By Bernard Hickey

Economists and the Reserve Bank broadly expect the Official Cash Rate (OCR) and floating mortgage rates to rise around 2% over the next two years, while house prices are expected to rise in line or slightly below inflation of around 2%.

Fixing or floating is seen as a close call and is dependent on a borrower's view on how quickly interest rates rise and their desire for certainty, although some economists have called this week to fix because they think interest rates will rise sooner and higher.

Most economists expect the Reserve Bank to start increasing the OCR from its record low level of 2.5% from either October 27 or December 8 and rise towards to around 4.5% by the end of 2012. BNZ's economists expect the first hike on September 15 and say floating borrowers should now think about fixing. BNZ sees the OCR rising to 5% by the end of 2012. Westpac sees the OCR raised to 6% by the end of 2013 and have also said now is the time to fix.

Stronger than expected GDP growth and inflation figures in mid July have prompted some economists to pull forward or harden up their views on when the Reserve Bank will next hike rates.See more here in Alex Tarrant's article on stronger than forecast CPI figures.

The Reserve Bank itself forecast in early June that the 90 day bill rate, which is typically around 0.2% above the OCR, will rise around 2% to 4.6% by end of 2012. That would imply floating mortgage rates rising to around 7.7% within the next two years from around 5.75% now. The Reserve Bank next comments on interest rates on July 28, but is expected to leave the OCR on hold.

The Reserve Bank forecast in June that house price inflation would be in line with or below the rate of inflation over the next couple of years. It is forecasting inflation of around 2% per year over the next three years. Economists are not unamimous on house prices, though most see house prices rising by around the inflation rate over the next couple of years.

Floating vs fixing?

Before the Global Financial Crisis this was an easy decision for most borrowers because fixed mortgage rates were almost always cheaper than floating rates. But that changed after the Lehman Bros crisis because banks were unable to find the cheap and easy short term wholesale funding that helped them keep fixed rates lower.

Since then the Reserve Bank has also tightened funding rules that encourage banks to fund more locally and for longer terms than before. This has made fixed more expensive than floating and is likely to keep it that way.

Any decision to fix or to float depends on how quickly and how high interest rates will rise. Floating makes more sense if interest rates stay lower for longer, while fixing makes more sense if the OCR rises soon, quickly and to a high level.

Fixing may also make more sense for those who place a premium on having certainty about their repayments, regardless of whether they are higher than staying on floating. It's a close decision if you assume the Reserve Bank's own forecasts for the 90 day bill rate are correct.

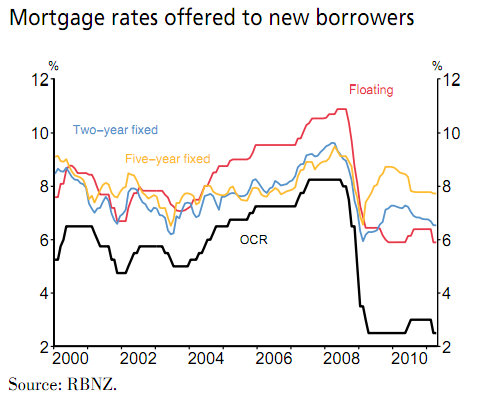

Here's the RBNZ's chart below showing how fixed and floating rates have tracked since 2000. And click here for our interactive chart showing average bank interest rates since 2002.

My view:

I think high household and government debt levels in many large developed economies will restrain global growth for some years to come and New Zealand households are being a lot more cautious about taking on new debt and spending than they were before the Global Financial Crisis.

Further financial market turmoil and a slow Christchurch rebuild may keep the OCR interest rates lower and for longer than economists think. That means I think floating is cheaper than fixing for now, but only because I have a more bearish view on global growth than the RBNZ and economists.

We have a spreadsheet which works out whether fixed is cheaper than floating, given the assumption that the RBNZ's forecast track for the 90 day bill rate is correct and given the current average mortgage rates. See the current mortgage rates offered by banks here. The spreadsheet shows the average one year rate of 5.89% is the best, the average two year rate of 6.42% for 2 years is second best with a 'loss' of NZ$78 over the two period of a NZ$200,000 mortgage, while the floating rate is NZ$880 worse off over the two years or NZ$8.50 a week.

I also think house prices will grow less than inflation and may fall further in some areas. I stick to my longer term view that house prices are still over-valued and will eventually fall to around 15% below their 2007 peaks.

They are currently around 5% below that peak and are down more than 11% in inflation-adjusted terms since that peak, which is the biggest fall in real house prices since the stagflation of the 1970s.

See David Chaston's article here.

The RBNZ's view

The Reserve Bank of New Zealand said in its June quarter Monetary Policy Statement on June 11 it expected to gradually increase the OCR over the next two years to offset a rise in inflationary pressures.

Here is its broader assessment on the OCR:

As GDP growth picks up, underlying inflation is expected to rise. A gradual increase in the OCR over the next two years will be required to offset this, such that CPI inflation tracks close to the midpoint of the target band over the latter part of the projection. The pace and timing of increases will be guided by the speed of recovery, but for now the OCR remains on hold.

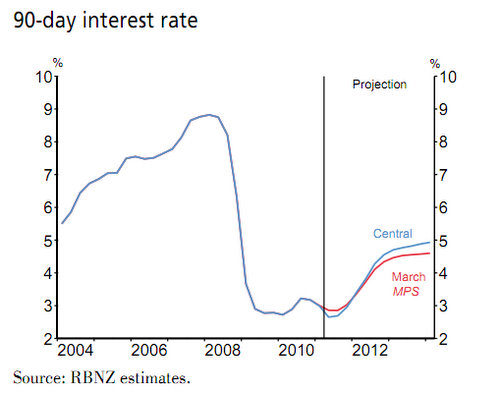

The RBNZ forecast the 90 day bill rate would rise from 2.6% in June 2011 to 4.6% by the end of next year and 4.9% by March 2014. The Reserve Bank doesn't forecast the OCR, but the market watches its forecast 90 day bill track as a close proxy of where the Reserve thinks it will be.

Here's the chart of the forecast. The red line is where it the forecast was in the March quarter monetary policy statement. Click here for our interactive chart of bank bill rates going back to 2000.

The Reserve Bank said in its June monetary policy statement it expected house price inflation at or below the inflation rate over the next three years.

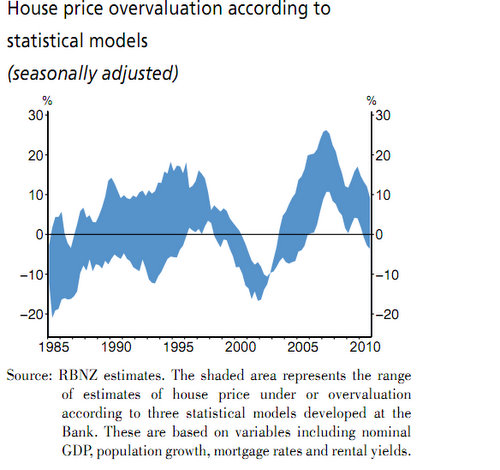

Here's its full comment with its chart below on how overvalued it thinks house prices are:

Consistent with subdued consumption, house prices are likely to increase only modestly over coming years. A number of in-house statistical models suggest that house prices continue to be overvalued when compared to metrics such as nominal GDP or rental yields (chart below).

As a result, house price increases are expected to be at or below the rate of inflation over the projection.

