By Elizabeth Kerr

Welcome back everyone. I had a nice warm and fuzzy column all lined up to get you refocused on your financial vision…but we can do warm and fuzzies together anytime.

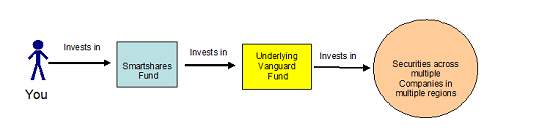

Instead this week I want to talk about Smartshares and the NZX again.

If you’ve been hiding under a rock for the past week make sure you read today’s’ column to the end because shit just got real!!!

No longer are we New Zealanders forced to invest our money machines in our own backyard, with a side helping of shares from Australian companies; we can aim for world domination for our dollars, because last week the NZX announced the introduction of 9 new INTERNATIONAL Exchange Traded Funds (ETFs).

That’s right, the NZX has partnered with Vanguard in America so we can get exposure to companies all over the world in a way the average New Zealand investor hasn’t been able to do so easily before.

Lets talk Vanguard

If you haven’t heard of Vanguard before then this is what you need to know. Jack Boggle, an insanely smart guy, figured out that to be a successful investor and make lots of money one doesn’t need to beat the market and get the best returns, one just needs to participate IN the market and the money will come - ie you don’t need to choose the winning horse in a race every time; you can just routinely bet a little on them all in each race and you will make some guaranteed money that way instead.

To add to his idea he looked around and saw the fund managers, even with their shiny shoes and expensive educations, couldn’t accurately pick the winning companies to invest in often enough over the long term to make all their clients wealthy, but were happy to keep charging them huge fees to keep trying.

So, Jack devised a low fee way of investing by using an index which gave average returns, but and here’s the clincher…did so consistently all the time, meaning the investor made just as much money over the long term. It is this theory which makes up the basis for the Smartshares products which I have written about before here and here.

The other really important thing to note is that no one really owns Vanguard per se. It exists solely as a vehicle for its investors to invest in these company indexes therefore can afford to keep the fees low as there are no profits required to prop up the company xmas party or payout performance bonuses to their staff.

How does it work?

If you’re interested and you haven’t already got a Smartshares account with the NZX then go online and click on Invest Now. There are already 10 Smartshares products to choose from within NZ and Australia. The additional nine international ones (to be available July 29) are listed in the table at the end of my column.

All you need to do is fill out the paperwork, invest an upfront $500 and a minimum $50 at least every time after that, and the NZX will go and invest it in the underlying Vanguard ETF fund of your choice from the nine offered. Your return will essentially mimic the same returns Vanguard gives all it’s investors in those funds, less NZX fees and tax of course

As you can see I’ve taken a few liberties and included some extra information in my table for you. Don’t blow an artery if I’ve got it wrong, you need to do your own due-diligence first of course, but I thought you’d be interested to know what the average returns over the last 5-15 years have been for some of these funds and what would be in your bank account if you’d invested US$10,000 with them at the time these funds were started. The first and most obvious is that all the funds have increased the initial deposit. But if you look at the actual graphs on the Vanguard website you can see there were some shaky times, and your knuckles might have turned white from holding yourself back from withdrawing your funds in fear.

Why Vanguard? Why didn’t the NZX just do it themselves?

Basically it comes down to scale. NZ is but a pimple on the globe and doesn’t have the money, or investor population to justify all of the work required to go and invest in 500 US based companies AND only charge a teeny tiny fee for the privilege. It just makes sense for the NZX to partner with someone who is already doing it well.

Why not just go direct to Vanguard yourself?

I have been reading the forums this week and I know some of you are still disappointed the fees aren’t as cheap as in the US and that you think you could save more money by investing directly through investment brokers in the US, and sending money via cheap foreign exchange vehicles. And yes, you could probably do that some of the time… but for the most part the power of these products is that it makes international investing accessible, cheap and easy for the average NZer putting away their loose change for an early retirement, and there is no faffing about with foreign exchange rates as that’s all taken care of for you. Other things to note are:

- If you were to go direct you would need a minimum of US$3000 to start your account, whereas with the NZX you just need the minimum NZ$500 and NZ$50 per deposit thereafter. Whoop whoop!

