By Greg Ninness

The Reserve Bank’s moves to slash interest rates last year caused a widening gulf to open up between the “haves” and the “have nots” in the housing market.

Interest.co.nz’s latest Home Loan Affordability Report has highlighted the growing inequality developing between people who already own a home and those struggling to buy one.

According to the report, the slide in the average two year fixed mortgage interest rate began in March last year when it declined to 3.31% from 3.52% in February. From there it continued to fall, dropping to 2.58% in November/December. March was when the Reserve Bank cut the Official Cash Rate by 75 basis points to a record low of 0.25%, where it has been ever since against the backdrop of the COVID-19 pandemic.

The cut in interest rates had an immediate effect on house prices, pushing the Real Estate Institute of New Zealand’s national lower quartile selling price up to $550,000 in December from $446,000 in May. That's an increase of $104,000 (23.3%) in seven months.

Around the country the lower quartile price increased by between $36,000 (11.0%) in Taranaki and $123,000 (29.4%) in Hawke's Bay over that seven month period. Lower quartile prices rose by $94,300 (13.4%) in Auckland, $74,000 (15.6%) in Waikato, $80,000 (16.0%) in Bay of Plenty, $102,128 (18.6%) in the Wellington Region, $65,000 (18.1%) in Canterbury and $81.500 (20.6%) in Otago.

The price increases in the middle of the market were even greater, with the REINZ’s national median selling price increasing by $129,000 (20.8%) between May and December.

For existing home owners those extraordinary price gains were like manna from heaven. It was like money dripping from the sky, pushing up the average home owner’s equity by more than $100,000 over seven months, or just under $500 a day, even if their property was a relatively modest one at the bottom of the market.

But to those who already have a home, even more will be given.

Not only did tumbling interest rates push up home owners’ equity, and therefore their personal wealth, if they had a mortgage on their property it would have pushed down their mortgage payments.

The monthly payments on a $300,000 mortgage at the March 2020 average two year fixed rate of 3.31% would have been about $1316 (for a 30 year term). But by November/December the interest rate had declined to 2.58%, reducing the monthly payments on a $300,000 mortgage to $1198, saving the homeowner $118 a month.

Those two factors combined have left existing home owners substantially better off, both in terms of their overall wealth and their day-to-day cash flows.

A kick in the guts

But for would-be first home buyers, hoping to make the leap on to the bottom rung of the property ladder, the decline in interest rates has been a savage kick in the guts.

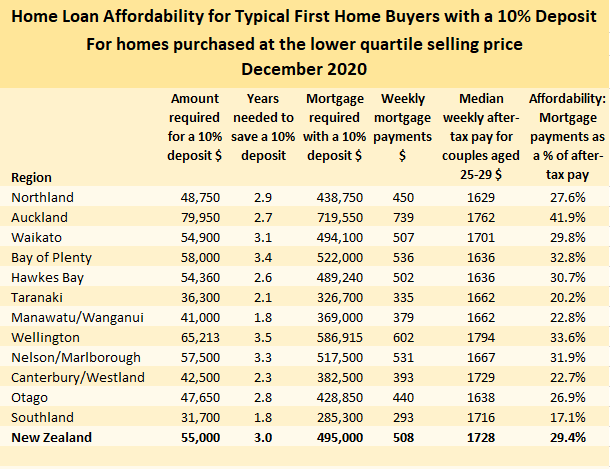

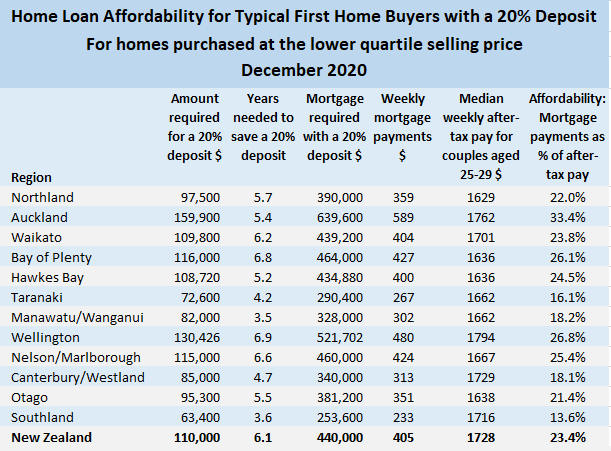

The amount they would need to save for a 20% deposit on a home at the REINZ’s national lower quartile selling price has increased from $89,200 in May last year to $110,000 in December, up by $20,800 (23.3%) in seven months.

The amount needed for a 10% deposit increased from $44,600 to $55,000 over the same period.

In Auckland, the amount needed for a 20% deposit increased from $141,040 in May to $159,900 in December, while the amount needed for a 10% deposit rose from $70,520 to $79,950 over the same period.

As well as pushing up the amount of money prospective first home buyers would need to save for a deposit, rising prices also increased the amount they would need to borrow for a mortgage.

If they had a 10% deposit they would need to borrow $495,000 to secure a home at the REINZ’s national lower quartile price. And if the home was in Auckland they would need to borrow an eye watering $719,550.

With a 20% deposit, the size of the mortgage needed for a home at the national lower quartile price was $440,000, and in Auckland it would have been $639,600.

Adding to their misery, any benefit that falling interest rates would have delivered via reduced mortgage payments was more than offset by the rise in prices between May and December last year.

