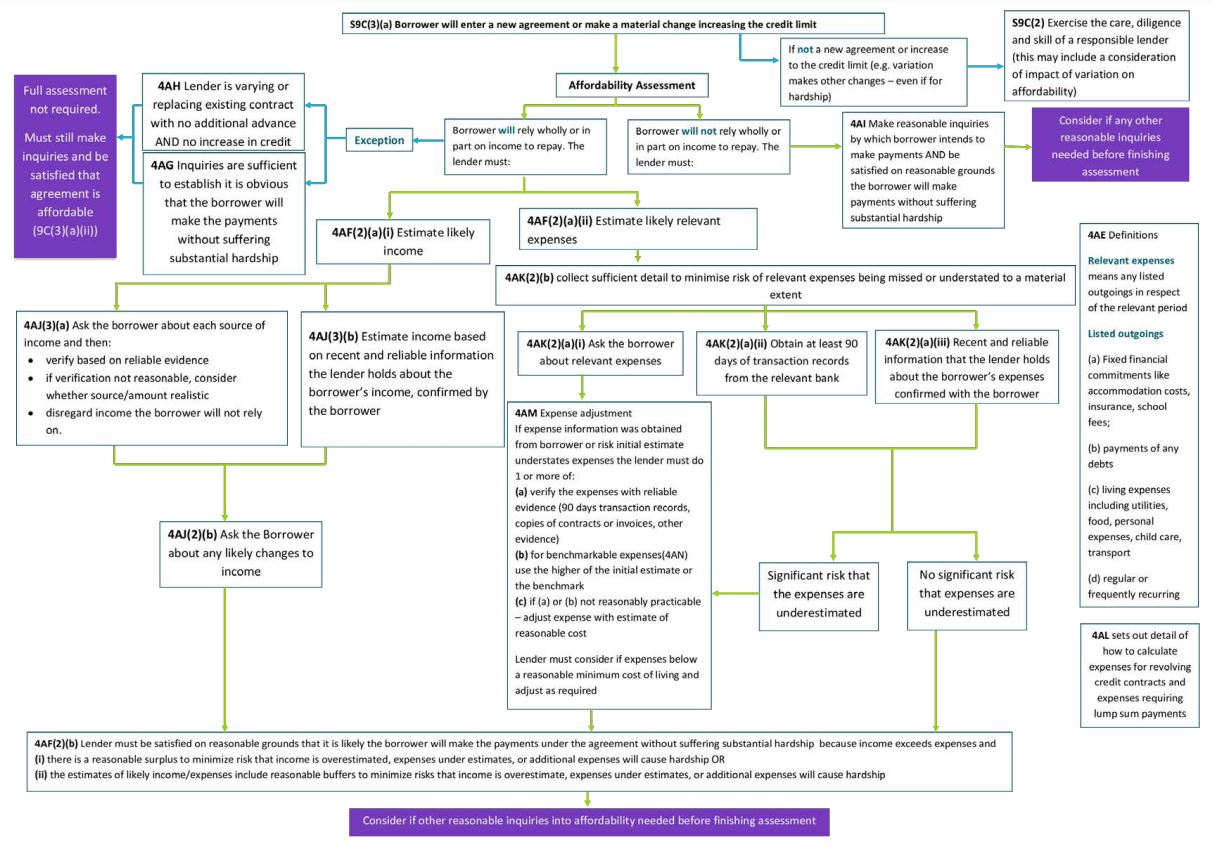

There's an old saying that a picture is worth a thousand words. So how many words is a flowchart worth?

That's a good question when it comes to the wordy one below, which features in an updated version of the Responsible Lending Code.

In a press release highlighting changes to the Credit Contracts and Consumer Finance Act (CCCFA) which took effect from December 1, Commerce and Consumer Affairs Minister David Clark said unfair lenders had been cashing in on Kiwi consumers for too long, and New Zealanders could expect better protection from high-cost loans and unaffordable debt.

However critics are far from impressed, saying there was no problem to be solved and the new rules are too prescriptive. John Bolton of mortgage broker Squirrel, perhaps the most vocal critic, worries about a government-induced credit crunch and said a fight for the free market economy is underway. Bolton has launched a petition seeking to have consumer finance laws reworked.

Looking at the flowchart, there are certainly plenty of hoops for lenders to jump through. In a report on the CCCFA changes, law firm Bell Gully notes despite intending to help lenders navigate the new regulations, the Ministry of Business, Innovation & Employment's updated Responsible Lending Code instead highlights its Byzantine nature.

