The Reserve Bank (RBNZ) has signalled the Funding for Lending Programme (FLP) it’s designing for retail banks has few conditions attached to it.

The RBNZ's Monetary Policy Committee (MPC) last month said it directed the central bank to be ready to deploy a FLP before the end of the calendar year.

The aim of the scheme, should it be implemented, would be for the RBNZ to provide retail banks with low-cost funding to enable them to lower interest rates. Having a new source of funding would make banks less reliant on securing funding from offshore sources and depositors. Banks could lower rates without worrying as much about this deterring depositors, and thus leaving them with a funding shortfall.

Ultimately, the RBNZ would want to see the support flow through the economy, boosting inflation and employment in line with its monetary policy mandate.

'Any conditionality, you want to be simple'

Christian Hawkesby, RBNZ Assistant Governor and General Manager of Economics, Financial Markets and Banking, updated media on Thursday on the progress the RBNZ was making in designing the scheme.

“You want it [the FLP] to be freely available and you want it to be taken up, potentially at scale, to lower the funding costs so that they [banks] can pass it on,” Hawkesby said.

“You want to keep it as simple as you can. Any conditionality, you want to be simple. You don’t want it to end up inhibiting the scheme [from] being used…

“If you design something that’s too complicated, [and it] becomes too much of a compliance exercise, it just puts banks off from using it. I think that would be something that we need to balance carefully when we do the design.”

Hawkesby said global experience was “mixed” when it came to central banks requiring retail banks to use the funding for certain types of lending or to lend to certain sectors.

He said more information regarding the design of the programme would be unveiled in the November 11 Monetary Policy Statement. He cautioned this didn't necessarily mean the scheme would be launched the next day.

Could a FLP be enough?

Hawkesby said the FLP wouldn’t have to be used in conjunction with a negative Official Cash Rate (OCR), even though the MPC believed such a programme would make a negative OCR more effective.

“We could launch a FLP in itself and see the impact that has on funding costs, how much that gets passed on, where the economy’s at,” Hawkesby said.

RBNZ Chief Economist and Head of Economics, Yuong Ha, stressed the decision around whether to lower the OCR would continue to depend on the economic outlook.

When the RBNZ in March cut the OCR to 0.25%, it said it would leave it there for at least a year.

Big or growing banks could borrow more via a FLP

Hawkesby said the interest rate at which banks would borrow at via the FLP would be “around the OCR”, so it could move around accordingly.

Asked whether limits would be put on how much banks could borrow via the scheme, Hawkesby responded: “What you’ve seen internationally is the limits being related to the size of the bank and their balance sheet to start with, and/or the growth of their bank balance sheet. That might be one way you provide an incentive that more funding is available if they’re expanding their balance sheet. That’s one approach or one dimension.

“The other dimension is, do they have eligible collateral to provide?”

Hawkesby said the RBNZ was still deciding how long the FLP would be available for and what terms that funding would be provided at.

Asked how the FLP would eventually be wound down, he said: “Having a longer window means there would be more staggering of its use. [Banks] wouldn’t feel compelled to draw it down immediately. Having more various terms - that sort of staggers the other end.”

Hawkesby wouldn’t comment on the quantum of the programme, but said: “The punchline is, it will be a substantial size.”

