature to do so if governance is failing the people. The economic data shows it, inequality is rising and more people are doing it tough, yet we double down on failing monetary policies. Why would those victimised by it want to play by those rules?

History would suggest they won’t forever and will in time change the rules for a fairer society - we of course can do that peacefully if commonsense prevails at monetary and fiscal policy levels - but it would appear those people are tone deaf right now which is worrying.

When will the powers-that-be realize what are the deep financial, economic and social impacts of the current monetary and tax policies ? We live in a real cloud cuckoo land if we think that we can create wealth by selling houses to each other, rather than investing in productive assets and promoting the real economy.

The psychology of these things is that its not until the dust settles that you ask the rational questions - like why didn't we do something/anything to prevent the distortion? (vested interest in regualators/governance seems to be a common theme).

Where else in the world can you make 20% per annum TAX FREE

From whom does one take it from, other than our children and those unable to save?

There is no incentive to invest in anything productive

Everywhere ..just buy BTC

Two slight errors here on buying BTC. The first that it's tax free gains. You will most likely have to pay, unless it's tax evasion you're planning.

But that's more than offset by the fact the gains are SIGNIFICANTLY MORE than 20% per year.

If you brought:

6 months ago: +175% p.a

1 year ago: +132% p.a

2 years ago: + 202% p.a.

5 years ago: + 935% p.a.

How much of this housing lending is for business purposes though? I have a loan against our house that has funded buying shares in a business. The bank hasn't indicated to me that it considers it business lending.

Most SME owners would secure loans against residential property, the banks don't really have a tolerance for anything else.

Australia’s banks turned into giant building societies, lending almost exclusively against residential property and rarely, if ever, making unsecured loans to businesses or people any more.

If someone asks for a business or personal loan these days, the banker asks for the house.

The result is that traditional small business lending has dried up, and with it business investment, while Australia has the highest ratio of household debt to GDP (134 per cent) in the world, since business owners have to borrow against their houses.

And, by the way, the upward pressure on values from banks has probably contributed to the over-pricing of Australian real estate.Link

Diversified portfolio - The rule even the lowliest investor understands. It is not like what's coming is not obvious. The greed is out of control in NZ. The bankers and investors are like those 300 kg people you see on the TV who can't get out of bed, know they will die soon but keep on eating greasy food anyway. Orr is their clueless partner who keeps bringing them the food. Why can we not vote against this insanity?

Yip we live in a democracy except for monetary policy - which is more important than ones ability to smoke weed, yet we get to vote for policy on one but not the other (ffs)

Well we are all very addicted to low interest rates now. It’s not going to end well if the supply runs out.

I could not agree more. A perfect description of what is happening.

What comes also to mind is the scenario where an alcoholic is given more and more alcohol to deal with his problems.

The Government really needs to do something, and urgently, about this madness: RBNZ's independence or not, we can't afford to have an out-of-control RBNZ creating all the pre-requisites for a future financial and social disaster with its reckless monetary policies.

Orrsum "It is not like what's coming is not obvious."

I don't know what's coming, please tell me and tell me when it's coming? Thanks

I would not expect you to know Yvil. You have always been supported by successive governments and reserve banks and think everything will always run smoothly because it always has. You have become far to comfortable.

Then perhaps you could help educate Yvil (and others) Orrsum. There are probably quite a few looking for tips on the future we may be ignorant about

The tide is turning against the speculators and a DTI ratio followed by a worldwide recession and then rising interest rates will decimate the NZ housing market. Not that I care too much now because me and NZ are over, but I would love to see all the smug spruikers of the world be brought down a peg or two.

So forget housing, accept renting and buy BTC for the long game then? Thanks - gonna open a wallet on Monday.

Grrr grrr grrr I love your posts lots of energy and anger which is what changes things.

Haha as an investor I think I know a bit about it and the description could not be further from reality. If you want to do well start getting up early everyday for the next however many years.

Watching the property bubble explode in the USA first hand, I learned that vested interests often think they know a lot on the way up but then go very quiet on the way down.

Thanks IO...U have tried to skew the subject again. What do you think about getting up early everyday??

IO you have met your match here. Flying High believes he is a genius investor so obviously must be.

That says it all doesn't it. Its not surprising as we are on opposite sides of the 6 foot fence so that would stop you from seeing unless you make some effort ...

Its more like a moat than a fence. You, Yvil, Hook and TTP are all living happily in your mansions surrounded by the moat. You have pulled the drawbridge up and think that you are all safe and secure and you will never let us riff raff have a chance at living in your wonderful safe haven. But the masses are gathering and they are not happy. One of us have just found the plug and the moats water is draining away. The tide is turning my friends. This last 20% push has broken the camels back. You just could not resist could you.

Orrsome, I am renting at the moment, that's right I don't own the house I live in. How is that for a reality check on your crazy pre-conceived ideas?

Do you still have the motels - what did you end up doing with the million dollars of un-taxed capital gains you made on your recent sale?

That's a very personal question but I don't have much to hide. Yes I still have the Motel, I'm actually working at the motel right now whilst my managers are having a week off at the Whangamata Beach Hop.