"The flowchart provided in the Code [below], though intended to simplify things, highlights the remarkable complexity of the new regime and the numerous gateways and decision points that lenders must navigate," Bell Gully said.

Why is it happening?

So why has the Government made changes to consumer lending laws and what are they?

The Labour-led government came to power in 2017 arguing changes made to the CCCFA by the National-led government in 2015 didn't go far enough to combat predatory loan shark and mobile trader behaviour. This concern was outlined by the then-Commerce and Consumer Affairs Minister Kris Faafoi in 2018.

“I’ve spoken with people who have been given loans that are clearly unaffordable for them, and others who have been lashed with huge penalties and fees. These practices trap people and whanau in an appalling debt spiral that is very difficult to get out of. We need to ensure the regulatory settings are right to stop the practices that get people into these terrible situations," Faafoi said in 2018.

However, critics such as Bolton say the changes go too far, stretching into all consumer lending including home loans. Banks are "forced to not trust what you tell them and dive into the details of your life," he said.

Bell Gully notes the Government first introduced responsible lending obligations in 2015 with the objective of ensuring consumer loans were suitable and affordable for borrowers.

"The obligations included new requirements on lenders to make 'reasonable inquiries' of borrowers before issuing loans, and to assist borrowers to make 'informed decisions.' The regime was intended to be flexible and 'principles based' and allowed a broad range of approaches to the various requirements. However, the principles were so broad it made it difficult for lenders to know precisely what was required. Equally, it proved difficult for the Commerce Commission to identify specific breaches, and the principles were very rarely enforced," Bell Gully said.

"In reaction to the uncertainty and to bolster the responsible lending regime, the Government has [now] introduced new regulations with much more prescriptive requirements around: (a) the suitability and affordability tests which lenders must conduct before issuing a loan to a borrower; and (b) advertising of consumer credit contracts."

In regards to new rules, Clark's press release highlights four key areas:

- Detailed standards for lenders assessing the affordability and suitability of loans

- Additional record-keeping requirements on lenders and duties on their directors and senior managers

- Responsible advertising standards

- Greater transparency and access to redress before debt collection starts

Bell Gully said suitability regulations are designed to set out a list of specific inquiries, including in respect of a borrower’s purpose in seeking credit, the required term of the loan, and the amount, plus other more intricate matters such as whether they accept the cost of any “non-avoidable” fees for add-ons that were not part of their stated purposes.

"The affordability regulations require various inquiries to identify whether the borrower can make repayments without suffering substantial hardship. In general terms: if the borrower will rely on income to make repayments - for certain high-cost loans - the lender needs to create an estimate of the borrower’s income and then also expense estimates using various specified tests, including new requirements to verify information received. Where the lender knows that the borrower will rely on means other than income to make repayments - or where other exceptions apply which indicate the risk to the borrower is low - a more flexible standard applies," Bell Gully said.

"The regulations governing responsible lending are complex and include a number of untested standards which are capable of wide-ranging interpretation."

Potential penalties for directors

Additionally lenders' directors and senior managers must undertake due diligence to ensure their organisation complies with the CCCFA.

"This includes: implementing, and requiring staff to comply with, procedures to ensure compliance with the CCCFA; ensuring that appropriate systems are in place to identify deficiencies with these procedures; and promptly remedying any deficiencies identified. There are significant pecuniary penalties in place if directors or senior managers breach this duty of up to $200,000 per breach, or joint and several liability for damages awards against the lender," said Bell Gully.

And there are potential civil pecuniary penalties of up to $200,000 per individual.

"Lenders are not permitted to indemnify any director or senior manager for civil pecuniary penalties or for any costs incurred in defending any proceedings where civil pecuniary penalties are awarded. A court may also order that a director or senior manager is jointly and severally liable with the lender to pay statutory damages or compensation where the lender has breached the CCCFA and the debtor can recover statutory damages or compensation, where the court is satisfied the director or senior manager breached their due diligence duty in respect of that same matter," said Bell Gully.

More hoops for borrowers to jump through

Last month Consumer NZ Chief Executive Jon Duffy told interest.co.nz the CCCFA changes were likely to result in borrowers having to "jump through a few more hoops before being given credit."

"While this may be painful in the short term, the new rules are intended to protect consumers and prevent them from taking on unaffordable and unsuitable debt," said Duffy.