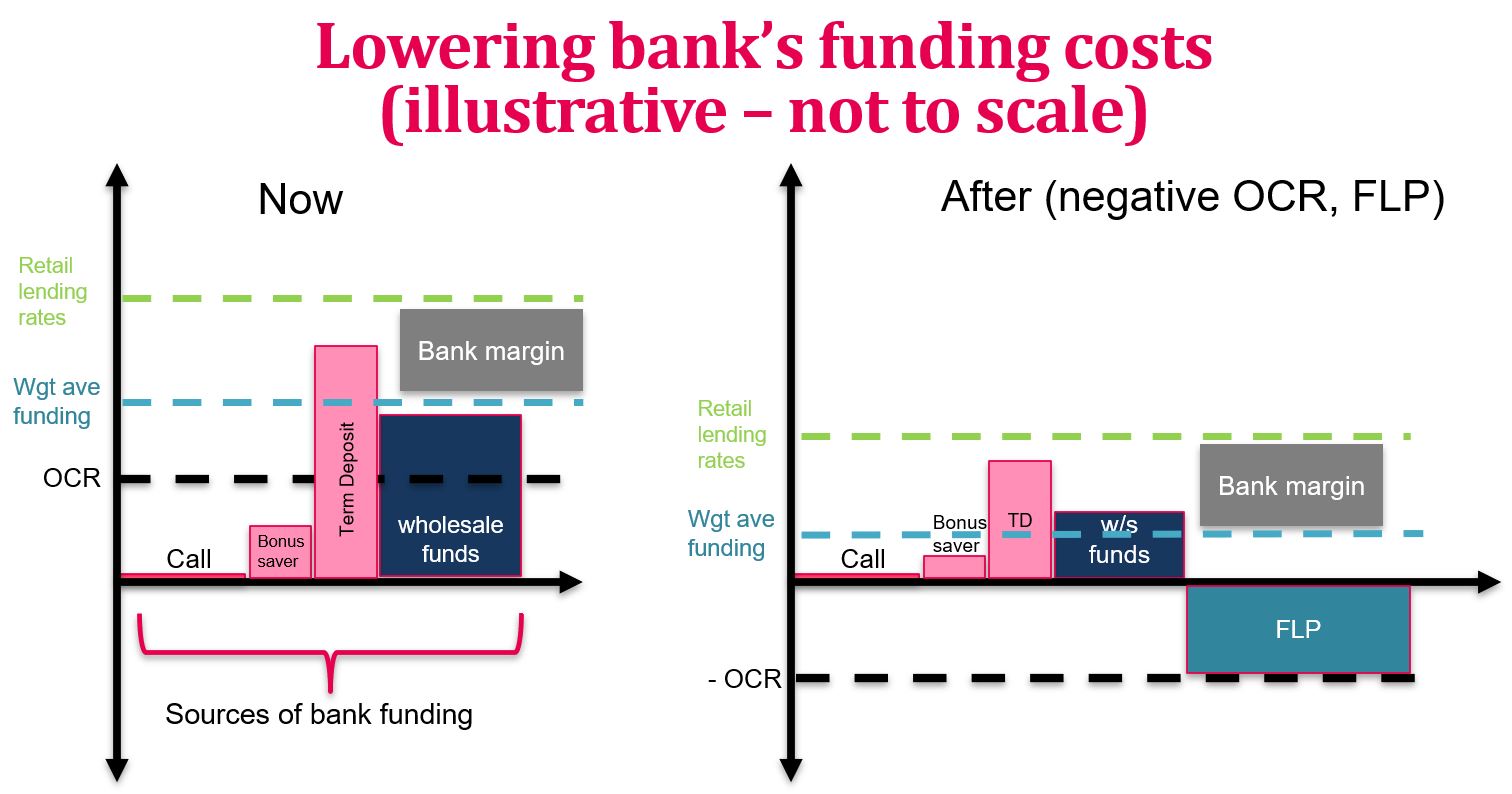

The RBNZ used this stylised graph to illustrate how the FLP would work, should the MPC decide to implement it and also lower the OCR.

105 Comments

These guys really don't know what they are doing, do they?!

If they did, why are we at this stage?

What has happened to all the other initiatives that they've trotted out to 'save' the economy? Is this it? Is this as good as they all add up to?

How many of these guys have worked in the outside world? Had to run a business and be successful at it or else they got the chop or went bankrupt?Any of them? How many time do they have to get it wrong before they get 'promoted' to a less harmful project - like running the RBNZ Stationery Department? Perhaps the art of being Stationary will be the necessary prerequisite!

I repeat - they don't know what they are doing.

They know exactly what they are doing. They have had a single-minded focus on one thing for more than a decade - more credit, more lending, more debt. They're doing a great job of it, too.

Agreed. Enslavement of productive activity via debt on assets. Just let the reset happen already.

Wait BW.

Reserve bank and government are hell bent on supporting and promoting housing bonanza that a time willcome when will door knock to give loan and may be give interest to use loan :).

Quite a few I know who are using tbeir existing equity to buy another house using interest only option. Taking more debt assuming that house price will keep on moving up and can sell anytime for a BIG profit.

The more they provide money and stimulus and the bigger it gets, bigger will be the damage if for any reason all this experiment fails. May be than the government will have no choice but to wave of the loan to avoid bloodbath.

[ personal abuse removed. Not necessary here. Ed ]

They and the rest of us have NO IDEA what would happen if they did none of the above. However, IF lending money at zero or negative rates was a good idea they would have started a few centuries ago.

All the theoretical modelling is BS.

"Making a speech on economics is a lot like pissing down your leg. It seems hot to you, but it never does to anyone else". Lyndon B. Johnson Quote sums it up best.

You've exactly described the current lot in government

Savers need to revolt. Mass withdrawals at one targeted bank each week for a month for as many customers who have cash that can be coordinated.

They don't want to give you any form of deposit guarantee and want to save the debt fueled and deflate the value of anyone who has saved cash and been conservative and pay you zero.

With social media it just may be possible to organize.

Even 10% of customers at a bank will get there attention. Might bring Orr and Robertson to actually speak to deposit holders and not only talk about this life saving of the debt fueled.

