Deposit insurance is likely to come at a "significant cost" to New Zealand deposit takers, and potentially depositors, especially as the scheme is built up, a government consultation paper suggests.

The latest consultation paper in the Government's ongoing review of the Reserve Bank of New Zealand (RBNZ) Act details the likely costs of establishing a deposit insurance scheme. As reported on Thursday the scheme, introducing deposit insurance of $50,000 per individual per financial institution, is not planned to be fully implemented until 2023. The consultation paper also looks at the likely size of the fund.

The deposit insurer's proposed objective is “to protect depositors, and in doing so, contribute to financial stability.” And its core function will be to "make timely deposit insurance payouts to the insured depositors of a failed depositor taker."

The Government has already decided the deposit insurance scheme will be fully funded by levies on deposit-taking institutions. Additionally the Crown will provide a funding backstop, read government guarantee, to ensure the scheme can meet its obligations to insured depositors.

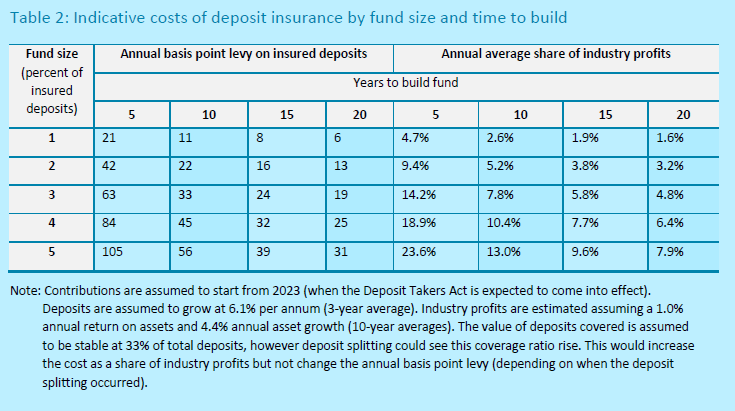

Table 2 below, from the consultation paper, explores the costs of establishing a deposit insurance fund of between 1% and 5% of insured deposits over a period of five to 20 years. According to the paper, a typical approach in other countries has been to build up the fund over five to 10 years.

"For a 2% fund size built up over 10 years, the levy on a $10,000 deposit would be $22 per year during the time the fund is being built up. If this was not passed onto the depositor by the deposit-taker, it would reduce industry profits by around 5% each year in that transition period. It is most likely the levy would partially impact depositors and partly industry," the paper says.

"These estimates show that deposit insurance is likely to come at a significant cost to deposit takers, and potentially depositors, particularly during the build-up stage or if the scheme is drawn on. To an extent, these costs can be managed through allowing longer timeframes to build up the fund, although this would result in a larger contingent liability of the Crown in the interim."

The paper does argue, however, that the implementation of deposit insurance represents a shift from an uncertain implicit guarantee to a managed explicit guarantee.

"An implicit guarantee arises from the revealed preference of governments to not impose losses on creditors, particularly depositors, in a crisis and therefore assist banks during crisis periods. The amount covered by such an implicit guarantee is uncertain, but results in an effective subsidy on bank’s debt funding. The subsidy is ‘paid’ for by taxpayers to the benefit of banks and potentially their customers. The new deposit insurance scheme will manage the government’s liability and ensures that the beneficiaries of the insurance, member institutions and potentially depositors, pay for it," the paper says.

What about the size?

In terms of determining the size of the fund, the paper notes a wide range of fund sizes internationally, ranging from 0.25% to 15% of insured deposits. It says there are two key factors for determining the fund's size.

Firstly, the availability and adequacy of deposit insurance scheme borrowing, and secondly the resolution authority’s preferred resolution method for different deposit takers.

"In a liquidation, the deposit insurance scheme would promptly payout insured deposits. If there are adequate arrangements in place for the Government funding backstop, it may not be necessary to create a target fund that is large enough to cover the entire amount of the deposit insurance payout. Instead, the deposit insurance scheme would borrow from the Crown, with repayment (including interest) made from recoveries on assets from the failed member and, if necessary, from higher-than-normal levies on surviving members," the paper says.

"In the case of a failure of a large deposit taker the deposit insurance scheme would likely protect depositors by supporting another resolution tool, such as the Reserve Bank’s Open Bank Resolution (OBR) tool. Under such a resolution, the deposit insurance scheme may make a contribution towards the cost of resolution and would not be expected to pay out all the insured deposits of the member. The deposit insurance scheme is also likely to have more time to raise any funding for a shortfall when using resolution tools other than liquidation."

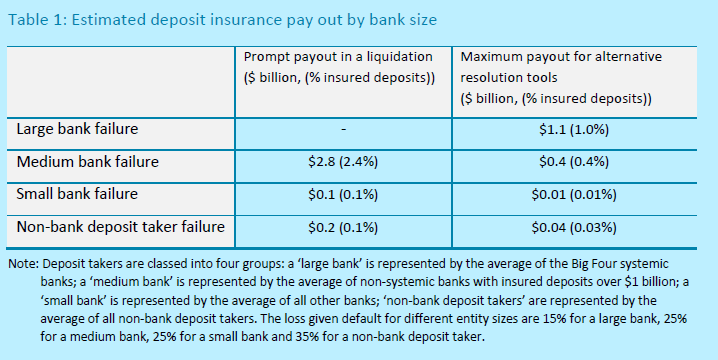

Table 1 below illustrates the obligations that could arise for the deposit insurance scheme under a liquidation and other resolution tools.

