Full implementation of a deposit insurance scheme is not scheduled until 2023, with the Government seeking feedback on key aspects of the scheme by October 23 this year.

Last December Finance Minister Grant Robertson confirmed the Government would introduce deposit insurance of $50,000 per individual per financial institution. An insurance limit of $50,000 would fully protect about 90% of individual deposit accounts in New Zealand, while leaving 60% of deposit funds exposed to potential loss. This is according to Treasury and Reserve Bank officials overseeing the ongoing review of the Reserve Bank of New Zealand (RBNZ) Act through which the deposit insurance scheme is being developed.

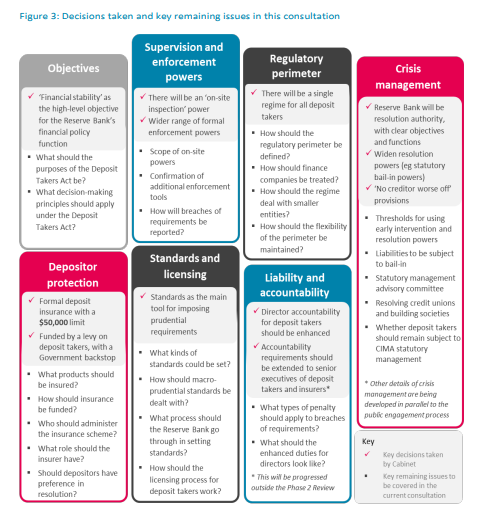

A public consultation document in the ongoing RBNZ Act review was released on March 13. Due to the all encompassing impact of COVID-19, the deadline for submissions has since been extended by six months from the original deadline to October 23. Both Robertson and the RBNZ have recently told interest.co.nz that they're sticking to the plan to implement deposit insurance as a part of the RBNZ Act review, not indicating any plans to fast-track the process.

The consultation paper looks at the prudential framework for deposit takers and depositor protection.

"Deposit insurance will be developed and introduced alongside the other elements of the prudential framework discussed in this document, with full implementation currently planned for 2023. Many of the operational elements of the scheme will not be decided for some time, and will involve further public consultation. These elements include, for example, regulations that require each deposit-taking institution to be able to identify all the deposit accounts owned by a single customer at their institution (a ‘single customer view’) and the size of any deposit taker levies," the consultation paper says.

Products deemed to be of lower risk and lower complexity proposed for inclusion

The paper proposes that the deposit insurance regime should cover prescribed types of basic deposit products, such as transactional accounts, on-call savings accounts, term deposits and redeemable shares offered by financial cooperatives.

"There is a strong case that transaction and on-call savings accounts, redeemable shares offered by financial cooperatives and term deposits meet the criteria for inclusion in the deposit insurance scheme. These products can be easily opened by retail customers; are widely held by New Zealanders; can be readily identified and measured by deposit takers; and, with the exception of term deposits, are primarily used for everyday spending. PIE deposits would be eligible for coverage on the basis that they are ultimately investments in the eligible products. Making these products eligible for deposit insurance is consistent with the Financial Markets Conduct Act, where these products are exempt from product disclosure requirements due to their lower risk and complexity," the paper says.

Additionally the paper says the Government proposes to include wholesale depositors, i.e. large/institutional depositors, within the insurance scheme, but exclude foreign currency deposits, deposits held by related parties, and interbank deposits.

Investments in other types of retail debt securities, such as bonds, debentures and capital notes, are not proposed to be eligible for deposit insurance coverage.

"These debt securities are typically offered as higher-risk (and higher-return) products; excluding them from the insurance regime would allow them to continue to fulfil this role in the market. They also do not provide transactional services, are not widely held by the general public and can have complex features such as differing levels of security and subordination. It is also uncommon for these sorts of debt securities to be included in overseas insurance schemes. Regardless of the specific boundary for insured products, public awareness of which products are and are not insured will be a critical determinant of the effectiveness of the scheme," the paper says.