Funny, we are in a similar dilemma, buy another house, 2 bedroom brick and tile (no mortgage, minimal risk except tenants), or take term deposits and go to Gov bonds. I'm happy to loose a bit with bonds but don't like the feeling of being screwed over by retail.And there is a healthy spread of local/global ETFs to balance out.

The message is clear from the Orracle. If you have savings you're a sucker, if you haven't got debt you're a dick, if you haven't bought property you're a proper plonker.

If you have savings you're a sucker, if you haven't got debt you're a dick

I know what you're saying, but I disagree. Fiat currency is still necessary at the moment. No point sitting in your debt-laden hovel if you have no money to buy even pot noodles.

I agree, I'm just venting my frustration at the one eyed myopic monster. There should be protests on the streets by the have-nots, because effectively the RBNZ is giving wealth to asset owners and making the have-nots pay for it. The worst thing is the Orracle's answer to this... "Well, there's more people with assets (debt) then without, so it's okay".

You elaborated that well

To set the record straight I, like many others have commented here find it deplorable the current government ran on sorting out housing only to let prices rise about another 30%.

I don't think this is a good thing for the country. It might make asset holders feel good. And right now it's pretty obvious there's fewer and fewer options for savers to get decent returns other than the housing ponzi - thereby exacerbating things. So no, I don't think it's a great situation right now where the country's going but I also cannot believe that the economic situation is not being discussed as an everyday topic and election issue which affects us all particularly a lot of the red voters who seem to be getting shafted. I'm not a red supporter and I'm not blue either, I think they're all pretty hopeless right now to be honest. But to clear things up, my estimation of what's happening doesn't necessarily believe I agree with what's happening. Not at all.

That's why I enjoy interest.co to hear other points of view, reporting of the facts or non-fact whatever the case may be.

.

The things is most of the have not sheeple in NZ did not realise that the inflation figure are being hidden behind the Land & RE, which is not part of the CPI equation - which means? - once those have not sheeple have a will to move beyond the current situations? - then they must demand more extreme/comparable pay rise, band together as mini unions to lift it up the price of petrol, local bread production, local meat, fisheries, milk for start - then those other professionals, banded to strike, demand immediate pay hike to compensate the actual living cost. NZ you won't achieve anything if you not banded together and pricing up more, that's how you carve it a real inflation in absence of govt. & RBNZ one sided/preferable interventions, off course they can hide those hiking price up away too, but then by that time - you know what to do. - Now, just image if every local effort independently hike their prices? - start from grocery, then to services, etc. - Just a thought.

Yes, at least that's my interpretation of the current situation based on the actions that seem to be occurring. So not really my message per se but yes it does seem debt is the new savings and savings is for suckers. I stand to be corrected anytime though, hence why I enjoy interest.co

Yes, but thing is, you have to dig deeper. Adrian Orr is doing his job, stimulating the lack laster economy. If things get out of whack, ie FMB struggling, then it becomes fiscal policy. Eg Australian government introducing FHB grants, NZ probably will soon follow. Or if rents rise, you get fiscal spending via rent subsidies. It's a complicated beast, but basically the objective of the game is to get vital capital blood into the sick patient.

I strongly believe, Orr & team also the current govt. - really have hidden agenda to stall the RE prices, every of their moves can be seen as to prop those asset movement up, for logical reasons if you want to see the result of peak movement? what do you do? .. keep on pushing it, further & further then you can see the effect. Mitigating it early, probably just try to make it a soft/glide motion - so for fast result? - push it, up, up & up. Removed LVR, Bank CAR, No TD guarantee, end of discussion about DTI. Covid is here, potential drastic result can only be achieved by pushing the imbalances furthest, so NZ? - please be kind, there's a plan that much of you don't know about are in motions right now.

This is crazy, do they really not understand that more lending is not the solution but the problem? If we need to get the economy moving we need to boost the services and retail industry, more cheap lending will just go to non-productive assets as it is already happening, which will not just not solve the problem but create a larger one down the track. Incredible.

Orr and Hawkesby give no explanation of how will they unwind the QE money printing. Once the debt fueled become even more hooked on it taking it away will be similar to trying to get a meth addict off the P pipe. I am convinced that it would be smart to get as much cash as possible out of NZ banks. Zero return with maximum risk of an OBR event.

A deposit holder does not have a sh#t show of being able to assess the risks with the NZ banks and especially now as in the world of Orr and Hawkesby and Bascard there is no need to provide extra capital for non-performing loans. Why all the BS fuss re ANZ's modelling underestimate its capital adequacy requirements a year ago?

[ Personal insults deleted. Last warning. Ed ]

Is the economy struggling at the moment? Genuine question.

Yes. And it's because the Debt we have collectively taken on, be it Public or Private has gone into the wrong areas of 'investment'.

