Predictions of more restrictive lending are playing out with credit bureau Centrix fingering changes to the Credit Contracts and Consumer Finance Act (CCCFA), rising interest rates, tighter loan-to-value-ratio (LVR) restrictions and the business buzz-kill Omicron as the culprits.

The proportion of mortgage applications resulting in approval fell to 34% in February, down from 40% before the CCCFA changes kicked in from December 1, while consumer finance conversion fell from 35% to just 28% of applications, said Centrix.

"Our data shows lending has become more restrictive since changes to the Credit Contracts and Consumer Finance Act came into effect in December, with the number of approvals down again this month," said Keith McLaughlin, managing director at Centrix.

The CCCFA changes kicked in not long after the Reserve Bank began its Official Cash Rate (OCR) tightening cycle in October, a nail in the coffin for low interest rates which, coupled with tightening LVRs and Omicron, created the perfect storm.

"Despite rising interest rates, mortgage arrears remain low, thanks to the large number of fixed mortgages. It is inevitable, however, that rising rates will eventually place increased pressure on households who are also facing rising inflation," said McLaughlin.

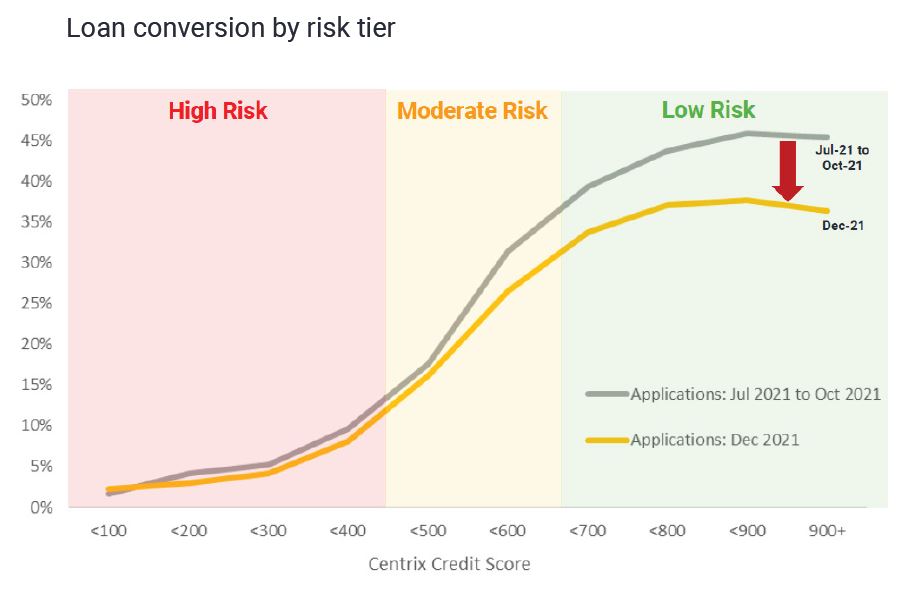

The CCCFA had disproportionately impacted loan approval rates for 'low risk' potential borrowers with a credit score of over 700, which was generally considered to be good, said Centrix.

The higher decline rate was not due to a change in the value of that credit score, but rather the CCCFA's "second leg" of the approval process, the affordability assessment, said McLaughlin.

This part of the process did not allow lenders to apply discretion over a borrower's ability to reduce their discretionary spending if interest rates went up. Instead, it was a snapshot of their spending habits at the time of application.

"Borrowers now have to satisfy the lender they have the ability to meet their financial obligations under different circumstances," he said.

The change was less pronounced in the moderate and high risk categories due to an already high decline rate and the changes making them no more or less appealing to lenders. The change within each risk category is shown in the table below:

Credit demand was flat in February, with demand down 3% y-y and buy now, pay later (BNPL) applications at their lowest since March 2020. While a post-Christmas lull was normal for BNPL, the deep dive this year pointed to the other factors at play, particularly declining consumer confidence amid Omicron.

Auto finance also fell from a peak in January, an annual high point for vehicle purchases anyway, but again a steeper fall than usual.

In line with expected trends, namely the come-down from the squeeze of Christmas bills, arrears increased across all regions in January, but remained low by historical standards.

Financial hardship was at a two year low, reported Centrix, and arrears on credit cards and vehicle loans during 2021 were at their lowest since consumer credit reporting has been in place. However, arrears on personal loans were particularly high.

Meanwhile, the retail sector's credit default rate shot up 24% y-y and Centrix put this down to price pressures, supply issues and less customers through the door while Omicron was rife in the community.

The hospitality and tourism sector continued to be impacted by restrictions and cancellations while construction had strong demand but lacked the labour and materials to meet it.

20 Comments

The graph is hilarious. Banks already had a responsible lending code and serviceability testing for housing. This government couldn't implement a bake sale.

