The resilient housing market is proving positive for household spending currently, but any subsequent downturn in the housing market in the future would be expected to suppress spending, ANZ senior economist Liz Kendall says.

In an ANZ Insight publication, Kendall says "so far", the housing market has been resilient, with housing credit growth supported by falling mortgage rates. She says the wage subsidy scheme has also provided a cash-flow boost to help households weather the lockdown-induced income shock.

"However, there is some evidence that households are nonetheless a bit more cautious about taking on debt. Mortgage lending has been supported, but consumer credit has contracted 11% since February; and borrowing by businesses (ultimately owned by households) has been gradually declining.

"We may see some housing wobbles emerge in coming months as fiscal income support wanes, though the extent that this might be counteracted by further declines in mortgage rates is unclear.

"Any downturn in the housing market would be expected to suppress spending further, deepening the downturn."

Kendall says a pull-back in spending on the part of households is bad for growth in the economy.

"But increasing one’s rate of saving is an understandable and sensible response on the part of individuals. When income or wealth positions are eroded, it is natural to want to shore up financial positions."

She says, however, it's not, in fact, yet clear what is happening with the savings rate.

"This actually isn’t an easy question to answer. The household saving rate is difficult to measure; it is the residual between measured income and consumption, where data on underlying income sources can be noisy and incomplete. Over the period of the Covid-19 crisis, measuring saving will be fraught with even more difficulties and volatility, given that income and spending have both been disrupted by the impacts of Covid-19 and associated restrictions. Saving data is also very lagged; the last data point we have is for March 2019, and we won’t know where it was in March 2020 until late this year. However, Stats NZ is currently working on producing this data quarterly and making it much timelier, which will eventually help improve our understanding."

Kendall says where the saving rate goes from here will depend on income and housing developments, and the impact of interest rates.

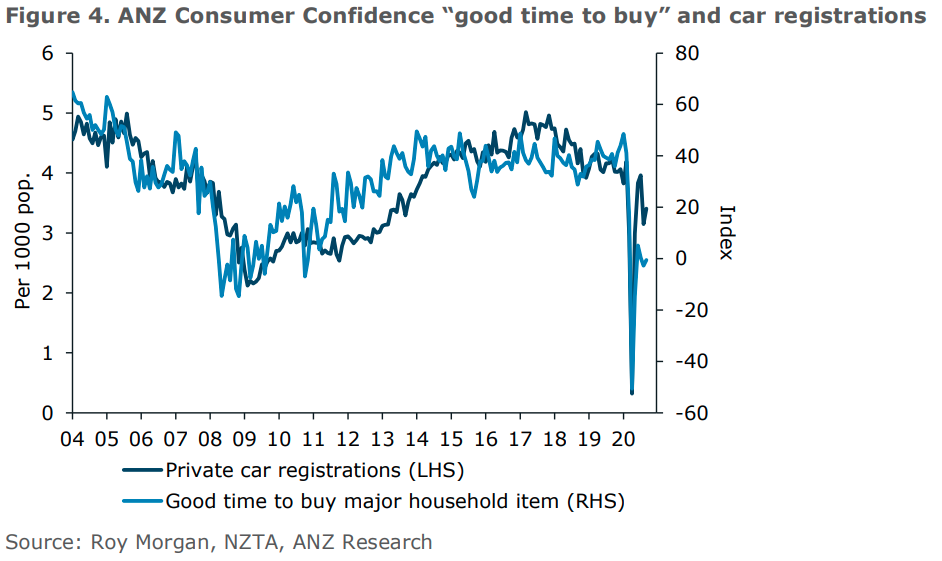

"It is unclear how these forces will net out. But often in recessions, the impetus to save increases. We expect that is happening now too, with dampening effects on growth. One thing we do know is that households are more reluctant to spend, with fewer households saying it is a good time to buy a major household item. The data is consistent with levels seen during the GFC – and this is passing through into durables spending. There was a flurry of car purchases post-lockdown, boosted by pent-up demand, a cash injection from the wage subsidy, and deferred travel spending. But sales have now settled at a more modest level and could come under further pressure as income strains mount (figure 4).

"But is this a higher saving rate or just the impact of lower incomes? Probably a mix of the two – we’ll have to wait to find out."

It is tempting, Kendall says, to look at household borrowing and deposit statistics for clues about household saving, "but the latter in particular tells us very little, unfortunately".

The strong increase in household deposits earlier this year has been primarily a result of the Reserve Bank’s quantitative easing (QE, or money printing) programme and the Government’s wage subsidy.

"Slower growth more recently has been a matter of timing of various financial flows, but assuming that ongoing QE continues to boost liquidity, deposit growth can be expected to continue, regardless of households’ saving decisions."

