By Brendon Harre*

Former Finance Minister Michael Cullen recently wrote an opinion piece on housing and monetary policy. To paraphrase him: the Reserve Bank are the Jedi Knights of the economy with interest-cutting lightsabers fighting against the evil empire of inflation. This worked when the problem was stagflation - high consumer price inflation and poor economic growth - but it is not working now when the problem is poor productivity, rising inequality and high house price inflation.

The Reserve Bank (RBNZ) has rejected Finance Minister Grant Robertson’s proposal for its monetary policy remit to consider house prices as well as its current inflation and employment targets.

Rather, Reserve Bank Governor Adrian Orr has suggested house prices be included in its financial policy remit - the way it regulates banks. The RBNZ has asked Robertson for debt-to-income (DTI) ratios be added to its macro-prudential toolkit, so it can restrict bank lending to those seeking large mortgages compared to their incomes.

In summary, Adrian Orr is not going to be a Jedi Knight fighting housing inflation but he will continue to protect retail banks from a crash in the housing market.

The Reserve Bank Governor went on to say: “Given the wide range and number of parties involved, and the complexity of underlying issues, there is a need for a single agency or ‘clearing house’ to co-ordinate the government’s response across agencies.”

This statement is not quite asking for an independent housing commissioner, which I will explain could be a way forward, but it is very close.

Michael Cullen sees an opportunity for monetary policy reform “in the current situation to make a quantum leap forward in dealing with some of our needs, which require large amounts of capital.” The primary needs are a big increase in the level of housing construction and infrastructure development, and a large investment in transforming the economy to meet New Zealand’s climate change commitments. There is a strong echo of the First Labour government in this policy prescription.

If the government intends to copy the Michael Joseph Savage Government and use the Reserve Bank to invest in a massive housing, infrastructure, and climate change build programme I would agree wholeheartedly.

Renting in New Zealand is bad - for low-income groups it is the most unaffordable in the OECD - as my previous paper published on interest.co.nz showed. The Government should transition from band-aid solutions like the Accommodation Supplement to comprehensive, long-term solutions like a large-scale public house building programme. But that is not the signal the government is giving.

New Associate Minister of Housing (Public Housing) Poto Williams states the government is on-track to produce 18,000 public and transitional housing places by 2024, or about 4500 government builds a year. This is a significant promise. Without adjusting for population, it would be the biggest government build programme over four years. Bigger than anything seen previously, including the First Labour government. But on a per capita rate it is only half the rate of the Savage government. The promised government build programme is about 12 per cent of total house production (which was almost 38,000 houses consented in the year to October 2020); it is also half the rate of those countries with large-scale public housing build programmes, like Austria.

It is also not clear how the government will go about building the equivalent of 4500 public houses a year. State house builds are currently running at about 2000 a year, although they are on an expansionary trend. There has been no funding announcement for the Community Housing Provider sector, so it does not have a significant build programme. There are some transitional houses, but not that many - currently there is a stock of 3650 with 120 added in October 2020.

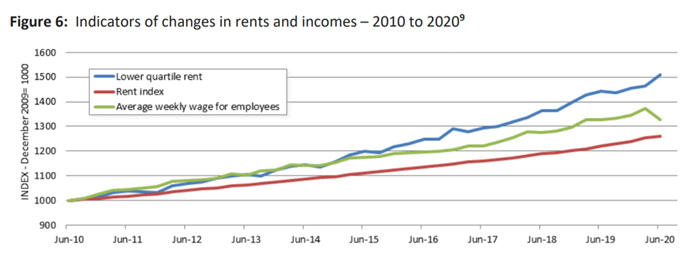

Lower quartile rent is inflating faster than average rents and faster than average wages. Source

For the rental housing market, despite some increase in supply, increases in demand is still the greater effect — it is pushing up rental prices, especially at the lower end of the market. As Stats NZ detail in a major review of housing the rental housing market is in even worse shape than thought. The government has tried to respond with initiatives such as Housing First, which created a stock of transitional housing. People are meant to live in these houses for a maximum of 12 weeks, but because there is insufficient long-term housing to move into, residents are staying much longer.

The waiting list for public housing is growing and now exceeds 21,000. This is due to a range of issues, including the private rental sector not catering for those on low-incomes, structural planning restrictions on building, and the public sector having insufficient resources to compensate.

In Parliament, Opposition Leader Judith Collins asked Prime Minister Jacinda Ardern if the $4600 increase in median rents since Ardern took office and the public waiting list ballooning to over 21,000 were signs of a housing emergency.

