By Jenée Tibshraeny

The government is trying to dampen investor demand for property by making investors pay more tax.

On March 23 it announced people who buy and sell investment property within 10 years will need to pay tax on any gains made. Investors will also no longer be able to deduct interest from their incomes for tax purposes.

The question now is, do these moves reduce the likelihood of the Reserve Bank (RBNZ) putting further restrictions on mortgage lending?

The RBNZ is expected to report back to the government in May on how it could restrict banks from issuing interest-only mortgages and lending to those seeking high levels of debt compared to their incomes.

Finance Minister Grant Robertson has been clear he doesn’t want first-home buyers impacted by any changes.

The RBNZ will undoubtedly be watching bank lending data closely between now and May, when it’s also due to release its biannual Financial Stability Report (on May 5).

It might start preparing a consultation on further restrictions, but it's unlikely we will see these introduced in the next few months at least.

Why?

The RBNZ might want to see the impact of the interest deductibility change, as well as its move to reinstate loan-to-value ratio (LVR) restrictions at a tougher level for investors before doing more to dampen demand for housing.

Most commentators suggest the interest deductibility change will have a significant impact - if not in terms of costing investors more upfront, then in terms of reduced confidence.

Neither Treasury nor the Inland Revenue (IR) provided any commentary in the Regulatory Impact Assessment on the change. Treasury said it didn’t support the change as it didn’t have enough time to analyse the policy.

Cabinet making such a significant policy change without the support of Treasury and IR, without knowing exactly how the policy is going to look, and without evidence to show it has modelled potential impacts, creates a fair bit of uncertainty.

Presumably the RBNZ will tread cautiously before introducing another restriction in this environment.

While the RBNZ is tasked with ensuring the surge in mortgage lending doesn’t compromise financial stability, it’s also tasked with keeping inflation and employment buoyed.

How has it endeavoured to do so since COVID-19 hit? Through lowering interest rates to ease debt-servicing costs and encourage investment. And where do New Zealanders like to invest? Property.

Worth more than a trillion dollars, or about four times the value of New Zealand’s annual Gross Domestic Product (GDP), the housing market effectively is the New Zealand economy.

RBNZ could've acted on interest-only lending by now

Had the RBNZ believed its efforts to encourage more borrowing and investment were putting the banking system at risk, it could’ve acted sooner to rein things in.

But, bar the reinstatement of LVRs, it hasn’t, raising the question of why it would do so now that government has acted.

