Today's Top 10 is from interest.co.nz's own Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

1) Luck running out for the Lucky Country?

Over the past few months I've published a series of articles about heat on the Australian parents of New Zealand's big four banks, and concerns about the Australian housing market. These have mainly run in interest.co.nz's daily subscriber email. With the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry the culmination of years of disgruntlement with banks' conduct and culture, one concern is the Royal Commission may be the catalyst for a credit crunch.

The argument here is that Australian banks will be forced to tighten lending standards and Australian regulators will have to enforce existing standards and rules more firmly than they have perhaps done so previously. This means the flow of debt to an already softening housing market slows, risking a significant housing market correction and potentially Australia's first recession since 1991.

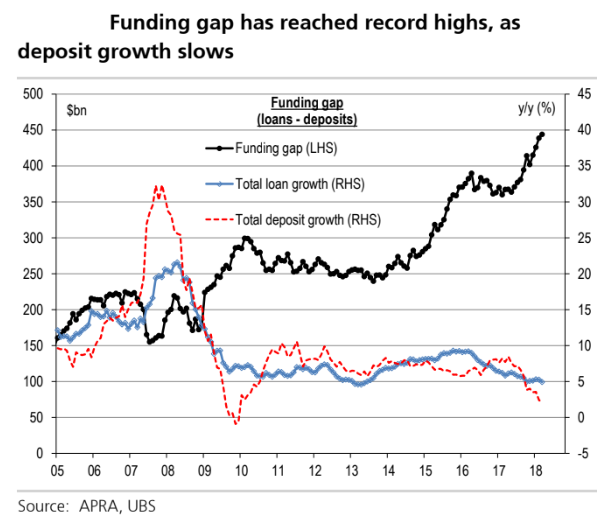

Prime pushers of this argument have been banking analysts and economists at investment bank UBS. As noted on Monday, UBS highlighted the weakest deposit growth since 1991 (yes, that year) of 2.4% year-on-year, has left Australian banks' with a record high funding gap of A$444 billion. The funding gap measures the differences between loans and deposits.

"It now appears that higher funding costs are likely a new structural feature of the Australian market. While the initial widening may have been sparked by moves in global markets, the persistence seems to be driven by domestic factors including a wider funding gap, slowing deposit growth and the bank levy," UBS says.

Given the subsidiaries of the ANZ Banking Group (ANZ NZ), Commonwealth Bank of Australia (ASB), National Australia Bank (BNZ) and Westpac Banking Corporation (Westpac NZ) almost completely dominate the New Zealand banking sector, these Australian issues must be at the top of our 'keep an eye on it' list of overseas economic and financial issues over coming months.

2) Like New Zealand's, Aussie immigration has been surging.

Regular interest.co.nz readers will be all too familiar with how strong New Zealand's immigration has been over the past few years. It has been one of the hot topics on our website, and a hot political issue too.

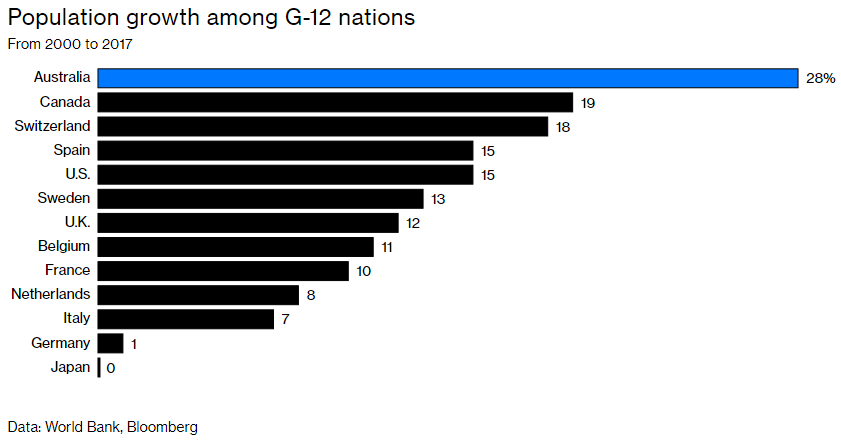

But we are not alone in experiencing strong immigration over recent years. Our Aussie cobbers, as Bloomberg reports, are poised to hit a major milestone.

The country’s head count will hit 25 million sometime this month - an incredible three decades sooner than the government had originally predicted in 2005.

Apparently one new person arrives in Australia every minute.

