By Rodney Dickens

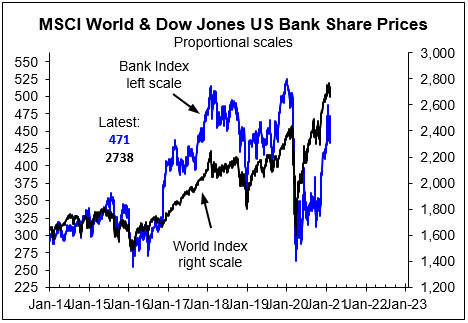

Contrary to the huge surge in business failures and personal bankruptcies that was expected globally as a result of Covid-19, rescue packages have offset the fallout - to the extent in some countries that business failures and personal bankruptcies have fallen below pre-Covid-19 levels. Reflecting this, US bank share prices – a gauge of the market’s assessment of the likelihood of US failures – have belatedly followed the surge in global share prices.

Massive actions by central banks and governments and super-low interest rates have saved the world from a financial crisis, but in doing so have increased the likelihood of a future crisis. The surge in global debt is fine while interest rates remain low, but as global GDP recovers from Covid-19, interest rates in most countries will increase. A W-shaped path is quite possible, but it is much too early to relax about global threats

Rescue packages have offset the Covid-19 fallout and to the extent that in some countries, business and personal failures have fallen

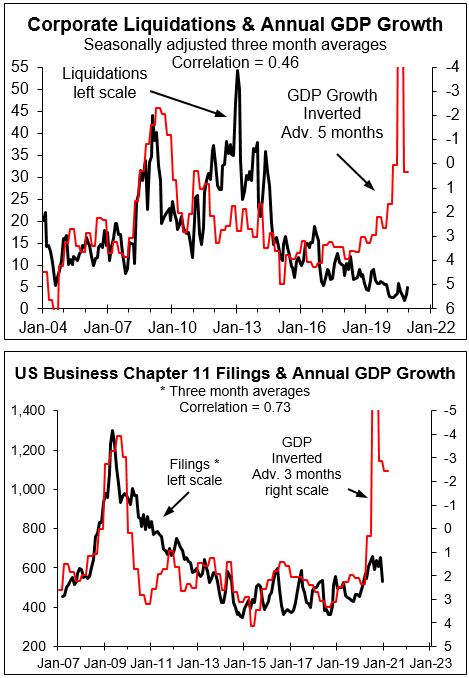

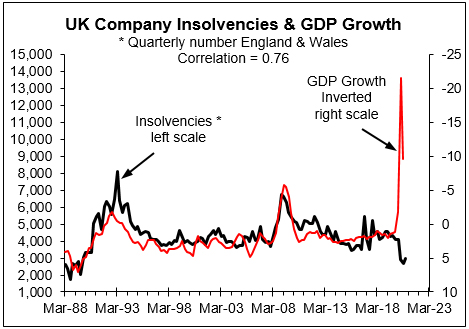

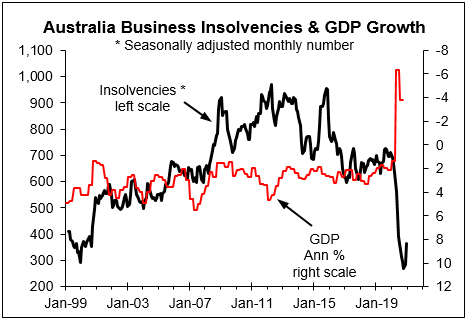

The four chart that follow are repeated from the June 2020 Briefing that looked at the links between GDP growth and business failures for NZ, the US, the UK and Australia. The correlations in the charts are the pre-Covid-19 ones, but for all four cases they will have fallen as a result of the Covid-19 recessions not resulting in a surge in the numbers of failures. In the UK and Australia, the rescue packages have been so effective the numbers of business insolvencies have fallen. The link in the adjacent chart wasn’t at all close in Australia pre-Covid-19 (top right chart).