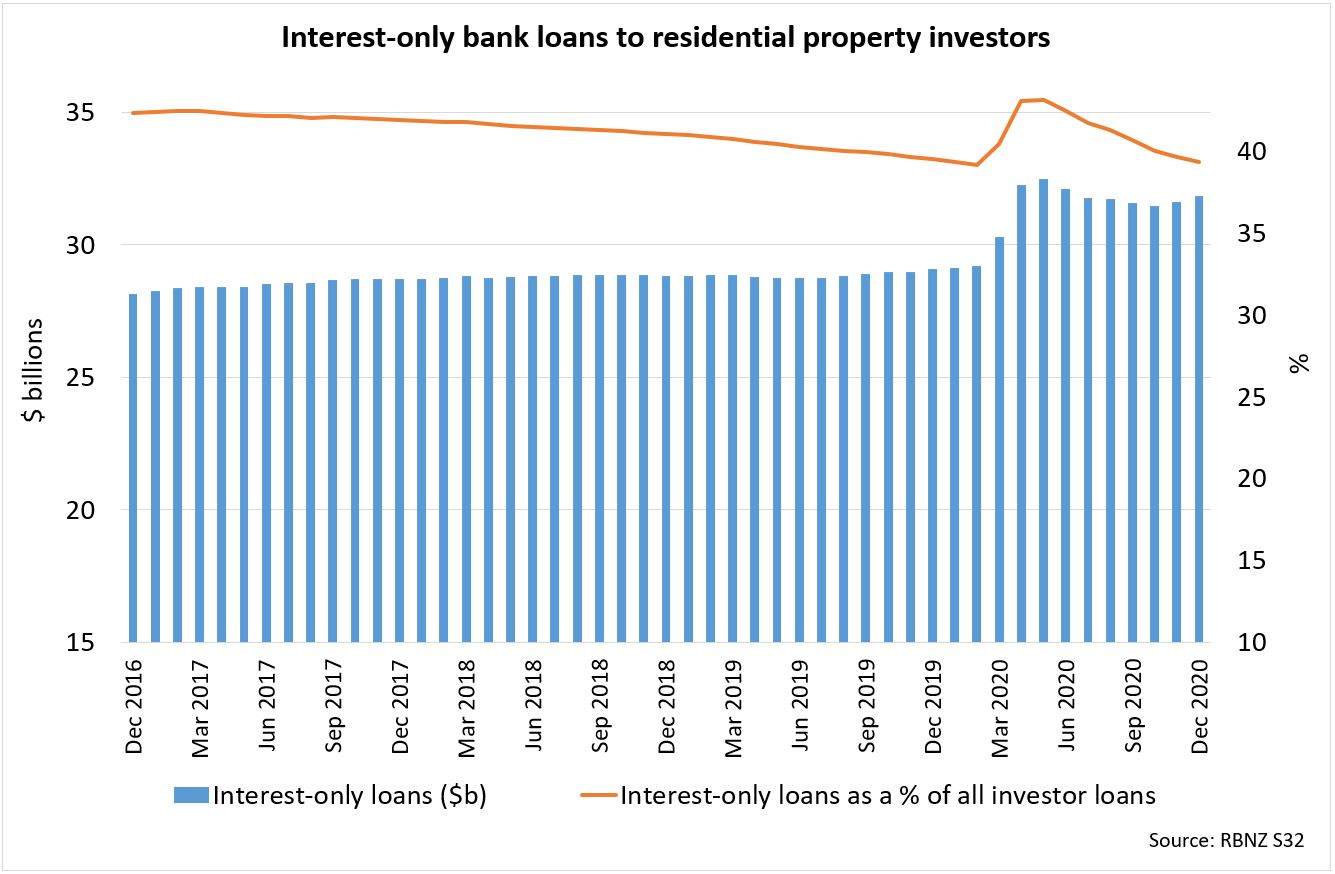

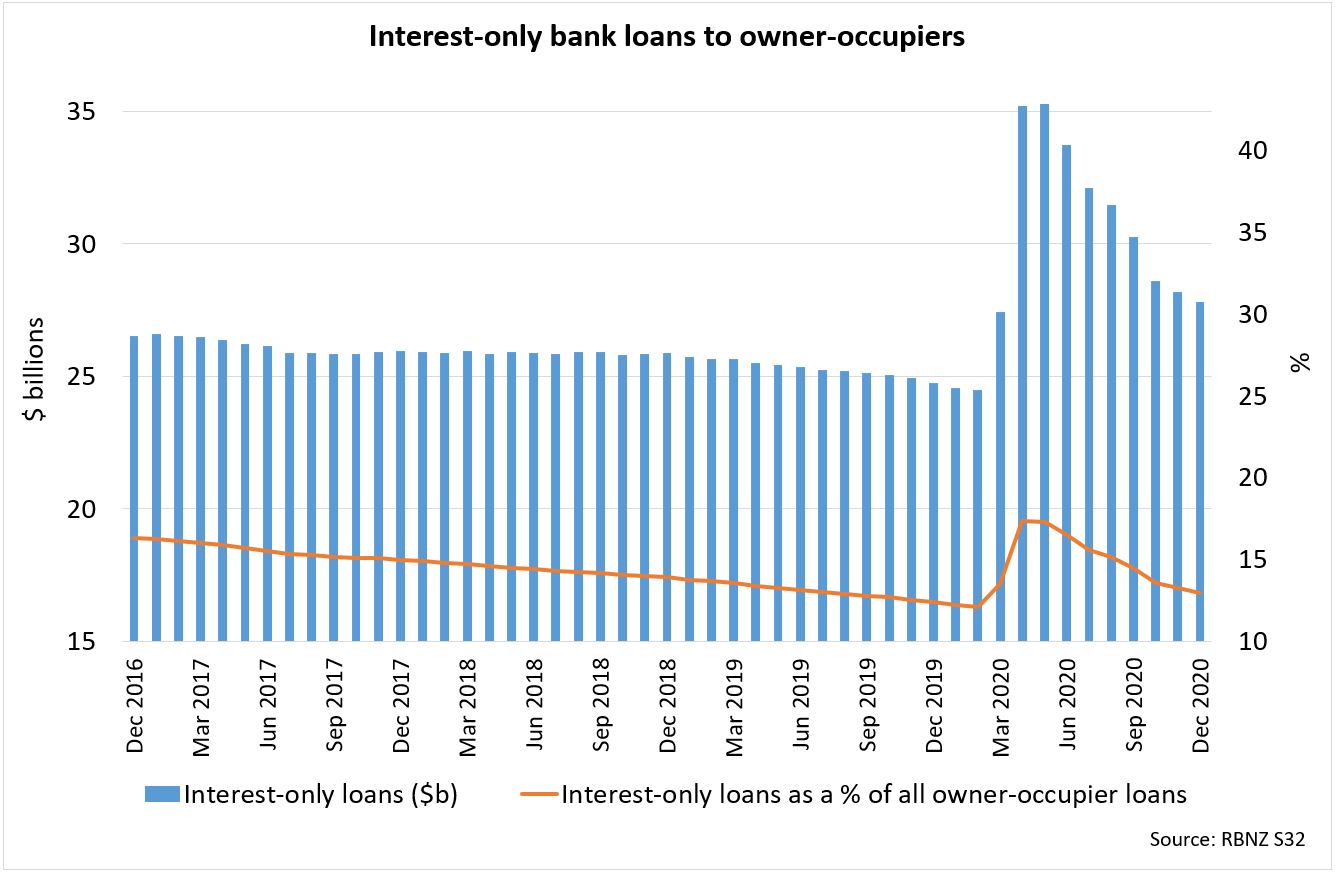

The data shows banks have certainly been engaging in riskier lending.

These graphs show how the portion of interest-only lending increased last year as banks were given a pass from their regulator to offer more mortgage repayment deferrals.

While the portion has dropped back down, the value of interest-only mortgages - especially for investors - remains at a high level.

The RBNZ told interest.co.nz it could restrict interest-only mortgages now if it wanted to - without the government’s permission.

“An interest-only restriction is not necessarily a macro-prudential instrument and the Reserve Bank could deploy it under s 78 (1) (fa),” an RBNZ spokesperson said.

“Section 78 (1) (fa) gives the RBNZ the power to regulate on matters relating to "risk management systems and policies" as long as it supports the soundness and efficiency of the financial system. A restriction on interest-only mortgage lending fits this category.”

However, when interest.co.nz asked Robertson’s office whether the RBNZ could restrict interest-only lending without government permission, a spokesperson from his office framed the situation differently.

They acknowledged the RBNZ could restrict the use of interest-only mortgages on a bank-by-bank basis as a “micro-prudential tool”.

But if the RBNZ was to implement restrictions on a system-wide basis, which is what Robertson’s asked it for advice on, it would be considered a “macro-prudential tool”. And Robertson would need to give the RBNZ permission to use it.

This is clearly a complex legal issue, but the fact Robertson and the RBNZ gave interest.co.nz different sounding answers to the same question, suggests the issue of restricting interest-only mortgages hasn’t been thrashed out in detail.

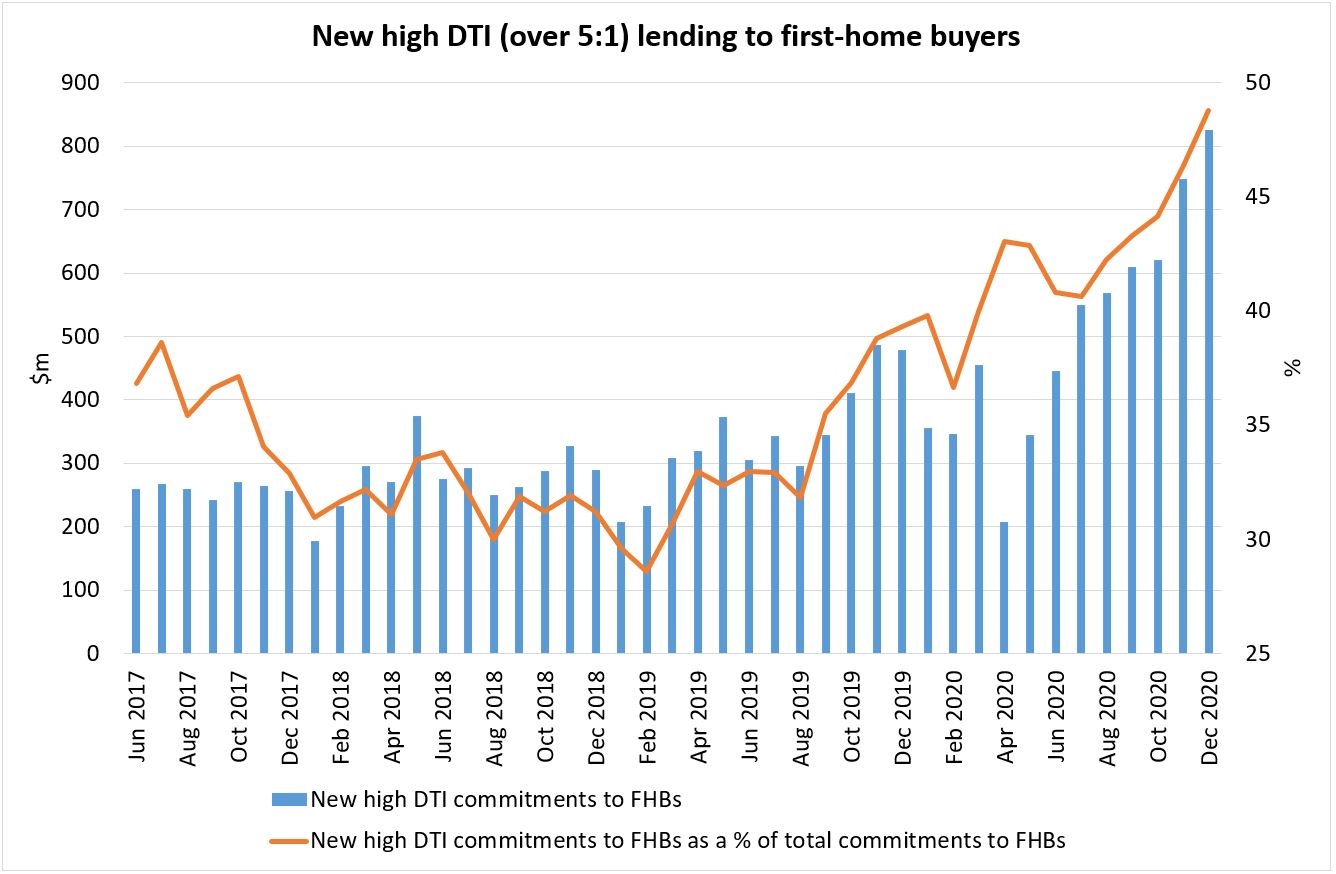

Data suggests any DTI restrictions should include FHBs

As for the introduction of debt-to-income (DTI) restrictions, the RBNZ has for some years wanted this tool, but governments have said no, as they’d make it harder for first-home buyers to get on the property ladder.

