By Gareth Vaughan

Just before Christmas, when most of us had Santa Claus and summer holidays on our minds, the Government confirmed it will introduce deposit insurance of $50,000 per individual per financial institution.

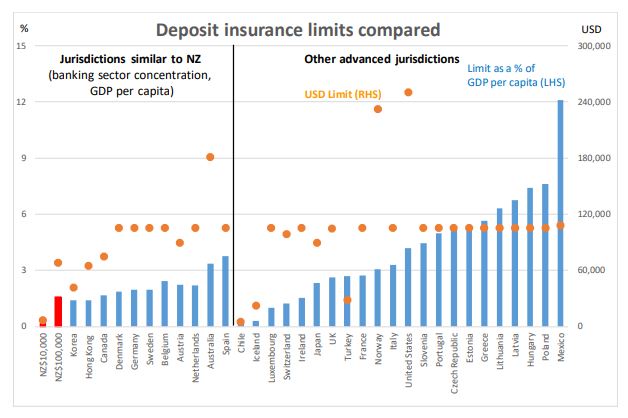

This follows years of debate over New Zealand's position as an OECD outlier in not having deposit insurance. However the limit, which will see deposits held by New Zealanders protected up to a total of $50,000 at a single deposit taker (banks, credit unions, and building societies), is significantly lower than limits in comparable countries. Australia, for example, has an A$250,000 limit for each account holder at every bank, building society and credit union that is incorporated in Australia and authorised by the Australian Prudential Regulation Authority.

Robertson says NZ not having a deposit insurance scheme means if a deposit taking institution failed, depositors would be dependent on a liquidation or receivership to try to recover their money, which could take years.

"An explicit deposit insurance scheme means that depositors will be able to have prompt and certain access to some of their money," he says.

The deposit insurance scheme will sit under a new Deposit Takers Act that will govern the Reserve Bank’s regulatory powers. Robertson says cabinet will make final policy decisions on the Deposit Takers Act and the deposit insurance scheme in mid-2020 following further consultation.

Why $50k?

So just how did the Government come up with the $50,000 limit?

Confirmation of the $50,000 figure came among cabinet decisions from phase two of the Government's review of the Reserve Bank of New Zealand Act after public consultation. However the consultation did not specifically ask what the limit should be. Rather we were told and asked: "The Minister [Finance Minister Grant Robertson] has made an in-principle decision that the depositor protection regime should have a limit in the range of $30,000-$50,000...what coverage level would be best within this range?"

How was the in-principle decision for the $30,000 to $50,000 range made?

Asked about this a spokesman for the team of Treasury and Reserve Bank staff overseeing the Reserve Bank Act review told interest.co.nz the recommended limit is consistent with guidance from international bodies that the vast majority of depositors should be fully covered, while leaving a large share of the value of deposits exposed to loss. The spokesman points to a December 5 cabinet paper released by Robertson. It says the $50,000 limit would cover "the vast majority of depositors, thought to be 90% or more."

However Robertson acknowledges consultation feedback supported a higher coverage limit in line with international practice.

"Insurance coverage limits in most developed countries are significantly higher, European countries have limits around NZ$175,000, for example," Robertson says.

Elsewhere the Canada Deposit Insurance Corporation limit is C$100,000 per depositor per institution, Hong Kong, Singapore, Ireland and the UK have limits per depositor per institution of HK$500,000, S$75,000, €100,000 and £85,000, whilst the US Federal Deposit Insurance Corporation limit is US$250,000.

Robertson points out that with the NZ limit applying per depositor, per institution, depositors will be able to obtain coverage for more than $50,000 by splitting their savings across accounts held at different deposit taking institutions.

"Applying the limit on a per institution basis means that deposit takers can readily calculate the insurance coverage of their customers, and that at the margin depositors are incentivised to diversify their accounts across the industry," Robertson says.

"I envisage that the coverage limit would be set by regulation, so that it is under the control of the Minister of Finance and may be regularly reviewed without needing to amend primary legislation. When the scheme is in place, it will likely alter depositor behaviour. More data will become available on the proportion of depositors that are fully covered by the limit. This supports the case for reviewing the deposit insurance scheme once it has time to bed in."

The spokesman also points to advice on international best practice from the Basel, Switzerland-based International Association of Deposit Insurers (IADI). March 2013 guidance from the IADI says; "Full depositor protection for the vast majority of depositors, e.g. 90% to 95% or more of all depositors depending on circumstances, is now seen as critical to overall financial stability."

$50k a compromise reached by Treasury and the RBNZ?

In December interest.co.nz reported Treasury and the Reserve Bank had been at loggerheads over the relationship between new bank capital requirements and a deposit protection regime. Additionally differences of opinion at the two government agencies might be a factor in why $50,000 was settled on as the deposit insurance limit.

