By Terry Baucher*

It would be fair to say that the shockwaves from Tuesday's announcements are still reverberating around investors and analysts and tax professionals.

The increase in the bright-line test period to 10 years was widely anticipated. But the move to completely eliminate, over time, interest deductions for residential property investors was a complete shock and has caused quite a considerable amount of commentary.

I would say at this point, I think several people have been extremely ill guided in some of the comments they have made online. Inland Revenue monitors social media, and some of the comments I've seen by property investors, understandably, given the shock and the implications for them, upset about what has happened and probably reacting somewhat intemperately, may come back to haunt them.

For example, saying that rent doesn't cover the cost of a mortgage and other costs, as one investor said in print, is an open invitation to Inland Revenue to raise questions as to why if that was the case, that person had purchased property. It opens the door for Inland Revenue to then go on and say, “Well, you must have acquired that with a purpose or intent of sale.” Which if that is argued bypasses the bright-line test. It doesn't matter how long you've held it in those in those circumstances, any gain will be taxable.

Now, that's an extreme response Inland Revenue could take. But as I said, I think some people might, to borrow a phrase, that my mother would use “Cool their heels a wee bit” and sit back and reflect on the implications of what's going on, rather than rushing to social media and excitedly make a comment that they may regret at a later date.

But still, there are good reasons, for people to respond passionately given its surprise. Under the Generic Tax Policy Process, changes like this are usually signalled in advance. The Government issues consultation papers, and there's a back and forth between industry specialists and Inland Revenue and Treasury on the implications of these proposals. That isn't going to happen here.

In the course of the group call made to tax agents and tax advisors before the announcement, Inland Revenue made it clear that there would be no consultation about the bright-line test period and on restricting interest deduction issue. Inland Revenue would, however, consult around a key point that is emerging. What is the definition of “new builds”?

So these proposals are all outside the normal process and has understandably drawn criticism along the lines of “Can the Government do that?” They can. And in many ways, it's surprising this doesn't happen more often in tax policy.

Governments around the world will move very quickly when it suits them or when they feel that they need to close off loopholes. Coming from Britain, Budgets were always full of surprises and policy announcements. Sometimes there might be some leaks ahead of the announcement, but generally speaking, every Budget always contained a few surprises.

Now, the other thing attracting criticism is how the Government has rather deliberately phrased the move against interest deductions as closing a loophole. As a few people have pointed out, this is not correct. The position is that interest borrowed to derive gross income, such as rental income is deductible.

But what has become apparent in the residential property investment market is that there's two parts of the economic return. There is the rental and then there's the capital gain.

And the issue was that many leveraged investors who are most affected was that they were getting a full interest deduction but would only be taxed on part of the economic return. That is the rental income. All things being equal the capital gain would not be taxed unless the bright-line test applied. Restricting interest deductions in that context is actually consistent with the general income tax rule that an expense is only deductible to the extent it's incurred in deriving gross income.

The current treatment is therefore an anomaly. What the Government has done is closed off an anomalous position, but only in respect of a certain group of investors, which again leads to outrage about the treatment. But that group is probably losing that argument about it not being a loophole, because to borrow a political phrase, “Explaining is losing” particularly if as in this instance a very technical argument applies.

Always at risk

But the overall point should be kept in mind, and this has happened before with the removal of the loss attributing qualifying company regime, tax preferred investments or rules that give a tax advantage will always be scrutinised by government. They are always therefore at risk of being abruptly closed off.

So, if you built an economic business model around relying on that, you are actually making yourself very vulnerable to a move like this.

Work in progress?

Moving on, one other point has emerged, which is surprising, and in the context of the General Tax Policy Process, concerning, is that it appears no details of the advice that was given by Treasury and Inland Revenue on the interest deduction move has not been made publicly available.

This is surprising because it implies that this policy is still being worked out. As a result of that the fiscal impact is not clear.

If the interest deductions are restricted completely, that means the Government's tax take will increase. And me and my fellow tax advisors have been crunching the numbers for our clients who will be affected. And we are giving them projections as to the likely additional amount of tax that would be payable. And that's potentially could be quite significant, although it could be that property investors deleverage as a result, which may have a wider economic impact.

This whole policy, in fact, is a good example of something that came up at a seminar last night, which I will talk about a little later, the law of unintended consequences. This is something that hasn't been done before and the consequences are still being worked out. One or two things I think that come to mind is we might see investors make more use of company structures because the corporate income tax rate at 28% is less than the 33% for property held in trust or possible 39% if properties are held individually.

I also wonder whether the Government should be looking carefully at the question of is the loss ring-fencing rule required any longer? One of the reasons that rule was introduced was the ability of people to leverage and get deductions for interest. But then, since interest deductions often represented the biggest single cost at a time when interest rates were higher, if they ran into losses, investors were then able to offset those losses against their other income.

Now, that loophole was closed off with effect from 1st April 2019. But the question remains now, given that the ability to leverage, which was the main issue around the need for loss ring-fencing, has been restricted, do we need the lost ring-fencing rules?

The other thing is, and this is something I think the Government will need to address as it was a stumbling block for the introduction of a capital gains tax, is that any gains will be taxed at a person's marginal rate. In a company the rate is 28%, but for an individual from 1st April, it could be 39%. So, there's a lot of unintended consequences and it's understandable to see why investors feel rather picked on at the moment.