There are many questions that can be put to government ministers on housing. In effect asking if they are housing Jedi Knights.

The biggest question, though, is whether the prime minister is a Jedi fighting the evil empire of housing inflation. It is quite clear to anyone following politics that National are planning to beat up Labour on housing issues just like Labour did when they were in opposition. Yet, neither party is prepared to go past tokenism and implement a genuine workable housing accord.

Ardern’s recent public comments on housing are closer to former Prime Minister John Key’s then Savage’s, even though Ardern has a portrait of Savage in her office.

By stating recently that the government’s goal is sustained moderation in house prices, Ardern gave the message that the market is too big to fail - that house prices can rise but not fall, and that this price guarantee is government and Reserve Bank policy. And there does not seem to be any suggestion there is moral hazard in these guarantees. Nor even an acknowledgement of the social costs (H/T Bernard Hickey).

The problem Ardern has with progressing a housing affordability agenda is that when the government is distracted by multiple needs, such as responding to Covid-19, housing demand and supply pressures can - and did - get out of balance, meaning house and rent prices inflate excessively. This creates a new, higher floor-price in the housing market and the ratchet effect of the rack-rent process stretches renters and first home buyers (FHB) even further.

Ardern’s second problem is the rack-rent process has created the perception she is soft on housing - that there will be no meaningful consequences if house prices and rents continue to inflate unsustainability. Meaning investors’ and others’ expectations of further capital gains is being reinforced.

Environment Minister David Parker has the task of replacing the Resource Management Act with two new acts - a Natural and Built Environments Act for most consent applications and a Strategic Planning Act for issues like transport - plus a separate law on managed retreat from land threatened by climate change.

This would be a heroic task in the best of times, but with a prime minister soft on housing - like they all have been for the past 20 years (arguably the housing political football started 70 years ago when the cycle of one government building state houses was followed by the next government selling them) - the task becomes mission impossible because no legislation can perfectly align all the involved entities (local authorities, government departments, developers, construction industry, iwi etc.) for all potential circumstances.

Parker has been set a heroic task but he lacks support from the head of his government because the prime minister does not have the credibility in the housing space to get everyone on the same page. David Parker needs a friend -he needs a housing Jedi Knight.

This is not a situation unique to Ardern. The last National-led government under Key faced the same difficulty with housing. New Zealand, therefore, has already seen what happens when the prime minister has their hands tied on housing. Action inevitably degenerates into the various involved parties acting at cross-purposes to each other, blame-shifting and finger-pointing.

Politicians have been in this situation before. The stagflation of the 1970s meant politicians lost credibility to run monetary policy to tame consumer price inflation. In particular, they lacked credibility to change the public’s inflation expectations.

But public opinion needs to change, too. As journalist Andrea Vance says, housing should be a right for all New Zealanders: “we should think of it in the same way we regard universally available services, like schools, hospitals and public transport”.

Successive governments at the central and local level have manipulated the housing situation for their own ends. As journalists such as Bernard Hickey have detailed, they have taken the fiscal benefits from a massive immigration boom yet underfunded the required infrastructure. They have deferred maintenance on out-of-sight infrastructure for decades because they did not want to impose rates increases on homeowners, creating a multibillion-dollar infrastructure deficit. Local government and electorate politicians have actively worked against moderate urban planning initiatives. The political class cannot put the affordable housing genie back in the bottle.

An independent entity with clear targets and tools is required to ensure housing as a human right is delivered for all New Zealanders.

Could an Independent Housing Commissioner be the Housing Jedi Knight that New Zealand needs?

I think it could be if the independent Reserve Bank governor concept is used as a guide.

What would the policy targets be?

I would suggest the following, in order of importance:

- Rents as a proportion of income falling below 30% for the lowest 20% of income earners.

- Median house prices inflate slower than median income increases.

- Housing market remains stable and does not destabilise the wider economy.

What would the tools be?

- Ability to fund an expansion of social housing placements as needed. Preferably using the Austrian social housing model because of its cost/benefit efficiency, its stability over the political cycle, and its transparency in achieving multiple goals - social, economic, environmental, architectural/construction quality.

- Ability to buy land in support of urban area spatial plans and release it at cost for urban development as deemed necessary. As a last resort, the Housing Commissioner should be able to use the power of compulsory purchase if there is evidence of land banking. For each and every instance of compulsory land purchase Cabinet level sign-off would be required.