The amount of money a first home buyer would need to set aside for the payments on an 80% mortgage for a home purchased at May’s national lower quartile price of $446,000 would have been around $342 a week. But by December the lower quartile price had risen to $550,000, pushing the amount needed for mortgage payments up to $405 a week.

If the first home buyer only had a 10% deposit, the amount needed for mortgage payments would have increased from $446 to $508 a week. If the home was in Auckland, the amount that would need to be set aside each week for the mortgage would have increased from $540 to $589 if they had a 20% deposit, and from $705 to $738 if they had a 10% deposit.

So the differences between the effects lower interest rates have had on existing home owners and those yet to buy their first home could not be more stark.

By every measure, existing home owners are significantly better off. They are wealthier and are having to pay out less in mortgage payments. For them, lower interest rates have been like money raining down from heaven.

But for hopeful first home buyers, the reverse is true. They will need to save longer and harder for a deposit and when they finally have enough for a deposit, the payments on the mortgage will eat up more of their household budget.

For many of those on average incomes, home ownership is fast becoming the impossible dream.

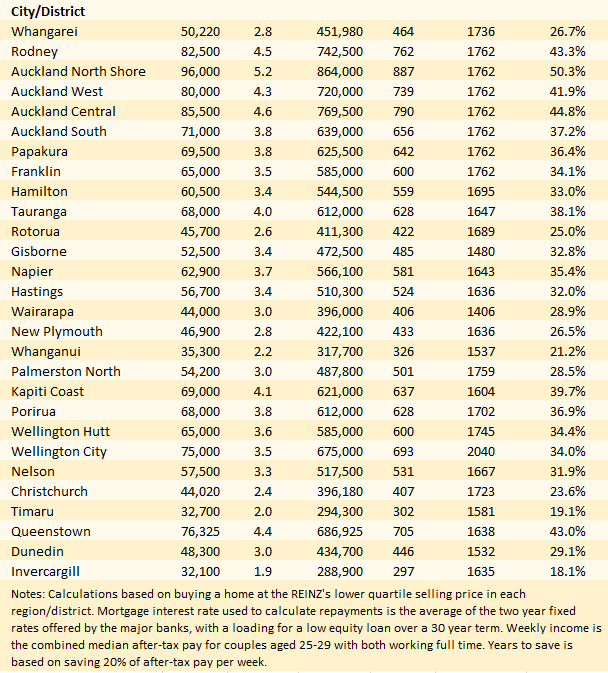

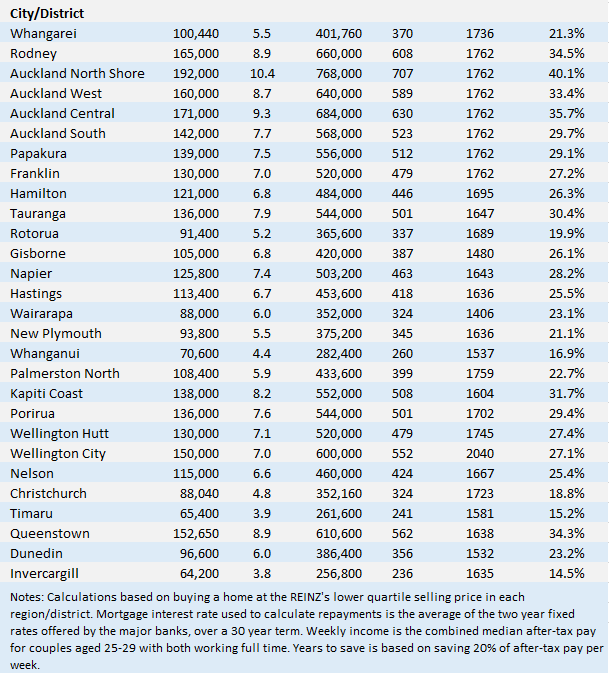

The tables below set out the main affordability measures for typical first home buyers in all of the main regions and districts throughout New Zealand, with deposits of 10% and 20%.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

211 Comments

Let's not forget, boomers paid 20%+ interest rates and didn't buy smashed avo on toast or silly things like iPhones. They deserve these capital gains and a rental property or two. Harden up younger generation, you've got it easy.

lol

Unsure if clueless or a meme.

Of course those same boomers were buying houses that were 3x a one earner households median income, save 33% of your income for three years and you could buy the median house outright!

Median income from all sources for an individual today in Auckland is $36k. Of course debt is much cheaper now but even then, saving 33% of your income for 3 years doesn't even get you half way to a 10% deposit!

The problem with the young is they think they should have a liveable house to start with. Want to live in Auckland where the jobs are? How about start on the property ladder in Huntly and do a small commute to the CBD. Don't buy your lunch and indulge in luxury items like a cell phone. Work multiple jobs, overtime and save save save. That's what boomers did anyway...right?

With COVID specifically targeting the 60+ demographic, maybe there is a just God in heaven after all? [sarcasm]

Maybe God (or whatever one calls the Creator) has seen how we have been abusing the planet leading to “climate change”and has released a virus to reduce the World’s population. A cleansing of the old and infirm. Who knows.

Nifty1 - It does seem pointless the boomers had it easy thing your going on about. A few points -

1. I don't think buying a home was ever easy at anytime.

2. Just because it looks easier at anyone time does not mean everyone did buy.

3. 3 out of our 5 children have bought in the last 2 years, 2 in Auckland and 1 in CHCH. The other 2 are offshore.

4. re channel your energy into how you are going to do it.

