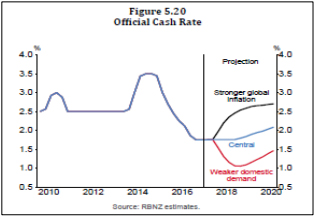

In the last two Monetary Policy Statements the Reserve Bank included alternative scenarios for the OCR in addition to the central scenario that involved roughly one OCR hike in 2020.

The first alternative scenario suggests that higher global inflation could warrant almost four 0.25% OCR hikes over 2018 and 2019 while the second alternative suggests that weaker domestic demand could warrant three OCR cuts next year. The question of whether weaker domestic demand could warrant OCR cuts is addressed in our pay-to-view reports. This Raving considers whether higher global inflation could warrant several OCR hikes.

The likelihood the future will turn out different from what the Reserve Bank is forecasting means including alternative scenarios in the Monetary Policy Statement is a good idea. However, as covered in this Raving, it is questionable whether there is a sufficient linkage between global and local inflation to warrant the four OCR hikes in the first alternative scenario.

Even if global inflation turns out higher than the Reserve Bank is predicting it is questionable whether this will have a sufficient impact on NZ medium-term inflation prospects to warrant several OCR hikes.

The Reserve Bank's alternative OCR scenarios

There are two parts to this issue: (1) whether global inflation increases; and (2) whether there is much linkage between global and NZ inflation. Higher global inflation should only warrant OCR hikes if it increases NZ medium-term inflation. I do not expect a significant increase in global inflation over the next year but at some stage higher global inflation is likely/possible. My focus here is on the question of the linkage between global and local inflation because even if or when global inflation increases it will only warrant several OCR hikes if it significantly increases NZ medium-term inflation prospects.

The direct link between global and local inflation

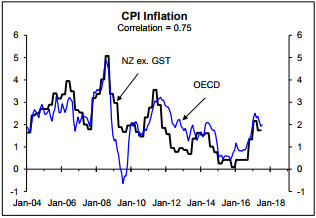

The adjacent chart suggests there is a reasonably close link between OECD and NZ inflation. I have excluded from NZ inflation the temporary boost in 2010/11 caused by the increase in GST from 12.5% to 15%. The peak correlation is coincidental at 0.75 compared to a maximum possible correlation of 1.0 (i.e. like a 75% pass mark in an exam). It appears that local and global CPI inflation largely move up and down together although there have been some exceptions. At face value this suggests that higher global inflation could justify OCR hikes based on concern about higher NZ inflation. With the two moving together rather than global inflation flowing through to NZ inflation with a lag there would be evidence of higher local inflation at around the same time there was evidence of higher global inflation (i.e. the second alternative scenario should just focus on the risk of higher local inflation). But it isn't as straightforward as the chart above suggests.

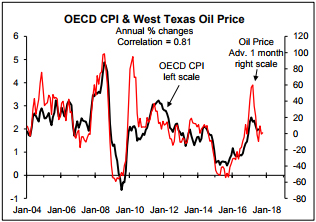

The reasonably high correlation between NZ and OECD CPI inflation is largely because upturns and downturns in the oil price flow through to both at the same time. OCR decisions aren't supposed to be driven by short-term spikes and tumbles in inflation driven by the oil price but rather by medium-term inflation prospects.

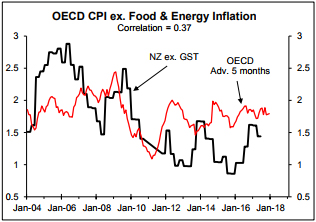

If there is an upturn in OECD/global inflation caused by a rising oil price it shouldn't justify OCR hikes even if it flowed through to a temporary increase in NZ inflation; especially if local developments imply different prospects for medium-term CPI inflation. This suggests we need to look beyond headline CPI inflation that is impacted significantly by the oil price.