- Ability to appoint and direct Independent RMA Hearing Panels to review planning regulations, such as occurred with Auckland’s Unitary Plan.

- How to fund this? - the Housing Commissioner uses the mana of their position to publicly request funding as required - something like the Climate Change Commissioner. Or possibly something like a 1% housing fund income tax that Austria has (see programme funding section here) for funding land purchases and capital grants for the social house build programme.

How would this work?

The housing crisis has grown for the last 30 years - it might take half that time again to resolve. Over time, the solution could look like this:

- Housing Commissioner focuses on their first goal - reducing rent as a proportion of income for low-income groups.

- Housing related inequality reduces.

- The Housing Commissioner’s credibility with the public increases.

- Capital gain expectations in the housing market declines.

- There is more investment in other more productive areas of the economy.

- Labour productivity improves.

- Housing Commissioner use policy tools to work on second housing target - house prices relative to incomes.

- Incomes rise faster than house prices.

- Eventually the housing market becomes affordable - first for renters and then for first home buyers.

- Policy success - Yah!

This is a repost of an article here. It is here with permission.

79 Comments

On this issue they are like helpless possums in the head lights.

They will be completely flattened in the next election.

Oh look; two moons!

There's only one party with any sort of chance actually gives a damn and that's the Greens, so if the labour party falls for ap them then so be it, the Nats will do nothing, ACT will do less than nothing

BS to the Greens - their answer is more tax. That won't do shit to solve or alleviate the problem

Just not going to happen. So many voted labour just to keep the greens out of coalition.

Which, in turn, will turn those who expected Labour to do the right thing closer to the Greens. If you don't like that, blame the same people who came over to Labour to give them the majority

Doesn't matter what I like. It just simple logic.

The greens won't be in charge. They are seen by too many people as extreme, idealistic, impractical and divided because they act that way all of the time.

They may well get more votes, but not enough.

I suppose that there is another way of looking at this.

The conventional political and monitory management frameworks are not working to serve the populations needs. This has been evident for several decades now. The financial levers during a down turn are very poor at effecting change and just seem to produce a whole set of new problems. The approach to date has been to cling to wrote dogma, rather like religious dogma and ignorance that held civilization back until the scientific and industrialization that has transformed the world over the last 200 years or so. The transformation occurred when we recognized how much that we did not know; thus embarking on our research and facts based upward acceleration.

Maybe admitting that we do not know what to do and and starting with a clean sheet of paper is the best approach. But my goodness they need to hurry and not take that as an excuse for endless naval gazing as we saw in the last term. The next election is racing up on them at an alarming rate without any apparent progress. Fail at this, this time and it will be two moons I am afraid.

Ardern and co can't even sort two way travel between us and the Cooks, something they've been jibbering on about for months. If there is to be even the beginnings of a solution to Housing affordability, I doubt it will be initiated by this hapless lot. There have been many workable solutions offered which, while individually not the solution, collectively could be a game changer. Govt reaction or engagement? - ZIP. Watch for a massive waste of resources channelled into RMA reform (more bureaucratese) and an assertion that "we're working on it" but little concrete action - Oh and a concerned but empathetic frown.

Don't agree with you much, but this is spot on.

Haha, so rare praise? thanx

I don't hold grudges, always happy to acknowledge good points.

Either way, thanx. The issue we all have now ,is how to get a majority Govt to actually do something. I fear that Labour will bumble along for the next 3 yrs and not achieve anything. Yes we can vote them out in '23 but nothing will change. The question remains - when will the people we elect get their shit together and do something??

Haha short answer... never!

Interesting to see though National now doing some real soul searching to come up with a plan for 2023.

Most of the brightest IQ shifted to OZ, despite Kiwis saying emotionally that it will raise both countries IQ? - We/OZ give them s*** for the Banking & groceries.

Majority of Covid new cases currently Auckland. Travel between Auckland and everywhere else in NZ fine. Travel to Covid free Rarotonga/Aussie, not fine, thank you Gruppen Fuhrer ardern - not.

reducing rent as a proportion of income for low-income groups.

This is an admirable goal. Actually, this could apply to all income groups. When I lived in Japan, I decided to move into public housing mainly because 1. The standard of accommodation was good; and 2. The location was close to amenities and my work (only 40 mins door to door by train and walk). The fact that I was working for a corporate on a higher-than-average salary was no barrier to being a tenant. Rent was calculated based on a proportion of taxable income and I estimated that it boosted my disposable income by approx 15-20%. Of course, more disposable income means that more of the share-of-wallet could be allocated to spending into the local economy. This has to be a good thing. Why the ruling elite in NZ cannot understand this kind of rudimentary economic thinking is beyond me.

