Well, if last month proves to have been a last big blow-out in mortgage borrowing before a slow-down then it was one hell of a blow-out, that's all you can say.

Records were shattered once again in March, according to latest Reserve Bank figures, with $10.487 billion advanced in mortgages.

That easily beat the previous record of $9.652 billion in December 2020, which was one of a series of records at the end of last year.

Up to the closing months of last year the record for a month had been only $7.3 billion, back in mid-2016.

First home buyers hit a new high too, borrowing $1.775 billion, which beat the previous record of the FHB grouping, also established in December 2020, at $1.686 billion.

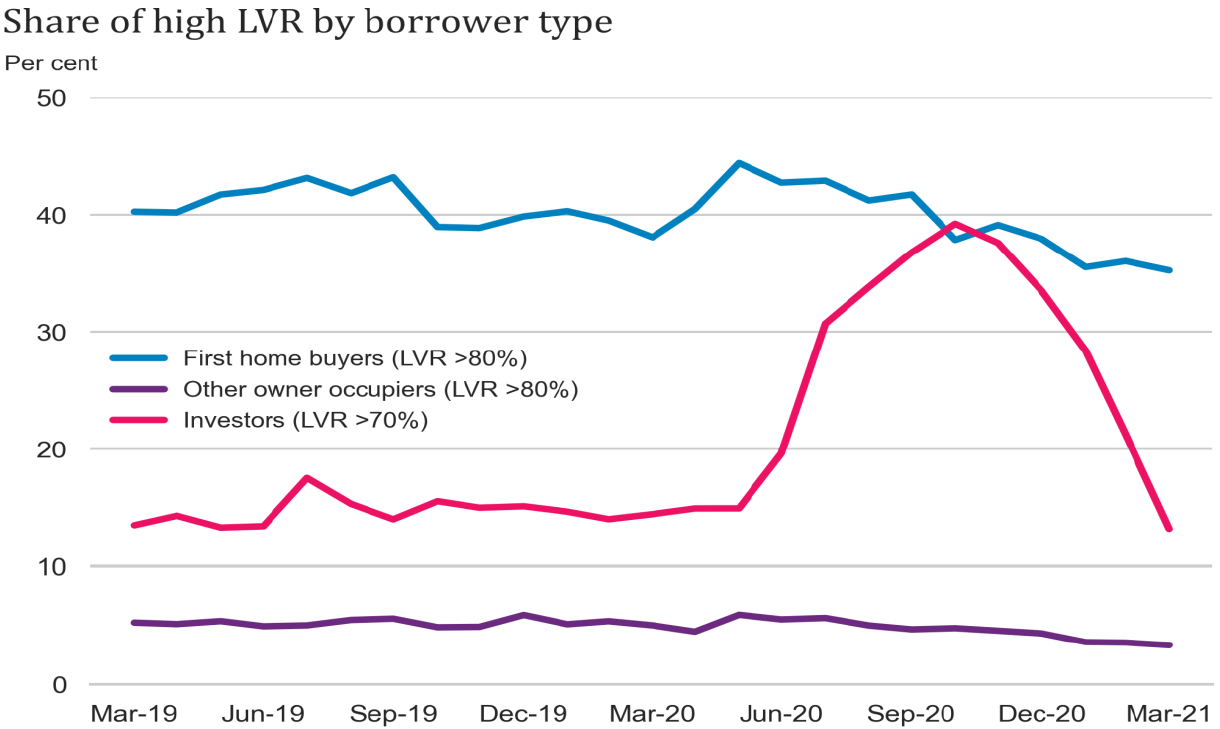

And the percentage share of the market increased again for the FHBs, up to 16.9%. This snapped the recent trend of a declining share after hitting a peak level of 20.4% in July last year.

While the FHBs have been declining in share, the investors have been heating it up.

They were strong in the market again in March, at close to record levels, with $2.325 billion borrowed, though this is below what they borrowed in December, and below the all-time high of nearly $2.5 billion borrowed by investors in May 2016.

The investor figures will of course be very interesting to observe in the next few months, with the move to 30% deposit limits having been officially re-introduced in March and then a 40% rule officially coming in at the start of May.

Of course there's also been the Government's March package of investor-unfriendly housing policy changes, which should inevitably have some impact.

Banks have been applying the new LVR rules already, so, much of the uptake in the past month was likely using up pre-approvals.

The $10.487 billion of mortgages advanced in March compared with just $6.181 billion in March 2020. And that figure for March last year was actually quite a buoyant one, with the lockdown not occurring till late that month and the market having been on an upswing before that.

In terms of the investors, they took advantage of the RBNZ decision to drop loan to value ratio (LVR) limits as of May 1 last year in response to Covid crisis.

Up to then they were required to meet 30% deposit requirement. The LVRs of course are now back, in response to the way the market has overheated.

During the time the LVRs and the deposit rules were off, the investors made hay, borrowing as much as over $800 million in a month (in both November and December) on high-LVR (above 70% of the value of the property) mortgages.

In the latest month this figure was down to $307 million in high LVR loans for investors - the lowest total for this group since June last year.