5. I worked offshore for 3 years early 80's to achieve it.

I wish you well if purchasing a home is what you want rather than finding excuses.

It may not have been easy but it sure as hell wasn't this hard. Basic affordability stats bear this out, as does declining ownership stats. This isn't really up for discussion. I don't want NZ to be a place where the only way people have to afford a house is to leave the country, leave those behind to prop up the state and pay for the infrastructure and then just pop back when they want to buy a house. I think is a big driver of animosity towards overseas Kiwis - unfairly so, perhaps, but there are certainly some who want to treat NZers who live and pay tax in NZ like resort staff.

Agreed, there is hard and there is 5x as hard. Also increased cost of living in the form of relative increased housing costs, results in is less money in the economy in the form of discretionary spending (smashed avo). All that lovely money going into investors pockets and into more and more ponzi building instead of the real economy

All of the above and compounded by governments who regardless of their political stripe, see their role solely as "fixers" so the market can do its thing, unencumbered. Economist Mariana Mazzucato's latest book makes the argument for "moonshot" thinking and is critical of the infantilisation of government in the last 40 years. It makes for compelling reading. https://marianamazzucato.com/publications/books/mission-economy/

We've been watching 70s sitcoms which were a bit before my time, i havent belly laughed so hard for a long long time. Good non PC humour. But looking at their houses it was cramped and there were the inevitable frequent power cuts from either inadequate infrastructure or the workers on strike, lack of money for the basics was another. There was plenty of daily issues the writers could utilize.

Shoreman...Buying a home without help was very easy at any time last century. Not everyone bought because (usually) they did not have role models or the financial acumen and knowledge which is usually gained from being passed on from relatives or friends ie it depends on your luck in terms of birth or who you talked with (friends, colleagues, at sports clubs etc).

I was lucky enough to play golf at a high end Auckland club as a teenager in the 1980s. A bank manager and a few older property investors provided me with a blueprint and the ability to see how easy it was to make (almost) unlimited risk free profit without any skill or effort whatsoever. So the biggest part of it was LUCK, as it is with most people, probably including yourself. Had I taken an interest in softball or rugby league none of it would have happened. Pure LUCK that I didn't. Had I not been born in the late 60's. Pure LUCK I was. Had my parents not lived in Auckland. Pure LUCK that they did.

Did you work offshore because you insightfully saw it as the best way to make money? I would guess you were LUCKY enough to have a relative or friend who planted the seed and guided you in the right direction. I would guess you grew up in Auckland and simply bought your first home there because of it. Pure LUCK. Offshore workers were incredibly over paid in the eighties. Pure LUCK. 40 year (1980 to 2020) Akld housing boom. LUCK.

Your last reply contended I was assuming (which I wasn't) so have taken the liberty to assume here. You can attribute your wealth mostly to LUCK. Please try to avoid the impression that you look down on others that were not as LUCKY. Your grand children are far luckier than you. They have a grandfather who appears to know the price of everything and the value of nothing. Their grandfather needlessly sold years of his life working when (it sounds like) he should have retired (very) young and used his wealth to improve the quality of his life. Your loss, their gain. I hope they do not repeat such an expensive mistake and choose to retire young. Please try to have a little more compassion for others. It is very hard to get ahead when trying to save $100K for a deposit while paying 40% of your income in rent, unless Daddy is worth 15M of course.

PS: probably my biggest area of expertise is in proportioning the luck and skill factors that relate to various outcomes. Cause and effect is usually very tricky to accurately quantify, especially when evaluating your own performance. Just be happy you have been extremely LUCKY.

"financial acumen"

Yes big problem. Peter Alexander accountant explained today on The Country midday show... compound interest is more important than shakespeare... so why isnt it taught more?

FH... Einstein described compound interest as "the eighth wonder of the world". I guess most teachers and academics default to book lessons as opposed to life lessons. IMO teaching Shakespeare to kids is worthless. It wasn't until I gained about 20 years of life experience until it even meant anything to me (or I could even understand what he was on about).

Yes, I worked off Shore as well, but not to buy a house, I mean if you just follow the logic why don't we ALL just go offshore to earn the money.

There may be benefits to travel, assuming that is why we do it, But for those that don't, why should there be a punishment for staying in NZ?

Nope, Boomers did exactly the equivalent of the day, what you are disparaging the younger generation for doing today, and the boomers received the same criticism from the previous generation as well.

'they think they should have a liveable house.' Classic. You do know that the health stats. already show the NZ has some of the most unhealthy housing in the developed world?

Nifty1,

As one of these so called boomers, I think you are talking crap. Sure, we paid high rates of interest on our mortgages and i worked hard-i was self-employed- but no harder than say my sons do today. I may not have had smashed avos but ate well and took regular holidays. One thing you and others forget is the effect high interest rates and inflation have on debt. You and others suffer from selective memory syndrome.

I think you are missing the sarcasm here LL.

I would say Nifty is another greedy landlord "Boomer" bludging off the taxpayer

The point being, the lower price debt was locked in, but the interest rates were not, so as interest rates fell so did your rate.

It's simple math to work out which one overtime is better to have, but since that seems to be beyond some, over the term of the ,mortgage it is better to buy at the lower price with the higher rate, than the reverse.

My parents bought a house on a quarter acre section in 1978 for $15,000 and paid off their loan within a year. The same house was recently listed for sale over $1,200,000, which is 80 times more than my parents paid for it. I'm told that my father was earning $30,000 a year at the time that they bought their first house. You'd need an income of $2,400,000 a year now for the same income to house price ratio on that property.