Ruth Smithers, Chief Executive of FinCap which develops and supports free financial mentoring services, said protections in the CCCFA are valuable for everyone in the community.

"Our financial mentors do excellent work in their communities and there will be more referrals to them under the [CCCFA] changes. What is meaningful is these changes will mean fewer people have to choose between eating and repaying a loan," said Smithers.

"The new law applies to all credit applications, small and large, including new loans and changes to existing credit arrangements. Examples include borrowing to buy a dishwasher, upgrading your car on finance, getting a home loan, or extending your credit card limit."

"It might be harder for consumers to get credit or a loan because the more detailed information that lenders need to collect may show the applicant can less easily repay the debt. Lenders will now also need to build in reasonable surpluses or buffers to ensure applicants will be able to repay the loan," said Smithers.

In a submission on the CCCFA changes in 2019, the New Zealand Bankers' Association (NZBA) said it had identified several areas where it was useful to stand back and consider what the proposed change was trying to achieve, and whether that change was a measured and proportionate response.

"One key to reducing harm from problem debt is supporting access to responsible, lower-cost borrowing. However, in our view, several of the proposed changes may unintentionally lead to conservative lending practices to the detriment of consumers," said the NZBA.

"We are especially concerned about the impact conservative lending practices may have on vulnerable consumers, including low-wage workers, immigrants, and refugees. Our members’ experience is that these communities already find it difficult to access credit from mainstream creditors, making them particularly vulnerable to predatory lending practices. Conservative lending practices, which drive consumers to higher-cost and potentially irresponsible lending, run counter to the important policy objectives of promoting financial inclusion and access to safer credit."

'Removing the flexibility of the market to solve problems'

Bolton said the CCCFA changes are a bigger deal than the Reserve Bank's high loan-to-value ratio (LVR) home loan restrictions because they are enshrined in law, whereas the LVR restrictions can be turned on and off.

Bolton, who has previously worked for banks, said the new laws are too prescriptive about how banks have to approve loans. This means credit managers can no longer make judgments because now everything has to be black or white.

"Credit managers look at every deal, at the total picture and get a gut feel on what's good. They can't do that anymore. There's a lack of discretion to assess someone's individual circumstances to make the best decision for them," said Bolton.

He's concerned there will be a government-induced credit crunch, arguing the Government is "removing the flexibility of the market to solve problems."

"It's a fight for the free market economy," said Bolton.

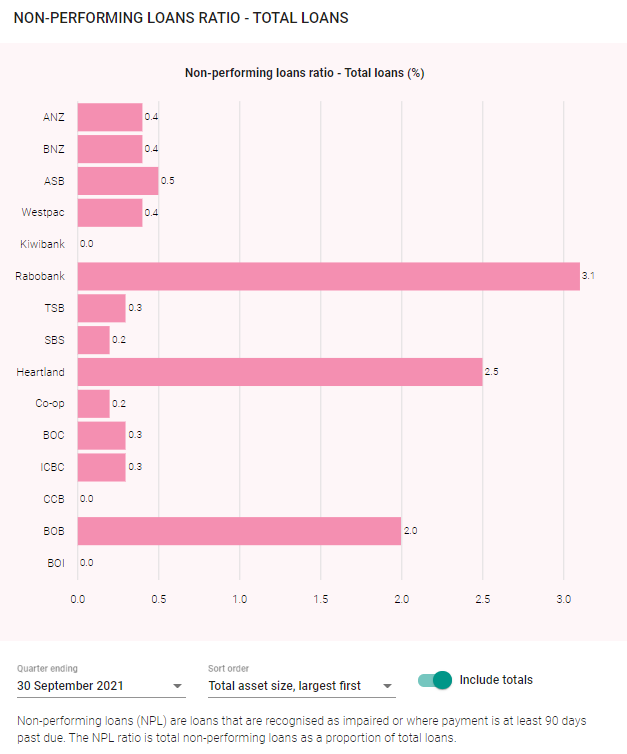

He goes on to say that NZ banks' are already conservative lenders, with low loan loss rates as highlighted by the Reserve Bank chart below.

Has the day come for non-bank lenders?

Bolton reckons one upshot of the CCCFA changes will be more home loan business for non-bank lenders such as Resimac, Pepper Money and Bluestone. Such lenders typically charge borrowers higher interest rates than banks.

