Online retail investment platforms Sharesies and InvestNow have both hit the half-a-billion-dollar funds under management mark this month.

COVID-19 has prompted tens of thousands of people to join the platforms, presumably in an attempt to buy cheap shares or get higher yields on investments as term deposit rates drop.

Around 75,000 investors have joined Sharesies since COVID-19 hit, bringing the total number of users up to 166,000. They each have an average of $3000 invested.

InvestNow hasn't experienced the same rush, but still added about 2000 users to its platform per month during March and April. It has 26,000 users, who each have an average of $19,000 invested.

Both platforms launched in 2017; Sharesies to a limited user base initially.

Sharesies co-founder Leighton Roberts in May told interest.co.nz, 70% of the platform's new users considered themselves new investors. He on Wednesday said new users were a bit older and had slightly larger portfolios than existing users.

InvestNow hasn't been quite so flooded by new users.

Its general manager Mike Heath said as well as growing organically, InvestNow expanded on the back of two purchases: the Rabobank fund platform in April 2018; and the AMP Capital direct client book earlier this year.

“We’ve had almost 100% retention of the Rabobank and AMP Capital clients, which shows experienced direct investors appreciate the high level of service we deliver – and our low costs,” he said.

“At the same time InvestNow has seen record new member sign-ups over 2020."

InvestNow is like a funds supermarket that gives users access to more than 140 funds managed by 23 investment firms. It also offers term deposits from five banks and plans to become a KiwiSaver provider in coming months. This would enable KiwiSaver members to diversify their investment across funds offered by different managers.

“We’re also exploring the potential to add NZ corporate bonds to our investment menu and – further down the track – direct equities,” Heath said.

Sharesies enables investors to buy shares in NZX-listed companies, as well as invest in managed funds offered by a handful of managers. It is planning to give users access to US shares soon.

Other than charging low, or in InvestNow's case, no brokerage fees, an appeal of these platforms is that they enable retail investors to invest small amounts of money. Some of the funds in particular would otherwise require larger investments.

