By David Hargreaves

It's genuinely difficult to work out whether one should be encouraged, or mortified, by the big numbers of young people now emptying their KiwiSaver piggy banks to buy first homes.

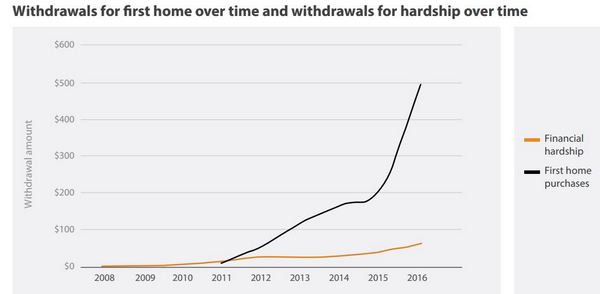

In its 2016 KiwiSaver report the Financial Markets Authority (FMA) notes "huge" growth in the withdrawal of KiwiSaver funds by members striving to buy a house.

"Nearly $500 million was withdrawn for this purpose in 2016, up from $214 million in 2015. The number of KiwiSavers making use of this facility more than doubled year-on-year, from 14,584 to 31,368. The average withdrawal increased from $14,658 to $17,896," the FMA says.

The FMA backs that up with this nifty graph, which very graphically indeed demonstrates the trend.

You can look at this trend in two opposing ways:

- The young are using an acquired nest egg to put into a bricks and mortar investment that will over time build for them the basis of a retirement fund.

- The young are stripping out funds set aside for their retirement and betting them all on one horse - the housing market.

Personally, I tend toward the second view. But equally it has to be willingly conceded that anybody who has pulled money out of savings and into, certainly the Auckland housing market, in the past few years is now well ahead of the game.

For that latter reason it's impossible to tell young people they shouldn't be doing this, because housing, particularly in Auckland, has been a one-way bet.

However, and this is always the difficult point to get across, housing doesn't always have to be a one way bet. Just because we haven't seen a crash in house prices doesn't mean there's some golden rule that means it couldn't happen. Houses are an asset. Asset values can tumble. That's why the sensible long-term investment strategy is one of diversification; so if one type of assets declines in value this is compensated by investments you hold in other asset classes.

Depending on houses

The main problem with encouraging the young to strip out their KiwiSaver accounts is that in effect this is further enshrining New Zealand's (over) dependence on the health of the housing market. All the (nest)eggs are going in one basket.

The other point is; how many of these young people will go on KiwiSaver contribution holidays once they've bought a house in order to service the mortgage - and never come back to contributing - a virtuous savings habit foregone.

The great potential thing about KiwiSaver - and it is starting to happen - is that it encourages both diversity of investment and rising levels of financial literacy in this country. On that last point, I'm afraid the travails of the finance company sector in the 2007-2010 period exposed an alarming paucity of financial literacy.

The way the Government is encouraging the young to raid their KiwiSaver accounts for a house has come as a counter point to efforts to rein in the housing market. The Reserve Bank's LVR measures, first introduced in 2013, have had the effect of making it harder for young people, with small deposits, to get a first home.

Hence the Government, which has done virtually nothing to dampen demand-side housing pressures, has tried to ease the pressure on itself with this half-pie 'solution' to the problem of would-be first home buyers getting locked out of the housing market and being, let's face it, a really bad look for the Government.

A better way?

I would prefer to see the young NOT raiding their KiwiSaver accounts. But as already stated further up in this article, it's difficult to make the argument against buying houses when that so clearly would have been the right thing to do in recent years.

Is there then a best-of-both-worlds solution?

I've long since thought in general we don't get anything like the best out of our tax system in terms of using it to encourage virtuous behaviour. It's too often used as a blunt instrument. But apply some subtlety and it can be used to incentivise.

What about a system whereby would-be first home buyers can withdraw funds from their KiwiSaver accounts to use as deposits on houses, but this withdrawal is regarded as a 'loan' from their account.

The loan is then repaid from their future income via some fairly aggressive tax rebates/discounts. Once the 'loan' is repaid, everything continues as before. This would both enable the first home buyer to 'catch-up' on where they were with their KiwiSaver savings and it would ensure they are kept in the habit and 'culture' of contributing to KiwiSaver.

There would be disagreement

The obvious argument against this is that it is one group of taxpayers sponsoring another.

What I would say is that the tax forgone now with such a scheme would be more than made up at the end by the increased retirement savings (and therefore decreased potential state dependence) of the people using the scheme.

It would be a genuine investment in the future.

Look, I'm the first to concede there might be problems with such a proposal. But alternatives to the current situation need looking at, I think, urgently. The scheme we have at the moment is a rush-job, thrown-together, idea that both has deficiencies and carries risks.

