By Alex Tarrant

If you blinked, you may have missed it. But Finance Minister Steven Joyce last week came very close to saying the National government wants all Auckland property values to become much lower than they currently are.

Not in those words exactly, but that’s how I’m reading through this line put out on Thursday: “We must keep a strong focus on land supply so that section prices become much more reasonable.”

You might not think it’s much, but I’m going to put it out there: This is the closest we’ve got to a senior National or Labour politician saying it would be good if New Zealand property values fell, rather than just banging on about improving affordability while ignoring the secondary question of, ‘how much would you like prices to drop by?’

It might have been a public relations accident. Joyce might have meant to say, ‘so that new section prices become much more reasonable’ and then do an Andrew Little by saying he only wants new properties coming online to be below average prices, while the values of existing properties remain stable (and definitely not falling).

He might have meant to say he wanted ‘some’ sections to be priced more reasonably. This would allow for a get-out-of-calling-for-prices-to-fall card of saying this wouldn’t necessarily impact the values of average existing properties, as ‘other’ sections might come on line priced less reasonably to balance things out.

But he didn’t. The quote as it stands relates to all sections. Now, take a look at your latest council rating or homes.co.nz valuation – you’ll see your section/land accounts for the majority of the value of your property as opposed to the ‘improvement value’ of the dwelling you have on it.

So, when the Minister of Finance starts talking about wanting section prices to become much more reasonable, that’s news. And by the way, we’re talking “reasonable” in the sense of inexpensive, affordable, cheap, moderate, economical and equitable.

Joyce’s comment came in a press release extolling research done by Sense Partners economist Kirdan Lees on the impact of New Zealand’s land use regulation on property prices. Headline: Regulation regarding what can be built where may account for 56% of the cost of an Auckland home. (See David Hargreaves' article on it here.)

The main gist of the research indicates our land use regulation is not sufficiently flexible to accommodate increasing demand for land in particular areas. “Most areas in the cities we study have failed to accommodate more people,” Lees says.

Let’s say people moving to Auckland earmark Ponsonby as an extremely attractive place to live. Initially we’d see a rise in values as they compete to buy existing properties people are willing to sell. Rising prices would catch the attention of other local property owners, who might then consider subdividing to capture that increased demand. The increased supply would take that upward pressure back off prices.

But what if you weren’t allowed to subdivide? Lees talks about land use regulation as a tax that raises the cost of a house. “This could include a multitude of land use regulations, such as height restrictions, urban growth boundaries, minimum lot sizes, minimum parking requirements and heritage restrictions. Moreover, these regulations are often a function of the broader urban planning system, including infrastructure funding.”

Lees cites some previous research of his showing that, aside from inner-city apartments, most suburbs in Auckland (and elsewhere) accommodated very few new residents between 1996 and 2013 (the point to which the research was current to).

“We conclude there is in general only a small relationship between density and prices, certainly much smaller than if the response to high demand were sufficiently flexible to encourage large inflows. This is consistent with the findings of the other methods that there are severe regulatory restrictions that characterise most cities as type 3 cities that fail to accommodate much demand,” he says.

“Our results show prices in most cities were expensive relative to construction costs in 2012 and have only increased. Moreover, our estimates that compare the price of land with a home to the extra value from a backyard suggest land use regulations are preventing sufficient supply response to meet demand. When a house with 400m2 of land is not much different in price from a house with 800m2 of land, we can use land more effectively to produce cheaper houses.

“There are many potential welfare costs arising from such high house prices, including labour markets distortions and inhibiting productivity and resource allocation. Well-functioning housing markets with flexible supply in high-demand locations should produce a strong correlation between prices and density. We expect supply to adjust and accommodate more residents and some extra demand to push up house prices a little. But our results suggest only mixed and modest relationships between density and prices. Only a few areas, such as downtown Auckland, are accommodating more households with new dwellings accommodated on the periphery of the city.”

The recommendation: “If policy advocates are interested in reducing housing costs, they would do well to start with zoning reform.”

Joyce argues the government has made movements on that front: “The new Auckland Unitary Plan, the latest RMA reforms, the National Policy Statement on Urban Development Capacity, the Crown Building Project, the Housing Infrastructure Fund, Special Housing Areas (SHAs) and increasing the availability of Crown land for housing, are all helping to increase land supply for housing.”

So all good then? There has been some recent good news. Prices in Auckland are slowly dropping. But what if after the election that turns around again (let’s say the current coalition can reform a government)? What if the onus falls on government to do more to ensure section prices actually do become much more reasonable than they are now – as Joyce has said he wants?

Will Joyce and Social Housing Minister Amy Adams commit to greater government-led or government-financed house building work, or central government overrides of local authority zoning rules with the express intent of causing section and property values to drop into 'much more reasonable' territory? I’ll leave that for you to decide.

182 Comments

Prices will drop whether they want or not. Banks are restricting credit, buyers are cautious, speculators want out, Chinese capital influx is gone and we're at the end of the debt cycle globally. There's simply no room for more craziness even if they want.

It has already dropped. Now it WILL go up.

Absolute garbage. What in your view is the peak level of house prices to incomes. 12x? 15x? Infinity? Is yours the buzz lightyear theory of economics? We are already at 10x in Auckland. House prices cannot rises permanently in ever increasing multiples of income. This is a pretty basic proposition.

Somewhere between 20 and 30 times would be ideal. Auckland should be a high end market and houses shouldn't be selling cheap. Workers can be subsidised by employers to live in more affordable areas like Pukeno/Tuakau/Huntly/Te Kauwhata.

That sounds like North Korea to me. Are you a fan of Kim Jong Un by any chance?

I thought they were brothers

Hahahahahahahahahahaahahahahahah ah hahahahaha ha ha, you're a wag DGZ. We're very comfortably in Decile 1 of wage earners, which when converted into a mortgage buys us the best part of nothing worth buying, yet we earn many multiples over the median household income of Orakei district. We could of course take our taxable salary elsewhere, and deprive the country of a couple of teachers' salary a year.

Hahaha you sound like you're rolling on the floor laughing. Hope that makes you happy. Have you tried La Fourchette yet?

Took a look at the site, will give it a go, from the site it looks a bit more European than classic French per se, if that makes sense?

Yes I know what you mean, but trust me the flavour is definitely French and I know all their chefs are too.

Because I'm not an international jet-setter I need you to explain what you mean by "more European than classic French" and how I could/should apply that to helping my financial decision making

You are pushing the edge DGZ

Ok, so I will mark down your view as "infinity".

DGZ could easily be confused for DMZ.

But seriously. It is interesting to consider what the upper limit on house price to income ratios is. I'd suggest it 10x isn't the top, it is very close to the top.