"If there was uncertainty around the availability of backstop liquidity and a preference for liquidation as a resolution tool for non-systemic deposit takers, the deposit insurer may want to pre-fund the obligation arising from the liquidation of two medium sized banks, or one medium-sized bank and several small banks or non-bank deposit takers – a fund size of around 5% of insured deposits. Conversely, with adequate liquidity and a preference for other resolution tools over a liquidation for larger banks the deposit insurer may want to prefund the obligation that could arise from the open resolution of one large bank or two medium banks – a fund size of around 1% of insured deposits,"the paper says.

Note the Reserve Bank has designated ANZ New Zealand, ASB, BNZ and Westpac NZ as systemically important banks given their size and dominance of the New Zealand banking sector.

Key design decisions yet to be made

The paper says key design decisions yet to be made include;

1) whether resources that would be used for a deposit insurance payout will be: collected in advance of a deposit taker failure through the establishment of a deposit insurance fund (ex ante funding); obtained after a failure has occurred (ex post funding); or obtained via a combination of both

2) if ex ante funding is desired, whether the scheme’s premium rates will be adjusted according to the risks that members are assessed as posing to the scheme (i.e. a risk-based, or ‘differential’ premium system)

3) on what base (dollar) amount the scheme’s premium rates would be applied (e.g. total insured deposits or total deposits) and how often premiums would be paid (e.g. quarterly, bi-annually or annually)

4) if ex ante funding is desired, the target amount of such funding (i.e., the fund’s target size)

5) the operational approach for the Crown’s funding backstop.

The paper says the proposed approach would see the insurer use a combination of ex ante, forecasts made before the event, and ex post levies determined after the event, from deposit takers to fund the deposit insurance scheme’s obligations.

"It is proposed that the deposit insurance scheme establish a deposit insurance fund in order to help promote depositor confidence in the scheme’s ability to fulfil its payout obligations in the event of a member failure and to reduce the amount of funds the government may need to provide in a failure scenario. In addition, under an ex ante funding model, scheme members that ultimately fail and require deposit insurance payouts would have partially contributed to the cost of these payouts. By contrast, under an entirely ex post funding model, only the surviving deposit takers would incur the payout costs of a failed deposit taker. Finally, there may be practical limitations to how much and how quickly scheme members could pay premiums after a stress event, particularly if they are in poor financial condition themselves."

The paper also proposes a "target size" for the deposit insurance fund, The factors used to determine the target size of the deposit insurance fund include:

1) the ‘severe, but plausible’ failure scenario that the Reserve Bank, as the resolution authority, believes the deposit insurance scheme should be prepared for (recognising that this scenario could involve the concurrent failure of several deposit takers of various sizes, and that the size of the deposit insurer’s obligation for each failed deposit taker would not necessarily depend on the amount of insured deposits of each deposit taker, but also on the resolution tool used to resolve each deposit taker);

2) the ability of the deposit insurer to obtain (borrow) funds, if and when needed (recognising that it may be more challenging for the deposit insurer to borrow large amounts quickly);

3) acknowledgement that funds held in the deposit insurance fund – which would most likely be held in either cash and/or low-yield government bonds – could otherwise be used by deposit takers themselves for more productive purposes, such as lending to the economy.

The paper says the scheme should ultimately, but not immediately, use a risk-based or differential premium system to levy scheme member premiums. It says prefunding would enhance public confidence in the deposit insurance scheme and reduce the need to temporarily access public funds.

"Higher target funding also reduces the potential need for the deposit insurance scheme to impose higher levies on surviving deposit insurance scheme members in the period after a failure event."

The deadline for submissions on the consultation paper, which is being overseen by officials from Treasury and RBNZ, is October 23.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

87 Comments

Surely with ex post funding, that would mean that either the term deposit interest rate would be lower than its competitors or the banks share price would tank? Both of which would reduce the likelihood that that bank would survive long enough to pay a cent.

By contrast, under an entirely ex post funding model, only the surviving deposit takers would incur the payout costs of a failed deposit taker.

If a bank has to call on this, it's already toast.

It might answer this in the above article, but I couldn't pick it up: Where would the funds built up go? Invested in the share market like most things or in more stable things like govt bonds?

Govt bonds stable?? I think there’s going to be a rude awakening on these in the coming years. Anyone who expects govt debt to be repaid is deluded or financially illiterate.

Depends on which govt. I dont see a huge issue in NZ at the moment, we were light on govt debt before this crisis started but clearly we are going to have a lot of issuance in the coming months. But all of that said, we will still be in a decent position, we simply need to broaden the tax base.

Have you looked at our private debt levels?

How do 'we the people' pay back government debt if our private debt is a record levels? Do we pay more taxes and default on our private debt?

I guess it means we take on less private debt in the future, so things like mortgage debts will need to be smaller = house prices fall.

Business growth may struggle as well as we will have higher provisional/terminal taxes for businesses as well as GST. This will result in even less available for staff wages. This will mean individuals will have less take home pay to service private debt = even lower house prices.

Uninterested, I didn't include this in my article but this is what the consultation paper says; "funds held in the deposit insurance fund would most likely be held in either cash and/or low-yield government bonds."

A Treasury official adds;

This is one of the details yet to be determined. Government bonds, as one of your readers has already suggested, is of course an option that would provide a high degree of liquidity if the fund were required at short notice. But decisions on this matter are still some way off.