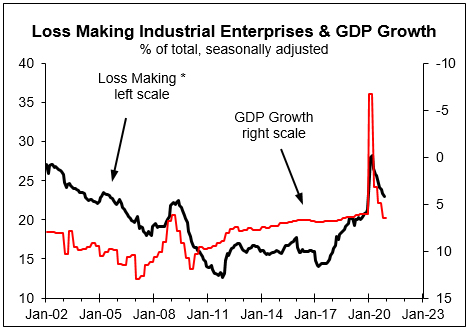

However, in China the Covid-19 recession did result in a spike in the per cent of industrial enterprise that lost money, while the recover in GDP has resulted in a fall in the percentage (next chart). To the extent the rescue packages resulted in fewer failures in some of the countries than would have been the case if it wasn’t for Covid-19, there could be a catchup in the number of failures as the rescue measures are taken away because the measures have kept some firms solvent when they probably shouldn’t have.

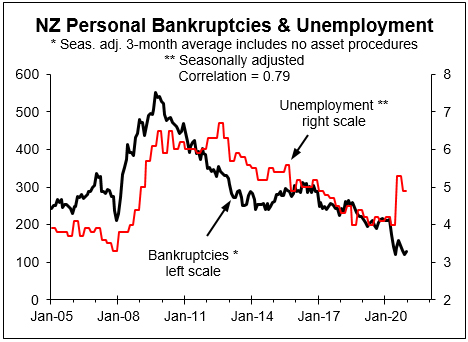

It is even more the case with personal bankruptcies and insolvencies in that rather than increasing as a result of rising unemployment rates, they have fallen as a result of the massive rescue efforts (see the next four charts; the correlations haven’t been updated).

Reflecting fading concern about fallout from business failures and bankruptcies, the US bank share price index has surged since late-2020 (next chart).

The experience with busines failures and personal bankruptcies has been dramatically different to what was generally expected after the first global wave of Covid-19. This link is to a video that painted a dire outlook for US failures and bankruptcies; it even suggested rescue efforts probably wouldn’t stop a surge. The surge in US bank share prices since November is an indication of when views started to change on how much Covid-19 would cause failures.

Super low interest rates and aggressive actions by central banks and governments to the rescue, but it has come at a massive cost that poses a huge threat to the future

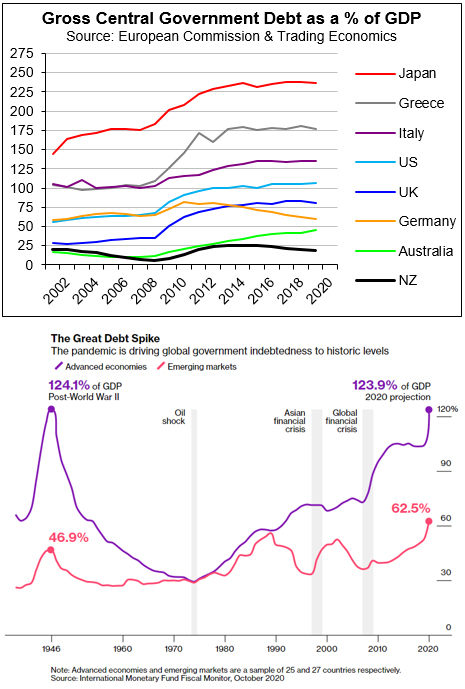

High debt levels were a concern in the big countries even before Covid-19 (the first chart below is only updated to calendar 2019). Global debt levels surged last year (second chart below and link that follows to the article titled “The Covid-19 Pandemic Has Added $19.5 Trillion to Global Debt”). Global debt as a % of GDP is approaching post WWII highs for developed countries and has exceeded it for emerging ones.

