The government maintains there’s less urgency for it to help housing developers secure finance than there was a few months ago when there were fears of a credit crunch.

It’s delaying, by an undetermined length of time, implementing a pre-election plan to underwrite “stalled or at-risk” housing developments.

“We’re not putting it on hold. What we’re doing is continuing to work through to make sure the criteria fit the current circumstances that we’re facing,” Housing Minister Megan Woods told interest.co.nz.

In August Woods announced developers would be able to apply for a government underwrite or direct investment to help get their projects off the ground. She was worried Covid-19 would see banks become risk-averse and become a roadblock to getting houses built.

A 'Residential Development Response Fund' was to be set up using $250 million of funding redirected from KiwiBuild and $100 million from the Covid-19 Response and Recovery Fund.

Woods expected Kāinga Ora would start receiving applications from developers in the first half of November.

Asked on Tuesday how things were progressing and when eligibility criteria would be released, Woods said: “That is a piece of work that we’re continuing to work through with the sector. When we first announced it, we thought it was going to have to be used a whole lot sooner than it looks like it will be.

“There were concerns, in the immediate Covid lockdown period, that we’d see what happened post-GFC [2008 Global Financial Crisis], where we saw a collapse of construction - particularly construction of affordable housing.”

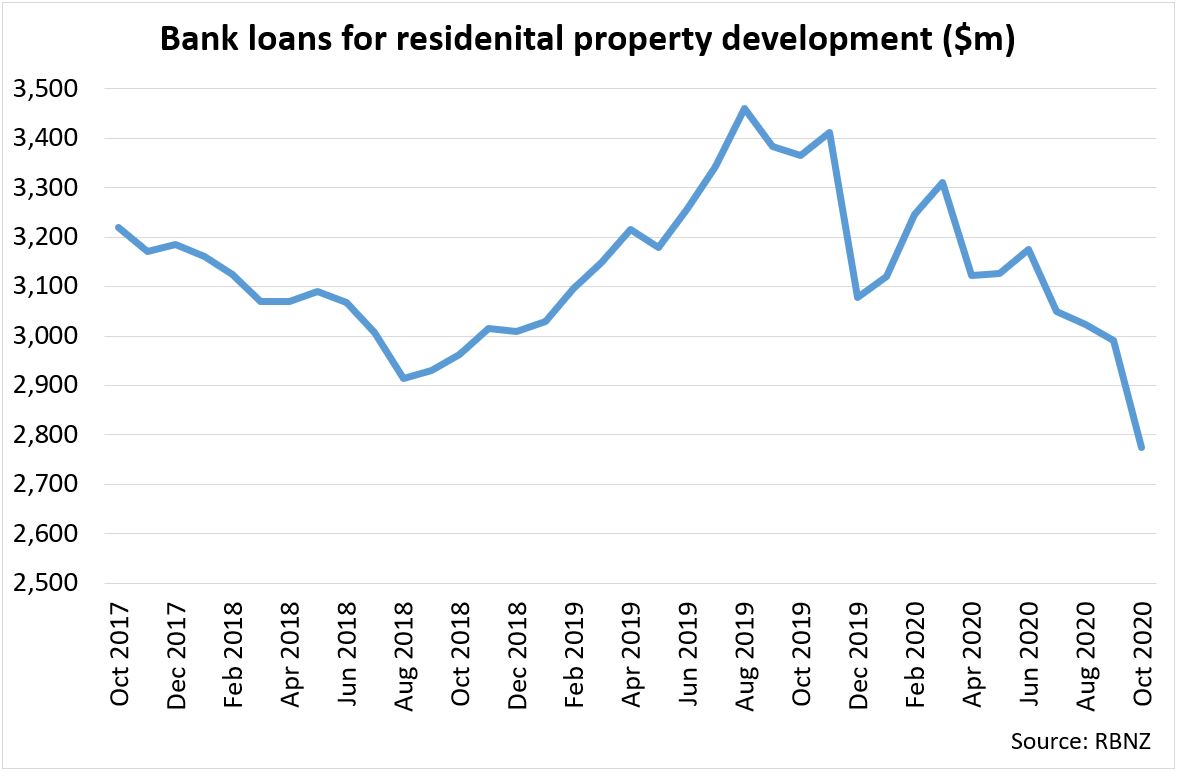

Lending for residential property development down 18%

Woods indicated the situation was better than previously thought. She noted the uptick in the number of building consents being issued:

Building consents - residential

Select chart tabs

But she didn’t acknowledge the decline in bank lending for residential property development. The value of these loans fell by 18% in the year to October, according to the Reserve Bank (RBNZ):

Meanwhile bank lending for commercial property development increased by 9% over this time and the value of bank lending against housing (investor and owner-occupier) increased by 7% from October 2019 to October 2020.

Banks have the cash...

It's worth noting the RBNZ has provided retail banks with ample liquidity through various channels since the onset of Covid-19.

The amount of settlement cash held by the RBNZ is sitting at $26.1 billion. To contextualise this level of liquidity, the highest amount of settlement cash held pre-Covid was $11.1 billion - a level hit in November 2008.

Banks have only needed to draw $1.3 billion from the Term Auction Facility made available by the RBNZ in March.

They have, since Monday, also been able to access up to $28 billion of funding priced at the Official Cash Rate via the RBNZ's Funding for Lending Programme.

Making criteria fit for purpose

Woods reiterated: “We’re continuing to monitor the situation and make sure that any [underwrite] criteria we put together are fit for purpose and are going to be what we need for the construction sector in 2021…

“We’re making sure that any scheme that we put in place is timed right to even out any downturn that we might see in the construction sector and to make sure that we are having a smoothing effect, which was always the purpose.”

Woods has previously said she would want affordable housing to be part of supported developments.

She wouldn’t commit to making the underwrite available for developers building co-operative housing or using alternate tenures, but said she was talking to the sector.

The Salvation Army has written to Woods, suggesting: “Your Government should use its KiwiBuild, Progressive Ownership and Residential Development Response Fund to encourage private sector alternative tenure initiatives.”

While KiwiBuild sees the government underwrite houses that meet a set criterion, the aim of the Fund is to assist in the development of a broader range of housing types.

National’s housing spokesperson, Nicola Willis, was interested in seeing the eligibility criteria for the Residential Development Response Fund.

“My concern with these schemes is always - how do you ensure it’s fair, so you’re not subsidising one property developer at the expense of another?” Willis said.

40 Comments

Is our Government not watching what is unfolding in the Global economy? We are only 10 months into this storm and meanwhile London, Canada, California and many other key places are going back into lockdown. Think of what that is going to do to many businesses and jobs. The defaults are only just starting for many and that all takes a while to flow through the system. Personally I don't think we have seen the true part of the storm yet. But hey, maybe I'm wrong.

Yep, you are :)

Seriously, I think perhaps they are worried about inflating the housing market even more. If developers have a floor under them, they don't have to be as careful with costs do they?

Yes 100% correct, but not because they understand why they would go up.

I would like to think they have had an epiphany about how it really works, but the only thing they have figured out is no matter what they do, prices are going up.

What they haven't figured out is what they are doing or not doing, is the wrong thing, and they don't know what the right thing looks like.

In short, they are clueless.

Just an idiot would believe a country's economy is isolated from the rest of the world these days so you are totally right, especially NZ where a large part of our economy relies on import and export and international tourism and university students. Vaccines might mitigate the hit but it is a bit too late already to even pretend nothing happened. This was a crisis that was cooking for a while COVID just triggered it faster than anyone would expected.

Exactly this - all the government's responses has bought us time to learn more about the virus and get to a vaccine, but all they did was delay the inevitable. A synchronized global slowdown will take effect in 2021 once the USA and Europe unemployment numbers start skyrocketing. Their housing bubbles will pop first which will initiate FONGO elsewhere as investors will try to offload while prices are still high.

New Zealand is a country with a relatively small population, with reasonable & sustainable exports unlike other bigger players who stand to loose much more in the COVID crisis.

The RBNZ and Govt alike are doing their best to stall hoping that a vaccine will be out by the end of 2021 and things will return to normal around 2023-24.