Barring a recession, which lets face it housing could cause, I do think we will see strong income growth over the next couple of years. I don't see that raising house prices but I do think it will help them adjust relative to incomes. Don't get me wrong, I still see a correction, I'm just saying an adjustment in incomes may do some of the work.

Strong income growth....from what? There has been minimal income growth over the last 5 years, what's about to change?

I mean, I appreciate this site runs on wishful thinking, but that is going a little too far

I do not care if every property investor goes broke, it will only release more houses for owner occupiers.

The people I feel very sorry for are the first home buyers and families that have had to borrow up the hilt to obtain a house. These people will owe the banks more than their properties are worth. Even if they sell and rent they will still have a huge mortgage to pay to the banks.

The main cause of all this is of course the National Government. They have been in power now for 9 years and suddenly there is a problem with housing. Anyone would think an election is just around the corner!!!

If this Government put the brakes on house prices 6 years ago, we would not be facing a catastrophe now.

I would like houses to revert to their long term average and for the average salary earner to be able to buy the average house. I don't have a particular wish for investors to lose vast amounts of equity, but we are now in place where there are no good options, only varying degrees of bad ones. If current owners suffer massive collateral damage on the way down, then so be it, that seems to me to be the least bad outcome here.

With what DGZ, how are you expecting property prices to rise? Face facts, the top end Chinese investors are gone and are not coming back. You've been left high and dry DGZ.

Take a look at the recent auction results, most properties are selling below most price estimates in the expensive areas if they sell at all. This is simply because the top end buyers have flow the coup they're no longer investing in little NZ because we're maxed out from income ratios in comparison to property prices.