Non-bank lending institutions are currently just a drop in the ocean of the home loan market. At the end of October $4.773 billion, or 1.5%, of outstanding home loans were held by non-banks, according to Reserve Bank statistics. The other 98.5%, or $321.555 billion, was held by banks.

But Bolton said non-bank mortgage lenders are now struggling to meet demand, in some cases with 15 day turnarounds for loan applications. For now they don't have the systems, processes or people on the ground to cope with the volume that's going to hit them, he said.

But because they're wholesale funded, funding's not a constraint. Resimac is listed on the Australian share market, as is Pepper after a sell-down by private equity group KKR. Bluestone is owned by private equity fund Cerberus Capital Management. Because of this Bolton suggests "they've got the capacity to step up, [and] the opportunity's in front of them."

Currently he estimates non-banks have 10% to 15% of the broker market, with brokers accounting for about 40% of home loans. He reckons non-banks, which don't have to comply with Reserve Bank LVR restrictions, could grow to 20% of the overall market.

Basecorp Finance Chief Financial Officer John Moody said Basecorp has noticed a significant increase in borrower interest since July, which he attributes to banks preparing for the CCCFA changes and potential Reserve Bank debt-to-income ratio restrictions for borrowers. Hamilton-based non-bank lender Basecorp has borrowed $500 million through two issues of residential mortgage backed securities this year.

In 2021 Basecorp has seen loan originations running more than 50% ahead of 2020, Moody said.

He said loan originations have increased markedly in November and December because borrowers are struggling to secure approval through banks under the new CCCFA criteria.

"These are in our view deals that would have been clearly bankable under the old regulations and credit policies of the banks."

"We understand from talking to a number of brokers in recent weeks that turnaround times have worsened significantly from October onwards, with this looking to be upwards of three to six weeks at present. Bank systems, and staff, are really struggling with the implementation of the new lending policies in response to the CCCFA, [and] both banks and a number of non-banks closed off early in late November/early December to new applications," Moody said.

In its annual non-bank Financial Institutions Performance Survey out this week, KPMG said non-bank lenders expect the CCCFA changes will see the cost of the lending process increase with this pushing up the interest rates they charge borrowers. Additionally the survey of 26 non-bank financial institutions suggests there'll be an increase in loan declines by 20% to 25%, and an increase in loan approval times by 25% to 50%, KPMG said.

Could NZ follow Aussie roll back?

Clark said as Minister of Commerce and Consumer Affairs, it's his responsibility to address concerns about lending practices, especially for those in vulnerable circumstances.

"This is why the Government has made a number of changes to the CCCFA. The Amendment Act and regulations require lenders to follow a robust process to determine borrowers’ income and expenses and will help to ensure that lending is affordable and suitable," said Clark.

"Lenders who act responsibly are already doing this and their borrowers will see less change as a result. The changes were developed after extensive engagement with the sector. I am confident the regulations will improve the quality and robustness of assessments carried out across the board."

"While the flow of consumer lending may be one part of the country’s economic recovery, this must not come at the cost of household borrowers being given debt they cannot pay back," Clark said.

So over time, will lenders and borrowers adjust to the new rules? Or could at least some of the new rules be rolled back?

Bell Gully points out that in Australia, which originally inspired the introduction of responsible lending rules in NZ, the Government is now looking to ease restrictions on lenders, warning against “unnecessary barriers to the flow of credit to households.” This is after Federal Treasurer Josh Frydenberg announced last year that the Government would "simplify the system by moving away from a 'one-size-fits-all' approach while at the same time strengthening consumer protections for those that need it."

"If the Australian government successfully pares back the regime, as proposed, it will leave a stark contrast to the detailed and prescriptive demands of New Zealand’s new framework," Bell Gully said.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

69 Comments

Faafoi in 2018 was referring to "loans" from loan sharks. Legislation 3 years in the making, now needlessly covers mortgages too... why? Of course some will say Labour, by doing the wrong thing has done the right thing. This govt wants to do the right thing but always screws up big time imo.

The amendments to the CCCFA 2003 are designed to protect people from themselves.

As we've seen, there are those among us who all too easily get themselves donkey-deep in debt - but that can have adverse effects on third parties......

Thus, I think the new provisions in the legislation are justified. Some people really do need protecting from their own worst excesses.

TTP

There could be a house price fall as a result of tight credit rules and limited finance. That would be a good thing

Can a similar framework be applied between the borrowings of a government today and the future generations that will have to pay it back?