Unlike most new diseases, COVID has the whole world working together to get a vaccine out as soon as possible purely because the economic ramifications to the world economy and the sheer human toll.

The recent rocketing of House Prices and surge in sales was expected, though it took a few months caused the RBNZ to heave a sigh of relief, but now as the fire has gone out of control, the RBNZ and Govt have gotten cold feet (thanks to the collective madness of investors induced by artful auctioneers and cheap fiat money from the patron banks).

So now the only viable option is to reign in the Banks and stall for a while till things cool off.

As for the first home buyers and affordable housing, nobody really cared, if fact if we don't have the working poor (landlords mortgage servicing slaves), our beautiful fool's paradise, would end up in catastrophe.

That's the bitter truth, even good old Labour at the helm is now bashful despite all that propaganda of affordable housing.

The current mantra is how best can we Stall, after things calm down it will be business as usual.........followed an exodus of disillusioned kiwis, only to be filled with more voluntary debt servicing slaves from overseas, while the sustainable ponzi scheme continues for another decade.

I agree with some of your points but there are more viable options to cool down the housing market, one of them being a BAN in housing investment for a period of time until wages catch up with current prices.

Great idea, but that's something that can never happen. At best, the market will consume itself amidst low employment and high prices.

As Prices will become more exorbitant:

Kiwi working class families will slowly be forced to flat-mate & share houses with others (some of them may even throw their hands up and get social housing OR move to Aussie).

Most low end fortune seeking immigrants who come in will end up huddling in single rooms of derelict houses, in over priced ghetto's (Mt Roskill in Auckland for example).

Finally, the flat mating / single room huddling / bunk-bedding will get saturated.

For all you may know it might even go a step further and end up like those Indian / Bangladeshi construction workers living in Dubai (and the good o'l kiwis might brush it off, saying Oh its Auckland)… but then what ?

The country will finally end up in Stagflation........... and as per my humble understanding, this won't happen for the next 10 years.

Till then, give big talks and keep kicking the can down the road.

Why not? It is a concept perfectly valid in a capitalist system. As long as we can afford investment in houses as a society we allow that, but since it is just a nice-to-have and not a necessity we can just get rid of it until further notice.

It is just matter of political willingness.

Jacinda "Slow down new builds now - house prices need to rise - it's what the people expect!"

and increase immigration to 100K+ per year from 2021

JA need to remind them "you can't always get what you want"

I believe they think house prices are going to tank.

The massive oversupply of housing and rising interest rates are going to hit together and on their watch.

I believe so too, it is the sensible consequence to a period of hyperinflation when the economy is uncertain, no matter how much low rates go, unemployment going up has a much more important role in rents and the number and size of mortgages being issued. Any smart investors know that too and are probably selling as we speak.

We need to be more specific with our wording, we have a massive oversupply of unaffordable house, and a massive undersupply of affordable housing.

And you are correct about what they are scared of, ie house prices going to tank, and they are also scared about the present rate of increases because they know it will lead to prices tanking.

It's not called a boom and bust cycle for nothing.

There cannot be a bust, as per gubbmint and RB policy. They fail to understand economic cycles require both boom AND bust, therefore they will destroy the economic cycle by creating more and more zombie industries. Add housing to that list (low productivity, high costs, high prices, pumped up by central bank printed money).

Yet banks have only needed to draw $1.3 billion from the Term Auction Facility made available by the RBNZ in March.

Only $160 million remains outstanding until tomorrow, when another $50 million settles.

I think this is BS. They have come up with another excuse to cover up their bureaucratic bungling.

My understanding is that many developers are finding it hard to get funding.

But when the land price is wrong (to quote the much-missed Hugh Pavletich), everything on top is wrong. And who limits land supply? Not the Central Gubmint - it's the dopey TLA's with their District Schemes. These creations are usually so complex that an entire breed of 'Plan Navigation Consultants' has emerged to guide hapless would-be developers, home-ownewrs, builders, architects et al, through the Byzantine Mazes. For a Modest Fee, natcherally. And with no results guaranteed - much is left to the Discretion of the Plannerz. And with no time-line - since the quaint notion that Time=Munny doesn't apply to the public sector.....

