By Zoe Wallis and Jeremy Couchman*

However, following an extended period of ultra-stimulatory global monetary policy, a number of central banks look poised to begin policy normalisation by raising official interest rates and reducing asset purchases and holdings.

A concern for us is what the withdrawal of QE will mean for global financial markets, and more importantly for the NZ economy. This note provides an explanation of QE, the impact it has had on the global economy, and the risks its withdrawal could pose to the New Zealand.

When central bankers go on a spending spree

Quantitative easing (QE) is a policy tool used by a number of central banks to purchase financial market assets on a massive scale in the hopes of stimulating growth and inflation. In response to the GFC of 2007-2008, central banks around the world co-ordinated stimulatory monetary policy to stabilise the global financial system – including cutting policy interest rates to near-zero levels and opening lines of credit when banks stopped lending to each other. However, despite significant stimulus, both inflation and economic growth remained sluggish in many developed economies in the years following the GFC.

In addition, the prevailing climate of fiscal austerity meant there was reluctance among governments to expand public debt to boost economic activity.

To counter this sluggishness, monetary policy was tasked with doing the heavy lifting and central banks such as the US Federal Reserve (Fed), the European Central Bank (ECB), the Bank of Japan (BoJ), and the Bank of England (BoE) all adopted unorthodox monetary policy as short-term cash rates hit zero lower bounds. Unorthodox policy included tools such as forward guidance (explicitly saying that interest rates would remain on hold for extended timeframes), negative interest rates, and massive asset purchase programmes or QE.

These QE programmes saw central banks hoover up public debt such as government bonds, private sector debt such as mortgage-backed securities (MBS) and, to a lesser extent, corporate bonds. By purchasing these securities, the aim was to inject cash directly into the economic system that would then be used by banks to increase available credit and foster growth.

Central banks’ QE programmes were used to maintain liquidity in the financial system and encourage lending, with the aim of boosting spending and ultimately lifting inflation.

However, the actual impact on the economy as a result of QE is somewhat opaque.

The general view held is that QE has helped drive up the price of debt instruments and therefore lower wholesale interest rates – particularly long-dated interest rates. The concurrent injection of cash from central bank asset purchasing encourages lending, investment, and consumption in an economy.

However, QE has also generated some unintended side-effects, including downward pressure on currencies in countries where QE has been utilised - resulting in claims of ‘currency wars’ whereby each country is trying to lower their exchange rate in order to boost their domestic economy. In addition, lower interest rates led to a search for yield among investors and as such drove up the price of global assets such as equities and real estate.

It has also been claimed that MBS purchases lowered the lending standards of US banks. Easier credit conditions could cause problems down the line if market participants have been under-pricing the risk associated with their investments - indeed this was a key feature in the lead-up to the GFC.

Finally, a key channel that QE operates through is the influence it has on market participants’ expectations for short-term interest rates. A demonstration of this was the so called ‘taper tantrum’ of mid-2013 that saw bond yields spike higher following the then US Fed Chair Ben Bernanke’s announcement that the Fed would start to reduce its asset purchases. Market participants reacted in part to expectations that tapering asset purchases also implied that short-term interest rates would rise faster than had been projected. The Fed had to delay the eventual tapering of asset purchases to December of that year.

The ‘tantrum’ was arrested following Federal Open Market Committee (FOMC) members using forward guidance on policy direction to assure markets that short-term interest rates would remain low well after asset purchases were reined in. Fresh asset purchases by the Fed were wound up in late 2014, but the Fed still reinvests principal payments and maturing securities.

Following the ‘taper tantrum’ episode, central banks have been a lot clearer in signalling the unwinding of asset purchases in order to reduce unnecessary financial market volatility.

Buying up the shop

The scale of some central banks’ QE programmes is staggering. The US Federal Reserve has total asset holdings of around US$4.5trn (an increase of over US$3.5trn since 2007), with the majority accumulated as a result of three purchase programmes named QE1, QE2 and QE3 that began in late 2008 (see chart below). The bulk (55%) of the Fed’s asset holdings are made up of public sector debt (US Treasury bonds) and MBS totalling around 40%. The US Fed started unwinding its asset holdings in October 2017, and has indicated that the process will be gradual and predictable. To do this the Fed is stopping the reinvestment of some of the proceeds on assets that mature.