There’s interesting commentary from the Bank of New Zealand which started its newsletter on this issue by saying that “The New Zealand government is dead set on containing soaring house prices. It has been saying so for some time now and prices have just kept soaring. So it should come as no surprise that their patience has now been exhausted and a full attack on prices is now under way.”

BNZ’s view is “Watch this space.” There will be a lot of arguments around the fall-out of this proposal.

The interest rate restriction rules, as an article in the Herald points out, are actually more restrictive than a similar measure introduced in the UK. What the British did was restrict the rate of the tax relief to the basic rate of tax, roughly 20%. These measures go completely further.

I feel that using something completely unknown whilst a shock to the system, and in line with what BNZ is saying the Government is determined to try and do, is leading the Government into untested waters.

And the alternative might have been to use an existing set of rules, the thin capitalisation rules, which might have achieved much the same sort of objective. But there will be a lot of fallout on this, and it'll be interesting to see whether there is some tinkering around the edges of these measures.

The bright line test

On the bright-line test itself, it's been extended two to 10 years. And there's going to be a lot of questions on this about the impact of that, but particularly for people who are in the middle of settling on properties.

Extending the bright-line test period to 10 years has now been passed into law as part of a tax bill. But it has also provided some commentary with useful examples of what happens with sale & purchases underway at the time the proposals were announced.

Basically, if an offer was made before the announcement on 23rd March and accepted before 27th March, then the five-year test would apply. But if, an offer was made on 21st March, but the seller accepted the offer and signed the sale & purchase agreement on 27th March, then the extended 10-year period would apply.

Another of the examples given was of a verbal acceptance before 27th March but the agreement is not actually signed until 27th March. Then the 10-year rule will apply.

So people will have been pressured to making quick adjustments right now to finalise the sale and purchase agreements. Not ideal, and there will be a few people who have been caught on the wrong side of the new 10-year period as a result.

In relation to conditional offers, for example, someone submitted an offer on 18th March, which is accepted, and the agreement was signed prior to 27th March, conditional on finance. If the offer goes unconditional after 27th March, in this case, the 5-year rule would apply. Alternatively, there’s a change in the agreed purchase price which happens after 27th March, the 5-year rule would be applicable.

There'll be plenty more commentary on this going forward. And it will be interesting to see the commentary in relation to the question of what expenditure becomes deductible as a result of a sale becoming taxable. We don't know yet if interest expenditure, which has been disallowed, will then become deductible if a property is sold and it's taxable under the bright-line test or any other measure. The implication is it should be. But we are we're going to have to wait till May when consultation on this will arrive.

The future of tax

Moving on to an interesting bit of fun I had last night with some colleagues. The New Zealand Centre for Law and Business ran an event where myself, Paul Dunne of EY and Geof Nightingale of PWC where part of a panel.

We were asked four questions around the future of tax. Do we need more tax? Can tax help the runaway residential property market? Will changing demographics result in a changing tax mix? And reducing taxes on the wealthy is this a discredited theory? And if so, what are the implications for that?

This whole thing would be a worthwhile podcast in itself, but it was interesting to see how Paul, who was a member of the 2010 Victoria University Tax Working Group, and Geof, who was a member of that same 2010 tax working group and the recent Sir Michael Cullen-chaired group were mostly in agreement with the need for a comprehensive capital gains tax or rather better designed set of rules around that.

I think the discussion is still there as to whether we need a comprehensive capital gains tax or should it be limited to a particularly troublesome asset class at the moment, property. All of the members of the 2018 Tax Working Group agreed with increasing capital taxes on property. And you'll note, by the way, some of the discussions that come out about the Government's bright-line test period, with Treasury suggesting a 20-year period with no exemption for “new builds”.

By the way, as I said we don't yet know what the definition of “new builds” will be. We're going to have to wait and see. And on that point, Paul and Geof both made very pertinent points that the law of unintended consequences is very applicable here. They have clients who are involved in property syndicates who were in the process of converting commercial property into residential property. The question now is, are these “new builds”? They don't know. So, there may be a pause while everyone waits to find out. What does that mean? No-one is going to commit millions of dollars to a project with an unknown tax outcome. So that was one theme of our discussions.

Do we need more tax? The view was that at roughly 30% of GDP, we should be OK. All three of us were in agreement that the ratio of government debt to GDP was not an issue, but we were all not so enamoured of high private debt as we see that as more concerning. So we had an interesting discussion and hopefully I can make the video recording available in due course.

Error correction

And finally, last week, I talked about charging interest at the prescribed rate of interest on overdrawn current accounts. I mentioned that from 1st April 2021 that rate was going to increase from 4.5% to 5.77%.

Well, another of my listeners from Inland Revenue has been in touch and thanked me for drawing their attention to this. It turns out that was a transcription error in their website and that 5.77% rate is incorrect. It will in fact remain at 4.5% going forward. So, thank you Rowan, for getting in touch. And thank you again to all my listeners and readers at Inland Revenue.

Well, that’s it for today, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week Ka kite āno!

*Terry Baucher is director of tax advisory firm Baucher Consulting.

104 Comments

'changes like this are usually signalled in advance'

Houses don't usually go up a hundred grand in a month...