Indirect links between global and local inflation

There could be indirect linkages between global and local inflation that warrant "higher global inflation" being linked to several OCR hikes. A line of reasoning could run that higher global inflation will flow through to higher overseas interest rates that will weigh on the NZD if the Reserve Bank doesn't hike the OCR, with the lower exchange rate flowing through to higher local CPI inflation via it boosting export and import prices in NZD terms.

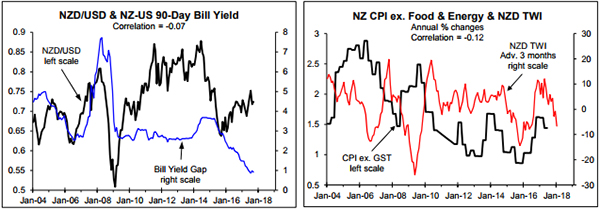

For this line of reasoning to be relevant there needs to be links between interest rate differentials and the exchange rate and between the exchange rate and local underlying CPI inflation. The left chart shows that since 2004 there is no link between the NZD/USD and the gap between NZ and US 90 day bill yields. It is a similar story no matter what interest rate differential is used. As covered in our monthly Forex Prospects reports, factors other than interest rates are generally more important drivers of the exchange rates (e.g. relative economic growth and NZ export prices). The right chart shows a very low negative correlation between the annual % change in the NZD trade-weighted exchange rate index (TWI) and NZ CPI inflation when the volatile food and energy components are excluded, with the peak correlation being with the TWI advanced or leading by three months. It is highly questionable whether there are any indirect links between global and NZ inflation that warrant linking stronger global inflation to a need for several OCR hikes.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

20 Comments

"with little link between underlying OECD/global and NZ inflation I question the merit of directly linking the outlook for the OCR to global inflation.

It's an opinion. of course, but why, is my question?

The Globe is awash with inflation - trillions of dollars/yuan/yen/euros etc of cash - at never before seen prices ( interest rates) and you only have to look at the NZ property market and the US stock market to see where that 'inflation' has gone. Ergo - there is a direct link.

But the bigger question is: "If all the inflation that we have generated in the last 9 years has done nothing to stimulate "CPI Inflation" then what will?" My answer is "Nothing" - until the price of money rises. And if that it reflected in OCR rises then when they come, they will come with a rush, and just like a coiled spring, release all the potential energy that 'inflation' has stored for the last decade.

(NB: The central banks, RBNZ included, need to step away from setting the price of money. Make lots of it if you wish - QE - or, set the price of what's already out there, but not both. The result of both is.... well, look around you!)

""If all the inflation that we have generated in the last 9 years has done nothing to stimulate "CPI Inflation" then what will?" My answer is "Nothing" - until the price of money rises. And if that it reflected in OCR rises then when they come, they will come with a rush, and just like a coiled spring, release all the potential energy that 'inflation' has stored for the last decade."

Ahh, whaaaa?

Do explain...

Inflation is an increase in the money supply - end of story!

The price of the money supply is embedded in all things - products physical and notional- so the higher the price of money, the higher the cost of 'all things'. Increasing the supply of money AND lowering the price of it is like Countdown baking 10 times as much bread as its customers want; lowering the price of it and telling them that 'If you don't buy more ( to raise the price - CPI 'Inflation') we will bake more bread ( QE) and lower the price again (The OCR etc)) It's self-defeating......and won't push up the price ( demand pull)

"Inflation is an increase in the money supply - end of story!"

No, that isn't end of story. You need to much better define the metric of inflation if you want to even try to argue that point.

As for the rest of that comment, you have a very interesting understanding of monetary economics.

"Inflation is an increase in the money supply - end of story!"

No, that isn't end of story. You need to much better define the metric of inflation if you want to even try to argue that point.

So we can safely relegate Greenspan's musings to the dustbin of history?

