Inequality is on the rise in New Zealand.

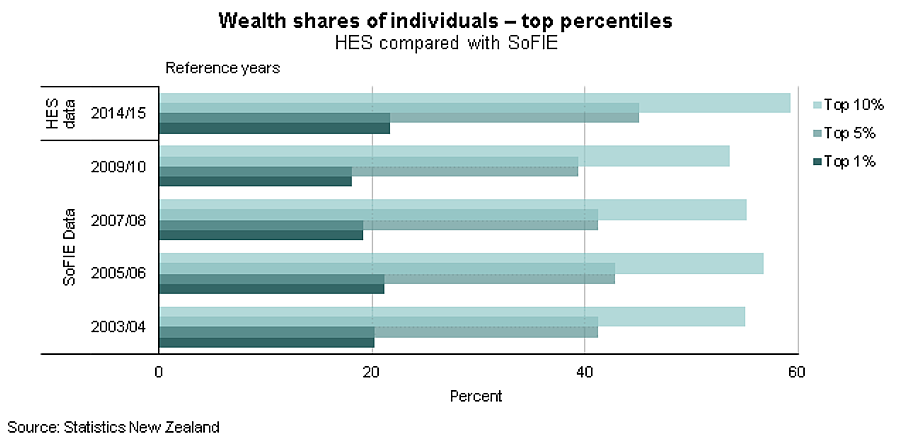

Around 10% of individuals accounted for 60% of the country’s net worth last year, up from an average of 55% between 2003 and 2010, according to new figures released by Statistics New Zealand.

The median net worth of individuals was $87,000 in the year to June 2015. The median value of an individual's assets was $160,000, while the median value of their liabilities was $28,000.

At $114,000, Europeans had a higher net worth than other ethnic groups; Maori $23,000, Pacific $12,000, Asian $33,000.

This graph shows how the concentration of wealth held by the top 1%, 5% and 10% of individuals has gradually increased over the past decade.

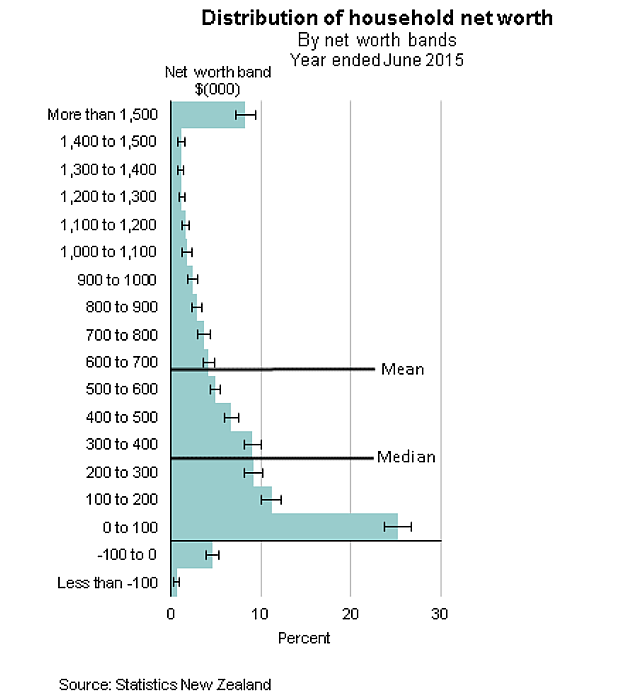

Looking at households, as opposed to individuals, Stats NZ reports the average New Zealand household was worth $289,000 in the year to June 2015. The median value of household assets was $400,000, and the median value of liabilities was $51,000.

Yet once again this wealth was not evenly distributed, with the top 10% of households accounting for around half of total wealth. In contrast, the bottom 40% held 3% of total wealth.

Five percent of households had negative net worth, and the largest proportion of households (25%) had a net worth between zero and $100,000. At the higher end of the distribution, 8% of households had a net worth above $1.5 million.