Robertson has been clear his preference is for such restrictions to only be applied to investors. But RBNZ Governor Adrian Orr has said targeting restrictions in such a way would be difficult.

What’s more, it might be difficult for the RBNZ to justify targeting DTIs to investors when first-home buyers and owner-occupiers are taking out increasing large amounts of debt compared to their incomes.

The RBNZ simply couldn’t ignore this substantive uptick in new lending to first-home buyers with debt more than five times their incomes (which is deemed high-risk):

The RBNZ doesn't publish DTI data for investors.

As with LVRs, the RBNZ needs to consider how this kind of bank lending affects financial stability. It isn’t tasked with helping first-home buyers into the property market, or keeping them happy come election time.

The removal of interest deductibility surprised most people - even to the point it prompted financial markets to bet on slower economic growth and thus interest rates remaining lower for longer. So anything is possible.

But for us to see DTIs imposed in the near-term, either Robertson or the RBNZ would need to change their approach.

And for us to see interest-only mortgage restrictions imposed in the near-term, the RBNZ would need to see risks it hasn’t seen to date.

The RBNZ would also need to be confident that taking more wind out of the property market’s sails to effectively protect banks from themselves, isn’t going to bring the economy to a standstill.

With its Large-Scale Asset Purchase programme coming up against a headwind, as Treasury issues fewer bonds than planned, it would be left with little choice but to cut the Official Cash Rate (OCR) into negative territory if it felt it needed to do more to stimulate the economy.

And what’s the last thing we need to tackle the housing crisis? Even lower interest rates.

*This article was first published in our email for paying subscribers on Friday. See here for more details and how to subscribe.

150 Comments

I swell with pride and confidence when I see those fearless leaders going in to bat for the asset rich

Orr & Robertson got this under control╚(ಠ_ಠ)=┐

Most property investors will pivot to paying down loans anyway and DTI is already largely covered by serviceability rules.

Eventually it wont matter, the RBNZ is forced by the Fed, 10yr UST yields are up massively this year.

Hope you're right

Exactly right. Just by looking at what is happening to bond markets and yield curves now, it is clear that the tide of higher interest rates is coming.

The RBNZ is fast approaching total irrelevance, as financial markets will progressively ignore its desperate last moves to keep the housing Ponzi alive for a little longer. Orr can take the OCR down to a negative level, try to talk down the yields, do as much QE as he likes, but in the end the forces of the markets (and the actions of the Fed) will assert themselves and completely overwhelm King Cnut (Orr) desperate attempts to cheat the market .

Yep. The tide is inexorably gong out and then we'll see who has been skinny dipping.

All the central banks - including the Fed - are using QE / LSAP and other tools to hold 10 year yield between 1.6 and 2. They are acting in unison and while they continue to do so, interest rates will be determined by Govt policy not the 'market'. We are entering a new era here.

Theft by another name

Inflation is theft - pure and simple

frazz,

Sounds good, but what does it mean? Theft by whom from whom? Where does inflation come from? here, our inflation as measured by the CPI, come entirely from the non-tradeable part of the economy. In other words, it's domestically driven. So, if my local authority raises rates to fund say, a better water infrastructure, then any inflationary effect is theft by your definition. If climate change brings more extreme weather events and this forces insurance companies to reprice their risks through higher premiums, then again that constitutes theft. Really?

Which is assuming of course that all important central banks in the world have the same national interest. Ho. ho, ho. Ah yes, the complete independence of thePBOC and ECB, among others.

The way to help first home buyers is to get the prices back down.

It's that simple.

DTI and a ban on interest only mortgages would go a long way towards this goal.

'DTI and a ban on interest only mortgages would go a long way towards this goal.'

THAT IS THE REASON OF IT NOT BEEN TARGET as they may say that want housing ponzi to stop but reality is otherwise.

Proved by their action or should say inaction.

Unfortunately, the property investors groups are a very powerful wealthy influential lobby group in NZ akin to the NRA in America.

I have never been a Labour supporter but I do respect Labour for having the balls to tackle this group with their housing policies.

House price increases would do tremendous social damage to this country if it was allowed to continue,

That boat has already sailed, the damage has been done.

Yes, it’s too late now. I saw a comment elsewhere describing the situation as trying to slam the stable door shut after the stable has already been flattened by a hurricane.

correct

also our business lobby groups who should be supporting the real economy and manufacturers have been hijacked by the banks

look at business nz.....current ceo is Kirk Hope ex westpac....ex-ceo is Phil Oreilly ex westpac

do you see a pattern?

I want to like this comment a million times and more.

Do Orr and Robertson decide over a round of golf how they will set up these sort of stale-mate scenarios where 'Grant wants this but Orr says too difficult. Pythonesque stuff

More like a single malt in some swanky Wellinton Club. (if there is such a one). Shades of Yes Minister come to mind.

FHB need to stop standing on the sidelines and make the lifestyle changes necessary to get on the ladder. Too many commenters on this website keep praying for the mythical reset which gets further and further away with each month of growth. Would hate to be in their shoes in 12 months time still hanging on to Mike Kirks cherry picked numbers. Guess that is just their lot as DGMs however.

2021 FOMO with a hint of condescension. A fine vintage.

Who says FHB are standing on sidelines? You are presumptuous. . Lifestyle changes? Have you been living under a rock? Couples both working, nurses, police, all sorts of hardworking honest kiwis are being locked out. You are so out of touch it's not funny. A reset is required for the whole countries financial stability. As others pointed have pointed out there will only be money for food and mortgage.. Nothing else. So forget anyone opening a business. Every second mom and pop business will be shut down

Christopher Luxon refers these mum and pop investors as “innovative, hardworking, risk taking”..,,

We are so lost thanks to our leadership. I was really hoping he might have bought some new thinking to the party but it doesn’t look like it

It's hard work having your name on the title of property surplus to your needs, and collecting rent each week for it.

Gnx, what did you expect? from my observations his leadership bases itself on God & Son Ltd.

I was hoping but not expecting....

Luxon is a born-again Luddite. Pure neo-lib. NZ's answer to Dick Cheney (convinced of his own right-ness). God help us if he gets to be PM.

House price are so high that life style change will not help unless they stop living.

This thought though good is no more valid specially in Auckland.