I really like Japan - they solved so many urbanism issues decades and decades ago.

Yes hopefully renting costs as a proportion of income reduce for all income groups. It should if renting for the lowest income earners costs becomes more affordable.

In Japan they have paper thin built houses because there's a culture in marriage whereby the new wife refuses to live in anything but a brand new house. So they are eternally ripping old houses down perfectly OK to put new ones up. Total madness. Good GDP.

In Japan they have paper thin built houses because there's a culture in marriage whereby the new wife refuses to live in anything but a brand new house. So they are eternally ripping old houses down perfectly OK to put new ones up. Total madness. Good GDP.

Nonsense.

Harre's article raises a lot of good suggestions. I think the rent issue could only be addressed by state providers (do State House renters still pay "market based rents"? If so why??) I'm not sure creating another bloated department of shiny arsed paper shufflers is the answer though. Surely the capability exists within MBIE, MSD and HUDA, it just needs coordination. Maybe the respective Ministers could actually start earning their keep?

No, Labour under Helen Clark got rid of the 'market rents' for State Housing in their first term. They are back to income-related rents, and that is set at 25% of (gross, I believe) household income. Here's the press release from the year 2000;

https://www.beehive.govt.nz/release/income-related-rents-what-it-means#….

..which has created the absurd situation where a pay rise can result in an eviction!

This also expose the stupidity of two system social housing approach - income related rents and the other being the wff accommodation supplement. Both administered by msd. One subject to a net income test, the other a gross income test and asset test.

Harre,s article is pie in the sky and given the abject failure at every level of state bureaucracy letting MBIE/MSD/HUDA operate those ideas qualifies as insanity per Einsteins definition.

Preferably using the Austrian social housing model because of its cost/benefit efficiency,

NZ likes to think of itself as having a sophisticated society among developed countries. And in many ways, it is. However, the economic and social hegemony is still very much based in the English mentality and class structure. The landlord / peasant divide. And that is very unsophisticated for a developed country in 2020.

It's clear that the Government doesn't want to engage any further on housing and is trying to change the conversation by talking up the "climate change" emergency or anything else. It appears that a future Prime Minister will have to lead Government to addressing this issue, in the interim we will just have to endure this situation. Well, not us obviously, I mean the poor and young of New Zealand.

"It appears that a future Prime Minister will have to lead Government to addressing this issue," - there you have it in a nutshell!! A Prime minister with the intestinal fortitude to actually LEAD and make decisions. Seems on the housing issue Ardern is not the one to do this, although in fairness I doubt "the other lot" is either. I think NZ may be approaching a crossroads at breakneck pace with no roadmap at hand.

Hook. that we are 'approaching a (housing crisis) crossroads at breakneck pace' has been easily foreseeable for a decade or more given we unsustainably grew our population at one of the highest rates in the OECD. Key and English were in denial (we don't have a housing crisis), Ardern this week seemed almost dismissive. Harre makes a sound argument for increased state intervention but other than tinkering it ain't going to happen, as he seems to sense. It needn't have been like this. We could have better regulated immigration to match our ability to create infrastructure but both recent governments chose not to.

Actually middleman, my comment about an impending "trainwreck" wasn't restricted to Housing per se. NZs entire structure is slowly but surely going down the gurgler. At our current rate of decline NZ will be a 3rd world status country in 20 - 30 yrs. Immigration wasn't (and isn't) the problem of itself. NZs ability to account for immigration and it's lack of foresight regarding immigration is the problem. While we have pissweak politicians and a self absorbed electorate nothing will change

What we need is a sovereign currency issuing government with the ability to finance housing and infrastructure without the need to depend upon taxation and borrowing.

But wait a minute! That is what we already have, it just requires somebody to tell our finance minister. Not a mainstream economist though as they have no idea where money comes from.

Certainly not Jacinda. Like all politicians she puts holding onto power her priority before sorting out social problems such as house price increases.