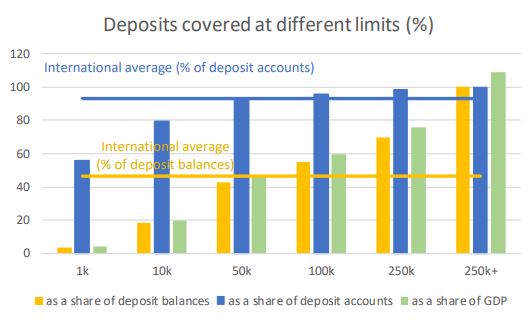

A Treasury information release from last July notes the Reserve Bank Act review team recommended about 95% of individual depositors would need to be fully protected from the risk of loss in order to mitigate incentives to join bank runs, whilst a meaningful amount of deposit balances, about 50%, would need to remain at risk to encourage incentives to discipline banks.

"Based on preliminary analysis, this implies an insured limit of around $100,000," the Treasury release says.

"The review team believe this level of coverage would be politically robust, reducing the risk of governments - when faced with a failing deposit taker - feeling pressured into using taxpayer funds to bail-out the institution or its depositors."

"The review team understands that the Reserve Bank favours a narrower, ‘avoiding hardship’ objective which they argue would imply a lower coverage limit – e.g., $10,000 – on the grounds that a financial stability objective would be unachievable without almost full coverage of deposit balances," says the Treasury release.

The Reserve Bank has traditionally been opposed to deposit insurance. For example, in a 2016 speech the Reserve Bank's then head of prudential supervision Toby Fiennes said deposit insurance blunts incentives for banks and depositors to monitor and manage risks properly. (Fiennes is now the Reserve Bank's head of financial system policy and analysis). The review team is advised by an Independent Expert Advisory Panel appointed by Robertson.

The Treasury paper goes on to say that a deposit insurance scheme's coverage limit should be calibrated to the scheme's public policy objectives.

"The review team’s recommended dual objectives for a deposit protection regime align with international best practice, and in turn imply an insurance coverage limit comparable with international norms - which reflect extensive experience around what level of coverage works, and what doesn’t, in advancing those objectives."

"For New Zealand, as an indication only, this could roughly equate to a $100,000 insured limit. Based on current data, this would fully protect 96% of individual deposit accounts - meaningfully mitigating their incentives to join runs - whilst leaving 55% of the value of deposits exposed to risk - preserving an important market-based channel to discipline bank risk-taking and absorb losses in a failure. This limit is also broadly in the region of the approaches seen in advanced countries with similarly concentrated banking sectors as New Zealand’s," says the Treasury paper.

"Alternatively, a deposit insurance scheme could be designed with the solo aim of preventing financial hardship for those with relatively low bank balances. The Reserve Bank suggests that such a scheme would probably imply a lower coverage limit, e.g. $10,000, than would be the case under the Review team’s recommendation. A $10,000 insured limit would protect 80% of deposit accounts and leave [about] 80% of the value of deposit balances exposed to risk."

(The charts below come from the Treasury paper).

What James Shaw was told

Meanwhile during ministerial consultation Associate Finance Minister and Green Party co-leader James Shaw asked how the $30,000 to $50,000 coverage limit was decided, and whether discussion of the range needed to be made more explicit.

The review team told Shaw; "International best practice for effective depositor protection system guides that the vast majority of individual depositors should be fully protected from loss, whilst leaving a large share of deposit funds exposed to risk, and thus market discipline: it is widely accepted that covering the vast majority of depositors strengthens the role of deposit insurance systems in the safety net."

"An insurance limit of $50,000 would fully protect about 90% of individual deposit accounts in New Zealand, while leaving 60% of deposit funds exposed to loss. This coverage is broadly consistent with modern international averages – especially keeping in mind that the share of depositors that would be fully covered is likely to be higher in practice, as depositors split their accounts to take advantage of the protections."

The Government says funding for the deposit insurance scheme should come from levies collected from licensed deposit takers. "I.E. a user-pays model where the costs are borne by institutions and potentially depositors benefiting from the scheme." The Government says it will provide a funding backstop, "so the scheme maintains public confidence even if systemic banks are under threat. Any funding provided by the government will ultimately be paid back by levies on deposit takers."

The review team estimated that at an insurance limit of $100,000, the deposit insurance scheme would have to borrow $8 billion from government to fund a payout for one of the big four banks. It estimated all costs would be recovered and all borrowings repaid within eight years.

(You can see more on the Government's plans for deposit insurance here and here).

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

16 Comments

How does this work. If $50K covers 90% of NZrs does that then mean only 10% of us has more than that invested. And even if the deposits were spread over another three banks, and exactly how likely is that let alone beyond three, then that is only $200K. If our Australian owned can front up $250K over there, much much vaster scale of operation of course, why then are NZ provided so little. Could it be that the cover here has had to be dragged down by the like of SBS,TBS,Co-operative.