I can’t agree more with this, I work a full time job, my husband works a full time and a part time job. We don’t have avocado on toast, haven’t travelled locally or internationally in the last 8 years, make our own lunches, don’t buy coffee, don’t go to cafes, no Uber eats, no dinner out, no flash purchases or anything. Kmart clothes for kids. We are living as tight as we can to pay the mortgage for a home we bought few years ago. I was so stressed trying to get on the property ladder then and I am so heartbroken for my peers now. People tell me look how much my property value went up last 2 years but all I can see is the stress and tears of those aspiring. It’s seriously heartbreaking. I don’t know how people with multiple properties get away with making such senseless crass comments. We don’t even get to breathe and enjoy our children’s childhood. What more do you want us to give up?

Having sat with a few people who have died at a young age...unfortunately paying down a mortgage isn't on their list of 'wish I did more of' when they reflect upon their lives. Yet that is what has been forced upon young kiwis by a broken financial system and people who have decided to turn 'homes' into stores of tax free wealth or passive income collection devices. #shame.

NZ has created a horrible mess for young people. Its no wonder our mental health and suicide stats are what they are.

IO, this made me cry a river. I totally understand. I have been telling my husband - let’s leave Auckland but he doesn’t want to leave his family. He wants to be around here as his dad has been battling a series of health issues which I am very supportive of and so admire but lately I have been saying let’s leave NZ. It’s just not worth it. Our mental health, like most of our peers unfortunately is not so great. It is such a sad state. This cycle needs to be broken.

What you are breathing?- the boomers will financialize that somehow if possible. Rent a breath

Climate Change Commission has entered the chat

Frazz this is a true story. My friend has recently separated from her husband. Her very well off retired parents own multiple properties around Auckland with 2 sitting empty for years. My friend has a 3 year old daughter and asked her parents if she could stay with her child in one of the homes sitting empty and get back on her feet and the answer was no.

Endless excuses from how this will make her lazy to granddaughter ruin the house and the list goes on.

As you can see the younger generation is very well supported by their boomer parents.

If that is her parents response in this situation, I can just imagine how supportive they must be in other aspects of her life. Sadly, there are more families that function like this than society likes to acknowledge.

That is disgraceful. Tell her to put them in the smelliest rest home she can find when the time comes

Yes, utterly disgraceful. Some people, whether 'family' or not, should be kept at a distance and others aren't worth having in your life, period. Healthy boundaries and relationships should be taught early and extensively in school. I've seen so much damage done, because people feel obligated to continue in abusive relationships that just destroy their mental health, ruining the good relationships that they do have and completely derailing their life.

Are you so sure about baby boomers? We remember what living in a decent society was like and many of us despair at what has been done to our country and are heartbroken watching hope being ripped away from our children. Sure there are quite a few of us who are are among these lazy greedy bastards. To me there seems rather a lot of younger folks heavily involved also. I know a couple of young chaps in their mid 30's who have made a killing and are now pretty much retired. Such an empty lazy occupation to devote ones self to, and I wonder how they will view their lives as it draws to an end. But these are the values that Ardern has sworn to uphold by never letting house prices fall.

dp

Time for a First home buyer Strike .Surely young digital connected can organise .

In 1882, on the Isle of Skye of Scotland the crofters staged a rent strike. A crazy property market was fueled by all the cash flooding into the country from the people who had made a fortune in the Tobacco and cotton industries in the USA. The government sent in troops, but the crofters stood firm. Electoral pressures including the election of rent strikers to parliament, forced the government to backed down and some legislative improvements resulted. Something similar happened again in Glasgow in 1915 resulting in some very strong changes.

There are two lessons.

1 If enough people band together and mount a rent strike, what can the government do?

2 If a party was formed to ruthlessly pursue affordable housing, elected members sitting on the cross-benches could wield enormous power to bring the government and government departments to heal. My guess is that there would be a lot of voters cheering them on from the sidelines. Since Labour's recent moves, I have been surprised at the number of older conservative normally right wing voters who have been supportive. They all know what has been going on is a rort that cannot continue.

In the end it will be the people versus the banks

Passerby,

Well put. Perhaps you should send your comments to Christopher Luxton and indeed, the entire National party.

Funnily enough ll01, back in the day when I thought there was a housing crisis, I wrote to the ever in denial JK and BE and my local Nat and never ever got a response.

In the recent past, I wrote to Jacinda and GR and only Jacinda sent a warm response saying that she has forwarded my emails to GR who is responsible for the several points and ideas I raised re housing. GR never once did.

Politicians only care once every 3 years when they want your votes and never after. As with Jacinda, even if you are well meaning and came to power with a genuine desire to help, you get consumed by the lobbyists and their blackmail.

As for Christopher Luxon, I don’t want to waste my breath on garbage. National won’t get any votes from 18+ to 40 yr olds, they keep at this for a few more years, their voter base is going to be so minuscule that they will be a minor party. So out of touch.

Every now and then you can get a message, salvo in this case, that says it all. Bravo!

So you are basically stuffed for life?

I hope not, and I’m on the property ladder (hate that word). I’m very worried however for people my age who are not in the property ladder and ones a bit younger. I feel like they are being stuffed and ofcourse worried for my kids when it’s their time to make their life.

It’s not just about me, it’s about generations. It’s easy for me to say I got in stuff the others, but that is how a society degrades. Humans are meant to be community based, looking out and caring for one another. When you rise, don’t be one of those who stamps on people and kicks the rest down the ladder, help the rest to rise with you. Even if you can’t help don’t hinder their progress.

I dont get it ... why do you talk as if international travel, coffees, cafes, dinners out and uber eats is your standard for happiness. Of course you get to breathe and enjoy you children's childhood. It sounds more like you're wedded to your indulgence

How about selling into this crazy market and make your killing, move into a rental and when the market crashes buy something that os less stressful ? I lived through the crash of the Japanese "bubble keizai" (bubble economy) and what I am living through now that I back in NZ gives me a strong case of deja vu. Exactly the same. And in our circle of friends we had two suicides and multiple divorces as houses bought on interest only mortgages or highly leveraged fell in value by 70%. Think also jingle mail in the U.S. You sure get to know how strong your marriage is then.

What’s your bias B727? How many rentals do you own?

IO

What significances that has to do with B727 post re FHB?

Given your numerous postings regarding property, do you rent or own your own home? That would provide some understanding to your views.

Genuine question.

B727 wants prices to increase because he owns (presumably) multiple homes. I’m renting because based on world standards NZ housing is massively over priced. It has also allowed me to invest my capital around the globe with great returns better than the NZ property market.

No doubt my bias is for house prices to fall and I’m open about that. 1) because it will be good financial stability 2) it provides some hope for future generations of nz’ers amd their mental health and prosperity.

Do the property spruikers want to be open about their biases abs hidden motives? They’re pretty clear to me but I’ve found I’m not as gullible as some other sheeples in nz.

Standing by for the lecture on how FHBs shouldn’t listen to me because I’ve been saying the bubble will burst for 5 years. Go for it P8 :-)

Do you want to tell everyone about your role with the property investor association while you’re at it?

All commentators should tell us how many rental properties they own before they give us an opinion.

A National party radio announcer in the morning should also come clean as to how many rental properties he owns.

Oh go on then, please elaborate on the "lifestyle changes" necessary to "get on the ladder".

For most that will be a plane ticket overseas.

Brock, have you considered cutting back on the 60,000 avocados per year that you eat? That may help you keep up with the housing market. /s

I have cut back to 40k. Is that not enough?

LOL - or how about growing tomatoes.

Oh go on then, please elaborate on the "lifestyle changes" necessary to "get on the ladder".