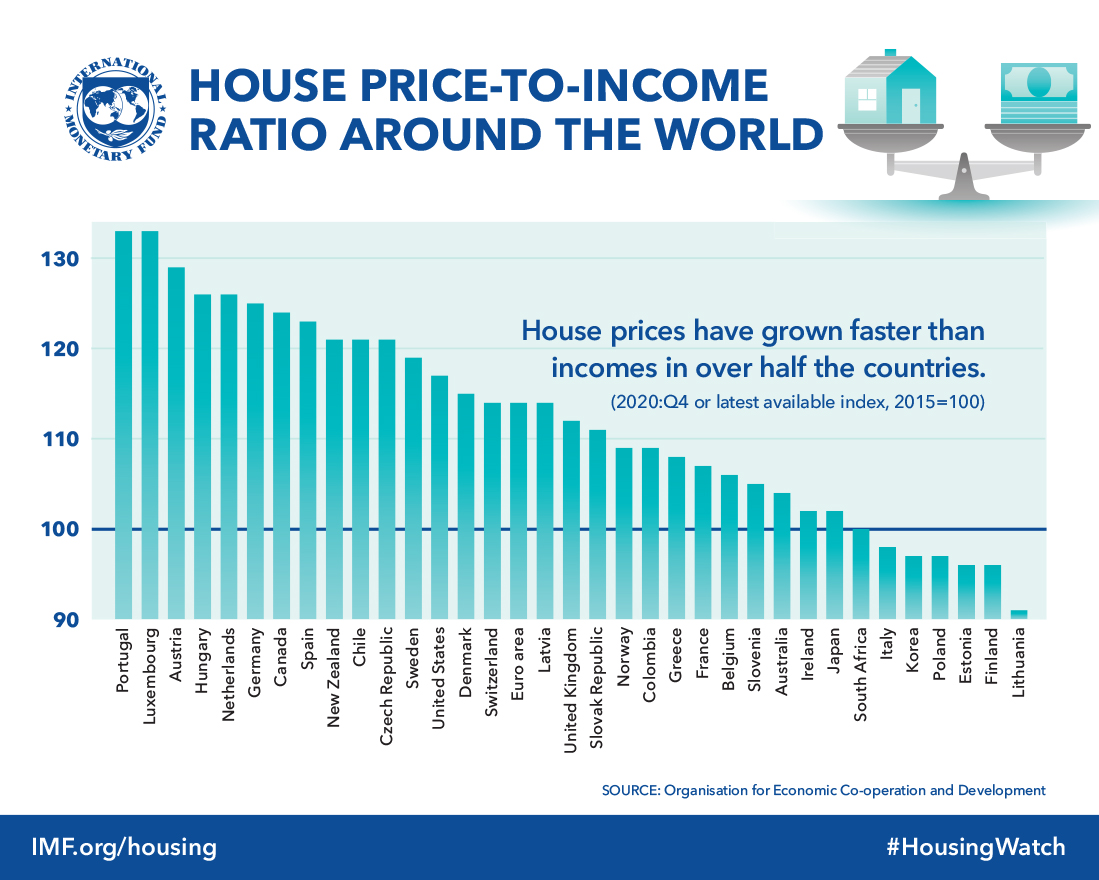

House Prices to Income Ratios Around the World

http://www.imf.org/external/research/housing/images/pricetoincome_lg.jpg

{kind=link}

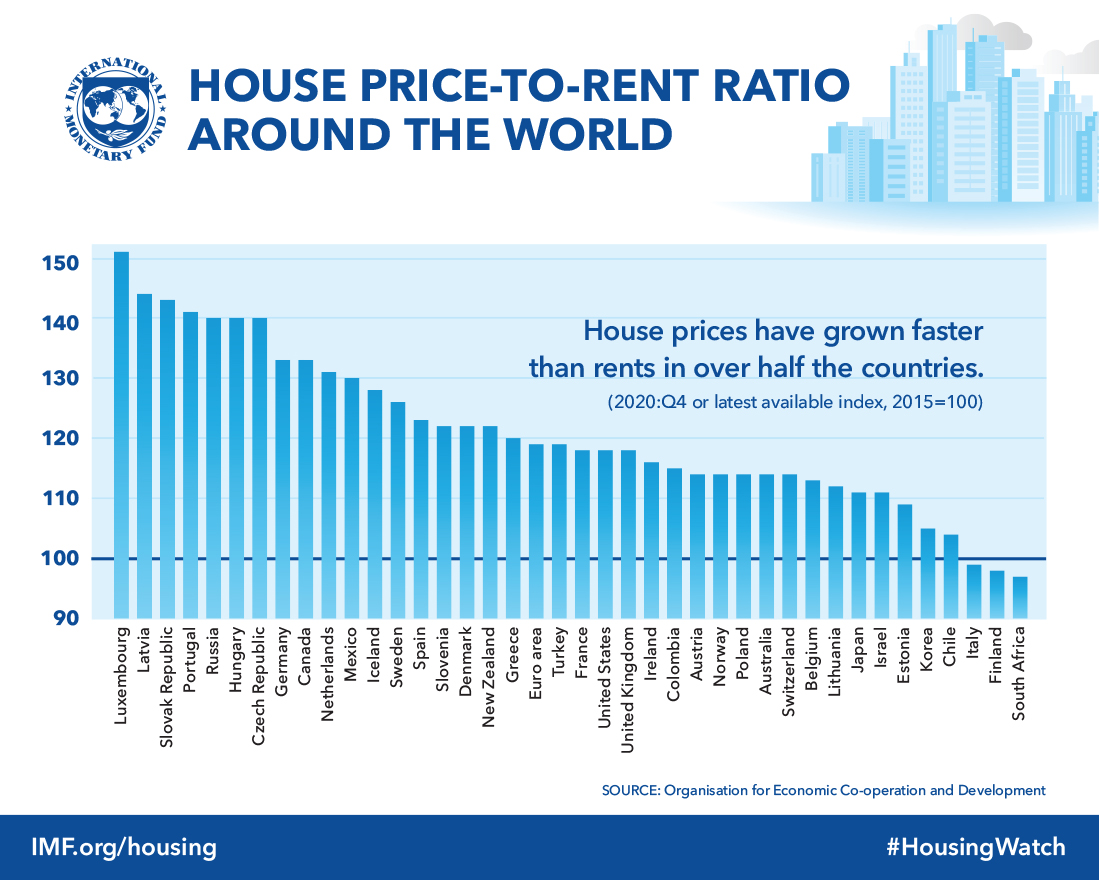

House Prices to Rent Ratios Around the World

http://www.imf.org/external/research/housing/images/pricetorent_lg.jpg

{kind=link}

Lol

Toronto House Prices Crash 192k since April.

https://www.youtube.com/watch?v=hGL0ysImPCo

Auckland Albany House Prices Dive 13.5%

https://www.stuff.co.nz/business/property/94154549/house-prices-dive-in…

The Crash Is Coming.

Oh no not again and no sponsor this time!

" There's simply no room for more craziness even if they want "

... ah come on ... this is New Zealand ... there's always room for more craziness hereabouts .... wide open sunny spaces for craziness to run about in .... most of it inside the heads of our politicians , local governments , and the RMA officials ... ever listened to Nick Smith or Phil Twyford ? .... craziness frolics and gambols happily without restriction inside those two craniums , let me tell you !

... insanity doesn't run in the house prices of Orc Land .... it bloody well gallops ... and so it should ....

Yeeeeee----haaaaaa ..... get along little filly , whooooo-heeeee ... we're all gonna be rich ..... Yabba-dabba doooooooooooo... ... rich , I tell you ..... RICHHHHHHH .... aha ha haaaaaaaaaaaaaaaaaaaaaaaaa ........

I actually think overseas buyer are waiting to see what comes of the election. If National win outright without needing NZ first, I would expect property prices to rise again

I'm with you and would expect to see a rapid recovery if the Nats get in with a landslide, the backlog of buyers that have been holding off for months now with launch into the market.

Where are these envisaged overseas buyers coming from? If they're waiting in the wings, how clued up are they on individual party policies regarding houses? Even if they are clued up on that, and they're from the UK or US, they'll no doubt be clued up on what a property bubble looks like.

And most importantly why would them coming back be a good thing?

And that is what I am seeing too, you cannot but notice the amount of Asians attending open homes - they are there and sniffing around just like the rest of us .... If a good property can be found now at a reasonable value it should be purchased pronto ... buyers are taking their time and evaluating all good ones as they come to market - election uncertainty and the Noise and Splashes that minor parties are making is distorting confidence - once that is cleared out of the way , the market will move again!

Sorry, are you saying the Chinese people you see hanging around open homes are these mythical overseas buyers we keep hearing about? Sorry, but that's completely delusional. Do you assume these are foreign buyers because they look "ethnic"?

I don't think they are foreign buyers. Probably just some of the many that have arrived over the last ten to twenty years. New Zealand is now a very desirable place to live for many Chinese people as is Australia and Canada. One reason that is not mentioned much is how desirable it is to have a NZ passport. The Chinese have discovered travel, I think much more so than Indians. Everywhere you go now you see many Chinese tourists and many of the Chinese who now call NZ home use the NZ passport to travel the world with its visa free benefits. I'm not sure why, I suspect it is quite a status thing to be able to travel around and they just seem to really enjoy it too, probably because of the years of living like the North Koreans do now.

I see, so these ethnic Chinese would be NZ residents who are going to save us all by continuing to pay for houses at stupid multiples of incomes at a time when owner occupiers and other investors aren't buying. So as to provide a market exit for all those investors queuing up to exit the market. But that's ok, because they have more money than they know what to do with, so they don't mind throwing some away.

That's good, v reassuring. Those ethnic Chinese residents really are awfully helpful people.

Except owner occupiers and investors are still buying and investors aren't queuing up to exit the market. i suspect most people think that many more migrants are on their way. The latest immigration figures seem to confirm this thinking is likely to be correct. People want to leave China, India and elsewhere so they can come to NZ and live the Boomer lifestyle.

Auction clearance rates and sales volumes are significantly down. Prices are materially down. I also think listings are up? So no, occupiers and investors are not buying in anywhere near the volumes they used to. Highly leveraged investors and zero or negative net yield landlords will now be heading for the door, as without capital gains their investment makes no sense at all and are often cash flow negative.

I kept a record of numbers for sale on TradeMe on Feb 3 2017. Current # in brackets:

Auckland City 1877 (1831)

Manukau City 1829 (1892)

North Shore 1055 (1021)

Waitakere City 926 (1131)

So fewer in Auckland City and North Shore and more in Waitakere and Manukau but not a huge amount. Listings have been steadily trending down over the last eight weeks.

Thanks for keeping this data Zach. What were they in July 2016 though?

While they are down on Feb 17 numbers, this is still historically high. Inventory moves quickly in March - June normally, but per REINZ sales figures it has not. This may also indicate the numbers down are due to withdrawing from sale rather than indicative of a buoyant sales market (no data-points currently show sales figures rebounding to my knowledge)

It's very interesting at least that the discussion seems to have moved on from "foreign buyers aren't a factor" to "after the election is done the foreign buyers will be back and our housing portfolio wealth will take off again". If ever there's a signal to politicians interested in the wellbeing of more than just a few folk, that's one... When even speculators are proclaiming outright that foreign buyers are pushing up housing prices.

Land use restrictions? The Auckland slumlord's not interested in any of that. Outside of your flash Ponsonbys and Remueras the bulging favelas are increasingly populated by garage and garden shed dwellers. Just pop a shed out the back yard, once it's signed off (if it is even consented at all) in goes the kitchenette and basic shower and toilet followed by the desperate tenants.

Just the other day one of these blew up nearly killing the unfortunate residents. The overseas based landlords were unavailable for comment.

