ANZ New Zealand's chief economist is suggesting the Reserve Bank may start easing its loan-to-value ratio (LVR) restrictions from the middle of next year.

Cameron Bagrie, ANZ's chief economist, says the first steps in the relaxing of the LVR restrictions on banks' high LVR residential mortgage lending could come next year, after the Reserve Bank's May Financial Stability Report.

"And what I mean by 'relaxed' is a marginal tweak in the first instance, as opposed to removing them completely. This would likely involve investors' deposit requirements being eased to 30% from 40% and perhaps some marginal relaxing of the speed limit for owner-occupiers, ie allowing a few more +80% LVR loans," Bagrie says.

ANZ is New Zealand's biggest mortgage lender with loans of $73.705 billion at June 30. The latest Real Estate Institute of New Zealand monthly figures show nationwide August house sales volumes fell 20% year-on-year, the equivalent of 47 less properties being sold each day. In Auckland sales volumes were down 21.5%. The August Auckland median price dropped $10,000 to $840,000 year-on-year.

Bagrie argues the case for implementing the LVR restrictions, which were introduced in October 2013 and revised in November 2015 and October 2016, was not overwhelming. And now that Auckland house prices are falling and household credit growth is running below income growth, people are deleveraging which is a sign the LVR policy may have "overcooked things," suggests Bagrie.

"LVR restrictions were always intended to be a short-term tool. The longer you leave them in place, the greater the potential for seepage and for lending to be diverted into unregulated channels. We do note that housing lending [growth] by non-bank lending institutions is currently running at 28% year-on-year, as opposed to bank lending at 6.9% year-on-year," Bagrie says.

The total value of non-bank housing lending, however, sits at just under $2 billion versus banks' housing lending of more than $236 billion.

Bagrie points out the impact of LVR restrictions can't be disentangled from the impact of other forces that have weighed on the housing market. These, Bagrie says, include the interest rate cycle turning, banks rationing credit to close their funding gap, overseas buyers being missing in action, and Auckland's underperformance versus the rest of the country showing affordability has been a key issue.

The risk is that the Auckland housing market takes off yet again after the initial negative response to LVR restrictions, he adds. Additionally Bagrie acknowledges demand-supportive forces remain evident including net migration hovering around all-time highs and interest rates being near historic lows. But, Bagrie says, "net-on-net" he believes we are closer to the day when these restrictions are relaxed.

Competition for deposits 'can ease up'

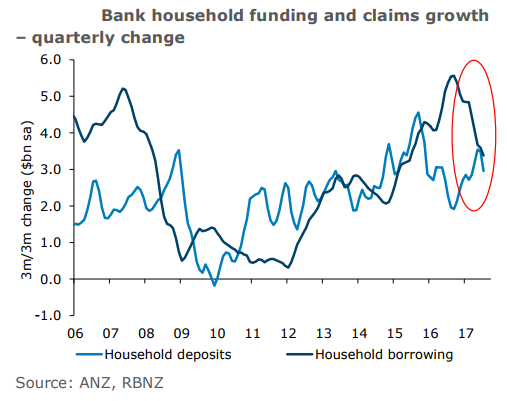

Separately Bagrie has been closely tracking the bank funding gap, being the gap between household deposits borrowed by banks and household borrowing lent by banks. When the housing market "took off" across the whole country last year, deposit growth slowed as interest rates fell and the funding gap widened.

"Pre-Global Financial Crisis behaviour was emerging again. That raised the ire of credit-rating agencies and the Reserve Bank, and once again increased New Zealand's vulnerability to the whims of global credit markets," says Bagrie.

"The problem New Zealand has is that it is already quite indebted, and the channelling of that international pool of savings into housing, which is not a productive investment, risks crowding out other forms of investment."

Banks have been getting more deposits in the door with deposit interest rates and borrowing interest rates both rising over the past year while wholesale rates haven't. Banks' rationing of credit, as Bagrie puts it, has worked.

"Annual housing credit growth is now running at 7.1%. But if we look at the annualised pace over the past couple of months, it is closer to 5%."

"That suggests some of the extreme competitive pressure we've seen in the deposit space can ease up, and the credit wheels can turn a little bit faster as we head into 2018. Both dynamics mean less pressure for retail interest rates to move up, outside of movements in the OCR and wholesale rates," Bagrie argues.