The Reserve Bank hasn't expressed a view on whether borrowers would be better off fixing or floating, but it notes that its ability to control the economy through the OCR is stronger when more people are floating rather than fixing. It said in June that the average duration of all mortgages was now below 6 months, compared with almost 2 years back in 2007.

ASB's view:

ASB's economists expect the Reserve Bank will start increasing the OCR on December 8. Here is their July 21 note previewing the RBNZ's July 28 announcement.

We expect the RBNZ to leave the OCR at 2.50% at the July OCR Review, with the tone of the accompanying statement likely to reflect the cautious optimism of the RBNZ. Recent developments would have given the RBNZ increased confidence that the underlying recovery in the NZ economy was gathering momentum. Added to that, there are emerging signs of inflation pressures off the back of improved demand.

These developments would likely make the RBNZ less comfortable. However, there are significant downside risks to the global growth outlook. Concerns about the sustainability of debt in some European economies and the risk of contagion have intensified. While the probability of a funding crisis in global markets looks remote for now, the RBNZ will be mindful of the significant consequences should this eventuate. In balancing the stronger domestic outlook and the risks surrounding the global economy, we expect the RBNZ will see a strong enough case for an OCR increase by December. Leaving the OCR on hold till then would allow the RBNZ to get a clearer picture of how inflation is trending and the NZ recovery is evolving.

They forecast house price inflation firming to around 3.5% by the second half of 2012.

ASB said in a July 1 note floating may be cheaper than fixing for the first year, but be more expensive after that, although it notes this all depends on how quickly the OCR rises.

Our calculations suggest floating could prove to be slightly cheaper than fixing for a year, due to the lower floating rate being paid over the coming eight months. However, for horizons beyond the one‐year mark, fixing may turn out to prove a cheaper strategy.

ANZ National's view:

ANZ (and National) Bank economists expect an OCR hike by December and increasingly see the possibility of a September 15 start. Here is their July 21 Borrower's Strategy note.

With the economy moving into expansion, the OCR needs to move higher sooner rather than later. Global events pose clear and significant risks, and may yet spell trouble. However, with inflation elevated, the RBNZ has much room for regret, and little room to manoeuvre, and we would not rule out a rate hike before December, which remains our core view.

In fact we are increasingly erring towards a September move. Put simply, the 50 basis points of “insurance” delivered in March needs to be reversed, and we can put it a strong case for it being now. However, some perspective is required. Even though the risk is that the OCR heads higher sooner or more rapidly in the near term, we need to be cautious about extrapolating this into a more prolonged cycle. As history (and the most recent Australian experience has taught us) we are still only looking at a trough to peak move of around 200bps.

Despite the low starting point, we remain mindful of near record levels of leverage, high exposure to floating rates, the growing importance of prudential policy and an uncertain global credit environment.

ANZ National's economists said in their June 24 Property focus they favoured floating over fixing for now...just. They said housing turnover was recovering but prices were "listless".

Mortgage rates were unchanged from last month. Given increased uncertainty, we favour floating for now. Broadly speaking, the rises implied by the mortgage curve are consistent with the RBNZ’s projections, and our own expectations. If it were purely a question of cost, it would thus be a line call between remaining floating, or choosing a fixed term like 2-3 years.

BNZ's economist Craig Ebert's view:

Ebert said in a note on July 25 previewing the RBNZ's July 28 rates decision it was time for the RBNZ to reverse its March 10 emergency rate cut.

While the RBNZ has a lot of counterbalancing news and risks to mention at Thursday’s OCR Review, the balance of it is increasing pressure on the Bank to begin removing its stimulus earlier than the December-point it signalled in its June MPS. While Alan Bollard is bound to highlight the surging NZD, and global risks, the domestic inflation picture should have him jawboning the door open to a near-term hike, consistent with, albeit not locking and loading, September.

We, of course, last week shortened our view to a September hike of 25bps, having long held to December. We believe a further 25bp increment will follow in October, and December, taking the OCR to 3.25%. And while the outlook gets a bit misty beyond that – which is where the global context and NZD cycle come into consideration – we believe the RBNZ will probably have to keep going next year, with a mind to a 5.00% cash rate by end-2012 to lean against strong core-inflation pressure.

BNZ Chief Economist Tony Alexander's view:

Alexander said in his July 21 weekly overview after strong CPI data that 75 bps of tightening could now be expected before the end of the year.

Last week the March quarter rate of economic growth turned out to be higher than we were thinking. This week it was the turn of inflation with the cost of living for the average NZ household rising 1.0% during the June quarter whereas a 0.8% rise had been commonly expected. The rise takes the annual inflation rate to a 21 year high of 5.3% from 1.7% a year ago and means that if your after tax income has not risen at least that proportion over the past year you are poorer in real terms.

So does the high result and high levels for numerous underlying or core measures in the context of the Reserve Bank trying to keep inflation between 1% and 3% mean that interest rates are about to shoot upward? Not at the next cash rate review on July 28, but come September 15 we expect a rate rise of 0.25% with another to follow on October 27 then another on December 8. That will mean that come the end of this year the cash rate will have risen from the current 2.5% to 3.25% and one can reasonably assume floating mortgage rates will rise by the same amount.

After that they may take a pause to see how things pan out. But come early 2013 we expect the cash rate to be at 5%. But we repeat our warning that at this point in the interest rates cycle forecasters tend to under-predict the eventual peak and borrowers would do best to run their cash flow projections assuming a 6% cash rate come the end of 2013 – though our forecast is as noted above 5%.

Alexander said it was now worth looking at fixing if the right rate came along.

If our latest forecasts prove correct then one would do better fixing one year today at 5.95% than floating and paying an average rate of 6.4%. One would do better fixing two years at 6.45% than floating and paying an average 7.2%. One would do better fixing three years at 6.99% than floating and paying an average of 7.6%.

Personally speaking then, if I were a borrower, given the recent economic data and our new forecast for when monetary policy tightening starts, I would be inclined to fix a portion of my mortgage in either the two or three year area.

Alexander also said in his July Real Estate Overview on July 26 the housing market had entered a cyclical upturn.

New Zealand’s housing market is trading at low levels with prices on average still some 4% below late-2007 peaks, construction near the lowest levels in four decades, and turnover less than half that seen in 2003/04. However there is a shortage of property now manifesting itself in agents reporting a sharp increase in difficulties finding new listings. This is happening at a time when more and more first home buyers are entering the market in an environment of increased discussion of the shortage, awareness of upward creep in rents and prices, and with interest rates set to come off their four decade lows.

While high levels of debt and low affordability by world standards will tend to constrain the extent of the housing upturn, barring a new global economic catastrophe, it appears that New Zealand’s housing market has started a cyclical upturn.

Westpac economists' view

Westpac economist Dominick Stephens said in his July 26 economic overview he expected the RBNZ would wait until December 8 before hiking, but that once it started it would raise the OCR towards 6% through 2013.

We see two factors that could leave the RBNZ cautious about earlier tightening. The first is that the New Zealand dollar has soared to new post-float highs (see below), which will directly help to contain inflation. Moreover, the RBNZ has a historical tendency to delay OCR hikes on the grounds that higher interest rates would cause a further unwelcome appreciation of the exchange rate. The second factor is the gathering clouds around the global economy.

