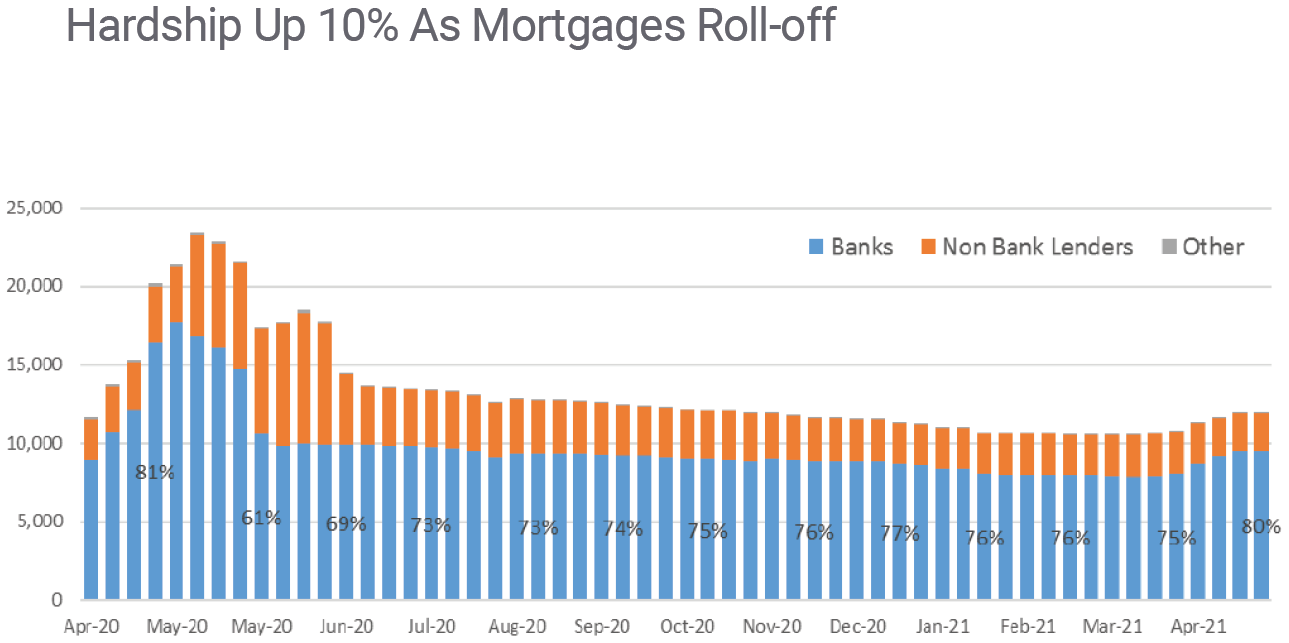

Credit bureau Centrix says there's been a big surge in the number of households in financial hardship.

In its latest monthly outlook looking at April, Centrix says the surge has followed the ending of the Reserve Bank's mortgage deferral scheme in March.

The scheme, originally intended for six months as a reaction to the Covid crisis, was extended out to 12 months. At peak about $20 billion worth of borrowing among 60,000 personal customers was on full deferral, but most of those on deferral had gone back to full payments well before the scheme ended.

Centrix managing director Keith McLaughlin says there's been a 10% increase in the number of households in hardship since the scheme ended.

There are now 11,900 mortgage accounts flagged as requiring Financial Hardship Assistance, compared with 10,800 a month earlier.

"...The ending of the Reserve Bank’s mortgage deferral scheme might result in increasing numbers forced to sell their homes, McLaughlin said.

"...While the numbers are still small, we anticipate this to increase further in the coming weeks as more households struggle to meet their mortgage payments and fall into arrears."

McLaughlin says although he knows banks are doing everything they can and working hard to support customers, "these households are going to need to make some hard decisions if they cannot take steps to meet their mortgage obligations".