" In the first six months of last year, it was reported that complaints about unsanitary and dangerous dwellings had reached 750 in central Auckland, with a further 500 in south Auckland.

One investigation involved a piggery converted into four accommodation units"

http://www.nzherald.co.nz/opinion/news/article.cfm?c_id=466&objectid=11…

...and Land Supply for even the favela sheds is limited by the Building Act 2004 - "No shed shall be closer than its height away from any property boundary". Have a look in even your back yards, and see where your shed is! 10/1 it's up against the back fence......

Thanks bw but looks like that restriction only applies to small sheds that don't require a building consent. You can go closer if it is consented but, as appears to be the case, these guys are not exactly keen on sticking to the letter of the law. The number of complaints will be the tiniest tip of the iceberg.

As with all things Council, THE LAWS! are only there to keep honest people, honest, and if in doubt, get the Council to change THE LAWS! eg: "Battersea Power Station Development Company, backed by a group of Malaysian investors, argues that the entire project may become financially unviable if it has to stick to its previous plans....Wandsworth council is expected to approve changes on Thursday

Lol, I have a wood shed and it's right against the back fence! It's not much higher though so maybe that is ok.

I wonder how much welfare was being paid to said overseas landlord in the form of accommodation top ups. Man, that infuriates me, to no-one else is welfare handed out so freely as it is to landlords, and foreign ones can avail themselves of these handouts as easily as NZ ones. Talk about unforeseen consequences when we came up with the idea of that.

Garden sheds are for storing gardening tools and equipments not for dwellers. All gardens in Ponsonby and Remuera should be in keeping with the BBC Gardeners World standard and have landscaping done by professionals. Lawn mowing, hedge trimming and tree pruning should be happening regularly to keep the place tidy and high-end.

Points awarded for consistently playing your "persona" DGZ.

Auckland's Favelas

Thanks for that gem - Favela should enter the Auckland Lexicon

Section prices are still pretty expensive. $450k+ in Auckland, $250k + in regional cities.

Unlikely that section prices will drop.

Bzzt. Wrong. Christchurch, largely thanks to the benevolent diktat of CERA and Brownlee, who basically threw the stoopid, restrictive land-restriction policies of local plans under the bus and let Ms Market work her wicked ways, has plot prices beginning with a 1.

Some data, so as to distinguish this from the anecdote so common in these arguments:

- Harcourts price range $100-200K - http://harcourts.co.nz/Property/Residential?pageid=-1&search=&formsearc…

- Branthwaite "sections from $185K" http://branthwaite.co.nz/rolleston-land-for-sale-canterbury/

- Ravenswood - prices strat sub $130K - https://www.ravenswood.co.nz/sections-for-sale/stage-1/

- Waitikiri - right next to a golf course...a couple in here at the $190K mark, 6km from Old CBD http://www.waitikiri.co.nz/files/stage4.pdf

Data beats anecdote....and Christchurch illustrates the results of freeing up land supply from the clutches of the economically clueless Plannerista....there just might be a lesson for Awks there....

And at those prices they will still be making heaps of money.

Christchurch must be an outlier then.

Palmerston North, Hawkes Bay, Hamilton etc sections are $250k +

We don't want to live in Christchurch, thats my most of the population are north in Auckland.

Ooh, but there's Hutt, with 230cm of groomed powder on top, and, why, that's a Season Pass clipped to the faithfull Volkl SuperStars, the sun is shining, and the Santa Fe's topped up with truck-stop diesel. You don't know what you're missing.....

The collapse is on it's way!

Shamubeel has bought a house. https://www.stuff.co.nz/business/opinion-analysis/94966044/shamubeel-eaqub-ive-bought-a-house-at-last

This is indeed worrying and probably more deserving of an entire article. We have grown to rely on Shamubeel always getting it wrong.

Hopefully this means that all the economic advice of 'renting is great', 'put all your savings into shares & kiwisaver', 'stop buying flat whites', etc ceases.

Read the article. He wants security of tenure for his family, which is understandable. He still thinks the financials are heavily stacked in favour of renting at the moment, which is right. I doubt he thinks this will be a financial bonanza for him.

Its never been stacked in favour of renting, maybe he has finally figured that out. EVERYONE I know know at the age of 50 or older who are still renting are now in deep shit.

I have to agree. I have done a lot of analysis on varying situations comparing rent to ownership.

In short renting does make sense when compared to a mortgage. From what I have read, and the analysis provided by Shameel and a lot of other "experts". This seems to be their core assumption, and using this assumption they are for the most part right. But...

What they forget is you don't always have a mortgage. This is where home ownership can make sense

The simplest sum is this.

Ignoring capital gains. Own a mortgage free home at retirement. Immediately, based on current rent you save approx $400 a week.

That's:

$20,800 after year 1 (Age 66)

$208,000 after 10 years (Age 75)

$416,000 after 20 yeas (Age 85)

Live longer, save more.

Pay off the mortgage earlier, and the sums rack up quicker.

Mortgage free by 45, then by retirement you are $400k up on a renter. If you invested that in the same way the economists have said, then you will be substantially better off than a renter at retirement.

Rght now, given prices and yields, it is materially cheaper to rent the average house than buy it.

Bobster, I have been thinking about this regarding my own situation. My house is worth about 1.5M so I could sell it and rent something similar. Renting would probably set me back about $900 a week. However 1,.5M would return only about $800 a week after tax if I put it in the bank so it doesn't seem to work out all that well. Especially if I suspect the house will keep up with inflation and the bank deposit wont as I will be using it to fund rent. It may just work out, sort of, but it's not certain enough to actually go ahead and do. in fact I'm pretty sure it would be a really bad idea.

The rent vs buy numbers have been crunched in various places, and the result is always rent costs are at a discount to mortgage payments at current prices. The debt service required for an average house is well north of its rental payments. All thing being equal, you are currently materially better off on a cashflow basis paying rent than paying a mortgage for a given house until debt service costs fall ie prices fall.

Bobster, as far as I recall it has always been this way. It doesn't seem to work out for someone who has a mortgage free house as I detailed with my own situation above. The few people I have known who have given up on owning there own house as it didn't make much financial sense have likely deeply regretted that decision. I remember someone telling me it wasn't worth owning a house back in the mid eighties and how it was so much better to rent. Back in the late nineties I held off buying and rented for a couple of years and thought I was winning as house prices considerably dropped at that time. However it was really stupid of me not to buy as soon as I could as i lost my rental and found myself homeless with a toddler and a heavily pregnant wife. All rental properties had queues of people wanting them and I was forced to buy a house that I didn't really like all that much although I later sold it for a 300K profit.