Australian consumers’ loss of confidence could hit the NZ tourism industry, and slower growth in China and India could hurt commodity export prices. Most importantly, financial markets’ concern about the impact on European banks of the inevitable debt restructure in Greece (not to mention worries about the long-term solvency of bigger countries like Italy), has caused a squeeze in credit markets that is being felt worldwide. Credit default swap (CDS) spreads for the Australasian banks have risen to their highest level since May-June last year, when Greece first required a bailout. If CDS spreads remain high for long, bank funding costs could rise, leading to a de facto tightening independently of the RBNZ, as seen in 2009.

Barring any reversal in these two factors, we continue to forecast a December rate hike, later than the Sep-Oct start that the market is currently pricing in. The real point of difference in our forecasts remains in the extent of the tightening cycle. The RBNZ’s most recent projections suggested an OCR peak of around 4.5% by early 2013; market interest rates, despite the more aggressive near-term profile, imply a peak of around 4%. We expect OCR hikes to continue through 2013, reaching a peak of 6%.

Stephens said in a media release on July 26 now was therefore the time to fix.

We don’t expect the Reserve Bank to begin raising rates until later this year, but we do expect a reasonably large OCR cycle.

We are forecasting the OCR to rise by three percentage points over the course of two years. That’s more than markets are currently pricing in, meaning now is a good time for borrowers to fix their interest rates

Here's Westpac Chief Economist Dominick Stephen's weekly video update that previews the Reserve Bank's July 28 statement.

Here is a summary of the various economists (and my) view on interest rates, house prices and fixing vs floating.

| Forecaster | First OCR move | Peak OCR | Fix or float? | House prices |

| RBNZ* | December quarter | 4.75% by Dec 2013 | Prefer you float | <2% pa |

| ANZ National | December 8 | 4.5% | Float for now | Listless |

| ASB | December 8 by 25 bps | 4.5% by Nov 2012 | Float for short term | 3.5% pa |

| BNZ | September 15 by 25 bps | 5.0% by Dec 2012 | Fix for 2-3 years | n/a |

| Westpac | December 8 by 25 bps | 6.0% by Dec 2013 | Fix | n/a |

| Bernard Hickey | December 8 by 25 bps | 4.0% by Dec 2012 | Float | -5% |

* Forecasts implied from 90 day bill forecast track in June 9 Monetary Policy statement

(Updated July 27 with BNZ's Alexander with Real Estate market review. Updated July 26 with Westpac's call to fix now and that the OCR would rise to 6% by the end of 2013. Updaged July 25 with BNZ economist Craig Ebert's view and results of our spreadsheet on fixed vs floating. Updated July 20, July 21, July 22 with more details from RBNZ, charts, links to charts, ASB's view, ANZ National's view, BNZ's Toplis' view, BNZ Alexander's view, Westpac's view, Westpac video, Table of forecasts)

132 Comments

Agree - I cant see Bolli raising OCR when dollars allready heading for parity with US

One thing I am warry about is that the interest rates keep low for next few years as globally economy takes longer time to recover. The house price will keep rising in this situation in NZ as NZ economy is in a better position. I will lose hope to buy my house back.

Why are bank economists constantly warning of rate hikes to come? Are they concerned about us? Or just making sure we can still afford our mortgage payments? Haha

We have been hearing dire warnings of large rate hikes for 2 years or more - hasn't happened yet. I guess they'll get it right soon as they accidently hit the cycle right.

As we sold our family home last year (for 2.5 times price paid in 2002 [info for property doomers]) and paid for breaking some fixed interest segments,[mind you we were able to buy a far superior home for attainable price] then I am not in a hurry to re-fix. One should remain fluid in these uncertain times!

I know a guy who bought in Onehunga in 2001 for 275k (a 3-bed bungalow) and his house is now worth 700k. But then I know of people that bought in Milford in 2004 - a 3 bed house on a huge site, paid 550k for it and sold it just last week for 660k - nowhere near the same level of appreciation. I also know of people that bought leaky homes that have had to pay as much in repairs as what the original house was worth to fix it, and others that bought an inner city apartment for 550k that's now only worth 300k in today's market.

I think this proves that there is no hard and fast rule. Some people have done well - others have been well and truly burnt - badly. Like anyone that bought beach holiday homes in Paihia in 2007 has probably lost somewhere between 20%and 50%.

I think if you go for a solidly built home in a reasonable neighbourhood in Auckland, then in the long run (10 years plus) you'll do well. But I don't think that we are going to see 2.5 times gain anywhere in the next 10 years.

Bollard is now in a damned if he does and damned if he doesn't position, perhaps because he didn't take earlier opportunities to act in a timely manner.

I think interest rates will soon become irrelevant, as a credit contraction will diminish its importance.

We are massively overexposed to debt on residential property. If you lose your job and can't pay your mortgage, does it matter if interest on your mortgage is 5% or 10%?

With a track record like Hickeys I suggest he keep his crystal ball to him self and stick to running a website.

BHs track record is better than the mainstream econimists from my perspective. I attend formal economic updates given by leading economists and BH wins overall, thats why I keep coming to the website

he nailed that 30% drop in house prices....

Mandy

Agrred

Despite saying what I said I still think he has many things wrong but his focus on the basic, fundamentals is unfortunately for many people, correct in hindsight. He isnt perfect but I think many appreciate an unbiased and fundamental view. If he wasnt right often enough I wouldn't bother

Spirk, I totally agree with you. I think BH is one of the best at his game... he nails it often, but I like reminding him on the few occasions he gets it wrong... keeps him honest and his feet on the ground... though mostly I suspect he doesn't care what I think and who can blame him really???

;~)

Many thanks Mandalay. Feet on the ground here.

cheers

Bernard

My pleasure BH, then my job on this thread is done... hope you had a fab weekend!

Bear in mind, Bernard made his '30%' call a good 6 months before the market collpased (when Lehman went down); when the OCR was still at 8.25%, and a year before QE was brought in to stop the bottom falling out of the West's world. Would his call have proven correct without those events? Who knows. But I reckon those things changed the views of very many people in the economic world.

Good point and I think the real point is that we cannot under estimate, tampering, twinking and interfering. I think BH would have been correct had all things being equal, and we have to read into what information we get, through the site, in those terms. What will the powers to be do, if they can.

just like Infometrics nailed that 20% increase prediction by 2012 (which I recall Tony Alexander saying was a realistic possiblity).....

Well maybe not in AKLD, but in many parts of Wellington & the Hutt Valley prices have dropped 10-20% from their so called peak in 2007.

Hey Sk...without this site to parade your self serving piffle you'd be nothing..so leave The Hickster alone..he's only human and is providing a service..contrarians are far better as they always give the factual -based downside ..the upside spin is freely available anywhere in the media etc.....you know about that spin ,now don't you SK !!

you're a really nice guy Rob of the North!

thanks, nanna...i just get sick of smug bastards slagging bernard hickey off for providing a great site and daring to take a stance..he never said he was right; just his opinion...

So BH has an opinion, you have an opinion, but any one who disagrees with you is slagged off by name calling...

I think you miss the point of this site mate, it's all about difference of opinion, it's how interest.co.nz and BH get traffic through the site. The more contraversial his opinion, the more people visit the site, more advertising is sold and BH and his team make more money... jolly good show... he's going to need all the mone

Am pretty sure he doesn't need you rushing to his defence, I've met him a couple of times and he looks like a big strapping lad and he asks the hard questions even to the big boys of Fonterrorists...ummm sorry bad spelling Fonterra...

Well that's just my opinion, am I allowed to have it????

No..you're not allowed to have any opinion as you're obviously an idiot..take your cocoa and go to bed, nanna...an early night will do you good...and hopefully sharpen up your mind to the way, the truth and the life....Darth Hickey is the man..and that's that !!!