Seems like a good idea to limit our propensity to live off the wealth of the young, as we've been doing far too much of. Definitely in housing.

In public sector it's not just debt but also deferred necessary maintenance/investment we're unwilling to pay for that leaves a cost for the young to pay.

What is the origin of the term 'donkey-deep'?

I am surprised kiwibank has no impaired loans,I thought they would have a lot of money out there on personal and debt consolidation loans.

Latitude (Australia) do the Kiwibank personal and DC loans

latitude,previously known as gemoney.I remeber reading about them when they listed.reckoned not for widows and orphans as they only do high risk loans.

Of course banks ought not trust what they’re told by borrowers. It’s as if the GFC never happened.

Bolton's making this out to be a way bigger issue than it is. It's just putting the spot light on some of the fudged numbers in mortgage applications that are used to make the deal work. The manipulation of income/expenses/liabilities will now be harder to get away with. No doubt he's fearful that he won't make as much profit going into 2022.

If he raises any points it's why don't non bank lenders fall under CCCFA?

The housing market has now completely seized up. So stay put, and forget about buying or selling for 6 months until this latest govt blunder is fixed up.

This 'blunder' has taken decades to create...it isnt going to be 'fixed' in 6 months

Well put. Ardern single-handedly tanking the housing market. Clearly none of the keyboard warriors commenting here are trying to buy or sell a house.

If people being honest about financial position, income and expenses is seizing the housing market up...perhaps some are finding fault in the wrong place and should look closer to home.

Given the taxpayer always seems to have to be there to bail out some expectation of honesty hardly seems cause for tantrums.

This is only a partial step towards the inevitable.

If we are looking to have a sustainable society (an unsustainable one doesn't appeal to me, just sayin) then most forward betting has to be 'off'. The banks/lenders will be forced to recognise this anyway, it will show up as unspportable propositions. Ultimately, there will be zero growth, so almost no ability to 'repay'. Beyond that, de-growth - so less ability to repay. Not just interest, but the borrowed 'sum' also.

Interesting times.

I think you are right pdk with regard to the inevitable. The path of consumerism versus finite resources, but, the concept of a "sustainable society", especially one reached by piecemeal measures such as credit control, is a tricky thing.

What we have at the moment is government and commerce 'fishing' in the general population with tasty bait of huge warm dry houses/flash new electric cars/latest hi-tech gizmos, etc, all in the name of growth, but with an overlay of increasingly complex legislation intended to somehow make the whole process "fair" & "responsible".

But fishing with catch sizes and all sorts of other constraints requires strong policing to catch the irresponsible. And yet policing seems to bit a lost art in NZ. And all we are left with is rapidly increasing state bureaucracies supposedly, (hopefully) providing the policing bit, but in reality just making society less & less "sustainable " through surcharges, increasing taxes, and delaying form filling which in the end hit the vulnerable the hardest.

Perhaps it's time to make mortgages non recourse. That'd help their consideration of the future.

I've always been of the view that a complex and convoluted flow diagram is a waste of space.

And that it often points to a process that is too convoluted.

Banks already ask for all your account and credit card statements, run credit checks, ask for pay slips, accounts etc. as part of applications.

Without employing the services of a proctologist it's hard to see what additional information government could require borrowers to provide to banks!

It’s been pretty loose though. We applied approximately six months ago as considering upgrading. Big 4 bank, Partner banks with them, I don’t.

They didn’t ask for any bank statements, just pay slips. They didn’t verify any documents. Didn’t check if I was on a permanent contract - I could have been leaving the next week for all they knew.

I accidentally put down that we spend $110 a week on food for family of four (it’s more like $300 as we have a dog and teens, which is still quite low). No one queried it. I probably underestimated in every area really, no questions asked.

They approved us for a mental amount of money, pretty much on the basis of equity in our current house. We are actually quite prudent with money and still would have struggled to repay it if any form of life emergency happened.

This was from one of the more conservative banks - we also went to Westpac, same story except they wanted to give us an extra $150k.

Yeah, we applied for a mortgage loan pre approval recently and didn’t have to provide more than 3 months of bank statements and pay slips to get pre-approval in just a few days. All done over the phone too. And the bank offered us way more money than I would consider prudent to have as debt. The flow chart seems to overly complicate the new rules.

Did they use that data though? Often banks have an internal model that limits the lowest expenditure levels per person.

To me stagflation seems like the largest risk. If CPI is higher than wages it reduces the ability of people to service lending because their free cashflow declines. It erodes the built-in safety margins banks have used. Then people can repay loans and end up in arrears or, eventually, defaulting.