Source: https://www.bloomberg.com/graphics/2021-coronavirus-global-debt/

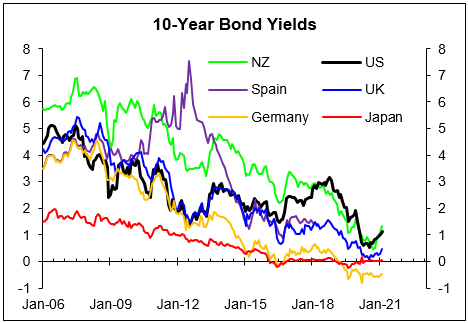

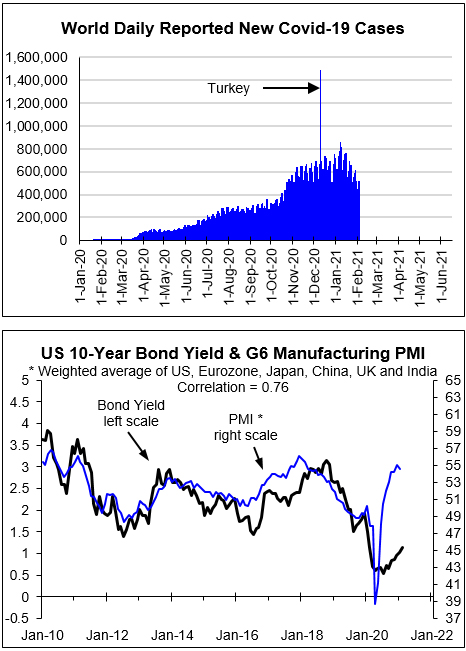

Super-low interest rates have come to the rescue so the cost to governments of the new debt is extremely low and negative in the case of Germany, while older debt that is maturing is being replaced by lower-cost new debt. This is keeping the cost of government debt down; but interest rates are starting to rise in response to the vaccine success (chart below for a selection of countries including NZ).

Concern about the economic fallout from the second and third waves of CV (chart below) has limited the increase in the US 10-year yield vs. the rebound is a leading indicator of global growth and trade (second chart below). However, if vaccines work reasonably well and global GDP heads back towards the path it was on pre-Covid-19, the biggest surprise relative to what bank economists predict will be rising interest rates that may trigger a W-shaped profile.

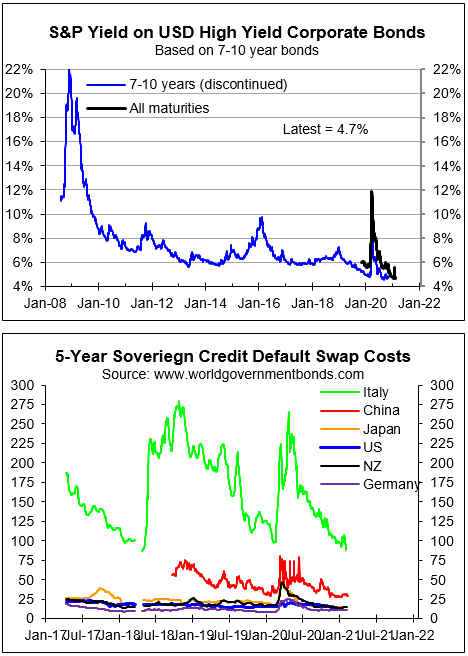

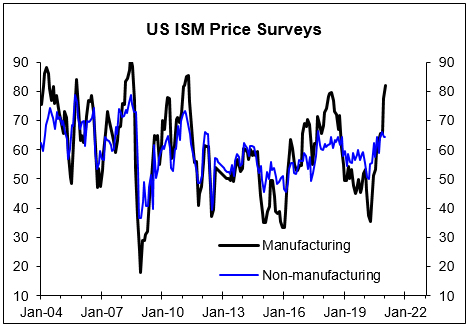

The starting point is calm risk markets after they were spoked somewhat by the first wave of Covid-19 (the two charts below). A global financial crisis is clearly not imminent, but the government and central bank responses to the Covid-19 crisis have added to what was already a huge debt problem and therefore must increase the risk of a debt-driven crisis eventually. In my assessment, the thing that may trigger a crisis is higher interest rates. The initial source of higher rates is the market reversing at least part of the Covid-19 related fall, but a by-product of Covid-19 for could be higher inflation as suggested by some gauges (see the third chart below).

On the one hand, the rescue efforts have saved us from a financial crisis, but on the other they have added to the threat and just kicked it down the road.

This article is here with permission.

47 Comments

Mass inequity will be the next global talking point / disaster...and we all know who to point the finger at.

Richard Nixon? When he abandoned the Gold Standard to finance the debts associated with the Vietnam War?

"President Nixon promised that the dollar would retain its full value. It only is worth about 15 cents today of what it was worth in 1971."

But hey. More debt is better, right?!

("Always blame the dead guy!")

Woodrow Wilson for flogging off the US federal reserve?