34 Comments

by Cowpat | 29th Apr 21, 3:23pm

Clearly todays RBNZ mortgage stats for March which undoubtedly Mr Hargreaves will offer some insight on ,put everything into perspective.

This trend of borrowing more has reached its peak and will be significantly lower from April

Yvil

Agreed.

The mortgage data will be based on contracts entered some six to eight weeks prior to Government’s 23 March announcements.

A cooling of the market seems highly probable based on housing reports, auction figures and going into the winter.

Yep totally agree Yvil. I believe this massive expansion of debt is part of the final stage of the 80 year debt cycle. The final “melt up” period is happening right before our eyes and not just here in NZ which many people don’t seem to have grasped. We are going on the same debt fuelled binge as the rest of the world. Looking at Barfoots auction results the housing market is definitely slowing. Stand by for some government incentives should the numbers drop too much.

Figures to the end of March. So now to wait and see if the recent measures, bright line extension, tax rebate removal, get any meaningful purchase. Put the cat back in the bag, the horse back in the stable so to speak. Except, the way things have been encouraged to burgeon, it will be more akin to getting the horse back into the bag, and and an elephant back into the stable.

A cooler winter market is also a good time for buyers to look around at properties - and be under less pressure doing so........

That's not insignificant, given the full-on activity of recent times.

TTP

Moving forward, why leave money in with the banks and risk it being used for their bail-in when you can invest it property where banks can't use to bail themselves?

Moving forward, why leave money in with the banks and risk it being used for their bail-in when you can invest it cryptocurrency where banks can't use to bail themselves?

Moving forward, why leave money in with the banks and risk it being used for their bail-in when you can invest it cryptocurrency where banks can't use to bail themselves?

The great thing about BTC in particular is that there are no bail outs. You're on your own. The biggest threat to BTC seems to that the central banks, govts, and commercial banks will pull their heads in and stop printing money like there's no tomorrow. Not going to happen. There's no turning back. The die is cast.

Brock

What is it; 97% of Bitcoin holders have less than one Bitcoin? Less than 60k on a good day.

Why do you think that is?

Hi printer5,

I was being facetious about the clown world drivel. But that's an interesting question.

The most obvious answer is that there are an awful lot of people holding bitcoin and only 21 million bitcoins (eventually) to go around. Even less when you subtract what the whales are holding.

https://insights.glassnode.com/bitcoin-supply-distribution/

As you can imagine, when it first started over 12 years ago there were only a small amount of people involved in the eco system, ergo high wallet concentration.

As the network has developed, and the supply rate has been cut down, the distribution of BTC has increased as the larger earlier holders have sold some.

A number of large quantity wallets have had their keys lost, due to the small value they were worth at the time, so that is gone for ever.

And custody services hold a large number of Bitcoin, but for a larger number of people.

Also retail tend to buy in more near the peak of the market when prices are over brought, so they get a smaller amount of Bitcoin for their $$. Where as the smart players and long term hodlers keep accumulating and DCA throughout the bear market so they are likely to have over 1 BTC.

Also it takes conviction to commit your $$ to buying BTC, and a lot of people jsut arnt well researched enough to have that. With increasing research comes increasing conviction and increased purchase of BTC.

https://decrypt.co/60021/the-number-of-bitcoin-on-exchanges-is-starting…

The number of BTC available on exchanges is falling rather fast. very bullish for price and long term accumulation/hodling.

There is not just residential property as an investment class.

There are many opportunities in several different investment classes, and NZ residential property is the most inflated of all.

it is INSANE!

The fact that the government is doing basically nothing, dragging the foot as slow as possible clearly shows that they should not be in the driver's seat!

You mean households have been taking on eye-watering amounts of debt through zero fault of their own and the government is to be blamed for this entire mess?

Who do you think should be in the driver's seat instead? (A)NZ National Party and its current leadership that blames inadequate supply for FHB woes when 2 out of 5 houses are still being sold to speculators/investors.

What is the alternative? Do you agree that people need a roof over their head or do you think people can subsist in a tent? Rely on landlords to provide accomodation and risk rent increases? I bet you're against capping rent increases also. Do you rent or own your own home, or are in social housing? If you own your own home then STFU

Kiwis have again been borrowing up large

Only because they can. This headline could easily be 'Banks have been creating money like there's no tomorrow.'

And that is the reality. A steady stream of funding to specu-punt primarily on houses. Of course, there's multiple trade offs, the main one being monetary debasement. But many people don't really understand that yet.

As long as the Ponzi exists, I cannot see how we can have anything other than month after month after month of record borrowing. It's the only way to keep the houses changing hands at these nose-bleed prices - including the price increase that must be added on to each subsequent sale to keep the scheme viable. A Ponzi scheme such as this one is reliant on new punters entering all the time, plus an ever increasing supply of cheap bank credit. It is not so much a case of 'helping FHB's onto the ladder' as of finding more suckers to keep the scheme going. As soon as the whole think starts stalling due to a lack of mug punters, decreasing credit, or increasing cost of money (or all 3) it collapses, hence the juxtaposition of the increasing angst of the stakeholders and enablers against their continuation of cheap and plentiful credit and grants to help more suckers enter the game.