As for the profit from the sale of my house, my bank, who used to ask me every 6 months if I needed money to invest in anything else, insisted it be used to repay various mortgages on other properties (including the Motel). They took real freight back in May because I'm heavily exposed in the accommodation business.

So now I rent my place (for 12 months) I own other properties that are all mortgage free and I feel quite stupid having sold my house and especially about being mortgage free, actually I absolutely hate it. I have sworn not listening to BW ever again

Right - so you still have significant skin in the game despite telling people you're 'just renting'. Was just clarifying on the off chance people got confused about any biases you may (or may not...) have.

We really should have a profile attached to each commentator that says how many properties they own - it would make the biases and heuristics you see in the comments here much easier to see through. It would be great if all our public servants had to do the same - so when they comment on monetary/economic policy you can see that they own 3 rentals and have a vested interest that the average 20 year old doesn't have.

If I was mortgage free on multiple properties there Yvil I'd find something much better to do with my time than troll people on here! I'd buy a boat and be out cruising the gulf and catching some snapper.....perhaps a bit more golf.

Hilarious, he hates being mortgage free on several properties and also runs a business. Most here, younger people especially, would just dream of being mortgage free on an owner occupied home.

Young people have been dreaming about being mortgage free on a home since they invented mortgages Nifty1. It's nothing new. I also think you've misread Yvil's post - he's exposed to the accommodation sector due to owning a Motel, a risky and potentially loss making sector atm.

You've read it wrong Hook, he owns several properties that are mortgage free and he hates it. He rents the house he lives in.

How is it possible to be as tone deaf as these people?

Maybe so. I'll let Yvil explain it better.

Nifty1, Hook, here you go:

I had mortgages on IO of course, where interest cost about $72'000 pa

I have now repaid said mortgages and I rent a place for about the same $72'000 pa

So is it all even? Absolutely not, the mortgages were tax deductible as they were used for the businesses so $72"000 - 33% tax deduction = $48'000 pa

What's more the interest rates have dropped and are going to drop even further, so the $48'000 is more likely to be around $36'000, about half of the rent I'm paying

If Yvil is an owner of a Motel complex then I totally commend him. Not a prospect I'd be remotely interested in, regardless of the income. IO, some people are motivated to provide for themselves in later life, or provide for their children as an inheritance or be able to help their children into ownership. Trying to make them out as some form of economic criminal is, imo,akin to shooting the messenger before you've even read the message.

You're right. I feel sorry for him. Being mortgage free on several properties is hard, I'd hate to be in that position.

Nifty1, you're probably too upset to listen but I'll still give it a go.

Our parents (mine too) told us it's a bad thing owing money, they were right for everything that devalues, cars, holidays, all consumer goods but unfortunately it's a bad lesson for asset that rise in value over time. A mortgage for real estate is one of the very best things you can have to get ahead in life. It's probably very counter-intuitive for you or "laughable" as you say but if today, you open your mind just a little that a mortgage could be a good thing, then your day will be worthwhile

I'm not upset at all, I actually find it funny how out of touch you are and think you've got it hard owning multiple mortgage free properties. You're right, the mortgage over 25 years has done you a great service and made you wealthy. You're not alone with this, many people fortunate enough have greatly benefited from this. What you and others who it has benefited don't realize is how much of this wealth accumulation was pure luck and that as a result of you all doing the same thing it's now inflated house prices so much that it's locked out a generation from house ownership. You're clearly oblvious to this and probably think it's a level playing field to that of 25 years ago.

I never said "I got it hard" I think I have a wonderful life, also I'm very aware it's not a level playing field and it's definitely not a fair world, imagine being born in Syria. Nifty you're making many wild assumptions here,

Saying you hate owning multiple mortgage free homes comes across that you've got it hard and are looking for sympathy.

Looking for sympathy? On an anonymous site? You don't know me well, I think that's silly

There is no way anyone with experience will be able to convince those who don't have experience.. especially on this crap site. The "poor hard done by" are far more vocal and numerous than those who are experienced. Look at the general theme - uni students and academics with zero experience but tonnes of opinion

'Crap site'. Wow, what an insult. No one, including you, has to be here and comment or read.

It's pretty odd if you think it's 'crap' and comment here so regularly...

Nifty1 how is the current situation any different to the post war years when the Govt of the day gave returning servicemen farms and landholdings (The Ballot Farms) over and above those who stayed in NZ, supported the war effort but now couldn't aspire to owning a farm??

Life isn't fair buddy, there are always casualties but those who can learn to get up off the ground will succeed, those who don't will fail - an immutable fact.

It's massively different Hook/Yvil. Can I just reply to one account?

Nifty

"it's locked out a generation from house ownership"

Utter b*llocks. Simply blame shifting yet again.

Anyone who has bought a property in the recent past has done well and many are young FHB.

We have one person posting here that they bought as a FHB three years ago and their 30% equity is now 60%. His mortgage is now no doubt considerably less with interest rates falling about 30%.

According to RBNZ data there are 29,000 mortgages - most likely over 50,000 people who as FHB have made a serious commitment and bought in the past 12 months.