Duh, just stop eating avocado and buying iPhones and SkyTV and you will easily save another $2,390,000 on top of what you are currently saving.

so true

the boomers have done the maths

The house I grew up brought for $19k is now for sale at $2 million , an increase of $38k per year. No pool and a stones throw from 70 thousand cars going past every day.

I think your figures are wrong. Very few people would have been earning $30K in 1978 so its not a fair comparison. We came to NZ in 1974 and my father had been given a house in the UK which we sold and he still needed a mortgage in NZ, in fact from memory they still needed a second mortgage and the interest rates were horrendous up near 20% on that second mortgage from a lawyer. We had a few very lean Christmas's before that was paid off as I distinctly remember the quality and quantity of the presents dropping off big time .He was a skilled Engineer so pretty sure his pay wouldn't have been rock bottom either.

Yes Boomers sole income earner worked tirelessly (well not Sundays) to get a roof over the family head. Had to come home to a cooked dinner and Lion Red...urrrgh.

Defo urrrgh on the Lion Red

Well if you hate it then "defo" time for one mmmmm, as a primary school kid the guys at the panel shop would give me a drink on the way home from school ... love the smell of hops

Make mine a BRB IPA. Cheers

Nifty

Get over your baseless pathetic anti-boomer bias and blame shifting.

Boomers bought their homes 40 years ago. An increase in house value for retirees especially means absolutely zilch - a paper increase in the value of their home does not buy a single extra slice of bread.

If you want to look to winners, look to later generations who have purchased homes in the past decade. They have seen both their home increase in value (and unlike boomers are at that stage in life to leverage for investment properties) and have seen their mortgage repayments half.

Rather than simplistic blame shifting, try putting up comments that have some basis of validity. Your attempt at being cynical isn’t clever - just same old same old.

Pathetic.

Cheers

"An increase in house value for retirees especially means absolutely zilch"

Hold up...

1.They can sell up and move to a smaller town, with stacks of cash left over...

2.They can stay in the same city, downsize and release cash

3.They can have the ability to reverse mortgage and release equity/cash - stuff an inheritance for their kids

4.They can sell one of their rentals and release their capital gains/cash or they can justify hiking up the rent for more income

5.They can sit back and get angry at young people thinking they had it harder back in their day

Nifty

Yes . . nothing that I wouldn't expect from one besotted with "poor me, poor me" and blame shifting.

Absolutely no reason why any FHB couldn't follow your advice on points 1 and 2. The majority of boomers do not have rental properties and in fact I recall figures (Retirement Commissioner I think) that over a quarter of retirees still have a mortgage.

As for point 5 - you are doing an exceptional job at something similar and need to get over it.

Many boomers - including in posts by me - are concerned about the issues.

However while it is an issue, continual pathetic whingeing and whining and blame shifting such as your comments achieves absolutely nothing constructive towards solving the problem.

If you are in the position that you don't have a home and want one, you need to face the fact that many of your peers do. Why is that Nifty??????

Printer 8

"Absolutely no reason why any FHB couldn't follow your advice on points 1 and 2"

I'll give you one...employment.

"Many boomers - including in posts by me - are concerned about the issues."

But you don't want to hear about it from the people on the 'front line', far too annoying & confronting right.

Nifty

News for you.

Here in Hawkes Bay many young Aucklanders are coming here. Talking with people in the hospital administration large numbers of positions are being filled by people from Auckland and Wellington, and same with schools. Talking to some property investors they are seeing more and more prospective tenants coming from Auckland and Wellington as well as South Africa.

As previously posted, I got out of Auckland over 30 years ago as I thought property prices in Auckland even then were too expensive. Turned out to be best financial and lifestyle decision I made.

Maybe you need to do some serious thinking and stop coming up with every reason to blame shift. After all Nifty, as I have said many of your peers are FHB - according to RBNZ, despite covid 40,000 mortgages (70,000 people???) were FHB in past year.

More young people fleeing from the city to rent in Hawkes Bay & filling property investors houses - wow that's great news for FHB's...

You my friend come across as a stereotypical boomer - even though the facts are clearly highlighted in this article you still don't see the problem.

Nifty

"More young people fleeing from the city to rent in Hawkes Bay & filling property investors houses - wow that's great news for FHB's..."

No, not at all!!!!

Coming to the Hawkes Bay to get on to the property ladder.

Your comments suggest that you really do need to stand back and look at your view - its pretty black mate.

Despite Covid those 70,000 FHB over the past year (150,000 over the past two years) have had the imitative to get out and do something about it. The majority of those 150,000 FHB will be millennials who despite it being really tough have had a far more positive view and initiative to do something about it.

Yeah, its tough but wallowing in self pity and expecting support is not going to change anything for you other than making you bitter and twisted.

Blaming boomers is just blame shifting: you need to look at those peers of yours who are recent buyers who have not only made great capital gains and seen their mortgage interest fall (and hopefully you wont choke on your coffee, unlike the mortgage-free boomers they have not benefitted from this but suffered falls in term deposits interest rates).

Yeah, the current economic environment is tough for many; those who have lost their jobs, those who have lost their businesses, those who are homeless, those paying high rents without the accommodation supplement, those with term deposits to supplement their incomes . . . . but here we are we have the "poor me, poor me".