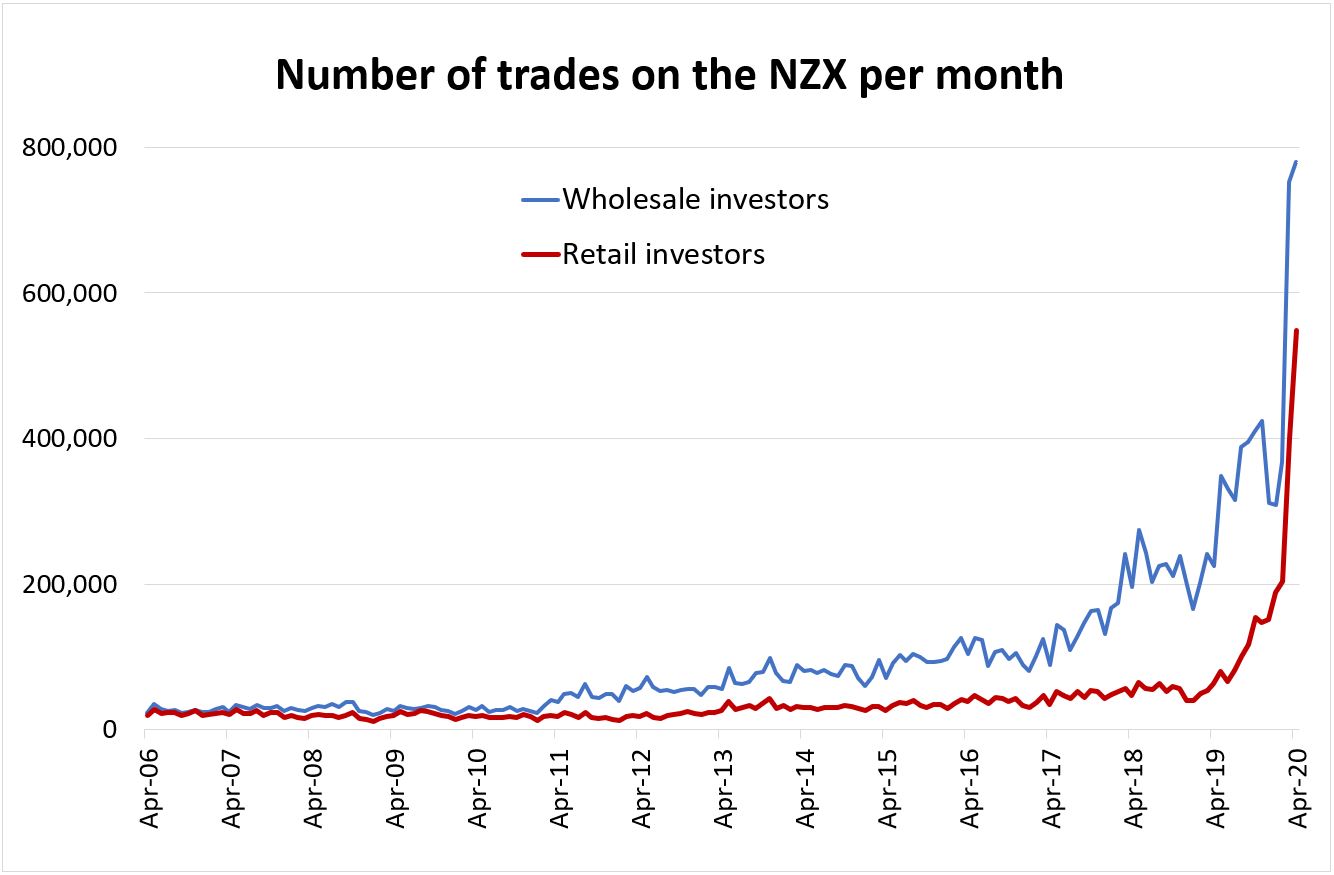

The increase in popularity of both platforms is perhaps no surprise given the spike in NZX trading activity in recent months. The uptick was so major it crashed the NZX's computer systems in April, prompting a major review by EY.

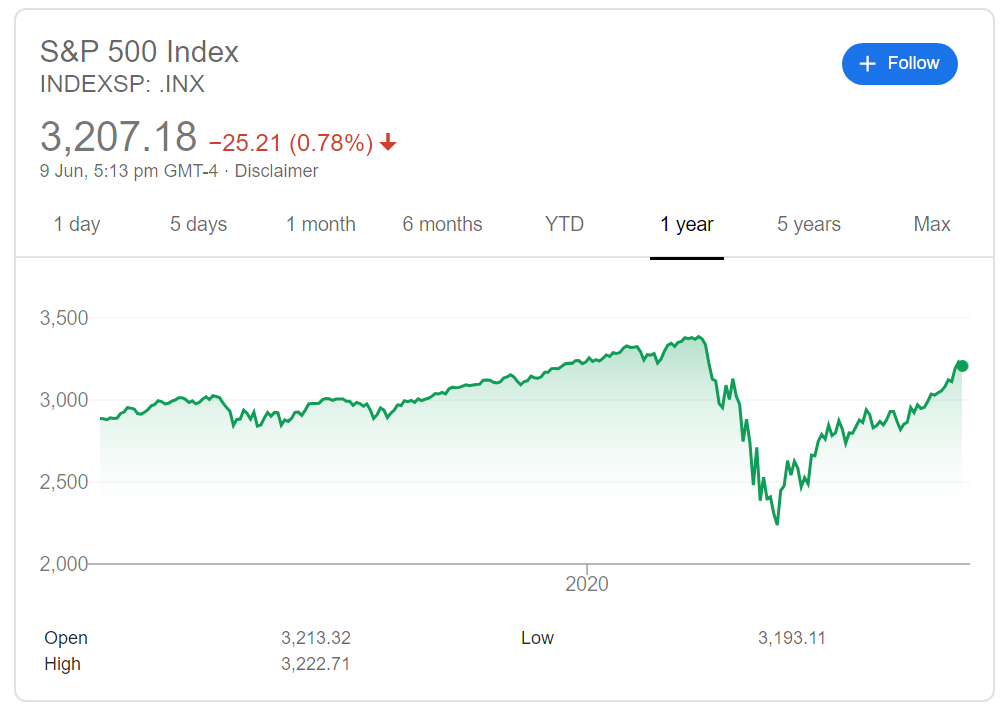

While COVID-19 is still causing havoc around the world and unemployment is only going up, stock markets have rebounded more quickly (for now) than expected.

The uptick has been aided by central banks around the world printing billions of dollars as a part of quantitative easing programmes.

The Financial Markets Authority (FMA) in May suggested do-it-yourself investors don't dive head-first into the share market now, if they haven’t done their homework.