Rob of the north

Some famous quotes from the great one: "Impressive. Most impressive. Obi-Wan has taught you well. You have controlled your fear. Now, release your anger. Only your hatred can destroy me." "The force is with you, young Skywalker, but you are not a Jedi yet. http://equotes.wetpaint.com/page/Darth+Vader+Quotes

hey there, Uncle Darth...good to hear from you even though i note your voice still sounds like you're talking through a soup strainer?...mum said to say g'day....

well, it seems like the old saying " a chain is only as strong as it's weakest link " still stands true with some of the nannas you have to contend with on here...i'd vote them off the island if it were me and i was the boss like you...but i guess it provides you with mild amusement.

stay cool till after school, uncle, and may the bourse be with you !

Even BH has to come to your rescue... brilliant! I rest my case though, you're just rude, hiding behind the anonymity of the interweb!

BH is my father ...now be a good nanna and give up on this topic and go find another post to moan and groan about.....unfortunately, nannadalay...you're the weakest link and as such, have been voted off this island :-)

even more brilliant, nothing like being chastised by your Daddy on an open forum...

yawn, boring ....

SK dont be too smug about Bernard Hickey's projections . He may have the last laugh yet .

If inflation sticks at around 5% , it means the RBNZ will be forced to act radically increasing the OCR

If mortgage rates go anyhwere near 9% , many Kiwi's instalments on their homes will increase by 50%. That will precipitate a crisis.

If all of this happens at the same time as a fall in commodity prices , it could lead to the perfect strom for New Zealand . Remember commodity prices cannot be manipulated and are really subject to market forces , and prices will always revert to the average in the long run .

What will this mean for house prices

Simply , a big number of desperate sellers in the market and prices could fall steeply.

The problem is if interest rates rise that combined with the increasing bills ppl are suffering will kill our already faltering economy.....notice that un-employment is high, virtually no wage increases and certianly none of note...and still quite high private debt.....unlike previous rate rises in the past to take too much money out it isnt the same this time.

I would assume also that if interest rates rise so do CC's rates, business overdrafts, car loans, HP etc....all this is pain....then its not a case of "containing inflation" its a case of us descending into recession/depression, its a very step slide on the other side me thinks.

Commodity prices seem to be waning. The US data if it leads ours shows CPI dropping back....

House prices, same as our economy, ppl are hanging on because they either dont want to take a loss because they over-paid or are too greedy....at some point their circumstances force a bail....hmmm I also wonder at the rumours of a mortgagee backlog....banks might panic as well......

Farming? so milk solids take a nose dive and then how safe is the farming sector? I can see some ppl think that rising rates are inevitable, soon and will be hefty....if there is an un-seen tipping point and we cross it, an OCR of 0.25% wont stop the downside.....I wonder how Bollard sleeps at night sometimes.

regards

nothing like the joy of other peoples misfortune hey Boatman... ?

But I suspect the crisis you so gleefully semi-predict is NOT going to happen and Kiwis are pretty safe in their family homes and PIs will be smiling as their investments grow!

Mandalay

In my view any crunch is clearly only possible, nobody knows what will happen, but its quite possible based on the facts. More importatntly it gives a warning for many to be ready and to be ready, for a "crunch" of some kind

agree again Sprik... ouch twice in a row... I think someone spelled it out rather well somewhere on this site and if I find it I'll give them the credit - "bulls make money, bears make money, but pigs get slaughtered" Aint that the truth?

Bernard: you say house prices currently down around 5%, obviously using qv index data, which is good. Now inflation bewteen 07 and now is around 14%, correct? Giving around 19% decline in real terms?

The only service he is providing is for himself - creating worthless provocative and consistantly incorrect predictions which you fools lapup driving traffic to this website - can't fault him for that.

I can fault his gormless 'followers' however.

Your emperor has no clothes.

Whenever bottom of the barrel "investors" hear someone claim that property prices are heading up they accept it as a self evident truth and utter gospel, but when someone reports negative property news you bottom of the barrel "investors" jump up and down about how the information is wrong and stupid.

Poor old SK the RE and property shill, his whole world continues to fall apart, because his whole world is property and nothing else!

LOL

So where do you think interest rates are headed?

no where, I think!

Hey but then I could be like one of the rocket scientists here in this website and got it all wrong.. we are only human, someone said..

not you chairman Moa... you're.... well... a moa...

Another person who either has a very short memory, and/or only read or remembers the 'hickey headlines...NOT the contect or details...then starts spouting.

The fundimentals we used back in 2006 told us to bail out...we did, nothing to do with BH...in fact I believe it was before BH even published....and so did a lot of other savvy investors.

Now BH is saying interest rates going up, and still over valued, well he is right, and most of his long term predictions have been damn close to spot on....Also note, BH prediction went thru to around 2018..But of coarse u would know that , right?

So dont come here, Im sure there is lots of sand to stick your head into.....I mean you could just sit back and relax knowing your property decisions are um sound.....

regards

so why do you bother coming to this website if you think it is worthless?

Ego?

Cam,

Flatlining .... if banks raise too fast too soon, then their assets (houses) will go down in value. A delicate balancing act currently.

They are trying to hurry people into borrowing, because the money is there, but people just dont want to borrow.

The bottom line is, the interest rate isnt going to go up in a large scale until the housing market turns strong.

Better stop here, otherewise my car will blow up tomorrow morning when I start it...

The big big assumption that Bernard's making here is that interest rates will only go up if we as borrowers can afford them...a big big assumption based upon past history. The facts are that interest rates will go up if inflation remains high, irrespective of our ability to survive them. And what's driving inflation ? Food and energy prices for sure, but also rampant money printing that has boosted inflation to 6.3% and heading higher in China - remember China, the manufacturing base for the world, and the country up until the last year or two assisting us by exporting deflation to balance out the inflation in the western world - that's changing dramatically with big price risies now starting to come out of China.

And what will be central banks attitude to the deterioration of the economies of eurpore, and in particular, the US - allow unemployment to drive higher, and deflation to take hold, in Obama's election year ?...fat chance. So its just a case of whether QE3 (more money printing) comes this side or the other of year's end. This is not the world that we've known in this generation.

Global interest are negative in real terms, and are bottoming - the downside is very limited, the upside is without one if the worse scenarios occur...and it that comes to be and realised, the spike in rates will be too quick to catch -

Float with those risks over-hanging us, no damn way - I fixed last week and will sleep well. How's that saying go again ? Bulls and bears make money, but pigs get slaughtered.

or more likely deflation and a depression....if its a spike and the banks say they have cash and the RB can lend if they are locked out then I cant see much of a spike before the world's economy nose dives to frankly hell...ie the equiv of the Long Depression....or we could be lucky and do a Japan.....Im betting its the former.

regards

Well Steven I'm betting its both, inflation, a spike, and then eventually deflation when money printing is given up - remember, in the decades since the world went off the gold standard there have been plenty of big recessions but never one example of deflation.....plenty of inflation which accompanys central bank growth of the monetary supply, but never deflation. Personally I'd like to survive the inflation (many won't) and then take some advantage of the deflation.

Whichever way it works its way out, for the highly indebted countries and individuals, it will be a depression...and that can be an inflationary depression, at least initially.