Meanwhile, it's proposed that insured products be set out in regulation, with the list of eligible products able to be updated and adjusted to reflect changes in product offerings.

"Future consultation will also look at the treatment of joint accounts, complex deposit types (such as accounts held by trusts), and customers who have temporarily high balances at the time of failure due to certain life events."

Key government decisions

The Government's previously announced in-principle decisions include the establishment of a deposit insurance scheme, funded by levies on deposit takers, with a maximum coverage of $50,000 per-depositor, per-institution, the designation of the Reserve Bank as the resolution authority for deposit takers, with clear statutory functions and objectives and the ability to restore to solvency or to recapitalise a failed deposit taker using statutory bail-in. That means providing the Reserve Bank with the ability to ‘bail-in’, that is, write-down or convert to equity, certain unsecured bank liabilities, as a new mechanism to recapitalise a failing bank.

The Crown will provide the deposit insurance scheme with a funding backstop, or Government guarantee, to ensure that the scheme can meet its obligations to insured depositors. Additionally NZ's two separate regulatory regimes for banks and non-bank deposit takers are to be united into a single ‘licensed deposit taker’ framework.

"New Zealand does not currently have a deposit insurance scheme. This means that, in the event that a deposit taking institution failed, depositors would be dependent upon a liquidation or receivership process to try to recover their money, which could take years. An explicit deposit insurance scheme means that depositors will be able to have prompt and certain access to some of their money," the Government says.

"The coverage limit will be reviewed once the scheme is bedded in and better data are available. The number of depositors that are fully covered once the scheme is in place will depend on how many have multiple accounts at their institution (the Review does not currently have complete data on this). It will also depend on how responsive depositors are in splitting their accounts across banks and other deposit takers in order to maximise their coverage."

"The introduction of the deposit insurance scheme reflects a desire from the Government to protect vulnerable depositors. The failure of a deposit taker could create significant hardship for depositors that rely on deposits to fund day-to-day transactions. Deposit insurance means that protected depositors do not need to invest time to monitor the riskiness of their deposit taking institution, which is a difficult task, even for sophisticated creditors that have large amounts of money at stake," the Government says.

"The protection provided to depositors will also contribute to financial stability. The deposit insurance scheme is expected to enhance public confidence in the financial system, lowering the likelihood that financial stress is magnified by depositors withdrawing their money at the first sign of trouble."

NZ is currently an outlier among OECD countries in not having deposit insurance, and the $50,000 limit is low compared with most other countries. You can see all our previous deposit insurance stories here, and all our RBNZ Act review stories here.

Depositor preference up for debate

The paper also looks at the possibility of whether to introduce a preference for insured depositors as part of the deposit insurance scheme, or retaining the status quo which is depositors continuing to rank equally with other unsecured creditors in the event of the liquidation of a deposit taker.

"Depositor preference is achieved by altering the legal hierarchy of claims in a liquidation to rank depositors above other general unsecured creditors (depositors currently rank equally with these other general unsecured creditors). Under a depositor preference regime, depositors, or the deposit insurance scheme representing them, would receive the proceeds of liquidation before other general unsecured creditors and shareholders, who would rank below them in the creditor hierarchy," the paper says.

"Depositor preference could be introduced by adding a new class of preferential creditors to Schedule 7 of the Companies Act (and, to the extent applicable, other relevant legislation). In the wake of the Global Financial Crisis, a number of jurisdictions have reformed their depositor protection schemes, and this has included supplementing deposit insurance with depositor preference (for example, both the EU and the UK have introduced preference regimes). At the end of 2013, 62 of 99 deposit insurers reported to the International Association of Deposit Insurers that they had some form of depositor preference in their jurisdictions."

The paper says responses to previous submissions were evenly divided on whether depositor preference should be introduced.

"Some of those in support of depositor preference mentioned that the depositors of credit unions already rank ahead of other unsecured creditors and a preference would enhance market discipline for other deposit takers. However, a number of banks and the New Zealand Bankers' Association noted that depositor preference could significantly increase the cost of wholesale funding, particularly for small banks," the paper says.