That's a bit unfair. She's inherited a problem created by successive previous administrations, what she does about it will prove her mettle. Given that, I doubt she'll do FA. The voting electorate (both at central and local govt level) have created the situation we're now in - it is for the electorate to sort out rather than blaming their representatives. When people bleat about high house prices they should also remember their low rates bills have, in some respects, contributed. These are the people that voted for councillors and politicians pledging low rate rises and static taxes - you get what you vote for and thus have no one else to blame

The cost of infrastructure is getting beyond the ability of ratepayers to pay for. Old infrastructure is nearing the end of its life now and needs replacing, just look at the underground pipes in Wellington City, a hundred years old and now failing and the cost to replace them is in the hundreds of millions. Councils are limited in their financial abilities, they can borrow or sell off assets or raise their rates which people cannot afford.

treadlightly , councils have a requirement to rate according to depreciation of their assets. The fact they have shunted replacement cost funds in to "nice to haves" is both an indictment of councils but more so an indictment of voting ratepayers. Short-sighted, apathetic ratepayers have allowed councils to ignore their core business - provision of services, and they are now reaping the rewards.

Vector (Auckland’s power lines company) is even worse. They get elected to the board with the promise of giving everyone a rebate every year (which I’m sure we are double taxed on prob better just to charge less). Seems to be no interest at all in improving or maintaining the network. It’s starting to look a bit third world with power lines crossing roads all over the place. Every time there is the slightest bit of wind half the network falls over. Yes you get what boomers vote for I guess.

Don't lay the blame for the general electorates failure on one section of it JJ. That's just plain lazy, as is the rest of the non voting and apathetic Vector customer base.

Hook, you need to factor in Clark,s ill advised decision to grant councils the power of general competence which allowed them to invade areas previously ran by private enterprise and no surprises how that has been a disaster -ChCh city council - Flower Show debacle, Buskers stuff up and the total waste of ratepayer $ on cycle ways whilst the infrastructure is still in disrepair 10+ years posy quakes. No doubt many examples in Akld & Wellington too. Removing that certificate and only reinstating it when all councils core services are completed efficiently economically and have been for a decade.

She will not admit that she wants the current prices to go down. Rather she wants the current pace upwards to slow down. The horse has bolted. There is no determination by her to fix the current crisis as admitting that you want prices to drop means political suicide. Keeping your hands on power is more important than principles/ doing the right thing. Politicians are totally disappointing and it’s a world wide problem.

Seems to me that Jacinda is already worried that a failure to do anything about the rapidly rising house prices will greatly diminish her chances at the next election. Therefore I fully expect some significant action from the govt to try to take the steam out of the market. I have no clue what that action will be, or whether it'll work, but I'd be surprised if they did nothing. My sense is that the issue is getting too much bad press, and Jacinda's survival instinct is too strong.

Another excellent comment, especially on rates and the eternal local government mantra of keeping rates down.

All govt spending is taxation - no matter how you dress it up.

A good piece Brendon.

My views on housing in the last week or two have shifted a bit.

Firstly, and most importantly, I think it's damage control in terms of house prices. This is not a defeatist perspective, but a realistic one. Even a Labour government that calls itself transformational is not interested in bringing down NZ's horrid median multiples.

So given this, what can we focus on?

1. Ramping up state house building. It needs to be at least 4500 homes per annum, preferably more.

2. My previous idea of the government building affordable housing becomes unrealistic. The focus should always be housing the most needy so efforts and resource go into state house building.

3. Given 2, we should effectively give up on achieving affordable owner occupier housing. Hence let's focus on the private rental sector.

4. Given 3, what do we do to get the private rental sector more functional? Well, we need to keep seeing the high building rates of townhouses and apartments. I believe an important facilitator of that will be the government's National Policy Statement - Urban Development.

5. Given 4, and the futility of achieving affordable owner occupier housing (point 3) we need to think very carefully about reducing investor activity. If we accept the obscene level of house prices, then we can change our view of investors from foe to friend. Under this view, we need investors to keep plowing into the market, buying townhouses and apartments off plans indeed, can we somehow incentivise investors to buy new builds?

And given this, DTI's could be a very bad thing with unintended consequences.

Nice bit of intelligent and workable suggestions Fritz. Don't usually back your missives, but this one is right on the mark. Well done

Thanks Fritz. I am pleased I have provided some food for thought. : )

I think they either need to go full free market (build what you want where you want) or full on socialist regulation (such as a ban on turning existing houses into rentals). At the moment all the regulation is based on helping the entitled not the poor, it’s a phoney free market when it suits.

.

You got anything constructive to offer?

Yvil, you imply there’s no problem with house price inflation? Let’s be clear, rising house prices (mainly land) create no additional wealth, they merely transfer wealth from future landless generations.