Actually, if you look at the data, that has NOT always been the case. The ratio of rent:price (and therefore rent:mortgage) in NZ has climbed to 136 when pegged against 2010. This is among the highest in OECD. Auckland will be MUCH more than this

https://data.oecd.org/hha/housing.htm

For reference, most others are 105-110 range, including AUS, UK, US etc.

Right now, it's financially much better to rent. All your numbers of selling up and rent you'd have to pay need to include the rates, insurance and maintenance costs - adding $100+ p/w. Even on TD, you'd get ~4%, so less tax = $830 p/w + $100p/w saved in Rates etc = $930 p/w. Plus, you're not paying the mortgage. You'd be better off renting at $900 p/w

Of course, you'd need to Bank/Invest the difference.... being better off renting does not mean consuming the difference, otherwise, yes, you'll be stuck renting later. But if you've invested it, you will still have an asset in retirement (plus K/saver).

Don't forget - in order to retire as a home owner and realise the value of your house, you'd need to sell, which many retirees don't want to do.

A renter can always purchase in a cheaper market - i.e. outside Auckland, with cash, upon retirement.

Zach - is your property freehold? I see there are no mortgage payments in your calculations. Nor rates, insurance or maintenance.

So I rent a house that is worth around 1.5M. It costs me 680 a week. With the extra money I save I pour it into my business to grow it faster. Works for me. And Im only a couple of years off 50. the tide mark of shit (deep?) is around my feet only, occasionally ankle height.

So I now own a house worth $1.0M. It was costing me $640 a week. I hit the finish line age 48. Basically I now have options to do anything I want now and even working is optional. I think you begin to start to see things very differently from age 50 onward, perhaps 55 at the latest. Hope you can sell the business for $1.5M and buy a house if you wanted too.

We can't say he's wrong. He can't say when a correction will occur but I remember him saying we were heading for a banking crisis if we racked up property debt like we have. But I would that outcome is a possible, not a probable. It just hadn't occurred yet, so he may just have been early.

He's wrong, there you go, I said it

@ Bobster .... He is wrong, I have done that analysis and complicated spreadsheets 17 years ago , however lucky that I didn't pursue it .. it proved to have so many unknowns and very difficult variables to predict ...let alone disasters in the World economy that can make you lose everything.

So he was and Is wrong - sugar coating it is just face saving

We are Not Germany nor Switzerland .. and that comparison is also wrong ... our people are "different" and our tenants are even more "different" -

Yvil can enlighten you about that ... you only have to be there for few weeks to know why !!

Mortgage costs vs rental costs on an average home show a 25% discount in favour of rental costs. Given current yields and house prices, he is right.

Wow, really?

But Eco Bird has done a really complicated spreadsheet!

Surely you would thus believe Eco over some stupid economist? I mean, what would they know about financial planning vis a vis Eco Bird?

Yes notice how the RE's claim to know all the numbers but never share them. But then most RE's are professional liars.

I don't believe RE agents are all professional liars. This is a generalisation that is irrational. I think some are but most are just normal people like you and me.

I agree. They aren't professional liars. Just b/c we think property prices are inflated, we shouldn't generalize.

They are normal people, it's just that some of them purport to know more than they actually can, and people believe them. Given they are in a position of trust, they should though be required to be more guarded with their expressed views.

if he " always getting it wrong" then we can count on house prices falling for another year or so now he has become one with equity and debt

Shamubeel probably hasn't moved in yet and only then will he find what a different headspace it is. It's so good for him and he didn't even know that before. While he just worked out the security thing - the control factor is vital. He's going soon to realise the value (not dollars) of control over little stuff - improvements - even colours await him. So welcome Shamubeel.

Bit sad really that many others remain who haven't worked out what a house really is. Hint - it ain't just dollars.

He now agrees with Bob Jones:

"So what should mum-and-dad investors do for their retirement? For homeowners in Auckland, Wellington, Hamilton, Tauranga and arguably Christchurch, take the wisest approach to the one life you have and adopt the elementary wisdom of Epicurus. Ignore the often self-serving condemnation of fund managers and the well-meaning puritanical scolding of Don Brash and other commentators and put your spare cash into your home. It will bring you pleasure as you constantly upgrade while raising a family and will prove the best investment proposition, so long as the people inflow continues, which it will. As you approach retirement – and as has always been done – sell up and downsize, either to a city apartment or the likes of Nelson. That will leave a cash surplus more than would been have achieved through enduring a spartan life-style through saving. Only then should investment arise as an issue."

http://www.noted.co.nz/money/investment/sir-bob-jones-on-how-we-get-it-…

So you and Bob Jones don't get it either Mortgagebelt - or maybe it's just you Mortgagebelt because Bob is smart and sees the joke.

Ownership is great karma. It ain't calculating on 'inflows' or 'gains' and certainly not (heaven forbid) planning onselling up and shuffling off in your carpet slippers to Nelson

What I don't understand is how home ownership is regarded as such a great thing and people understand its value as being something more than just dollars and cents (i.e. its the security, freedom, pride etc) - then why would they want to take that right away from other people by outbidding them at auctions and owning rental properties? (where all they are doing is owning the property because of the dollars and cents - those are two very diverging positions to take).

That would be very two faced, morally unethical behavior, especially when they know that young families would like to experience that same sense of freedom and security - it must cause significant 'Cognitive Dissonance' as people say....have your cake and eat it too sort of mentality.

"I love housing because of the security, freedom and pride it gives me, therefore I'm going to live in mine and enjoy those things, but at the same time I will take away that right from the next generation because I like money'....

Rightly or wrongly and whether people agree with it or not, accept it or choose to fight it. We live in a capitalist world where human nature will remain unchanged and people will always put their interests in front of others to ensure security of themselves and their family. It is a basic human trait, there will always be someone bigger & richer than all of us and they will win. It is the reality biscuit, eat it.

Exactly right. Have you heard of "The Scorpion and the Frog" story?

https://en.wikipedia.org/wiki/The_Scorpion_and_the_Frog

No but took a quick look; pretty bang on

yes, spot on - thanks for sharing that ...so true

So it is rightly or wrongly?

It is what it is.

And what is 'it'?

(greed)

And what follows greed?

(fear)

And when does the cycle end?

(those that are greedy now are really just fearful because they're scared they're going to miss out - its okay though because as you say its just human nature...)

envy it seems in you case ...

Funny how greedy people like to accuse their non-supporters as envious, like in their own minds they view themselves as some sort of success story that should be looked up to - when in reality its a long way from the truth! Good for you paashaas

It's neither right or wrong, it is what it is. What is right to you is wrong to someone else, and conversely, what right to someone else will be wrong to you. Who are we to tell others right from wrong? do you like others telling you what's right and what's not...