"Some submitters also said they were opposed to increasing the complexity of New Zealand’s creditor hierarchy. If depositor preference is introduced in New Zealand, it is proposed that it will only apply to insured depositors. The alternative options are to prefer both insured and uninsured depositors equally; or to prefer insured depositors above uninsured depositors and uninsured depositors above general unsecured creditors. Limiting the scope to insured deposits would maximise the deposit insurer’s recoveries in a failure (as insured depositors would rank above all other general unsecured creditors) and limit the risk of unintended impacts from the introduction of preference."

Meanwhile the paper suggests the Crown's deposit insurer will be located within the Reserve Bank. This is due to the "high costs" of setting up a stand-alone entity, the proposed narrow mandate of the insurer, and the synergies with the resolution, policy making and statistical functions of the Reserve Bank.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

55 Comments

Why even worry about it when the government is clearly prepared to bail out anything and everyone during a crisis to the tune of billions of dollars anyway ?

Because the US bail outs are failing and if they fail NZ bail outs fail.

Because people will worry about it and runs on banks are worse than you’d want an economy to get.

'and the ability to restore to solvency or to recapitalise a failed deposit taker using statutory bail-in. That means providing the Reserve Bank with the ability to ‘bail-in’, that is, write-down or convert to equity, certain unsecured bank liabilities, as a new mechanism to recapitalise a failing bank.'

There we have it, time to get your money out of the bank.

Very good research and articial Gereth. Especially at 5.00 in the morning...

It may be too late if you haven't got it out already...

Nah. Problems start happening when mass hysteria hits. Most kiwis are still unaware that anything bad could happen.

I really don't want to see a Northern Rock event, though that banking collapse in the UK did help to vastly improve saver protection. Pity NZ didn't take any notice since then. BBC Northern Rock: How the crisis improved savers' protection. https://www.bbc.com/news/business-41226937

So am I reading this correctly..... our cash in the bank is not covered at all as things stand right now.?

Not one cent.

And the Govt / bank can choose to 'bail in' your money to save the bank for the greater good.

Adding to Kezza's comment and responding in part to Carlos above, while the Government is bailing "everyone" out, that does not mean depositors. They are supporting workers by subsidising business's through the crisis. So the OBR may still be enacted if this crisis goes far enough. what style of haircut do you want, no matter they give you white walls? Bank hairdressers may yet be an essential business in this crisis. This is about bank health not yours, you don't count!

In many respects you can't blame the Government. They are trying to ensure jobs survive the lockdown and what ever comes after. The problem is people are at risk and they are driving a lot down a deep, dark hole with little hope of being able to climb out.

Correct.

Australia provides deposit protection up to $250k.

It used to be $1M. If you have $1M you can spread it around four Australian accounts at $250k each.

Correct.

Australia provides deposit protection up to $250k.

It used to be $1M. If you have $1M you can spread it around four Australian accounts at $250k each.

That’s technically incorrect Aussie changed the rules to a bail in if need under high stress

Also note you will struggle to get a term deposit rate in Australia above 1%, yet NZ still has 2% headline rates.... and this is the rub... there is no free lunch.

I suspect a high proportion of those moaning about the lack of deposit insurance are also moaning about low interest rates on savings..... well... the bad news is that introducing deposit insurance will probably take ~0.6%-1% off the rate you are getting on your deposit. Are we all willing to accept that? Maybe some are, maybe some arent.

Why not let depositors choose. Let me put my savings in a Westpac unguaranteed savings account and earn say 1% while someone else can choose to put the money in a Westpac guaranteed transactional account and earn 0.1%. For 0.9% extra interest I will sign whatever waiver or acknowledgement is required.

If i am willing to acknowledge and accept the credit risk why do I need the government to tell me what is safe and what isnt.

Its no good everyone saying "Yea, i want deposit insurance". Why not push the argument forward and say how much you are willing to pay for it.