They were afraid of pissing the Banks off Foxy, so they kept it light. Too light in my opinion. the Banks should be fully liable for all their depositors funds and if their practices are sufficiently shady to put them at risk, then the shareholders should be liable for them. (note i am a shareholder of one, albeit a very small amount). The pollies are too scared of big money to do anything really meaningful.

Interesting though i note that at the up-coming meeting at Davos, a topic under discussion will be the future of economic policy, seeing as how the masses are starting to revolt against existing and past practice.

Yes Murray the whole thing looks like half a horse, and to borrow from the late David Lange, you don’t need to look too hard to see which half it is.

What most people have forgotten is that nothing has been said about OBR - will that remain - it needs to as it gives access to the transaction system quickly anyway - and with OBR there is still a requirement for a de-mininimus exemption or cut off for retail - and that is effectively guaranteed anyhow under the statutory management rules - in fact all liabilities of the failed bank, once assumed by the statutory manager are guaranteed - so the acutal amount could be higher - just the ex post amount that requires pre-funding is lower.

And to be fair - the fence at the top of the cliff - capital is being significantly increased and therefore the ambulance at the bottom (deposit insurance) doesn't need to be as well equipped. This is where Treasury got it really wrong - capital is not fungible for deposit insurance - it is far superior - and is about maintaining stability - Deposit insurance is about maintaining votes. Why should we pay to keep the politicians happy. Rather have much much more capital and not have a failure in the first place.

Also - average retail depositor in NZ is very very low - only a few have real savings - most retail savings are in kiwi-saver - so its not about the smaller guys dragging the average down - its about a structural difference between us and Aussie - savings in NZ is in housing and kiwi-saver - these aren't held by the banks as liabilities.

Foxglove,

For a number of years now, I have split my TDs over 6 banks. I did that because NZ had no Deposit Insurance, but assuming that at some point, pressure would be applied to bring us into line with other countries.

If necessary, I would see no problem in adding further banks to that portfolio. It requires a bit more effort to do this, but not much.

"When the scheme is in place, it will likely alter depositor behaviour. More data will become available on the proportion of depositors that are fully covered by the limit."

Of course! For me it will have an instantaneous effect. Unless the interest rate is higher for higher sums to counterbalance the loss of security.

"An explicit deposit insurance scheme means that depositors will be able to have prompt and certain access to some of their money," he says.

Isn't that the role of OBR? Or doesn't he know about that scheme?

"An insurance limit of $50,000 would fully protect about 90% of individual deposit accounts in New Zealand, while leaving 60% of deposit funds exposed to loss. This coverage is broadly consistent with modern international averages – especially keeping in mind that the share of depositors that would be fully covered is likely to be higher in practice, as depositors split their accounts to take advantage of the protections."

Totally inadequate, given the regulatory freedom, banks are able to game for excessive short term gains at depositor's expense.

In reality the money supply is “created by banks as a byproduct of often irresponsible lending”, as journalist Martin Wolf called it (Wolf, 2013). Thus the ability of capital adequacy ratios to rein in expansive bank credit behaviour is limited: imposing higher capital requirements on banks will not necessarily stop a boom-bust cycle and prevent the subsequent banking crisis, since even with higher capital requirements, banks could still continue to expand the money supply, thereby fuelling asset prices: Some of this newly created money can be used to increase bank capital (Werner, 2010). This was demonstrated during the 2008 financial crisis. Link -section 5

How do PIE deposits fit into this ? Will they be protected to the same degree?

Unitised pooled investments are a real complicating factor.

they wont be and neither should they be - they are unitised and should never have been covered in the previous scheme either - they are not deposit - they are an investment in a fund that invests in short term assets. Losses to the assets will adjust the fund - and if there is no liquidity to pay out- you dont get your money until there is PIEs are not for short term consumption and payments in the financial system.

Mark L,

Yes.

deposit insurance objectives globally are to avoid political fall out on failure. If you want true stability, higher capital is the best preventative mechanism to avoid failure. Best practice doesn't mean matching amounts - it means matching practices and processes. Lazy assessments and review. Have deposit insurance - but link to the average wage - perhaps ours is so low, because our average wage is so low when compared internationally - and also because our savings approach is to hold in housing and kiwi-saver - and neither of those are guaranteed from failure

INSANE,

One can buy full insurance for just about everything else in life (with a small premium), but the government decides no-one can fully insure bank deposits.

The deposit insurance should have been set to match Australia's.

i wonder if this is more to do with negative intrest rates there was and is still no reason not to with draw all funds from the banks except money needed for bills

As long as you have the likes of Toby Fiennes influencing policy you will not get any educated or logical decisions coming from the rbnz. Just read some of his comments and you'll realise he is an ignoramous when it comes to his theories on what a central banks roll should be.. Only 40% of actual deposits covered? Why bother.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.