Commercial banks are relying on the Reserve Bank to operate within inflation and employment targets.

Exactly. Everyone loves to say “banks stress test at x%”. But the question is how diligently they validate the inputs to those tests. Garbage in, garbage out

My experience with banks is similar to yours. They just accept whatever you tell them for expenses

"He goes on to say that NZ banks' are already conservative lenders, with low loan loss rates as highlighted by the Reserve Bank chart below."

Must have a different meaning for the word conservative ...when house prices are in excess of 10 x median household income.....and defaults dont tend to happen when the underwriter throws 10s of billions into the pot...not something thats able to be continued.

Can anyone of the bright people on interest.co.nz or the members posting comments do an analysis on how much percentage of the nz working population who pay their own cash afford a million dollar house while also living a decent life which will result in happy population as a whole?

You can forget the rising interest rates to dampen the housing market. Its the CCCFA that will change the market. Lending is alot harder now and banks are not lending as much as they use to which then creates a gap in what vendors expect and what people can actually buy. The amount of scrutiny that the banks are going through on your statements is somewhat crazy and I dont see a way forward that will improve unless CCCFA is reworked (which I wouldn't hold my breath with the current government). You can expect house prices to drop or people will just stay where they are and not sell. The Government are shooting themselves in the foot as new homes cannot be built because developers cannot get the finance they need in order to build them.

Govt. over reaction. Some changes were necessary but not to this detail.

As a broker myself I am more concerned about how the CCCFA is affecting lending to small business (SME) owners who require capital to grow their business. It is virtually impossible to get funding for a growing SME when using residential property as security and therefore SME's are forced to go to second tier lenders who charge considerably more for the lending. The flow on effects of that will mean more business failures, higher costs for all of us and more lives destroyed.

I 100% support tighter criteria on non bank lenders but the CCCFA has totally missed the mark and will likely see a rise in more predatory lending but those working outside of the rules

CCCFA only applies to personal lending, not business lending regardless of the type of security.

Many small business owners use their home equity indirectly to fund their businesses.

The government doesnt wasnt you owning your own business, they want the state to own and control everthing so they can borrow billions per year and pay you a living allowance. Property owners and investors are evil remember.

given how many billions the taxpayer poured into businesses, perhaps there should have been some equity passed to IRD

This just sounds like a rabid talkback caller

Yes MortgageBelt, I know.

If they accurately declare the purpose of the funds, they should be paying a higher premium. Given how tiny the lending for business secured against a resi property is (per RBNZ) I imagine there is already either a lot of lying by borrowers or a lot of 'dont tell me what it is for ' by lenders.

Yes that is correct but that isn't how the banks are viewing it (if there is residential property as security)

Which banks out of interest? That's definitely an extremely conservative view of the legislation.

All of them from what I have seen. I was chatting to a main bank commercial manager yesterday and he said they are applying CCCFA to all deals regardless, it is making things incredibly difficult for the staff as well as clients. There are many clients that fall outside of the CCCFA criteria but the banks are not recognising that.

As aside I have just had a deal declined by clients existing bank, small top up for renovations, clients are paying more than is required on existing lending and because of that the servicing doesnt work for the top up. The bank wont let them go back to the minimum repayments on the existing lending to make room for the top up. This is the sort of rubbish the CCCFA is throwing up

I dont own a house, but do own an SME, we have funding by way of an OD against the business assets (stock), currently at 8.3% plus all the usual fees. Welcome to the real world.

What you should be badgering on about to fix then is the risk weightings set by the RBNZ. These are set at much higher rates for businesses loans as opposed to home loans, which is WHY the banks prefer to lend for mortgages, not businesses. They are also why bank lending when broken down by loan type as a percentage of total loan book, mortgages have been screaming ahead for the past couple of decades to the detriment of all other loans. Which is partly to blame for the terrible productivity we have in this country...

Yep couldn't agree more!

Agreed. Risk weighting on residential mortgages might have initially made sense. But the lower capital requirements made the Banks willing to lend obscene amounts, creating a feedback loop of higher prices, more lending. Its now at the point where it has created systemic levels of risk as Banks are so over exposed to a single asset class that is massively above its long term price relative to key measures (income, rents etc).