It is you really need to read it and think about what the article says - you can't get over it that it is not boomers that are the big winners here. Try homeowners with mortgages - its in the headline - and the vast majority of those are not boomers as you wade in and blame.

Cheers

Ok Boomer.

Coming to the Hawkes Bay to get on to the property ladder...

Wow theres a life ambition, the property ladder... What a waste of life - lining a bankers pocket. Im 50 and dont own one, but I do have a business and a boat and plan on sailing away from this madhouse.

No FOMO for you Sluggy something akin to FISH is relevant

You'd be lucky to be afford a house in Hawkes Bay if you've moved here in the last 12 months as a young Aucklander in the last 12 months - median prices up 29% to $653k, incomes in Hawkes Bay (and opportunities for good jobs) are much lower than main centres. The market here is red hot - multiple offers on pretty much anything listed. It's pretty disheartening for young buyers turning up to open homes when there is a line of late model SUVs parked all the way up the street owned by investors. Finding a place to rent is equally as difficult..

Its great you kids have managed to get onto the housing market - they must have good jobs and upper quartile incomes (or partners do). A credit to you. Unfortunately most aren't so lucky.

Yeah exactly and to quote the facts in this article: "$123,000 (increase) (29.4%) in Hawke's Bay over that seven month period."

Printer 8 please read and absorb.

Nifty

Yeah - due to all those Aucklanders moving here and getting on the property ladder.

I mentioned that earlier - you need to think about it a little more and you may click.

Cheers

Sure house prices aren't increasing because of all those investors you've been talking to? Sounds like they're busier than ever. Yeilds must be good too. There's only so much buying power for an FHB if they have an admin job or work at a school.

.

" Get over your baseless pathetic anti-boomer bias and blame shifting" get over your millennial out of touch lah lah land - give up your cell phone? Most roles now include this as a tool for the job. You are so far out of touch it beggars belief??

You started at the bottom of the Ponzi scheme and now think you worked so hard for the large increase in asset prices - laughable that you actually think todays economic conditions were the same at yours.

frazz

Don't tell me I am out of touch and it beggars belief.

I have two sons and two step sons - all millennials all with homes. None had help from bank of Mum and Dad.

Maybe you need to honestly ask yourself whose comment "beggars belief".

While you hold onto this blame shifting as an excuse, you will achieve absolute nothing constructive.

As I advised Nifty; many, many of your peers including my four sons have homes . . . . why don't you?????

(Suggestion - look at Nifty's comments regarding actions boomers can take and think how at least points 1, 2 and 5 could apply to you)

I own a house that has increased value by $170K in 2 years, ..due to my hard work?? - unlike you I think the system is broken - severely. Get ready for the uprising..probably later this year.

Ignore pedant8 frazz - he's hopelessly out of touch. Much more interested in virtue signalling, and then telling others to "harden up" than admitting that NZ has an actual housing crisis built on the back of his generation which requires a nationwide paradigm shift.

Ezy

You feeling a bit sore because I have picked you up a number of times (with reference to supporting data) regarding your Covid-conspiracy based claims.

Never claimed there wasn't an issue with housing and have posted a number of times for an economic reset.

Need to challenge whinging and whining, baseless blame shifting, and conspiracy theories - I'm consistent on that as it achieves nothing.

P.S. You know when someone is defeated or don't have good argument . . . they resort to name calling. Well done Ezy.

Typical of your idol, Trump? :)

Cheers

Ok boomer

What do we need to do to get ready for the uprising (probably) later this year? What are you on about?

If homes rise by anther 20% this year then expect some backlash from the great unwashed...

Increase the rent so when the uprising comes it'll be on foot cos there's no money for gas.. Bahahahaha

Don't give up your day job Hook te hehehe

I only work a couple of days a week for playmoney now, so I can afford to sit here and read all the bitching going on - quite entertaining

frazz

Well - you are a real, real winner.

House gone up in value (be able to leverage off that); and mortgage interest rate gone down? A double win whammy!!!!

According to Nifty you must be a boomer - one of the privileged to blame.

. . . but there again boomers will have been disadvantaged with falling interest rates on their term deposits they budgeted to supplement their pension.

Cheers

Did'nt realise owing a house was now a game for winner and losers?

It's not a ponzi scheme if rental yields can cover the mortgage interest.

Zilch gain eh? What about leverage with bank who decides on investor loans??

REAL rate is what counts, ie after inflation.

So they did not pay 20% when inflation was 17% did they?

Exactly.

Exactly. Average salary increased by about 60% between 1975 and 1979!

Well, rather than being prudent and saving 1 - 2 years wages (with the help of 15+% term deposit rates) to buy a house outright, they'd rather take out several mortgages at 20%+ interest rates and have 6 kids. Financial stupidity.

Meanwhile today the younger generation must save 1 - 2 years wages for a deposit, with the help of 1% term deposit rates. That's before we start talking about a 13% of gross pay student loan payments.

Worth noting that student loan repayment is at a higher rate than Australia's repayments, which scale with income, and never come close to the flat rate we apply our rates at. Their repayment threshold is also 2x ours. So if Australia, with higher wagers, lower living costs and cheaper houses, thinks that's a fair place to start deductions, what possible justification could there be for NZ's system to be the way it is?

Nzdan.. and 30%+ on rent and $1000 PM at the supermarket for most couples. A young couple living in Auckland, earning the average wage have almost no chance of saving $150K for a deposit without the help of Mum and Dad. The numbers don't lie.