CHAIRMAN GREENSPAN. The problem is that we cannot extract from our statistical database what is true money conceptually, either in the transactions mode or the store-of-value mode. One of the reasons, obviously, is that the proliferation of products has been so extraordinary that the true underlying mix of money in our money and near money data is continuously changing. As a consequence, while of necessity it must be the case at the end of the day that inflation has to be a monetary phenomenon, a decision to base policy on measures of money presupposes that we can locate money. And that has become an increasingly dubious proposition.. [emphasis added] Read more

What you quote is very different to bw's statement that "Inflation is an increase in the money supply - end of story!".

In a broad stroke, it may be true. Fundamentally it is not.

I think you need to have a quick look at what's happened with US money supply and velocity.

https://fred.stlouisfed.org/series/M2V

https://fred.stlouisfed.org/series/M1SL

To get inflation you need an increase in GDP in nominal terms, GDP = MS x MV

Yes that's my understanding. Print all the money you like. But if it's just sitting on the sidelines, and resources moving into or recycling through whichever market stays the same, then there is no inflation. Start throwing more of that money after the same resources, and, well, the price 'inflates'.

The price of the money supply is embedded in all things - products physical and notional- so the higher the price of money, the higher the cost of 'all things'. Increasing the supply of money AND lowering the price of it is like Countdown baking 10 times as much bread as its customers want; lowering the price of it and telling them that 'If you don't buy more ( to raise the price - CPI 'Inflation') we will bake more bread ( QE) and lower the price again (The OCR etc)) It's self-defeating......and won't push up the price ( demand pull)

Would you care to explain how this applies in the case of Japan? Or does it only apply in English speaking countries?

Once money is created it must find a home somewhere. If it isn't in CPI or GDP metrics, then the correct methodology is to find where it is located, not ignore its existence.

'll be a little less subtle than Nymad - c'mon, really? Inflation is the factors of supply and demand coming together. When demand goes up putting stress on supply systems, cost can increase causing inflation. Note that greed can also be a cause of inflation, as increasing demand can also lead to people seeing an opportunity to put prices up to make more money per unit, or to control demand.

It is not an increase in money supply, this is more likely a consequence of inflation.

@bw Its easy to create headline inflation, give money to ordinary people. Its also easy to create money without creating headline inflation, give money to the rich.

You're assertion that the money created in the past is like some coiled spring, is pretty lose with the mechanics of money. In order for past money printing to become inflation you need to couple it to the goods and services economy. These transmission channels are well understood and are largely confined to fees charged on asset sales.

This is a relevant article & comments

https://wolfstreet.com/2017/10/02/chart-u-s-treasury-yield-v-euro-junk-…

"if we lived in a world in which massive amounts of money exist, but there are actually very few places to profitably engage that money, then wouldn’t we expect interest rates to be unusually low?"

Yip - growth is dead.

Ive been declared medically incapacitated and let go after 23 years and have had a 200k super payout.....where to put it......????....... an OBR event could be on the cards......

yes indeed - i wouldnt be keen on holding too much fiat currency when it breaks

id be thinking useful stuff which may get disrupted when supply chains seize up

If Jacinda gets in, Kiwibank, as it is a Labour sacred cow which will be bailed out?

Maybe 50% shares? and the rest spread around 4 other banks?

It is mad that high-risk Euro junk bonds are priced less than US treasuries, the least risky asset in the world. This artificial pumping of asset prices is likely to end badly - exactly how is not known but badly. Bigly bad.

yip can only conclude that the money printing / asset inflation is designed to delay the nasty feedback loop that the system is in fact bust.

It is temporary can kicking at best but it cant end well

You mean that it cant end well for everyone.

"The reasonably high correlation between NZ and OECD CPI inflation is largely because upturns and downturns in the oil price flow through to both at the same time. OCR decisions aren't supposed to be driven by short-term spikes and tumbles in inflation driven by the oil price but rather by medium-term inflation prospects."

An oil bull market is potentially a huge factor and could run a very long time.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.