Elaboration - If possible go home or stay home with your parents as long as you can. Stop buying Apple products. Don't own a car. Stop daily coffee buying. Pack your own lunch and cook your own dinner. Don't waste money drinking in bars. I have a daughter and money flows through her hands like water! Right now she is looking to go flatting as she wants the freedom. Her costs will consume her income and more. It will be impossible to save a deposit doing what she is planning.

B727

Well said.

Fortunately large numbers of FHB have purchased each and every year. Those that have procrastinated waiting for the bubble burst as called by numerous posters for the past four years have just got further behind.

Fortunately large numbers of first bitcoin buyers have purchased each and every year. Those that have procrastinated waiting for the bubble burst as called by numerous posters for the past four years have just got further behind.

Further behind what P8? A mountain of debt?

B72,

What an arrogant pr....ck you are.

No need for slander on this website. I suggest that if you simply put as much effort into understanding property trends as feeling hard done by you may well be on the other side of the fence. I guess some people need it all done for them, very sad!

B727..why do you always come across as such a pompous piece of male appendage?

Where oh where does this mythical ladder lead.... nirvana perhaps.

First home buyers want to buy a home, as is implied by their moniker. Roofers want to climb ladders... and fireman.

That Boeing version was from the late 50s era, so does explain the archaic mindset. Plenty from that era just ended up still in our care, mostly towards terminal, still asking for medication subsidy..and? mostly attended by renters or those mortgage to the neck.

Weak, predictable & disappointing. It seems property investor mentality on the tax deductibility rule is "its just like paying an extra 1% in interest, so if your mortgage is 2% you're now effectively paying 3%". I suspect RBNZ will see it similar and continue to do everything they can to keep rates low.

Yep a lot of the new measures will not find the target. A self funding property investor will not be affected and for those needing finance, well it’s still nets out cheap doesn’t it. Holding a property for another five years not all that inconvenient probably. Doesn’t sound like interest only mortgages are to be addressed and investors using a company for that business will still borrow at household mortgage rates rather than commercial company rates. So as it washes out, the tides of it all, have not changed all that much imo. Status quo will just burn on.

It's not just us: https://www.theguardian.com/business/2021/apr/01/how-do-we-fix-the-uk-h…

High asset prices are a problem everywhere (although arguably the price of stuff is less relative to the price of financial assets). Recently there has been much talk of high house prices in the US too. It’s easy to get caught up in our Kiwi snow globe and think that there’s an organised property lobby like the NRA and greedy investors are behind it all, but we in a globalised financial system where New Zealand, in reality, just goes with the tide like flotsam.

Yeah but if you look at how much NZ house prices have increased in NZ over the last 40 years vs those in the USA - we're completely out of control in comparison.

that point has been illustrated somewhat in the USA by CV19, the flight from the cities. People have found they can purchase homes with sections very cheaply in satellite townships compared to their city apartments. If they can work from home even better. Even then a two hour drive off peak back to the city is no great challenge or problem over there and quite often rail is available too.

Real Shame if RBNZ finds excuse to not ban or restrict interest only loan.

Real intent is exposed which is not using the best available option to target speculative demand as interest only loan supports and promotes speculater.

It's probably one or the other with interest tax deductibility and interest only loans. To do both at once seems harsh. I guess banning interest only for those who don't have a pressing need could be phased in slowly. I suspect the banks may start to get a bit reluctant to renew it when the interest only period expires.

Zach...question is, apart from unbridled and irresponsible greed, why the banks ever allowed interest only loans in the first place.

Wow...seriously this what behind the door understanding is between Mr Orr and Mr Robertson OR all the crying and shouting by so called investors lobby has done the job.

Interesting and shameful though expected but still ....

I'm not sure why no interest deductions were implemented before stopping interest only loans. Having to repay principle over an average maximum term of 25 yrs, out of income after tax is the bigger chunk of money.

Further if you really want to favour first home buyers, reduce the term of borrowing as you age. $1m in 30 yrs is a different proposition to $1m paid back in 10.

Rents only cover interest payments on current house prices. Other costs also rising fast so investment already needs a sharpened pencil to stay in the black. Can only put the brakes on.

If this article is correct it shows that the entire set up has systemic issues and is focussed on the wrong things.

Which is directly responsible for causing pain and suffering for the people it is meant to be protecting (in the form of the increasing wealth gap, and the intergenerational poverty trap that we are seeing creeping up into the bottom of the middle class now).

FHBs must be allowed to take more risk to get into the grossly over inflated property market. As they will gamble more / work harder to stay in. What benefit does allowing investors take more risk have for society?

We have already pumped millions into filling the boots of people already in the property market with extremely low interest rates. If the RBNZ can do that they can send a little bit of help in the direction of those desperate to own their own home.

RBNZ are lazy fat cats and articles like this make me genuinely angry.

Have been observing how likes of Orr's and Robertson's play dirty and have been vocal that Jacinda Arden is lying when she says that have no silver bullet. In absence of Silver Bullet anyone would use the one nearest and that is Interest Only Loan.

Since the earlier announcement by government have been commenting that reference of Interest Only Loan and DTI is for effect only and trying to delay and avoid.

Do this people not realised that in today's time of instant news and social media where views can be expressed and exchanged, hard to manipulate and they now stand exposed.

Why have we got 25% of OO on interest only? Are they just using their primary residence as an equity bank to purchase investment property?

Correct. We were offered the opportunity to do this when looking to purchase a new house while keeping our current house. Put most of the mortgage onto our current house and slap it on interest only, meaning a lower amount on P&I. The cash flow impacts would have been amazing.

It's that kind of thing that the new law stamps out completely.

A lot of them will be revolving credit. But equally I have talked to a couple of people who bought their first home on IO terms - they literally couldn't afford to buy otherwise. Dangerous stuff

"They acknowledged the RBNZ could restrict the use of interest-only mortgages on a bank-by-bank basis as a “micro-prudential tool”. But if the RBNZ was to implement restrictions on a system-wide basis, which is what Robertson’s asked it for advice on, it would be considered a “macro-prudential tool”. And Robertson would need to give the RBNZ permission to use it."

This a game between Robertson an Orr. Robertson is unwilling to do anything without advice in this context but when it comes to interest tax deductability prepared to do something with little or no advice.

I'm quite convinced Labour has a coterie of outside financial advisors from whom its taking advice or at worst they are calling the shots.

The cabinet, Robertson and RBNZ are playing with serious matters and its many New Zealanders who will and are suffer from it. The Nats wouldn't be any better either.

Worth more than a trillion dollars, or about four times the value of New Zealand’s annual Gross Domestic Product (GDP), the housing market effectively is the New Zealand economy.

The all to visible symptom confirming rent extraction undertaken primarily by the Australian owned local banks.

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $301,450 million (60.46%) of total lending) as of February 2021 - source.

GDP qualifying business lending was down 4.1% annually.

Those stats are a great synopsis of the state of our economy.

The economy is all about extracting rent through the real estate sector, the financial sector, the health insurance sector, monopolies and the infrastructure sector, to benefit the few.

This is why the future is getting worse and worse for young people each year. If you were 'established' (i.e. homeowner, with kids etc) before 1998, those people think NZ is great. Often mortgage free, with the boat and caravan, possibly a rental and gaining passive income from younger people.....For people who were not in that camp (entirely not their fault), those people are finding NZ a hell hole of expensive housing and low wages.

