Kiwibank is launching what the bank describes as its lowest ever home loan rate.

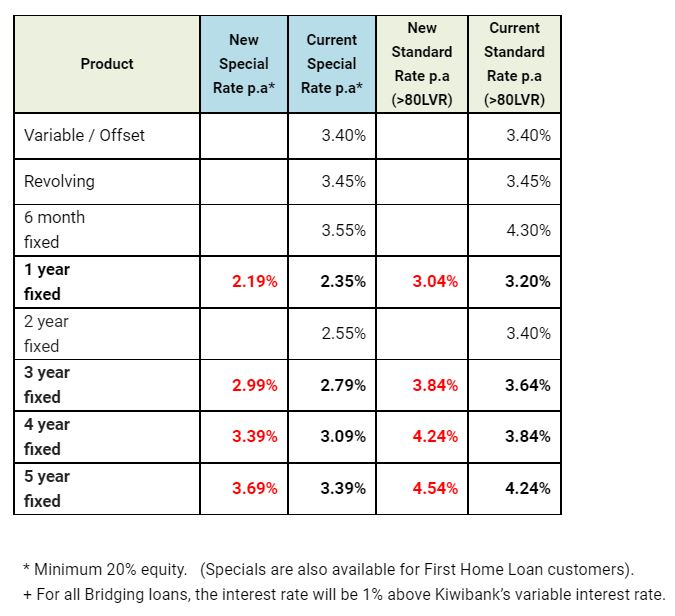

From Tuesday, June 8, Kiwibank will offer a one-year fixed mortgage rate of 2.19%. Borrowers will require at least 20% equity.

The new offer reduces Kiwibank's previous one-year "special" of 2.35% by 16 basis points.

The 2.19% one-year rate is lower than what the big four banks offer, but not the lowest one-year rate on offer from a bank. The Bank of China, The Co-operative Bank and Heartland Bank all have lower one-year rates, while HSBC and SBS Bank also have 2.19% rates.

The Bank of China has a one-year "special" of 2.15, The Co-operative Bank has a first home buyers "special" of 2.09%, and Heartland Bank has a 1.85% rate. See all banks' carded, or advertised, home loan rates here.

Meanwhile, Kiwibank is also increasing three, four and five year fixed-term rates, as shown in the table below. The bank's three-year "special" is increasing 20 basis points to 2.99%, and its four and five-year rates are being increased by 30 basis points each to 3.39% and 3.69%.

One useful way to make sense of these new changed home loan rates is to use our full-function mortgage calculators. (Term deposit rates can be assessed using this calculator).

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options.

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at June 4, 2021 | % | % | % | % | % | % | % |

| ANZ | 3.39 | 2.25 | 2.45 | 2.59 | 2.89 | 3.90 | 3.99 |

| 2.99 | 2.25 | 2.49 | 2.59 | 2.89 | 3.19 | 3.39 | |

| 3.39 | 2.25 | 2.49 | 2.55 | 2.79 | 3.09 | 3.39 | |

| 3.55 | 2.19

|

2.55 | 2.99

|

3.39

|

3.69

|

||

| 4.15 | 2.25 | 3.25 | 2.59 | 2.89 | 3.19 | 3.39 | |

| Bank of China | 3.45 | 2.15 | 2.15 | 2.55 | 2.75 | 3.05 | 3.35 |

| China Construction Bank | 4.70 | 2.65 | 2.65 | 2.65 | 2.80 | 2.89 | 2.99 |

| Co-operative Bank (*FHB only) | 2.25 | 2.09* | 2.59 | 2.59 | 2.79 | 3.09 | 3.39 |

| Heartland Bank | 1.85 | 2.35 | 2.45 | ||||

| HSBC | 2.79 | 2.19 | 2.19 | 2.45 | 2.69 | 2.99 | 3.19 |

| ICBC | 2.89 | 2.25 | 2.35 | 2.35 | 2.65 | 2.89 | 2.99 |

| |

3.39 | 2.19 | 2.39 | 2.49 | 2.79 | 3.09 | 3.39 |

| [incl Price Match Promise] |

2.89 | 2.25 | 2.45 | 2.49 | 2.79 | 3.09 | 3.39 |

Fixed mortgage rates

Select chart tabs

52 Comments

Perfect time for retail banks to give the housing market a little lift. The music must never be allowed to stop.

Excellent! Now who else is courageous enough to do the same and continue the property boom!?! Let's go!!!

To the moon!!

Interesting move... clearly must be lots still out there wanting to fix short term.

No point if your mortgage needs to be paid on a 30y term.

Are there many people these days actually thinking they're going to repay their mortgage in full without selling/downsizing/relocating?

That's my plan. 4 years in to my 30 year mortgage. 19 to go. Will probably be paid off in another 10.

But we built a passive house, top double incomes no kids.

Yup our plan too. 4 years into an initial 25 year mortgage, have just refinanced 4 year fix on a 9 year loan.

what? whats the logic behind that statement?