Trouble possible for developers

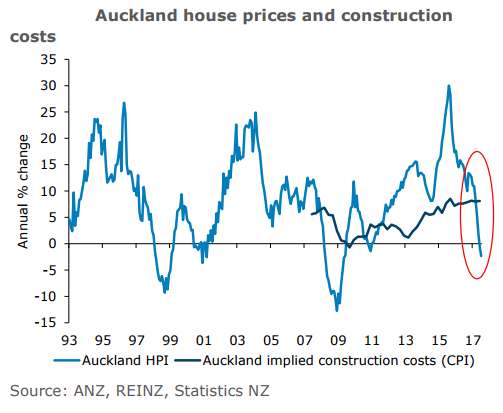

Meanwhile, Bagrie is also watching the intersection of falling house prices and rising construction costs, noting this combination could spell trouble for developers.

"We've seen a major listed company [Fletcher Building] take some big hits over a couple of projects. While that's non-residential work, one wonders about the residential area too. Real Estate Institute of New Zealand data shows Auckland house prices are down 4%. However, some suburbs are anecdotally down 10%. You take price falls of 5% to 10% and construction costs rising over 8% and whammo, you have no - or even a negative - margin. If we look at a different measure of construction costs - the value of consents per square metre - which has bobbled around between 10% and 15% per year, the story is even more worrying," says Bagrie.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

65 Comments

I wonder why ANZ would have different opinions than RBNZ? Could it be one has an invested interest in profit and the other does not?

Wow, a bank that doesn't like LVRs, who would have thought...

Snouts at the trough don't want gravy supply turned down.

Yes. the bank see deleveraging as being a bad thing. Haha. Funny. Most sane advice is that now that interest rates are low, you should pay down your mortgage, not increase the damn thing!

The problem New Zealand has"...So, Cameron, it does have a problem.

is that it is already quite indebted....Yes, Cameron, it is.

and the channelling of that international pool of savings into housing...Yes, Cameron, it does

which is not a productive investment ....Quite right, Cameron, it isn't.

risks crowding out other forms of investment....and the answer, Cameron, is to drop the very policy setting designed to fix all your above comments?

Stick to Retail Banking, Cameron. Macro Economic Policy doesn't appear to be your thing.....

Funny, you are like wow, I agree with all the macro things this guy is saying except one thing, well he must be an idiot at macro!

:-)

Here are a few important bits you missed:

"And what I mean by 'relaxed' is a marginal tweak

The risk is that the Auckland housing market takes off yet again

"net-on-net" he believes we are closer to the day when these restrictions are relaxed

Honestly that seems like a pretty balanced and nuanced view. I guess the CE of NZ's biggest bank maybe does know a thing or two about macro.

People forget, or don't want to know, about strangeling developers! ... If they stop building, as Cameron rightly explained, the whole market will rise again ... some naive people here also believe that the coming Gov has the holy grail of building and it will solve the issue of affordability and supply! .... maybe some of that will happen gradually in few years down the track, but not enough to make a big enough dent in the increasing demand ( which is mostly organic growth as David Chaston once explained)...

So cheering about falling house prices can backfire badly and accelerate countermeasures to hold prevent a carnage elsewhere .... Relaxing LVR gradually is actually a good call ...

As I and many often mentioned here - the Housing issue is not a simple problem , it is very complicated and multi pronged issue which needs careful handling.

Aren’t new builds generally owner occupied so they only pay 20% deposit anyway. So how would dropping LVRS effect this area

Lending for new building is exempt from LVR limitations, so difficult to see why relaxing LVRs will assist new building.

True, new built buyer are Owner occupiers ... but the lending constraints now in place on developers by the banks is that they need to sell most ( i think 80+%) of their projects ( or town houses / apart) off the plans before lending them any money - on the other hand banks stopped lending for off-the-plan purchases as there have been many developers pulling the plug on projects because of lack of funding --- at the end of the day it all goes back to various lending restriction imposed by the RBNZ one way or the other to cool the market ..... vicious circle drama - not straightforward solution ... Stats NZ said today that fewer homes were build y-o-y to August - just about 10,000 nation wide ... which is another factor in exacerbating the problem ...

http://www.sharechat.co.nz/article/7e48661c/nz-residential-consents-hit…

That is bad considering interest rates are so low. Aren’t low interest rates normally a time where housing gets better, not worse.

