By Murray Jackson*

The Reserve Bank of New Zealand (RBNZ) has asked Minister of Finance Steven Joyce to modify their Memorandum of Understanding (MoU) on macro-prudential policy to add debt-to-income (DTI) restrictions to the toolbox.

In response, Joyce has asked the RBNZ for a rigorous cost-benefit analysis (CBA) on DTI limits. The RBNZ has indicated the CBA will commence in March.

The issue is important: Excessive house price appreciation fuelled by easy credit not only has a very high cost when the inevitable credit crunch arrives, it also has the potential to create allocative inefficiency and inequity between sectors of society.

A DTI tool should be in RBNZ’s toolkit

There is increasing use of DTI and (loan-to-value ratio) LVR limits by central banks to address risks associated with surges in house prices and credit extension. The IMF says: “As part of the macro-prudential policy toolkit, these limits help to create buffers and curb excessive private sector leverage and this helps mitigate the effects of shocks on the housing sector, and thus on economic and financial stability.”

They also say: “DTI limits can offer an important complement to LTV ratios, since they tie indebtedness to household income”.

The RBNZ reports that at least 10 advanced economies already apply a limit on high-DTI lending.

DTI limits make intuitive sense because they limit debt on the basis of income which should be relatively stable, and not on house prices which might have already been inflated by easy credit. With only LVR limits applied, a house owner can borrow more on his mortgage if the house prices increase, so LVRs are somewhat circular and provide no absolute limit on credit growth.

As the Treasury has put it: “DTIs are particularly salient to financial stability as they are more reflective of sustainability of debt through the ability of borrowers to repay, and are less influenced by fluctuations in the asset prices (which bite at the point of sale) that LVRs are subject to”.

In the New Zealand context these lending and borrowing constraints are particularly important policy issues. Unlike most other countries we like to compare ourselves with, the RBNZ does not set out standards for the underwriting of housing loans, and neither does it require each bank’s lending standards to be published.

If you ask a bank in NZ about their loan underwriting standards they will tell you this is a commercially sensitive matter. However, we know from the banks themselves that they cannot prevent themselves from making risky loans.

The CEO of ANZ has said as much: “Coming hot on the heels of the Reserve Bank proposal to force residential property investors borrowing from banks to have a deposit of at least 40%, one of Hisco's key points was that this restriction ought to be even tougher. He proposed a minimum 60% deposit. Asked whether ANZ would just go ahead and set the 60% limit itself, Hisco said this wasn't a solution.”

Earlier, in 2013, Hisco also made the comment that: "At the end of the day you’d have to ask yourself really whether if somebody has only got a 5% deposit that it’s a good thing to actually put them into a home loan." If he were to have asked a depositor he would have obtained his answer.

Rather than developing rules for underwriting standards or their disclosure, the RBNZ relies on its “self-discipline” pillar, whereby the RBNZ seeks to encourage sound risk management practices in banks.

This is clearly not working. Private debt to income is growing, the proportion of rental property in the housing market has increased, banks are still making a high proportion of interest-only loans, and they are lending at DTIs of 9 to 12, even though the banks themselves think the ideal range is 5 to 7.

The RBNZ has described the lending origination policies of the banks as follows: “These origination policies of the banks are aggressive by international comparison – in the UK speed limits on high DTI loans have been established for lending above 4.5 times income with Ireland at 3.5”.

There is little in the regulations that actually requires sound risk management practices in NZ banks, they are only encouraged, relying on the “self-attestation” of bank directors that risks are managed in accordance with their bank’s “risk appetite”. There is no system for requiring bank directors to undertake training in identifying sound lending practices that are necessary for the stability of the financial system as a whole.

So, in the absence of essential hard backstops represented by meaningful DTI and LVR limits, there is no reason for a bank depositor in NZ to believe that lending of their deposits by the banking industry is being carried out prudently.

Has the RBNZ shot itself in the foot?

Housing market imbalances have seriously deteriorated since the bank first expressed its concern in 2013. The first signs of financial fragility surely must be recognised as having arrived, not least because even bank executives are saying so: “When asked about the implementation of debt to income tools (DTI), executives are in unanimous agreement that the RBNZ’s consideration of DTI measures are taking place a bit late in the cycle, as DTI ratios have already exceeded levels that would be considered ideal”. KPMG FIPS 2016.