We have a massive misallocation of capital in this country and its going to be a very painful experience transitioning away from that (and history suggests it will happen).

The way interest rates have been manipulated the last 30-40 years has been extremely beneficial to those born prior to approx 1975 and extraordinary unfair to those born after 1980-1990. A rigged system is the best way to describe it and given what is going on in the US 10 year treasury, its possible that cycle has just come to an abrupt end.

We traded our jobs for debt, that's what "free trade" was about. China got the jobs, we got the debt.

Wages have not kept up due to the pressures of "free trade" to level global labour costs. The FIRE industry seems above government regulation due to oppressive corporate protection clauses written into trade agreements, hence the majority are financialised into serfdom, as are elderly savers, without recourse other than to down size to an out of area neighbourhood, absent family ties.

It's not over until the Washington Consensus is dismantled.- the entitled 1% are hardly in favour of this outcome.

Great overview there Audaxes.

Differe from the views above who are doing well, but can't allow themselves to see the harm.

Is this government appointed to serve lobbyist or average Kiwi.

Average Kiwi may not have lobbying voice but If and when they react, will be violent and government should act now to avoid as the responsibilty of it is with Jacinda Arden.

Not to test patience of FHB and average Kiwi.

Should wait as article mentions Likelyhood so still a chance that better sense may prevail.

Advise to Mr Robertson and Mr Orr do not play passing the parcel game anymore before expectation and advise of FHB and average Kiwi helplessness and frustration turns into warning.

I can never figure out why our so-called democracy tolerates the existence of lobbyists; it seems fundamentally undemocratic, especially as their dealings with government members are behind closed doors.

If we must have lobbyists then at least all their interactions with government must be open and transparent. Why aren't the members of our political studies departments at universities crying out against this anti-democratic anomaly?

Visit the Willard hotel in Washington DC. There in the lobby sat President Grant giving audience to those needing favours and much more and thus became the original lobbyists. Original hotel burnt down, but you can still visualise the scene.

Good point. I suspect that JA is listening to the RE lobby (who are certainly vocal). Problem for her is that the average Kiwi is being pushed into becoming one of the 'working poor'. The latter group is growing and although we may not be as vocal, we are definitely becoming the majority.

That’s been my call; RBNZ would be hesitant to take any action in their May Monetary Policy Statement (I think due 26 May) which would have any effect on housing until such time as impacts of Government actions on housing market become clear and at this stage there is no apparent certainty.

RBNZ will not want to take action to undo what they have tried to achieve regarding wider economic stability and stimulus (although at cost to FHB and those with cash such as TD) and in doing so protecting jobs and businesses.

Ban the use of interest-only and top-up loans to fund additional properties and we'll put another nail in this Ponzi scheme's coffin

and cash backs too.....

should you really be taking on a massive mortgage if you don't the funds to pay the furniture mover.....

the whole thing is a rigged game to screw kiwis

Have never witnessed the resentment that can be felt now in this K shape recovery.

Governments role is very important and when resentment is at peak, government (even through rbnz) should not give options and if given should act to avoid bloodbath (which cannot be seen as now but is building).

If such a situation arises, government should not hide behind that were not advised or not aware of or did not see it comming as when it will burst, it will be sudden like puss in the wound and could be in extreme.

Still feel that Jacinda Arden government will act or advise rbnz to act or may be rbnz itself decides to act so one should wait and not prejump as also Jacinda Arden is lucky to get an oportunity of lifetime to undo the balance tilted towards rich -, in this case investors and turn NZ economy dependency away from housing alonetowards productive economy and think beyond elections and vote ( though will be hard).

Ray Dalio's recent comments:

Based both on how things have worked historically and what is happening now, I am confident that tax changes will also play an important role in driving capital flows to different investment assets and different locations, and those movements will influence market movements. If history and logic are to be a guide, policy makers who are short of money will raise taxes and won’t like these capital movements out of debt assets and into other storehold of wealth assets and other tax domains so they could very well impose prohibitions against capital movements to other assets (e.g., gold, Bitcoin, etc.) and other locations. These tax changes could be more shocking than expected.

https://www.linkedin.com/pulse/why-world-would-you-own-bonds-when-ray-d…

Reading some of these comments I think it's a case of be careful what you wish for. It's a sh$&+ situation that we are in at the moment but I don't think anyone really wants a 20%+ price correction and that's not just serving self interest, it wouldnt be good for anyone. A gradual shifting in power between FHB and investors plus a gradual improvement in supply prob the best case outcome. I'd rather have 0% HPI for the next 5-10 years than -20% then +30%

Even if 20% fall, will go back just few months and on an annualised basis will still be 20% plus gain.

Of few who bought recently, FHB may feel bad with notional loss as not selling now and are in for long term but speculators who have bought recently for fast money will be worst hit but even in them who have been in this activity number of time will survive as must have made heaps in before transaction, so if get stuck in last, is fine as 9verall will still be in profit.

Yeah I know a lot of people who want a 20%+ price correction. It would be very good for them. Based upon the average house price in NZ, that is going to be hundreds of thousands of dollars less of mortgage payments for them over their lifetime. So the bigger the fall, the better for them.

If everything else stays the same then sure, but it won't. Regardless of the high starting point a 20% correction is still severe and the flow on effects could be massive. Some people could save 000's but others will lose their jobs. Don't forget that for every buyer there is a seller, that money still flows around the economy.

Wrong roystendc. I want a 20% price reduction - and more. And I am not alone. (note: am a property owner)

I want 25 % correction.

Sorry I accidentally pressed report for this comment. For the record I completely agree with your sentiments!

I want a 20%+ price correction.

Looking forward to the lecture about how terrible it would be for me.

I want a 20% price correction - I'm thinking of my kids (and their friends) more than myself these days.

I’d love a 20% price correction. Or even better, double it.

It might cost some jobs, but if it doesn’t happen the long-term damage will be far worse. I honestly believe it’s destroying our civil society, our very national identity, and any sense of social cohesion. Landlording is treasonous at this point.

If you can't get any capital gain, and with the removability of deductions, you need a price reduction of near 40 to 50% to get suitable cash on cash return based on yield alone or a large rise in rents.

The trouble is when you let the horse bolt-on not addressing the real underlying problem way back, then any tinkering with base fundamentals of the financial model now can have a multiplier eg remove interest deductibility not only removes some yield but could stop capital gain, which only gives one or two options to fix it, further falls or rent increases. The Govt. has said they don't want to see prices or rents rise. Which leaves only one option.

I think even the most rentier apologist would agree we have had a Boom - I wonder what comes next?

How many who are locked out of the market will wait ten (plus) years for that zero house inflation to improve affordability?...and would you prefer a 20-30% crash now over a 50-60% in the next year or two?

"it would be left with little choice but to cut the Official Cash Rate (OCR) into negative territory.."

Someone posted on here last week words to the effect "The OCR has always been the determinant of interest rates here', and of course we all know (or should) "No! It hasn't"

When are we going to recognise that the economic policies tried in New Zealand and adopted by the rest of the World have failed, and they have done more harm that good?

The OCR was introduced in ~ 2000

Inflation Targeting via the CPI ~1990.

The Philips Curve from ~1960 is widely recognised as flawed. Yet it's still studied by The Fed.