I would argue that even if restrictions are removed there is no guarantee that the situation will improve. Because asset prices are now so out of balance with incomes we have reached the situation where no one is willing to make a decision / take a risk (lend, buy, develop) because the consequences could be dire for any or all of the parties concerned - the market has in effect frozen. The only way I see out of this is for the central government to step in and take the risk.

Housing tracks affordability, not income.

that is not true at all ... developers and property investors are in the "business"of building and making a reasonable profit for the taking that risk and using their expertise and connections . ... business people take risks every day ! the market is well and alive but it is choked to control the run away of housing prices ...

You are only talking about the end users who are also constrained by lenders ( FHB are only 20% of the market) and there are people who CAN buy now if the lending is loosened a bit ....

There are buyers in every market and every price bracket .. each has his affordability issues - even the ones in the $1.5M - $2.5M mark !!

"There are buyers in every market and every price bracket .. each has his affordability issues - even the ones in the $1.5M - $2.5M mark !!"

That reminds me of my friend when he got a job for 300K a year a few years back after Uni. I was going to him his round, in front of his wife. She was saying to me that its not much money and I didnt realise how tough life was. I said yeah its tough knowing what colour your next Audi is. They solved that issue and just went with Black.

In context it not as much as Wayne Rooney makes or Bill Gates. But its a hell of a lot more then a fair number of people make.

More like banks sales guys not getting their regular bonuses because new ponzi debt leverage based lending is down. Property as an asset class is in la la land, and we should avoid having more petrol poured on the fire by the banks.

The distance between old homes and new homes is only going to grow. But if you have the money and you’d like a new home. Why not. But if builders, property developers, councils can’t match the prices people are willing to pay they better have a long think about there game. In the end if people leave that only makes things worse

While the problem is currently evident for developers - the issue is that the land prices need to fall sufficiently to provide comfortable margins on development. Anecdotally investors were previously paying well above the viable price of land on the expectation of future price increases and for land banking. News of a declining market may bring this land to the market at reasonable prices - hopefully before we see mortgagee sales of vacant land.

Meanwhile the banks are still making enormous profits.

I prefer DTIs rather than LVRs being the main tool for owner occupiers but it really looks like the ANZ is looking to revive the investor lending and if we have a Labour/NZF coalition we will see prices continue to correct so I doubt many will be keen to invest in a falling market anyway until it bottoms out.

I would like to see DTI for implemented for Owner occupiers and LVRs stay as they are for investors

Thegic - what do you base your comment upon that "the banks are still making enormous profits" ?

The banks make a return of about 12% p.a. after tax on their equity, (about 18% before tax). This is far above any reasonable cost of capital.

In comparison the RBNZ makes only about 6% on the Crown's equity in the RBNZ. Pitiful really, and shows that the Crown is not getting its fair share of benefits from money creation.

Peri - totally irrelevant what the RBNZ returns on the crown equity as a comparison. Yes banks make around a 12% return on equity which is about mid-point in the range that the NZX companies make (Google it). Anything less than that and a public company should not be in business, in fact over time wouldn't be. And if the NZ Aussie banks weren't making double digit returns, their allocation of their parents capital would be adjusted very quickly (read less funding for NZ business and house buyers etc). We can only hope that they continue to make acceptable returns.

Peri - the RBNZ's return on the Crowns equity is totally relevant to business profitablity equations. Yes youre dead right the banks make about 12% return and as I also point out to thegic here, (average of the NZX). But any public company that isn't consistently making double digit returns should not be in business. And for sure, if the NZ Aussie banks weren't achieving that at the least, their capital allocated out of Australia would be considerable reduced (read less funding available for business and house buyers to borrow).

thegic - I think you're confusing a big number with profitability. I don't suspect you'd say the same about the likes of Briscoes 28%, Restaurant Brands 20%, Hallesteins 16% etc that are 50-100% more profitable than the banks. Peri is right, the NZ banks make a return of about 12% on capital which is about mild-range in the returns that NZ public companies earn. They invest billions of dollars in NZ to garner that returns compared to a few hundred million at best with much of the rest.