"Restricting interest deductions in that context is actually consistent with the general income tax rule that an expense is only deductible to the extent it's incurred in deriving gross income." Thank you for clearing that up. Another hint, business can make next to nothing or even run at a loss and expect someone to buy it for more than the seller paid for it. Apart from ponzi schemers selling to muggins. Property investment is not a viable business unless the numbers stack up, and maybe they do for someone but those will have debt kept at a reasonable level. The real intention for many investors is clear.. Coast along and make huge gains. They'd better watch out, IR have minions monitoring social media just as police do

"Coast along and make huge gains' - this is the very definition of parasitic - extracting wealth from society without contributing to the creation/expansion of its wealth.

The argument has been that because Landlords are businesses and interest is a genuine business expense therefore like other businesses they should be able to claim. It's obvious there are plenty of landlords that are barely running at a profit thanks to deductibility, so they're well overleveraged. This is a deliberate exploitative business decision, which is probably where the idea of a "loophole" comes into it. Keeping insolvent companies alive (Landlords) through the various tax rebates while they wait for capital gains to grow, which is not what the system was initially designed to do.

It's not the business limb of the deductibility criteria that most small landlords would have claimed interest deductions under, rather the limb that allows expenses (e.g. interest) deducted when incurred in deriving income (e.g. rent). The law says "income " not profit (see https://www.legislation.govt.nz/act/public/2007/0097/latest/DLM1513555…).

If renting is not a business or an income earning activity then you would not expect the rent charged to be taxed. As rent continues to be subject to tax without the corresponding deductions normally permitted for incurred costs the new law is clearly focussed on punishing investors by IR having its cake (i.e. taxing rent) and eating it too (i.e. no deduction for costs incurred in deriving that rent).

These changes are to effect social change, there is no tax policy basis that can justify the new law.

Perhaps the tax policy needs updating. Could call it ponzi economy limb. So the whole of NZ is not labouring to enable ponzi participants to make out like a bandit. Then there will be no further arguments. In fact all arguments are intellectual and give leverdged investors false hope

Well put , i might add that even the IRD did not support the introduced interest rate change.

As a landlord with one property I'm off to tell tenant that in obligatory 60 days their rent is going up by 6.6% or $30 per week . All done within current rules given the relevant prices in the area

HeavyG..there may be no tax policy basis that can justify the new law. However, there are strong moral considerations and a desire to effect social change stemming from our desire to make NZ a more inclusive environment. If it sits better with you, it can be viewed as a type of sin tax similar to the one we need to pay on cigarettes and alcohol. It is a non argument to contest it is unfair to pay tax of cigarettes when bread and milk are not taxed in the same way. There are valid reasons for the tax differences just as there are valid (moral) reasons why interest deductions should be a deductible expense for a real business but not for property investment.

To me, the main objective is to remove (most) investors from the (second hand housing) market to give FHBs more of an opportunity. None of the existing houses will magically disappear and by forcing investors to build (or move into a real business) the changes are likely to see an increase in the supply of housing. If issues like rent increases, unoccupied homes and conversion to Air B n B or commercial become a problem then swift action can be undertaken.

And as the author points out, negative gearing is basically an admission that a rental is being held for capital gains and therefore should probably be taxed as such irrespective of how long the property is held. Ensuring that from now on the IRD correctly applies the tax laws related to capital gains on investment properties is just another tool that needs to be used to level the uneven playing field a little more.

Morals are like the proverbial, everyone has their own. Some think the Government confiscating farms off the white farmers in Zimbabwe was morally justified. Some probably think confiscating homes a person owns but does not live in is justified. The old end justify the means argument.

Enacting a law or regulation does not mean it is right or correct, that decision is in the hands of those affected and they will make decisions that may take time to effect so Govt may have created an explosive Pandora's box that will open in 2022 and those hit by the explosion will not understand how it all happened, and will demonstrate just how little so many have failed to learn from History.

You do not buy a business solely for the tax advantages. Most property investors- speculators buy solely for the non taxable profit from capital gain or tax write offs. Hence property investment is not a real business and should not be treated like a business.

itsme..some people also regard ticket scalping and drug dealing as businesses. It is up to each individual person to allow their moral compass to point them in the right direction when it comes to property investment. And if that does not work, we can regulate and legislate to ensure that the actions of a few are not harming many.

Legal opinion from MBIE classifies land lords as a business. You provide a service and are paid accordingly. As such your post is nonsense but your not alone. Just as an aside describe to us all what you see as the difference between an investor and a speculator

Hi GPH, Not sure if your question about the difference between an investor (rental investor), and a speculator (speculative investor) is rhetorical, but the difference comes about because our system ie Govt. policy, allows two different types of capital growth to exist (can exist at the same time) and therefore two different types of investors (and you can be both at the same time)

This is a repost but this is how it works.

There are also two types of capital growth, value-added and non-value added.

For a typical rental investor in a free market, they get neither. They buy the property and make all their return on yield, and money spent on the property on maintenance is just to retain its amenity value and any increase in price (and therefore rent) is based on basic inflation. They get no value-added or no non-value-added growth. For this to work yield has to be higher, which is easily achieved if we lower the price, but only if you get to buy at that price. If you have paid today's price, then you would have to raise rent to achieve a higher yield in lieu of any capital growth, otherwise, take the equity loss.

Any developer investor can get the same as the rental investor but they also get the value-added capital gains by taking raw assets eg land plus building equals finished house, ie the sum of the whole is greater than the value of the individual parts. Thus extra 'sum' they make is because they added value and is the reward for their effort and risk.