The Central Bank of Ireland has warned from its experience in relation to the implementation of macro-prudential tools: “The worst policy mistake is to delay implementation too long, until loan levels and house prices have reached unsustainable levels. As we know all too well in Ireland, at that stage no policy option is appealing”.

The Bank for International Settlements also emphasises that: “Costs of a mistimed activation are asymmetric, as delayed action is generally more costly than a premature intervention”.

Even the RBNZ itself has expressed similar sentiments.

● “The ‘smoke detector’ or ‘macro-prudential’ role emphasises that the central bank has a fundamental responsibility to act before the first flames of financial crisis appear”;

● “It also requires the willingness and capacity to act before those first signs of financial fragility develop into a fully-fledged financial crisis”.

Surely a prudent regulator would use the tool?

Unfortunately, in an apparent effort to reduce the political impact that accompanies a change in regulations, the RBNZ is saying that that even if it obtains the DTI tool, it says “is not proposing use of such a tool at this time”.

As a result, it seems a challenge for the RBNZ to justify the acquisition of the DTI limits by cost-benefit analysis while simultaneously saying it will not use it. If the benefits of employing the tool exceed the costs, then surely a prudent regulator would use the tool?

There is evidence that macro-prudential measures only work when policymakers take a tough stance but it seems that the RBNZ is searching for a tool that works by reducing “animal spirits” with a vague threat of the regulation of credit, rather than employing a tool that actually regulates credit.

It seems that the RBNZ intends to use the tool as a bluff, unfortunately the bluff is unlikely to work as the RBNZ is demonstrating that it has little appetite to actually constrain the supply of credit (notwithstanding that housing sector credit has been growing at over 8% per annum on average over the last 20 years, and most recently was reported to be growing at about 8.7% per annum).

Thus there seems to be a fundamental flaw in the RBNZ’s use of macro-prudential tools, in that it seeks to use them on a discretionary basis. Unfortunately, it is now finding that no time is ever a politically acceptable time to place a constraint on credit.

It should now be apparent that macro-prudential tools to reduce risky lending and reckless borrowing must be permanent fixtures because there will always be strong impediments to them being implemented as they are needed.

What will be the RBNZ’s proposition and counterfactual?

Notwithstanding the above, perhaps we should assume that the RBNZ will not have a counterfactual of doing nothing. But what would doing something else look like? In addition to further modifying the LVR limits, the already agreed macro-prudential options for the RBNZ are:

● Further adjustments to the Core Funding Ratio;

● Countercyclical Capital Buffer;

● Adjustments to sectoral capital requirements.

The latter two have the promise to be very effective. For example, if they were employed to increase capitalisation requirements so as to increase the banks’ Tier One Capital from the current average of 12% (Tier One Capital to total assets) to 17%, the rate of credit growth that banks could support would be quickly reduced down by about 4% to about 5% p.a (assuming their dividends remain constant relative to their Tier One Capital). However, unfortunately, because the RBNZ has limited itself to making only modest adjustments in these regulated parameters, they have concluded that they would not have any actual effect.

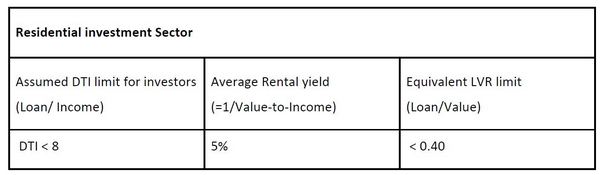

It seems that the LVR limit is the only tool that the RBNZ has any appetite to apply. As has been the recent practice of the RBNZ, the periodic resetting of the LVR limits would seem to be a practical option for the counterfactual. At least for the residential rental sector, it is straightforward to determine an LVR that would perform the same as a preferred DTI limit, illustrated as follows:

Given the rental investment sector is the most dynamic and so most potentially destabilising sector, perhaps the RBNZ can curb the extremes of the credit cycle by implementing a process that synthetically achieves most of the effect of a DTI limit: By routine resets of the LVR limit to the residential investment sector as a function of the prevailing rental yield.

Will the RBNZ look at wider economic efficiency?

In previous assessments, the RBNZ has been inclined to confine its examination of efficiency only in relation to issues within its view of its statutory responsibilities, i.e. it has confined its considerations to the promotion of financial system stability. In addition, there seems to have been ideologically driven barriers to imposing regulatory constraints on credit, even when credit expansion is damaging to society.