For an industry that just 'clips the ticket' I think banks do pretty well for themselves. It's not like they produce 'real goods', I guess that's why a lot of people view the industry as parasitic.

Plutocracy - parasites ? The naivety of people about banking's place in the world is breathtaking. Banks do far more than just "clip the ticket" they take credit risk that ensures that "real goods" can be produced. Trying doing it without the credit risk being covered and funding being obtained. And is there a skill and risk in that, take a look at the BNZ of the 1980's who didn't have it and only survived in name through it's fire sale to an Aussie bank, try looking at nearly every NZ financial company in the 2000's who no longer existing. .

I'm not arguing, I'm just echoing common sentiment. The notion that they exist to 'sell debt' seems to irk some people. I don't think people generally have any issues with commercial lending, it's when money is funneled into non-productive areas of the economy that concerns arise. Luckily, housing is a productive part of our economy so this isn't a concern.

That is the wrong common sentiment ... Banks are the "Oil" of business and industry without them, and the money they make available, life will go back several decades and bartering would be very much in fashion again ....

You mentioned: " it's when money is funneled into non-productive areas of the economy " like what? If " housing is a productive part of our economy so this isn't a concern" ??

I guess you lost few readers here ....me included

Then I really don't understand the point you were making Plutocracy, and I'm not sure what the non-productive areas are that they "funnel" money into ? But I agree that the common man's undertsanding of banking is extremely limited but that doesnt stop them from making uninformed comments and perpetuating misinformation in areas such as "banking profits". I think its just a simple case of people for some reason seem to have a dislike of services that they have to use and "ultilities" seem to be the prime area for those (banks, power companies, councils, etc) - all very child like sentiment really.

An example of lending to the 'unproductive economy' might be if banks were lending money to people who were using it to speculate on property for capital gain. This has the potential to inflate property prices thereby enticing more people to do the same. This could conceivably create a form of 'pyramid scheme' which would be based on the premise of constantly rising house prices.

I dont have a problem with Banks making money, but I do have a problem with how they lend. Lending to people at 10 * plus DTI's, plus other instances.

I was a bank teller many years ago out of Uni we would get all these people come into the Bank on Friday and hand over most of their salary to pay off loans that had over 20% interest with AGC. I was only young then but I felt for these people, but AGC loved these people. I couldnt lend money at these type of interest rates to lower income people. These are the things I dislike about banks, people who are not highly educated in financials are taken advantage of. Its something I will never forget.

But I agree that the common man's undertsanding of banking is extremely limited but that doesnt stop them from making uninformed comments and perpetuating misinformation in areas such as "banking profits"

Exactly.

What banks do is to simply reclassify their accounts payable items arising from the act of lending as ‘customer deposits’, and the general public, when receiving payment in the form of a transfer of bank deposits, believes that a form of money had been paid into the bank.

No balance is drawn down to make a payment to the borrower.

The bank does not actually make any money available to the borrower: No transfer of funds from anywhere to the customer or indeed the customer’s account takes place. There is no equal reduction in the balance of another account to defray the borrower. Instead, the bank simply re-classified its liabilities, changing the ‘accounts payable’ obligation arising from the bank loan contract to another liability category called ‘customer deposits’.

While the borrower is given the impression that the bank had transferred money from its capital, reserves or other accounts to the borrower’s account (as indeed major theories of banking, the financial intermediation and fractional reserve theories, erroneously claim), in reality this is not the case. Neither the bank nor the customer deposited any money, nor were any funds from anywhere outside the bank utilised to make the deposit in the borrower’s account. Indeed, there was no depositing of any funds.

The bank’s liability is simply re-named a ‘bank deposit’.

anks create money when they grant a loan: they invent a fictitious customer deposit, which the central bank and all users of our monetary system, consider to be ‘money’, indistinguishable from ‘real’ deposits not newly invented by the banks. Thus banks do not just grant credit, they create credit, and simultaneously they create money. Read more

Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.