Perhaps people needing to take out $750k+ home loans in Auckland & Wellington just to purchase their first home & get on 'the ladder'. Later down the track these people want to sell & buy their second home & required to take on more debt due to ever increasing house prices - a new 30 year term taken. They find they have life events that pop up - have children, purchase cars, renovations, divorce etc which require more debt or reducing payments/interest only. They repeat this until retirement. Was that original 30 year term stuck to? How will most clear this debt in the end? Selling/downsizing/relocating home/retirement village.

I didn't ask you to trot out your favorite rant, I wanted to know what logic (if any) turns the previous post into a statement that makes sense

That's it buddy, a real scenario facing many who are buying into the market today.

You asked a question. It was answered, but apparently the answer is a rant?

The answer doesn't address the question, so yeah, its an off topic rant.

The question was whats the logic behind : "No point if your mortgage needs to be paid on a 30y term." which was in response to a comment about people fixing short.

Plenty of reasons to fix short, regardless of what the mortgage term is. Then main one being the short term fix is so much cheaper, the only reason to fix long is if you are worried about extremely fast rate increases or need certaintity of outgoing for a longer term.

I was refering to my statement in which you replied to asking for logic... follow the thread? Seems you're abit lost.

No, you are the one that can't follow threading on this site. I didn't reply to your comment, I replied to b21s comment

The real story is the increase in the 3, 4 and 5 year rates. People think long-term when taking out a home loan, don't they?

People also think lowest repayments possible when taking out a homeloan...

1) If you're paying down big chunks of your mortgage each year, a lower short-term rate now will cost you less overall than paying interest at a higher rate in the future (unless rates rise sharply over a short period - unlikely though)

2) investors can cream better returns at lower short-term rates and look to raise rents to cover higher future rates

I agree. With a 1.5% differential rates would have to increase quickly and substantially for anyone to be better off fixing for 5 years. Though it depends on your risk tolerance.

Bingo, this rates curve makes it even more attractive to take the cheap short term rate and max out payments. Going to crunch the numbers on where we end up after a year or two of short term fix and increasing payments by 30% vs 3+yr fix with the same repayments.

Yup , take the lower rate, and the highest repayment rate you can afford , plus save as much as you can to knock a chunk off it when it matures in a years time. worth it just to see the years knocked off the maturity date , and the total interest paid over the life of the loan , but also hard to lose out unless interest rates increase massively.

And with the last decade of generally declining interest rates, that's paid off as the best strategy.

It looks like we're now in for a period of rising rates, but the bottom end rates are at the same time getting cheaper, so it makes it even more difficult to justify locking in a rate that is quite a lot higher now, for gains in the future that may never eventuate if rates stall or start declining again in 18-24 months time.

If you factor in the very high purchase prices people have been paying lately, that also strongly incentivises them to pay the lowest rates available, even if that's not the best choice in the medium-long term.

"It looks like we're now in for a period of rising rates. .."

Nope

Cant happen

Oh you must not have read the article. 3yr-5yr rates put up TODAY. Banks care about the wholesale curve. At start of the year (01/01/2021) the 3yr swap rate was 0.3585% and today it is 0.8373% that's up ~48bps. Don't underestimate the speed at which this can accelerate. 1yr and 2yr swaps still artificially held down by FLP etc. The 1y2y is heading up fast so don't be so sure those who fix 1yr now and then 2yrs next year will be better off. Maybe diversify so split mortgage across 1yr/2yr/3yr tenors with maybe a 50%/30%/20% split or something. I don't know.

Did you not read anything else in the comment?

That was kind of my point ;)

-- but wouldn't Orr and Robertson love to have almost everybody on floating or short term fixes -- certainly gives them the best bang for their buck when making OCR rises --- bit conspiracy theory but TBH would not rule out some under the table coercion !

ps - took 2.99 for 5 years just over 3 months ago -- feel very smug! -

That offers you no flexibility at all. I'd be edging my bets a little with these mortgage rates and using any savings in an offset account paying 0% interest, lets say 10-20% of total mortgage. Then I would select a 1,2,3,4 and 5 year mortgage weighting each to suit you better.

It worked for me as when a term ended I changed to an offset as I had more income and savings. Overall I paid a lot less interest than 2.99%

Agree. A mix of tenors probably suits best. But also bear in mind that with a steepening curve that banks are in-the-money on their hedging (swaps) so you could probably break and negotiate no fee so some flex in reality even if fixed all for 5yrs.

dont need it -- i could repay it all - just 200k -- BUT its good debt at that price and i have more invested in various other assets and some investments that return better than that -- if i pay any more off -- i cease to be a good bank customer - so keeping it there -- but previously always had tranches and revolving but no need now - there is virtually no downwards movement possible -- so its all upside risks -- and 5% would cripple many - equity rises are one thing - but people are at cashflow replayment limits which will be the stressor

I’ve always thought that splitting a loan removes any bargaining power you have. Eg if you split your loan over 1,2 and 3 year terms, as soon as your 1 year comes up for renewal the bank knows you’re not going anywhere so don’t offer a discount. I’ve always put all my money on the single short term, and negotiated hard each time. And check with other banks on what they will offer. Using this technique I’ve paid massively under carded rate for years.