Monthly FHB numbers for the past four months are at a record high since RBNZ first collected data in August 2014 - currently twice the number compared to 2014.

Interest.co reports show improving affordability.

So stop with this generation thing; take a good look and seriously ask yourself why you are bleating-on while many of your peers now own their home.

Baseless blame shifting is simply providing false justification to avoid accepting reality. Exactly as Trump is doing and you are right up there with him.

Cheers :)

Raging on a Sunday Printer8, not a good start heading into a new week.

Nifty

Not raging at all. Totally amused by comments such as yours and just bringing discussion back to reality.

Apologise to be bursting your bubble protecting you from reality. However I hope the week ahead goes well for you.

As for me, heading into the new week is no different to the weekend - same old, same old so don’t worry.

Cheers :)

So his right to provide for his children by turning residential properties into rental houses greater than the need of some other person's children who simple wanted one of his rentals as their first (and only) home? How is that fair on the other family. Or is Yvil's family more important than that other family?

That you can't see how this doesn't work across all of society - when everyone thinks they are helping their children by buying up houses - but in fact they are just buying the house that some other persons son or daughter wanted for their first home - its absolutely stupid! All it does is pushes prices up and increases debt.

Our fear of the future makes us greedy - and being greedy means we lose our moral compass and can't see the forest for the trees. Sorry Hook - completely disagree with you.

The slave masters had the same idea. They were only looking after their childrens futures. Building up a profitable cotton farm. Whats the problem with that? It is shocking that this mentality is still with us today.

When did Yvil suddenly become the Salvation Army?? Obviously his future and the future of his children (if he has any) are his primary concern. I may be speaking out of turn but I'm fairly sure Yvils concern for his family FAR outweighs his concern for someone else's family - as it should.

Whilst you're entitled to your opinion IO, if you're that concerned about other people's families I suggest you join Habitat For Humanity

Why do I get the feeling Hook and Yvil are the same person?

Hah, I thought it was just a matter of time until someone suggested this. So you and Orrsome are the same and all the others who agree with you… Com'on

Hook, the "you're a bad person for looking after your family because somehow it must be at the expense of others" is just a shallow excuse, if there was a chance for Orrsome or Nifty to make some money, they would al of a sudden completely change their tune.

This is where ethics and morals come into the argument - if making money means buying a house that some young family wanted for their first home....count me out. Especially when a person already has their own home - why do you need another?

We live in a primarily Christian based society. One of those key teachings was to do with 'love thy neighbor' and 'give and you will receive'. Instead landlords think its 'turn thy neighbor into a rent slave' and 'take and you will receive'.

If you think the quality of society will improve by being greedy - well you're going to have to think again.

Christianity is well out the door in NZ, anything goes now. What are morals?

IO, lost the argument so go back to moral and ethics bla-bla-bla, like you don't buy cheap stuff made in Asia by people who earn NZ$5 a day, get off your high horse and get real, stop judging others you're no better than us

I don't claim to be better than anyone - nor have I. I'm simply point out what ethical actions might look like and what they might not look like as well. We each reap what we sow when the time comes. And if you want to take advantage of a situation at the detriment of others within your society you can but it does come with consequences.

Taking advantage of a situation created by others is called "opportunity". Even the Vatican know this - and they are the richest organisation worldwide, no consequences coming their way recently

Your definition of opportunity is very different to mine.

It's called diversity of opinion. Nobody is inherently right or wrong - they just have their own approaches.

Yes and I'm glad we respect each others so much in forums like this :-)

IO

According to a previous post of yours you have been predicting housing bubble burst now coming up to six years.

If that has been your view for holding-off buying - in which time houses have increased considerably - the that was your decision. 50,000 young FHB have purchased in the past year - you appear not to be one so that is fine, your decision and so accept the consequences.

Wear it and stop the seemingly envy based slagging others who have come to a different decision, have acted and have done well.

Cheers

"We live in a primarily Christian based society. " - wow, you are seriously misinformed. Thankfully I don't live a "Christian based" life where humanity has the ultimate right to constantly debase, degrade and destroy it's natural environment. I do however believe humans are the current resource. Some can farm them, some get farmed. That's why Capitalism was invented.

And that's probably why it will die.

No xmas this year Hook, or presents in your house?

Just another day off. I'll enjoy the sunrise and I'll give the bulls a scratch behind the ears (They like that,If they don't run me over), take the dogs for a run. Probably feed the local hawk with a rabbit, listen to the tui's and the thrushes singing their hearts out. Just another day in paradise. TBH I do feel some sympathy for urban dwellers - I long ago turned my back on that dysfunction

Guess you're right - but I'm just trying to remember what other holidays we in the anglosphere have for people who were born and died/resurrected (supposedly...) 2000 years ago? And that its the year 2020, not the year 143355453132421342342351345132423412341. Don't we swear oaths on the bible in relation to law and governance?

Tbh I'm not sure there's too much relevance for most of NZ Holidays. Most of them are a holdover from colonial origins. Guy Fawkes always gives me a chuckle - celebrating a failed terrorist attack on a largely irrelevant Parliament (in the NZ context). ANZAC should have pride of place (IMO), followed by Matariki. Easter is a usurped pagan festival which is actually out of sync with our seasons.