Risk weighting for residential home loans should have increased as their total exposure to the asset class increased. As house prices deviated from long term trend (relative to income/rents) risk weightings should have increased. But no, we have a situation where the RBNZ implicitly guarantees the banks, and will step in to save them if anything goes wrong. So Banks are free to lend massive sums, with minimal capital, so maximum profit. All while the taxpayer will ultimately foot the bill.

If only there had been a similar event in the last 20 years where we could see how this would all play out that we could have learned from ... oh wait

Communism in action once again.

But then again what do you expect for a far left radical government hell bent on beating the country into serfdom.

Roughly 40% of the poulation are already in serfdom.

Communism ? best read up on that one, tends to be loosely thrown around when feeling threatened.

"Look! Communism!" has become the modern Godwins law.

"Look! Something I don't like! Communism!"

Having lived in a Communist country, you would be surprised how easy it is to get credit there, far easier than in NZ via "non bank lenders".

Yeah, the crying of communism at everything one doesn't like - and heck, the identification of Natbour (they're both so close) as something other than generic neoliberal - just makes folk look a bit unhinged.

I went through the diagram. Didn't seem onerous at all, pretty much what I would expect and what I have had to provide when applying for loans from banks in the past... it seems to me the people screaming at this must be those that have been knowingly fudging numbers to make loans go through...

I heard a statistic on (I think) the radio a few days ago, that 300,000 people in NZ are in negative equity.

With the rate that house prices have been increasing, I don’t imagine many, if any of those people are in negative equity for mortgages.

‘I’m sure these measures will have more than the intended impact on mortgage lending, and less than the desired impact on the loan sharks, payday lenders, vehicle finance companies and After-pay.

That's consumer debt, which is very different from housing mortgages.

Don't believe 300k in negative equity for 1 min.

I know someone who can't sell their home and downsize because they won't qualify for lending under this loanshark rule. Same bank, similar income, lots more equity, no dice. This is going to blow up on that idiot Faafoi in a big way next year.

Far reaching effects on for eg retirees who can’t sell their houses as Ardern has completely stopped the property market with a sledge hammer.

How is it that retirees can't sell their houses?

Example, met someone yesterday can't get buyer for big family home 1.85 not cos of lack of buyers but buyer can't get finance. So that downsizer can't build their new place.

Im sure they could sell their house, they just need to accept as more appropriate price.

Exactly.

Lower the price to meet the market.

They can't sell their house for an unrealistic price? Perhaps they could try a realistic one or an auction without reserve.

Is there a feeling they're entitled to a certain price?

The graph on on non-performing loans doesn't tell me much. Its interesting from a relative point of view between banks. I'd prefer to see non performing loans vs the banks (tier1?) capital as a %. This would give how close or far away a particular bank would be from their capital. !00% being all the capital consumed by the non performing loans. This would be of interest more so on residential property than all loans. Of course the bank may not have to use any of their capital as there'd be some residual value of the asset (residential property in this case) as in a rising market banks unlikely to loose anything.

The flowchart doesn't mention DTIs etc which shows me the banks that have extra measures in place have enough loans written for the year and are shutting up shop for the summer, not ideal

Actually, now that we have this law we probably don't need DTI ratios

Protecting people from being exploited by other people.

This is an absolute overkill.

With an average of 0.71% of non performing loans, NZ is way ahead in terms of loan performance compared to the US (1.07%), UK (1.22%) and Australia (1.11%).

The entire exercise is a farce and a distraction from real issues- it isn't about people taking loans, it's about people having better quality jobs in servicing those loans.

While the motivations behind the drama is questionable, you are right this is another spanner in the works to halt the country's economy.

But what if the non performing measure is simply due to the pyramid scheme? If borrowers limited in the amount they can borrow (which makes sense, because 10x income is nutso territory)... then this measure might change, right?

Excerpt from oneroof

"Consider this: just adding soy milk to your daily takeaway coffee - at a cost of 50c - will reduce your ability to purchase a home by $2,210. Not the daily coffee itself - that reduces your ability to purchase by over $20,000 - just adding soy milk. Think about how many small purchases we make regularly that we don’t even think about: our two streaming TV subscriptions instead of just the one we watch, that extra-fast broadband service that we don’t particularly need for scrolling our Facebook newsfeed. All of these will add up to significantly reduce applicants’ ability to afford a home in the near future."

Summary: accurate accounting for income and expenses may result in banks lending less than they might otherwise have.

I stopped eating for 3 weeks and and saved $650 this will increase my ability to purchase by $10.000.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.