The reality of how money is created today differs from the description found in some economics textbooks:

Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits. Read more

.....the banking system does not simply transfer real resources, more or less efficiently, from one sector to another; it generates (nominal) purchasing power. Deposits are not endowments that precede loan formation; it is loans that create deposits. Money is not a “friction” but a necessary ingredient that improves over barter. And while the generation of purchasing power acts as oil for the economic machine, it can, in the process, open the door to instability, when combined with some of the previous elements. Working with better representations of monetary economies should help cast further light on the aggregate and sectoral distortions that arise in the real economy when credit creation becomes unanchored, poorly pinned down by loose perceptions of value and risks. Borio Page 17 of 38

“In a barter economy, there can rarely be investment without prior saving. However, in a world where a private bank’s liabilities are widely accepted as a medium of exchange, banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet.” Read more

After creating their liabilities banks are loathe to reward the owners (depositors) for the risks undertaken.

Great links, thanks Stephen.

Banks do not at any stage create a fictitious deposit. There is no need.

Imagine a bank has $0.

It loans $100 to bob and now the bank has -$100.

Bob however has $100 in his cheque account resulting from the loan. That deposit is literally there. So the bank now has a loan to the customer of $100 and a deposit from the same customer of $100. The bank is balanced with a net position of $0.

Banks do create money but they are not loath to pay depositors. The article implies the deposit isnt needed but it is.

Bob withdraws and spends his $100, now the bank is -$100, the bank must borrow that money back at midnight in order to balance and the bank will pay interest to achieve that.

Bank economists clearly have a vested interest in keeping house prices propped up as their employers have been loose with lending. Many customers risk negative equity. There should actually be a sentence at the end of these "independent" think pieces explaining the economist's employment relationship. Now why would we take away LVRs when they are starting to do what they were designed to do. Better our current slow deflation than a crash.

No way, it should be at the very start so we know before we read the article, oh wait...

ANZ New Zealand's chief economist...

Huh, look at that, right at the start.

I take it you work for a bank or in that line of business

It is a real shame that Interest.Co is really just a site for envious negative people apart from a few that always get shouted down by the negativity.

It hardly helps people make financial decisions as its slogan says.

What I would advise is that if people are selling their property then I would be buying if the numbers stack up!

If you are worried about the Auckland market contracting and the numbers don't stack up then look elsewhere, as Christchurch is going to grow significantly in the next few years and will be NZ s city of choice.

The Man has spoken!

There’s a third option, don’t encourage people to buy something in Auckland that is clearly over priced and they have every right to live it. Don’t blame the locals that can’t afford Auckland . Blame the government and RB that let overseas investors and local investors threw low interest rates and no restrictions get out of control. The fix isn’t sending the poor out , who’s going to pour your gas, a city needs to be for all people. Not overseas investors buying out the rich, the rich buying out the poor and the poor being kicked out. It’s over anyway the overseas investors is gone and depts threw the roof, it’ll take years to get over that. LVRS are only a small part of it and as prices go down and some go under water all dropping LVR will do is on paper give them a little fat in the property which would we good but hardly get house prices changing the direction they’re in. Down. And for the good. FHBERS DONT BUY FOR AT LEAST 6 months better still a year

The MAN 2 - heartedly agree with you on all counts. And having been to Chch recently, you may be understating it.

Nothing to do with envy you silly boy. Its to do with a bent and warped system that allows the asset class to engorge themselves to the detriment of non asset owners. I watch in dismay at the greed of boomers who refuse to see the obvious. I watch smart well educated young people getting burnt out and depressed with what the boomers are doing to NZ. You are such a dick.

"Nothing to do with envy" seems like a falsehood when its followed by "you silly boy."

Not when his handle is The Man.

Ive heard of people yelling out to other guys in sport say your the man, but not someone give it to themselves. Weird world we live in. I blame Facebook.

Not envious of anyone good on ya. Maybe envious of young footballers like Neymar, or rockstars. But Im taking it your neither a young rock star or an young awesome footballer making hundreds of millions.

But Im happy for you and Im sure most people are, maybe the handle makes it a bit hard to be happy.

Property is nice but I like people like Rod Drury, who create global scalable businesses. Thats the type of business I want.

But as for property I just want property affordable for the average Joe or Joette. Not sure how that can get misconstrued any other way.

Yes, let us please distinguish a true tall poppy, from the likes of Val and Stephen Adams to Dr Lance O'Sullivan and even Bill Gates (who I reckon is kind of an accidental multi billionaire) from a rank weed, shall we?