Meanwhile, the official also added this comment on bail-in;

In response to one of your articles last week, we also noticed one or two of your readers make some comments about the proposed power to bail in unsecured liabilities. Some had taken that to mean both that the Reserve Bank had already been given this power and that ordinary deposits were able to be bailed in with that power. Just to be clear, the bail-in power does not yet exist and won’t exist until legislation is passed giving the Reserve Bank that power. Nor has a decision been made on what liabilities would be eligible for bail-in. This is one of the questions that we are currently consulting on.

So not a guarantee, rather a new fee that banks can charge.

That's how it works overseas, term deposits are even safer due to this guarantee, but they pay less.

There ain't no such thing as a free lunch.

but can they go negative in a deflationary environment? because that's what's happening today. Why spend when your money is worth more next week/month/year. It's the nightmare scenario for the economy, I thinks its unavoidable after a period of excess.

I definitely see deflation ahead. Most firms are going to have to cut their fees and prices on goods and services.

Fuel prices will be subdued. Rents subdued and down a bit.

Although groceries may not move down, in fact may go up a bit.

So perhaps only slight deflation overall.

Deflation for discretionary spending, inflation for essential spending. In other words, a continuation of the past few years, except the gap between the two widening.

Agree to some extent, but housing costs? Deflation on that

lets see how oil prices flow into the economy and perhaps a falling chinese currency, both highly deflationary.

In 1973 OPEC started to restrict oil supplies and the world went into recession and self sustaining inflationary crisis. I have read and starting to come around to the view that the action by the FED and Central Banks was wrong, it's was a one off cost increase that was turned into a needless nightmare for many by actions of Central Banks. I started in business with %18.5 on my O/D and if I nudged my limit %24. Yet I had the resources to pay the bill ,even if it was my biggest cost, imagine if those interest rates came back? economies would fail, we don't have the incomes, costs are too high etc. That money has been siphoned off into bank profits and proliferate Gov't spending and the speculative economy.

I now suspect a more deflationary outlook will become the norm, as AI and the information age repress costs especially in energy.

Prices already soaring at New World in my area. 50% to 100% on some items, especially fresh produce. Shouldn't be a problem though. Due to the fact that the govt. puts GST on fresh fruits and vege, the obese NZers can just buy some mac and cheese and a coke instead, maybe they haven't jacked up those prices yet....

Where will the funds come from? Us!

“The shock of the recession and destruction of wealth will leave a legacy of increased financial caution with households wanting to build precautionary savings and companies striving to repair damaged balance sheets...a sustained upturn in inflation would be preceded by a final bout of deflation.

And that comment re when Inflation is going to arrive? Spot on!

https://www.marketwatch.com/story/this-recession-will-finally-end-the-p…

Thus, in the depths of a deflationary crisis it won’t matter if the central bank goes a little crazy. In fact, from the policy perspective, the crazier it seems the better off we all are.

And we can all probably agree that $900 billion in five weeks is at least theoretically in that realm.

But here’s the thing: if this is massive-scale money printing, where’s the inflation?

I don’t mean right now; it would take a little bit of time for that to show up in the CPI or PCE Deflator. Rather, there are very deep, sophisticated markets where all they think about is future inflation. Any chance the Federal Reserve’s overheating printing press creates that spark of price acceleration is going to show up right here right now.

Therefore, if the Fed just “printed” an absolute flood of new “money”, TIPS markets (and curves) would be all over it. But they aren’t. Inflation expectations are actually going the other way. Link

Perhaps the $907 billion wasn’t money printing?

It’s a reality that has dawned on the bond market especially 2014 and after. It hasn’t hit the mainstream yet because Jay Powell is given the benefit of the doubt for no more reasons than his job title. Performance doesn’t matter, the whole financial press caught up on the logical fallacy of appeal to authority.

The guy may run the Federal Reserve, but it’s not like the Fed is a central bank.

Again, don’t take my word for it. That’s what these markets are all telling you. As the dollar continues to rise, propelled by a global monetary shortage that continues if pulled back once more into the shadows, no one is expecting much of the FOMC. Read more

The RB has one job, keeping the banking industry secure, what a major fail.

Low interest rates have encouraged risk, now we are being told, 'if borrowers who took risk go broke, the fault is on the depositors', your deposits are a promise to pay by the mortgage holder, only as good as his/her promise to pay.

The 5 billion a year siphoned out of the economy by the banks over the last decade is just a minor aberration in the great scheme of things.

Most deposits are relatively small, held often by pensioners who have saved over their lives to have a secure retirement. The reality is that a small percentage have large deposits that represent a disproportionate percentage of bank deposits.

My business is farming, over the last decade more and more land has been owned by less and less people or often corporates. The elites have made a killing, able to access funds easier than traditional farming families, four bigger family farms around here were sold before christmas, all to corporate interests. Regional councils treat corporates differently, just chucking that out there.

This is not the direction of the country most of us would choose, we were a nation of middle class landowners/homeowners, these indebted speculators are where the devil is hiding.

Low interest rates have encouraged risk, and endangered the very core of both our economy and our society.

I have no doubt we will slip into deflation, I think it's inescapable.

When someone takes their money out of the bank, lets face it there are a lot more buying opportunities today than there were last year. Perhaps they buy a farm, the seller has debt, they buy a farm with cash, farmer pays off his debt and that debt is cancelled out, so is the deposit.