There would be a way of using the collateral of the KiwiSaver account to get Kiwis on the property ladder - without spending all the silver today. And the Government needs to have a look at this before too many young New Zealanders are committed to having all their eggs in one basket.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

32 Comments

Kiwisaver is also not a one way bet. Except for the managers and their fees.

Kiwisaver is not a single thing, you can essentially invest in whatever you like. It's certainly easier to diversify your kiwisaver than your house, I'm shifting mine to Simplicity which is not run for a profit, has low fees, and will spread my money over companies throughout the world. I fancy my chances compared to leveraging heavily into a single asset.

Simplicity, huh.

Let me guess, you also invested in Harmoney when it first arrived on the scene and also get a 3rd party to do your tax refunds?

Making financial decisions based on marketing isn't something to be proud of.

50% right, I dabbled in harmoney but most of my P2P cash is elsewhere now. I'm quite capable of doing my own tax returns. My decision was based on research, not marketing, I wanted the cheapest possible access to worldwide index funds, Simplicity is now cheaper than my old Superlife account, so I switched. I've got no desire to throw money into actively managed funds. But hey, thanks for the patronising assumptions.

Fair enough, then. Good motivation then, I guess.

It will be good to see their returns next year. I would be very surprised if there was an arbitrage, but hey we will see.

For something as long term as KiwiSaver, I would always go active.

My thinking is quite the opposite. Long term we can only expect returns of ~5-7% if we're lucky, if you're paying 1% fees that's up to 20% of your gain gone straight out the door. Lower fees are the only thing I can measure that correlates to future fund performance.

Mmmm, true. You assume that index funds and managed funds return the same amount, though?

That's what the evidence suggests, the average managed fund returns what the market returns (minus fees). There's obviously a large spread with some doing better and some doing worse, but I don't believe you can tell which is which in advance. When you take fees into account, the average managed fund performs worse than a similar index fund. You may well do better with a managed fund, but it's an extra gamble.

The evidence depends on your perspective.

There is equal evidence for both. If, however indexed funds were more efficient, we would have no managed funds.

Plus, in terms of financial fundamentals an index fund isn't that attractive.

All my reading is that index funds (overall, long term return etc etc) stack up just fine. In retrospect it's easy to see individual winners and losers. But the task is to decide now for what might happen in the future. The other evidence is that past performance in not future performance.

There are studies supporting active funds, but quite often they play on survivor bias and ignore the ~5-10% of active funds which die off each year, which tends to cut off the negative tail of their results.

Index funds are certainly growing their share and I'd be surprised if they didn't continue to do so, it's getting to the point where there is research going on to figure out the proportion where index funds become so prevalent that the market no longer operates efficiently. Active managers are using this research to show just how 'dangerous' index funds are.

Even Harvard experts lost a couple of billion on their endowment. All those highly trained experts couldn't beat an index.

"Trying to Beat the Market

What is Harvard getting for that money? Mr. Perry and others point out that if Harvard had passively invested in a standard mix of 60 percent stocks and 40 percent bonds, it would have gotten a higher rate of return — 8.9 percent over the past five years, versus 5.9 percent with its active in-house management, according to The Boston Globe.

"Everyone thinks they’re so smart they can beat the market," but few investment managers do, Mr. Perry says. "That seems like that should be a concern for investors and alumni. They are paying these supposed experts $70 million a year to lose money."

http://www.chronicle.com/article/What-a-2-Billion-Loss-Really/237965

nymad,

"in terms of financial fundamentals an index fund isn't that attractive". Can you explain that more fully? What makes indexed funds inefficient?

nymad,

"in terms of financial fundamentals an index fund isn't that attractive". Can you explain that more fully? What makes indexed funds inefficient?

mfd,

You are right about fees. with any investment,the only thing you can control is the level of fees.You cannot control future performance and what happened in the past is of no help. As a stockmarket investor,most of my portfolio is in directly held shares with no fees at all,other than initial commission and for wider exposure,I use low-cost ITs like City of London and a few others.

Errr no. I opted to pay an extra $50 on my Mortgage each week and so far I'm the winner. Anyone giving their money to someone else to "Manage" for them has rocks in their head unless your just starting work and plan to pull the money to buy a house.

So how does a young person pay back student loans, pay living costs, contribute to KS for retirement and also save a deposit for a home? Very difficult to do unless they are promoted into a high paying job.

The reality for many would be to use those savings in KS as the main form of savings plus the home start grants etc on top. If you buy a house before 40 there is still 25 years to save plus the option of downsizing if req.

Agree an incentive to continue contributions would be good. Maybe the banks could offer FHB a .1 discount of their fixed mortgage.... Yeah right?