The graph suggests an amazing conclusion - credit is being restricted to those who used to get credit, while those who never could still can't. Remarkable.

Would be much more useful to show one line divided by the other to see more clearly how the change is distributed. Looks like a 25% or so reduction at the high end, but hard to tell at the low end on this graph. Could easily be 25% there too, but that wouldn't support the conclusion Centric are trying to reach...

"...It is inevitable, however, that rising rates will eventually place increased pressure on households who are also facing rising inflation," said McLaughlin.

Inflation increasing at 6% and Wages at 4% seem to be a classic symptoms of overheating. RBNZ don't seem particularly interested in the sustainability of growth but just in trying to not prick the bubble.

People are getting poorer and feeling the financial repression of these crazy central bank policies - no wonder people are in Wellington throwing 💩 at police.

Unless something changes, the social unrest is only going to get worse, not better.

Completely agree.

Personally, I'm doing OK financially, but when I look at the K shaped recovery, and the way that real people are struggling with rents, living costs, and the impossibility of ever owning a house, it makes me want to go throw 💩 as well.

However, I think they should be throwing it at the RBNZ offices, and not just at parliament.

Yes and yet the RBNZ are simply a puppet of the Fed. So oddly our future rests in the hands of an external influence. We go where the Fed goes.

And the Fed/USA is being tested at present by Russia (and perhaps China...). That outcome of that challenge could see a change in world reserve currency.

If that happens the RBNZ would no longer be a puppet to the Fed but to whatever other monetary agreements are made post conflict. If that happens, the asset bubbles that the Fed have created will have no state backing.

The world could get very interesting this decade, if not already. Everything we've known the last 30/40/50 years could be completely reversed - and the future look nothing like what we've recently experienced. It will be a complete shock, especially to those 40+ who have experienced lives where everything has more or less worked in their favour (no major conflicts, beneficiary monetary and fiscal policy).

However, I think they should be throwing it at the RBNZ offices, and not just at parliament

Should be next on the cards. Soon those protestors are going to realise that Covid mandates are just the problem on the surface, monetary (and lack of effective fiscal) policies are the real deal making average Kiwis considerably worse off.

Once borders reopen to foreign visitors and workers, expect rents to go up again with a spike in demand and more landlords chasing short-term renters.

Yes, I agree 100%. They are a bunch of unelected, unaccountable and incompetent muppets who do not have the decency nor honesty, even now, to admit that they have got their recent monetary policy settings seriously wrong, and who do not seem capable of correcting them even now, when the evidence of overheating and of a serious inflation problem is overwhelming.

Yet another article stating the CCCFA is restricting lending... not that it's a bad thing

When you want someone to lend you money, to do whatever you want to do with it, why are you surprised the lender puts some conditions. Find a lender whose conditions you like or just wait till you have saved it yourself. Borrowed fund 101.

The huge run up in asset prices was enabled by the availability of cheap credit. Now that the taps are being turned off on both the cheap and availability side the people that were benefiting from all that credit are starting to squeal.

The housing ponzi requires more borrowers to be found to lend ever more credit to. Where can we find more credit worthy debt slaves?

There is always going to be some fool who would still be ready to believe in the "there is still room for upwards valuations" real estate agents' BS. But the problem is that the Ponzi is starting to run out of such fools. This always happens in the end, whenever the theory of the greater fool is applied to any market, be it tulips or investment housing.

Debt is not a great thing but now it's become a necessary evil.

Debt creates huge levels of inequality in society if it's let to run without any checks and balances.

'400,000 people are behind on their loan repayments' - Stuff reporting this from Centrix report. Seems .... like a big number.

The situation is not good out there in the market with small business. A cafe owner in a decent Mall in a well to do area is not even making sales of $500 a day. This is from the cashier working there. And they have to pay staff too..

But yeah it's easy to borrow money so let's create more debt.

Our beloved PM and FM will save us again by giving away from their big pot of gold.

15.1 per cent of borrowers in Gisborne are past due on some form of loan

I'd note that these scores are just based on performance on previous loan contracts. They don't consider anything about income (e.g. servicing) or the deal (e.g. LVR). Therefore someone in 'low risk' might actually be declined on the basis that they are actually high risk once information on income, expenses, loan size and collateral value are considered. It's a bit disingenuous calling someone low risk just because they haven't missed a power bill payment.

100%

There's a lot of hurt & anger out there. It is not hard to find. The protest was just the tip of the iceberg. They are marching here, there & everywhere. And, it is not over yet.

Some advice for the govt: Let it rip & let it go. Enough already. Problem for them is that you take away the covid narrative & what do you replace it with? Underneath all the covid noise, it get's even worse. We're in for a politically dramatic period over the next 18 months. It will be no place for the faint hearted.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.