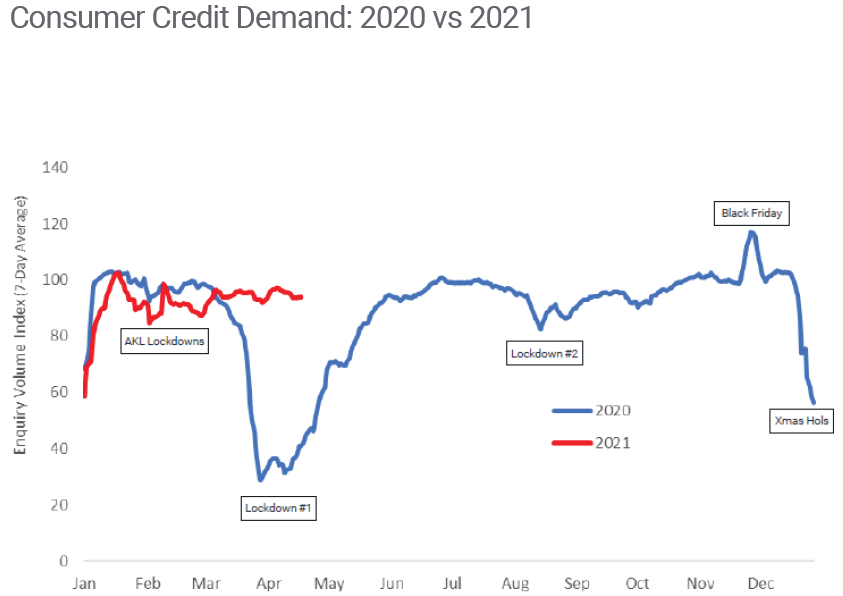

The hardship being suffered for some comes at a time when other people have be clambering into mortgages in huge numbers.

Records were shattered once again in March, according the most recent Reserve Bank figures, with $10.487 billion advanced in mortgages.

And McLaughlin says April saw mortgage applications "at 20% above our baseline".

He says that credit demand continues to remain strong "across all sectors".

"This strength speaks to the recovery that has occurred following the collapse in the credit market this time last year when the country went into Level 4 lockdown."

Overall credit demand in April was back to 94% of pre-Covid figures, McLaughlin says.

"Credit is a leading indicator of confidence. People borrow when they feel confident that they can meet future repayment obligations. The strength of the credit market shows that, despite the challenges of the past 12 months, we are seeing a return of confidence and stability."

83 Comments

'The hardship being suffered for some comes at a time when other people have be clambering into mortgages in huge numbers. Records were shattered once again in March, according the most recent Reserve Bank figures, with $10.487 billion advanced in mortgages. And McLaughlin says April saw mortgage applications "at 20% above our baseline". He says that credit demand continues to remain strong "across all sectors".'

If you are one of these people currently borrowing as much as you can get your hands on, going like the clappers with your ears pinned back, do you have any concerns at all about interest rates rising or the global economic significantly deteriorating, or is it very much a case of 'everyone else is doing it, so I am doing it too'?

If you can afford it why not? Long game you can't lose, so what if interest rates go up to 5%, 6% be a bit tight for awhile but can't lose if your playing the long game,

If interest rates go up to 5 or 6% you're assuming that wages will have increased dramatically, otherwise how are you paying for all of your other bills in addition (i.e. we have high inflation) - but ask your boss or CFO if he see's 5 or 10% wage increase p.a. over the next 10 years - while his/her company is loaded up with debt and any increase in debt servicing costs will need to be addressed first, before passing any wage increases to staff.

Well said IO

Servicing has already been tested at 5% or 6% so you already know you can afford it unless your situation has changed. It would just mean less disposable income for a while.

Good point, why do DGMers assume all borrowers are maxed out. I could handle 20% interest rate on current income without batting an eyelid.

It's a fair point, but serious inflation would be another wrinkle in the plan. What if all your other costs are going up at the same time as your repayments? Disposable income could shrink very rapidly in such a situation.

How would we get high inflation as well as a high OCR? I mean it sounds scary but what scenario are you envisaging?