Im as sure as I can be that long term we have a 10 or 20 maybe 30 year global depression coming ( which sees me out :/ ) Now will we see a short term spike in rates? depends on "spike", a small bump to say 4% OCR for a year at most two? yes possible, 6%? maybe....<10% no I cant see it....straw that breaks the camels back....IMHO. Besides which at 36% for the Greek bonds its the end game now me thinks....Italy is 5 or 6%, Portugal is toast, Ireland a basket case....Eastern Europe a wasteland....Germans saying nein.....man I think the EU is just so b*ggered....Then look at the states in the US, California is a mess, and heading for a credit downgrade (finally) other states look bad as well....plus all the other problems, plus Congress playing chicken with the debt ceiling...and actually I think they will default, its what they want.....bring Obama to is knees and get him un-electable....

Now is it (the inflatonary spike) from printing? not directly as the printing is less than the private spending being withdrawn, however that seems to be a EU and US situation, it seems we see inflation caused by these two....but its CPI and not core....core I think is still flatlined. So Im not worried about inflation yet....if I see 5%+ wage agreements as common, yes OK we have a big problem Houston....but I cant see that myself......the unions can demand whatever they want I think the employers will just say lump it or quit we cant make a living....

Kind of interesting situation if Labour wins of course (and yes it still isnt that likely) the unions will be demanding "decent" pay increases so just how long will Labour's tight fiscal policy last? 2 weeks? got to wonder....

regards

Yup, I agree both the US and europe are buggered for a long time, but how will authorities respond to that ? more money printing is my guess despite the obvious inflation risk - they'll feel they have no choice. And its not just those two, China is a huge money printer as it has to do so to enable to maintain its currency peg against a sinking UD Dollar. How high could rates go here if inflation remains elevated, well it depends how elevated I quess - at the current 5.3% inflation rate, somewhere north of that number, but when rate do normalise again above the rate of inflation, mortgage rates of 9-10% will be as terminal for some borrowersas 20% rates were during the 1980'S.

Inflation happens under certain circumstances,

1) Must not be zero bound conditions (US is in that and so really is the EU, ditto japan)

2) A boom economy where more and more money is chasing to few goods, we have a capacity over-supply.

3) Low un-employment, the US's true un-employment is closer to 20% than 10%

4) Private sector spending does not contract and leave a black hole, consumer spending is 70% of the economy so we have a huge black hole to fill

5) Wage increases at or above inflation, we dont have that....

6) Energy and raw material costs are a minimal % of manufacturing costs.

7) Energy costs are less and preferably significanlty less than 6% of GDP we are at or above 6%...

All the above point to a long term trend that is not inflation but in fact deflation in terms of National GDP, the pie will overall be getting smaller....also where are all these above heading? further into deflation certainty....and all the Central banks can do is print...and yet waht do they ant to do? raise rates....making that black hole bigger.

Frankly for me its downright wierd.....everything screams deflation and depression, but right now we are seeing CPI high....driven by the money printing...can it continue with QE3? QE4? when the economy shrinks by 10% a year, thats 800billion for the US economy alone, (so you are right to question) what happens if the Fed prints 800billion a year?

I think the average voter is frankly f*cked out of sight.........

Hmm, money printing, where is that money going? its going into the banks but isnt making it to main street, instead the banks and big lenders are borrowing or using it at extreamly low rates and buying everything they can with this hot money...incl commodities.. At some point when its looking like a nose dive for the global economy they will exit their positions and we will free fall.....hence sky high interest rates I cant see happening, or if they do it wont be for long or that high, it cant be sustained....but even at 20% OCR frankly thats better than one or two decades of depression.....My grandparents lived through that and my parents were born during it...its scared them for life....its even flowed onto me....but thats good becasue Im cautious and should survive this in not to bad a shape...."bigdadddy's"? and Olly's? well they will be interesting to watch. Firesales come to mind, reading the GD history is fasinating, I suggest its worthwhile, even youtube has good bits.

regards

Steven I caught somewhere the interest rates during the great depression stayed at around 10%. I haven't seen confirmation of that though.

I think you have to look at interest rates for what they are, the cost of money. One perspective is that if there is a contraction/deflationary period, then money will be in short supply.

Flip side is the no one can afford to borrow.

Hard to say which way it will go. GFC II could wipe out most of the electronic money (>98% of M3). But we are already seeing deflation I believe, even with QEII. The money supply is shrinking because of velocity has dropped through the floor.

Hmm, need to find more info on this (10%)....I saw a comment that bonds got to 7% at one stage for the US Govn, I assume for a decent period (it was some "old guy" chuckling on how much money he made on that).....funny how investors can come out with the good ones but not mention the bad ones...sounds like fishing.....

"if there is a contraction/deflationary period, then money will be in short supply." yes, hence the term cash is king I suppose. From what I could see if you had access to cash during the recession you could by distressed comapnies at firesale prices and hence you could "prosper" .....

From what I can see there simply was no credit during the Depression, it simply was not available....kind of odd....but also who will borrow today knowing tomorrow the asset will be worth less but the debt remains? unless you can make a profit that is....and that was scarce during the GD....

I might do some digging tonight, this interests me...(excuse the pun).

regards

I researched somewhat.....from what i can see nominal US OCR was 4% or less, 1.79% was quoted at one point, but if there is deflation at 10% the effect interest rate is 12%~14%....who borrows at that rate? in a huge depression?

regards

Ok, it isn't obvious and easy to find though is it? Obfuscation?

I guess the angle I can see is that because there is minimal money available, the price comes at a premium. But of couse no one is borrowing which drives the price down. Hmmm.

Good work anyway.

Mortgage Belt - banks don't raise rates, central banks and the market does - banks just take a spread but don't set the levels.

The near zirp decisions by the RBNZ cannot continue without inflation eating away at govt real revenue theft...already punters are spending less...as prices rise and not incomes, they will be spending proportionately less every year....Bollard is playing a dangerous game of bluff.

The wise will do what they can to protect themselves from a level of inflation rising above 4% over the next year and going higher beyond that. Any ocr hike right now will not show up in the market and economy for at least 18 months. So either Bollard will have to raise higher and move faster, or he will fail to cage the beast.

The other damage not mentioned in the stupid media, is the destruction of the saving habit. So the dream by English that we will all be saving more...complete pipedream. The failure within National is that the power players think $1000 a day represents a normal wage....how bloody dumb are they?

"Almost one third of Kiwis say they are expecting difficulties meeting credit obligations in the next three months, with Christchurch residents under some of the biggest financial strain."herald

Haven't the banks done well....you really have to congratualate them you know...they farm stupid Kiwi....!

Dumb and Dumber, two well known Kiwi, believe deep down in the mashed drugged rubbish that serves them for a brain, that the banks are here to help...yes it's a laugh but there you are.

And so the advertised banking bullshit blathers out more happy family stories with lots of warm fuzzy shite pictures of mum and dad and the sprogs lapping up the new car and furniture and house and garden and holidays...whatever Dumb and Dumber can be convinced they NEED...it's all theirs and only takes a minute to collect at their local bank....

Don't ya just love the banks....real nice they are.

OCR wont go up while the Kiwi dollar is heading up.....Job's are on the line, Tourism is taking a massive hit, exporters are really worried and JK is even worried at the high dollar, the last thing they need OCR to go up more money flooding in and push the dollar even higher. My friends in IT in CHC now the overseas owners are thinking of taking the jobs back to America, as NZ labour is not so cheap now with dollar so high....you need a job to pay a mortgage that rate can be 1 percent or 10 percent you will still need jobs.