Ask yourself "Where would New Zealand be today if it had to stand on its own two productive feet and not rely on ever more immigration and debt." The answer? Well, struggling to use your word.

"Where would New Zealand be today if it had to stand on its own two productive feet and not rely on ever more immigration and debt."

Probably in a much better position than we're in now.

(Doesn't read well does it?! My point is, that we couldn't stand on our own two feet, today, without the crutches of support I mentioned.)

Are you talking about the real economy or the false economy?

Or the black/cash/underground economy? Could be like Italy's - 20% of uncounted GDP....

I'm just failing to see horrendous data tbh. I expect it is coming but I don't see it yet. The Q/Q GDP collapse isnt really worth looking at in isolation.

"Is the economy struggling at the moment? Genuine question"

Great question Uncle Bulgaria, apart from the generally preconceived idea that times must be terrible because of lockdowns and closed borders, the real answer is "no, not really".

This sarcasm?

I don't think he's being sarcastic. In 2012, the unemployment rate was almost 7%. Perhaps matching true rate right about now. Inflation a bit higher than now. Did the RBNZ start chucking free money at banks then? My genuine question, slightly expanded, stands - is the economy that bad or is this a massive overreaction?

The economy is on life support...but COVID a great excuse for central banks to over do the money printing as the economies were already very fragile. Doing everything they can to avoid deflation. Including containing to throw future generations under the buss to protect asset prices. Moral hazard everywhere in my opinion.

No sarcasm at all, my companies have recovered really well from lock down, most of my friends are doing well, I see restaurants, cafés, malls full. Have you experienced difficulties with your job I.O?

I’ll leave you to see the world through the rose coloured glasses. Guess everyone should just return their COVID allowances and we remove all mortgage deferrals (you know those extreme measures put in place to prevent complete economic crash) given how strong the economy is (oh I’m being sarcastic).

I dont think that's fair. There is no big denial of obvious pain in certain sectors but it doesnt feel like a dead economy to me and yet the kitchen sink is out. ANZ biz survey today shows a net positive result. 'Stunning rebound' says Sharon Zoellner. Primary producers are flying. Construction back to normal.Tourism actually half decent over last few weeks. I must be in a big fat bubble because I know one person who has lost their job. I'm just keen to have some evidence of the actual apocalypse that RBNZ is addressing.

You're absolutely right U B, note that I O has provided no valid argument to support his view that the economy is in the doldrums apart from cynical sarcasm

Probably need to address UB last wordings... that indeed RBNZ forecasting as such, is that a fake news Yvil? - don't address the novice here. Those so called experts? you may need to tabulate their wordings from earlier this year, also those 'Bank economist' - Now, imagine if you're passenger on one of those ill fated 737max - on the ups & down flight nose, you have internal knowledge of Boeing, FAA then now this up/down - the Captain sounding try to assert calm, put your seat belt, turbulence, experience difficulty.. then followed by silence. But, hey you're welcome to argue there and then.

That’s nonsense Yvil and we both know it. Why the need for such extreme stimulus responses to prevent it all from falling apart? It may appear healthy at the surface but why then the need for such extreme monetary and fiscal responses? Without those input in the current market who knows what state we’d be in. Happy trolling someone else.

That's precisely the point. Wage subsidies and loan deferrals were indeed needed when we locked the country down at level 4. Now though, it is very questionable if the country indeed needs the massive RBNZ stimulus as, in my opinion, the economy (including lockdowns, wage subsidies & mortgage deferrals) in doing pretty well. That's why many are questioning the RBNZ's moves to further lower interest rates

This Yvil? Ok let’s just remove all the QE, wage subsidies and mortgage deferrals then and see where the economy is at. But yes everything is dandy because of those extreme measures.

That's messed up thinking, the economy is what it is now, including all the negative effects of lockdowns and the positive effects of stimulus. You, trying to remove the stimulus to talk about the real economy is like me removing the lockdowns to say that's the real economy, it's just plain wrong thinking. The economy is what it is right now including CV, lockdowns and all forms of stimuli. As such I think the economy is not doing that badly at all

Yes and the person in ICU on life support is doing rather well also. Full of life and vitality.

$100B QE = 55K for EVERY working person in NZ. Looking at it that way can you now see why it doesn't feel like a dead economy?

Does it mean that RBNZ is forcasting more trouble time ahead for drastic measufe and many thought that NZ is on the way to V shape recovery.

The more they try and expand the bubble, more trouble even if it corrects slightly as will create panic leading to crash.

Let economy now run by itself with little damage and come out of fear of correction. Like Life cycle economy cycle has to run jts own course. Just like money cannit help to run away from life cycle so does cannot run away from economy cycle.

Will RBNZ govetnor be held accountable if economy crash by his action in future ?