All have had detriment impact on both our economy and society. That's why we are all posting about it on here, today. We all know, even those who like higher property prices, that 'something's wrong' with the way the RBNZ and the Government are running things. Throw in an archaic measure of economic growth called GDP, and we have certain failure.

The best determinant of price for anything, is an open market, free of interference.

Trying to run an economy by controlling one aspect (the cost of debt - % rates), and not others (the exchange rate, and the amount of debt issued into the system free of productive effort) cannot work in anything but the short term.

The RBNZ is there for a purpose - to smooth market gyrations and ensure the lawful running of our economy. Not to control it.

Once it does that, as it now does, it's only a matter of time until the whole lot resets. And that will be at the most inopportune of times, as these things always are.

"Well, give us an immediate solution" I'm often told. Ok.

Let the RBNZ simply control the amount of money in the system, not the price of it. The true definition of Inflation and Deflation. (Some will say 'that's what we used to do, and it's the same thing), but I'll suggest it has a lot more going for it than what we are doing today.

bw - did you see that George Gammon is filing a lawsuit against the Fed for its failure to carry out its responsibilities iaw Federal Reserve Act 1913.

https://www.gofundme.com/f/sue-the-fed

It just seems bizarre that a state run entity - like the RBNZ can pick winners and losers by raising or lower the cash rate - and those decision have a massive impact on asset pricing if you understand the theory of discounting future cash flows to infinity.

I didn't. Thx for that.

May be this is what is to come.

This type of event has never been witnessed before not the level of Stimulus - fiscal and monetary measures all under the excuse to support without taking counterstep to avoid or minimize the side affect that could play havoc in time to come by this huge measures.

Removal of LVR was a wrong decession when had plans to drop OCR to zero and another mistake was not reintroducing as soon as was evident that house price were riding in double digit on a monthly basis ( now if the fast growth stops or falls is because of law of diminishing returns and not for policies) AND NOW Biggest blunder will be to not control interest only loan in zero interest environment.

May be happening world over but our concern should be our country - our home and Mr Orr should not be allowed to get away with his whims and fancies instead what is good the country in long term.

1920’s Germany.

Well at least they could blame a crippling burden of WW1 reparation, societal upheaval threatening their established and imbued class structure, and to boot, escalating communist insurgency. No internet those days, just what the radio, papers & town hall speakers said. Like it or lump it.

"It just seems bizarre that a state run entity - like the RBNZ can pick winners and losers by raising or lower the cash rate"

I do not necessarily disagree .

However - at least the cash rate applies to all types of business equally and blindly .

How about that other state entity ( the government ) picking winners and losers far more directly and specifically by letting all but one kind of business an income tax deduction on interest costs ?

.. and do not ask me how many properties I have ( your standard response to an awkward question ) .. told you already - I have none.

paashaas...they have also picked out heroin and meth from all the products bought and sold and put measures in place to stop it. Is that your definition of picking winners and losers and are they wrong to do so? Buying more than one house is akin to ticket scalping and has the same toxic results. We need to change our mindset as well as the law. The job of the Govt is to protect the well-being of society.

Major determinant of house price increase (and hence asset growth for top 33% of pop) is banks continually increasing amount will lend at ever decreasing rates, or nil interest etc. That is, artificially driving market. Without continuous extra dollops of stimulus (cf Fed and markets) housing price growth stalls and market goes flat. Ditto quantum credit growth. Credit growth unfortunately has little if any connection to productivity growth which is the real driver of healthy growth in an economy. As Steve Keen has repeatedly stated for last 12 years, if the carousel stops, the Ponzi stops. This is what is meant by the commentariat referring to "confidence" - meaning "Fed put" or in housing terms, eternal promise and delivery of "more" from gov or RBNZ. Now the gravy train has stopped. So, back to 2019 market over next 6m, that is, flat to 5% price growth. Inflation rising and currency dropping add interestingly to the mix.

Is Interest Only Loan not a deadly cocktail with low or zero interest rate and perfect recipe for Speculators ?

It is obvious and one does not have to be economist or so called expert or even Robertson or Orr to know what they are doing or not doing.

If aim of Jacinda Arden is and was to Target speculative than controlling Interest Only Loan is the best option.

Their action or inaction on Interest Only Loan will judge, what their true intent is.

taim...well put. Exactly. May will show whether they are for real or just posturing. It will let us know whether they will continue to prioritize the rich at the expense of the poor.

(The USA) can’t pay that debt down through any realistic budget process. We, along with the rest of the countries in the developed world, are going to have to take extraordinary measures to control and reduce our debts and interest payments. There are several ways to reduce the debt, but they all amount to essentially changing the terms of the debt... Making such a prediction now seems rather stark, as (that option) will not be popular or pleasant, so is unthinkable today. But when we have our backs to the wall, we will all start thinking about unthinkable things and actually doing some of them.

(Mauldin)

Hi Jenee, If the purpose of this article was to generate reaction, it sure has been successful and thanks for highlighting and starting the debate.

Not sure if people in power will read this article or reaction that follows but is a good start and hope that more journalist / media take it up.

Agree

RBNZ can only do so much. The government should take the opportunity to look into property agents charging model. Those guys are ripping people off, big time.

Should look into property agent who plays on FOMO.

May be auction with declared reserves as will save time and money of many buyers in due deeligence and manipation by re agent.

What is this people waiting for - another month like february where house prices rose by $100000 in a month :

https://i.stuff.co.nz/life-style/homed/real-estate/124715576/increase-i…

Auctions should work to find a willing buyer, not a willing seller.

Vendor Bids should be illegal, and auctions should work the way they do (or used to!) in the UK.

If you have a property to sell, and the vendor has a reserve of $500k, the auctioneer starts the bidding at, say, "$750,000 dollars Ladies and Gentlemen. Do I hear $750k?" If no one bids - which they don't - the next price is LOWER. "Do I hear $700k? Come on buyers. We're here to sell this property today" and if that doesn't extract a bid, the auctioneer goes all the way down to $490k, and if no one has bids, THEN the property is passed in.

It's the opposite to here, where vendors bid their own property up and then have them 'passed in' and that's what the press says on Monday morning "Passed in at $750k", when it's not a real bid at all.

Agree government should look for some changes and should be prepared for hard resistance from the industry and it's lobbyist.

Chart 2. Interest-only bank loans to owner-occupiers

Wow - what a story that tells - in a word BUBBLE.

House prices were so high, hardly anyone could afford to pay both interest and principal on their residential property. So, what did the banks do in order to keep up the writing of new mortgages? Indebt them more by switching them to interest-only.

Unbelievable. You'd think the RBNZ would be looking at this data real-time and ACTING. But no.

They are acting.

It's just that the RBNZ and you and I have a different understanding of what "Financial Stability" means.

Didn't we all learn the lessons of 2008, that Financial Stability and an over indebted property market don't go together? As you write, no.

Kate when I started working for a trading bank in the early 1960s none of them (BNZ, ANZ,BNSW,CBA,NBNZ) could lend for housing and nor could they lend much outside of primary production,commerce & industry.Home lending was primarily Building Societies, Savings Banks, Solicitors. I bought my first home in 1969 courtesy State Advances & capitalising of family benefit. The RBNZ then kept lending under tight control it was called in banking circles the corset. Trading banks only entered the mortgage market when they opened internal savings banks in the 70s. You may remember that when Rogernomics took hold that banks then went on a lending splurge, interest rates got up to around 19%, lending became like iron filings to a magnet.Trouble is they didn’t know how to lend safely, sensibly in terms of collateral or even actual ability to service the debt. That all culminated in the crash of 1987, the banks wrote off colossal amounts of bad debt, and NZ lost control of the BNZ going to NAB & NBNZ to Lloyds. That though pales in comparison of the monumental pyramid scheme of debt we 8have today. Putting out fires with gasoline, hardly covers it.