The amount that the Fed has let roll off has started small, with up to $10bn per month from October 2017, which will be increased by US$10bn per quarter until it reaches US$50bn per month. Both the advance signalling and slow pace of the sell down by the Fed is deliberate to limit any negative fallout in financial markets. Nevertheless, the Fed’s balance sheet is envisaged to end up at a higher level than the circa US$900bn pre-GFC size. This is in part due to the need to meet the growing public demand for currency. However, QE is likely to remain a viable policy tool for the Fed (and other central banks) to help navigate their economies through the next economic crisis.

The ECB has a significant and ongoing asset purchase programme (APP) that includes asset-back securities, covered bonds, government debt and even corporate bonds, to the tune of €2trn and growing. On October 27 the ECB announced that it intends to begin tapering its asset purchase activity. From January to September 2018 monthly asset purchases will be halved to €30bn. The ECB stopped short of announcing an end date of asset purchasing and instead made a cautious statement that it was ready to up the level of purchasing if conditions warranted.

The BoJ has a relatively long history of using QE as a policy tool. Through much of the 1990s and 2000s Japan suffered a period of muted inflation, even deflation at times, and lacklustre growth. As a result, the BoJ undertook a QE programme in the early 2000s to boost lending by financial institutions. Following the GFC the BoJ has undertaken several iterations of QE, boosting its asset holdings (largely Japanese government bonds) to almost ¥500trn – approaching the size of Japan’s entire economy and equivalent in size to the US Fed’s balance sheet. More recently, the BoJ adopted a new policy of yield curve control, or adjusting long-dated bond purchases to steepen the yield curve and promote bank lending – banks typically trade on the margin generated by borrowing short and lending long.

Following the financial crisis the BoE also fired up its own asset purchase programme focused on the purchase of gilts (UK government bonds) from various financial institutions. In addition to UK government bonds, the BoE also purchased some highly-rated private debt. The BoE’s asset purchase programme target reached £435bn, after the Bank decided to boost the limit by £60bn in September 2016 in the wake of the Brexit vote. Since the Brexit vote inflation in the UK has surged as a weaker British pound has seen a jump in the cost of imported goods and services. The BoE has not signalled any near-term withdrawal of QE to counter rising inflation, instead focussing on using interest rates to tighten policy settings. The BoE hiked the official policy interest rate on November 2nd from its record low 0.25% to 0.50%, and signalled a very gradual hiking path – two quarter-of-a-point hikes over the next few years.

All’s well that ends well

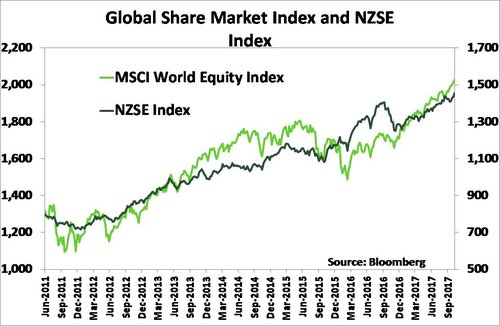

The ambiguity over QE’s influence on global financial markets and growth is matched by the uncertainty surrounding the possible fallout from its eventual withdrawal. At the extreme end, the unwinding of QE could cause a sharp correction in asset prices that have been inflated by the ultra-accommodative policy of the post-GFC era. A number of equity market indices (including the NZX) are now regularly punching through all-time highs and price-to-earnings ratios look stretched by historical standards.

Among developing economies, credit spreads (the margin between low risk and high risk borrowing rates) have narrowed to almost pre-GFC lows as investors have been hunting yield in increasingly risky areas. In housing, many markets around the world (including in NZ) have seen house prices diverge from fundamental benchmarks such as income. In Auckland for instance, the median house price-to-income ratio is well over nine times – well above the international affordable benchmark of three times income.

Among all these signals of frothy asset markets, measures of market volatility such as the VIX index (a proxy for risk aversion) are eerily quiet.