Guy Fawkes is maybe relevant to Huguenots but Catholics might want to check out why it’s celebrated.

IO, your "skin in the game" thing is ridiculous, you're trying to infer that some of my comments are made to influence others for my own gain, That's exactly what you're getting at. Actually skin in the game means that I have deep knowledge of RE since I've been dealing with it, day in day out for 25 years and that I know what I'm talking about

Or you have deeply ingrained biases because you don't know anything else. But you can't see it because you can't see the forest for the trees.

. . . and IO you continue to hold on to this housing bubble burst for the past five plus years.

Mmmm . . . . not sure as to who to date doesn't know anything and can't see the forest for the trees and has been wrong.

Cheers :)

P.S. As to the future; if betting, the odds are at least slightly stacked against a bubble burst. Rightly or wrongly after all the actions Orr has taken it appears he will likely be doing his best to try to ensure that there is not considerable correction undoing all actions to date.

Every action they take to delay a correction only leads to a larger correction, this article is yet another warning sign showing imbalances continuing to build, and the rate now they are building.

Orr has already overextended himself, there is going to be mounting pressure on the reserve bank now to stop making the problem worse.

Massive Conspiracist with a capital C that's orrsum Awesome but a little sad being left in the cold

There is no correlation between getting up early and a central bank dropping interest rates and flooding a market with QE.

Perhaps not IO. But there is a correlation between getting up early, applying yourself and being ABLE to take advantage of said QE and low interest rates.

Not interested in 'take advantage' or 'getting ahead'. I'd rather just be a beneficial member of society who contributes and pays my taxes and leave the place in a better state than I found it - but when so many people are 'taking advantage' and 'getting ahead' they forget who they are leaving behind - their brothers, sisters, children, nephews and nieces. We need a collective approach - not I'm going to get up at 5am so I can turn my neighbors home into a rental property.

IO, do you own or rent?

IO questions and judges but he/she is not brave enough to share anything real about his/her life, too scared of being judged by people like him/herself

From earlier IO posts... he told us he worked in the USA and witnessed the credit crunch first hand then came back to NZ in 2013 and started looking for a house but refused to pay the 'exhorbitant' Auckland prices. He has been grizling ever since. In between trading stocks and precious metals after he read some Ray Dalio spruiking. Not exactly the honest taxpaying benevolent citizen he wants to make out as now

How does any of the above point to me being a benevolent (or other type of) citizen? In either the good or bad sense?

Can you remind everyone how many rentals you own HW2 so we can be clear where you stand on the discussion around lending to housing? If non - well great. If multiple, then you probably have a bias that everyone should know about.

"by Independent_Observer | 29th Nov 20, 3:51pm

Not really sure how anything further than that is needed on a website like this. And besides, an online persona appears to lose its charm if people know too much - I'd be a fool to share much more. If I wanted people to know everything about me - I'd be on the stuff.co.nz or FB comments sections."

Gee, conflicted??

Beautiful!

IO questions everyone about their biais, knowing now that he missed buying a house in 2013 because he thought it was too expensive, it becomes now crystal clear why he is so much against people owning property and it sure has nothing to do with morals

Really curious why you spend so much time commenting here if you are so well off.

Gee, I would be travelling, eating out, going to films and concerts...

Genuine question - why are you here?

I am here because I am angry about what this country has become, especially the greed and inequality that all this housing nonsense of the last 20 years has fostered.

I would like to think you might be here because you genuinely think housing ownership and investment is a way for people to improve their lives. Unlike some other spruikers here, you do seem to have a smidgeon of humanity.

You do seem to miss a major point though as to how hard it is to get on to the property ladder now, primarily in terms of getting a deposit together.

I read the articles to keep informed.

I comment in the hope I can help someone just as someone helped me understand Real Estate when I was in my 20's. Unfortunately I find it really hard, most commenters are more interested in arguing rather than learning anything. If I can successfully convince a few people to buy their own homes rather than keep renting and being scared that the market is going to crash, then I'd be very happy

I suspect it's good ole Houseworks back with his nasty trolling antics.

You mean I don't gloat when I sell a house and make a million dollar profit? Is that what you mean by not sharing personal information?

I have owned property in the past (never been in the rental game, nor will I ever while young people can't afford a first home) but have been some what nomadic work wise jumping around the globe and cities in NZ. Currently renting. Have worked public and private sector.

Not really sure how anything further than that is needed on a website like this. And besides, an online persona appears to lose its charm if people know too much - I'd be a fool to share much more. If I wanted people to know everything about me - I'd be on the stuff.co.nz or FB comments sections. Perhaps I am and have talked to you there? ;-p

"beneficial member of society who contributes and pays my taxes"

faker ... really you are not much different to a venture capitalist other than you have a smaller sum yet like to portray the benevolent (yes I'm sure you probably are too) victim. All the best

I've worked both public and private sector - I've paid plenty of PAYE over those years.

