By Jenée Tibshraeny

Competition in the motor vehicle finance industry is hot, as New Zealand firms and households are buying record numbers of vehicles.

The Motor Industry Association (MIA) reports 12,100 new passenger and commercial cars were registered in March, making it the strongest March result since 1984.

MIA chief executive, David Crawford, attributes the growth to strong net immigration, competitive pricing, and end of financial year deals.

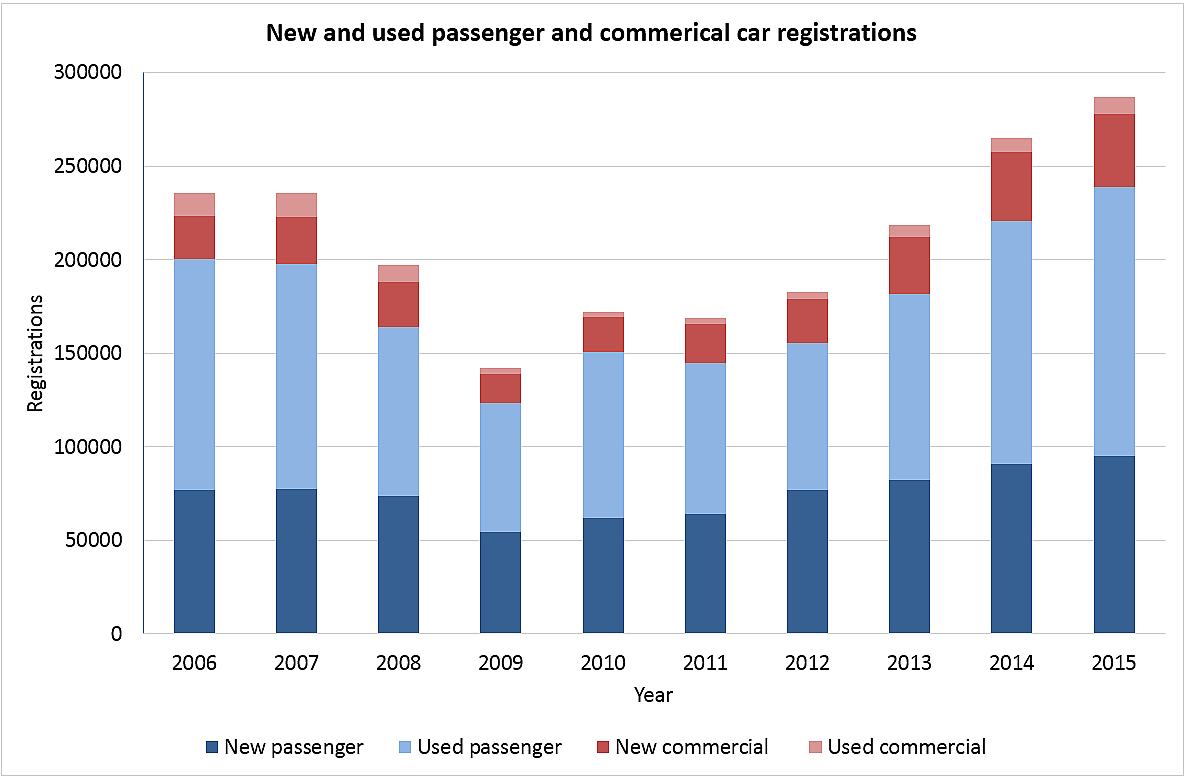

The number of new and used passenger and commercial cars registered in New Zealand has been steadily tracking upward since the end of the Global Finance Crisis. Registrations increased by 20% from 2012 to 2013, 21% from 2013 to 2014, and 8% from 2014 to 2015.

Growth has come from both passenger and commercial vehicle sales.

The chief executive of UDC Finance (a wholly owned subsidiary of ANZ), Wayne Percival, says “Traditional mums and dads are buying new vehicles again… Cars are really good value; people are changing cars because the economy is going well; money is quite cheap.”

KPMG’s head of financial services, John Kensington, says much of the growth also stems from car rental businesses and taxi companies, which are expanding and upgrading their fleets to cater to the influx of tourists to New Zealand.