Non-value added capital growth is making money from a property without the need for yield or adding any value-added input. This can only happen when there are restrictions (not a free market) in the system eg land supply, consenting cost, and time delays which allow rentier monopoly to occur ie supply is less than demand, and in fact, if you own that supply, the less you do with it, the more you will make relative.

Govt. policy allows non-value-added behaviour to happen, and rather than change the policy, they are going to tax the very behaviour they encouraged.

So if its not a business its a hobby and not taxable.

I just discovered Inland Revenue has something called an Intention Rule, which states if it was your firm intention to buy the property for the purposes of selling at a later stage, you must pay tax. That means, myself being the honest type, I would have to pay tax on my "first home" because it would be my intention of selling at a later stage to get a better home.

This is more messed up than I thought. Or is it just one of these technicality rules that nobody cares about?

https://www.ird.govt.nz/property/buying-and-selling-residential-propert…

Nearly everyone buying a property will sell it at some stage. However, this alone isn't enough for any profits to be taxed. In most cases you don't have to pay tax when you sell your main home or if you bought the property as a long-term rental investment.

Nzdan...I believe the regulations need to change. Specifically I think the last part you posted should be deleted and replaced with something stating that all investment property will be taxed at the point of sale as it was purchased (at least in part) with the intention of making a capital gain. Why? Because in almost every case, it was.

Karl - if the inflationary element is excluded then you may have a point but then the inflationery element of business profits and deposit interest should be treated the same.

The intention rule you refer to is in section CB 6 of the Income Tax Act 2007 (see https://www.legislation.govt.nz/act/public/2007/0097/latest/DLM1512414…).

However, section CB 16 of the Income Tax Act 2007 states the intention rule does not apply to a person's home (see https://www.legislation.govt.nz/act/public/2007/0097/latest/DLM1512444…). Take a chill pill and relax.

I hope you've got an accountant helping you dear

Has there been any indication of the additional tax take once the interest deductions have been removed?

I saw a figure of $600m as a combination of both the BLT and interest deductability - 4x the increase in the top tax rate will bring in. Things are ripe for a tax switch

".....saying that rent doesn't cover the cost of a mortgage and other costs, as one investor said in print, is an open invitation to Inland Revenue to raise questions as to why if that was the case, that person had purchased property. It opens the door for Inland Revenue to then go on and say, “Well, you must have acquired that with a purpose or intent of sale.” Which if that is argued bypasses the bright-line test. It doesn't matter how long you've held it in those in those circumstances, any gain will be taxable.

CB4 Income Tax Act ??Is this not what this piece of legislation is about? .

Presumed Intention. Rebuttable presumption with onus on the owner to prove otherwise.

No, over time as rents increase and the investor is in a position to pay down debt the property may become profitable. You don't have to be making a profit on day one to ward off a claim you are a speculator.

Agreed HG: however one needs to be careful and it may not pan out the way you intend e.g. mortgage interest rates increase or changes in personal circumstances and it may not be profitable when intended.

A scenario: owned a rental prior to last Tuesday, interest rates go up, after six years one decides I'm outta here and sells (beyond the applicable five year Brightline Test) and makes a very great big capital gain while never having made a profit on rent . . . . . "ah ha" says IRD you never made a profit and never intended to.

As the article correctly comments - "It opens the door for Inland Revenue to then go on and say, “Well, you must have acquired that with a purpose or intent of sale.” Which if that is argued bypasses the bright-line test. It doesn't matter how long you've held it in those in those circumstances, any gain will be taxable".

That is quite possible and as Jaf comments: "Rebuttable presumption with onus on the owner to prove otherwise".

It is interesting we have this notion that one is innocent until proven guilty - and generally that is so except when it comes to IRD. They can make a determination and it is up to you to prove otherwise - and there are considerable numbers who can attest that this has led to expensive court cases while IRD continues to apply penalty rates to the extent that bankruptcies can follow.

Was advised very early on that always document your intent. An easy way is when dealing with the bank at the outset is document your intent - they will want to know anyway - and get them to stamp and date it and you file it; this could be just a very brief half page calculation as to how a profit could be turned successively over four of five years at expected interest rates.

I was advised (by someone who had experienced IRD issues) when I bought an old pretty derelict property - not cash flow positive - but with the intent of developing it as a home which would have had great capital gains. However if things changed and I needed/wanted to sell and did so at a profit even before development then I had a way of showing my intent by means of a timeline and funding arrangements including sale of existing home as part of that funding - and had it date stamped by the bank. Things did change near completion . . . fortunately IRD didn't come knocking claiming I was simply a developer seeking capital gains.

The reason the Brightline test was introduced was because IR never raised the ""ah ha" ...you never made a profit and never intended to" argument. It never raised that argument as it had a snowball's chance in hell of being successful before a judge as it would require the implication that the investor knew future interest rates, rental prices, sales prices and the requirement to sell at date of acquisition. A fantastic claim that has never seen light of day and never will.

If 'market rent' does not cover the capital cost of the house - then regardless of the owner, the renter won't be able to afford to rent.

Government 'will take action' if rents spike, Grant Robertson says.

https://www.stuff.co.nz/life-style/homed/housing-affordability/30026401…

I think we can safely say Grant follows through.. It won't happen over night but it WILL happen :D

Rents can't help but spike - has anyone seen the projected rates increases? Otago regional council 46.5%, Environment Canterbury 24.4%, New Plymouth District Council 100% or thereabouts over the next ten years, to name just a few. To cover off the cost increases coming down the line landlords might be justified in increasing rents by similar magnitudes.