IO

No sympathy or not interested in helping those who sit back and don't have initiative and critical of those who do.

Simply a philosophy for self-appeasement as part of reality denial.

P.S. If you want to use the sloppy argument that investors are leaving people out of housing - then by the same poor logic, property investors are providing some housing for the otherwise homeless. :)

Go back and reread the original proposition which was "to do well" there was no reference to having to be a property investor, or even homeowner. Time to go to SpecSavers!

The problem isn't that I can't see or read, but more that I can see right through you.

If you want to become wealthy or happy learn to work harder on yourself than your job as personal development lasts a lifetime. Getting and becoming are two sides of the same coin as you have to learn to handle the responsibilities that come with greater income and wealth or you go backwards. Example if an impoverished person was handed a million bucks would they really know how to handle it well... so they have to 'become' a millionaire as well

In terms of personal development - I think you're stuck at the independent/interdependent growth stage. You think your actions have no implications on other people. When you realise we live in an interdependent society and what we each do impacts other people, then you might see that landlording in a time when young people are struggling to buy isn't a particularly virtuous trade - you might then question 'what are my morals and values'? Is taking rent from people or buying that rental property at a price that that young person can't afford a very nice thing to do?

So yes you are right - personal development lasts a lifetime. Some can see past themselves though in that process. Being on a website like this with a name such as 'flying high' and talking up property investment to some people who can't afford to buy is hardly a sign of great personal development (FYI)

Right now I am in my weekend bach lakeside in the city. Is that fair, absolutely it is, or have I taken a home off someone else who wants a home for themselves. You speak like there is a finite number of homes which means some people have to miss out. Flying High refers to my love of international flying which I am not able to do until the virus has been killed, I also used to be a pilot. High is just a pisstake for those who voted in the referendum. I realized later that FH also refers to First (but not last) Home, a very topical issue you would agree. Much like yourself IO could be a reference to IOU or Interest Only take your pick.

Good for you - hope your back flying high soon enough (honestly).

Kiwibank with 88% of its loan book on housing - I would not touch it with a barge pole.

You'd think being a Kiwi Bank with 51% Govt ownership they'd support all Kiwi sectors & diversify... clearly not.

How do they sleep at night? They are leaning heavily over a cliff and Orr is holding their hand keeping them from falling 100 meters to their death. I am starting to wonder if Orr gets a weird kick out of taking the banks to the brink so that he has total control of their destiny.

Herein lies the problem; the RBNZ lowers interest rates to encourage businesses to invest, but 60% of it just gets “invested” in housing, as if we didn’t already have too much of that.

The Govt through Kiwibank will likely invest 88% into housing...nice.

Respectfully disagree " The New Zealand economy is more of just a housing market than ever "

Stats NZ provides wonderful infographics relating to both GDP/ economic growth nationally and regionally . In the past two decades it is clearly not so

http://infoshare.stats.govt.nz/datavisualisation/gdp.html#53

All ready built, bank leveraged residential property speculation is a non-GDP qualifying transaction. Hence, a minor fraction of bank lending (credit creation) is underwriting GDP qualifying economic endeavour.

The Business Loans are well understated due to the fact that many Housing Loans are used for Business purposes and that isnt recorded by Banks... in a study undertaken by one of the Banks a few years ago, followed by a big push to ensure that the correct loans were underwritten, as much as 5-10% of Housing loans $ amounts are used for Business purposes...not to mention Personal purposes (ie new car, boat, etc).

The loans are still secured against housing so kind of the same thing. Alot are probably paying residential rates too as opposed to business rates.

The problem I have is the banks want a CGA for business lending. This gives the bank the powers to appoint receivers for my business if they see fit. This is too risky for IMHO, so you have to borrow against a property to lend to your business.

Sorry GSA

A historical note. Nothing new.

Ten years ago .... Back in 2010

Bernard Hickey produced a daily column here on interest.co.nz called 90 seconds at 9:00 am - on property

There was a regular contributor with the nickname of Chris_J who wrote informatively on property. He was the manager of a family investment company investing in properties. While he never disclosed how many properties they controlled, his posts indicated they had a substantial portfolio. My guess at the time would have been in the vicinity of upward 50 houses, possibly nearer 100. In one post, while discussing numbers, in an oblique attempt to deflect, he revealed there was a Christchurch family who owned more than 1000 properties in Chch. This was in 2010. Chris_J was in the process of rotating out of Chch and into Remuera and St Johns. They took all their earthquake insurance proceeds and re-investing into Auckland. He went quiet around 2013 and hasn't been back

Auckland Property Investors' Association President David Whitburn was a regular periodic commentator, in 2010 and 2011, spruiking how he doubled and quadrupled his equity. He also has gone quiet. Disappeared around 2014. Those interested can apply the search function using his name

Recently we have seen the emergence of details more property empires being published in the news. Young bloke in Taranaki with 20 houses, 2 of them trashed by tenants, two Aucklander's claim portfolios, one of 60 homes, another of 70 homes. No trouble. Last week was the occasion of a member of Auckland Property Investors Association announcing knowledge of 4 Auckland based Portfolio Owners, each with over 200 homes.