It’s not rocket science to reduce land prices, there’s just no political will to roll back the regulations that have created the false scarcity. In no particular order; remove the urban growth boundaries, presumptive right to develop/subdivide, growth infrastructure funded by central government, use tax/rates to disincentivise land banking, compulsory acquisition orders for holdouts, upzone existing housing.

Yes, the solutions to reducing houses prices by taking waste out of the system are obvious to you and me, and I also suspect to the Govt. (in hindsight) but the truth is they have created a 'monster' that they now can't control, even though they pretend they can.

For example, they say the LVR's they will bring in in March are expected to lower price rises by 1 to 2% but don't state what this is of the top of. Is it 1 to 2% less than a 20% increase or a 30% increase?

Also if they know that exactly what amount of LVR increase will take that much of prices, then they should be able to tweak the LVR enough so there is no increase. But of course, they can't do that because they don't have any real control.

They seem to be able to make the big decisions for events outside of their control like COVID, but for events that are of their own making, they have no ability to change, which suggests they don't have any real control.

We need a Jedi Knight but have ended up with Darth Vader and the evil Empire.

In summary Dale you are saying; "We need a Jedi Knight but have ended up with Darth Vader and the evil Empire."

In outcome we have. Right outcome vs wrong outcome, both sides of the same force.

Remember of course that Darth Vader was a Jedi Knight, and while he did come back to the good side at the end, it was too little too late.

For some reason, I can't help but see the Greens as Ewoks. I know I have just insulted one of them, but not sure which one.

Perhaps Governments actually prefer rising house prices, which keeps all the homeowners and landlords happy, and likely to vote them back in.

20% of the population won’t plan ahead for their lives, will have kids, live benefit/pay check to benefit/pay regardless of conditions, and will always need State housing, or accommodation supplements or looking after in many ways.

Is it the Govts responsibility to cater for housing, cars, food, clothing, or are citizens best to provide primarily for themselves and their families?

To me it looks an awful lot like a bubble,

https://www.investopedia.com/articles/stocks/10/5-steps-of-a-bubble.asp

The bubble phase

The bubble phase begins when debt growth is faster than income growth.

This is when debt produces income less than the sum of principal and interest payments. The debt growth becomes unproductive.

Yet rising debt growth still produces strong returns in assets, income, and overall economic growth. The price of financial assets is a function of money and credit spent divided by their quantity.

Even if the debt being produced doesn’t throw off the cash flow to make these debts viable, there’s a tendency to extrapolate the past and assume it’ll be like the future even when the underlying conditions change

Or maybe ‘fundamental value’ is about right taking into account the consumer flight to safety, desire for security in very uncertain times, low interest rates, QE, tax on interest/investments, a generation waking up to house buying at a late age, rental income, - and the thinking that everything else can be taken away or dissolve but a house & garden remains (assuming repayments are possible - but even that was stretched this year with mortgage deferments etc).

Except that happens in every bubble— people think something has changed fundamentally rh justify the prices. And then they learn it hasn’t.

Build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes, build more homes,

Houses are being built at a rate not seen for decades, there is not much ability to build more, faster. We need anti-greed laws, frankly

Yes, why are we making this so complicated?????

#rentcontrolnow.

Done.

No new commissioner needed; no new office to service the new commissioner needed; no new legislation to give the new commissioner a set of new powers needed; no new money needed; no new labour force needed; no new NOTHING needed.

Just regulate the private sector rental market.

I'll say it again: #rentcontrol now

Where has rent control worked? We can’t just force our way to happiness through regulation. This gov was already becoming known as the gov of unintended consequences, rent control would just further it along that path.

What you and others who say such things seem to fail to recognise, is that we have a terrible housing situation for far, far too many people, that is hardly a measure of success. What it is, is more like economic cannibalism.

I don’t fail to recognise that at all. I’ve been constantly bemoaning our housing situation and particularly the monetary system responsible for it.

It depends, "worked for whom" are you asking?

Where have the desired outcomes been achieved without a whole host of unintended consequences is my question.

Rent control is like treating the symptom and not the cause for me.

Here's a good look at various studies from the US;

https://jacobinmag.com/2019/11/rent-control-housing-crisis-affordabilit…

The question is, 'Is rent control to be seen as some sort of Triage, or is it the new normal?'

I note the use of rent controls in locations they mention are in areas where they have restrictive land policies.

If the people really really really want rent controls, they can do it now, without any help from govt.

It is called a nationwide rent strike. It it's not happening, then I'd suggest it's not of sufficient interest.