Under a framework that has been in place since the late 1980s, migrants applying for residency are scored on criteria such as English-language ability, education level, and professional skills. While the system has often been cited as a model for countries seeking a more managed approach to immigration, Australia’s largest cities are starting to strain under the continued influx, which is equivalent to one person arriving every minute.

Some of this sounds familiar on this side of the Ditch.

Some may scoff at the thought that 25 million people makes Australia - which in terms of land mass is the sixth-biggest country in the world - feel crowded. After all, there are cities in Asia with a population bigger than that. Yet the majority of Australia’s 3 million square miles is uninhabitable desert, and even many of the greener parts along the coast struggle to secure adequate supplies of fresh water and face periodic drought and wildfires.

For residents in cities that have traditionally ranked among the world’s most livable, life is getting tougher. Home prices are high, roads clogged, classrooms overcrowded, and wages stagnant. Many Australians blame immigration - and inadequate planning to cope with it - for the problems.

There is one clear winner: the economy. The nation, whose fiscal year ends on June 30, just marked its 27th year without a recession. New arrivals have been a key driver of that remarkably long streak: Annual population growth that’s averaged 1.5 percent for the past four years has essentially produced the equivalent gain in gross domestic product.

Things don’t look nearly as rosy when measured on a per-person basis, though, so even as the country as a whole gets richer - and some businesses and individuals prosper - many aren’t feeling the benefit, as wage growth remains near record lows.

And;

The consequences of curbing immigration could include falling house prices, reduced workforce participation as the population ages, and shrinking tax revenue.

David Chaston has done some number crunching for me, and says on the Bloomberg chart below NZ would sit just below the Aussies at 25.8%. At the end of 1999, the NZ population was 3,851,100. At the end of 2017 it was 4,844,400.

Moving onto one of our much smaller neighbours, where my family and I enjoyed a holiday during the recent school holidays, China's growing influence in the South Pacific can be seen. According to the Samoa Observer, Samoa's debt to China increased to $410.01 million in 2017 from $315.16 million in 2013, having at one point hit $439.40 million. The money owed to China is a significant chunk of the Samoan Government’s total debt, which stands at $1.1 billion.

The debt to China, according to renowned South Pacific journalist Mike Field, is equivalent to $812.25 for every Samoan. Not a small sum in the context of Samoa.

Every man, woman & child in Sāmoa owes China US$812.25https://t.co/V3gE9w2Isj

— Michael Field (@MichaelFieldNZ) August 1, 2018

Jack Ma is best known as the co-founder and executive chairman of Alibaba. However, he also has an interest on the side that appears to be doing pretty well. It's called Ant Financial Services Group. The Wall Street Journal has the story.

It handled more payments last year than Mastercard, controls the world's largest money-market fund and has made loans to tens of millions of people. Its online payments platform completed more than $8 trillion of transactions last year—the equivalent of more than twice Germany’s gross domestic product.

Ant certainly sounds like one to watch, especially given it's courting the wrath of China's state controlled banks.

China’s banks complain Ant siphons away their deposits, causing them to pay higher interest rates, and is a factor leading them to close branches and ATMs. One commentator at a state-owned television channel described Ant’s huge money-market fund as “a vampire sucking blood from banks.”

The authorities are also weighing whether to designate Ant a financial holding company and require it to meet bank-style capital requirements, people familiar with the matter say. That would likely affect its profits, which last year came to $2 billion, pretax, on roughly $10 billion in revenue.

Investors remain spellbound, rewarding privately held Ant in June with a $150 billion valuation on paper, more than twice its valuation in a 2016 funding round and above that of Goldman Sachs Group Inc.