New Zealand households are being a lot more cautious about taking on new debt and spending than they were before the Global Financial Crisis.

Figures that support this?

Household borrowing in terms of debt to nominal GDP:

March 2006 - 84.45%, March 2007 - 91.30%, March 2008 - 93.91%, March 2009 - 95.04%, March 2010 - 96.30%, March 2011- 92.95%

Business borrowing

March 2006 - 34.97%, March 2007 - 38.68%, March 2008 - 40.68%, March 2009 - 43.30%, March 2010 - 39.01%, March 2011 - 37.11%

Agricultural borrowing

March 2006 - 17.84%, March 2007 - 18.80%, March 2008 - 20.36%, March 2009 - 24.34%, March 2010 - 25.30%, March 2011 - 24.00%

The only debt/gdp % that is rising is government/public debt -- from 20.14% in March 2008 to 30.29% in March 2011.

So where is the 5.4% gdp growth coming from. How sustainable is it?

FYI housing credit growth at record low 1.3%/yr in May http://www.interest.co.nz/charts/credit/housing-credit

The problem I have with debt v gdp is if GDP shrinks faster than debt is shrinking it looks like the borrowing is going up...

regards

With an expected early start to interest rate rises, strong new zealand dollar, weak immigration, tax changes affecting depreciation claims and offsetting losses against other income, baby boomers entering retirement years, rising inflation and a stagnating housing market....

Is there a perfect storm on the horizon for the New Zealand housing market?

WFF - a perfect storm, yes.

Why you limit it to the housing market, beats me.

http://www.scoop.co.nz/stories/PA0408/S00411.htm

You folk didn't even acknowledge the nettle - let alone grasp it. Stop wasting time posturing, step up to the media and state the truth - that growth is both an invalid goal, and is unsustainable in any case.

That would be telling the punters the truth.

Chamberlain went down in history as a dickhead. He wasn't, but that's his epitaph. Labour would do well to think about that.

Well its more likely to be deflation longer term....and yes to get back to historic norms we need house prices to drop 50% and yes it looks like a perfect storm. Now the ppl who bought in the mid 90s (and before you scream and shout, yes this includes me) have had a hugh windfall for zero work, and if its wiped out, no biggee IMHO. The ones i really feel sorry for are those on the treadmill for 5 or less years and have borrowed at 90%+, it will wipe them out.....and then some.....

If it goes I think its going to be big....

regards

Don't get too excited,... Proably No Rate Rises according to JBWere

"Doyle said Goldman Sach's Leading Global Indicators measure showed a worryingly sharp slowdown in global growth in recent weeks, which could have an impact on the New Zealand economy if it continued. "Momentum has evaporated," Doyle said. "If things remain this weak, rate hikes will be the last thing on Dr Bollard's mind by year end."

"We've been here before, more than once. "Those believing higher rates in New Zealand are a lay down misere should consider how finely balanced the world economy is at this juncture."

Saying something is one thing, but the data tells you otherwise, for now the inflation rate is almost 6%, hardly evidence of momentum evaporating.

The RBNZ and/or government need to do something to get it under control.

The government needs to get serious about using other measures to help contain inflation, to compliment using just interest rates, whether it's taxes or whatever.

to start with its more like 3.2% once GST is taken out....and CPI inflation isnt the same as momentum....and to set policy / controls you look at core inflation, thats about 2%....

"Under control" there is nothing to control....think of it as raising the nose of a plane to far...you get a stall and a nasty dive.......the dive is deflation and depression....oush

But if you are a saver that is exactly what you want....3% nominal interest rate, OK pay 1% tax but those dollars buy 10% more every year and thats tax free, so 11% income tax free....as a saver whats not to like?

As a debtor on say 6% mortgage thats a rate of 16%!!!! oh bugger.

regards

F^^^en hell! Economists talking sense! Economists recognising the interlinked nature of the global economy! Economists who don't somehow think NZ is going to boom as most of the rest of the world struggles!

Why I'll de darned!!!!

I agree..........

regards

FYI I've updated with BNZ's view today that a September 15 rate hike is warranted.

cheers

Bernard

Who would have thought ey?

A bank saying interest rate rises are warranted?

Rising interest rates, plus negative migration - not good for housing Tony A et al!!!!

Keeps imported inflation down,Matt, with a firm kiwi; stopping disposable income pressure, that leads to "Honey, We'd better sell the house to eat!" But one way ( higher rates and mortage payment stress ) or another ( not higher rates, and a kiwi fall, and CPI pressures) 'what can't be sustained, won't be'.

People are so jittery at the moment bollard doesn't need to raise rates, just mention that maybe he was kinda, sorta thinking about it, that'll have the same effect.

Westpac in oz predicted a ocr drop and it dropped the aud!

Tell the people in Central Auckland.. Mt Eden, Epsom, Mt Albert etc prices for houses sold in 2007 selling for 200k+ more now.. that's a huge increase.. and selling in a matter of days...

2 houses sold the other day in Mt Albert one for $1.4m the other for $1.6m thats nuts and people queing to purchase..

I think for maybe the first time average house prices are not a true reflection of whats happening...

Its because these housing people are chumps, there are more fools out there than wise people, and thats why they line up to buy. They think they are better off paying $600 a week to "own" a property than $300 a week in rent. OH BUT RENTING IS JUST DEAD MONEY, lol so what is interest then? OH IM SICK OF PAYING SOMEONE ELSES RENT, so youd rather pay disproportionate amounts of interest? The fools will continue to line up until they really realize that the jig is up. There is going to be a lot of insolvent people walking around one day, the smart ones got out of the housing game a while ago.

Sssh! Don't explain it to them, or you'll remove their reason for living!

No muppet, you fail to realise the sheeple are really just as dumb as sheep...they will always run in a mob and be in the control of one dog....when the dog woofs "buy buy buy"...the sheeple will buy...or "borrow borrow borrow" as is the case.....it's so friggin easy to farm an idiot population.

Even Parky got sucked in!

I have 3 words that made Warren Buffett the richest man in the world. Selective contrarian investment.

FYI I have updated with BNZ's latest views, including from Tony Alexander on fixing vs floating.

cheers

FYI I've updated with ANZ National and Westpac views, and updated table of views.

So put a note in your calender for January, check OCR....personally I still think its going no where...Greece isnt fixed....neither is Portugal or Italy....or any other on-going disaster you care to mention.

regards

Actually the OCR will probably need to be dropped again. So many over 25 s out of work, under employed and/or signing up for tertiary courses. Economy still fragile with no widespread 'recovery'. As someone said all is needed is the threat of mortgage rises ...

No what is needed is a real economy, where jobs come from a healthy productive sector, and policies that encourage that.

Not one pumped up by artificial consumer spending because of extended periods of low interest rates - kinda like what we have now.

From Aussie, on a "Close Up" type show ~Property Plunge.

http://www.youtube.com/watch?v=oE20DWnsEpo&feature=player_embedded

"I don't think anyone saw it coming."

UH DUUUUUUUUUUUUHHHHHHHHH!

Ya can't lose with property, maaaate!

Ive been playing around with Zillow. Ive a friend living up here and its interesting to see whats happening, play around with different areas

http://www.zillow.com/homedetails/2210-Hope-Ln-Redding-CA-96003/1522153…

I know the area this house is in if you drag your mouse over the graph you can see whats happening. Its actually lifted but it depends on whether it was a short sale or not. There are two house markets, owner selling and bank selling and the difference is huge. Im looking at farms but they are still in the clouds.