If we do see a sharp correction in asset prices, then the implications are severe for the global economy – possibly akin to another GFC. However, there are reasons to believe that a full-blown financial crisis is less likely this time; banks are better capitalised than prior to the GFC, and central banks are battle hardened and more capable at keeping the financial system from seizing up. Moreover, there are signs that the unwinding of policy will be less astringent on the global economy than some believe. For instance, markets look to have taken the US Fed’s process of policy normalisation with grace. The Fed has already lifted the Federal Funds rate four times since late 2015. In addition, the Fed is leading the pack by starting to gradually reduce its vast cache of assets – a process that it signalled many months in advance. The muted response from financial markets to date from the Fed’s policy announcement suggests that the cautious approach is working. The rise in US Treasury bond yields we have seen in the past year has been more a product of the Trump administration’s expected fiscal stimulus package rather than the Fed’s policy tightening.

Home comforts

For the NZ economy, the effects of the removal of QE are likely to be indirectly felt. The RBNZ has not undertaken any QE itself as the OCR, despite sitting at a record low of 1.75%, remains comfortably above an effective zero lower bound. However, financial markets are the main channel that the removal of QE will likely flow through to NZ. As global central banks start to sell down their asset holdings, global yields (specifically longer-dated ones) would be expected to rise and feed through to higher wholesale interest rates in NZ. Local banks would then pay more to source funding from the wholesale market, sending fixed-term mortgage rates upward – adding pressure on indebted NZ households. The other financial market impact is likely to come from a weaker NZ dollar. The withdrawal of policy stimulus offshore comes at a time when the RBNZ has signalled that interest rates will remain on hold until mid-2019 (although we expect interest rate hikes to start from late 2018). Interest rates differentials are likely to move in favour of offshore markets, leading to a decline in the NZ dollar, boosting tradables inflation and the export sector.

While we don’t believe that the NZ economy is in any imminent danger from a QE-induced global recession, it’s worth examining the implications for NZ of such a scenario.

If global asset prices fell sharply in concert, as monetary policy is withdrawn around the world, the next financial crisis could be triggered. Looking at the 2008 GFC for possible cues, there are two key channels that these events could impact the NZ economy.

First, NZ could be shut out of funding markets as global investors rush for safety. Global investors tend to shun commodity-based economies like NZ in times of crisis. This is a serious proposition for a country like NZ that relies on global financial markets to fund its capital account deficit. Difficulty faced by the NZ banking sector to access global funding markets would have significant consequences for the housing market as credit conditions tighten. The economy could then see confidence and spending deteriorate and further worsen a slowdown in the housing market – particularly if highly indebted households are forced to sell housing.

The second channel is via an eventual downturn in global trade, which we saw following the financial crisis of 2008. The export sector would face a hit to incomes and also pullback spending. However, depreciation in the NZ dollar would be expected to cushion the blow somewhat.

Fortunately, local policy makers are well placed to respond in the event of a worst case scenario. For instance, the RBNZ still has some wriggle room to cut the OCR if needed. In addition, NZ government debt as a share of GDP is low in comparison to many developed economies (currently net debt is 22.2% of GDP as at 30 June 2017). There is scope for increased government spending and investment if a global downturn deteriorates, particularly from a new Government that will want to prove its mettle when the chips are down. Moreover, with a shortfall of home building at present (particularly in Auckland), there is clear demand for investment – such as housing and transport infrastructure.

Conclusion

In response to the GFC of 2007-2008, central banks around the world adopted a number of unconventional policy tools, including the wholesale purchase of debt instruments or QE. The widely accepted view is that QE depressed long-dated interest rates and boosted demand for an array of asset classes. Some of the unintended consequences of QE, such as increased risk undertaken by investors in search of yield, may be sowing the seeds for the next global downturn. However, we don’t expect the unwinding of QE will tip the global economy into recession. Given central banks are likely to unwind QE in a controlled and predictable manner. In future QE is likely to be kept in the policy toolkits of central banks around the world as one of the last lines of defence in response to severe economic and financial crises.

The RBNZ did not revert to using QE following the global crisis. Nevertheless, the withdrawal of QE is expected to affect the economy the NZ economy indirectly via financial markets, both through rising longer-dated interest rates and a lower currency. If the unwinding of global policy stimulus tips the global economy into the next global recession, policy makers in NZ have room to manoeuvre to counter the fallout, including cutting the OCR further and instigating expansionary fiscal policy. Let’s hope they don’t need to.

Zoe Wallis is the chief economist at Kiwibank. Jeremy Couchman is a Kiwibank senior economist. This article was first published here, and is re-posted with permission.