This is exemplified by remarks made in the Parliament’s Finance and Expenditure Select Committee where the ideological position was stated that “DTIs and LVRs distort the market” and any imposition of such limits “prevents the New Zealand’s lending system from working as it should, and any interference would favour one group of borrowers over the other”.

Such an ideological position fails to account for the extraordinarily damaging effect of money creation via credit, and that a “free market” as regards to credit can mean corruption of the free-market in physical assets and goods. Creation of money by credit is never conducive to a free market because money creation has the greatest effect on the price of the assets where it is first directed.

Effects are both intersectoral (the Cantillon effect) and intertemporal (Hayek). It is therefore imperative that the process of monetary injection via credit expansion, and its economic consequences, should be constrained from the excesses to which it is prone.

The RBNZ has expressed awareness of these issues. In 2011, in its initial investigations of macro-prudential instruments, it expressed the view: “.... Regulators have largely ignored the externalities arising from the connections between bank lending and the broader macro-economy.

In particular, less attention has been paid to the ‘dynamic externalities’ created by pro-cyclical lending behaviour: – the tendency for financial institutions, households and businesses to become overexposed during an upswing as asset prices (and collateral values) rise, and to become excessively cautious during the subsequent downturn thereby amplifying the macro-economics cycle”.

Potential additional “dynamic externalities” that arise from failing to have credit constraints such as debt-to-income limits include:

● Potential owner-occupiers being priced out of the market, preventing them from purchasing a house, and depriving them of the non-pecuniary benefits that accrue from home ownership (such as family stability, optimal maintenance and renovation, higher saving, earlier family formation);

● Disproportionate investment of intellectual capital toward property investment;

● Misdirection of the country’s credit towards activity that is either unsustainable or causing negative effects, and away from productive enterprises;

● Reduced quality of life by retirees and savers when artificially low interest rates are imposed by the Reserve Bank when the inevitable financial crisis arrives;

● Losses to savers as a result of financial instability (such as via the Open Bank Resolution, or OBR, mechanism).

It could not be a “rigorous” CBA if the RBNZ were obliged to ignore such costs to society.

If the RBNZ does look at wider economic efficiency does it have adequate models to measure it?

The RBNZ does not yet have a “flow of funds model” as a means to understanding the effects of credit growth and the likelihood of entering into debt-driven recessions. The RBNZ seems to only employ its DSGE model. DSGE models assume that sectors of the economy are always in equilibrium and so they cannot but fail to examine the potential disruptive effect of the financial system on the real economy.

Moreover, the RBNZ’s DSGE (NZSIM) model includes only three optimising agents – households, domestic firms, and import-distributing firms. There is an implicit assumption within the model that banks only operate as financial intermediaries, so ignoring how “cash in bank” can be created out of nothing by double-entry bookkeeping.

In addition, financial crises are assumed to arrive only by external shocks as opposed to endogenous instability inherent in the financial system. As a result, the model cannot hope to examine the cycle amplifying effect caused by housing investors driving the house-price-credit loop leading to financial instability and crisis, and neither can it examine all the consequential societal impacts that are now becoming so well known in the real world.

This is in contrast to the recent work of the Bank of England which has developed an agent-based model of the UK housing market to study the impact of macro-prudential policies on key housing market indicators.

The Bank of England believes: “This approach enables us to tackle the heterogeneity in this market by modelling the individual behaviour and interactions of first-time buyers, home owners, buy-to-let investors, and renters from the bottom up, and observe the resulting aggregate dynamics in the property and credit markets”. They have found how the model shows how rental investors:

● Drive up house prices in booms, and drive down prices during busts;

● Crowd out owner-occupiers from housing, reducing their market share, turning them into tenants renting from investors that bought the houses.

A path forward?

If the RBNZ conducts its CBA by examining the issue of economic efficiency and welfare of easy credit on the whole economy, using realistic models of the economy, it should find that its priority is to prevent the destabilising impact of investors on the housing market by developing a DTI limit for that sector. A DTI limit of 8 might only apply to investors buying existing homes, and thus the Minister should be alleviated from any concerns for first home buyers and the funding of new home building.

If the RBNZ is prevented from implementing the DTI tool, then the RBNZ can still achieve most of the benefit by establishing a routine process for adjusting the LVR limit applicable to the residential investment sector by reference to the prevailing rental yield.