I would think the biggest problem is the destruction of the middle class. if the middle class in the USA have lost 7.6 trillion then whats it take to wipe out the Aussie banks and its ponzi financial system, 100 billion? Then what happens to NZ when the milk price tips over, its already started? A big dip has got to be due its only a commodity and prone to over production. Who's going to pay, thats what Im trying to get out of, paying for someone elses mess. I didnt borrow more than I could service, I pay a decent amount of tax but as to paying for others stupidity, don't count me in. Why would a bus driver buy a 1.56 mill house? What dork financed him. What did the RB do about it?

Andrewj. like it or not you are already footing the bill for other peoples stupidity. Leaky homes, SCF just to name two... how do you thing the poor buggers who can't afford to buy a home, even when on close to a 6 figure income in Auckland feel when they have to pay for other peoples stupidity... government bail outs for the rich... woohoo! Best part is no CGT, I love it,

- house costs 200k, it's leaky,

- pay 75k in legal bills,

- government uses tax payer money around 150k to fix said leaky home,

- home flicked off for 600k...

- 325k CG for nuthin...

got to love NZ when only being rich will do!

Now the biggest rort is in the state sector, 5 weeks holiday great pension, great job security.

5 weeks...piffle....three months on offer AJ...go teaching...if you dare!

Thought about teaching but I dont know anything, retired at 47 and 52 weeks holiday is something one gets used to.

Yeah me too...had to slog on til I was 52..what a bugger. Sod teaching past 52...recipe for an early grave.

Pension? Im not aware any state workers except pollies get a pension these days, you have to do your own thing, been that way 20 years I think....job security, Im watching ppl going....its done via "re-organisations"....guess what they are jumping on the plane to OZ....

regards

I used to live on Massachusetts ave and the prices appear to have picked up. Not bad buying when the kiwi reaches parity

I'll hang up before I bore you all.

I liked the chart, for that property, that shows everything is flatlining to falling, except the huge jump in the line that shows the vendors asking price !

Yeah, that is quite funny - and I agree with Andrew's comment below - if the flat lines and drops reflect mortgagee sales prices, then they're really in the s#it - whether we'll get there is another matter.

Kate flick that windy spot off, leave the pine nuts for someone else and go for this place,

its off observatory circle and I think its a bargin at 2008 prices, just along from the VPresident, whats his name his helicopter makes a racket but you get used to it not as bad as those windmills. NZ embassy an easy walk, lots of SS around to keep you safe in those black SUV's.

If we get to parity and it goes for 2008 prices some lifestyle blocks around here could do a swap ;-) I mean 1.6 mill, couldn't build a dairy shed for that.

Kate, just emailed it to a mate, looks like its taken, his wife took one look and said "im sick of Gumboots and the mud", and the neighbours would be of a higher standard( debatable) so long as he can flick his Fonterra shares he's going to make an offer. They will fit right in with the dog and 4x4, few chooks.

A farm around here that sold for 9 mill after getting to 6.3 at auction, he tells me the bank did a 5 years interest free deal on to get it to 9 mill. Its pub talk but interesting.

No one is going to like this but have a look at median multiples

http://viableopposition.blogspot.com/2011/02/demographia-international-housing.html{kind=link}

hahah .... we're off over there in a couple of days - I hear they're having a heat wave - sure am gonna miss our gale force southerlies here in the Ruahine foothills :-).

Doing Honolulu, then Montreal to the east coast of Canada and back down the east coast of the US, then heading inland to Pennsylvania - where we head back home from.

Will check the pad out on the way through - though I agree about the questionable neighbours. Nothing like good 'ol NZ where my neighbour is gonna deliver a few kids (likely in a howling gale) for me in our absence!

Cheers.

And its pretty cheap in NZ$, 1 think you would get it for 870k or a mill NZ, nice walk down to Georgetown and rock creek, then the national Zoo is close, so a good area lots of places to walk but not at night.

this link has the area

http://www.zillow.com/homes/washington-DC_rb/#/homes/for_sale/Washingto…

I like DC it close to lots of places and we had alot of fun there when the children were young with holidays at Chesapeake and Virginia. Also zillow is a bit misleading sometimes as banks have to buy property back at the mortgage value so they turn up on Zillow as a sale but are no such thing.

My god are we in the shit.

WE used to holiday here look at the graph, great place.

http://www.zillow.com/homes/Saint-Michaels-MD/47520_rid/

in the 80's they seemed soo much richer than us, now we have caught up, must be the dairy boom. We should all move and take the place over. iTs an easy drive from the place in DC we could be like the Clampets.

And look at the cost of a 4bed/2bath modern home under $200K;

Same price in Palmy - 3bed/1bath (90m2) on less than a 300m2 plot of land.

http://www.trademe.co.nz/property/residential-property-for-sale/auction-393630366.htm

Sumthins gotta give.

I dun know ,I mean ones in PALMERSTON NORTH and the other is in one of the most attractive places on earth were you can walk out the door and go sailing, eat a few crabs and shoot deer and Canada geese from your back door, who wouldnt go for palmy. And the average wage in palmy must be,like, 3 times what you would earn in Maryland. Think you better look around PA to get a real comparison, then you better watch that Clampet movie again.

Be fair - I've got possums galore for game, gorse to keep me occupied in my spare time and one of the world's most polluted rivers on the planet to take the vistors to - not to mention standing under a wind turbine --- now that's a real thriller.

Oh, and I forgot - there's also the world famous Mt Cleese;

But hey, it's home and I gotta admit, I can't wait to get back and I haven't even left yet!

You should see a doctor about that, they can treat you for palmerstonitis now.

Did you click on the photos of the st michaels house I mean those views stink, take the nice quiet sub in Palmy anytime, besides those gang members are so entertaining.

:-). Indeed!

heck, Im more Patriotic than you,in May I sat at a Rodeo with my hand on my chest as they played the National anthem, admittedly if I didnt I would have been the only one not. My second daughter was christened at the Washington Cathederal. I think the house in 607 cove road saint michael was were I used to stay for weekends, I will ring up and ask, if it is then the market in the States is getting cheap, it was a fantastic place to stay we fished and hunted and had a ball.

Yeah, well having grown up there, really had enough of the congestion, the dirty winter slush, and (perhaps more than anything) the fervent patriotism towards a plutocracy that couldn't give a stuff about the average citizen. Whereas we talk about the weather here in polite conversation - they talk about their health care plans (or not, as the case may be).

Not to mention the shops, shops, shops, shops and all those $$$SALES$$$ signs screaming at you everywhere. Mind we've pretty much got there since.

Gimme my deck, a front paddock with stock browsing in the foreground, against a NZ sunset viewed across clean, fresh air and a good red from the Hawkes Bay anytime. It's funny, I'm still a US citizen - and I could live and work anywhere there - but there are so many NZ places I still haven't lived and worked yet - which hold more appeal.

dont forget Dannevirke.

I was brought up in rural NZ and always felt i was missing out on the world and all its happenings. I can live in Europe as long as the eu stays together otherwise its has to be Devon. I spent some time in India and afterwards the farm felt 'so cool' .Unfortunatley NZ has a date with destiny too.

Devon... That has to be regarded as the most twee choice one could make... Teletubby land.

Family in Somerset/Cornwall etc.... (and PN!!!).