Of course it's greed. Something hard wired into all human beings (and I'd go out on a limb and say all living creatures) to advance themselves are their lineage. Just like the same greed you are adopting wanting things to change so you can have a slice of the pie- exact same thing, just two different perspectives.

Sounds like you've been heavily indoctrinated into the western world doctrine and way of seeing things - you see the world completely through a greed/capitalist paradigm. That doesn't sound like a very enjoyable way off living your life? Pretty hard to see the big picture through that lens....

Ever read any Lao Tzu?

A journey of a thousand miles must begin with one step... :)

I am just calling it as it is... don't worry I don't agree with it when I see those that sit on their yachts with billions of dollars and think "man if you gave all the poor people in the world $100 you'd still have plenty" but it is what it is. And I do read so much on here about 'dark lords' etc and just wish we all weren't tarred with the same brush. Many investors on here would have gotten in at the right time, worked to get there, not had a hand in driving up prices beyond the reach of many and take care of their tenants.

That one step could be away from this system that we've created which is making a lot of people very unhappy....its forcing them to be greedy to try and get by. But the problem is, because everyone is trying to beat each other, nobody wins....the world is interdependent...if you win, someone else probably loses....we should be trying to help one another not beating one another....

'I am just calling it as it is...'

Do you see any need or responsibility to make a change? Or are you going to try and beat the masses at their own game that I think you recognise as being flawed?

I agree and you absolutely make some great points. How do we address the challenges around those that want more but won't work for it? As a society we have those that refuse to work & take handouts on one end of the spectrum then those that take it all at the expense of others at the other end of the spectrum. Most of us would sit somewhere in the middle but how do we then balance things out when you do have the impact of those that want it all but won't contribute? It's a tough one & id imagine the reason why the rich get richer

So we need a significant paradigm shift propertyminx - if you think that the capitalist model is the way ahead, then you need to be aware of the fact that its causing inequality and inequality means poverty, and poverty means handouts....so if you support capitalism it means you support handouts....and it sounds like you're a fan of capitalism so it means you're also a fan of handouts, but you tell me that you're not...so which is it?

I am definitely not pro-handout. I am not necessarily pro capitalism. I am pro "work smart, play smart" whatever political bucket that fits. But until you tell me independent observer that you are housing one of the 40,000 plus homeless in your house, I won't believe you are not about your vested interests either.

Go get 'em propertyminx - I'm sure you'll win and this will make you very happy....

So, so, so well said propertyminx

If Bill Gates gave all the people in the world $10 each he would be bankrupt. If he gave all the poor in the world (virtually none of whom are in NZ) $13 each he would be bankrupt. Being on the dole in NZ puts you in the top 20% of the world's highest income earners.

I was greatly influenced by this TV show when I was young:

Monkey Magic Opening + Closing Themes

I even travelled to Xian in Central China and climbed the pagoda where they stored the scrolls brought back from their journey to the West.

It's neither right or wrong, it is what it is. What is right to you is wrong to someone else, and conversely, what right to someone else will be wrong to you. Who are we to tell others right from wrong? do you like others telling you what's right and what's not...

Please define 'it' so it's clear what you mean. 'It is what it is'...what is 'it'?

Are you referring to greed like propertyminx? The greed is just simply greed? It is what it is...?

It's not the self interested people that bother me, it's the people that act outside their own interests that I'm concened about. As with the GFC in the USA, a lot of the greed driven behaviour was self defeating. If people could learn the lessons of past financial bubbles and use them to protect their own welfare then we would all be better off. Unfortunately, as soon as the next gimmick comes along people are all "I can make money by doing nothing, sign me up!"

Consider this - if 100 people borrowed $1M and bet on black at the casino then around 46 of them would be millionaires and around 54 would be broke and in debt. I'm not sure that outcome is better than what people who have jumped on the property train recently will experience.

Interesting article from Sir Bob. The context was some people telling mum-and-dad investors to buy regional commercial buildings and his take on why that was a terrible idea.

He's talking about putting money into your home - I.e. just live in it. Deleverage, enjoy life.

Nothing in there to support the common thread of commenters here who prattle on about how awesome an investment rental properties are.

Conversely he's about to discover that the (pick an annoying property rights issue of your choice, here) that was of no concern when he rented his home, now becomes a legal case to be settled by him with his neighbours in court. He'll no doubt rely upon the Code of Compliance issued by his Council, who when approached for assistance will reply 'That's a Civil Matter for you to attend to.'. He'll then realise that Council Codes of Compliance and Building Codes have far less protective value than he previously thought. Owning? It has it's benefits, and a number of drawbacks - just as renting does.

So bw - the big problem of owning your house is suing everybody? Really? Is that everybody or was it just you?

I really doubt that will be his experience. I bought a house six and a half years ago and it sucks so much money. It was and is a tidy place built in the early 1970s but you still get bills, bills, bills. I've spent about $10k per annum on improvements. Now granted I've made all that back through capital gains but if you ignore those it has cost be around $45k a year to own my own home (opportunity cost of capital, rates, insurance, improvements and maintenance). The only way owning a home makes financial sense is if you are getting a significant capital gain which lets face it is unlikely over the next five years.

But I do like home ownership as a consumption decision. I put my TV on the wall yesterday - I wouldn't be drilling holes in my rental. People just need to be honest they are consuming and stop pretending housing is a get rich quick scheme.

Shammy-Bill's buying of a house in Orc Land is the economists opposite of Bernard Hickey's selling of his ...

... we all guessed , a few years ago when the hickeysterical Bernard sold up , to shift to Wellywood , that it was a sure sign there was plenty of meat left on the Orc Land house price bone .... and it was ... it really truly was ....

And now , Shammy-Bill's purchase of a house in Orc Land is a sure sign , equally so , that prices have peaked .... topped out brothers and sisters ... on the cusp of the turning point .... set to head back down ....

Actions speak louder than words. The fact that Shamubeel has entered the housing market at the worst possible time speaks volumes about his understanding of the property market. I shall never listen to him again

But he bought the house to live in, not to flip for capital gains. So why does it matter that he bought at the worst possible time?

For an English speaker the word "reasonable" is almost meaningless especially when there is no clear context and more especially when spoken by a politician. I can't believe the writer has made such a big deal out of this.

Alex I love your writing but with due respect I think you have this wrong.

It's pretty clear to me that Joyce is referring to prices of new vacant sections in greenfield areas. That is quite distinct from property values overall.

I'm with Fritz

Land component value tends to be greater than Improvements.

So section prices will influence the land component of properties in similar suburbs.

Existing sections aren't disconnected from new sections even if they are in different places. If new sections become readily available and significantly cheaper, this will drive down existing house prices (unless there is a restriction on the ability to build).

Flat Bush appears to be ground zero for Auckland sections. Seriously the best part of a million for 350sqm no longer with the bushes, just flat.