Problem is, everyone is holding the risk now without that many people necessarily being aware they are.

1 or 2% TD return..either number is worthless anyway, you're loosing money due to inflation. 5% instead of 5 1/2-6%...quite palatable to me. Even at 2.5% it is not worth having your money in a TD long term no matter what's going on in the world, especially without deposit Ins.

148 countries have deposit insurance out of 196 countries in the world. NZ is just so much smarter..along with the 40 od other underdeveloped countries you have probably never heard of.....perhaps invest in Pastoral House at the top of the page...they'll give you 6%...…:)..for sure

OK, so now we can prepare.

Term deposits which are in for more than 3 years should be $50 grand max. And should be spread around between the 4 Oz banks. Although if the Kiwisaver is with one of them so, no more in that one.

And maybe put more than 50 in Kiwibank given that there would be way more pressure on the govt to bail out that one.

Any extra above this into Kiwibonds.

Sorted.

If your money remains intact until then.

I've been thinking about moving all my term deposits into kiwibonds as they mature in the next 1-3 months. 6 months kiwibond term. Does that make sense in the current environment, or am I about to do something stupid?

My goal is to minimise losses, at the moment I don't care about the returns as long as it's not negative.

That would be an extremely conservative move. Not stupid.

At 0.75% before tax, it is a very low payout if you put everything in there, but then again, times are uncertain. By the way, tax is small if the interest rate is small!

In recent times the powers that be have made term deposits way worse by instigating OBR, covered bonds, the notice period for early withdrawals, the recent reduction in required core funding ratio and with the lowering of the cash rate, interest rates have dropped!

Plus Kiwibank used to be guaranteed by NZ post, not any longer.

Deposit insurance sounds insufficient to me to cover large bank failures.

Its all been one way traffic.

Definitely adds up to an all pervading nervousness with me!

Thanks for the feedback. I have 2 term deposits maturing this week, I think I'll transfer that money to kiwibonds then.

Am trying to figure out myself how Kiwibonds work and how to buy them through the share trading platform. Have bought shares but not bonds.

I sent them an email and got a response quite fast. (nzdm at computershare.co.nz)

Cheers.

This will just drive rates to zero even faster, adding to the deflationary pressure. Between this and the minimum wage increase, it's like pouring fuel on the fire.

I would suggest if you have large sums of money in a bank account that you consider doing something with that cash so it can't be confiscated.

Not very reassuring all this..

23 October 2020 deadline for consultation? The likelihood of a banking crisis in the next few weeks or months seems high. This is one of the scariest articles I've read in a while. I thought it was an April fools day joke, but sadly not.

Yes agreed it's ridiculous that the NZ Government has dragged it's feet over this for such a long while, it's been well over a year now since they first started to discuss saver deposit protection schemes. This is clearly choosing to close the stable door once the horse has fallen through the floor.

Not sure Winston would stand by and see his voters to lose their bank deposits.

Winston tows the Labour line now days. He has done his time and wants out.

AND

Can we trust Wontson to do anything his is meant to do now?

Remember his speech when he announced he had negotiated a coalition with Labour .... he warned that the world was building up to a financial crisis, and not to blame the government when it all hit the fan.

I see the deposit insurance covers basically all accounts including on call/ everyday ones. Does OBR cover those too or just term deposits. The other thing I've never understood about OBR was whether it completely wiped out shareholder ownership and do the deposit loosers then gain shares or ownership of the entity.

Shareholders, bondholders get wiped out first and then all depositors lose everything over an undetermined but probably low amount and probably don't get it back, and no, they won't own the bank or the Govt they just bailed out with their life savings

So who then owns the bank?

Nobody. The bank owns all of us.

I have been holding physical cash for a while now because of this, better safe than very sorry. Greece and Cyprus good examples of what can happen

long ago, I pointed out that having the stuff you were gonna buy in the future, was safer than holding proxy.