- You can call the NZX for support and not need to be awake in the middle of the night trying to get hold of someone in America to answer your questions.

- The dividends are paid out to you in $NZ.

- AND (this is important!) you have the option of reinvesting your dividends back into the fund again if you want to.

- No foreign exchange process that needs managing by you and a third party.

- As with all Smartshares products, it's all automatically and impartially invested according to a companies weighting within an index.

What are the fees then?

The very first time you make an investment into one of these international Smartshares products you will need to pay an Application Fee. This will be $30 for amounts less than NZ$20K or 0.2% for amounts over NZ$20k. This is a one-off fee. If you are intending to keep investing in your chosen fund at all thereafter you don’t have to pay it again.

The fee by the NZX for managing these funds for you is 0.30% for the US 500 Trust (USF) and 0.45% for the 8 others.

Who likes PIEs?

No I’m not talking pastry and mince I’m talking Portfolio Investment Entity. This means that the funds will be taxed at 28% flat. No questions asked.

What happens from here?

Well the Financial Markets Authority (FMA) has to give these new Smartshares products their big fat tick…and then it’s open for your business from tomorrow hopefully.

In closing

I’m coming dangerously close to endorsing a product here, but I’ll stop short by repeating the power of these funds is in the accessibility for average NZers who want their money to swim with bigger fish, but don’t have the time, inclination or aptitude to figure out how to do it all themselves. If you’re thinking of giving it a go – which fund would you choose?

|

Smartshares ETF Name |

What & Where |

Fees |

Fund Performance |

|

1. US 500 Trust (USF) |

Invests in Vanguard’s S&P 500 ETF, which aims to track 500 large securities listed on the NYSE or NASDAQ markets. (VOO)

|

Vanguard Fee:0.05%

NZD Fee: 0.30% |

$10,000 USD in June 2010 would be $20,888.83USD today.

An average return of 16.55% per year. (no data earlier than 2010) |

|

2. Europe Trust (EUF) |

Invests in Vanguard’s FTSE Europe ETF, which aims to track securities in developed European markets including Germany, Switzerland and the UK. (VGK)

|

Vanguard Fee:0.12%

NZD Fee: 0.45% |

$10,000 USD in June 2005 would be approx $17,440USD today.

An average return of 4.70% per year. |

|

3. Asia Pacific Trust (APA) |

Invests in Vanguard’s FTSE Pacific ETF, which aims to track securities in developed Asia Pacific markets, including Japan, Singapore and Australia. (VPL)

|

Vanguard Fee:0.12%

NZD Fee: 0.45% |

An average return of 5.34% per year over the last 10 years.

$10,000 USD in 2005 turned into $16,817USD today. |

|

4. Emerging Markets Trust (EMF) |

Invests in Vanguard’s FTSE Emerging Markets ETF, which aims to track securities from emerging markets including Brazil, China, and India. (VWO)

|

Vanguard Fee:0.15%

NZD Fee: 0.45% |

$10,000 USD in June 2005 would be approx $21,494USD today.

7.36% average per year. |

|

5. Total World Trust (TWF) |

(VT) Seeks to track the performance of the FTSE Global All Cap Index, which covers both well-established and still-developing markets. Has high potential for growth, but also high risk; share value may swing up and down more than U.S. or international stock funds. Only appropriate for long-term goals |

Vanguard Fee:0.17%

NZD Fee: 0.45% |

$10,000USD in 2008 will have turned into $14,365 or 5.3% average return per year.. |

|

6. US Large Value Trust (USV) |

(VTV) Seeks to track the performance of the CRSP US Large Cap Value Index, which measures the investment return of large-capitalization value stocks. Provides a convenient way to match the performance of many of the nation’s largest value stocks.