“We would caution against developing a new, untrained, appetite for trading on the NZX during this period of volatility and uncertainty without doing sufficient research,” it said.

The regulator’s warning came as its Australian counterpart, the Australian Securities and Investments Commission (ASIC), released a paper ringing the alarm bells over the spike in retail investors chasing quick money.

"Retail investors chasing quick profits by playing the market over the short term have traditionally performed poorly – in good times and bad - even in relatively stable, less volatile market conditions," it said.

32 Comments

I've been pleased with Sharesies - not just for the ability to invest small amounts at a time, but for the nearly real-time transparency of prices. For far too long the share market has locked out smaller investors like me, either by requiring us to have to go through a highly priced broker who demanded a larger parcel of shares to be purchased, or through a general level of mystique and paternalism by those who were able to purchase these larger parcels.

In these current uncertain times it's certainly been interesting to see traditional knowledge about the market get swept away by irrationality. I'm not suggesting that's either 'good' or 'bad', but it does seem like it took a very long time for people such as myself to be able to learn directly, and not through some conservative and arcane intermediary.

Broker websites that I know very clearly state 76% of all retail accounts lose money. In the short term, and while fractional investors are making genius plays like buying Hertz and Chesapeake just before/just after bankruptcy filings, everyone’s boat is getting lifted. But fundamentals (And creditor hierarchy) matter, and anyone drawn in now by fractional investment platforms with cute and accessible names and advertising on Instagram or whatever might just learn this soon.

Sharesies/Hatch/Robinhood etc with the custodial format don’t give you the same benefits as the ‘arcane’ broker path of direct ownership either, and lack some of the more sophisticated hedging tools too.

/paternalism

Is it the right time to buy when everyone is buying (even people who had never invested or heard about stock before) and stocks are near all time high despite economy being badly affected by Panedemic and only thing keeping it alive is printing of money by government in full swing.

Time to book profit as now, it needs one bad news (As if, we have no bad news now) and stock market may tuumble.

I don't disagree. Not everyone gets to win the race and the difference between equity markets and economy is not well understood by first timers. But kiwisaver has made us all investors by default, so it's better to take an active interest than a hands off approach..

I am a KiwiSaver account holder in a growth fund so my profit margin flows, both positively and negatively, with bonds, domestic and international share prices. As I don't own the shares I don't get the bi-annual or annual (profit) dividends of my investments. In these times,I am sure there are no dividends paid out as well, companies may also stop trading therefore giving the investor a total loss. Having said that I am interested in investing in the NZ sharemarket but as a individual invester what shares can you buy and what shares carn't you buy ?

Remember the Stock Market Crash 2008? Sure do! Nasty.

The Finance Company collapses a few years before that? Shiver…Oh, yes!

The DotCom Bust of 2001? Just. It was early on in my career.

The Rusian Debt crisis of ’98 and the collapse of the US fringe bankers? Not really.

The Goats and Ostrich Farm Bubble before that? Nope.

The ’87 Stock Market Crash? Yes! I read about it in the history books!

So if history is anything to go by, the promoters of Sharesies should be picking up some vacant farmland about now and get some breeding goats in ....That's probably as good a buy as anything else.

I'm as old as the '87 crash, but before that, nope. Mind you, that's what the internet is for.. and opinion is divided 'out there' on buying or not per se. Just because bubbles burst due to overvaluation doesn't mean there isn't money to be made e.g. A2 shares gaining 25% from Jan to late March. Not everyone's a winner.. but some picks are better than others.

You can buy NZX50 and around a dozen ETFs

Ostrich farm bubble was hillarious. A dear friends parents went large on ostriches saying the ability to use ostrich tail feathers to clean integrated circuit boards in computer equipment meant the ostrich industry was gonna boooom. After I showed them how to easy it was to clean a circuit board using a can of compressed air I was not invited to dinner for several weeks!

Logicthinker,

As a novice, I would strongly suggest that you contact a broker like Craigs. There are several of them. They do have higher dealing costs than the platforms but can help you to start building a portfolio. if you feel comfortable, then you can start educating yourself by learning what the different terms mean-P/E ratios, ROE, debt/equity and so on. Investopedia is a good place to start.

"The Financial Markets Authority ...suggested do-it-yourself investors don't dive head-first into the share market now...without doing sufficient research”

Do research? What on earth for! Fundamentals don't apply any more and haven't for over12 years.