We've managed to sustain low inflation and low interest rates for a long time, so why can't the inverse be true? We seem to have broken something.

The whole purpose of low interest rates is to get people investing in riskier assets.

Not necessarily:

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

So is your theory that low interest rates creation inflation? 1970's and 1980's had high inflation and high interest rates or has that period been deleted from all memory?

"It's the 1970s, and the stock market is a mess. It has lost nearly 50% over a 20-month period, and for close to a decade few people want anything to do with stocks. Economic growth is weak, which results in rising unemployment that eventually reaches double-digits.

The easy-money policies of the American central bank—designed to generate full employment by the early 1970s—also resulted in high inflation. The central bank (once under different leadership) would later reverse its policies, raising interest rates to some 20%—a number once considered usurious. For interest-sensitive industries, such as housing and cars, rising interest rates cause a calamity. With interest rates skyrocketing, many people are priced out of new cars and homes"

"The great inflation was blamed on oil prices, currency speculators, greedy businessmen, and avaricious union leaders. However, it is clear that monetary policies, which financed massive budget deficits and were supported by political leaders, were the cause."

Any of this sound familiar?

https://www.investopedia.com/articles/economics/09/1970s-great-inflatio…

Yep, the oil crisis of 1973 and 1979 energy crisis resulted in high inflation and recessions in the 1970s and 1980s. Are you picking a repeat of these in 2021?

Inflation means your debt shrinks, not the value of the asset.

"why do DGMers assume all borrowers are maxed out I could handle 20% interest rate on current income..."

They dont. Its not relevant

Like everyone else, I assume you need an income?

And your income relies on the whole Ponzi holding

I dont think all are maxed out, but you read the insane questions in some forums like - the banks wont lend me the money, so which second tier lender should I go to first - there is a prevalent "you cant lose on this" attitude by the lesser read/educated/other of us.

I really struggle to believe this. With 6% being double current rates , pushing payments from 30% ( last affordability from int.co iirc) household income to 50%+ (allowing for principal not doubling) seems a bit fanciful.

It would also mean banks would need to start stress testing customers at 10% for lending....

Think about it

Is that why the Fed has been buying junk bonds (i.e. to save insolvent companies with debt that nobody else will buy?)

Someone who’s never applied for a mortgage wouldn’t know that.

Agreed. A 2% interest rate increase in a $600k mortgage @ 30 years is $150 per week. Or 10% increase on a $100k salary.

agreed, but the long term average interest rate in New Zealand is 8%. If that doesn't worry you, then yes, go for it. What could go wrong ;)

Oh that’s the long term NZ interest rate is it? Exactly 8%.

Wow some people are such know it all’s .

' a market crash which will never happen.'

The apple never falls far from the tree eh!

LOL this is so true.

The majority were saying that a housing crash was impossible - in 2008. The funny thing is that some of the most vocal in their groundless optimism were Irish and American housing specuvestors.

But hey maybe NZ is immune to the laws of economics.

But that's what the RBNZ and government want isn't it? Debt expansion? I.e. house prices to keep rising because that is what voters want and it generates 'wealth effect'.

Government and RBNZ is responsible for creating FOMO like never seen before and now only God knows where all this will lead to.

RBNZ can delay but cannot avoid and as Mr Orr has another two years to go, may be, he will be happy if he can sustain the ponzi till his term end by not acting just like politivians who think till next elections.

Given the numbers, less hesitation because there is now so many in so much debt that rising interest rates seem unlikely to be allowed to happen. Collectively it's now too big to fail - we already got a taste of that in the first lockdown when the government was quick to support property owners with mortgages.

C65 and C66 discontinued.7 April 2021

The bank customer lending collection was introduced as a temporary data collection in late March 2020. Its purpose was to monitor the impact of COVID-19 on the banking sector.We wish to advise that the weekly survey which collects data for the C65 and C66 tables is now being discontinued.The final publication of the C65 and C66 tables will be on 13 April 2021. This publication will include data for the week ended 2 April 2021.