That's the risk, deposits get spent cancelling out others debt and money starts to disappear, ( Deflationary). One thing I know about my industry is there is a lots of debt, Banks move to 20 year mortgages over the last two years has totally changed the game, it's sucked money out of rural economies.

This is going to be incredibly hard and complex to fix, but lay the blame where it belongs, failure of the Reserve Bank to regulate and not allow a friggin casino economy to develop.

More than likely, insolvent banks in NZ will be bought out by large Chinese banks

Great post Andrew - agree.

The question comes back to why we have agreed to 2% inflation targeting? In the end, isn't that why we have interest rates near zero? (because everyone is trying to continuously achieve 2% inflation)? Or have I missed something?

The story appears to be that 'we' have to hit a target, regardless of productivity, and actual health of the economy. And to achieve that inflation target, we will drive rates down because we're not seeing the growth we expected, creating debt and asset bubbles, which introduces greater risk to the system, but we can't reward conservative investors with an appropriate reward for their risk because the OCR is near zero! If anything, returns on deposits should have been rising the last 10 years as our banks exposure to the NZ property market grew. But if the risk free rate determine by government bills is near zero, how would a bank justify a much higher rate? The margins are so low...

The world has gone mad and the longer we fail to address the underlying problem, the worse its going to get. In part, its why I think we actually need to have a massive recession/depression to reset everything and start with a clear sheet. It will probably be beneficial with a longer term/utilitarian perspective. Rewarding non-performing risk is distorting markets and behaviors - warping the quality of our society.

For me, this raises many questions like do we actual record inflation well with the basket we have? (should other assets like property and share capital values be included in the inflation measure as there appears to be a relationship?) Why 2% and why not 4% inflation? Why avoid recessions? (they appear to be regenerative).

Agreed - inflation targeting hasn't worked (particularly when the measure of inflation is constantly fiddled with!). I'm no expert, but maybe something like trying to match credit growth with GDP growth could work?

I think in theory that is how it is supposed to work - money supply = inflation.

https://tradingeconomics.com/new-zealand/money-supply-m3

So if you look at M3 - you'll see the chart has almost perfect correlation with housing market inflation. So our money supply has just gone into houses - so yes we do have inflation at the same rate as money supply, but its just not measured. So instead Reserve Banks are saying 'where is the inflation?' - well its in our house prices not in the productive economy. If we measured it against houses and had the 2% inflation target, we would have been putting rates up to prevent the credit bubble from growing so big and slow the rate of inflation. Hence we may find ourselves up shit creek without a paddle in the coming decade/s.

The odd thing about this with further thought is that we've had high inflation but we've tricked ourselves into thinking we haven't by reducing rates so low to cover the debt costs so it appears that there wasn't any inflation in the CPI basket. Completely bizarre (house prices, the debt associated to those prices and the inflation targeting have/had become a self licking ice cream cone). The future will have to pay the cost of that unmeasured inflation - unless of course the system resets itself via a significant fall in house prices and associated debt to new lending.

Policy/incentives all wrong but at least it made part/s of our society feel wealthy on paper.

Interesting chart. I was referring to GDP rather than inflation - if credit growth matched GDP growth, then at least new credit would be matched by equivalent income (and hence reduce the chance of credit bubbles such as the one we have had forming).

Brilliant post!

I think most savers wold be happy with some type of insurance/guarantee to protect their life savings. Banks could even provide an 'opt out' option if some savers are willing to take the risk. Even when banks like Northern Rock collapsed in the UK back in 2007 during the GFC, there was a run on that British bank which made the banking community nervous where the British Government had to force Saver Deposit Guarantee of up to £85,000 per person.

BBC article: Northern Rock: How the crisis improved savers' protection. https://www.bbc.com/news/business-41226937

if depositors are taking more risk they should be rewarded for it. We live with an artificially created interest rate, nothing to do with market fundamentals. i would argue that this has led to distortions in the economy that are going to be very hard to fix without a lot of pain.

Yes agreed "depositors are taking more risk they should be rewarded for it". And so much for NZs Rock Star economy, most of that artificially created interest rate was developed by John Key by allowing lots and lots of so called foreign investment, which then just turned out to be money laundering from Asia which was completely unsustainable.

I think all the locals around here are well aware that the bigger indebted farmers are mostly only paying interest, and at a lower rate than the rest of us. It's a distorted market that benefits the risk takers who have the RB covering their backs.

Eventually the party will stop Andrew an those doing the hard yards (in an honest fashion) will be rewarded - principles dictate so. Even though it seems unfair at present.

What should happen is someone sets up an easy means for small depositors to invest in gold at the Perth mint. If you are not making money or negative on your deposit at least have it in something real. That would get interesting.

Depends if economies completely go down the plug hole over this virus especially those that have largely invested in dodgy deals, which we know Australia very much has. You only need to take a look at Iceland for an example of what can happen. During the GFC Iceland turned out to be one of those countries who had been playing the global market by attracting lots of foreign investment, and which led to their economic collapse.

Here's how Iceland's banks created the crisis. First, they lured deposits from the Netherlands and the United Kingdom by offering 15 percent interest rates. They could offer these rates because the value of Iceland's currency, the krona, was high. It had become a major trading currency. That drove its value up 900 percent between 1994 and 2008.

That also created inflation. Housing prices rose. Between 2003 and 2004, the Iceland stock market skyrocketed 900 percent. By 2006, the average Icelander was 300 percent wealthier than in 2003. Many Icelanders added second mortgages using cheap foreign currencies.