Oh dear, even my garden is bigger than that. It is ridiculous to pay over $1m to live in such a tiny plot of land and so far away from the city. It's ground zero alright.

Now, take a look at your latest council rating or homes.co.nz valuation – you’ll see your section/land accounts for the majority of the value of your property as opposed to the ‘improvement value’ of the dwelling you have on it.

Not so for Hutt City Council as of 1 September 2016. Value of improvements accounts for 52.86% of the total capital value. Unfortunately, the latter value, of course, is what I have to insure improvements for in case an act of total devastation visits.

I might be a special instance since I petitioned QV over inadequacy of older valuations where my land value certainly did account for a greater share of the capital value?

I made a case, before the Christchurch earthquakes, that EQC has little other than QV improvement values to ascertain property recovery costs, post a catastrophic event, thus these values needed to better incorporate the extraordinary high cost of building materials and their subsequent erection.

Take a look at 8 Kitirawa Road.

2014 CV = $2,100,000

Land value = $1,960,000

Value of improvements = $140,000

https://beta.aucklandcouncil.govt.nz/property-rates-valuations/Pages/ra…

Another one - take a look at 17 Komaru St.

2014 CV = $2,250,000

Land value = $2,100,000

Value of improvements = $150,000

https://beta.aucklandcouncil.govt.nz/property-rates-valuations/Pages/ra…

Perth Apartment Crisis.

https://www.stuff.co.nz/business/property/94154549/house-prices-dive-in…

The Crash Is Coming.

Thanks for making a slight change john wheeler. Good on ya! LOL

Yay a new article.

Good on ya JW.. rub it into those moulded minded speculators

Of course, its London and Auckland is different

The buy-to-let stampede begins: 'How best to sell my 37 properties?'. Like hundreds of thousands of his generation, Graeme Cook turned to property as his favoured means of amassing wealth. But he started earlier than most, and went into it on a far greater scale. And now, like one in five landlords, Mr Cook, 53, wants an exit strategy. He plans to sell most, if not all, of his properties....A weakening housing market, tough new legislation and the tightening of affordability checks by lenders are but a few problems causing landlords to run for the hills

http://www.telegraph.co.uk/personal-banking/mortgages/buy-to-let-stampe…

... if nothing else , this article ably demonstrates how useless a Capital Gains Tax is ... the government cannot collect it , 'cos the investors is continually putting off selling any properties because of the CGT itself ... also holding up the supply of properties to new investors or FHB's ... 'cos the investor is hanging on , even though he doesn't want to ... he wants to cash out , and to get on with his life elsewhere ... but the CGT gums up the whole process , frustrating everyone ...

Whereas an annual land tax ... by comparison to the CGT ... raises regular monies for the government ... is cheap and simple to apply .... is unavoidable .... and frees the system up ... allows everyone to get on with living the dream , rather than needing to plot a scheme , to dodge the taxman ...

Jawohl, sticky ursine. And the beauty of Land Tax is that it could be applied via existing powers: Local Government (Rating) Act 2002: Schedule 3 - Factors that may be used in calculating liability for targeted rates

1 The annual value of the rating unit.

2 The capital value of the rating unit.

3 The land value of the rating unit.

4 The value of improvements to the rating unit.

5 The area of land within the rating unit.

6 The area of land within the rating unit that is sealed, paved, or built on.

7 The number of separately used or inhabited parts of the rating unit.

8 The extent of provision of any service to the rating unit by the local authority, including any limits or conditions that apply to the provision of the service.

9 The number or nature of connections from the land within each rating unit to any local authority reticulation system.

10 The area of land within the rating unit that is protected by any amenity or facility that is provided by the local authority.

11 The area of floor space of buildings within the rating unit.

12 The number of water closets and urinals within the rating unit.

So all we need is for a few TLA's with the requisite combination of economic nous, vertebrae and cojones, to Pass a Rissolution, invoking some combination of the above.

But such beasts are Rarer than the Jabberwock, so perhaps we need a Plan B.....

My notion would be a Land plus Sumptuary (Google it ya lazy sods) combined Taxeration along the following lines:

- Pure land tax at base, using #3

- A differential rate based on the division of #11 by #7 - which is the average living area per separately inhabited unit. Anything over say 140 squares per such unit, and you're gonna attract a swingeing rate.

- A differential rate based on a division of #12 by #7 which is the average number of loos per living unit. Exceed 2 and watch yer rates go through the roof.

- and of course this applies to Uses (see Schedule 2) so exempt Commerce, Industry etc from the Sumptuary side.

- And for those with a historical bent, a Windows Tax should be possible somehow, but perhaps I'm getting carried away here....

The point is simple enough: the tools are in the bag.

Wether some like it or not - It is not that price will fall BUT price are falling and will continue to fall for sometime before they stabilize for a considerable period.

By wishing and repeating that price will go up - if that was how ecenomy worked their would be no problem in the world. Best is to ignore such people and comment. - why even bother to respond as they are so desperate that by repeating are trying to convince themselves that all is well as even they know that now the only way for house price is Down.

Should pity with them instead of arguing and if by feeling that worst is over(infact is just the begining) if it makes them feel good- so be it but by denying the fact will only bring more misery to them.

I think the national government should set up a depression clinic for all those speculators they are about to ditch

I understand they're already full of people they've ditched the last 9 years....

Don't forget 10x should mean 10x your nett income. I wonder how many Aucklanders take home $100k per year in order to buy a $1mi properly in your average suburb?

And if you happen to house-hunt in DGZ you'll need $2m for an average 2-bed duplex.

The average salary in Auckland is 75,300 pa( https://www.google.co.nz/search?safe=off&rlz=1CDGOYI_enNZ681NZ681&hl=en… ) which means that a couple who are both on the average salary should make $150,600.

Average is a terrible measure, when you you mix in the millions the ceos make

Average salary is more like $48K and the average household income is like $78K which is far more believable. Never got to $75K in my life unless you factored in the commission and the company car into the equation.

Up to date median household incomes, based on the giant IRD PAYE records, are here. By city.

@David Chaston. Thank you for the post, very interesting figures!

The Sense Partners report looks like a wonderful example of how economists can reason in a circular fashion. If we assume that land prices are mostly due to regulation then we can prove that land prices are mostly due to regulation. It's more subtle than that (well, a bit!) but does seem to include the idea that a properly-deregulated area should be able to respond to increased demand by increasing supply (by intensification) so that price scarcely changes. Visualize that inside the DGZ. Their figure 1 astonishingly shows huge regulation costs that almost entirely account for the variation in NZ land prices. This must be the answer that Steven Joyce wanted but it doesn't make it correct or even vaguely plausible.