TMI for you mere mortals. What happens now is for our eyes only.

Adrian, Grant, where did you leave the sticky tape again? By the financial sector? What's it doing there? What do you mean you dunno?

Negative interest rates here we come. The ponzi is too big to fail. The clowns will do all they can to keep their s##t show mess going as long as they can.

As much as I would like to think interest rates will rise...they won’t. Look at US debt levels to see why.

Then we are going to face a serious inflation problem. The Inflation would increase everyone's cost living, especially the home owners. It's lose lose situation. The better solution is slowly increasing the interest rate. Housing market would take a hit for short term, for long run, it benefits everyone.

The point is so much debt has been taken on that the global economy will crash like never before the moment they put rates up. The problem now being that inflation cannot be tackled via interest rate hikes - simply because the world would default.

Why does msm not ask mr Orr this question I can only wonder. Fear perhaps.

Absolute shambles created by the central banks who would not let rates rise years ago and thus clean out all of the non performing businesses and overlerveraged speculators. Thus we all pay for their madness.

Now the Fed and co. just buy the junk bonds of those non-performing businesses resulting in a bunch of otherwise insolvent firms to keep operating in this bizarre economic system.

Watch for some serious intervention for Grant to target his most hated groups in society (Cullens 'rich pricks', landlords, and now you can add everyone over $60k in salary), to try and prevent inflation being caused by the policies and monetary conditions they have enacted. They won't be able to move interest rates as that would slow the economy from our existing recession level, making economic conditions even worse.

Watch for holding interest rates, continued borrowing, further interventions and redistribution, unintended consequences and lots of PR bluster, while ultimately the interventions fail.

You can’t fight the FED. Give it up.

I think roughly 90 % of people are reasonable with their money… 10% are not… so the 10% in hardship is not that surprising to me

I think 90% of people treat debt as income, and are going for the best lifestyle they can borrow.

These are nearly 12 thousand mortgage holders. At some stage in the past they were credit worthy enough to get a mortgage. So probably not complete financial basket cases. The mortgage is the 1st thing you pay. Not the last. How much do they also owe on tax,rates,utilities,insurance,hp,credit cards afterpay etc. A few hundred "Bank Recommended"sales a month at the same time that credit availability is tightening could have a fast acting effect on prices.

I certainly hope not Tom, that would be terrible

do you mean people or governments??

I think roughly 90 % of people are reasonable with their money… 10% are not

I suppose 90% is an overestimation, especially when broader metrics and surveys on domestic borrowing and spending across the country suggest Kiwis lack financial literacy (euphemism for inept, clueless and deluded as the Commission of Financial Capability puts it).

Our unaffordable housing market has locked out many from getting up the property ladder, including those bad with personal finances and get a mortgage due to insufficient savings, poor credit history, lack of solvency, etc.

https://www.stuff.co.nz/business/money/122542786/kiwis-are-clueless-car…

"Kiwis lack financial literacy"

I have 2 friends approaching retirement with all their retirement savings heavily geared and tied up in NZ residential property.

So everything invested in a subset of a single asset class (Property), in a single region (North Island), in a single currency (NZ$). Clearly, like many other Kiwi "investors", they wagged the "diversification" class. TTID?

That's right - our masses aren't too fussed about financial literacy when buying a dump anywhere in the country is likely to yield a decent income and strong capital gains in the short run.

Higher education, innovation and gainful long-term employment aren't priorities in NZ because the fortunes of the rich are tied up in commodity trade and asset speculation, and the ambition of the masses are limited to buying a house.

Well Tom, your 2 friends have done exceptionally well wagging the "diversification" class and investing in residential NZ property for the last 10, 20 or 30 years

Surely that relies on the amount of debt. If you have endlessly stacked debt trying to avoid income tax, that will be a mountain of debt with rates this low.

??? If his 2 friends bought houses, 10, 20 & 30 years ago they did really well, period.