“It’s Toyotas, it’s Nissans, it’s Holden; it’s those sorts of vehicles that are contributing towards the big growth in the sales,” he says.

To what extent is the spike in car sales causing debt to spike?

So how much debt are New Zealand firms and households clocking up to buy these vehicles?

This is difficult to quantify as it would require all the banks, building societies, finance companies and peer-to-peer lenders separating their motor finance figures out from the rest of their lending, and making these figures publically available.

However we can make some estimates using figures from a sample of finance companies that specialise in motor finance: BMW Financial Services NZ, Mercedes-Benz Financial Services NZ, Motor Trade Finance and Toyota Finance NZ.

Together the four motor finance companies have grown their net loans and advanced from a total of $1.64 billion in 2011/12 to $2.01 billion in 2014/15. That's an increase of about 23%.

They’ve also grown their net assets from $271.6 million to $279.6 million over this time, just 3%.

And collectively, their net profit after tax has eased back slightly from $38.5 million in 2011/12 to $37.2 million in 2014/15. That's a fall of 3%.

While we obviously cannot draw a complete picture from this sample of the motor finance market, what we can see is that while finance companies are lending more, they aren’t necessarily making more money.

Why isn’t profit growth shadowing lending growth?

KPMG’s Kensington says car manufacturers are putting retailers under pressure to reach higher sales targets. They’re pushing more vehicles into the market, which is seeing car dealers drop prices just to keep stock going out of the door.

Dealers’ margins are also being depressed as a large portion of their sales growth is coming from the rental sector, which receives discounted prices and often deals with wholesalers directly.

Making a lower margin on car sales, Kensington says dealers are relying on the finance, insurance, servicing and parts sides of their businesses to bump up their profits.

“By the time dealers put a set of mags on the car; by the time they finance the buyer – even if it is only at 2% or 3% – they get the income a different way. And if they don’t do it, someone else will,” Kensington says.

How much bargaining power do borrowers have in this competitive low interest rate environment?

Commenting on the level of competition in the motor vehicle finance industry, the executive director of the Financial Services Federation, Lyn McMorran, admits, “Car dealers have a vested interest in moving the motor vehicle and financing it. There are some good deals out there.”

She says the positive credit reporting that’s been available for the last couple of years – the availability of more detailed credit information on consumers between different agencies – is going to give people with good credit histories more bargaining power and spur them to seek better deals.

“If you’ve got a really clean credit history, you’d expect to get a better rate than someone’s who’s had the odd 30 days where they’ve been in arrears,” McMorran says.

“As consumers become more aware of the value of their good credit histories, it will drive more demand for better deals.

“People don’t realise the powerful position they’re in if they meet all their commitments on time.”

What are finance companies doing to win customers as competition heats up?

Commenting on the level of bargaining power borrowers have, UDC’s Percival says, “The price of the car, the accessories of the car, the whole thing gets packaged up; it’s got to be competitive.

“A customer can go to a certain dealer in Wellington for example, or buy that same car anywhere in New Zealand, so the whole package needs to be put together well. The interest rate is only one component.”

UDC, a plant, equipment and vehicle lender, has been on a strong profit run over the past few years, featuring record annual net profit after tax of $57 million, a rise of 11%, in the year to September 30, 2015.

Speaking last November after UDC had posted its annual results, Percival said UDC had continued performing strongly into the new financial year, with October and November both delivering more than $100 million of new lending per month. Key growth areas were motor vehicles, construction and road freight, Percival said then.

In terms of car finance, he says UDC’s key success is around making the point of sale attractive.

“Yes, it’s got to be a competitive rate, but if you make the buying and financing process quick and easy for the customer, they’ve got no need to go anywhere else.”

Percival says having one place for buying a car and getting finance takes away the hassle of having to make trips to a bank or building society as well.

KPMG’s Kensington agrees: “If it’s finance offered on the yard, and it’s quicker and easier to approve than going back to the bank, people might take it from the yard or the yard’s finance company.”

How are banks’ attitudes to motor vehicle finance changing?