Warning to readers: do NOT try to read section 1.5 "Our four methods" and drink hot coffee at the same time.

Govt moves before election to build Auckland houses

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

There're already too many houses in Auckland, just look at the TradeMe listings! Instead of building more houses in Auckland I think families should be encouraged to make the move to Kaitangata. http://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=118…

... three points .... one ... if there's plenty of houses in Orc Land why suggest that families ought to be moved to Kaitangata ?

And C , if there's too many houses in Orc Land why does it cost $ 900 000 to buy an average one which is so crappily constructed that the SPCA would happily prosecute you for ill-treatment & animal cruelty if you deemed to house chickens inside of it instead of humans ..

About bloody time

Bloody cowards.. claimed there is no housing crisis all along.. before election they bend...

National have announced they are setting up a housing infrastructure company to spend $600m on housing. My first question would be: is Gerry Brownlee going to put put in charge of it like the Christchurch rebuild?

https://www.stuff.co.nz/national/politics/95022183/government-setting-u…

They'll just spend the whole $600 million on chocolate biscuits for the meetings.

so they sell the ministry of works then slowly recreate it under a different name years later

At last a great smart initiative to have a PPP to build infrastructure - ACC saw the light too like Samubeel did at last lol... I will be the first to buy into this if it was offered to public subscription ... Good Move ..!! lol, left Labour paddling in the mud !!

Ahhh, Labour have been promoting ideas like for a few years....

Not one of the twits and tools in power have an ounce of common sense.

A days work would kill em....

An ounce of commonsense, a great weight on their minds.

We could have all worked together...built a Great Nation like Trump espouses as he glad hands all the other layabouts around the World. I suppose I should have joined them, but once bitten twice shy.

Getting into power is easy with Money behind you, especially in this fixed world we live in.

Bit fixing what is sorely broken...no bleedin chance.

REVERT TO LONG TERM AVERAGE ............... thats probably the best we can hope for with respect to house prices .

I would like to know what the 10 year average house prices was ( adjusted for inflation)

The better way to look at it is to look at the long term average for price to income and yields. The former would require more than a 30% drop in real prices, the latter 50%.

Penny dropped yet?

I was just looking at Devonport on homes.co.nz and a thought occurred to me. Whatever the governments lies are regarding the level of foreign investment, the projected prices on homes.co.nz absolutely must be predicated on a percentage of foreign purchasing which is close to 100%.

look at the projected prices for neighbouring houses 2.1 mill 2.5 mill 2.6 mill 1.8 mill 2.5 mill 3.4 mill. Any of the streets! in any nice area of auckland, Mt Eden, Remuera, whatever.

Tell me which double income no kids buyer in NZ can afford 2.5 million dollars? What deposit would they need? Which bank would lend them the money? At what interest rate? Even with help from their parents! It's just not possible! Those valuations are the foreign buyer price.

Absolutely correct - Those valuations are the foreign buyer price

You could be right fat pat. Take a look at this: New teachers quit city, delay kids, due to unaffordable housing Two-thirds of Auckland's new teachers plan to leave the city, and many female teachers are postponing parenthood because of the city's housing costs, a new survey has found.

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11894085

And that's a huge problem, which impacts families immensely, my daughter's school is a couple of teachers down. It's nothing to do with wages, they would need to have their salaries doubled to make property affordable. Building houses in the back of beyond won't help either.

Its also the reason why Auckland will fail. You cannot just increase one sectors wages without more problems created and lose competitiveness in the tradable sector.

I recently came across a case in San Francisco of a nurse on 180,000 and still in relative terms unable to get into their property market.

Don't you think schools should chip in to help accommodate these teachers to keep them?

Have you taken the opportunity to look at school budgets??

Who is actually chipping in when a school chips in?

Yep, parents and tax payers.

The bubble has enough tax payer support already.

I don't think the money should come from the school's budget. I think parents should donate generously to make this happen to keep good school teachers.

That is insane, the problem is staring you right in the face - housing inaffordability. Teachers should not have to rely on charity to be able to live and work. It isn't only teachers though, it's multiple professions, are your wealthy foreign buyers going to retrain so they can take up these pivotal roles?

I'm coming to the conclusion that you're a poe.

As a temporary measure, all the wealthy foreign buyers with children attending public schools should chip in to help provide accommodation to quality teachers.

No they shouldn't teachers, and others in a similar income bracket, should be able to buy their own home without artificial assistance.

Yes I know and I agree with you, that's why I said "temporary measure" until the situation improves in the long run.

And how in your view does the situation improve?

Funny conclusion when you consider the current temporary tax exemption on foreign income for new migrants.. for the first four years..we actually provide an incentive to come by given tax advantages compared to residents..yet the residents prick up the tab for the additional consequences...case of unintended consequences or simply no thought applied.

Dp

That comment deserves a forensic analysis together with an article on its own

I'd suggest maybe we start with camps where we can concentrate people together then transport them from there to workplaces. This will help keep wages low in line with National's seeming priorities vis-a-vis immigration, and navigates around Auckland's issues with lack of housing and land.

What's a POE? - is that a chamber-pot or what?

A slightly more intelligent troll https://en.m.wikipedia.org/wiki/Poe%27s_law

Dp

I see on occasion, the senior professional couple on combined 500k paying the 1.5 million mortgage (usually interest only), lease the euro cars and pay private schools wondering why they have no disposable income..rare thou:-)

They probably own a $5m home in a swanky suburb somewhere in Auckland on the cliff top over-looking the Waitemata Harbour. Their income would have been all tied up in the house and mortgage, but their net worth would be in the millions you would think?

Well .. not exactly .

Plenty of people with lots of equity in their existing homes and investment properties ( the same frothy market has seen to that ). If you are selling in Remuera and buying in Devonport it is much the same thing .

Not a few returning cached-up Kiwi expats ( or perhaps those are foreign buyers within your definition )?

The govt know prices in Auckland are dropping and it looks like Joyce is planning to take the credit, albeit a few months late to make the statement....

Watch for a quick about face if there was a crash.

Another failure by the misfits..

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11894085

Stephen Joyce is talking in riddles .............there is no way section prices will collapse with demand for housing so high .

Quite simply 21,000 people need houses right now and there is nothing for them , now add another 6,000 new migrants a month and what do we have ?

Here we go again...demand from owner occupiers do not support prices at current levels. See rental prices, which are a good proxy for demand for housing as an accomodation asset. Rental prices have gone nowhere. It is INVESTOR demand which has had the biggest impact on credit, facilitated by loose mortgage lending which has created a vast debt fuelled bubble. Owner occupiers pay debt service from salaries. At 10x income, houses are severely unaffordable for owner occupiers. If the market was to rely solely or predominantly on owner occupiers, prices will fall.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.