So say New Plymouth rates average $3,000. Up 100% over 10 years. Thanks another $300 per year on average. So rental go up $6 a week each year more than covers it.

Seems reasonable and manageable.

Mortgage costs have gone down by how much over those 10 years?

Rates are still deductible for property investors.

Why wouldn't they have already put rents up if they could have? Landlords costs aren't typically able to be passed onto the renters, because they're already charging the maximum. Of course there are individual situations where market rent is not being charged, but as an entity, landlords charge as much as they can, and don't put rent down when their costs go down. They put rent down when demand goes down or supply goes up.

Rate arrears will spike as well last reliable info I saw was ChCh rate arrears were 24,000, may be more now and will undoubtedly increase if interest rates increase and the recession we are currently in turns to depression.

With interest only loans next to go it’s interesting times for highly leveraged investors.

It’s going to be interesting to see how the banks respond.... will they require higher deposits and interest rates?

This thing could unwind very quickly

Cant wait to see it personally

Already know of an investor on interest only being told by his bank to begin paying principle off - seems banks need to improve their capital position after covid relief looks like expiring. The same will apply to TD rates - banks will need to encourage these to improve capital.

Another informative & helpful article. Thanks Terry

Farming of debt structured to avoid tax while paying ever stupider prices is killing NZ. It is the foundations of Ponzi. Burn it all down.

Agree. We don't need that money circulating the economy this year.

So all the criticism of government for tax changes was lot of BS supported by opposistion, so called economist and experts.

Similarly RBNZ in consultation with government should act on interest only loan and act fast.

Maybe we will see the large corporates move into the housing investment area. As they can more cleverly structure their tax obligations etc.

In which case renters will be worse off - or at least kept at arms length in the rental agreement process.

If they did the govt would move to prevent. They are clearly signalling they are taking the profits out of the market. Take the hint and get your money working in another area, it's clear as day they will keep adding tools until what they have works to curb and/or bring back prices to wages.

You seem to be laboring under misapprehension .. that this ( or any ) government can always achieve what they wish .

When you discover an non property investment with a decent yield to risk profile please share.

It's all about greed then right?!

That is the government's intention to have more institutional landlords, who supposedly can provide more stable rental than private landlords, interesting read from another commentator, https://croakingcassandra.com/2021/03/24/messing-around-with-housing/

Great, as long as they are new builds

We are set on making everything so complicated, if a DTI was introduced it solves almost everything.

Keeps houses aligned to wages, stops "investors" being speculators. Some investors are leveraged to the hilt whilst only drawing bigger all in revenue.

And for those wanting to change to a limited liability company wont they have to pay GST on the sale price when they sell?

I kind of agree, but DTI settings would still be under control of Reserve Bank, like LVRs? Current stewardship of Orr indicates even with that tool RB would have opened the floodgates late last year and unleashed the dogs of leverage.

This definitely reduces the power of leverage. Albeit only reduces the power by approx 33% of the power of DTI. From central govt perpsective - maybe thinking is that it is a good tool to have in power of govt rather than independent RB, in case get another dud like Orr?

Coming from something like Terry who consistently advocates higher taxes on capital income and whose business stands to benefit greatly from the tax changes on the table - I say this article is a pretty damning indictment.

Well Mr Robertson deserves a plus for standing

https://www.nbr.co.nz/story/no-intention-go-past-housing-interest-deduc…

Now should follow up and ask RBNZ to act on Interest only loan and stan up like a true leader for not falling for all the noise and pressure thrown by vested biased forced.

Am I reading this article correctly that interest and repairs may still be tax deductible if, and only if, the property was purchased with the intention of providing long term income? The details are still being clarified. Is this correct?

The change is no deduction for mortage payments. Principal repayments have been disallowed since adam was in shorts and now interest will be disallowed too. Yes other expenses still qualify

If we are to accept that a much greater number of people could well be renting for life from now on, then how that happens absolutely MUST change, how can anyone think it is fine that someone is subjected to being ejected at any moment, that they cannot afford their home (affordable is what even rented houses must become for these people) and that some control freak landlord is commanding how they live in "his/her" house.

I think we need to cultivate different ways permanently rented houses are both owned AND rented (leased) and the whole "it's my house, I say what goes" attitude has got to be gone, with more co-operative ownership to take its place. It does not mean that houses will no longer be available for short term but there will be far fewer of them, and hopefully not a great deal of demand.

I actually blame the way houses have been rented in this country, to quite a large extent, for much of the break down of society and the traumatization of people locked out of ever having somewhere to call home, take a bow, all you people farmers out there.

Change has to come

Interesting to see how bad policy leads to worse.

Covid19 overreaction -> economic destruction -> ultra-low interest rates -> asset inflation -> reactionary ad hoc policy response.