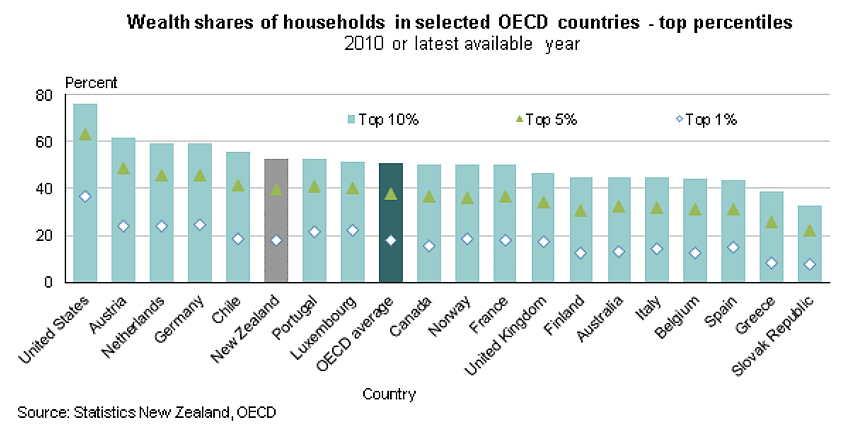

Stats NZ reports the distribution of New Zealand's wealth is on par with that of other OECD countries.

“The top 1% of New Zealand households had 18% of total net worth – the same as the OECD average, but slightly higher than in Australia (where the top 1% has 13% of net worth),” it says.

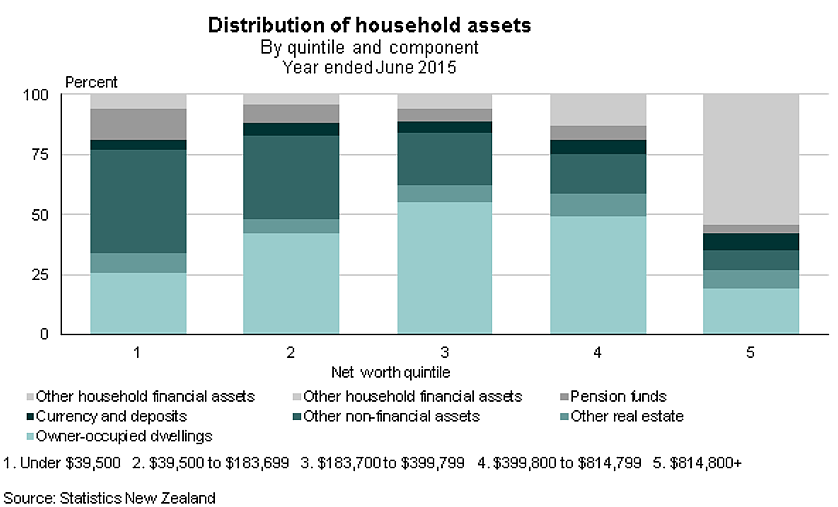

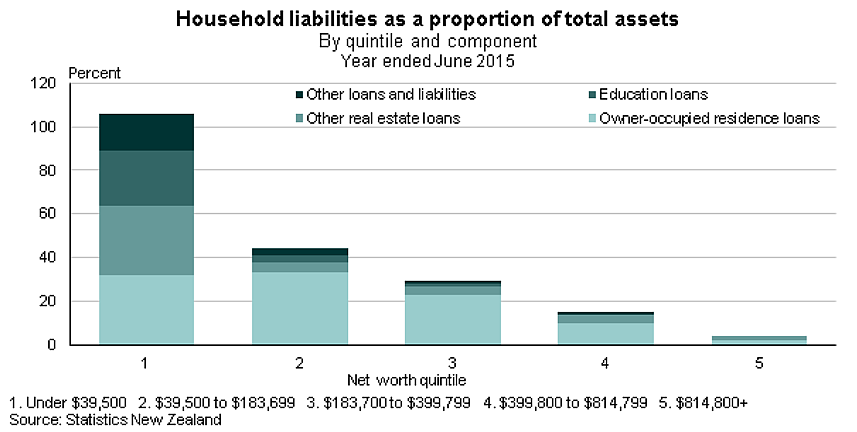

Looking at the distribution of assets, it’s interesting to note wealthier households had much greater shares of their assets held in financial assets (cash and deposits, shares, equity in trusts and businesses and other financial investments).