*Murray Jackson is a commercial advisor working in Wellington in the oil and gas industry.

29 Comments

Their is no will on the part of the government as are in favour of Ponzi scheme as anything to derail it, will burst sooner than later and for them it is important that it continues atleast till next election.

Simple question to national that the media should ask them but fail :

National did agree for DTI last year (Ex PM John Key is on record) but now is evident that it was only a delaying tactics from them, for if they were serious they would have asked for the report from RBNZ at that time only and not now.

Banks lending at DTI ratios of 9-12 are like drunk drivers hurtling down the highway.

Only a matter of time until a power pole is in an inconvenient place. It's insane it ever got to this state.

Even 5-7 seems reckless to me, if that is the lower end of the scale in recent lending...Ay carumba!

What are the international examples of DTI applied to INVESTORS. The Uk only applies to owner occupiers. Big point you conveniently left out.

You say ratio of 8 for investors based on 5% yield, 40% equity.

Is this gross yield or net of rates insurance maintenance? How can maintenance be estimated? So must be a gross yield?

In my experience with banks owning several properties they would be unlikely to lend over 8 DTI taking gross rental income.

If you force them to include analysis to arrive at an income per rental net of rates, insurance (easy), and maintenance (less easy), then I still think they'd be lending to investors under 8 based on their own serviceability requirements, which generally assume a 7.5% interest rate, if you can easily sell make paymentas at that they generally happy.

This is close to how Uk treats investors, NOT with DTI but with assumed interest rates as a sort of stress test.

Prices are falling in auckland, they would need to not just stabilize but start growing at 3% plus per quarter again before DTI would ever be considered.

Meanwhile, back in Palmy, the first home buyers are trying to beat the auckland investors over very limited stock and double digit gains there will happily continue for another 2 or 3 years and RBNZ govt. media won't even notice. Fantastic buying there.

Good comment Simon. I too found the bank getting very cagey when DTI approached 8. Everyone seems to ignore that in the UK DTI only applies to owner occupiers.

Well it is national government prerogative to either allow or not to allow but yes what is annoying is their playing games with the country and not being forthright but again that is politics - Bad politics.

Auckland house prices ought to be in some way commensurate with Auckland wages, and not with the amount foreigners are able to borrow from overseas. Slapping Kiwis with DTI’s in the name of financial stability seems disingenuous. It’s just as likely during that during the next financial crisis, piles of foreigners sitting on Auckland real estate will all be watching NZD with their fingers on the hair trigger SELL button.

It seems that the RBNZ intends to use the tool as a bluff, unfortunately the bluff is unlikely to work as the RBNZ is demonstrating that it has little appetite to actually constrain the supply of credit (notwithstanding that housing sector credit has been growing at over 8% per annum on average over the last 20 years, and most recently was reported to be growing at about 8.7% per annum).

Exactly.

Central bank orthodoxy works on credibility and expectations, meaning that under ideal circumstances monetary policy declares a thing and the rest of the markets and economy create that thing simply because they believe the central bank will if forced to. If everyone believes that a central bank is all-powerful, or at least something close to it, then if that central bank declares 1% inflation to be its target 1% inflation it is very likely to find. Read more

One should surely believe the citizens are past expecting miracles from pulpably incompetent central bank officials? And yet I am still waiting, after many years, to witness any signs of public revolt.

Need policy to exit or stop overseas owners that pay no income tax in NZ, and bring in DTI on investor lending and make tax offset credits only available on new builds. Now who should we vote for to make that happen .....

We all know the real solution is for the government to take the land back off everybody and redistribute like Zimbabwe. House prices in NZ are cheap compared to overseas and our interest rates are double triple quadruple in some cases higher than U.K., US and Singapore. Interest rates are what keeps house prices in check.

I thought 40% deposit has taken the heat out if the market and its now luke warm so we should be cruising along without any hard bumps going forward. If it has not, tell me more. If it has then why are we hell bent on trying to go further and actually "kill/break" the market?

From reading various commentaries, it appears that the LVRs are reducing credit enough that some are losing the incentives to build. As this article has mentioned, they also don't restrict credit being drawn when house prices continue to increase, nor against leveraging multiple homes against each other. It's an inaccurate fix for the reasons that are stated here, and DTIs don't have so many of these problems.