People going around buying up existing property are most definitely not in the former class. Get out the brush cutter.

Here is another tall poppy, I do not think $$$ are the only way to measure this by https://www.stuff.co.nz/national/96827225/hurt--hope-christchurch-volun…

Fair comment Laminar. And I actually thought about the same thing you said before I commented. I'll guess I'm aware of a blight in journalism with promotional articles, political commentators employed by political parties etc. Generally, in publications I am used to seeing a couple of sentences, usually in italic font, emphasising the potential conflict of interest of a contributor. While you may pick up on this potential, a lot of readers don't and there can be a blurring of interest unless it is spelt out. I am actually one of those people who used to just naturally assume no bias with these economists till I thought it through. Another classic in the media used to be the Police Association. People assumed they spoke for the police. They in fact were a union, and probably needed to be announced as "Police Association union spokesperson...". Im just aware this is a slippery slope.

Well we agree on the importance of bias. Interestingly though bank executive relationships with their CE are often strained and the CE's generally insist on a degree of separation. A good example is Tony Alexander who has had rather extraordinary disagreements with his past CEO.

Bagrie has in the past distinguished himself by making tranche lending strategies known to the broader public. This approach of breaking up loans in to smaller parts that roll over in sequential years costs banks money but avoids a lot of sob stories. He said this at the same time as ASB famously raised interest rates just weeks before an OCR cut, with their economics team claiming the OCR would likely be rising soon.

Exactly Laminar - they are frustrating type comments seen all the time. As someone who has worked with several bank CEs and more than one bank over the years, I haven’t seen one that was influenced by the bank itself in the way people state (and I saw no evidence that the banks even attempted to) - the economists might listen to people opinions, but they are fiercely protective of their views as they have reputations to protect - its hard enough getting forecasts right without having others or worse your employer trying to direct you. Another case of people assuming the worst, which probably says more about them than the economist

Commercial buildings seem to tick along much more balance. Without massive booms and bust. I have to pay 40% deposit with a maximum loan period of 15 years . Your payments are a lot higher so you pay it of quicker . Maybe housing could learn a thing or two here. But of course people greed for more will never let this happen. O my god pay something off , NO WAY

Commercial carries quite a bit more risk which is why its LVR requirements have generally been stricter. Commercial is exposed to a much greater chance of long term vacancy and is subject to loss of tenancy resulting from an occupants financial failure more often than residential.

I never said it didn’t, I have commercial and you can also get good leases and they pay the outgoings and most of the interior work and GST. But looking at housing at the moment I’m simply saying if housing investment property was left at 40% deposit and put to 15 years the risk might be better. After all they’re both investment and MAYBE investment housing should be separated from housing owners occupied. It’ll be investors mostly making these bubbles . The same focks that want the LVRS lowered. And to tell the truth most people couldn’t afford to go commercial. You need money and housing investors of today are just money movers and with high LVRS they’re stuffed . That why the banks are crying

LVR requirements should represent the relative risk to the institution of A) having to make a recovery against the asset and B) the likelihood of that assets value falling, so it would not make much sense for residential and commercial property to have the same lending policies.

This idea that investors are a bunch of morons willing to pay anything for property is ridiculous. If you sell a property for a good price its not likely an investor buying it. They tend to think about these things with care and make less emotional decisions. Investors will usually target higher yielding areas, properties that carry discounts due to been run down or are in some way less favored by home owners who bid emotionally, typically don't understand the market they are in and frequently over pay.

LVR restrictions will very likely be used to slow climbing markets and to soften the landing of falling markets, that is stability. Banks are not crying and this economist made some very balanced statements.

To be honest four years ago the reserve bank might have hoped that government might have moved on housing supply by ammending the RMA, incentivising local authorities to concent and/or offering tax breaks or rebates on new building. However of there is one thing we've learned over the last four years it's that we can't underestimate sheer obstinance of government on even modest housing refom.

Good point, its funny how central banks seem to forever be sucked in to believing that the govt/markets are competent and will correct issues in anything approaching a timely manor.