All the amateur property investors will lock in 5yr rates this year. And in 5yrs time they may face 6% 1yr rates. And then let the natural cycle of economic ups and downs kick in. Too much artificial stimulation has created an inevitably huge future recession by allowing inefficient businesses and overhyped get rich quick investments to become mainstream. See you all in 5 years!

Property investors if they are smart will pay off 20% of their loans in that time.

Yip, and the 'smarterer'? will cash some of the portfolios, trick that bright line test, trick the IRD then move the fund to OZ master, split it with max 250k (as per TD guarantee), spread the eggs means just that too.. don't put it all in NZ.

Always very interested to read about 'debt levels'. I have always been pretty old school in that I don't like to carry debt and aim to pay off debt ASAP. I have been criticized heavily for this view by people saying that with rates so low I am "dumb" to not take advantage i.e. buy an investment property(s). It annoys me a bit as it is often said in a very condescending way and I feel it is probably more to try to convince themselves of how brilliant they are with their finances (not)!

Well as it turns out I am very very glad I am the way I am. Due to a combination of things out of my control I am currently facing redundancy and the peace of mind knowing that we have no debt, will have a roof over our heads and can pay the bills whatever happens is great.

The debt levels that some people carry and that we have 'normalized' over recent years is beyond belief to me, but then I am different I guess, I am happy with what I have and don't feel like I need 5 investment property's to be 'successful'.

I will be very interested to see the outcome with even a modest rise in interest rates, I imagine there will be a lot of people losing sleep!

Well done Smudge. Sorry to hear about your change in circumstances but as they say - he who laughs last... You've taken a measured approach which has stood you in good stead - debt free

Awesome!! I feel exactly the same way. People always saying the same to us. You are mortgage free why don’t you go buy some properties so you can live well when you retire, get ahead blah blah blah. Get ahead of who? All the have not’s who just missed out on one more house due to greed? Hard no from me. Maybe if we save enough we will build a rental property as that is the only way I could morally do it.

Smudge... sounds like you have a sensible take on things. A good number of investors are of the opinion that there is no risk associated with NZ property investment and that things are certain to continue the same way as they have done for the last 40 years forever, regardless of the warning signs. There are many things that may cause you to have the last laugh, high interest rates being just one example.

"A good number of investors are of the opinion that there is no risk associated with NZ property investment"- Really Karl, who died and made you the spokesman for NZs property investors??

Hook... you just have to pay attention to what most of them post on here and listen when communicating with others. If I really need to dumb it down for you here goes.

On the basis of what I read on forums such as interest.co and from what I hear when discussing the property market with investors a good number of them are of the (completely asinine) opinion that there is no risk associated with NZ property investment. In recent years the number of investors who speak on the future with almost total certainty has increased noticeably ( IMO not coincidentally) in tandem with the rise of pornographic-like publications such as One Roof.

Some of us decided that things were getting a bit risky with property a couple of years ago and made regretful decisions though. I think to be successful you need to be positive which means believing "there is no risk associated with NZ property investment" or there is a risk but it's a risk worth taking which is closer to the truth. It seems a lot less risky than many other things. I wouldn't call it asinine. Many people never achieved even a modicum of success because everything seemed too risky. It was risky but it was also risky to do nothing. A fact they didn't consider deeply enough.

Understood but keep in mind that there are more investment options than just property. Yes they still carry an element of risk also but the are still options and are potentially better for our country's future in respect to cost of living, supporting business, narrowing the haves/have nots gap etc. and that is appealing for some people.

You can invest successfully without borrowing $800,000.

Zachary.... yes of course having SOME of your wealth in property is an acceptable risk. But to have almost all your wealth tied up in property is unacceptably risky to any sensible and rational person. Also using leverage increases risk hugely. Personally I recklessly gambled by putting all my money in property and leveraging massively, even gambling my parents home as security. I was young, stupid, ignorant of risk and lacking in knowledge of investment but good luck was my saviour.

Todays investors who also choose to (over) leverage and refuse to diversify (for the same reasons I did) may be lucky as well. Then again there is a fair chance they won't be. As I said, IMO, believing there is no risk in NZ property is completely asinine.

I have always maintained this view on debt. FHBer 3.5 years ago, over that time we've dropped our mortgage payment schedule from 25 years to 13 years. Been told "oh you should leverage up to 80% for a rental/new house". I'd rather keep the debt low while making higher payment amounts.