Hugh is despised by the wingnuts who comment on the content at Kiwiblog. I don't really understand why.

Because Hugh is beholding to no one and tells it like it is, repeatedly. They try to drown him out, he just gets louder, they try to ignore him, but he is there consistently.

They hate him because he is right, and they cannot stop him from says it, on a free-speech platform.

It's a delight to watch.

If only the dopey prats bothered to read the District Plan (get with the times waymad, it's not the 1980s anymore...). It still astounds me that developers haven't even read the planning rule book before they design something. Architects and pretend architects (architectural "designers") are even worse. You wouldn't expect this sort of behaviour in any other industry. Developers in NZ are poorly served to do their core business. Hardly ever meet a planner working for them. It's no wonder there's so many "delays". Most of it is self inflicted due to poor up front resourcing.

Good points.

But it's easier to blame the bureaucrats (noting they certainly deserve some of the blame).

Architects are often the worst, because of their arrogance (sorry for the generalization, but it's often true)

Do you mean the 80's and historically every decade before that that was 3x median income?

It's the restriction of land that is causing the majority of the price rises.

Any saving on any other input gets captured by the most restrictive part of the system, which is the land.

It's council policy that sets how much land and where gets released, hence the restriction.

If planners have had any input, then it means they are also responsible (partly)for the high priced poor quality housing or at least enforcing the rules that make them so.

“ You wouldn't expect this sort of behaviour in any other industry.” mate, I am actually expecting this type of behaviour in any industry. I wonder if any manager in any company has read the Employment act, they are almost all breaking it sometimes without even understanding. This is all called unproductive unprofessionalism, direct result of Curren RBNZ policy - gamblers are always saved

She's taking waffle to cover up Labour's lower-quartile building failures.

We ALL Know it's Low-Cost-Housing that needs to be underwritten. Larger homes are more desirable to build because developers make more money - less risk, therefore easier lending.

She has no nuance on this one.

"Woods has previously said she would want affordable housing to be part of supported developments. "

Good to see in the decade since Hobsonville Point and the SHAs, we're getting some fresh new plans - which sound suspiciously like SHAs.

“We’re not putting it on hold. What we’re doing is continuing to work through to make sure the criteria fit the current circumstances that we’re facing,” Housing Minister Megan Woods told interest.co.nz.

Riiiiigggghhhht. Say again?

Bunch of gobblygook designed to obfuscate and confuse.

The amounts outlined are so small as to hardly justify the Ministers time at all. I'm sure the Housing Minister has better things to do with her time and more ambitious initiative she'd love to discuss.

I hope it's a case that they've been holding back, monitoring the situation, evolving their thinking with the current events, and are happy to modify their promised plans based on new happenings.

Unfortunately I suspect it was forgotten about, likely an email that didn't get a reply somewhere in Wellington a long time ago is now getting a rocket under it.

Just"Print! And Walk Away!"

Nice one.

We have gone from a minister who promises the world but delivers zip, to one who promises zip and delivers zip.

In a funny way, I kinda miss Twyford's hollow bravado...sort of...

Twyford and his Kiwibuild will go down as the biggest failure of any govt in our history.

But yes I miss his enthusiasm. During Kiwibuild he was like a dog chasing cars trying to grab any idea he could.

Jenée - not sure if you read all the comments but if you do, the next time you might have question time with the PM could you ask:

A recent poll indicated that 75% of kiwis want house prices to fall in order to improve affordability (per the poll in the news last night). How and why do you have the view that the majority of kiwis want house prices to rise if it appears that simply isn't true?

(based on the poll, the PM is basing her political stance off a false narrative - which is a very dangerous thing to do....we'll end up like the United States if we head down that path. Not sure who is advising her on this but she needs to get some better advice...pronto).

I think half the challenge with a question like that is figuring how to catch her out on what would likely be her bullsh*t PR response.

What is confidence crunch going to look alike?.. anyone. Almost like nothing happened, even govt announce surplus. How could we define what supposed to be a negative outcome, become positive? I guess it's relative where you looking from; face to face my left arm is your right arm, your negative is my positive, my positive is your negative.. but if we can change to game rule at any moment notice, anyone interested to play with you?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.