Get them locked in on a one year rate and know they probably won't change banks when the interest rates go up in 12 short months

Reeling people in with the one year special, but look what's happening elsewhere in the curve. When it comes time to roll that - you'll be staring down the barrel of higher rates for every maturity. I wouldn't touch the 1 year with a bargepole.

So what's the alternative, then? Take a 2 year rate now and you think in 2 years time it will still be 2.55%? If that is the case, would the 2 year rate not also be 2.55% 12 months from now?

Or you'd ask them to charge you the old 2.35% 12 month rate instead, so when it ends in 12 months time the rate will still be 2.35% and you won't have sticker shock going from 2.19% up to 2.35?

If you take the 3 year rate (that they just increased), at the end of it the 3 year rates are likely to be the same or higher than they are now. Perhaps the 1 year rate will be lower at that point, so you'd get a decrease going from 2.99% to something lower, but you're only on that 2.99% rate because you chose to be on it just now and you could have been on lower 1 year rates for 3 years and likely still paid less interest over the period in total, especially if you made any lump sum repayments.

Really don't understand what your comment is trying to say - other than if you wanted to fix for 3+ years you should have done it yesterday. But that's hardly worth saying.

Whatever we do, we're gambling on the future. The only difference is some people have more confidence in their ability to predict it, and maybe in some extremely rare cases more actual ability to predict.

I'm sympathetic with the argument to fix long for the same reasons I'm sympathetic with people who take out insurance. Probably end up paying more but get some stability in return.

If you can afford to fix long, then why not just fix short and pay the same as if you'd fixed long?

Aside from paying it off quicker, it has the added advantage of building up a surplus in your mortgage, so if you need to go on a repayment holiday or interest only, the bank well be more favorable to your than if you're already riding the 30 year term loan limit.

Seems like the only thing you're hedging against is rates going up very very quickly. That simply seems unlikely to actually happen.

Yes, it's just insurance against steep rises. We'll all have opinions on how likely that is - I wouldn't rule it out myself but maybe it's not the most likely outcome. Personally I've gone for a 1 year fix as I'm in a position to overpay fairly aggressively, and have other investments I could sell if I really needed to bring the mortgage down. No need for the insurance any more.

They were making a big song and dance about floating rates being too high when they cut theirs to 3.4 last year but haven't passed on any of the 0.75 OCR cut to their floating rate since?

The OCR was already 0.25% when they cut their rate to 3.4%. https://www.interest.co.nz/personal-finance/105458/kiwibank-cuts-floati…

I stand corrected.

Those getting in now will be the ones that will be hit the most if they chose they 1Y rates, pretty dirty move if you ask me.

Good timing, just when we've had pretty much the highest house price growth in the world, from an already very unaffordable level.... Just in time to lure in greater fools, who don't have the financial literacy to consider how their cashflow might change with interest rates.

https://www.stuff.co.nz/life-style/homed/real-estate/125348365/nz-numbe…

One false move by this govt in regards to china or covid, and these rates wont be going up.

I bet on rates going down. Debts to high and rising rates will kill the economy. You watch Orr, he will start waffling about transitory inflation, COVID risks blah blah. They have no ammunition left now.

"They have no ammunition left now" ... that is precisely why they should hike. Give them a tad more ammunition to fight the next crises. Imagine where rates would be now due to COVID if the Fed didn't give itself room with hikes in 2015-2017.

The mob will tell you rates are going up. Don't listen to the mob.

The mob will tell you rates are going up. Don't listen to the mob.

The 1 year rates are starting to look attractive.

For buyers, it's like a 1 year rates discount. If you're a marginal buyer, this is a golden opportunity- you're given 1 year to sort out the rest of your finances. Top that with price appreciation, this is a double win for every buyer.

Be quick.

Pump dat ponzi

Locked in 3.09% for 4 years with ANZ and increased our payments. Was tempting to fix shorter on a lower rate, and it'll probably work out cheaper over that 4 years if we instead fixed 1-1-1-1 but I was drawn to the stability/peace of mind.

Current payment schedule has us mortgage free in approx. 9 years, so certainty for 45% of the current loan term.

I fixed for 5 years at 3.2% on a 5 year term.

However truth is that this and that needs doing too and chances are we will add more debt before my 5 years are up and I meet the mythical mortgage free end of the rainbow. But it was nice to think it was possible for a fleeting moment.

We're very fortunate we purchased where and when we did. We've completed done all the "this and that's" that need doing i.e. new hot water cylinder, roof repairs, new car etc so unless the wife convinces me to upgrade (she's trying) we're on the home stretch.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.