32 Comments

By purchasing these securities, the aim was to inject cash directly into the economic system that would then be used by banks to increase available credit and foster growth.

The Federal Reserve credit created to purchase QE eligible securities ended up on the central bank's liability reserve ledgers to credit the respective authorised bank sellers. There has been no attempt by said banks to leverage these QE reserves under the moribund fractional reserve money multiplier facility using the current 10 percent reserve ratio. Under modern money credit creation regimes banks are unlikely to seek to use obligated reserves to underwrite any fresh credit fabrication when they better serve unencumbered as Fed required 30 day liquidity backstops. Read more

The effect of the Trump tax plan is dramatically worse than anticipated for other countries, including Australia, ( and by extension, New Zealand) because of a 20 percent excise on many goods and services produced outside the US.... the plan – to promote activity in the US, which will disadvantage the rest of the world....also invites other countries to do something similar so you would have a whole breakdown of what was the international tax rules by treaties if other countries follow suit. And that is really damaging to trade.

http://www.afr.com/news/policy/tax/trump-tax-a-de-facto-trade-barrier-2…

Great article, thanks. I find it amazing though, that the brightest financial minds in the world have only a faint idea of the consequences of QE and its unwinding

Well said Yvil :) I can only imagine the negative effect this will have on asset values as the tide goes out. The party funded by boat loads of cheap debt is over. It's now time for many a speculator to pay the piper.

R-P, I never said anything about "negative effects". Also, you're making up that "cheap debt is over"

Maybe they're not the brightest financial minds and more fool us for believing they were.

If we are talking about central banks and central bankers, then what does matter is money. It seems obvious to the point of absurdity in having to write it, but the last ten years and for even longer than that central banks have, to put it mildly, become less familiar with the subject. Read more

Great article, thanks. I find it amazing though, that the brightest financial minds in the world have only a faint idea of the consequences of QE and its unwinding.

Yes. Great article. Would be good if the Hosk could read this (and actually understand the nuance) and relay the message to his audience.

While the "experiment" unwinds, NZers still tend to think that we live in an insulated cocoon and our asset prices are driven by dynamics that have no relationship to this "experiment." Of course, that's nonsense as the ANZAC bubble would not exist without wholesale funding. People will say that mortgage funding can be sourced internally, but that misses the whole point that it's much better to use wholesale funding as the cost is cheaper (borrow low, lend higher).

NZ is in an insulated cocoon JC

You buy lots of rental houses and you’re sweet

If interest rates go up you just sell a house

The economy booms with highest ever level of migrants

You get cheap workers and sometimes you don’t even need to pay them

Everything’s sweet

Auckland property never goes down in value

Always doubles in value in just 7 years or was that 10 years Depends who tells story

Right now property is going up in value in Epsom & Remmers because everyone wants to live in congestion

It’s a no brainer

NZ is in an insulated cocoon JC

Subconsciously, that's what has been drummed into the sheeple by institutional power (unfortunately I think many of our leaders and role models actually believe it, which means they're oblivious to risk through interconnectivity) . Our media is the town cryer and often publishes nonsense articles comparing NZ to the rest of the world. This reinforces the beliefs that we're somehow unique and different). We've been told about our "success" but not actually been provided with any evidence-based harratives as to how that success has been achieved.

If it's any consolation, Australia is in the same boat. They also believe the bullshit peddled to them. It's not very healthy for society to become so superficial and malleable.

Im sure Tony Alexander would explain it better

Possibly. I think Rolling Stone and Matt Taibbi do a pretty fine job too. Much better than someone with vested interests like a bank economist.

Not be confused with QE

NATIONAL Australia Bank and Westpac were among global banks to borrow billions of dollars in emergency funds from the US Federal Reserve at the height of financial crisis.

NAB was the biggest user of the emergency facility among local banks, borrowing $US4.5 billion from the US central bank. NAB, which operates a small US bank, turned to the Fed three times as the crisis intensified.

A New York-based entity owned by Westpac borrowed $US1 billion from the Fed, at the time pledging more than $US3.3 billion in collateral to back the loan.

http://www.theage.com.au/business/nab-westpac-tapped-fed-20101202-18i58…

<

The net result for those countries that have QE is that their citizens are getting considerably poorer on a relative basis and that is causing resentment amongst the electorate hence people grasping at populist policies.