The banks used $100 billion in deposits to invest in foreign companies, real estate, and even soccer teams. That amount dwarfed Iceland's 2008 GDP of $14 billion.

Then the 2008 global financial crisis shut down bank lending. Like U.S. banks Bear Stearns and Washington Mutual, Iceland's banks went bankrupt. The government couldn't bail them out because it didn't have the money. Instead of being too big to fail, they were too big to save. As a result, these banks' financial collapse brought down the country's economy. Iceland asked its neighbors Luxembourg, Belgium, and the United Kingdom to insure bank deposits of its branches in their countries.

Iceland's Government Collapsed and they even had to bar capital from leaving the country.

For more info read The Balance: Iceland's Economy, Its Bankruptcy, and the Financial Crisis. https://www.thebalance.com/iceland-financial-crisis-bankruptcy-and-econ…

There's already an easy means for that. Open a Hatch account, transfer money, buy their gold backed ETF.

can you expand on this a bit?

Think referring to PMGOLD:

Not sure how much more I can explain it:

https://www.hatchinvest.nz/ - sign up

Transfer money (goes into US denominated bank account, safe from the OBR).

Buy perth mint ETF: https://www.aaauetf.com/

There's already an easy means for that. Open a Hatch account, transfer money, buy their gold backed ETF.

The cheapest and easiest option is the Perth Mint digital tokens on a blockchain. Only available to U.S. and Aussie citizens right now. If it were available to NZers and had NZD exchangeability, it would be a good solution.

The madness entered into by central banks is simply supported by trust in the money that they print. The more deflationary it gets, the more money they will print. Having had some years to look at all this, I sold my house, closed my business, and took everything I could feasibly take "off grid". If you invest in gold, be it actual, or digital, or especially etf, you must ensure that the gold is allocated. This is the most important point about gold, as unallocated gold is not actually owned by the investor. Settlement will more than likely only be paid in cash. Perth Mint investments are unallocated, yet the funds are guaranteed by the federal bank. A company like bullion star, or silver bullion, based in Singapore, give you legal title of your gold, and store in a non bank vault. It is also fully insured. Storage in non bank facilities is also very important. With bullion star, you can also store in nz, but the fees are a little higher. You transfer your storage at any time, so that may be useful. There is a lot of information to understand about gold, not something I recommend anyone simply jump into. There are two centres which specialise in the manipulation of the gold market, since Nixon took the usd off the gold standard, and the need to keep the price suppressed, though not that successfully, means an understanding of the lmba, in London, and the Comex, in New York, along with the wgc, the world gold council, will help give you a better idea of the entire gold market. There is paper gold, and there is physical gold. Paper gold would have us believe that there is many times more gold than there has ever been mined, that's why they have trouble settling accounts with actual gold. This is a long story, so I wont bore you more. Needless to say, there is big disconnect at present. Should you find actual gold, that you can buy at the spot price, you'll be doing very well. Demand for physical gold is at an all time high. Bullion star has a good website, with interesting articles, I recommend a visit.

Do your research, just remember, allocated, and non bank storage.

The other obvious way, is digital assets, which include digital gold. This is equally, a large field, and something that shouldn't be rushed into. All digital assets are based on blockchain, which simply translates as a ledger. The aspect of digital assets, including digital currencies, is that they are decentralised. People that are disillusioned with central bankers, love this aspect, it's the key reason bitcoin was developed. There are a limited number of bitcoin that can ever exist, so no endless creating more of them. There are over 4000 digital assets and currencies out there, so you need to take your time studying. I approached both with a try and see/learn approach.

That is, if you have say $10,000 sitting around, why not put $1000 into a digital currency that you have checked out? Then you can carry on studying, and if say something like the financial system froze, at least you'd have something else to pay with, which is not part of the system.

Probably way too much info, yet as you asked, thought I'd try throw some light on the topic.

It's pretty clear, the rbnz rush to protect peoples debt, yet can't get there a into g until 2023 to do something for depositors, how do they get away with that stuff? Because they know most kiwis have debt, not deposits. Encouraging people to invest in stocks and property, yet again. I reckon getting off grid is the only way. Keep what you need in the system for cashflow, plus a bit more, and take the rest away from irresponsible financiers.

But the mass of household debt in NZ, as I understood it, was held by a minority of the population...?

Is interest.co.nz ever going to present any comment or article on economic modelling presented on the different strategies to the pandemic on the NZ economy?

Here is Dr Kirdan Lees, University of Canterbury for example;

https://www.newsroom.co.nz/2020/04/03/1114247/a-sudden-stop-covid-19-co…

Well that seemed to answer a few questions I had.

Mostly I now understand that the government is still going to be ultimately responsible in a large failure.

Depositers will be screwed either before or after a failure.

Saving is still for suckers, debt is good.

Looking at what Andrew wrote I can't help but agree, so perhaps the real risk in failure sits with the mortgagee so why not make them pay for the fund.

Probably because property has been the sacred cow in NZ and everything has been done to nurture and protect it, including eroding the value of folks' savings over the last decade. Heck, it got to the point the RBNZ asked for a DTI measure to try to slow down all the money rushing into the asset price bubble, yet Bill English refused to give it to them, because hey, rock star!

Which bank is actually in the best position (i.e. free cashflow and/or reserves) to survive?

without the market setting interest rates it's hard to know. In a free market rik would be reflected in interest paid to depositors. SCF was a good example, they were paying depositors way above the competitors, yet RB totally missed the ponzi scheme at the front door. One of the biggest disasters in NZ financial history.