Yes and NZ is even worse than many countries due to our high cost of living - groceries, utilities etc.

lol, back then they don't have iphones. But they have washing machines or TV cost more than iphones. Man, it's silly that you try to compare with two different technology eras. Sorry, your comment doesn't make sense. Yes they deserve capital gains to a level. But not 20% a year.

Legit question: Why do they 'deserve' capital gains?

I have to say I agree with massive respect to the older generations. I am a millennial born in 88 and I am getting sick of the increasing number of whiny younger generations. My wife and I have worked our butts off, cut our stupid expenses relentlessly, including sharing a single bed between us for a year as well as many other ways, and did everything we could to ensure our future. We became independent of family support, by choice, from our 20s, and were able to pay off our student loan, get jobs and secure a house. If we did it, so can you. Stop whining and start planning..

Agree. I'm born in 87. Purchased a few years ago and am now mortgage free on my owner occupied house. Just takes years of living below your means.

But a few years ago isn't now though, is it?

Well done. Have you done the sums to see if you could do it now on a house worth twice as much on what your salaries were then? That is what most are faced with now.

Yes full credit to the posters above for making it happen, but just because it was possible then doesn't mean it's possible now, or that the same sacrifices are possible or yield as much benefit. And that's not to say they didn't work as hard as they did, but just that they probably shouldn't have had to. Dollars spent on mortgages then is money you could have been using for families, improving living standards, investing in shares or businesses or even saving towards retirement. We are taking money away from those activities not just in the here and now, but committing it for 30 years at higher at higher and higher levels. That doesn't bode well for job creation or consumer demand down over the coming years and decades.

I made it happen in 2017. But not everyone can move to a small regional town (with the backing of their employer), live with the inlaws rent free for 6 months and buy within 500m of a train station with a daily commuter rail service that takes them to their office in the city.

In 2017 that house was low $200's, it's now valued at mid $400s. Unfortunately today that rail service still takes 4 hours out of your day.

Yup according to the bank calculator (Westpac I find has the best https://www.westpac.co.nz/home-loans/calculators/how-much-can-i-afford/) looks possible since rates have more than halved over the past few years. Only challenge would be saving a deposit. But back then, we used a 20% deposit. So would just need to use a 10% deposit these days. Usually you can find a bank doing owner occupier loans @ 10% deposit these days. Just might not get the best rate since its a bit riskier at 10% deposit. But it would still be a lot better (more than half) than what we got back in the days. And in a year or so once the property goes up around 10%, would be able to go onto the cheaper 2.29% rates these days.

None of which justifies us making it increasingly harder for the generations who follow simply so our portfolios can keep going up. Which is the problem with our policy approach currently across government and reserve banking.

We use welfare to prop up prices and rental yields, and monetary and immigration policy to ensure prices are never allowed to fall as they might in a free market. This is just a silly wealth transfer scheme and younger generations can rightfully highlight the unjustness of such welfareism for investment property and wealth transfer by policy.

There are many steps that could be taken to help aid housing affordability - as occurred in New Zealand for earlier generations (especially post-war). Earlier generations including Boomers massively benefited from these. To turn around and use policy to live off the wealth of following generations is abhorrent. It is a moral issue. And while government and reserve banking is infested with property investors no measures that might aid affordability seem likely to be allowed.

Well summarised, a moral and sustainability issue.

House prices rising at $500 per day. Over a year that would equate to 182 new iPhones. I’m not sure why all these lazy young people are buying so many phones each year instead of a grossly overpriced house??

The adage 'Get on to the property market quickly (beg, borrow or take a gift from parents) is a wisdom that is ever lasting in Aotearoa.

Bahaha, wow, I'm a gen x and I have to say what an arrogant attitude to take, boomers could buy houses without needing 6/7 times their income, you could do most the work on your houses yourself as council restrictions were not half what they are today, extra jobs, yea sure, do you know how much tax you actually pay and what you pocket. And as for you comment on buy in Huntly for a short commute... Haha so if you start at 8am for example, you leave home for the Auckland City area, you would be out by 6:30am and if you finish at say 5pm, home by 6:30 with traffic that you had the luxury of again having half today. But wait they should now get another job in there somewhere.... Sit back and shut up because people like you make every other generation laugh at your arrogance. Oh And you do realise cell phones are not a luxury anymore,?

Woosh!

pftt... whatever.... we're you paying 10x your household income for a house?

Apparently getting yourself in debt to the tune of 7, 8, 9 times household income, with the only conceivable exit strategy being a continued doubling of house prices every 10 years for the next 3 decades (fingers crossed!), is considered "winning".

I bought a year and a bit ago. I don't feel like I'm winning. Frankly, I'm terrified.

Same. A massive mortgage, interest rates likely to have bottomed out or close to it and an enormous amount of principal to repay from income that barely sees any inflation. Yes the equity has gone up on paper but the gap between it and the cost of any sort of upgrade in future grows larger and larger so the effect overall feels negative.

Yup, I'm quite happy to talk about my ownership experience to date so people know what young people are dealing with. I have one on the way (already years older than my parents were when I was born) and eventually space will become an issue. We face doubling our mortgage if we want to add a bedroom, on a much lower household income. Until I borrow to buy another house, or my mortgage comes off fixed, the gains from a lower interest rate are an illusion; it doesn't stop everything spiraling out of control in market the mean time. And of course, if there is some sort of reset, the paper gain disappears and then job security gets thrown into the mix. This isn't the States. We can't just walk away and start over.