Yes David, I too am not sure if the big Kiwisaver withdrawals are a good thing or a bad thing. I'm a strong supporter of KS and also of the idea of house ownership as good financial base for the family.

I don't think the issue of which is the best investment is core. The house you live in is not a financial issue only.

So overall, hard to decide.

Maybe the sum drawn from the Kiwisaver account should be treated as a liability to the fund , even by way of a second interest free ( or interest bearing although there could be tax implications ) mortgage registered simultaneously with a Bank Mortgage ( to keep costs in check )

This way the KS fund is somewhat protected .

Here we go again - another make-work complication

You are treating first homes as a financial investment. Given nz tenancy laws where you can be kicked out for no reason with only 42 days notice, i think youll find for most its about putting a secure roof over your head, somewhere you can safely call home.

If we have affordables houses people wouldn't need their kiwisaver for a house deposit

Yes I certainly agree. And the only real way of doing that is to get property prices to drop. It can be done, all we need to do is slow down foreign buyers by introducing a foreign buyer tax similar to Canada.

Home sales in the Vancouver area fell by 33 per cent in September compared with the same month last year as the market adjusts to the B.C. government’s 15-per-cent tax on foreign buyers, according to data released on Tuesday by the Real Estate Board of Greater Vancouver. The tax took effect on Aug. 2.

Vancouver property sales plunge as foreign-buyers tax takes effect

http://www.theglobeandmail.com/real-estate/the-market/vancouver-home-sa…

"..... slow down foreign buyers by introducing a foreign buyer's tax similar to British Columbia"

That hasn't worked so well - from a Canadian perspective

1. Vancouver volumes for September fell 33% but prices hold

however

2. August volumes in Vancouver fell 27% but volumes in Toronto (no Foreign Buyers Tax) rose 25%

They just move from British Columbia province to Ontario province which didn't do the tax thing

Depends on how you look at it. All the young Canadian's that I know are jumping up and down with joy at the news of the -33% price drop! They're all looking to head back to Vancouver in the near future to take advantage of the fact that they will soon be able to afford a home in their own city.

I wish I could say the same for Auckland and the young Kiwis here!!

Agree with most of the sentiment that drawing down on retirement savings is not the way to fund a house, or housing bubble in the collective sense.

However, most of the young Canadians you know should read the article and notice that 33% drop in SALES volume is not the same as a 33% drop in PRICES, which appear to be much the same...

If the goal of a tax is to discourage foreigners buying our property, it should just be a 100% tax on any profit. Not anything less. Any reason why profits should not just remain in NZ?

Flooding the market on the supply side as well as DTI to cut out investors on the demand side are both necessary for a price drop to more sane levels.

Thers plenty of data showing significant price drops in vancouver.

couldn't agree more CJ099. More subsidies through kiwisaver are not the solution, that'll only inflate prices more

I Disagree

1. According to Bloomberg it has had an impact on price ... from rising 1k a day to a 10-15% correction already .... sounds like it has made a difference

http://www.bloomberg.com/news/articles/2016-10-04/vancouver-s-1-000-a-d…

The tax has accelerated a slowdown that began earlier in the spring as prices reached eye-watering levels, said Wayne Ryan, a managing broker with Re/Max Holdings Inc. who oversees a team of about 100 brokers in the region. “From the peaks last April, we’ve probably seen a 10 to 15 percent correction,” in prices for detached homes, he said.

2. Solution is apply it Canada wide so they move to places like NZ that don't tax foreign buyers.

NZ has the lowest purchase tax in the world... ZERO %

house...inflation...house price goes up

kiwisaver...inflation...currency worth less

Its always interesting hearing this line of thought but the reality is anyone who knows whats going on with Central Banks and NIRP knows the world is in for potentially tens of years of next to no returns on Bonds etc ahead. There's also a very valid reason people dont invest in stock markets - in NZ because of 1987, globally because everyone knows share buybacks are now par for the course with Central Banks signalling they're getting ready to buy stocks. That is why when we arc back to houses being bought with kiwisaver at the very least a buyer knows he will get something physical against this drear backdrop.

For more info on NIRP I recommend Mauldins analysis on why future pensions are going out the door - http://www.mauldineconomics.com/frontlinethoughts/zirp-nirp-killing-ret…

I read with disdain that the author of this article suggests changing kiwisaver.

But the article backs up what I have advised my kids.

My advice is to buy a house using kiwisaver and then put in as little money as possible as they wont see that money again till there 65, if the rules don't change and the rules have already been changed more than once.

My advice is to not trust someone else with their investment money but to get involved themselves and do their own investing. Its fun and empowering.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.