Will RBNZ govetnor be held accountable if economy crash by his action in future ?

Nope. Accountability will probably be directed towards you and me. Not borrowing enough to take on greater risk for the good of the whole.

Oh C'mon man ! Stop winging it. Let the ponzi fail. It's getting ludicrous now. [ personal abuse deleted. Not necessary. Ed ]

Sooner or later, people, and the banks have got to take their medicine. I'm a property guy, and I think it's bloody madness. I don't like what's happening to a lot of people I know.

Bottom line is that whether you agree or disagree with RBNZ action the reality is that mortgage interest rates are going to be lower.

For the home owner with mortgage clearly it is worthwhile to currently fix short term as next year the signals are its going to be a whole lot better.

For a potential FHB, the above applies and in the interim the reality - whatever the sentiments on this site regarding housing and RBNZ actions - is that those reduced rates are going to stimulate house prices in the short term. However, as I have often posted, I would be prudent and pay down the mortgage and as one is in homeownership for the long term, short term fluctuations are irrelevant provided one can service the mortgage.

Like it or not - that is seemingly the reality.

Note that while there are lots of those on this site who see themselves as all knowing calling Ponzi scheme and bubble burst, well I would put greater weight on Treasury who see a 5% fall - and that fall may be from levels than currently and is in the range of buying well and buying poorly.

A forecast is just a forecast. Many institutions and several forecast were taken completely aback and demonstrated completely wrong by the occurrence of the GFC and the associated collapse of house prices in several countries.

If we look at the fundamentals, housing prices in NZ do look in a very dangerous territory, and compare quite badly in international terms (https://www.imf.org/external/research/housing/).

Extreme intervention by the RBNZ and unsustainable (in the longer term) extreme loosening of monetary conditions have muddled the waters and temporarily perverted the normal functioning of the market, but I am wondering how long this is going to continue for.....

I am not predicting catastrophic falls, but I would not be so cocky about the future movements and risks (quite substantial, considering the fundamentals) either.

fortunr

"A forecast is just a forecast" - agreed it is a forecast not a certainty.

However, I am prepared to take on board what MetService forecast and depending on their forecast either take the sunblock or raincoat but knowing that it is not a certainty.

I also agree with you and I am concerned about the sustainability of house price rises beyond the short term (e.g. a year). For that reason, as I mention I would be prudent.

I don't see RBNZ being inept - their current action is about economic stability and I don't believe that they are of the view is to then allow the housing market to crash resulting economic instability. For that reason I see some rises in the short term, followed by a flattish market - possibly for considerable time - due to disjoint between incomes and house prices.

P8.. agree price rises may well continue for a year or even longer but would question long range MetService forecasts if Met had financial interests in sunblock companies and were predicting record sunshine for years to come.

I agree. Unfortunately.

Mortgage rates will start with a 1 by May, it's going to stimulate the market more.

I don't agree with the approach - but that's the reality.

Fully agreed, the only things that RBNZ must do now is to execute FLP quickly, then extend the offer of OZ banks deferral further to minimum 12 months more, the next Lab govt. will stop the wage subsidy but will re-name it to Covid grants income supplements. BUT the most important here? that after the March negative interest to at least being implemented at -10%? Orr & the teams must quickly expand the QE into shock & awe movement tripling/quadrupling it into 300-500billions - This way it will surely, negate any bad sentiments/market confidence.

I dont mind interest rate goes lower. Actually we will be more than happy to welcome it if it's forever low. But can it be? When is it going to go up? By how much percent? By doing more stimulation, when can we get the economy back on track? When we get there, how much percent interest rate is going to increase? If interest rate increases, what are the policies from government to keep housing price from crashing?

These questions need to be answered by our government and RBNZ. But of course, they won't tell you the truth. Because if they do, no one gonna continue to play this ponzi scheme. After four years, they are all retired or off duty. There will be other people to be blamed.

If I may have a go at answering your question, I would say interest rates won't go up with any significance (read 2% or more) because, quite simply, too many mortgagors will start defaulting on their loans. You may reply "too bad for them" but reality is that NZ house borrowing is so huge that we cannot afford mass mortgage defaults because it would plunge the country into a real, deep recession/depression that will make our current situation look like a walk in the park. No government or central bank will want a deep recession/depression to happen under their watch. I'm not putting a judgment call on it, saying it's right or wrong, but that's what it is going to be, interest rates won't be going up.

So are you saying inflation rate will never go up to more than 2% and we are going to stay within recession forever like Japan? Because this is the only way to stop interest rate going up. RBNZ was very clear about this, they adjust OCR by looking at inflation rate. Both depression and inflation are the worst nightmares for New Zealand's economy. If we don't create healthy productivity, we might get stagflation which is even worse.