Just glad we bought on the North Shore when we could. Our repayments are now less than what we were previously paying in rent for a far worse house.

Isn't about last laugh.

More about who gets it

These time frames to save will only be accurate if house prices stay the same. In reality, they will be much longer as while you are saving, the lower quartile price is increasing, continually shifting the goal posts.

Yup, reminds me of the "just buy a do-up!" - doesn't really work when the land price is the thing you're really being hammered by, and new houses aren't supplied onto the market priced at a "do-up" rate. Lots of owner-occupiers and flipping culture in the 1990s took a huge chunk of the do-ups off the market and made them mid-premium homes, and a big chunk of the ones that were built new then leaked.

"Do ups" are bought by speculators/developers now, demolished and chucked into the landfill to make way for having every growing thing removed, all the top soil removed (to lord knows where) for some hideous construction that will see the entire section bar a few scraps concreted for multiple dwellings, for what, the bloody ponzi that is rapid population growth. It's madness and it is going to be a tough teat to wean ourselves off, which we must do.

For existing home owners those extraordinary price gains were like manna from heaven. It was like money dripping from the sky, pushing up the average home owner’s equity by more than $100,000 over seven months, or just under $500 a day, even if their property was a relatively modest one at the bottom of the market.

At the very same time currency debasement marched on as the purchasing power and hence the value of wages collapsed.

Even my $652 fortnightly pension payment annualised represents a return on a principal investment of $6,780,800 earning the ANZ "SeriousSaver" rate set at 25bps.

At the very same time currency debasement marched on as the purchasing power and hence the value of wages collapsed.

You're one of the rare commentators who really gets it Audaxes.

THE RB OCR/CPI model is deeply flawed and greatly harming the position of those who do not own their own home. Further I cannot see how it does any thing to meaningfully help the economy. Lets look at how it has performed since the GFC -

The interest rates from 2008 fell dramatically initially, bounced around something under 3% until 2018 sometime then steadily fell until until practically nothing. Note it was falling significantly before the pandemic.

https://tradingeconomics.com/new-zealand/deposit-interest-rate

If low interest rates were effective at boosting the economy and raising the CPI, you would see evidence of that by way of a growing economy leading to a need to raise interest rates inside that 12 year period. There is no evidence of that in fact towards the end of that period they had to lower interest rates further. Therefore you can conclusively conclude that there is absolutely no linkage between lowering interest rates and raising economic performance.

Over the same period however we all know that house prices have galloped until we now face the ridiculous situation that we now have.

https://www.globalpropertyguide.com/Pacific/New-Zealand/Home-Price-Tren…

Thus we can categorically claim that lowering interest rates does absolutely nothing to help the productive economy, but is strongly linked to house price inflation. But we keep on doing the same thing and expect it to help.

As Einstein said - the definition of insanity is to keep doing the same thing and expect a different result.

Lets think about what might be going on in the real world to explain this.

CPI goes down so RB lowers the OCR.

Those on fixed incomes (16% of total population over 65) receive less so spend less, save harder and depress the economy further.

Property investors pile into the housing market with the cheaper capital so house prices rise. This becomes a positive feedback situation so they are rewarded and fuel the bubble mentality further. They probably spend a bit more as a result of their confidence and stimulate the economy. They are not a large percentage of the population so their stimulation contribution may not be that great.

Existing home owners benefit from the increased wealth effect, spend more and stimulate the economy. However recent first home buyers will have had to pay a high price for their home so will be paying a higher mortgage. They will not be spending much.

Next we come to the very large group of people (getting close to 40% of the population) who have to rent. Increasing house prices have a very depressing effect on their disposable income so this will tend to strongly depress the economy.

When you consider all that it is very hard to see how the net effect of lowering the CPI can stimulate the economy and it would not be surprising if it depressed it. Pretty much in line with the evidence set out above.

If lower quartile is too expensive and rents are $550 + in Auckland, how does the upper third of pop expect the lowest third to afford places to abide and be available to do work for the top third?

This is how "society" falls apart.

Indeed, but workers are free to ask for more money AND leave if refused.

Workers are their own worse enemy. If you CANNOT quit your job, doesn't that MAKE YOU A SLAVE ?? Pretty much the definition of slavery bro.

SO DEMAND more money and if refused - leave. If you can't do that and refuse to admit you're a slave - maybe seek some free psychological help in facing your reality and moving forward ??

Slavery, condition in which one human being was owned by another. A slave was considered by law as property, or chattel, and was deprived of most of the rights ordinarily held by free persons.

Exactly; 'human resources' deprived of the ability to own land/property - sums up the plight of many hard-working Kiwis. Very sad.

Satan's daughter (JA) will be adding that to her dream board for young kiwis

RSE workers for inner city jobs?

If anybody wants to create a petition to defund TVNZ, I'll happily sign. Sadly people voted for zero change and they are getting just that. Ironically they'll probably vote Labour back for a 3rd term.

Would be interesting if people had to declare who they voted for before posting comments.

I voted for labour. I almost didn't vote, because all parties are out of touch and in denial with issues bigger than our carbon emissions. Sustainable population, pollution, housing, sustainable food production etc.

But it seems it doesn't matter who you vote for, at the end of the day capitalism wins.

Globalism wins.

The establishment never loses, at least.

The present system in NZ means if you voted right, then that is crony capitalism, and if you voted left, then that was crony socialism.