Smokefree 2025 -> over 2 billion pa. tax revenue from the poorest of the poor -> MSD crisis, Whānau Ora, emergency accommodation, working for families, accommodation supplement.

fat pat,

"Covid 19 overreaction". Really? Not one of the many people I know living in the UK would agree with you. They have been living in lockdown for much of the past year and they are deeply envious that i could fly to the South Island for a 5 day cycle ride. Actually, they envy the simple things even more; like just being able to head out for a coffee as i am about to do.

linklater, my personal opinion is that covid is between 5 and 10 times worse than the flu in terms of infection fatality rate. I conclude that by looking at the overestimate IFR from the American CDC which says ~10x, and more importantly by looking at the excess death data on euromomo. There is however, an inexpensive medicine, namely ivermectin, which lowers the death rate in mild moderate to severe hospitalised patients by 87% according to the meta analysis of randomised controlled clinical trials. Combined with risk mitigation from zinc and vitamin D3 supplementation, and infection control measures, COVID19 could've been managed as though it were a bad flu season. We're past that point now. It's politicised. Too many reputations, and too much money has been staked on the current narrative to acknowledge anything else. It's all very Orwellian.

Horse do-dos and as exhibit 1 I give you Brazil.

What our covid response has done that isn't that positive is create a safe place for all those people who can bolt back here so as to get away from it. Many of those have residencies and citizenships that seem to be just a convenience, I am picking they will be away again as soon as the coast is clear.

Love how people quote Orwell or rather Eric Blair, who was a socialist.

As far as I can tell Brazil has opaque data regarding excess deaths. Perfect for obfuscation, and muddying the waters.

From Croaking Cassandra:

"And don’t go blaming interest rates for the house prices, as the Minister tries to do (waving his hands and suggesting here are lots of things outside his control). Did you know that, even now, real interest rates in most of the advanced world are even lower than those here (in the US, for example, the real 10 year government bond yields is about -0.7 per cent)?"

House prices aren't doing things in countries with even lower interest rates, which suggests that something quite different is going on.

As I've often said when people trot out all the excuses about why we have high houses. Other places have these same issues yet have affordable housing.

The main difference, as the evidence shows, the more restrictive the housing policies, especially land, the higher the house prices.

A LL has the right to control how many people occupy the property, also whether they smoke and the types of pets amongst other responsibilities of the tenant. It is a two way street as you would be quick telling the LL to fuck off coming round at stupid hours or without notice

I'd want to see the whole damn sector revisited. Get rid of interest deductions by all means, but watertightness repairs should be deductible, as should insulation to comply with rules around minimum standards for healthy homes.

The government is adjusting the available returns around property investment significantly downward. If you have a lot of property investments, the party is over. Sell up and move that capital somewhere else, stocks, bonds, commercial property? If this doesn't do the trick they will keep adding legislation until it works. The policy isn't about targeting investors it's clearly about targeting inequality and about time

That's the crux. The anger comes from the realization that they lack the skill and insight to succeed at other investing categories - they just want a free ride, easy gain investment class regardless of the cost to society.

How about those with property in their portfolio that are mortgage free?

So the removal of interest deductibility is because of untaxed capital gain? Then why not introduce a broad-based capital gain's tax? Not every investor sold had gains, and not all gains the same from every sale. Why not just tax people on the actual money they have made, which would be fairer. It should also cover farm land, commercial property, retirement villages & various investment portfolios, all of which are making huge untaxed capital gains (also mainly owned by very wealthy people).

The real reason to single out residential property investors was to deflect public attention from focusing on the real issue of "supply", which they have failed to address, and is incompetent to solve. At the same time, they had tied their hands by rolling out a capital gain tax. So now the only thing they can do is to single out one group of people and make them the public enemy......

With the numbers of people coming into the country, building at a rate not seen for decades, and undersupply and neglect for years and years there is no way to keep up with demand, bar miracles, so it is pretty damned ugly watching house prices just keep bounding away from first home buyers and the people farmers (landlords) with all the buying power. The whole system is rotten to the core

The people-farmers abject hatred for first home buyers is on display in all its ugliness now. First home buyers used to be simply 'buyers' ie people wanting to pay off and finally own, after decades of paying the bank interest, a home of their own. Now most people (most people want to own their own home) are hated by a small group of very vocal, aggressive ponzi schemers. I can't wait to see the next round of spankings

Supposedly FHBers make a person homeless because of rented vs owner occupied occupancy rates and they also bid up the price of a house at auction which means investors are forced to pay fist fulls of extra cash to out bid them and then the Landlords are forced to charge more in rent to compensate because Landlords work on cost + etc. This then filters through to other aspiring first home buyers who must pay extra rent thanks to their ex-renting peers for their frivolous bidding techniques. The biggest losers out of this are the Avocado orchards.

Love this!

Dago. Gee after labelling the landlords as haters and calling them derogatory terms you proceed to revel and delight in punishments towards them. I certainly hope with that attitude that you're not a tenant.

I completely agree that the house price has gone too high. Actually, all assets price have inflated due to the endless money printing (The government had plenty of warning about it last year). So is punishing the exiting landlord going to increase supply, and providing accommodation for the homeless? Ok, there will be extra tax revenue, which could be used to pay for more motel units. But is that the outcome we all want? If they had the gut to implement capital gains tax, or listen to the warning and not relaxing LVR last year, or reform RMA to solve land supply issue, we would not be in such a difficult position today. Remember, this new policy does not affect the wealthy people with no mortgages.

There are also two types of capital growth, value-added and non-value added.

For a typical rental investor in a free market, they get neither. They buy the property and make all their return on yield, and money spent on the property on maintenance is just to retain its amenity value and any increase in price (and therefore rent) is based on basic inflation. They get no value-added or no non-value-added growth,

Any developer investor can get the same as the rental investor but they also get the value-added capital gains by taking raw assets eg land plus building equals finished house, ie the sum of the whole is greater than the value of the individual parts. Thus extra 'sum' they make is because they added value and is the reward for their effort and risk.