Then there was the 20 year old Princeling who arrived in NZ as an international student and within 6 months had acquired a portfolio of 5 properties in up-market Takapuna worth $10 million

Such investors are in business and should be paying business interest rates. RBNZ Graeme Wheeler wanted to do that but was squashed by PM John Key. Such businesses of this magnitude are creating a David and Goliath Market. How private individuals wanting to buy a single home can compete against such financial muscle defies logic

This is the way - and so it continues

Of course we also all remember bernards famous 30% housing crash prediction. I wonder if the country would be better off right now had that happened instead of the RBNZ propping it up all these years?

Yes I do remember that - vividly - but never marked him down for it - I held a negative view also

He was wrong, and so was I

Yes well no one can predict the future and he did have a good reason to predict that. Kind of funny now though just how wrong he was.

Pity is - he is now gun shy

Ditto, I don't criticise the prediction as "wrong" either, because that's what "should" have happened in any recession caused by the economic lockdown. But Govt/RBNZ as part of the "Washington consensus" to help markets also massively distorted markets. As Bernard explains:

“No-one could have predicted this boom" is only true "in a limited and short-term sense. If the Reserve Bank had not cut the OCR from 1% to 0.25% and then embarked on a $100b programme of money printing and bond-buying then there would not have been the fall in mortgage rates to around 2.5% that triggered the latest boom."

https://www.stuff.co.nz/business/opinion-analysis/300168640/heres-why-y…

Rod Oram added:

"The RBNZ’s overly-generous and economically distorting support for bank lending is at odds with its assessment of the financial health of banks and businesses"...and "its efforts now to drive bank lending up and interest rates down are doing more harm than good."

https://www.newsroom.co.nz/pro/rod-oram-awash-with-money

Iconoclast

I never bother reading of those who have considerable portfolios especially if they have acquired these in quick time.

They are generally very, very highly leveraged and as soon as advantage conditions for achieving their “empire” change (e.g. rise in interest rates or slight correction) they go under.

I recall being in the PIA during the boom 2000-8 and talks from these high fliers at meetings who were also featured in the PI magazine. The GFC wiped them out never to be heard of again. A small group of us - some who had been in the association many years - gave up as members of the PIA around 2005 smiling in amusement and had a small informal group who meet monthly for coffee which was far more productive. Some continue today while others such as myself retired by choice.

Great article David. May I suggest we look at it from the lender's perspective? Say you or I have $1 million to lend, are we going to lend it to:

1) A start up business who has a 20% chance of doing well and lose our $1 million in the other 80% case ?

2) Someone to buy a house and if they can't repay us we have the comfort to take over the house ?

The answer is quite obvious...

Owner occupied housing is generally not an income emitting asset. Income producing enterprises must be financed to employ mortgage indentured household occupants.

No one is disputing what you're saying Audaxes but Yvil has plainly laid out the reason banks aren't lending to Business, although he did miss the point that Business (generally) isn't interested in borrowing anyway, but are more interested in shoring up balance sheets or paying down debt. I'm sure you're aware many normally regular dividend paying companies have either reduced or suspended dividends recently.

Indeed - Banks extend ~60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them a RWA capital reduction incentive, to do so.

{kind=link}

Interesting table. Could you replace the RWA with "likelihood" of failure I wonder if you took away the insurance cover?

Audaxes your comment has little relevance with the point of my post but nice use of fancy words, sure to impress a few

"Income emitting".

༼ʘ̚ل͜ʘ̚༽

As a bank should, hire business banking specialist who have the ability to identify that 20% who are going to be successful and back them to succeed.

Banks don't take any comfort in taking over a house - this is an extremely costly and a time intensive exercise.

by Nifty1 | 29th Nov 20, 10:20am

Most SME owners would secure loans against residential property, the banks don't really have a tolerance for anything else.

Hmmm.. make up your mind Nifty1 - seems the so called specialists are a bit risk averse anyway.

No I think its a matter of the banks not investing in specialist to make these decisions. It's also a matter of credit policy setting the tolerance for such lending.

Tbh, I doubt many so called "specialists" actually have much of an idea about small or startup businesses so it's really up to the borrower to put a well researched and costed Business Case in front of them. Included in that should be some form of qualification regarding Business Management. Even with all that provided, due to the risk profile, most banks would still require security over housing. The failure rate of startups is far too high to be anything but a gamble with an unsecured loan.

This is the problem, it's in the too hard basket. Instead banks put everything into housing, with no diversity. Housing goes belly up and they're screwed.

4 out of 5 new businesses fail, no "specialist" is going to be able to predict which 20% will make it and which won't, there are far too many variables

Perhaps some of them fail because they didn't have sufficient funding & cashflow? Perhaps they didn't have the right help or guidance . I don't think a business specialist would pick 100% right, just like a homeloan specialist doesn't - mortgagee sales. There's always going to be risk and allowance for bad debts/right offs. Down right avoiding business lending like Kiwibank, seems like a bad move if sh*t hits the fan in the residential property market.