Pitting finance companies against banks when it comes to motor vehicle finance, Kensington says generally speaking, “Everyone wants to grow their loan book, because the bigger your loan book, the more margin you make.”

However he notes banks last year started distancing themselves from motor vehicle finance, opting to pass second tier borrowers on to the finance companies they fund.

He says the competition he saw among banks for finance company type car loans in 2014 has dropped off, as banks are less frequently trying to get their customers to add car loans on to their mortgages. This way banks don’t muck up their mortgage lending.

“If you add a car to the value of a mortgage, you start to use up any head room in the mortgage and if it goes above 80%, you’ve got all the 80% [loan-to-value ratio] lending rules to comply with. And that’s a decreasing asset,” he explains.

“Whereas if you spend $100,000 on a house, in theory you probably add $120,000 to the value of the house so you may not breach the 80% rule.”

Kensington says passing motor vehicle lending onto banks’ finance companies also puts capital between the bank and the ultimate borrower.

If the bank lends to the customer, it takes on the risk of the customer. However, if the bank lends to the finance company, which lends to the customer, the finance company’s capital acts as a buffer zone protecting the bank from taking on all the risk.

Kensington essentially says banks are distancing themselves from riskier, less profitable borrowers.

“Banks are really good at raising and lending enormous amounts of money.

“Once they start going out of their traditional markets [IE mortgages], into areas like car and personal finance where there’s a greater level of default, the banks aren’t as well set up to cater for these customers as the finance companies are.”

He says the average mortgage goes through 90% of its life without a glitch, yet car and personal loans take a lot more managing.

Commenting on Kensington’s observation about banks’ changes of attitudes, Percival says ANZ may refer business to UDC depending on the type of customer.

What impact is P2P lending having on the motor vehicle finance market?

Borrowers are also turning to peer-to-peer (P2P) lenders for motor vehicle finance.

Squirrel Money says a large portion of the finance it provides is for car purchases, while Harmoney says cars are the fifth most common reason borrowers seek a loan.

Kensington says borrowers are attracted to the convenience of going online to borrower, rather than going to a bank.

“P2P lending is more about the “now generation” wanting to have everything happen right now.”

While P2P lenders claim the quality of their borrowers is high, Kensington says, “This will never be known until there’s another downturn”.

“That’ll be the only time we truly test that P2P modelling of what a person’s credit rating and interest rate should be. Until then, while we’re in near high employment, near record low interest rates, it would be hard for P2P lending not to work.”

How risky is this high level of debt being clocked up?

The Financial Services Federation’s McMorran says, “Generally speaking our members are still pretty happy about the amount that they’re lending.

“While they’ve been lending more, it’s not at the expense of the quality of the lending. They’re not seeing a sharp increase in the amount of arrears. It’s a good place to be at the moment.

The figures tell a similar story.

The average ‘impaired asset expense: average loans and advances’ between BMW Financial Services NZ, Mercedes-Benz Financial Services NZ, Motor Trade Finance and Toyota Finance NZ, has improved from 0.47% to 0.35% from 2011/12 to 2014/15.

Percival says UDC’s improved the quality of its loan book off the back of it focussing on providing finance for those buying new rather than used cars.

“We do a lot of used car business, but there have been a number of other players come into that market, and we’ve sort of let them have that. We know the history of that market. We know where the quality lies. We’re very comfortable with where our quality’s lying.”

Kensington explains that in the five, six or seven years since the GFC, the quality of lenders’ loan books has improved. Bad loans have been cleared as borrowers have paid their debts, and there have been a run of mortgagee sales.

“The quality of the book is still very good, but it could tilt either way. If our dollar dropped, and dairy prices suddenly went up again, and our other exports doing well continue to do so, you could see a bit of a boom in NZ; you could see the areas that are causing some concern for banks around their lending go away. Conversely, you could see the opposite.”

Does it really make sense borrowing to buy a depreciating asset?

While it’s important to ensure responsible lending, Kensington is also an advocate for responsible borrowing.

“Any sort of money spent on consumable, or partly consumable items, in this environment… you’d have a bit of a worry about. It is a time for people to still be prudent.”