I would suggest that if one of them topples, they would all go, in NZ. Kiwibank might not though as it's ultimate owners are the government and the way I see it, if one bank fell over the government would see it as an oppourtunity for Kiwibank to grab all it's lending. Then they could keep it on govt life support until things turned around.

If they topple the gov't steps in under obr and restructures the bank then the the bank is basically nationalised and all deposits are guaranteed, the thing to do would be to move deposits to that bank with a gov't guarantee, i mean all depositors should do this.

??? Have you read the OBR? If a bank is in distress in NZ, all depositors funds are frozen. When a bank re-opens, the non-frozen portion is government guaranteed. You are treated as a creditor and "a portion" of your money is returned. In the quaint examples they gave when they put this policy out, you get 20% of your money back, which would be a likely scenario.

However in my example above, I suggest Kiwibank is a bit safer than others, because it's essentially already government backed.

i read it a long time ago. I'm not as confident in Kiwibank as you are.

Any Depositor Guarantee, whatever the size, is in effect the sovereign ( Government) taking responsibility for the 'safety' of creditors (savers).

The easiest answer, at the risk of flogging the dead horse, is for ALL and ANY New Zealand citizen that wishes, to open a Savings Account with the RBNZ , with interest rates set at the OCR minus a margin to cover the transactional costs. All other transactions (mortgages, term deposits etc) would be the exclusive domain of the commercial banks.

It's in effect what they are doing anyway, by Guaranteeing Deposits.

Any savings headed to the RBNZ accounts would be lent out by them the the commercial banks at whatever rate the RBNZ thought appropriate to the circumstances. It keeps any nervous savers funds at arm's length to the commercial banks.Easy!

(NB: Suggestion for anyone who is super-nervous about The System here and wants to quarantine their savings - If you are a taxpayer, prepay your taxes. Deposit $X with the IRD and use it against future tax liabilities. It's what a currency is anyway, a right to taxation. And when it all blows over, ask for a refund at the next assessment time)

Is it even possible for private citizens to have a savings account with the RBNZ?

No. its not a retail bank. And has no purpose being one.

What is the difference between doing that, and buying Kiwibonds?

The difference is that the money you put into Kiwibonds has to be paid from a retail bank account and redeemed via a retail bank. So you can't avoid having to use a retail bank account if you want to access your money or shift it around.

The RBNZ.collects stats on profitability, liquidity and capital and ratios from deposit takers on a monthly basis. Why does it not publish these? They are due 20 working days after the end of each month. It wouldn't be a big table.

What’s the point of deposit insurance anyway? It’s just unnecessary overhead. If a bank finds itself in negative equity then the government could just step up and immediately take ownership of all bank deposits and use all government resources to freeze bank assets and recoup losses.

I guess without some form of guarantee many people may become risk averse to deposits with banks. And if the above is true, then why do we bother having banks as private entities? No point paying the executive of banks millions a year in wages if they have no responsibility? Just make them a function of the reserve bank.

given what they are paying on deposits at the moment, and after tax on any interest earned, is it worth the risk? Kiwibonds seem a much better risk to return ratio (Basically zero of either). Certainly considering putting our spare money there once we've paid for certain things post lockdown.

why do we bother having banks as private entities

Who has the right to create money in the economy? at the moment governments and commercial banks. What are the consequences? In NZ we have a boated financial sector and asset bubbles. While government debt is only ~20% of GDP, private debt is a whopping ~90% of GDP. It's pretty clear to me who the irresponsible party has been. Perhaps we need a government owned national investment bank do direct credit to the right places, SMEs and infrastructure projects rather than real estate speculation. If we want to keep banking private then perhaps we need de-aggregation to smaller banks as the economist Richard Werner advocates. Regarding confidence; Both OBR and deposit insurance definitely erodes my confidence in the banking system. The only thing that would give me confidence is an unconditional government guarantee. I think a 50K limit is a good idea.

What's the difference between employment insurance and deposit insurance?

Would appear our government is happy to play the role of employment insurance but not savings?

And isn't saving critical in terms of future investment - i.e. growth? So by destroying savings, you're destroying the future and ability to achieve the thing government appears to want the most?

I would also think it's time to have a discussion about how business can deduct interest costs. In a productive economy I have no problem with it but when your economy is based around speculation on assets then I find it egregious.

Many of my friends have interest costs high enough to ensure they never pay tax after depreciation, I now have come around to thinking an asset tax that was tax neutral, built to capture the freeloaders in our economy is a good idea.

Just on this topic and our landlord friends can probably answer this. Do property investors pay residential rates of lending or business rates? And if they have the benefits of being a business, including deductions etc, shouldn't they be paying the same rates as other forms of business?

Yes and GST.

New Zealand's mortgage debt to GDP will breach 100 percent for the first time this year. By 2021 mortgage debt to GDP will in percentage terms continue to increase and be twice that of twenty years ago . At the same time the value of housing will begin to fall. As the main drivers of New Zealand GDP growth are emasculated, it is not surprising that there is no urgency to protect bank deposits, given New Zealand has rapidly joined the QE club

Haha and what happens if our GDP has contracted significantly already?

Wait for the potential household debt deleveraging via property sales (both voluntary and forced via mortgagee sales) due to rising unemployment, and drop in tourism (fewer Airbnb rentals).