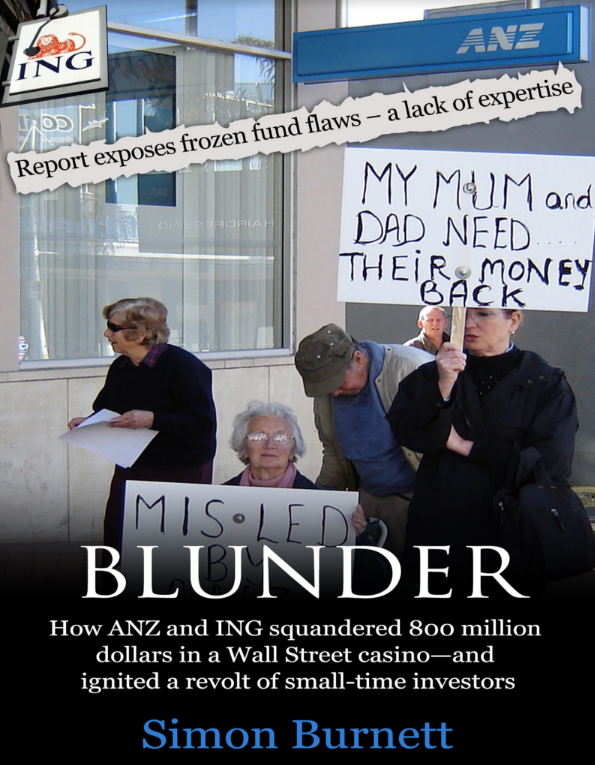

Ex-Pat NZ journalist Simon Burnett has published a book on the ANZ-ING frozen funds debacle from a few years back. Burnett acknowledges he was an investor and protested outside an ANZ branch.

The ING Diversified Yield Fund and the ING Regular Income Fund were frozen in March 2008, affecting around 15,000 investors and $520 million. In 2010 ANZ and ING agreed to pay investors $45 million to settle a dispute with the Commerce Commission over whether they misled investors. Investors had also been able to recoup money through an ANZ and ING settlement offer, receiving compensation from ANZ or through the Banking Ombudsman, or by claiming adjustments on tax losses in relation to their investments.

Burnett notes he got 66.46% of his original investment back, with others getting a full refund and some much less.

In these days of an FMA and RBNZ review of bank conduct and culture, the ANZ-ING frozen funds debacle from a decade ago is a salutary reminder of how financial services firms can mis-sell unsuitable products to retail investors.

Here's Burnett;

The ING sales pitch—which the ANZ presented to its customers—was cleverly worked out. The funds were not made to sound too good to be true because the targeted risk-averse bank depositors were unlikely to respond to such lures. Most depositors were aging and intent on preserving capital. So ANZ/ING played carefully. The returns were said to be similar to rates offered by the likes of Southern Cross Building Society; “hardly what you would call aggressive investment behaviour,” said Auckland accountant Hector Fsadni, who invested money in one of the funds. “The risk-free rate plus 2 percent was thus presented as akin to a term deposit,” said an Auckland fund manager, Norman Stacey.

The ANZ identified the depositors it wanted to hit, and its advisers picked up telephones. If anyone proved reluctant, the advisers called again ...and again, as in my case. The insistency was matched by the beguiling Pied Piper sales tone. . . this was a deal you couldn’t refuse. Some ANZ advisers strongly implied that the bank would need to go broke before the investments became endangered. Economist and commentator Gareth Morgan said, “The advisers are totally ignorant. They’re not advisers at all. They’re product salesmen.”

They certainly did not know what they were selling. The likelihood of any banker both knowing enough about an item as Byzantine, convoluted, fraud-filled, and opaque as a CDO and, at the same time, possessing sufficient talent to be able to explain this to a layman was zero—as becomes clear in this book. Most would not have bothered trying. Many of the worst advisers in New Zealand are employed by banks, according to Naomi Ballantyne, who quit ING in 2009.

6) Lipstick on a pig?

Parliament's Economic Development, Science and Innovation Select Committee has reported back to the House on the Financial Services Legislation Amendment Bill. This bill includes measures aimed at reducing misuse of NZ's problematic and flawed Financial Service Providers' Register (FSPR), something I've written about at length over the past few years. Basically the problem has been anyone from anywhere can register a company on our FSPR and then target investors/customers anywhere in the world, resulting in many scams and rip-offs conducted by NZ companies in all corners of the world.

The Select Committee is recommending changes. These are improvements. But I'd still rather see the FSPR scrapped altogether given MBIE's reasons for its existence don't stack up in 2018. The key changes the Select Committee recommends are below.

Clause 64 of the bill would insert new section 7A into the Act, amending the requirements for entities wanting to register on the FSPR. It would remove the current “place of business test” for registration. Instead, it would require anyone wishing to register on the FSPR to provide financial services to persons in New Zealand, or to be licensed under other New Zealand legislation, or to be required by other New Zealand legislation to be registered on the FSPR.

We consider this requirement important. However, we accept that it may result in the loss of oversight of some providers that genuinely provide services from New Zealand to persons overseas. We accept that the Government needs to be aware of these providers to comply with international standards on money laundering and the financing of terrorism.Additionally, clause 84, amending section 44, would allow regulations to require companies on the FSPR to inform clients or other persons that registration does not mean active regulation and oversight. Clause 72 would amend section 16 of the principal Act to allow the Registrar to obtain information about the extent to which a provider provides a service in New Zealand and to deregister companies that do not provide the information. Clause 74 would amend section 18 of the principal Act to enable the Registrar to deregister companies that misrepresent the extent of their involvement in New Zealand in breach of such regulations. We consider these measures sufficient to combat misuse of the FSPR.