She says that, likewise, if some households are borrowing more, that doesn’t necessarily mean that in aggregate households are saving less.

"So the upshot is that the saving rate is almost certainly rising, as that is an intuitive response to income uncertainty. But we’ll have to wait to see it confirmed in the data. And deposit and lending statistics are not the place to look."

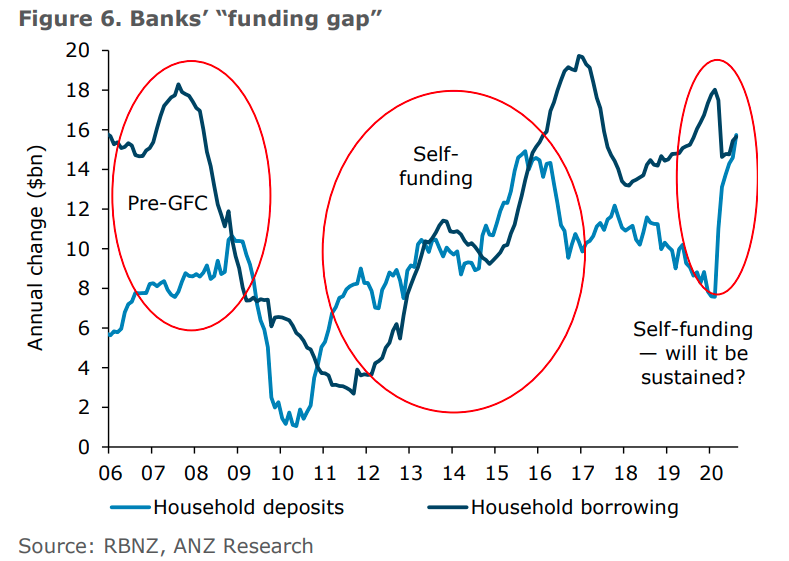

On the Reserve Bank's plans to introduce a Funding for Lending Programme (FLP) by the end of the year, providing money cheaply to the banks, Kendall says this would provide stimulus in and of itself, but could also be used in conjunction with a negative Official Cash Rate to make it more effective.

"An FLP will reduce bank funding costs and thereby weigh on deposit and lending rates, but by how much is unclear. (Note that to the extent that banks take the funds, this will boost the money supply and deposits too.)"

The overall impact of the FLP scheme will be greater, Kendall says, if banks access the scheme at scale and use the funds to lend. But even if the banks do not use the funding, knowing the programme is there as a backstop should contribute to downward pressure on retail rates.

"Take-up of the scheme will depend partly on the strength of deposit growth, and whether banks can “self-fund” through that (figure 6).

"Although deposit growth is expected to remain robust, we expect there will still be a reason for banks to take up funding via the FLP, because it will be cheaper. But how much funding is taken – and how stimulatory this will be – will depend crucially on the strength of credit demand," Kendall says.

"Downward pressure on retail rates will provide an incentive for households to borrow and spend. However, although we expect the FLP will be stimulatory, households are likely to remain somewhat cautious towards debt and spending as the weak economic environment becomes clearer.

"As such, the RBNZ is likely to conclude that more stimulus is required beyond the FLP for it to meet its inflation and employment mandate. We expect that the OCR will be taken negative in April next year."

54 Comments

Anyone know why qv results don't seem to be getting released anymore?

Is that because they dropped corelogic?

Narrabeen

"Anyone know why qv results don't seem to be getting released anymore?"

QV is now called CoreLogic.

CoreLogic data - using exactly the same parameters as QV - continues to be released. RBNZ now use "CoreLogic" data but note that it was previously called QV.

My understanding is that CoreLogic is USA in origin. In the USA they are involved in a range of data tracking and analysis and have become involved in Australia and NZ especially in property data. My understanding is that QV were previously using their systems and CoreLogic may have had some buy in.

I think new QV values were suspended for a year a couple of months back but unsure.

The “wealth effect” is real, and a good thing in times like this.

Why the Wealth Effect Doesn’t Work.... history suggests the opposite: it is higher savings rates which lead to economic prosperity....why do so many “preeminent” economists falsely believe in ... the wealth effect? It is because of their mistaken understanding of the nature of savings.

https://mises.org/library/why-wealth-effect-doesn%E2%80%99t-work

No. The 60% + of NZ homeowners after checking Homes.co.nz & OneRoof -

https://streamable.com/ytua8i

https://www.nber.org/papers/w15075

"Once we control for the endogeneity bias resulting from the correlation between housing wealth and permanent income, we find that housing wealth has a small and insignificant effect on consumption."

https://www.nber.org/papers/w9848

"The findings suggest that most macro models which make no allowance for transitory variation in wealth that is orthogonal to consumption are likely to misstate both the timing and magnitude of the consumption-wealth linkage."

https://www.nber.org/papers/w14204

"In a representative agent model and in the Yaari-Blanchard OLG model used in the paper, there is no pure wealth effect on consumption from a change in house prices if this represents a change in fundamental value."