They may have borrowed heavily $80k to buy a $100k house 30 years ago which is now worth $800k

They may have borrowed heavily $160k to buy a $200k house 20 years ago which is now worth $800k

They may have borrowed heavily $320k to buy a $400k house 10 years ago which is now worth $800k

They have now almost $2 million in equity if the never repaid a dime or much more than $2 million if they were on P&I.

Anyway, they have done really well putting all their eggs investing in NZ houses

Yvil, only you wrote 10, 20, 30 years. What Tom wrote was, "I have 2 friends approaching retirement with all their retirement savings heavily geared and tied up in NZ residential property." So he's saying that they are *currently* heavily geared. Yes they probably have done very well for themselves but are now at risk going into retirement with a lot of debt at high LVRs.

I asked a question of a colleague that has recently levered up for a second out of town rental property, what would happen if the property market turned. "We have a bit of equity so we'd just sell rentals and be okay".

That's assuming there are buyers-a-plenty in a property market bust of course.

I'd continue to suggest if Kiwi were actually financially literate they would look at the financial system and run for the hills.

I'd continue to suggest if Kiwi were actually financially literate they would look at the financial system and run for the hills.

The 'financial system' relies on the sheeple not being financially literate.

Bitcoin, equity or houses, even Dogecoin. What isn't inflated at this time?

It's 10% of people with mortgages. Not 10% of people.

Actually, ignore that. It's a 10% increase in hardship.

Only 4 out of 20 properties (20%) sold in the second 10am session in the Highbrook auction rooms today. Is this the turning point? Anyone buying now could be regretting a large mortgage in a few weeks time as they slide into negative equity.

https://www.barfoot.co.nz/auctions-live/sessions

In the morning season 14 out of 36 were sold in both room combined - Highbrook and 1 was sold after the auction.

Though number of house sold were low but the price that houses which were successfully sold was HIGH.

Another 29 to go.

Yawn. Anyone that couldn't do the math and realise they were in the crap once their no mortgage period expired is now facing commercial reality. Will the banks let it ride or will they force sell onto the market...?

Mortgage...from old French mort gage (“death pledge”)

And if they start forcing sales what happens to the value of the equity that is backing all those promissory notes they are holding?

"...and we will all, go down, together...yes, we will all..."

Median annual income NZ $53000....the half supporting the whole ponzi earn less than this.

This is the whole idea of neo-feudalism. Fighting for the opportunities to rent to the lower income members of society.

neo feudalism is even less workable than the original feudalism.

You still cant get blood out of a stone....something aggregate debt level proponents seem to fail to realise.

https://www.stuff.co.nz/life-style/homed/renting/125089461/government-h…

Hold on...Government housing policy was suppose to shoot up the rent as was highlighted by each investor / RE lobbyist OR was it just pressure tactics / blackmail just like now been put on rbnz governor to not act on speculative demand though he need no pressure as he himself believe in ponzi to continue.

Interesting rents are flatlining. And less demand. Good on those FHB who now own their own home. My son is one of them. Ditching his shitty rental before he turned 30 was one of his goals.

Before we go counting chickens on lack of rent increases, remember that the government restricted rent rises to once per year, many landlords took increases after COVID 6 month restriction ended last October. The new rental interest write off ban starts from October (when rushed legislation gets written). I'm picking the rental increases to start in Q4 when landlords can do their yearly increase.

I ditched a house, and it's still empty 3 months later. Had I kept it, I would have lifted rent by $100-$120 per week, as I could no longer afford to rent it below market level. Instead, the tenant, a young family had to move in with other family members. They could only find worse houses for an extra $120 rent p/wk. That's an own goal by the government.

They may be in hardship now, but the new swimming pool/ford ranger / boat looks sweet as.

Market is still at cruise speed even with full flap out and a Cb on the flight path.

If you’re “one of these people” you are paying $18k a year in interest and a few thousand more in other expenses and your property has gone up more than $20k per month in the last quarter alone.

The guy renting the same house next door is vaporising more than $30k a year just in rent and all he can do is hope there’s a meteoric rise in interest rates and a market crash which will never happen.