Non-value added capital growth is making money from a property without the need for yield or adding any value-added input. This can only happen when there are restrictions (not a free market) in the system eg land supply, consenting cost, and time delays which allow rentier monopoly to occur ie supply is less than demand, and in fact, if you own that supply, the less you do with it, the more you will make.

Govt. policy allows non-value-added behaviour to happen, and rather than change the policy, they are going to tax the very behaviour they encouraged.

Asked an agent today if they saw any changes and they said not in the big investors as they are more likely to be developers.

Seems like an uneven playing field for first home buyers if big business can buy up the residential properties as well.

I wouldn’t trust a word anyone says in this sorry saga

So called big investors might just be people who have used interest only loans and the increased equity in their holdings on the way up. They might be the first to fall over if required to begin principal payments.

I think it’s going to be a rout.... just wait for the first news of listing increasing.... who’s going to buy when you think it’s going to be cheaper in another years time.

I wouldn’t trust a word anyone says in this sorry saga

So called big investors might just be people who have used interest only loans and the increased equity in their holdings on the way up. They might be the first to fall over if required to begin principal payments.

I think it’s going to be a rout.... just wait for the first news of listing increasing.... who’s going to buy when you think it’s going to be cheaper in another years time.

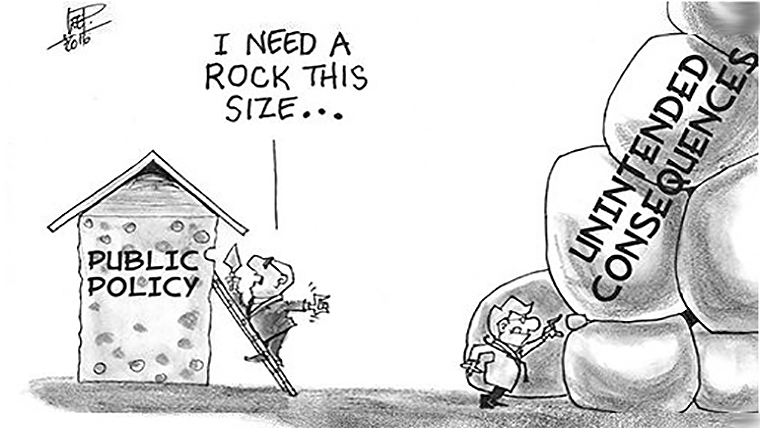

Btw I do like the cartoon caption at the top of the article ... watch out robbo!

"For example, saying that rent doesn't cover the cost of a mortgage and other costs, as one investor said in print, is an open invitation to Inland Revenue to raise questions as to why if that was the case, that person had purchased property. It opens the door for Inland Revenue to then go on and say, “Well, you must have acquired that with a purpose or intent of sale.”"

Hey what?! Now theres a big jump to a conclusion thats not necessarily what the person intended. Mortgage costs include both capital repayment as well as cost of interest expense, people know that. With low mortgage rates the capital repayment portion of mortgage payments is significant right from day dot. It impacts cashflow considerably

It seems ironic that the government is pinning most of the blame on investors. What about their rezoning of thin strips of land near main roads for terrace housing and apartment buildings? Those sections are selling for Lotto Powerball figures. How easy is it to deal with councils? How easy is it to buy reasonably priced building products? What quantity of labour and material was wasted rebuilding all the leaky homes due to slack oversight and regulations? What about all the QE and low interest rates to create the so called wealth effect? No, leave the landlords alone, it is the self-appointed geniuses in government that have led us where we are today. Sorry, but I do believe that none of these people actually know what they are doing.

Ah, so it's everyone else's fault. We generally try to get kids out of that sort of "It's not fair" finger pointing when they're about three.

Unless the "It's not fair" finger pointing is directed at property investors. Look at all their greedy profits! I feel the same way when I shop at the supermarket or hardware suppliers.

I don't think this is about blaming investors at all - more about levelling the playing field between investors and owner occupiers.

Do you think that it was fair for investors to have a tax advantage over owner occupiers (through the deductibility of mortgage interest)?

I think when the government started selling state houses and encouraging the private sector in to this market it needed these incentives. If you have no debt on your rental house you pay income tax on your profits. Like any other enterprise, interest costs should be tax deductible. Perhaps Labour should look at a tax on the equity in people's houses. That would really flatten the prices and collect more tax to help the struggling FHB's.

Unintended one year of LVR removal & QEs/FLPs that outshine all OECDs in term of country size of everything.

Then lowering OCR - what's the result of that? the intention vs. the unintended result?

Now, this tinkering with Tax - surely there's a good intention behind it.. but let's see both real result.

For sure, in NZ only F.I.RE economy? - Every body join the drug addiction band wagon of economic darling:

https://play.stuff.co.nz/details/_6244892732001

Good time still ahead folks!, NZ has indeed beaten the UK, Canada, US, OZ for housing. But still need to surpass Luxembourg. Winning the cup, desired place to live, lucky C19 border, vaccine - Don't read or listen to what all those OZ Banks economist say, but see what they do on their loan approval book, so.. apply now!

The UK situation isn’t quite as clear cut as Mr Baucher implies. There is a 20% credit on the total interest bill, which still means no relief on the residual 80%, but also a catch-all CGT, and punitive stamp duty. And CGT also applies to baches and other second homes.