Well...to buy unit for 1.155 Million, will have to borrow more so no surprise.

https://www.oneroof.co.nz/news/first-home-buyers-push-auckland-brick-an…

What is surprising is that both Robertson and Orr still following the path of Wait and Watch.

Besides god, it is only these two, who can answere, why and what are they waiting for before taking action that they will know in next one month.

Govt. will not do anything because they clearly see the stats, that people are highly leveraged. Thanks to Orr for low rates and removing LVR with just a blink of an eye.

Now it's too late if they take any serious step it may lead to mayhem. As the old saying goes "A lie may take care of present but it have no future".

Govt. will not do anything because they clearly see the stats, that people are highly leveraged. Thanks to Orr for low rates and removing LVR with just a blink of an eye.

I think it's a bit disingenuous to blame the most recent actions govt and the central banks. This has been going on for a long time. And it's not addressing the real issue in that the train cannot be stopped now. It's not like turning off a tap. Biggest issue I feel now is that Orr and co probably feel quite powerful in what they can achieve. They may wrongheadedly believe that they can control the economy on a string. That should be a concern to people.

You are right every government has done this slowly decreasing, interest rates so they can get the GDP to go up. But this can stop it will just be a crash, it will eventually be a crash no matter what we do, hopefully doing something now will mean it will be as smaller one. But just put it off until later, just like the environment, hopefully it will be someone else's problem. I think an average house should be $300,000 so that a big drop.

The Ponzi scheme will come undone when interest rates suddenly rise due to an ‘unforeseen’ shock - I wouldn’t at all be surprised to see this happening within next 5 years

Rapid Inflation in the US is what to watch for, when the FED moves rates up, NZ will follow, as they always do.

Interest rates may not need to rise for the ponzi to look shaky. If capital gains start to flatten or house prices do start falling, the smart investors will sell, i.e. panic early.

Minksy moment.

Bored with Ponzi rhetoric. Look at cities in attractive countries and you’ll find suburbs around the financial districts being unaffordable to most. London, Paris, Amsterdam, Dublin, Edinburgh, Brisbane. Please someone, anybody, explain to me why people in Auckland expect a financial district on the waterfront in a place with great climate, wildlife that won’t eat you, in a stable political environment with crime controlled not to be on that list? Once the overseas buyers, and the property investor filth have been vanquished the reality will still remain that just like the average Pom can’t afford Leicester Square, so the average Kiwi can’t afford One Tree Hill. Parnell, Ponsonby and Remuera are Bond St, Regent St and Oxford St. It’s monopoly, just in a different city.

If you can’t afford to live there now, move on and look to an another amazing part of Aotearoa to enjoy. I left for the Waikato 2 years ago and have less debt, more time and a better life balance - I can’t live the life I want in Auckland, just don’t have that sort of income. I can’t afford a porsche or to fly front of the plane neither.

I'm with you, should have moved to Tauranga years ago and now can buy a Porsche but who really needs one. All I can say is WOW at the level of lending in March, it was simply staggering in a world where Covid is still raging. I think it was a case of the last train out of central for home buyers, everyone who possibly could do it has got onboard, it was a last chance opportunity.

It's not just about Auckland, though. Auckland is severely unaffordable, but the rest of the country is also unaffordable. There is just nowhere cheap to move any more. If you look at this list, every single city in the North Island has a median multiple of at least 6, and there are only 2 under that (just). There are only two cities in the South Island with a median multiple of less than 5 (and again, only just). You need half a million dollars now to buy a house in Masterton, for christ's sake.

https://www.interest.co.nz/property/house-price-income-multiples

I live in Masterton and agree. Our Core Logic mid-range valuation for a 3 bedroom 80sqm Keith Hay Home built in 86 on 1/5 acre has surpassed $500k. Went up $16k from 4 April to 18 April.

Feels like the market is now turning downward. A 4 x 2 bedroom in Devenport passed in yesterday at $1.7 Million ( 1 bid) it sold in 2016 for $2.35 M and its 2017 RV was $2.36M - so it was valued yesterday at 650K below its RV. Even if the house was a leaky home - $1.7M would be below the land value. Another property sold in Torbay for 100K below its 2017 RV

Looking at the Hutt valley market- 16% of houses now have a listed price (with 2 taking 50K off their listed price this week) - with approximately only 50% selling at tender each week for the last couple of weeks .

I've also been tracking a number of "nice " houses passed in at auction since the 12th April- real estate agents / auction houses are claiming those houses are selling within a couple of days- I suspect this is selective data as all the houses I've looked at are still on the market asking 100-150K over the passed in value.

Ahh Torbay my old stomping ground, it used to be nice 20 years ago but I hear its going down the toilet. There was always a few dodgy streets with the usual Bogans, I mean one house on Awaruku literally had the words "Bogan Villa" painted on it. I now hear that other streets are being called "Meth Ally". Not great when houses in the area are now well over $1mil.

As house price to be paid has risen a great deal in last 12m, no surprise that borrowing has risen a lot.

Existing borrowers also took advantage of lower rates to reset mortgages.

Are these increased loans separated out for analysis by RBNZ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.