CoH, you're right the historical thinking is that when inflation goes up, interest rates go up. I put it out there that if we get inflation, a big "IF", the Reserve Bank won't be raise the OCR significantly because it will know that too many mortgagors will default on their loans, thus leading to a catastrophic recession/depression. Throw out the conventional economy books, interest rates won't rise because they can't as it will precipitate the country into an abyss no policy maker will want to be responsible for.

And what about the burgeoning poor and shrinking middle class? I guess we just let them eat cake.

Can anyone explain to me why we bother with retail banks now? It would appear they are simply a drag on the ability of the central bank to get credit to businesses/households. And given central banks now carry retail banks risk, why reward them with any private profits? Makes no sense (to me any longer...) If their risk is zero, which is what RBNZ has just come out and made obvious for everyone (i.e. we save you no matter what happens) they don't deserve any reward...

Exactly. They now have a profit margin guaranteed by the RB, while also having risk taken care of by the RB.

At which point their existence is not justified, except perhaps by their expertise and infrastructure for delivering retail banking services -- which would not be that hard to replicate in the digital age.

Well you're right, in the near future I believe there will be no savings in banks, everyone will have debt, tax's will be a thing of the past and the interest you pay will be determined by your income. Interest and debt repayment goes to the Government. Banks will simply be terminals for debt distribution. Of course physical money is long gone by this stage.

I thought banks were supposed to be a safe place to store ones savings while not losing buying power due to inflation. But if we now can't earn enough interest on savings, where do people put their money, that is also safe and not are risk of the balance decreasing? At the moment bank deposits in NZ aren't even guaranteed, unlike most other countries in the OECD including Oz. So for the tiny amount of interest one makes. eg Does the risk vs reward now make it worth it, since they keep dropping their rates?

Is there any way to stop this from just going into residential property, which will grow the economy and jobs precisely not at all?

Have they changed the rules which force banks to hold property as preferential collateral when evaluating the safety of their reserves?

Apparently in other countries, they have set it up so it is focused on certain things. Why can't we do that, or is it intended to help keep the property bubble inflated as a form of 'collateral damage'?

I just wish they would show their projections of where they see things heading. eg What is the average house price projected to be in 5 years, in 10 years etc, as a result of this sort of thing?

I also wouldn't be surprised if 90% of NZs don't know anything about this or the QE's occurring, they just see it as boring money stuff. When it is infact incredibly important stuff that is going on. It doesn't even seem to be much of an election issue. The minor tax cuts are nothing compared to this sort of thing.

IMO it is like watching a slow car crash. It is so frustrating.

Brisket

"Is there any way to stop this from just going into residential property . . "

RBNZ has stated that is its specific intention in that it will be going into both housing and businesses.

The rationale for it going into housing is that it will produce lower interest rates, stimulate the housing market, encourage greater spending by home owners, and so stimulate the economy.

Like it or not . . . that is the reality.

Well they've failed with this homeowner, I certainly wont be spending more, quite the opposite, i'll be squirrelling away as much as I can, just a question of where. A small amount of PMs, some equities, and some cash.

And it will have that effect. But the answer no one knows is how much effect? In my opinion, not much.

I mean, my partner is already licking her lips getting a new car with the low interest rates and the extra $100 pw we will have when our mortgage rate is 2%...but if that happens here and there it might have *some* economy supporting effect but is unlikely to bolster inflation much.

They don't care what the banks do with the money as long as it reduces rates. As far as they see it, cheaper money protects jobs and there's no point complicating matters. If they try to restrict it to biz lending only, banks won't take the cash. See themselves as strictly number two to govt in effect on econ. 3-4% unemployment rate and 2% inflation are ALL that counts. Currently believe unemployment is 6 -7%. Source: a guy who was at meeting today.

More pumping of the housin ponzi, wow!!!!

IMO it is just kicking the can down the road. It has to be solved at some stage. but maybe massive inflation will solve it for them?.

Can we assume from the diagram the RBNZ (government) is in effect lending banks funding which incurs a negative OCR cost to presumably offset the banks paying negative OCR on their QE derived settlement cash assets? Nonetheless, the government is proposing to raise it's liabilities.

Thus:

The more only the government can borrow, the more only the government does borrow. And the more the government does borrow, the harder it is to get the economy growing (sorry, Krugman). The more difficult it is for meaningful growth, the more banks will only lend to the government. Link

I'm struggling to see problem RBNZ wants to solve by this. Banks awash with free cash already, evident by figures and impact (paying virtually 0% to savers). In past recessions lower rates helped boost consumption, so first response (QE & lower rates) fair enough, but if evidence now shows that lower rates when rates already low not have that effect, instead businesses tightening capital spend & hiring, and h/holds saving & paying down debt likewise, with lower rates not boosting consumption, and main effect blowing sharemkt & housing bubbles to extreme levels, doing more of the same rather than pivoting to a new strategy seems odd. Unless want to blow bubble bigger, expand wealth inequality, have an existential crash later that ruins more lives rather than limited correction now that people already braced for (paying down debt, etc). Hard to fathom. Guess I'm missing something...