Yet.

Harre mentions Savage several times, but then avoids advocating the Savage prescription - Reserve Bank credit for state house and infrastructure building. Zero interest, zero debt money direct to the government to invest in assets for the country. If the Reserve Bank can create $128 billion to generate more profit for the banks and rich investors it can do it for the government to build houses etc.

SocialCredit I am not against your policy prescription. I am not in the 'funny money' camp. I think if the RBNZ is printing money then maybe it should be for public capital works rather than given to banks to inflate asset prices. There is certainly a need for a big boost in public capital investment - to fix local authorities infrastructure deficits, to build multi-modal transport infrastructures, and to transform the economy to carbon-zero energy systems. Yet is NZ's economy in such a hole we need to boost the money printing programme? I think our economy is showing more resilience than that.

The main reason I did not discuss Reserve Bank credit is I do not think it is necessary to fix housing, which is the topic of my paper. Austria spends less than 1% of GDP on its social housing programme -yet social housing is a quarter of their new builds. A massive social housing build programme is not as expensive as people think and already NZ is doing half of what Austria is doing. It would not be that expensive for NZ to catch up with the likes of Austria or Singapore

For instance the Housing Commissioner could request the government issues $150,000 capital grants per social house using a competition model like Austria (criteria -economics, environment, architectural/construction quality and social) for the non-profit community housing sector. $1bn a year would produce more than 6000 houses/year. The target could be price-controlled rents that are less than 30% of income for minimum/living wage workers. I am sure this target could be met by the combination of capital grants and better planning regulations that the Housing Commissioner could oversee.

Hi Brendon

Social Credit (the party) did not advocate an increase in money creation but a transfer from the current Reserve Bank/Private Bank partnership to a Reserve Bank/ Govt partnership. The Private Banks have proven to be poor partners in this Nations' money supply with very negative results for a very large proportion of New Zealanders; change is needed in this space.

Re the housing shortage, wasn't there a report that there were enough empty houses to solve it? Maybe a strong Govt could amend the public works act so houses that have been empty a for set time could be subject to a compulsory purchase order by the State Housing Authority?

Nope that is a myth - probably concerned trolling from those who want to distract the conversation away from genuine solutions...

MMT gives us a true description of how our governments finances operate and it tells us that all government spending results in the creation of new money and that taxation and borrowing is something that happens afterwards. There is a great deal of information that can be found on the internet to substantiate this.

Economist Prof Bill Mitchell's blog is a good place to start. http://bilbo.economicoutlook.net/blog/

"Michael Cullen sees an opportunity for monetary policy reform “in the current situation to make a quantum leap forward in dealing with some of our needs, which require large amounts of capital.” The primary needs are a big increase in the level of housing construction and infrastructure development, and a large investment in transforming the economy to meet New Zealand’s climate change commitments. There is a strong echo of the First Labour government in this policy prescription."

YAY! Someone who finally get's it. Printing $128b and giving it to the already wealthy is stupidity of the highest order, but it is likely what the RBNZ will do. If the gubbmint (i.e. GR and Jacinda) had any courage, they would capture that money and instead put it into the biggest house building and construction package ever created.

Instead they meekly claim "but the RBNZ is independent... we can't do anything" etc etc abrogating their responsibilities as LEADERS and instead being the lapdog of property investors. Cowards who appear to just be in politics for the power instead of doing the best they can for the country.

Why do we need all these complex and bureaucratic ideas to fix housing? Stop banks from creating money, get rid of inflation targeting and make it easier to build. As an additional bonus, money would then flow to actually productive parts of the economy.

"Renting in New Zealand is bad - for low-income groups it is the most unaffordable in the OECD - as my previous paper published on interest.co.nz showed."

The writer property rams home how poorly New Zealand has run housing for decades, and properly identifies that independent bodies are needed to invent, prescribe, and administrate long term solutions, however, I think there are other solutions. Like PM Savage in the United States President Franklin Roosevelt likewise dealt to housing in the 1930's--the difference is FDR's solutions are still working and achieving target-(albeit philandering Bill Clinton just about destroyed the FDR institutions when in the late '90's his Administration pushed the banks to lend more to the inner cities. The regulations allowing more lending to inner city people of colour got picked up by the slick Wall Streeters and used to create "liar loans". The rest was history as it was central to the Global Financial Crisis when all of these borrowers with no income to support their mortgages got caught out-but that has long been sorted by a return to strict lending criteria, so much so that as of the end of Q2, 2019, Fannie Mae had made $181.4 billion in dividend payments to Treasury, and Freddie Mac had made $119.7 billion, according to earnings releases.)