Unfortunately hard work and productivity is what is needed but the people have become lazy , blame other for their woes and so I expect an accelerate decline in the economies.

The 50 year outlook for the mature economics is not pretty.

Got any evidence for those claims? Most sources I've read suggest people are working more and harder but getting less of the pie, with the middle classes in a slow process of being hollowed out. This ultimately doesn't help, because who's then left to consume to drive the economy?

Sounds like another portrayal like "young people just need to save, they're spendthrifts!" when the truth is they're saving at higher rates than previous generations.

This book is worth a read: The Retreat of Western Liberalism.

At least we do not have to ever repay our debt to Society.

At least we only need a fixation about Houses.

At least we can hold our head high, and our rates even higher. Than EU, USA, any point on the Compass.

At least we can compare our rates as being frugal, not over extended and that we can bank on.

At least we can leverage our interest only mortgagees up to where the sun don't shine.

Not blindingly obvious, this Shadow Banking lark eh...or so a little bird told me.

I wish they would stop Yellen for me to pay back Your....debt.

Signed a Poor Rental, mental lentall...for flippin Houses...from A...to NZ. via HK and all points of the Compass.

Fed up, to the back teeth, QE..D.

Alphabetically and Financially Challenged. though I may be...

Trillions in debt..I ain't.

DOH.

PS...Twenty bucks an hour....Chicken fed....sorry...Feed.

Are they actually unwinding? or is it just a slight of hand. It looks like they're tag teaming.

(this was from a year ago - would be interesting to see an updated graph)

http://www.zerohedge.com/news/2016-07-26/global-central-banks-are-all-q…

I don't think anyone believes them anymore. The sharemarket sure doesn't.

Things seem to be picking up and central banks like to take the credit. It is possible that QE merely substituted government credit for private credit and thus had very little effect....

http://www.zerohedge.com/news/2017-10-31/qes-untold-story-chart-fed-cor…

The massive forced injection of foreign "capital" into New Zealand, forcing up house prices and such, is surely due more to the massive current account surpluses run by China and Germany. These countries' current account surpluses require current account deficits of an equal amount in other countries.

If the money stops flooding into New Zealand we have to earn a living by selling goods and services, rather than by borrowing from abroad to buy assets off each other or selling assets to foreigners and new residents. This is mediated by the exchange rate falling. The adjustment means we need a lot less real estate agents and builders, so it seems harsh at the time. We just don't need all the new people we have accumulated to produce the goods and services we already export.

As the tide goes out and events unfold, the stark reality our prosperity was never assured by selling houses to each other will set in. The prosperity simply never was - its all a highly leveraged illusion that can be easily taken away. Thanks to Winston, it will be all about exports. Just not sure if talking with the Kremlin is the way forward! Sadly, we are up against stiff competition from bigger countries in the same predicament. This is yet another obvious reason howling speculators with massive interest only mortgages will be shown the door. They are a risk to financial stability and serve only themselves.

Yes, when the tide goes out only the debts remain. The good thing is that NZ actually has a perfectly sound and functioning economy that will be freed from the oppression of excess foreign capital forcing up the exchange rate.

Yes, when the tide goes out only the debts remain. The good thing is that NZ actually has a perfectly sound and functioning economy that will be freed from the oppression of excess foreign capital forcing up the exchange rate.

The need to fund deficits is the reason for upward pressure on the exchange rate.

RW, you state: "The massive forced injection of foreign "capital" into New Zealand" Can you please explain that statement

Mervyn King says that :

Short term interest rates are controlled by Central Banks,

Medium term interest rates are infuenced by "mkt expectations" ( eg. inflation/deflation, risk .etc ),

Long term interest rates are influenced by the forces of supply and demand.

With Medium term rates, traditionally, Central Banks try to influence mkt expectations ( forward guidance etc ) but have no real influence on Long term interest rates

QE was all about controlling long term interest rates, lowering them . ( As Bernanke says in his book ).

Unwinding QE will allow Longterm rates to move to the mkt forces of supply and demand... Will be interesting to see if Long term rates rise..., and by how much ??

...and the answer is probably in your post! "Long-term interest rates are influenced by the forces of supply and demand." and yet misguided Bernanke et al went about "..controlling long-term interest rates, lowering them". If they truly wanted to affect supply and demand, then rationally they should have raised long-term rates!