“Approximately two-thirds of household assets for the top quintile were accounted for by financial assets; for other quintiles, the figure was around 20%.” Stats NZ says.

“The difference reflects the ability of the higher quintile households to invest in financial assets, due to their lack of debt (relative to lower quintile households), as shown in the graph below.”

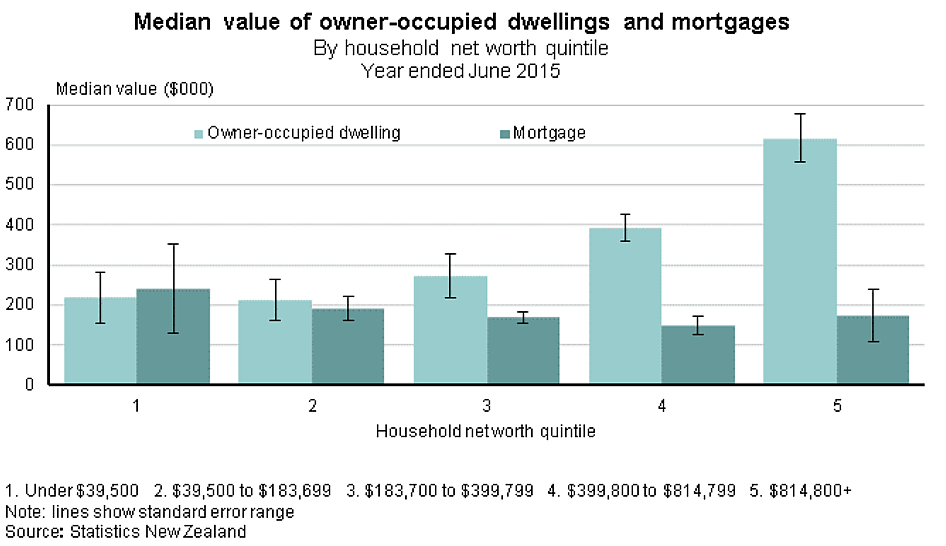

The most-valuable asset held by Kiwi households was the house they lived in, which made up 59% of all non-financial assets. One in two households owned the house they lived in. Housing also contributed the most to debt levels – mortgage debt was over 60% of household liabilities.

“Nearly three in five New Zealand households living in their own home had a mortgage, with a median mortgage value of $172,000,” says Stats NZ.

"Overall, for every $1 of assets they have, New Zealand households have 12 cents of debt.”

Yet as expected, households in the lowest net worth quintile had a lot more debt on their houses than those in the higher quintiles.

Stats NZ reports 14% of New Zealand households own real estate other than the home they live in (holiday homes, timeshares, commercial and residential investment properties, land). The median mortgage for these properties was $167,000, with the median value of these being $285,000.

Stats NZ has also looked into New Zealanders' use of trusts and concludes about 12% of owner-occupied dwellings were held by trusts.

The proportion of New Zealand households living in owner-occupied dwellings increases to 59% (from 51%) when including dwellings owned by a trust.

Furthermore, Stats NZ says a fifth of New Zealand households had involvement in a trust, in one form or another last year.

"For households with assets in their trust, the median value of those assets was around $700,000. For households that had liabilities in their trust, the median value of those liabilities was close to $300,000. These values are quite large as a big proportion of trust assets and liabilities relate to farms and owner-occupied dwellings," it says.

21 Comments

why the jump from 2010 to 2014? Do the years in between show the data wobbling around and decreasing at points ( somewhat like it does from 2005 - 2009 )?