The “wealth effect” is real, and a good thing in times like this.

Not necessarily. Doubling down on bubbles in an attempt to save the economy from imploding has never worked anywhere. There is no evidence of it. You're just trolling.

"Wealth effect" might be real, but it's certainly not helping our economy. Our annual GDP growth constantly dropped from 3.9% 2017 to -2% this year. Yet housing price is constantly rising, and OCR also dropped from 1.75 to 0.25 to contribute a lot of stimulations. What we are doing right now is not helping our economy and continue to back ourselves into a corner.

No, it is just another neo-liberal fantasy that tries to make everyone feel like the benefit of a few wealthy ones is also positive for them.

John Key realized that the only way we could all get rich and prosperous was for us all to sell houses to each other at a higher and higher price. He also realised massive immigration also helped to push up house prices.

Then reduced his exposure to the NZ market

I suppose it's a mixed bag. I have my spending crimped right back for fear of not being able to cover rent and bills.

I can't speak for the winners.

Given I'm already close to rock bottom on the consumption tread-mill, I suppose if asset prices go up or down I don't matter - I won't change my behaviour anyway, so the net effect will be based on the effect on other people.

Just remember debt is not wealth. Those taking on record debt to purchase property aren't wealthy unless prices continue going up, in which case the greater fool theory comes into play.

Article headline = Ten-Bob each-way bet

Update from across the ditch:

https://www.smh.com.au/money/borrowing/property-price-warning-as-jobkee…

But the Herald says New Zealand is different...

The resilient housing market is proving positive for household spending currently, but any subsequent downturn in the housing market in the future would be expected to suppress spending, ANZ senior economist Liz Kendall says.

This is an economic trick applicable to the already wealthy minority, but not to the asset deficient households who are the majority.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax. Link

Not sure it is the minority that this “trick” applies to. Don’t over 60% of NZ households own their own home? Over 50% in Auckland.

How many of that 60% have assets that exceed their liabilities in value?

Not sure, but surely it is a very high proportion, even when taking personal loans and hire purchases into account. Can’t be many mortgages “underwater” at this point given how the property market has performed.

So you're saying that a very high proportion have more equity than mortgage? Based on?

I said I'm "not sure". But given that house prices have been increasing strongly, is there any particular reason that you think any noteworthy proportion of mortgages are "underwater"? Seems highly improbable that many mortgages exceed the value of the property, but would be keen to see some stats.

Given that 100%LVR mortgages are very rare.. almost all of them

Not sure it is the minority that this “trick” applies to. Don’t over 60% of NZ households own their own home? Over 50% in Auckland.

The wealth effect relies on people having money to spend, unless they can borrow to fuel their consumption.

Unless you use housing as an investment it would be a pretty stupid thing to think you are wealthier just because your home is more expensive when you would have to buy another one in the same market unless you are planning to live under a bridge of course.

If stimulating spending is the goal why is the money not being distributed through a UBI instead of being handed out to the landlord class?

Good question to raise. Low income h'holds spend the most (as a proportion) of their income on base needs. Arguably, the best stimulation for consumption would be to hand out money (or vouchers) to those without the income and savings to spend.

.equally as bad idea. It would be spent and then we are back to square one. The solution is to allow the free market to operate...and allow cash (i.e resources which are scarce) to flow where it is most effective. Giving it to Joe to buy a new iphone, pay the rent or buy a box of beer solves what... apart from a bit of time)?

.equally as bad idea. It would be spent and then we are back to square one.

No. Consumer spending is the main engine of the NZ economy. You need h'holds spending on loaves of bread. If you have $500 and spend it all into the real economy, that's better than giving the $500 to me who has no inclination to spend it. Hell, I might even use it to buy some of that wacky Bitcoin. That's the last thing Orr and the ruling elite want.

..consumption is a negative not a driver. Productivity is required. So you want to provide the ability to consume without having to produce to supply the said consumption? How can that work?

Isn't that what's been going on for the past 10 years or so? House prices go up because of increased credit availability -> 'hard-working' mom & pop 'investor' can buy a new Land Rover without lifting a finger.

Isn't that what's been going on for the past 10 years or so? House prices go up because of increased credit availability -> 'hard-working' mom & pop 'investor' can buy a new Land Rover without lifting a finger.