Nifty1, look my post was very simple and straightforward, so please answer, if YOU have $100K of your own money to lend, would you rather lend it to a business with an 80% chance of failure or would you rather lend it to a person who wants to by a house knowing that you can get the house if he defaults ?

Please answer the question

Right now, I'd probably diversify that investment rather than putting my eggs in one basket.

So do 4 out of 5 property investor fail Yvil - because I thought they were 'businesses' and get the tax deduction benefits of being a business?

Unlikely IO. They're in the 20% that get supported by the Bank.

So are they not businesses then or is the comment about 4 out of 5 businesses fail clearly fake news?

Obviously it's not "fake news" as you obtusely maintain. Yes a professional property investor is a business and yes they're part of the 20% who don't fail. Simple really

How many businesses are there in NZ and what proportion of NZ businesses are property investors - anyone have the stats?

Given that about every second baby boomer you talk to appears to own a rental or two and will have tax deductions on that rental property - there must be hundreds of thousands (or closer to a million or more?) property businesses in NZ - and none of them fail because they aren't allowed to.

So how then do 4 out of 5 businesses fail if the most common business practice in the country - property investment, never fails because its not allowed to by vested interests including banks, the central bank and the government? Wish all other forms of small business had such protections.

IO you're using unsubstantiated assumptions to further your arguments. I don't know the % of Property Investment businesses vs "other" businesses actually are but just because your impression of "every second baby boomer you talk to appears to own a rental or two" fits your narrative, it doesn't change the fact that lending to startups and small enterprises is extremely risky and prone to failure

Not lending to them is equally risky as that is where innovation and productivity gains come from.

Its not like we've got the dotcom bubble on our hands here in NZ - but we do have a property bubble. Yet we think lending more to something that is already exceptionally highly priced is less risky than lending to something that might improve our GDP - well there's one of our issues.

Get out of your cloistered lecture halls and live the real world. It might teach you a usable lesson

Haah, the real world. NZ is not the real world. It is just a scruffy version of the Truman show with a bloated, red faced fat man with a head shaped like a turnip and funny glasses on doing all of the directing. I find it hilarious that you think any part of NZ is anything like the real world. Not been many places then?

Obviously watching a property bubble explode while working in an overseas country and the real world harm it does isn’t actually real world enough when it comes to a topic such as this. Oh well.

Remember SCF Nifty1? Hubbard did exactly what you're advocating and took a serious bath, as did Hannover, ALF (for a time), Blue Chip. Even MARAC didn't do that well and was sold (to ANZ I think?) Watch Harmoney's fortunes going forward, the next few years will be telling for them.

Ohhh that's a great post Hook! Great examples of why banks are not soo keen to lend on businesses in uncertain times. I'm not saying it's right or wrong, but I certainly understand why they're reticent to lend to businesses

Aren't you a business owner Yvil? Sure you've had frustrations with the hurdles of borrowing from a bank for business purpose?

Let's not forget, the banks aren't lending for free. There's good profit to be made with the correct risk assessments made and investment in specialist staff. As stated above, it's in the too hard box. Housing loans are clearly the easy the option. It's a business decision not to diversify, as such banks shouldn't be bailed out.

Nifty1 how about answering Yvils fairly simple question regarding lending YOUR 100K without security over property?

I did, I would diversify my investment. I wouldn't go all in on either.

Actually you didn't. The question was "would you lend (unsecured) to an enterprise with an 80% chance of failure or to one with a guaranteed collateral?" So you'd put 65% into housing and 35% into mortgage secured small business loans?

You're not reading the comments right Hook, take abit of time to go through them. The investment question started as 1 million dollars and then you and Yvil changed it to $100k. No idea where you've got my potential ratio of investment?

Answer the question Nifty1 - 100K or a Mill. doesn't matter. Where would you lend it?

Nifty1 Nifty1 wherefore art thou? I'm still waiting for your answer

I'll tell you this much, I wouldn't invest it in someone who uses multiple accounts to back up their opinion on interest.co.nz, that's for sure.

haha.. so you still don't want to answer a simple question? Pretty sad you won't back yourself, but not unsurprising.

Yes I'm a business owner and guess what, the loans for my businesses are secured against… the real estate I own. Two advantages, 1 the banks are happy, 2 the interest rate is much lower. That actually illustrates perfectly my earlier point

The banks are happy because you own multiple properties, that derive an income of their own and are now mortgage free. Edit* you said earlier that you're mortgage free but now you've said you have business loans secured against your property?

Not everyone has the luxury of owning a home to borrow against. How'd you get started in the motel industry - where'd the funding come from?

You missed the possibility of the whole housing market turning to crap along with the economy and people lose their jobs, can’t service the mortgage, and no one wants to buy their house. Of course the bank CEOs are happy to gamble on that as worse case they just lose their job (and pretend they didn’t think it could happen)

Exactly - you have to view the system as a whole not as individual transactions to understand the true risk.