$500k @ 2.55% over 25 years = $176k in interest.

Consecutive $300k @ 2.55% over 13 years + $200k @ 2.55% over 13 years = $87k in total interest on $500k borrowings over 26 years.

I can't see interest rates rising at the bank unless the government comes up with another accommodation supplement - like 'mortgage supplement'.

Rosentein

What?

Yea you know - the government will say "If your mortgage rate rises we will cover the difference in payments" I mean why not? We already subsidise leveraged mortgage owners through other means - why not be direct about it?

Either that, or the Government will step in providing state advances lending of 3% p.a. for people who were first home buyers in the last 5 years and still own only 1 house.

There you go. You see? We gotta start thinking Soviet Union about this

There will need to be a sharp rise in interest rates, this is pretty clear to anybody who is realistic enough. This might become very interesting for housing speculators.

However I do not think that this is going to happen in NZ (and probably in much of the rest of the world too, I guess): there will definitely be interest rates rises (and sooner than many people may think), but I don't see the OCR going much over 1.5% by end of next year.

The simple reason is that Increases bigger than that may cause a bursting of the NZ housing Ponzi, which is already in an extremely inflated and fragile situation, and this is something which the Government will not be keen to see, for clear political reasons.

Forturn

Why just property speculators?

An increase of 1.25% in OCR is applied to mortgage interest rates then even FHB with a $700k mortgage are going to see $336 per fortnight increase in their mortgage payments.

Need to start paying down debt NOW.

You are right, but unfortunately like in all Ponzi schemes there will be innocent victims who bought late into the scheme without being aware of the risks. Maybe the Government will come up with some form of support for this category of people if things get really serious, who knows.

I agree.

For that reason I think it is unlikely that the ocr will be higher than 1% by end of 2022.

In fact I predict the ocr will be negative by end of 2022, as I think a financial crisis will arrive by then.

Careful Fritz, you are making a prediction in a short enough timeframe to be held accountable. You are breaking the Prediction Brotherhood rules.

Haha!

Hold me to it! I have called it for a year or so, I am not going to chicken out now!

Financial crises usually come around every 10 years or so, we are overdue...

Yes, the trend is your friend on this one.

Haha.. Fritz, the all seeing and monetary policy sage has spoken. Bow down and drink from his vessel all ye minions, and be proud of the opportunity to partake of his wisdom.

Or.. what a crock

Nice, man. Such a charming individual.

Why don't you go back to your bigoted, country bumpkin's man cave now...

Just looking at someone running around naked.. most entertaining. How's the sunburn going on those buttcheeks??

BTW.. drag your beltway urban butt out into the heartland - you might learn something.

I thought you would be out in your imaginary 40ft boat Hook instead of trolling on this site?

Not long before it will spiral out of control. 1% ocr end of this year. House prices going up more than 500 bucks a day. The ocr is probably not our biggest concern, people who really cannot afford living anymore is the worry. The FHB who think they missed out, will not feel so bad after all.

Fritz,

So, you expect to see a 'financial crisis' before the end of next year. That's easy to say, but from where? To have any credibility, you need to provide some analysis-how will it play emerge? Without that, you are just another bag of wind.

Even? if OCR must increase, do you think govt. & rbnz will just sit still?: firstly, more QE by rbnz, into provision by govt hands to administer sudden good spike of charity, subsidies; accommodation, wages - then the real salary/wages active earners massive appreciation review (whoaa to that). When there's a will there's a way. But sadly, this usually come at the cost of world/public 'confidence' - It is always 'possible' to defer a bad news of terminal illness just for the sake of making everyone happy, new method of treatment, new clinicians, new hospital, new this and that but eventually though it's either delay=time=cost more to it, or just a simple death.

Will we even be living in a positive rate environment in a decade? My guess the prevailing equivalent measure will be the rate at which Reserve Banks are purchasing assets as %GDP.

In New Zealand we see an aging population, declining productivity, increasing levels of state and personal debt, perpetually low levels of investment in infrastructure and increasing sales taxes. There is no reason intrinsic to New Zealands economy to expect interest rates to remain positive over the medium term.