Take a look at the situation here:

1) https://tradingeconomics.com/ireland/households-debt-to-gdp

2) https://tradingeconomics.com/united-states/households-debt-to-gdp

The combination of high household debt, high house valuations, large numbers of negatively geared property investors led to financial vulnerabilities that many in NZ overlooked. If people knew where to look and what to look for, it was clear that risks were elevated.

Meanwhile property promoters are still talking about the underlying housing shortage, inward immigration, 10 year property price cycles where property prices double, low interest rates boosting demand. Now property mentors are claiming returning expat Kiwis will boost demand and this will result in rising property prices.

Who lists their property for sale during a lockdown? Perhaps the impatient, the fearful? Lockdown date 26 March, property listed for sale date 2 April 2020.

Property in Auckland just listed for sale by a property trader. Bought on 30 Jan 2020 for $430,000 (massive 38% discount to RV of $630,000). Now listed for sale after 2 months of ownership.

Some observations: external wooden stairs not painted, decking not painted, fence not painted, unable or unwilling to get home staging in. Perhaps urgent to get to a basic sellable condition?

https://www.trademe.co.nz/a.aspx?id=2594393889

https://www.qv.co.nz/property/12-broadfield-street-massey-auckland-0614…

More property traders likely looking to get out, as their expected sales price may now be lower (under current conditions) than their cost of purchase plus cost of renovations and financing costs for the period.

If 90% of individuals have $50k or less (a previous article in interest) and get their deposits paid back, what happens to institutions eg Kiwisaver, investment funds who have millions in cash or cash equivalents in banks.? Loose all their deposits? Get to keep their all of their deposits? Subject to OBR? The media including interest have geared their articles to individual deposit holders. I might have missed something here on institutional deposits. I'm fairly certain that a fund I'm aware of does not split their cash or cash equivalent deposits between a number of banks.

What about foreign currency deposits held via a local bank? Would these fall under deposits and be subject to what?

So, after years of having my deposit rates sacrificed to the speculators, best I can now hope for is what? Negative term deposit rates ... or may as well be.

For the next decade here's my prediction for all asset classes: nil returns. Nada. Nothing. Central bank stimulunacy has broken the investment world (not the pandemic, although that is the perfect storm trigger).

Quite right, with one thought:

That cash you have in liquid deposits of all sorts? It doesn't matter if it 'earns' minus 5%. It only matters "what it can buy", and if that is 10% lower in price than today's same-for-same asset, then you'll be a winner!

But as for those other non-liquid asset? "What to do with them" is the question on every fund managers lips "Convert them to cash, now? Or hold them and benefit from the Upturn?". You don't appears to see one - neither do I.

I've been a perma-bear for last three years, so was all cash and treasuries/bonds outside my house. But even I weakened six months ago and put more than I wish I had (now) into a commercial property fund because I was so desperate to get a yield which after tax bet inflation. It's only a portion of savings, not fatal, but it irks ... I'll keep that for long term now (and at least an unlisted fund so didn't suffer the 35% average drop the NZX REIT's suffered, because they were trading on that as a premium simply via the way stimulunacy turned all share valuations lunatic).

For now just sitting waiting. I had said when S&P in US went below 1900 I'd put money in shares, but I'm thinking when it gets to about 1000 now ( which is coming, I think, albeit there'll be a few idiot rallies in between as Fed positions itself to buy the entire means of production in US through their sharemarkets.

"put more than I wish I had (now) into a commercial property fund because I was so desperate to get a yield which after tax bet inflation."

1) what do you think will happen to commercial property prices? Do you expect them to rise or fall? By how much?

2) what are the current rental yields on the commercial property portfolio?

3) what is the LVR of the commercial property fund? The higher the LVR, then it will magnify the unit price (both on the up and on the down)

That cash you have in liquid deposits of all sorts? It doesn't matter if it 'earns' minus 5%. It only matters "what it can buy", and if that is 10% lower in price than today's same-for-same asset, then you'll be a winner!

But as for those other non-liquid asset? "What to do with them" is the question on every fund managers lips "Convert them to cash, now? Or hold them and benefit from the Upturn?". You don't appears to see one - neither do I.

Yes, well said. Actually, Japanese households have been strong savers in cash, and despite the negative effects of a dire deflationary environment (lower incomes predominantly), this has worked in their favor as consumer prices have fallen (as well as house prices and rents). Now there are some fundamental differences between NZ and Japan:

-- NZ doesn't have a savings culture. It's paycheck to paycheck on the whole.

-- NZ doesn't have the consumption volume for businesses to thrive. For ex, NZ businesses could not thrive on the margins that Japanese businesses survive on.

-- NZ doesn't have the scale of capital investment, production resources, and supply chains to develop businesses such as Daiso.

Supposedly Japan has negative interest rates. But I was looking at their rates and they are above 0. Not much above 0, but they are not negative. Not unless I am missing something

Nominal retail rates from banks to customers are still positive ...albeit negative real rates after tax and inflation. The negative rates are from the BOJ to the retail banks to ensure the funds/debt created by BOJ are put to work in real economy and not parked with them. Same as in EU, although I know at least German savers with more than 200,000 Euro have to pay the retail banks to hold it.

First expert 2020 forecast /comment 31st Dec 19, 11:13am

" Looking back at last year’s predictions it appears that this site’s comments section has become overrun with pessimists of low acumen and high confidence. Pity you can’t buy an investment property with upvotes fellas. As far as upvotes go, the dumbest amongst you sure did get the most of those in 2019. "

Its only April ,many of the 2020 forecasts provide an insight as to how Kiwis can apparently purchase very expensive real estate, acquire a mega mortgage , yet have almost no or limited savings to offset a change in circumstance,. Pessimists of low acumen indeed

The odd thing is that the worse the news gets, the stronger the denial appears to become.