Kind of like that. But also think about it like this. Couple in their suburban bolthole chatting about their friends Wayne and Charlene who're taking a week off for a winter holiday in Samoa. The couple want to do similar. After all the monthly expenses, there's little left. But hey, they're paying down the mortgage and the debt servicing is down. What's more, Granny Herald has been reporting on all the outsized gains and Chinese walking around the suburbs with big bags of loot. Some data suggests the value of their house has gone up. So maybe no Samoa, but there's a great package deal to Fiji.

..consumption is a negative not a driver. Productivity is required

An economy may have low productivity (as many believe NZ has), but consumption (expenditure into the real economy) is the key driver regardless. Japan is the perfect example of this. Productivity in terms of how it relates to industrial production is relatively good even though consumption growth is stunted.

If you think consumption is the answer then lets celebrate the next swarm of locusts. You actually believe that nonsense?

Any notion of free market died when banks started QE. It is now a rigged everything and protect asset rich regardless economy

Exactly right. Hard working Kiwis are, to all intends and purposes, subsidizing a parasitic landowning class through a reckless loosening of the monetary conditions, an uneven tax regime that does not treat all investment classes in the same way, and housing subsidies. There is no free market in NZ now - in a real free market the market forces would have been left to determine the necessary adjustment to the currently inflated house prices, and the corresponding re-direction of resources towards the productive sectors of the real economy.

Agree - its like we're regressing back into the dark ages with lords and serfs and instead of royalty who set the rules to decide how to punish the serfs and enrich the lords, we have central bankers.

Resilient housing market a positive for household spending, says ANZ

Correct, provided it is running on fundamentals and not artfically poped up specially in this uncertain time and worst damage that could be done for very short term gain is removing the LVR as now more are streching with minimum equity so now with even little correction, may run into negative equity. Agree RBNZ will not let it happen by throwing everything to support as now the risk is even bigger BUT what if it happens and economy cycle run its course.

No one like recession but it happens and many time is trigger by catalyst beyond control like panademic.

Except for that resilient is not an adjective that can be applied to the current market since its sustainability is impossible short term.

Plain and simple correct AZN analysis there - the stronger the FIRE economy? the stronger will be on economic spending. We're all hope that RBNZ will go on OCR negative territory by Q1 2021, by them hopefully they'll tweak further of FLP 2.0, which touches most of ordinary kiwis for the LVR opposite decision. And by our academics, professionals get together calculation & think tank? - We really do hope Orr and the team to increase QE/LSAP into at least 300-500billions, territory - this is NZ safe zone economic certainty in the midst all of this Covid period.

Mortgages are debt accruing to bank profits going to Aus. Meanwhile consumer debt down 12% from Feb. So this implies consumer demand will fall regardless of splurge on mortgages.

Exactly, all the income that will go into servicing mortgages will not be cash moving hands.

Which means reduced income for business, which means reduced profit, which means no wage increases, which means stagnation - all of this in an environment where we could have deflation (or even stagflation is you talk to some). Its not a road to prosperity - perhaps more a road to long term misery.

ANZ: "Wahoo! We run a business that can't fail! The RBNZ and government won't let it!"

Exactly - this is one of my key pains right now is why do we have a private retail banking sector if they carry no risk? The executives don't deserve private sector wages. And as there is no risk, nor apparent competition as its more an oligopoly, then why reward boards, directors, executives with such high wages? Business and people may as well just have credit accounts direct with the RBNZ - cut out the middleman. Then the RBNZ can control lending to their hearts desire, which is apparently what they want but are struggling to get the retail banks to do.

Any thoughts?

RBNZ wants to get lending going as in the modern economies, (hooray!) only private bank lending creates money (which juices asset prices!) and they want more for some reason because, something, something, dark-side, something..

It's the definition of moral hazard: `lack of incentive to guard against risk where one is protected from its consequences`. Something to be always avoided, becomes extremely predatory. Sad-face :-(.

How much would a house be worth if it was built at the bottom of a cliff, where a few years back an earthquake-induced rockfall had wiped out the previous house. And a few years after that another 'quake nearly wiped out the replacement one? Not much!

But what if the Council put a note on the LIM saying "We will not let the next earthquake damage this property because we've piled up a whole heap of boulders; the stuff of the last earthquakes, to stop that happening again".

Even less, in my opinion. But, Hey! Caveat Emptor.

Monetary Policy didn't stop the last lot of market 'corrections' and neither will it the next, no matter how hard the RBNZ et al cross their fingers or put out reassuring 'news' bulletins hoping they can.

I guess you'll be voting "YES" to the cannabis referendum

There doesn't seem to be much discussion about NZs situation when things like the wage subsidies end and the mortgage referrals end. Surely these will have some effect on NZs housing bubble?

Knowing my luck, if as a first home buyer, I go and buy my first home, then the NZ housing bubble will pop, and I will be left with negative equity. .

My fear precisely. I'm out.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.