The world's economy is a total s$#t f@*k waiting to happen. Huge debt, low productivity, finite resources, nothing left in the stimulus bag of tricks. Unless someone actually decides to start spending lots of money on infrastructure (Trump promised to but still hasn't) it's hard to imagine how we can turn this frown upside down. Baby boomers are now retiring, a huge population that will require unprecedented pension and health expenditure from countries with high debt and ugly deficits. Demographically over 60's have a very deflationary effect on an economy so whilst they may be sitting on asset wealth in inflated housing prices, in many countries across the world, there has never been an exception to the spending habits of this age group.

So if Bagrie, or any other economist wants to present a honest forecast for how this will affect us, then i'd be really interested to listen but as it is, all I am hearing is the same old techniques and solutions that have frankly, delayed the pain and done nothing to prevent it.

Plenty of studies have shown how monumentally rubbish human beings are assessing risk. We overstate potential upsides and understate or completely ignore downsides. I look, and I look, I read and I read, but all I see on the economic horizon for NZ is a cluster f*%k.

It's not about jealousy. I'm not egging on the "Great Reset". I just kinda think it's inevitable when I look at the data.

Thats not really difficult to see but its difficult to time. They don't call Japan the widow maker because a countries demise is hard to predict as occurring 'at some point'.

Well if we just look at the demographics, the baby boom was a bell curve, and because demographics are so incredible reliable (compared to most other measures anyway) we can at least look at the timings of that factor. So the top of the curve would have most boomers dying 2030-2035. But the cost economically in health and pensions, and the deflationary effect on their lower spending as a huge population, will be felt from now.

If Gen X had been bigger generation than boomers, it wouldn't be so much of a problem, but Gen X are much smaller. It's hard to see how a larger preceding generation can be funded by the tax revenues of a smaller following generation. Now, IMO this is a huge reason why, the countries that are popular for immigration are allowing huge migrant populations in. Most immigrants are of working age.

Yes thats a reasonable example of how to make an assumption and get caught in a widow maker trade. Just looking at any one factor is basically flipping a coin because you're working with almost no data. I can see your logic and its hard to argue that the path the west is on ends well but i dont agree that you can just look at demographics and time a major decline.

That's basically the flawed premise Gareth Morgan used in his 2006 Book, 'Pension Panic'. Lucky I didn't follow his advice or I'd be over $1,000,000 worse off.

Ex Expat. The world economy looks extremely different now that in 2006 and I don't have a clue what financial advise Gareth Morgan offered then.

I am certainly not making any financial suggestions and the issues I am presenting are factual demographic factors not speculation. How the markets and global economy cope with the factors *is* entirely open to speculation sure, but I certainly haven't presented a premise or suggested any particular financial decision be based on that so your million is here nor there (although well done for finding a way to flash your wealth).

All I have said is that a few of the aforementioned demographic factors will have a defationary effect on the economy in various countries between now and 2035. And that the world economy is in bad shape to weather the next recession, unless very different tactics are used, which is purely my opinion as I clearly stated.

I agree with Laminar that timing such matters is impossible.

GM advised that people get out of residential property, particularly family homes due to demographic based demand reduction. He didn’t take the possibility of immigration into account, hence he was way off.

As for mentioning the amount, it’s not unusual apprecation for Auckland’s Eastern Suburbs over the last decade or so. In real terms it has no meaning as it’s not money I intend to ever spend. It will be preserved for my children to hopefully ensure that they can afford their own homes. The reason to mention it is to highlight how big an impact the forecasters can have on our lives if we follow their advice. Bernard Hickey was very vocal during the GFC, but he and GM were very wrong. Who knows, they might be right in the next decade, but that’s little comfort when we all have a finite life. It sounds like you are a lot younger than I am. Another decade will take me to superannuation age. It’s vital to have a mortgage free home to be able to live on that. If I’d followed Hickey and GM I would be facing a retirement without a home.

Laminar, I wasn't suggesting that you could only look at one factors and time a decline. I was just discussing one particular factor that is predictable. There are obviously infinite factors that could change the picture. A major war, major infrastructure investment, debt forgiveness, some new tech or invention that changes how we live opening up new growth areas, continued mass migration, change in global economic theory etc etc. Certainly not a widow maker urge to put all wealth in one highly speculative investment?

A fine demonstration of why demand-side tools won't fix a supply-side problem.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.