|

Vanguard Fee:0.09%

NZD Fee: 0.45% |

$10,000USD in 2004 would be $19,950USD today representing an average return of 7.36% per year since inception. |

|

7. US Large Growth Trust (USG) |

(VUG) Seeks to track the performance of the CRSP US Large Cap Growth Index. |

Vanguard Fee:0.09%

NZD Fee: 0.45 |

$10,000 USD in 2004 would be $23,980USD today. An average return of 8.06% per year. |

|

8. US Mid-Cap Trust (USM) |

(VO) Seeks to track the performance of the CRSP US Mid Cap Index, which measures the investment return of mid-capitalization stocks. Provides a convenient way to match the performance of a diversified group of medium-size companies. |

Vanguard Fee:0.09%

NZD Fee: 0.45% |

$10,000 USD in 2004 would be $24,475 USD today. An average of 9.67% since inception. |

|

9. US Small-Cap Trust (USS) |

(VB) Seeks to track the performance of the CRSP US Small Cap Index, which measures the investment return of small-capitalization stocks. Provides a convenient way to match the performance of a diversified group of small companies

|

Vanguard Fee:0.09%

NZD Fee: 0.45% |

$10,000 USD invested in 2004 would be $24,762USD today or 9.42% since inception.

|

*** use the codes in brackets and bold text - for example (VB) as immediately above - on the Vanguard.com website to see the Smartshares underlying Vanguard fund performance. It’s really quite interesting and you can compare different funds performance against each other.

29 Comments

''you can just routinely bet a little on them all in each race and you will make some guaranteed money that way instead. ''

You seriously thought about that phrasing did you? The word 'guaranteed' ?

well unless the nags all run backwards one is destined to cross the line.

Besides that though.... what fund would you choose?

"Renaissance Technologies Medallion Fund" if they let you buy in :P

"Two Sigma" is also decent.

Berkshire Hathaway has some managed funds that some kiwisaver providers buy into.

Generally funds with over 30% pa averaged over the last 20 - 30 years are likely to keep performing well.

Would that be the same fund that charges a 5% fixed fee plus a performance fee of 30% or more???

Yes. Their before fees return is usually over 75% pa. Looks like you have to be a RenTech employee to buy in these days. :(

Correction: Jack's name is actually John Clifton "Jack" Bogle .

tell me a little bit more about the pathetic liquidity of Smartshare funds in general and the exorbitant fees for index funds! These funds are also unhedged!!!!

Much rather just buy vanguard through ASX

Agree with this comment too from my own bitter experience with TNZ and WiNZ. NZX needs to provide some serious liquidity provision to make this attractive.

What's the story with the liquidity? I recently invested in Smartshares (FNZ) as it was the only ETF option for drip-feeding small amounts monthly. I struggle to deduce liquidity from the summary on ASB, though the depth and turnover don't appear to be very high. What constitutes decent liquidity, and is there a real issue selling when you need to?

Nice earner for NZX, that is pretty expensive passive management in my view when you consider Vanguard's actual cost.

Elizabeth, are you able to put up a poll to see what most people's picks are? I'd be quite interested to see the results, which would be clearer in poll-form rather than reading through individual comments.

Hmm... So we get everything except the one thing that has made Vanguard so successful: low fees. The proverbial baby has been tossed out with the proverbial wash water...

I thought this was quite exciting. I was surprised more has not been made of it since it was announced.

Seems to be drawing a lot of criticism though. For my mind I have never had any liquidity problems with FNZ. The fees don't seem unreasonable, especially given the accessibility, given that I am not (and most people aren't) in a position (or inclined) to be investing directly with Vanguard.

In the first instance I think S&P 500 will make a welcome addition to my portfolio.

NZX is effectively taking advantage of the fact that NZ market is seemingly too small for the likes of Vanguard to offer a retail product directly. End result is you end up paying too much for a very cheap, unsophisticated product and without the liquidity support, in my view.

Does someone else offer a regular contribution into an S&P ETF for a lower fee? That is where I see the real value in Smartshares. It allows for some with a small capital base ($500 + $50/month) to build a diversified portfolio that would be otherwise impossible.

Is there an alternative? ... or even a cheaper alternative? Lets see how many people actually make an investment and then discuss again. People have been asking for products like this for a long time.... but i wonder how many will actually use them.