For those who manage their debt well (and potentially have large income inflows, where I presume the same rules still apply to collectives), they have no ridiculous capital requirements and are unimpeded in their continued borrowing. If such a measure were considered, it should be in some part a replacement to LVRs.

https://www.squirrel.co.nz/news/musings/tighter-credit-policy-will-driv…

This guy says it's more the banks coming down on Chinese liar loans than LVR restrictions.

John Bolton has the best handle on the housing situation I believe.

I would add though that Auckland is in a unique situation this time around as is the global financial situation with maximum debt.

From the Horses Mouth - Back in January 2017

Let’s get this clear, the single biggest change implemented by banks was restricting offshore income for mortgage servicing. This rule change has effectively stopped Chinese buyers in their tracks and nothing will change that. Our (Squirrels) volume of NZ resident Chinese buyers is down around 65% and anecdotal feedback across the market is similar.

Many Asians are self-employed so (their reported) taxable incomes are generally low. That makes servicing debt difficult to prove. In the past, the way around this has been “offshore income.” Business owners will be loathe to pay more tax (report more local taxable income) simply to buy property, especially if the property market is softening.

When you say: "Business owners will be loathe to pay more tax (report more local taxable income) simply to buy property" - Are you saying such business owners are currently evading tax that is rightfully owed?

Your question would be better directed to John Bolton - I simply added the rider in brackets to make the implication of what he is saying more understandable

The proposition they are low income earners runs counter to the assumption we encourage Highly Skilled, High Value, High Net Worth migrants

The paradox is if they are earning overseas income and they are reporting it to both the banks and the IRD the amount of tax assessed is the same as if they earned ALL their income in New Zealand - they are liable for tax on overseas income - if they are playing by the rules then Bolton's comment is flawed

True, this was the case found in Vancouver when the authorities finally stood up and took responsibility enough to look: suburbs of mansions populated by people with poverty-level declared incomes, enjoying the free schooling and medical care of Canadian society while not paying taxes into it.

If Auckland market is hit too hard expect a cut in LVR to stimulate growth to prevent a crash.

Why should only those who were lucky enough to be born in certain generations be able to buy homes easily. Surely we have a better and happier community if everyone has the same opportunity to buy houses with similar DTI ratios. I paid my first house off in three years. Who can do that today?

I brought my first house in my twenties my deposit was 2/3 of the price and the loan was only 2 years my gross income so I paid off very quickly as the interest rate was double digit all on a average wage.

That can not be done today no matter how people rail on about young people spending on eating out etc and we went without.

What your saying is that you managed to save or were given 4 years your average salary to buy the place. E.g one third loan two thirds deposit, that would be about right now for most towns in new zealand

Look at the house price growth graphs. Since 2008 there has been seriously abnormal growth rate vs long term averages. Putting massive pressure on employers to pay more just so people can pay rent or buy a house. Would perfer to see housing correct vs employer/economy tanking from wage pressure. Housing is not the economy.

Exactly right - this is why the world economy is in trouble - a housing value Ponzi is the only growth area left.

Housing cant correct ... because the economic system / debt issuance would seize up.

Barfoots "At present, the market has divided around the $750,000 mark. Above this point sales numbers and prices remain consistent. Below it uncertainty has developed as to whether asking prices represent value for money, and sales numbers have fallen"

One thinks that the DTI horse has fled the stable some years ago....

Tony A has had to say sorry

http://www.stuff.co.nz/business/90090644/learn-from-boomers-comments-sp…

I wonder if he is still intending to hold his "How to win friends and influence people seminars? "

You just beat me on linking that. I guess talk of a BNZ boycott hasn't been going down well with BNZ.

I liked the 7 points he made, I thought that the surrounding Narrative wasn't the best way to present these.

I only liked 1 or 2 points the rest seemed to diverge from reality. It he'd taken a less arrogant tone and applied some personal finance math it would have been more productive. He's also detached from the fact that there are a lot of people that are just working to live and have no luxuries or spending they can cut out.

With respect to his meth lab house suggestion he understands very little about the decontamination risks or the hidden costs. He seemed to believe that it's just a run down house where you replace some timber and plasterboard and everything is fine. Most people that I know have very little experience in dealing with hazardous solvents and have no idea of the risks.

Perhaps a bank economist should be more scientific, well-grounded and not insult the bank's customers younger than baby boomers.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.