Good point Sadr001. I have just spoken to a Diane Ramsay from Stats NZ who confirms the department doesn't have any other historical data, collected using a similar method, that its 2015 data can be compared with. The best it has is the Survey of Family, Income and Employment figures from 2003-2010, which I have included in the story. Stats NZ confirms it will repeat the same survey it has done to produce the figures published in today's report, every three years, to create a time series for comparison. There are of course other measures of inequality that can be derived from comparing incomes for example.

Thanks Jenee, really useful

Given this dynamic has been occurring throughout the world, especially in those countries pursuing neoliberal fiscal and monetary policies, it is hardly surprising Trumpism and Brexit have occurred. From a position of high private debt even 9 years ago, governments and central banks have mostly followed contractionary fiscal policies, but monetarily have quadrupled down on debt. Fix a loan with a much bigger loan. The world certainly required monetary expansion to get out of the GFC, no doubt including slightly lower interest rates. However the authorities did little to increase consumption, or inflation, or wages, or infrastructure spending (which would likely have lifted all three). More direct monetary funding of fiscal deficits would have fixed all three, without actually the need for such huge monetary expansion. The argument against this is usually that it is somehow hard to turn off. Yet central banks are now finding that turning ultra low interest rates off is much much harder. The asset bubbles are already fully inflated, and will do damage when they are popped. So they feel stuck in their low interest rates.

The only way out I see for the world is a good dose of helicopter money, followed a year or two later by gradual interest rate rises.

The world needs to inflate away some debt through increased net wages and consumption. Or you can blow up asset bubbles and just make everyone poorer. The Christchurch earthquakes mitigated the economic effects in New Zealand somewhat, by bringing in $20 billion of insurance money, but that effect has likely finished. We all know our housing issues, where the inequality noted in this article is part of the story.

My points above suggest one way out of the problem. Or we will have our own version of Trumpism/ Brexit.

But no amount of fiscal playing round with helicopter money changes the REAL physical energy & resource limits/problems we are now hitting. When our energy supply is disrupted, any faith in money will evaporate.

Current very low commodity and energy prices demonstrate we have en economic issue, and not resource constraints, at least in the developed countries. (High population growth, low income countries in the Middle East and Africa are under real stress, but that is a different issue, other than the spillover emigration effects). If and when fossil fuels supply does peak, and then reduce significantly, there may be an economic issue. Separately I understand global warming is a real concern, but I also understand there is enough sunlight hitting the planet to allow us to move away from fossil fuels. Indeed, one of the great economic opportunities/necessities of the next 30 years will be making that move.

You have obviously not been keeping your eye on the ball.

http://crudeoilpeak.info/world-outside-us-and-canada-doesnt-produce-mor…

http://crudeoilpeak.info/peak-oil-in-asia-and-oil-import-trends-part-2

Energy prices have very little correspondence with realities of peak oil..

As for 'enough sunlight hitting the planet to allow us to move away from fossil fuels'; this has been discussed at great length previously. It is a myth insofar as no systems exist to collect and utilise that energy at a rate to make any significant difference and no such systems can be constructed. The 'promise' of solar has been promoted since the 1960s and remains unfulfilled. Rather like the 'promise' of nuclear generated electricity 'so cheap it won't be worth metering it'.

Meanwhile, the meltdown of the planet continues to accelerate:

https://ads.nipr.ac.jp/vishop/vishop-extent.html

By the way, we don't have '30 years'. The crunch will come before 2020.

totally agree - we are within 3 years of the crunch, 5 years max.

I don't see the crunch coming that fast short of an asteroid hitting the earth. While its inevitable its all going to hit the fan sooner or later, the earth just cannot maintain the population growth and fossil fuels just have to run out eventually I give it till 2050. Still if you look at some people, they are living like its all going to end in 2020, perhaps I should join the party.

Stephen - you are right that we have an economic issue - it is that we cant keep adding debt to generate demand - and demand is what gets Oil out of the ground and commodity prices up.