There's good money to be made by savvy bankers and brokers from all sorts of cashed-up 'investors', and they are going to take it.

(Someone show me their research that shows Air NZ is worth more than 1 cent, other than the $900,000,000 facility that the company is waiting to fleece the taxpayer of and tell me it's worth $1.85 that it currently trades at!)

Research! Give me a break.

Even first timers get 10 free company profiles with Simply Wall Street. I'm not advertising for them, just questioning the assumption that first-timers won't research how they spend their money.

I know what a financial analyst and their analysis looks like; I employed them, and a 1, 10 or 100-page production by a broking house isn't it.

By the time most people; most by far, understand what that 'research' tells them, and buy", the really clued in are already selling.

Fair enough. I guess that's what disruption is. It may be I come back to these forums looking for better advice having lost my shirt. But I am pleased to have the opportunity of finally being able to purchase shares after years of effectively being locked out from the market.

Mā te wā.

An opinion from a 'researcher' that I have time for, and just like the best of them, he didn't 'go public' with his view until AFTER he'd got himself set. But, of course, it's just another view that makes a market.

Stock markets are “lost in one-sided optimism”, according to Jeremy Grantham, the veteran strategist known for calling several of the biggest market turns of recent decades....economic realities had been “temporarily overwhelmed” by central banks’ unprecedented stimulus efforts, he said, but “it’s hard to believe that will continue”.

https://www.ft.com/content/ca6fef7a-7caa-4e89-927a-e3043bd0dc3e

How have you been "locked out" of the share market? ASB Broking and Direct Broking have existed for about 20 years now, so there has been nothing stopping you from self directed online share trading. And both at least provide free research and financial analysis for NZ listed shares. The minimum NZX share parcel is a mere $500. I suggest if you cant scrape together $500 you probably shouldnt be investing in the share market at all, and should be focused on saving an emergency fund in a bank account.

Yip my general observation the last 3 months or so has been a lot of new investors buying up large, then I look to Warren Buffett who hasn't been.

Why research when you just need to decide if there will be more QE? If yes, buy. If not, hold?

Rumours and Fake News are the new Research ?

What about Kernel and Hatch ?

On a lighter vein, this may explain our behaviour ?

Quote :

The Boredom Markets Hypothesis, BHM Syndrome, is the idea that a lot of individual investors buy stocks mainly because it’s fun, and that the more fun stocks are, and the less fun everything else is, the more they’ll buy stocks. In a pandemic, when people can’t really leave their house and sports are canceled, there is a lot less fun to be had elsewhere, so trading stocks seems relatively more fun, so people buy more stocks.>>>Matt Levine.

It may be true specially with market rising after the initial tank.

Yes that probably contributes.

You know what else is boring? Bank deposit and term deposit rates. Especially alongside any hints that bank stability is not a sure thing in the current environment.

So if banks are unstable, what do you reckon their shares will be worth if any of them makes good on that stability you mention?

My view? $zero the second any one of them hits trouble.

Its been interesting to see that the two entrenched direct broking services, ASB and ANZ have responded somewhat to sharesies and so forth by reducing their charges for smaller parcels in recent years, which is good for investors who wish to reinvest dividends into their portfolio.

Sharesies is a great platform. I hope they survive the public outcry if all their new small investors lose their shirts.

That said the ride up has been incredible the last few months.

I'm reminded of that old song - how does it go?

"Catch a falling knife and put it in your pocket,

Never let it fade away,

Catch a falling knife and put it in your pocket,

Hope it funds a rainy day"

With deep apologies to Perry Como....

Sounds like Hertz Rent-a-car investors!

2 cents today, and that's down another 30%, on their way to worthless.

https://nz.finance.yahoo.com/quote/HTZ?p=HTZ

I hope these fools running where Angels fear to tread are not using borrowed money

Unless you're risk averse why would you keep it in a term deposit - returns are so piddly it isn't worth it. Of course markets will always win in the end no matter what jiggery pokery governments and central banks throw at them. This could end in tears.

Still waiting for proper 2FA two factor authentication to be implemented on sharesies.

Saying we are secure is all well and good but many people still use passwords that are easily broken by computers in several minutes.

I love the idea and execution otherwise, very promising new startup.

But early days, wake me up when you implemented 2FA.

I have an account with Direct Broking for long time holds and one with Sharesies to purchase short termers to sell when they move upwards.

Works for me.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.