Mind you... It would be interesting to know how many parents are following their kids these days... Lots of lost wealth.... Pack it in now please, I'm feeling homesick.... :)

Pack it in now please, I'm feeling homesick.... :)

Awww, that's nice. Our kids are dual US/NZ citizens (me the Yank and hubby the NZer). Took them alll over the US and parts of Canada when they were younger ... Vegas, Denver, Florida, NYC, Wash DC, LA, San Diego, Chicago, New Orleans, Phily etc. Always wondered whether one of them would settle there. But, nope - not even a hint of a consideration - as the Other half would say it's because we brought them up on meat pies :-).

Ive family in Cornwall, Fowey or to be more acuate Par, my wife is from nr Sidmouth,family up on Dartmoor too. Looking at going back for a bit to keep an eye on the lot, I like it more than the wife. Daughter in London one in California one waiting to go to the UK. Hope to keep the wealth intact, which means away from the GB pound.

When we first started up here - you might recall we were trying to find a place in Central HB!

Hey, speaking of views - have sent you an email - we're definitely biased but that's gotta be close to utopia? That's what we traded for this one. Wasn't easy :-).

Well as I've always said, the best thing about Palmerston North is leaving it!

Hope Bernard's not reading this, he'll come up with some absurd asumption that our houses are over priced by %30 again. Rubbish its much much more than that as the famous Jkey said' its time he got a life.'

Now I understand why bank economists are trying to make us worry about rising interest rates: It's to lock us into fixed rates and stop us moving to Kiwibank or TSB .... If we fix then they will sting us for $10,000 of so-called 'break' fees...if we try to change .... .

"Darren Pratley, chairman of the Mortgage Brokers Association, believed there was self-interest in the trading banks' view on fixed mortgages.

"A large percentage of those banks' books now are floating, not fixed, and people can shift to another lender if they want to. I think you are seeing the differences in commercial interest in those statements."

Well after having read this thread and giving the matter much thought, my advice, for what it’s worth, is for all the bank economists and Bernard too, to get together on a regular basis where they can all have a good long hard look at each other’s crystal balls.

that's porn isn't it?

Hello

The banks have wheel barrows off money, but the market is still quiet.The peasants are still not brave enough to borrow money as the job situation is not good.How can you put up the rates when everything is going up.Its funny how nobody is talking about ETS tax,this combined with the CGTax talk.The Ma an Pa kettles can't afford to pay any more increases,having low rates has been the best thing in years for families.

Bollard knows that working people are hurting,keep house loans low on the family home.

What do you think

OMG 121 Orakei Road just sold for 1.51Mil - 2008 CV is 1.17Mil. Went to the open home a few weeks ago and thought it might fetch 900k...I am shocked.

Don't be. There are still a few fools out there who think its a great idea to put so much money into one asset. They will learn the hard way unfortunately.

Look at it this way. When buying stocks on the Dow, you have the option of leveraging, which means if I buy a stock for $1, I am able to buy another stock for $1 because the broker will lend me money to do it, so I have $1 of sotck that I have paid for and another $1 of stock with borrowed money. It is the same principle with leveraged property if I have a 50:50 ratio, which a lot of people don't. A lot of people borrow $2 for every $1 they put it. Thats a heavy bet on one type of investment, and it means that if you are wrong that you will lose a lot more than you put in = bankruptcy for a lot of people. Its not a good bet.

Is it worth $1650 per week in floating interest? Or maybe rates are on the rise and that 8.3% for 7 years fixed looks good - so $2400 per week? But, hey, I guess if you have finance at 3.7% then it looks good at $1075 pw ? And all this is pre tax, plus expenses, if it's your home!

In saying that Nick, a friend of mine has described to me how it was living through the Great Depression. He lived in Mount Eden at the time and they had to scrimp every penny they could to pay their mortgage, very tough living back then I can imagine. What this tells me is that if people were having big mortgages then, and they have big mortgages now, then in 50 or 100 odd years they well have mortgages too.

BUT

The difference here that must be noted, is that this was for 4 acres, not a leaky townhouse or a house on a hill in Orakei. It was an asset worth having, and worth keeping.

Is it worth more than this place? Is it bigger and better? Wages Higger in the area?

http://www.zillow.com/homedetails/3708-Fulton-St-NW-Washington-DC-20007…{scid=hdp-site-map-bubble-photos

This is not a NZ house.

I know but you could own it for under a mil NZ. It make a nonsense of house prices in NZ. And dont say its not due comparison, the new globalised world is going to give us some surprises. This house is a walk from Georgetown, surounded by Embassy's and high net worth individuals, why is it not worth more after all interest rates are lower?

FYI I'm of the opinion that housing is still well over inflated and so are stocks, and TBH, I really think that traditional methods of investing i.e balanced portfolio, are going to have to be thrown out the window, simply because times are very very different to what they were a while ago. Now every Tom, Dick and Harry has access to huge amounts of information at their fingertips, staying ahead of the pack is even harder with smartphones and the internet.

At this piont in time Im with BH stick to floating, and his long term predictions and (mine from 2006) on house prices.

What does concern me is the bit of daj vue of the pre and Muldoon yrs ....

low inflation, static markets, printing money and inflation being primarly imported, beyond our control....We have had record low interest rates, and the 'classic ' elastic effect. Keep in mind the long term. 8.3 % ave mortgage rate...

I would not be at all suprised inflation and interest rates climb far faster than predicted, and far higher....I would not be suprised at 12 or 15% interest rates in 12 or 18 months, and stay up there for a long time....How many remeber the 25/27% mortgage rates of the late '70s / early 90s?

So I would stay at floating, for now, then hook into long term, as long as possible but below or as near as possible to the 8.30%.

House prices...well have beemn stable for now, over valued waiting for the long term ave (40 yrs) expolated out, to meet the current value....only then will we have another bouyant housing market.....On the other side, those who have low equeity (low deposit) motgages and have not as yet mamaged to pay off and/or inflated values to give them the majic 1/3 equity of what they posses, could be in trouble. This could again influence the housing market, keeping it flat with the flooding of 'need to sell'

The big issues on intererst rates is going to be imported inflation from world wide comodity shortages and the US and other major players printing money resulting in them inflating their way out of debit.

Its not all about stats, charts..its far more than that....history, long term experiance, politics, elections, and a simple gut feeling based on those.

I had a pleasant coffee with BH and DC a couple yrs back now.....I did not fully agree with much of what DC said at the time, but "inflating out of debit" has certainly since, had a great influence on my thinking since, as events have unrolled since late 2006.

Now updated with ASB's new commentary sticking with December 8 first OCR hike despite the market moves.

Also updated with detail on fixed vs floating. Our spreadsheet ,which includes the RBNZ's rate hike track, says one year fixed cheapest, then 2 year fixed and then floating. My pick though (for what it's worth) is slower and lower OCR hikes because of global uncertainty, high currrency and deleveraging.

cheers

Bernard

Bernard all you need to do is phone the bosses of the big four...ask them what they intend telling AB to do...the Stone Cutters rule. JK and BE are just puppets in this greater game of 'farm the Kiwi'.

We need a steady and certain shift away from being a debt loaded wreckage to an economy with excess saving. It's not going to happen because the banks won't allow it.

Wolly: done and dusted. weeks ago.

FYI have updated with Westpac's Dominick Stephens saying fix now and that the OCR will rise to 6% by the end of 2013.

cheers

Bernard

FYI Updated with Tony Alexander's last comments on the housing market entering a cyclical upturn.

http://tonyalexander.co.nz/wp-content/uploads/2011/07/REOverview-July2011.pdf

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.