McMorran says borrowers should think twice before taking the easy option of adding their car loans to their low interest mortgages, as they’ll end up spreading the debt over a longer period of time, clocking up more interest in the long run.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

14 Comments

I purchased a new Ford Ranger last year May, and when negotiating a final price after playing off different dealers, the outfit I bought from tried to get me to finance it. their push was quite hard so I looked at the terms - 9% interest stood out when all other interest rates were 5 or lower. The finance companies should be raking it in.

What are some examples of the car finance interest rates?

12 to 17%, unless it's a new car deal.

However he notes banks last year started distancing themselves from motor vehicle finance, opting to pass second tier borrowers on to the finance companies they fund.

Phew, that's a relief for bank depositors - other than the fact it's a given financing house improvements all but guarantees an instant 20% return. Who needs a lottery ticket or a business venture? 80% LVR and a stupid, compliant domestic bank funding base and it's a wheeze - if the finance company rolls over, cut it loose via bankruptcy, given the collateral is decreasing (probably depreciating). Too easy.

Crazy to borrow money for a car unless absolutely vital, especially a new one.

I had assumed that rich people who buy new BMW would be able to pay cash, but I discovered the majority borrow for these vertically depreciating assets.

The Govt of course is effectively borrowing (from the taxpayer) 100% for it's BMW fleet.

And it won't pay it back...

Pay it back...what a joke...never has, never will, will be the death of us all.

These gouging heartless monsters in their Chauffeur driven German tanks, playing follow my leader....way too many of em...way too overpaid, over indulged and long over due for an over haul....and an oil and grease change.

A wee percentage at a time. But really taking the p--s....we could replace em with robots and automate their stupidity....would save a lot in the long run.

Nothing surer than death and taxes...not sure which will last the longest....them or us. Some have been sucking on the taxpayer for so long, they have almost withered and died in office.

(But still they hang on for their automated pay-rises and pensions)

Only some people, the chosen few can avoid the burden of State taxes, others, will pay, until the day they die.

And cost us all all a packet.....and we get to pay for our own deals....one way or another..

Cars don't get me started.....spent out...and still paying others for the joy ride...of a lifetime.

MoM (East Coast US analyst who has been pretty much on the nail this last decade) categorises a lot of US automobile lending as sub-prime, and there's no reason to think that Godzone is much different.

http://maxedoutmama.blogspot.com/2016/04/comments-possibly-ill-advised…

Personally I have spent a lot of money of cars but have no regrets as they are one of my passions. Life is too short not to follow ones passions. The money spent has not affected how I live in retirement. In Auckland especially the Jones have a lot to answer for. So many people borrowing for cars or leasing them just to keep up the image. I hope they are stashing it away for retirement as that stage in life will be long for many.

Not a finance comment, but related, if a third of these new registrations end up on Auckland roads,when will 5 a.m to 9 p.m Grid lock occur? 1/4 million more cars on Auckland roads within 4 years? Simple math, even allowing for 5%vehicles retired each year,

We used bestcar to help us negotiate a great price (more than I could have possibly done) for our VW, however after reading this I wish I had negotiated harder with VW on the finance rate - didn't really think I had a option on that one!

Thousands of people are putting a new car "on the house" with an interest only mortgage at 4.5%. The house as an ATM now back in vogue eh!

When it blows I just wish it was only limited to the fools involved. meanwhile here is me looking at awful returns so throwing it all onto the mortgage as fast as I can.

Quite easy to get a big discount on a VW - they are having a tough time with year on year sales well down since the controversy over emissions.

Whatever you pay for Eurotrash, V W in particular, is just the deposit

The figures that are more interesting are cars financed for 5-7 years. A 3 year loan is not a big deal it's the longer terms where people end up trapped in loans that are a problem.

How many people have a car loan with a large payment but live from pay to pay? What happens when they can't afford to make the payment? How many suckers are getting all the extras because they are just borrowing the money anyway?

There are people who buy cars on their credit card and balance transfer to a 0% card that they repay within a year. I suspect there is a lot more car financing going on than what is evident. I only really want to know how many crappy loans are out there.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.