How about inflation? There are many ways by which inflation can enter the system, and if it happens the RBNZ is mandated to control its levels through the appropriate monetary settings.

By the way it is factually untrue that productivity in NZ is declining: see https://www.stats.govt.nz/information-releases/productivity-statistics-…. Yes, the increase rate in productivity has been declining in general (but not always and not in all sectors), but not productivity itself.

Moreover, infrastructure spend in NZ has been increasing since 1992 (although NZ still has to do some significant catch up work in this area): https://www.infometrics.co.nz/new-zealand-infrastructure-spending-lags-….

Current emergency monetary settings are creating huge distortions, and it is just a matter of time before the RBNZ will be forced to bring these settings to more neutral, normal levels.

Yeah, Peter Schiff is calling Stagflation: https://www.youtube.com/watch?v=UvjIqwlqfng

He sees inflationary pressure and upward pressure on rates building.

This is the reason I haven't piled into the Ponzi - I just don't have the courage to commit a hard saved deposit and to a 30 year, 650k mortgage for an overvalued shitbox when these risks are in plain sight. I will take my chances on the side-lines.

I agree. Your "shitbox" comment is spot on - I am amazed not by the prices but what you get for the price.

I listened to the fellow on your link and he makes some good points. However the long term trajectory is lower productivity and lower rates unfortunately. It may be there is some sort of recovery but the scale of debt liabilities outstanding is such that a very small change in retail rates severely crimps consumers spending.

Thanks, good points and I enjoyed your response. I think StatsNZ are only referring to only Labour Productivity. Typically the measure I would use would be would use GDP per hour worked or per capita, as is preferred by the OECD, EU etc. Unfortunately peak GDP per hour worked was 2012 and peak per Capita was 2014. The link you've provided appears to be in agreement with my comment about permanently low per capita infrastructure spending in New Zealand.

Regarding your last point often Reserve Banks have talked about normalising rates over the past two decades but I think we have to be realistic. The "productivity puzzle" still exists and measures to promote credit creation do not appear to be helping, in fact they may be at the root of the problem according to some. I think there needs to be some moderation of future interest rate expectations by Reserve Banks, if a situation persists it is no longer a rescue.

Aging population, declining productivity, increasing debt. What about new zealands golden ticket to counter all that.......immigration!

That increases gross GDP measures but as the measure of productivity is per capita that's less certain. In many ways you might argue that New Zealand's persistent low productivity may be partly due to poor immigration policies depressing wages and removing the economic incentive to invest.

With one of the highest rates of foreign born citizens in the OECD you might argue New Zealand kind of proves that immigration isn't a silver bullet.

Yes with our Covid free status there would be unlimited people pouring in here if we let them in.

https://www.stuff.co.nz/business/opinion-analysis/300223000/property-in…

Eventually, the debt have to be repaid. But why bother? leave it to next generation, if NZ need more just print it out, austerity to pay it down? no way, immigration is the answer. Heaps of world Billionaire, will seek refuge in NZ, move here? bring capital? you're welcome. Just support those golden NZ currency (housing that is), which going to be supported this 2021-25 by Insurance, climate & carbon neutral announced by dear leader - this all has been choreographed - the phantom funding for it, wait.. wait.. more massive QE/FLP.

Government (RBNZ) is suppressing the 10 year yield rate using QE (it’s real purpose). And Japan has shown that sovereign states can do that for years. Govt ability to anchor interest rates and inflation using tools at its disposal is underestimated.

The indicators of primary concern should be household and business debt - and our household figures are grim. We need an economy and society that helps people earn and pay down debt by being productive and contributing to the country - and that means admitting that an economy based on boosting house prices, virtual monopolies with huge profits, and govt subsidised rent and wages is an unmitigated disaster.

Also worth noting that Govt debt is irrelevant for a sovereign country that can set the interest rate and control the prices of its bonds in the secondary market (or choose not to issue them at all). Also worth noting that a lot of sovereign states owe a chunk of their ‘debt’ to the banks that they own. When your left pocket owes your right pocket some money, I wouldn’t call that ‘debt’.

Perhaps the author has not been listening to Jerome Powell, who has made it clear that interest rates are going to stay for much longer. Will there be a day of reckoning? Perhaps, but not yet.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.