Yes, a really interesting look at history, Foxglove. Thanks for that.

We bought our first home in 1979. We had three mortgages - the PO Savings Bank, the BNZ and a loan from a solicitor... each having a higher interest rate. And the BNZ wouldn't take my earnings into account, given I was a married woman without kids :-), and I was earning more than my husband at the time.

How the world has changed - and I often wonder whether for the better.

I was also working full time in 1987 (two kids down the track and the husband had taken over the child-raising work) and a number of those in my Dominion Building office at the time had borrowed money to invest in the stock market. Crazy, I know.

And yes... hard to believe that madness pales in comparison to this!!!!

Aye that first home, summer hill stone, 3 bedroom, 1 bathroom shower over the bath, laundry in a cupboard, kitchenette & living room. Think it cost $17,000 or so to build. linoleum kitchenette,bathroom, carpet lounge & our bedroom, rest varnished chip board. Saved for & did all landscaping, paths fences ourselves & ditto for standalone double garage. 1976 got another job in another city but nearly lost it as couldn’t sell the house, finance was still very hard to get for potential buyers.And then did it all over again in our new location. Virtually the same thing but a bit bigger and garage underneath as a split level. Never owned any property other than my own home, worked my way up the ladder dependent on the policies of the governments of the day, and it seems now I am a public enemy! What is overlooked is that today it is very easy to borrow and often those that do cannot differentiate between money in their pocket that is earned or borrowed. Friends of our have a son in mid twenties, BCom thingy, good job & prospects & has savings but also each largely on hock, 2018 V6 SUV, trail bike & jet ski plus an almost maxed out credit card. He is looking to buy a house with partner luckily she is none of those things and has enough savings probably. In our equivalent day we just couldn’t borrow like that and that, thank god, became the habit.

First house 1975 age 23. Built it myself for so cost $25K but otherwise would have been $40k. Had savings, got SA mortgage $13k.

Double income about $10Kpa but kids so soon single income.

Mortgage to single income. 2.25 multiple.

Mortgage to double income. 1.3 multiple.

Cost to double income. 2.5 multiple.

Value to double income. 4.0 multiple

All best estimates 45 years later.

I don't think we are treating our young people well in 2021. NZ has not been managed in NZers interest.

Ironically, for all the critical comment lately on this site, including me, re Robert Muldoon’s Prime Ministership I recall him being interviewed, when he was powerless, about the rampaging reforms & restructuring of Rogernomics, he said it was setting out to destroy the foundation and values of traditional NZ society. Some say he was the best socialist prime minister that the Labour party never had? NZ is very small and very remote, its economy just flotsam & jetsam in the wake of the great powers.Perhaps Rob, had a point, look to your own first and no need to join into anything, in terms of global fashion, unless you can keep it under control. NZ is now under the control of foreign banks, dead square and centre.

As a young banker, BNZ was offering staff loans to purchase shares in the newly floated BNZ. Prior to it going belly up. Some borrowed up to 20k. I was among the few who declined such a loan. And of course, the shares!

Banks and most borrowers not interested or counting on ever paying it off... only in transferring the debt to someone else. Don't get left holding the parcel.

They seem worried to follow thru against, the tax avoiding debt stacker's. None of this group vote Labour but to hold back Dti and termination of interest only, it makes them look scared.

I guess they can keep lifting taxes again and keep pumping accommodation supplements and overpriced hotel emergency accommodation. Lets face it is nothing more important for tax dollers than protecting the ponzi. Nurses, teachers, doctors and infrastructure etc. don't really matter do they.

Clearly they don't matter to anyone. Kiwis are slowly being pushed out of NZ

Some Great Comments

The "Housing Crisis" is the result of financialization of our economy. It's lead to pervasive poverty, substance abuse, exploration, crime and lack-of-opportunity. There is a deficient of hope.

People OFTEN don't bother reporting crimes, INCLUDING VIOLENT CRIME. Targets of burglaries get more responsiveness, sympathy and advice from their insurance companies. Security cameras are the norm [if one can afford] and the smartphone camcorder the only layer-of-defense for the poor. I think it's reasonable to say the NZ Police are regular perpetrators of harassment and assault on the citizenry and amongst themselves.

The RBNZ and the Labour government have overseen the biggest wealth transfer in living memory. NZ's financial structures exist to enrich the top fourth of society, AT BEST. Anything that might cause the top 1/4 of society to suffer the consequences of greed or the painful side of risk.. apposed to infinite increase/leverage.. well, that's not allowed.

Unfortunately the result of protecting broken systems and bad bets is continued [at pace too] deterioration. People are already starting to withdraw from nightlife and the middle class (whatever that is) are keenly feeling the social disfunction. Louis the 16th retreated to the bubble of Versailles when France was falling apart:

The richest Kiwis retreat to ostentatious suburbs, real-estate only accessible by boat or plane [usually helicopters], gated communities.. even crown limos with accompanying bodyguards. At Versailles it was all about palace intrigue as the peasants suffered under an evermore burdensome yoke. SO IT IS TODAY with vain photoshoots, award ceremonies and general celebrations of wealth.

It's all very gross and shameful IMO and NO WAY to govern a country.

deep thinking, in the early hours Zack. Could I just add that a prime contributor to today’s escalating ills of our nation is the imbalance sewn early on and directly into the fabric of society summed up under the one word racism. NZ has clung for far far too long onto the colonial ideals of the mother country and that has percolated on the boil if you like, into much of our civil unrest. Sure there has been since the 1980s, the Waitangi Tribunal, financial redress but the social and psychological stigmas linger, well and truly. Influx of other ethnicities, caucasian and beyond, has hardly improved matters as it has not been well planned. If it had, some locations other than Auckland might have accommodated some of that pressure more equally. You know I look around and as mentioned before here, I cannot help but think of when I was a small boy on the farm, when mother let the lid off the pressure cooker too soon, and dinner ended up on the ceiling.

Bingo, Fox.. but you missed the recent hidden discrimination news lately past beyond that Tribunal news. Exploit of world human resources;

- 140yrs ago, the British took Indian as workers for sugar cane business in Fiji. To date? those Indian never been acknowledge as 'Pasifika'

- C19 from last year, to date most Kiwis just started to hear that there were annual imported workers into NZ enslavement industries.

- 2013-2018 within 5yr census the Asians ethnicity grew by 350-400k, third largest ethnicity.. BUT? support is only for the rest.

- NZ may decide to keep on and on about Maori or Pasifika support.. but I think the day of reckoning of those Asians import migrants healthworkers, being enslaved, sidelined, not getting any jobs/promo.. just to mop the rest home floor etc. coming closer - work strike is on card being discussed. Ssssh...

Trying to control asset prices is like trying to control Covid. You can attempt to intervene but ultimately forces beyond your powers will prevail. The real problem for housing is all the cheap money. But if you take that money away, it will be time for the soup kitchens. US Federal debt is around 130% of GDP. It is only sustainable through low or perhaps even negative interest rates. I love this site https://usdebtclock.org/#

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.