I know..... let's all take our deposits out of the bank and see how quickly they come up with a guarantee. Remember, they need us more than we need them!

This should've been put in place post gfc for this very event. Massive fail by the RB. The Aussie banks are exposed, caught with their pants down as the enquiry found. RBs push for increased capital ratios another very telling sign they were worried about banks exposure before the black swan landed. I think the govt will put a guarantee in place within months, they must before default rates potentially skyrocket once mortage holidays expire & the goodwill currently being extended by the govt towards banks dries up. Banking may need to become SOE again & regulated by very conservative policy towards residential lending, consumer finance and more progressive lending for business that is not secured by residential property/land but against the viability of that productive enterprise.

IMO it is going to have to be similar to what they put in place when the GFC occurred, without any top cap. Minus guaranteeing finance companies. So they need to make it only apply to banks.If all goes well, then no banks should fail, but it at least provides certainty. A big reason sharemarkets crash is uncertainty and panic, so we don't want this to occur with banks.

As an expat who lives and/or works in the US, Canada and Japan, I'm still waiting for a Kiwi -- any Kiwi -- to give me even a single good reason why NZ houses are priced so high.

No, "because we excitedly reassure each other that's what they're worth!" is not a good reason.

Because that is what people are willing to pay. It is largely about what people can afford to service and been conditioned to pay. But if one person loses their job, and immigration and demand falls, and there is a lot of uncertainty, things potentially can change.

Because every Saturday morning there is a huge pullout in the NZ Herald (sponsored of course by the real estate industry), that is bigger than the news section, that has been fueling real estate by telling Kiwis they are missing out by not being in real estate and expounding how much of a bargain such and such property is, even though it is a hundred year old home in Mangere ( or wherever) with no insulation and rats for tenants selling for $1.2million, when in fact should be bulldozed.

Who needs Coronation Street....I've watched with fascination and will continue to do so.....stay tuned for the next exciting episode coming soon to a venue near you.....

"give me even a single good reason why NZ houses are priced so high."

Lessons from the US GFC 2008 / 2009

Cause of the housing and credit bubble in US

From the May 2010 FCIC interview with Warren Buffett, a reknowned investor and Chairman and CEO of Berkshire Hathaway

MR. BONDI: As I mentioned at the outset, we’re investigating the causes of the financial crisis. And I would like to get your opinion as to whether credit ratings and their apparent failure to predict accurately credit quality of structured finance products, like residential mortgage-backed securities and collateralized debt obligations, did that failure, or apparent failure, cause or contribute to the financial crisis?

MR. BUFFETT: It didn’t cause it, but there were a vast number of things that contributed to it. The basic cause, you know, embedded in psychology –- partly in psychology and partly in reality in a growing and finally pervasive belief that house prices couldn’t go down and everyone succumbed –- virtually everybody succumbed to that. But that’s –- the only way you get a bubble is when basically a very high percentage of the population buys into some originally sound premise and –- it’s quite interesting how that develops –- originally sound premise that becomes distorted as time passes and people forget the original sound premise and start focusing solely on the price action.

So every -– the media, investors, the mortgage bankers, the American public, me, my neighbor, rating agencies, Congress –- you name it -– people overwhelmingly came to believe that house prices could not fall significantly. And since it was biggest asset class in the country and it was the easiest class to borrow against, it created probably the biggest bubble in our history.

"Asset appreciation, draws in people that really don't know anything about the asset. They start being interested in something, because it is going up, not because they understand it or anything else. The guy next door, who they know is dumber than they are, is getting rich, and they aren't. And their spouse is saying "can't you figure it out too?" It is so contagious. That's a permanent part of the system."

I think a lot of people are nervous about their savings in the bank about what is going to happen, and no matter what they say, I don't think this is gong to change. Espcailly based on all the questions people are asking financial experts in the media about this very point. Infact, just look at the panic buying a the super markets, where people bulk purchased early to avoid having to shop when people will be sick. Nothing the government or stores said prevented this occurring.

Unlike most countries, we have no deposit guarantee scheme.The OBR system is a risk to savers. The $50k planned DPG is poor compared to the rest of the world, and if people have a a reasopnable amount of money save for their retirement in the bank, we don't have enough banks to share money between banks to carry that risk by sharing the money between banks. We provide insurance for our homes, but not for savings in the bank. If they are going to charge per 10k deposits, then this shouldn't have any limit.

I think they are going to have to come out with something soon to provide certainty through this

196 countries in the world. 148 of them have deposit insurance. The other ones are probably countries you cant spell or have never heard of. NZ is way smarter than all the other 'developed nations'.

Besides, it'll give the govt something else to put GST on.

Deflation is going to be unstoppable. No zero interest policy nor any QE can stop it. Massive QE through a period of several years, and negative interest rates have created not a iota of inflation in Europe, for example, nor in Japan Particularly in the housing market, deflation is going to be a sustained and prolonged phenomenon. Only exceptions: medical costs, council rates and some basic food prices. Not a bad time to be a farmer or a doctor.

“The deadline for submissions on the consultation paper” is October.

This all should’ve been done 5 years ago. Now we’re heading into a deep global recession, and very uncertain economic times. But no, don’t hurry or anything...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.