Have to disagree with Mr Baucher about ending tax relief being a shock. It was flagged last year as a possibility and has been widely discussed. Always on the cards. Best commentary I’ve read was John Roughan in Saturday’s NZH. And of course he’s very right wing.

The problem really is that the aim of most property investors is to make tax free gains while being subsidised by non investors. Quite a common practice to even leave homes empty, especially with overseas buyers who often act through proxies here. Total rort.

You really do not know what you are talking about ...

"The UK situation.. There is a 20% credit on the total interest bill, which still means no relief on the residual 80%"

In fact one gets relief on the whole of interest repayments , just at a fixed ( 20%) tax rate , not at whatever marginal rate one has .

Assuming most landlords here in NZ would be on 33% rate an equivalent measure here would only have about 1/3 of the impact of what is actually announced. What Robbo is doing here is simply unprecedented.

Just on thing matters. Will National repeal the Capital gains tax and get rid of that weird tax on business turnover that’s been selectively inflicted on just one type of business enterprise ?

Oh yeah, and how long until the next election.

They won’t. Because it will bring in a huge amount of tax meaning income taxes or consumption taxes won’t need to rise so much to cover the Covid reckoning. Another factor is that it’s a popular vote winning policy. Not everyone is a landlord.

Capital gains tax's have been in place for decades in Australia. Is that why Sydney home prices are so cheap?

Shhhh

Property investor here, I've bought a few shitters, fixed them and rent them out. Can afford the tens of thousands in extra tax since I invest for cashflow and have been gradually building up for years. I guess I'm a speculator who exploits loopholes in a ponzi scheme now.

The property I buy is usually uninhabitable and I sometimes have to use asset lenders until they are repaired. I pick those types of homes are about to become 20% cheaper because no sacred FHB would ever look at them. Rent will be a bit (not as much as people say) higher after repairing. Just have to make sure my numbers stack at 1.5x what the banks lend at on P&I.

Keep calm and carry on.

The real rental crunch may be in really nice suburbs with top school zoning as those properties will have lower yields so investors might not bother with them. Who knows, the government surely doesn't.

Massive generalisation about first home buyers. I've seen plenty of dumps transformed by hardworking optimists.

Interesting that in the Govts. response, there has been no acknowledgement between long term rental investors and speculative investors.

Maybe that is because the long term rental investors also benefit from a system that allows speculative investors to drive up prices and there has been a morphing of the two.

To paraphrase George Orwell's Animal Farm:

"No question now, what had happened to the faces of the Investors. The Govt. outside looked from rental investor to speculative investor, and from speculative investor to rental investor, and from rental investor to speculative investor again; but already it was impossible to say which was which."

You are known by the friends you keep. Maybe rental investors need to choose better friends.

Interesting article, yeah I had kind of forgotten about the ring fencing changes, you would think that should do enough on it's own to stop a lot of the silly things that had been going on, but they haven't really even had time to kick in much.

You do have to wonder if they gave the ring fencing enough time to start having an effect as well, if given a couple of years to work, the interest changes probably weren't needed.

You would have also thought that the removal of most depreciation and redefining what is a chattel would have done it.

But of course, none of it does, when you have a shortage of supply, as this just turns the business model into a cost-plus supply model rather than a market-driven model, ie you just add it to what you charge renters, and the Govt. has also subsidized any shortfall, so this further encourages it.

The removal of interest by itself is not the issue, but it has been the cumulative effect of ringfencing, lack of depreciation, chattel redefinition, LVR increases, banks tightening up, and now interest deductibility that has brought this to a head.

The interest rate removal is just the straw the may break this camel's back.

Dale..we can only hope. And if the RBNZ remove interest only loans (with immediate effect) in May there will be an even higher chance of success.

The Elephant still in the room for me is new builds. This is because most new builds are on the fringe on land that they have paid the landbank price for, which was 'baked' into the cost long ago. IE yes it is some supply, but it is a historically expensive supply.

And focussing on new builds, this will be a bit counter-intuitive, but it actually decreases supply, ie rather than ALL land, both for new and existing, being treated equally, the focus is on a smaller part of the whole ie new builds, so the pie just got smaller, ie less supply to demand.

And the price of all land is set at the fringe, so it will affect the price of all new builds going in.

It's hard for housing to become more affordable when your input costs are dearer, especially if they are non-value-added costs because they don't improve the amenity value and take money away from other more important areas.

philthy...ring fencing is definitely a good thing and should remain.

After reading the article in this morning's Herald about how many multiple rental properties and farms that are held in trust by our politicians, one can understand why property prices have been allowed to get out of control.

Terry think you might be wrong here :

"The interest rate restriction rules, as an article in the Herald points out, are actually more restrictive than a similar measure introduced in the UK. What the British did was restrict the rate of the tax relief to the basic rate of tax, roughly 20%. These measures go completely further."

They can take off income the lower of any of a number of measures, one of which being 20% interest expenses (and if they do this then they cannot also take off all other expenses like rates, insurance, PM fees etc like we still can in 4 years). Rates, insurance, depreciation chattles, maintenance can run much higher than 20% of interest expenses even at 80% LVR. NOT that im giving the govt any ideas.

Correct me if I am wrong.

I'm in the market for a property tax expert, like many I suspect. Lawyers and accountants must be loving GR

Clearly the only fair way forward to satisfy all arguments moralistic or otherwise is to introduce a comprehensive CGT including the family home.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.