We recommend amendments to new section 7A, inserted by clause 64, to ensure that all New Zealand financial service providers to which the Anti-Money Laundering and Countering Financing of Terrorism Act 2009 applies are still required to register on the FSPR (subject to any exemption in the Act).

7) Fancy some food from Fukushima?

Some seven years after a nuclear crisis following the massive tsunami, testing apparently shows no radioactive threat from produce in Japan's Fukushima. But would you eat it? According to The Japan Times, local food producers and fishermen are still struggling to win over consumers both in Japan and overseas.

But local producers say they still face crippling suspicion from consumers.

More than 205,000 food items have been tested at the Fukushima Agricultural Technology Centre since March 2011, with Japan setting a standard of no more than 100 becquerels of radioactivity per kilogram (bq/kg).

The European Union, by comparison, sets that level at 1,250 bq/kg and the U.S. at 1,200.

It seems consumers aren't bowling each other over in their eagerness to buy food from the Fukushima region.

The Fukushima disaster has devastated a previously flourishing local agricultural sector.

“Profits have not yet reached pre-2011 levels and prices remain below the national average,” said Fukushima representative Nobuhide Takahashi.

The situation is even worse for fisherman, many of whom have survived only on compensation paid by the manager of the defunct Fukushima No. 1 nuclear plant, Tokyo Electric Power Company Holdings Inc.

The tsunami destroyed ports across the region and demand for Fukushima seafood is low despite an even stricter testing standard of 50 bq/kg.

“When we catch fish and send it to market in Tokyo, some people don’t want to buy it,” said Kazunori Yoshida, director of Iwaki’s fishing cooperative.

As a result, fishermen brought in just 3,200 tons of seafood in the area last year, down from 24,700 in 2010.

8) Trump cops it on Twitter.

I was planning to make this a Trump free zone. But I just can't resist this crack at the US President. In one of his recent Twitter barrages Trump suggested his former campaign chairman Paul Manafort, who is on trial for bank fraud and tax evasion, had been treated worse than Al Capone. Below is one of the responses this elicited.

The main difference between Al Capone and Donald Trump is that we've actually seen Al Capone's taxes.

— Nick Jack Pappas (@Pappiness) August 1, 2018

9) Manafort highlights America's kleptocracy problem.

According to Franklin Foer in The Atlantic, Manafort's plight is a wake-call for the United States to awaken from its slumber about the creeping dangers of kleptocracy. His is certainly an interesting tale.

So much about America’s view of itself resists accepting a disturbing reality. Conventional wisdom long held that America’s free market would never tolerate the sort of clientelism, nepotism, and outright theft that prevailed in places like Brazil and Italy. Americans thought that globalization would export the hygienic habits of this nation’s financial system and its values of good government to the rest of the world. But over the past three decades, the opposite transpired: America has become the sanctuary of choice for laundered money, a bastion of shell companies and anonymously purchased real estate. American elites have learned to plant money offshore with acumen that comes close to matching their crooked counterparts’ abroad.

Manafort is one of the architects of this new world order. During the 1980s and ’90s, he provided strategic advice to the thuggish dictators who served as proxies for the Reagan administration’s anticommunist foreign policy. With his mastery of American media, he helped sanitize crooks like former Philippine President Ferdinand Marcos and his wife, Imelda - the symbol of their rule, the 3,000 pairs of shoes she owned, was still fewer than the number of people killed by the regime. These dictators (also Angola’s Jonas Savimbi, the Congo’s Mobutu Sese Seko, and Kenya’s Daniel arap Moi) should never have been respectable figures in Washington. But Manafort reinvented them as latter-day Thomas Jeffersons, allies in the cause of democracy, and successfully lobbied for them to receive arms and aid from the U.S. government.

10) A goal mash-up.

I love the World Cup and always try and watch as much as I can every four years. For the first time ever this year someone else in my house watched more than me. My eight year-old football mad son. This is a New York Times link I sent to him recently that nicely highlights the Latin American enthusiasm for a goooooooooooooooooooooooooooal!!!!!!!

20 Comments

Re: #2, Australian immigration.

The Guardian essential poll: 64% of Australians think their rate of immigration is too high, and 54% think Australia's population is growing too fast.

https://www.theguardian.com/australia-news/ng-interactive/2018/apr/24/t…

Do the same in NZ

You would get an even higher dissatisfaction in Auckland

Rural NZ would either not care or be outright dismissive and say Auckland deserves all it reaps.