Banks only wish to lend to those with pristine or near pristine collateral and guaranteed incomes, which means the already wealthy. Government funding bank deposits helps offset bank QE costs associated with a negative OCR regime, but does not reduce the issues banks have with higher risk debtors' ability to liquidate loans, unless the government takes the losses for this type of lending.

Seems some US policymakers see dangers of groupthink fixation on old strategies in a different environment:

"Fed's Kaplan rejects adding to QE, eyes eventual taper," 9 October 2020

https://www.reuters.com/article/usa-fed-kaplan/update-1-feds-kaplan-rej…

Why is the RBNZ so hellbent on lowering interest rates? Lower interest rates are not needed now.

To stimulate inflation. That's their raison d'etre

Hasn't worked in Japan or Europe, what makes Orr so confident or should I say indifferent to glaring evidence, except possibly deeply held ingrained beliefs?

Orr has either been groomed or indoctrinated. It's really the only way to get to the position he's in.

We might be able to hold off the pain for another 2-3 years...

Fritz, in today's economy, lower interest rates do not stimulate inflation

Well, that remains to be seen. They clearly think it can.

Perhaps more in an attempt to keep us out of the hands of that nasty deflation

That's not how it works, more debt is not more money in the economy but just the other way around, more income spent in servicing loans means less consumption which leads to deflation.

[ ranting abuse is just not needed. Debate the issues raised. There is no place here for making it personal in that way. Ed ]

Internationally these schemes are limited by DTIs and other macroprudential mechanisms to prevent catastrophically reckless lending.

.. the most important macroeconomic variable cannot be the price of money. Instead, it is its quantity. Is the quantity of money rationed by the demand or supply side? Asked differently, what is larger – the demand for money or its supply? Since money – and this includes bank money – is so useful, there is always some demand for it by someone. As a result, the short side is always the supply of money and credit. Banks ration credit even at the best of times in order to ensure that borrowers with sensible investment projects stay among the loan applicants – if rates are raised to equilibrate demand and supply, the resulting interest rate would be so high that only speculative projects would remain and banks’ loan portfolios would be too risky. Link

This is why interest rates keep falling - nothing to do with central banks - banks are failing to find borrowers capable of securing adequate collateral and income to meet their lending standards, hence they push interest rates down hoping to entice the already wealthy to borrow against their better judgement. Other than that funding government debt will suffice.

Woods is little more than a parrot.....of nothingness. It all sounds like she's saying something meaningful. If you pay close attention, you can see that there's nothing there. [ Borderline. Please make sure you discuss issues without personal insults. Just because someone else doesn't have your opinion doesn't make you right and them wrong. Stick to the issues raised. Never insult. Last warning. Ed ]

It's not an insult. Nothing more than an opposition politician might say or what a media commentator might say. I will explain. Politicians who claim to be a kind of fairy godmother by maintaining house prices (Woods doesn't dictate markets) while providing affordable housing to FHBs is promising the moon.

I'm sorry but I think that if you're in a position of political power, then you should expect public criticism. Nothing I have said is vindictive or nasty towards her character.

I apologise for questioning the kindness and/or intelligence of our perfectly perfect prime minster or for observing that her henchmen are busy destroying the lives of our friends and families.

I shall immediately report to the re-education camp. Lets keep [house prices] moving! Be kind!

This is awesome! I really hope this is set up by Xmas. As soon as it's there I'm going to my bank to ask for a loan at 0% to cover my rent for the next year.

Why did it take them so long to do something to help us battlers?

Was checking newshub news and RBNZ has made it clear that they want to see house price going up and will do everything to ensure that house price keeps moving up as only solution that they have to fight panademic and to boost economy. Economy = Housing Sector.

On this website so many comments against RBNZ and Government as wants house price to fall and hoping that it may in future, once stimulus and mortage holiday ends BUT face the reality as one cannot fight the reserve bank and government so either jump and buy in your budget that is pay million for a pigeon hole with life time of debt in Auckland or move out as no one is in for FHB as expecting house price to go up by 20% to 50% in a year.

50% Crikey. Who said that?

No wonder RBNZ is running the way it is, finding reason to support housing ponzi as chief economist advisor seems to represent his community.

https://www.newshub.co.nz/home/money/2020/10/reserve-bank-says-house-pr…

Jacinda Rden says that do not want house price to go up and RBNZ wants house price to go up.

What is happening. Media should ask JA for her response on the same.