And the problem is that there is more proxy - more forward collective betting - than theree is planetary underwrite.

Something has to give.

So you have stashed a lifetime supply of fuel, vehicles, hardware and other things you can't make?

I also got cash out 3 weeks ago. I had to wait 3 days for the bank to get it in and it wasn't actually that much. Problem is if hyper inflation hits the western world then it makes no difference as paper currency is worthless. I'm thinking maybe i should buy the ford ranger I've been looking at..

I am no fan of those smelly things: driving along behind them with the windows down is very unpleasant. Plus they are tall and wide so you have to be miles behind them to have a safe and relaxing drive. They accelerate fast but are very slow on the corners.

However, if you have your heart set on one, I suggest you wait for 6 months or more, there will be a flood of second hand ones on the market to choose from.

You got me there because my friend dragged me out of a ditch with his ranger and the power was impressive. Would consider any ute if you recommend.

This is outrageous. While they have dithered with no deposit insurance at all, and are still planning to not act until 2023, the housing market and general economy is going to be on its knees and banks along with it. They should step in immediately and implement deposit insurance of at least $150k, if not more. Do they want a run on the banks?

Pathetic. NZ and its bloody "consultations"

Don't worry this is not going to be the biggest credit crunch and liquidity crisis in history and the banks are fine and the sea is drinkable water.

How long til your and my deposit is regarded as fair game for the men from the ministry to come in and give you your hair cut.

Agree. If there was ever a time to quickly step up and assure (and insure) people their deposits are going to be safe, this is it. Plenty of us saw a situation like this coming, not the pandemic specifically but any big catalyst event like this, why didn’t they?

The reserve bank will be monitoring daily cash and atm withdrawls and will act if a run is starting.

Act how? By freezing bank accounts, closing down withdrawals? Oh that would be just great for NZ’s economic position in the world. They need to insure deposits so it’s not a possibility.

Yes, the guarantee would come immediately with the stroke of a pen.

Problem is kiwis will accept it and cindy will front the media saying it's for the greater good and about kindness.

Other countries there would be riots. Funny enough riots were all over the world recently like yellow vests in france and the Chile protests and hong kong etc. Those have all been shut down so now is the time to pass laws that take away our freedoms.

That is absolutely bang on the money, excuse the pun. Because if a run starts then freezing is what they will do like Cyprus but that simply would destroy nz.

We have no hope with this govt in charge by the time they do anything it will be to late.

Jacinda needs to grow some balls and lead instead of papering over everything.

Luckly I took my money out of NZ last year and will leave in Australia as they seem to be on top of things and will come out of this in a stronger position

For fairness we need a scheme to confiscate all houses over a de minimus of one average house per couple, to be sold to bail out the banks, to balance the OBR bare faced robbery; we could call it the OHR??

If an OBR event seems likely, surely many would buy houses and take a moderate haircut, rather than a 95% haircut??

Open Home Resolution.

Genius. It could also help achieve the Kiwibuild numbers, given we have 300,000 rental houses already receiving welfare subsidies to improve yields. Takes only a third of those to make up KiwiBuild.

Thanks Orr & team for listening to moi.. ;-)

Now, move all those idle funds to ASEAN banks, foreign banks in NZ or just across the ditch, the OBR is coming before that 2023. Which parts that I've stated in this website not happening again?.. they'll listen to moi for sure

I'm guessing more than likely they will eliminate cash and go full digital so we are trapped in the banking system. It will allow the banks to go deeply negative with rates.

The govt will use the covid 19 saga as the reason saying the cash is dirty and people could become infected. Infact supermarkets are advising no cash. This is the excuse they are looking for.

When i gave my submission to the reserve bank last year on the future of cash. I suggested that digital is fine so long as you can store digital currency outside the banking system. But i was strongly against banning cash.

If they do go digital then I'm moving my currency into a credit union.

Not insuring our bank deposits,which consist of our life time savings, is like ruining our lives. Can we all come together and send a petition to The PM or Finance Minster?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.