Jack Ma's pre-tax profit on Ant seems too good to be true - 20%? who's he ripping off?

Good heavens. We don't need central bankers being bestowed chiefly status.

Oh shit we are in trouble...

That was a great article though Gareth. Thank you

his own Harem was a logical next step.

It is astonishing that Australia's population hit 25M thirty years before it was predicted to just thirteen years earlier. Things can change very rapidly.

Just shows what a useless measure GDP really is when importing 'the Third World' and Third World Values, is the only way to sustain it year on year.

Agreed. Australia's permanent migration programme is in complete shambles. Businesses use these to keep wages low while consumer demand and profits soar in the name of skilled migration.

Just look at these statistics published by the Dept. of Home affairs on the skill stream of migrants:

Between 2011 and 2017, more PR visas were issued to cooks in Australia than to software engineers, developers and programmers combined.

https://www.homeaffairs.gov.au/ReportsandPublications/Documents/statist…

#3 And who is Samoa gonna vote with every time they get the chance?

China could buy all the Pacific Islands (NZ included) for a rounding error on their balance sheet....

And that is "free market" in action.....

Overseas Investment Bill seems to be making progress, they were on Part 3 of 4 by Thursday night.

Also supplementary order papers seem to be only by the minister.

End of next week ready for third reading perhaps?

ANZ ING Frozen funds was a deceitful manipulation of conservative investors, it was amazing that all these people gathered together not knowing each other to hold a powerful financial institution to account and won!

ANZ had not counted on some of these people being clever and connected.

Simon Burnett's book is an excellent read, 10 years on investments around today have familiar look to them.

Connection became our tool on the road to defeat these banking giants , the days of divide and conquer for the banks was no longer as the internet joined our group as one . We were always one step ahead of them , one of the crowning moments being the ING/ANZ road show a second attempt by these banks to convince investors they had done nothing wrong and this was simply the investments affected by a down turn . Anyway we ripped them apart with a plan that got stronger from Invercargill to Auckland . For a blinding read about a monumental David versus Goliath victory factual story Simon's book is a must read .

One commentator at a state-owned television channel described Ant’s huge money-market fund as “a vampire sucking blood from banks.”

Haha awesome, makes a change from the banks sucking blood from everyone else.

Many thanks to Simon Burnet who has worked for many years now creating a book that records the ING/ANZ debacle . Thanks also to those of us who took these banks to task and spent many long hours planning and carrying out our protest .

Oh what a wonderful thing hindsight is! People nowadays working themselves up into fits of rage over the deceitfulness of banks knowingly selling CDOs not worth the paper they were printed on. Disgust at dishonest sales staff that didn't know that these things were much riskier than the punter was expecting.

The big flaw in this view of course is that in the mid-2000s, only a tiny handful of people did know how toxic these things were, and i'll bet not many of them had the full picture. S & P and the other agencies were giving CDOs AAA ratings, financial experts had worked out theorums and formulae to prove these things were solid, and the sales staff were just as knowledgeable about the risks involved as practically all financial journalists.

I have never been able to work up much sympathy for the investors. They bought into a product that was not sold as "risk free", as is obvious due to it paying 2% above the risk free rate, just before the biggest financial crash in 70 years. Bad timing. Tough luck.

i don't have any great affection for banks. But if you see the mob chasing banks with pitchforks, you know more pointless agencies and dumb regulation is just aound the corner.

Lets try to reduce this to a level anyone can understand , i purchased a bottle of Gin advertised as Gin then found it was water . I went to the shop and asked for my money back they refused . So i then took it to the company that made the Gin and they ignored me . So i then went to government and regulators who eventually did something about if and found the manufacturer guilty of misrepresentation fraud . i suppose having trust in what one thinks are reputable companies is what a thing of the past .

A desperately poor analogy. Gin is gin and has been homogeeous for hundred of years. Bonds are futue cash flows and no-one knows the future. Banks sold these as conservative. Were they being deceptive and reckless. Possibly, but likely not. CDOs were attracting AAA ratings at the time.

To break this down to the simplest level for people slow on the uptake. The future is not known at the present. Investments are a punt on future epectations. If a once in 70 year event occurs then no matter how conservative an investment is there is a high risk of failure.

Trust is one thing, but having a capital guarantee is another, and you don't get that at a 2% over the risk free rate, because even government bonds aren't riskless in a financial meltdown.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.