"a market crash which will never happen"

Do you control the future?

We have all of the conditions set for a major economic blowout.

Robert Shiller (nobel prize for asset pricing) has a good book. Irrational Exuberance. The section on real estate is very good if you haven't read it. If you disagree with that, then its like telling Einstein his theory of relativity is wrong without even having a physics degree! But as I am continuously reminded, property investors are more intelligent than people with nobel prizes in specific fields!

Been hearing that for years Amigo.

Must be quite a life practicing such a doomsday religion.

The difference is what I said is happening NOW and HAS happened.

Your opinion for the future and my opinion on the future are just that opinions.

I know I’m bloody glad I’m not a renter.

Falling house prices is a very positive thing! Hardly DGM - only DGM if you have too much debt or exposure to that asset class.

Rising house prices is very doomey and gloomey because of the long term implications it will have for financial stability and ability of younger people to have a meaningful life (home ownership/financial stability).

Who are they positive for? The tiny fraction of renters that can buy at prices 50% less than what they are now.

A minority within a minority your logic is ridiculous.

You dont have to go more than 30 years back to see that your comment regarding monorities is ridiculous. Housing was very affordable. Now it is a debacle that can only explode, there is a clear divide that is growing between renters and our lords, it will not end well.

Falling prices are only an issue for those who own multiple properties and rising prices only benefit those with multiple properties. Everyone else buys and sells on the same market. Rises further screw FHB while the owner occupier with one home buys and sells in the same market. Ok not sure what minority you are referring to.

How many FHB/Renters are between 50% and 80% there with a deposit? Someone currently with $50k would have a 5% deposit on a $1 mill property and might not make the cut with the banks. If prices were 50% less they'd have a 10% deposit on a $500k property.

Sorry but silly comment. That's like crying about not being able to afford a 2M house if you can only afford 1M. Yes there's not many lower price properties around but there are still many provincial towns with houses under 600k of which 50k is a good deposit with a second tier lender.

All investments marketed to the general public, with the exception of NZ residential real estate, carry a warning similar to the following:

"The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable guide to future returns"

Is this reasonable? Please discuss. Useful reference material can be found by searching "Property Bubble" and USA, JAPAN, SPAIN, IRELAND or LONDON

But New Zealand is different.

Its educational that people are talking about possible rates of 5 or 6 % like they are scarily high...it demonstrates just how unprepared the market is for reality.

Because that’s more than a 150% increase than what we are at currently. Ie. that can’t happen over a short term.

Far too much focus on nominal values and not on percentage terms on this site.

10 Year Treasury Rate is at 1.63%, compared to 1.60 % the previous market day and 0.69% last year. This is lower than the long term average of 4.36%. Theres a 200% + move and it mostly happened in a lot less than a year.

Because many FHBs who are borrowing a bulk of this money and bidding prices up probably weren't affected by the 2007/8 financial crisis, due to still being at school or uni. I remember back in the 90's it was huge news when the interest rates went below 10%, and that was considered ultra low!

Housing debt is painted by some as being 'good debt'. But if people are over paying, it could turn very bad. Peopel are getting hooked on these low rates, but at some point in time, someone is going to have to pay the piper when interest rates rise.

I remember buying a first house back in 1993-94 with a 5% deposit. The interest rate (no fixed available) went from 7.5% when we signed our S&P agreement and got our mortgage, to double digit by the time we moved into the house.....

I see the risks, but I can't see NZ or most of the world unwinding interest rates quickly.

Is Orr still pretending to be sick, hiding under the blanky, pretending he's invisible and hoping nobody will notice he hasn't made an announcement about DTI's or interest only loans. I wouldn't put it past the arrogant buffoon... and Bascands interview the other day, wow uncomfortable guilt on show for all to see. Pathetic and so far out of their depth its excruciating.

He might be off trying to sell his trust's rental property portfolio to settle all the Interest Only mortgages tied to them. I think his properties are the ones being passed in at Auction.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.