JimmyJones, the RBNZ and the government have made it quite clear that while "they are concerned how fast house prices are rising" they do not want to let house values drop. Your or my opinion matters little, the RBNZ & the Government will make sure there's no housing crash, they made that very clear and they have the power to make sure house prices won't crash

Its more a thing of 'confidence' now - not 'control'. If the tide turns there will be little that RBNZ or the government can do (animal spirits) - unless the start paying everyone's mortgages?

jj.. that's a big part of the problem. Banking execs are incentivized to take big gambles to gain max bonuses. And not to care at all about what happens once they have moved on. Taleb calls it The Bob Rubin effect.

But who creates the job that generates the income to pay the additional mortgage?

Well because house prices are guaranteed to double every ten years we can just all borrow more money now and spend it. It’s like a RBNZ guaranteed lotto ticket. No one needs to actually do any work do they?

IO The mortgage, rates & insurance are being paid by the tenant in the form of rent

Or the State, in the case of Transitional Housing which is where the real money is. A growth industry with unlimited finances.

Yes and where does the tenant earn their money to pay those bills so those people in those industries get paid?

They earn it.

From WFF, and labouring for the Accommodation allowance. ;)

Haha unfortunately you're right in a number of circumstances.

Where do those renting secure funding to meet the landlord's demands?

This is like a healthy organism explaining to a parasite that its behaving like a leech but its confused as it thinks its the healthy organism - but then realises there are no leeches attached to it - only it attached to the healthy organism.

It's hard to see the situation improving when those in charge (Orr, Robertson, Ardern) can't even see the problem, as indicated by their frequent comments. They tend to think that if the rate of house price increases, slows down somewhat, then all will be well. But I read recently (forget the source) that it would take 45-50 years of a housing price freeze in order for incomes to attain the level at which housing becomes affordable for median earners. So is the time ripe for a new political party (The House Party)? : ), whose primary platform is to tax property speculators, at punitive amounts, say, 20% if sold within the first six months, 40% in the next six months, etc. The party spokesmen could go on RNZ and proudly declare that his or her main qualification is that they are not an economist (whose inflation-targeting policies of the last several decades created this mess). If the idea resonated with enough people, it could serve to influence the major parties. Ah well, a man can dream...

We don’t have as many of those one policy parties as you would expect under MMP. Even the greens are not just an environment party. A party as you discussed could easily hold the balance of power. Although if that happened and the tax was implemented then it’s the end of the party so unlikely to get much financial backing.

A "housing party" in kingmaker position is one way the bubble ends. A very realistic scenario if labour sits on there hands for the next 3 years

Either way I'd say it's reasonably clear that by 2023 efforts to cool the market through regulation and supply should start to filter through. How much higher prices get to before then though is anyone's guess.

TOP party already exists, no need for another one. They would transform the tax system and dramatically change the economy towards productive businesses instead of speculation. The idiots of NZ however all believe it could never work (i.e. they are trapped by tribalism/comfortable life (if they own property)/populist thinking). Most simply think they have an "anti cat" policy (despite Gareth Morgan having nothing to do with the party anymore) and have eaten up the idea that if they vote for something different, it will be wasted.

Great article, DC. I've always idly wondered why the RBNZ does not gently nudge the regulatory settings towards a higher RWA on resident housing (perhaps differentiated by usage: home versus rental etc) in order to (again, gently and with perhaps a considerable lag) rebalance things.

Perhaps later this decade, after a nasty episode or three?

Here's something for all the "equality" crowd. If you have your "ad blocker" turned off you'll notice a constant ad promoting some sort of clothing - it's worn by a reasonably attractive white girl - not an Eskimo. If the clothing was relevant and effective you'd expect an Eskimo to advertise it - the fact it's some sort of girly who's probably never been near the snow (unless Daddy paid for it) but she gains exposure says it all

Wow. That's some pretty blatant trolling. It's pretty obvious you're just dying to be called out so you can complain about over sensitive snowflakes.

By the way, Hook, on the internet people tend to see different adverts.

He's a little redneck trolling from the provincial heartland.

He is getting those advertisements because of the porn he watches, he clearly isn't into equal opportunity there.

Finally other commenters are calling out IO for what he is. Mike Kirk has gone awfully quiet all of a sudden also.

Would you like to explain to everyone ‘what I am’?

A very judgemental person, you have a history of asking others personal questions and whey they are brave enough o open up about their own lives, you use that information to tear them apart and let them know how bad they are. Not cool at all.

That would be a very judgemental thing to say! ;-P (can you not see that you have judged me with equal amount - and can you not see how that would make a person a hypocrite? To claim someone is judgemental, but in the process of doing that, you are judging them)

https://i.pinimg.com/originals/fa/08/53/fa08537fdd7342ec6f6600179865d9a…

{kind=link}

So true even for residential building banks are running scared. I got a response back from bnz who were potentially my clients best option for servicing to build a new investment property except they want a 20% higher servicing capacity to alow a build vs investment purchase. Previously the rbnz was incentivising new builds which would help economy growth and the housing shortage - but this seems to have been thrown out the window now

Man, I had no idea TSB and Kiwi bank were 86% and 88%. Unfortunately, once my TDs with these banks mature I will no longer be supporting these NZ owned banks. Seems like any serious property downturn would put these banks at much higher risk than the Aussie ones.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.