The resource issue is that we have run out of cheap to produce Oil and new resources for easy growth, so this weakens demand.

Unfortunately Solar is a red herring in terms of a substitute for fossil fuel - too expensive and inflexible.

The sun supports solar, hydro and wind. Price signals, when fossil fuels do become more expensive, will encourage much more rapid use of these technologies. Fossil fuels won't go to zero overnight. I'm reluctant to ask what your "crunch" looks like, as I suspect David doesn't want to start another "armageddon is coming" thread. However it's a wet day in Auckland.

the trouble is Fossil fuel price rises dampens growth ... which is what we cant generate! Its a reinforcing deflationary spiral. Its actually the financial side that crashes through ever falling affordability of more debt ... result just like Solid Energy - the coal is still sitting there on the West Coast, but its just not viable to get it out (and certainly not on scale to keep the system running). The IEA was warning that new exploration was severely comprised back when Oil was at $80 a barrel ...

As for the crunch, take away fossil fuel and you take away trade and food. Countries like Saudi had a population more like 1 million than their current 30 ; pre the industrial ability to import food. The UK imports a third of its food and relies on oil/gas for producing other rest etc ... Its ugly.

My point being that if you cant get growth when we have fossil fuels, expecting growth when we try to "replace" them with less efficient, less transportable, more expensive and intermittent energy sources is obviously hopeful to say the least.

I don't agree with you on Solar, the really advanced countries like Germany are well on the way to using renewable s. I was quite shocked (pardon the pun) to see how advanced they are with electric. We have not even started in this country relative to Germany and we have the space for wind generation and solar panels with better sunlight. The price of the solar panels has crashed over the last few years and I'm seriously considering putting 4 on my roof for just the hot water as a start. The Sun and the wind are going to be the only choices in the future short of some miracle breakthrough in energy generation.

Germany might be well advanced, but its not going to pay off ...

http://www.wsj.com/articles/germanys-expensive-gamble-on-renewable-ener…

One comment "“One government estimate projects the Energiewende by 2040 to cost up to €1 trillion, or about $1.4 trillion, or almost half Germany’s GDP and nearly as much as the country spent on the reunification of East and West Germany"

And the kicker .. Solar panels are produced by burning tonnes of dirty Chinese coal ...

if its any consolation the statement "...wealthier households had much greater shares of their assets held in financial assets..." tells us they are as impoverished as anyone when SHTF. ie when the financial system collapses (for good). Because most of these so called assets are reliant on future income streams which just arent there - because the net energy to deliver it wont be there. Collectively we are way past a possible unwind of the Ponzi.

Interesting, thanks

"The median net worth of individuals was $87,000 in the year to June 2015. The median value of an individual's assets was $160,000, while the median value of their liabilities was $28,000."

Shouldn't the net worth equal the assets less the liabilities?

That would be true if the averages were taken. In this case it seems the populations of asset holders, liability owers, and net worth were separately considered, and the median taken for each one. If one population has a longer or shorter tail, and or a shallower or steeper peak, then you will end up with the medians being quite different people.

What about demographics? surely an aging population will be richer?

It's normal for young to be poor and old to be rich.

And we have a lot of hard working baby boomers.

All the above comments reflect the common mistake most make - too much focus on technical detail while the problem is fundamental. The root problem is the "free market" economy of Milton Friedman's economic theories. The "Free" means free of regulation, but the truth is they are not free of manipulation. The big players manipulate and control the markets, stifling and influencing any potential competition. Governments have bought into this. What is required is balanced Government regulation to put the brakes on greed.

The alternative is more of what is occuring - jobs exported to areas of low labour cost, those remaining reduced to low paid, part time (our Government refers to it as job flexibility), real incomes diminishing, disposable incomes dropping faster, equity gap increasing. In other words big business is re-inventing slavery, abetted by Government making rules that limits the power of workers and putting all the power in the hands of the business.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.