Therefore what New Zealand needs in 2021 are principally these policy changes and new institutions dedicated to enabling change:

1) Use funds from the Cullen Fund to create a NZ version of Fannie Mae/ Freddie Mac. 1st time home buyers and anyone buying below a threshold tied to Median Price per City or Region are allowed to buy Mortgage Insurance to drop Down Payments down to an affordable 5% of Purchase Price. In the US this is only a 1% addition to borrowing rates-thus they borrow at 3% Interest+1% Mort Insurance=4% total cost. Once 20% equity is achieved and proved by an updated Valuation the 1% surcharge drops away. This protects the Banks and insures a social goal of getting 1st Home Buyers on the property ladder virtually as soon as young people want to.

2) Immediately increase House Stock for 1st Home buyers over the mid term by a change in both Taxation and Rates for Property Investors. Over 5 years move Rates from Residential to Commercial to increase the cost and lower the reward to Property Investors outbidding 1st Home Buyers for the lower quartile in each Local Territorial Authority. While rents would rise give Renters below certain Income thresholds on a sliding scale Credits for their "homestead". Every family should have a homestead rate, but wouldn't apply to their second plus homes. Thus penalize the Investor to get them out of the Single Family House market and into other forms of investments, while using this increased taxation to subsidize the worthy renters.

3) Impose a Capital Gains tax on all property sales, save for the "Homestead".

4) Create an Independent non elected long term planning body for each City or Region that would insure land is available with infrastructure in place when the time is needed for that land. eg Up in Dairy Flats north of Albany over to Helensville are thousands of Life Style Blocks on former subdivided farms. That would allow Auckland City to Rezone that land Residential when the time comes, and assess the cost of infrastructure brought to that land to the current property owners. The Planning Body will signal long in advance that this is there plan. Most land bankers or other rural owners will fold their cards and sell to property developers who respond to the market and build the houses needed in a timely manner. Sure not nice-but wasn't Flat Bush agricultural not so many decades ago? Constraints on Residential land expansion create monopoly like conditions for current owners of land. Cities need to expand to offer their young affordable opportunities for housing, and that should be a social contract to the young.

5) Create Municipal Bonds for the purpose of funding local infrastructure. Basically those paying the top tax rate for individuals are the buyers because they pay no tax on the interest received, and bond funding is usually over prescribed (meaning lower interest rates for councils) plus because it raised locally from taxpayers rather than overseas banks there is no exchange rate risk cost built into the interest rate.

Think Big projects to be sure-but never more needed than now.

I like this article in that there is a good attempt to define policy that would work.

But its too late. Describing something as "too big to fail" is just a way of saying "too big to fix" or "too hard to control".

Its just a nice way of the govt saying they can't or won't do anything substantial to step in.

Which is exactly why it will fail.

X

More public housing will simply transfer accommodation supplement to a subsidy of rents in public housing so no net cost difference just an increase in the public housing empire/debt. Housing is the main criteria Banks use in providing finance to small business so understandable that Govt/Banks would not want to see large decreases in values. Working from home will and is having an effect on commercial property values especially office space and if Covid continues to hinder Travel and social activities business failures will be followed by property value reductions as seen in the US were the second largest Mall owner CBL is in liquidation due to rent arrears also affecting the largest Mall owner. Covid has and is creating a seismic shift in economic activity that seems unaddressed and not understood especially by the current govt. Failure of the 3 Gorges Dam if it happens will be a catastrophe on a scale never seen before and our MSM have never mentioned it !!??.

I support Policy's 2&3 as for how would it work - it wont , its pie in the sky and politicians who implement it will eat humble pie with cyanide seasoning for decades.

So in summary based on your 3 posts. You agree with 2 out of the 4 policies and think the other 2 will not work because government departments are useless?

The Jedi knights are clearly duo RBNZ & govt.; (remember as JA/Lab stated, it's all about the 'supply')

Govt: Removal of bright line test is a must, allows rental increases to 4x/yr max., create new housing agency PR, more permanent flexi-wage subsidy, FHB subsidy PR, increase salary/wages to catch up with the rising cost.

RBNZ: Keep the lid on that LVR, DTI, TD dep guarantee, Bank CAR, more QE/LSAP, negative OCR soon then doubling the effort but more focus FLP into housing activities. The faster & bigger stimulus, the quicker the...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.