Well the RBNZ are supposed to be independent, so if they have a different opinion than the PM then that is acceptable.

Suppose to be independent.....

You are correct, now one understand that RBNZ is nit out to protect and support average Kiwi but Chinesse as they are the main beneficery of housing rising price / speculation and this is not a racist but fact.

Officials say house prices falling would be the "worst-case scenario" for our economy while it recovers from a recession.

Reserve Bank (RBNZ) chief economist Yuong Ha referred to house prices falling as a "deterioration of wealth", which could not be afforded during the COVID-19 economic recovery.

He must be joking - how could anyone consider shelter a major pillar unpinning the basis of wealth for a so called developed market economy?

I have never read anything more sickening in my life.

Lots of ranting on here, which is all well and good and is focused on exactly the right things (which I and many others have been screaming about for a decade or two both here and other places).

However the polls show most of you have already or are going to go out and vote to keep everything the same by voting for one of the two large parties or their cronies (ACT/Greens). If everyone actually believed what they are saying on here, they wouldn't keep voting for it.

Robertson and Orr have already said they do not care about asset price appreciation and will let it appreciate to infinity, no matter the cost to the economy, our productivity etc. Same from National, ACT would open the floodgates even more.

Hi Blobbles, you are correct. It is a pity many FHB who are working hard to buy first home and if price keeps on going up by 10% or 20% literally on a monthly or quarterly basis is frustrating for them, as house price were already high and now with RBNZ policies to push further, FHB may even have to give up on dream of having a house - it is sad and NZ has no leader just politicans and the same apply to JA.

Feel really bad for FHB and can understand how RBNZ and even government are so openly adding salt to their wound and FHB have no option so ranting.

Maybe FHB should take to street and need more for their voice to be heard - that time is not too far away.

As soon as a FHB buys, their opinion changes dramatically. They switch from wanting house prices to fall to wanting them to rise.

Ensure that you have a quick liquidity, and comparable/more pay being offered in OZ for your skills - then move on. If you're mostly a good experienced member of police force, engineer, technician, teacher, healthcare staff and other professionals. Really, it's not worth it to stay here - across the ditch? you'll see the difference for sure.

Admittedly, not sure if this is the correct place to ask.(I apologize in advance if this is not)

Are there any political parties this election who have indicated they will be looking at the Reserve Bank Act and the RBNZ and whether their current mandate and policies are still pertinent in the current environment? I feel I have had a good dive into the policies of each party, but none appear to have substantially touched on the Reserve Bank act nor the RBNZ's role.

I will admit, I'm a bit confused that after almost 10 years of this, Central banks appear to be continuing with more of the same of lowering interest rates and seemingly expecting something to change when I feel clearly it isn't.

There is a bit to unwrap here, but always good to start at the base assumptions.

First the mandate of the destruction of 2% of purchasing power every year as a goal, the 2-3% price inflation target. Some of the best periods for citizens of a country are where you have wage inflation and price deflation, you get rewarded for real responsibility and life becomes easier every year, employment also is maximized.

Why always lower CB interest rates, hopefully not based on the assumption that inflation is only a monetary phenomenon. If you don't have inflation, monetary policy must be too tight, so you have to loosen it - and you do that for a bit, and no inflation so you do it some more. Then you run out of the Central Banks pricing of the cost of money (always cheaper than market) - and you have to reduce macroprudential. But what are you chasing? What if things were structurally deflationary - which you can get from non-monetary sources historically (industrial revolution, or post feudalism, maybe computers and robots, and some CB moves will never get inflation if you end up with debt saturation) and you are chasing 'inflation' down the rabbit hole.

Where does it end up, there are some scary places...

Loss of trust in the central bank? Due to silly stories that make no sense.

Reduced trust in money? If you cant get some small return for your unsecured loans to a banking institution or a fair wage that tracks necessary asset prices.

Juiced speculative asset price returns? Draining everything from productive assets.

Extreme and amplified (positive feedback loop) social inequality? Due to speculative asset returns.

All of these things have been seen before, extreme social inequality never ends well, the cost generally being the loss of civilization.

FLP is similar to the Aussie TFF? Central bankers - always another three or four letter acronym to hide the real meaning in a sound bite. Who benefits?

Given the possible outcomes for citizens, who is actually running the country, the central and 'private' banks - or the government? We need new thinking.

Agree but unfortunately most don’t understand it nor care to try and understand it. Currently policies if left unchecked and continue to grow in the direction they are, may destroy the society we know. History doesn’t read well when society creates oppressors and the oppressed.

I cant believe labour / left govt lets them do this. Really all this is doing is deflating the value of cash against assets. All this fake created money is just devaluing what people's salaries / cash are worth.

Hence why gold and Bitcoin are doing so well right now

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.