The price of money is in all things, and lowering interest rates has just produced the 'unexpected' - a deflationary environment from which there is no probable means of escape....

A lot of detailed focus; and detail is important; but you can lose sight of the forest for the trees. My view of the big picture is that the world got into serious economic trouble because financial institutions were allowed to create unsustainably vast amounts of debt which was not supported by real assets. The inevitable crash took down the whole economy including the real economy. In response governments bailed the perpetrators and then pumped vast amounts of cash into the economy to try and stimulate investment and activity in the productive economy. This cash they used was not supported by anything real and is as imaginary as the debt that caused the problem in the first place.

The fiscal stimulus pumped up asset prices and speculation, but it's effect in the productive economy was muted at best and to make matters worse the lowering of interest returns had a chilling effect on peoples spending. In other words the assumption that these forms of stimulation would give a healthy boost to the real economy is wrong and all it did was pump up speculation and asset prices. This increase in asset prices and the passage of time have gotten us to a point where the fear has diminished and the real economy is starting to recover. I.e. a pretty obtuse link between the corrective measures and the desired result.

In the process however the side effect has been the creation of a huge world wide bubble in fixed asset prices, which just about takes us back to where our problems started.

Somebody with a few brains needs to come up with far better economic models that address these silly situations, because we seem to have gone around this track a few times now and it is past the point when something better needs to be done.

To take just one tiny example: term deposit rates.

When these went down, a good number of people left their money in them.

The resulting resident withholding tax that went to the govt reduced.

Unintended consequences.....

Chris-M

I'm quickly becoming a fan of yours. I find your post above brilliant, concise, to the point, without getting lost in technical jargon and also without heavy bias of the "brigade"

I'd be very interested in your opinion re the outcome of unwinding QE, if you'd oblige

I second that.

I have a long term view on that, which is probably well known to longer term contributors. There are only two options, keep printing or default. Once money is printed/created, it exists as debt somewhere in the economic system. It requires new money to be printed to pay the interest in the previous created debt. You decrease the rate of money creation then it results in default on debt somewhere. Think is that with the international flow of money, that debt could be anywhere. The real problem is that debt is matched as an investment somewhere, perhaps your kiwisave fund.

Think of this from another angle. The price of debt is so low because nobody wants it.

In all honesty I don't know. Our crazy management of economic crises has lead to a cycle of crashes from bubbles or over valued assets that has been addressed by fiscal stimulus that in turn leads to the next bubble. Looking at this history the easiest thing to say would be that we are due for another crash followed by another round of stimulus. The reality is however that we have not really got out of the last round of stimuli. If a crash happened in say 6 months time what is left for them to do? Scary. The "hit" of capital asset appreciation has lead us to a point where we are now totally addicted to the stimulus of easy money. Is it possible to wean us of our addiction and quietly deflate a bubble? That would take a hell of a lot of wisdom, very steady hands on the economic tillers and most of the worlds economies working together. - Pretty unlikely. The free and easy money has build asset bubbles in some parts of the world, some are truly scary e.g. Property in China. We also have large debt bubbles all over the place. These are just sitting there like bombs waiting to explode. Anything could set them off and when anything looks like it might the governments just throw more imaginary money at it, which ultimately just makes things worse. Added to this, the world is now facing very heightened social, political and security challenges.

What are the other choices, go cold turkey on debt, let the debt addicts suffer the consequences and preserve government intervention for saving the innocent and virtuous victims. We almost have to go through something like this before we can straighten out our messed up system. One of the fears that I do have is that the politicians could resort to a period of high inflation to inflate the problems away. This would be very unjust as it would reward those who messed up the system with all the debt fuelled activity while penalising those who have virtuously saved up bank deposits. I haven't answered your question I am afraid. The only advice that I can think of is to invest in things that are of real value, that will still continue to be needed regardless, and are not overpriced.

The only advice that I can think of is to invest in things that are of real value, that will still continue to be needed regardless, and are not overpriced.

Well...er...that really narrows the list down!

Am still trying to think of the first item on the list.

I know folk don’t enjoy recessions but Westrrn world and China have caused a huge debt mess by panicking into splurge of debt to avoid any downturns. Like not burning off scrub, this results in bigger conflagration later. That later is this year

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.