Elizabeth, thanks for making learning about this stuff more accessible for beginners like myself. I have recently sold a rental property in Auckland and have some money to invest. I'm not loving the rates that the banks offer me for a term deposit or a savings account but I will keep some of my money there as I'm relatively risk adverse. Would you suggest that investing in one or two of these funds (possibly including an NZ one) would be a good way to get started? Thanks.

Hi Biologist. I'm not a financial adviser so i can't really tell you what to do. I could tell you what I would do if it was me... and this could be helpful to discuss with a qualified financial adviser ... or you could ignore it completely. Why don't you email me on elizabeth.kerr@interest.co.nz

Can some one quantify these liquidity problems? is it an issue for someone who might want to occasionally sell 2 - 3k worth?

Or is it only a problem if you are dealing with 10's/100's of thousands?

SmartFONZ isn't too bad, but SmartTENZ and SmartMOZY seem very very thin, potentially a big spread for even a small parcel.

The process for getting the money back again is the same as with ordinary Smartshares. You need to use broker (which may cost a small fee) and they will sell at the rate of the day, and you can expect it in your account in approximately 3 days. Has this differed from anyone's experience? What are the liquidity issues some of you are concerned about?

I think the effects of poor liquidity I would be concerned about are larger bid/ask spreads leading to higher trading costs, the hassle of using limit orders rather than market orders and the potential for greater divergence between the price of a fund and the value of its underlying shares.

PIEs are taxed at your prescribed investor rate (PIR). If you earn less than $70k your PIR will be less than 28%.

http://www.ird.govt.nz/toii/pir/workout/toii-pir-workout-how.html

These ETFS (VOO, VB etc.) appear to be domiciled in the US. If that is the case, non-US investors will likely be liable for US estate taxes on their holdings if they exceed US$60K at the time of death. See the discussion here:

http://andrewhallam.com/2014/01/expat-index-investors-should-duck-u-s-e…

There are some products on the ASX that are purposefully domiciled in Australia to avoid this US tax grab (e.g. NDQ from betashares). http://betashares.com.au/products/name/nasdaq-100-etf/#each-overview

I wonder if Smartshares/NZX has considered this issue?

When I first read about these funds' introduction, I was excited too. I'm a big fan of Vanguard's low fees and non-profit philosophy. For drip feeding investments, the NZX versions might be a good option. For larger one-time buy and hold investments, I'm not so sure. After studying the offer documents, I don't think I'll be selling my direct investments in US domiciled Vanguard ETFs to buy any of these NZX Smartshare wrapped versions. First, I have some tax questions to figure out.

These NZX SmartShare wrapped Vanguard ETFs appear to be listed PIEs taxed only at the 28% rate. Great for some, but for lower rate taxpayers, is the excess tax paid able to be taken as a credit?

Unlike an individual or family trust holding overseas investments directly (and taxed under the FIF rules), it appears these listed PIE Smartshares funds cannot choose the CV method to calculate income. Couldn't this result in more tax paid in years when the total return is less than 5% for the SmartShares fund vs directly holding the foreign ETF?

In "Other Tax Considerations", I noticed that the Smartshares fund holders may be entitled to tax credits for US withholding tax, but "No credit will be available to the Smartshares Funds in respect of taxes withheld at source on distributions received by the Underlying Fund." I interpret this to mean non-US foreign taxes withheld from dividends received by the Vanguard funds. I'm pretty sure I get to use these credits for Vanguard international equity funds I hold directly. Why can't SmartShares forward them? Are they being used to satisfy the 28% PIE tax?

Any chance the existing Kiwisaver funds will start investing in these ETFs ? At least the Growth Funds ?

Do you know if it's better to buy the NZX Vanguard ETF's through Smartshares or Super Life? Super Life say that their fee's are lower than Smartshares but I'm not sure?

I have the same question. Not sure whether to go with SuperLife (which I think has lower fees) or SmartShares (which seems more popular/known about).

Superlife is investing EFT via Kiwisaver. I didnt investigate the fees between them. But it is obvious con is you wont see the real cash in Superlife until 65 or dump out of the kiwisaver prematurely.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.