I think it’s more like crony capitalism at the moment.

If capitalism was winning, the houses would be affordable. Restricting supply and skewing the tax base ain’t capitalism.

I agree with your comment re TVNZ. As far as voting goes, I will admit that I voted Labour (due mainly to their performance re Covid), as well as National's non-performance. I've realised now that the Govt have simply been lucky re Covid (and that luck may still run out). It's also become obvious that they don't know how to fix the housing crisis which is getting worse by the day - real one trick pony.

Yeah I often watch the biased , one sided international news channels for humour value. CNN, Sky News Aust, Fox even BBC. We can now add the blatantly left leaning TVNZ to the villains. And most do not even notice it.

I noticed it a few years ago..... and haven’t watched mainstream news or tv since.

If your only source of news was TVNZ you would think Donald Trump only had the support of redneck blokes with tattoos, beards, wearing singlets and driving around in pickups. You would never guess that around 70m americans voted for him in a year of the worst pandemic in living memory.

I would be happy to vote for/help establish a party dedicated to a single issue. Affordable housing.

With nearly 40% of the population in rental accommodation being screwed by landlords and both major political parties, there are a lot of potential supporters.

Fix this problem and a lot of other problems will be greatly reduced.

You would get my vote.

Did you see the article on Stuff late last year..... Mike Greer homes had sourced some new Japanese houses that could be imported into NZ, would be cost effective to built and built to a much higher code than our current building standards.... great, lets do it..... But no! They could only be imported and built as long as they were built to a much lower building code to match our current standard!

I read it at the time - very interesting:

https://www.stuff.co.nz/business/opinion-analysis/300140577/what-can-nz…

Panasonic just released this 2 weeks ago; the Waikato test builds mentioned in the above article are going ahead.

https://homes.panasonic.com/english/news/release/2021/0108.pdf

In that article it said that if they could Guarantee 1,000 homes they would set up a NZ factory.

I looked up some of their projects of the Japanese company as attached. Look at the project for an apartment block. (note in NZ apartments appear to cost a lot more per square meter than single dwellings.

150 million yen = 2.2 Million NZ

17,800 square meters

Cost per square meter NZ $120

https://news.panasonic.com/global/press/data/2018/08/en180807-2/en18080…

Voted for TOP as they are the only party that get's it and has policies to do something about multiple messes we find ourselves in.

Everyone who voted for Labour and National voted for the status quo, so I hope you like to lay in the bed you made. They all told me TOP was a "wasted vote". Well, voting for the two "do nothing" parties is what I like to call a "masochism vote". Let's see how much pain you can endure before you wake up and realise that "voting for the winning team so my vote counts" doesn't make you a winner.

It was TOP or Green for me and I went Green.

I had seen enough in Labour's one term to 1) see they were generally incompetent and 2) were much more vested in the status quo than their 'transformation' rhetoric might suggest.

This site has really changed its tune. All through last year the monthly home loan affordability articles kept touting it was still 'affordable' to purchase a home despite ever rising costs, adjusting the repayment term from 25 years to 30 and basing it on the lower quartile damp dump which banks would probably find several issues with and be reluctant to lend on.

Yeah 2020 was a crap year for affordability, but lets not act like this hasn't been the case for several years back to back now.

You are still catching up then. Site has only changed tune to reflect the last 6 months of unprecedented ponzi profligacy. Talk to any real estate agent and they are saying it's crazy, the more genuine ones especially are totally gobsmacked by what is happening

Back in the day that was called healthy spruiking.

I have to say - when Covid hit, I thought, ah good, finally a correction is coming - but I learned - never bet against the (Reserve) Bank. So now I'm all in the other way. No Central Bank can unwind the ponzis they have created, so I call their bluff. Dollar denominated assets to the moon. Government to run PR, house the collateral damage and create artificial floors to the price of houses and rent through WFF, accommodation supplement, and local government clusterf*ckery. It can't stop now.

Yep - I was long cash, waiting for the inevitable correction. I now can't even contemplate holding anything in cash. We're slowly on our way to MMT, and we all know how that will end up.

Yeah to be fair there was a sweet spot a year or so ago where interest rates were low and prices weren't rising that much. As a FHB I benefitted from that.

That sweet spot evaporated from about 6-7 months ago.

dago... how much free money was given to the RE industry in last years record year and how much has been repaid. Think I know the answer to the second question.

Grotesque amounts of borrowing and not much paid off, it's all being put on tick

This corrupt PM and her cartel won't be happy until kiwis are living in Hong Kong style cage coffins. 'First world problem' my ***

Who needs Satan 'roaming around like a lion seeking to destroy people' - we have an Ardern! Lucifer should be taking notes. That's writing down notes Ardern, not bank notes - don't want to put more ideas in your wee head.

That's harsh - on Satan

True

That is a good characterization of Adern. My experience is that the most evil and bad people are frequently the most charming and charismatic people you could hope to meet. That gives them the maximum scope to get away with their evilness. Obviously bad people are far easier to spot and act accordingly.

I worked with a business owner like this, total sociopath, was constantly throwing all the staff under the bus, walking all over them to get his way every single time. Utterly single and bloody minded about extracting every last cent like blood out of a stone. A truly vile and criminal individual who treated his own children badly. Everyone walked on egg shells around him all the time. He took the wage subsidy for all staff promptly fired them and kept all the money. A-hole.

When dealing with customers the charm came on like flicking a switch. I had never witnessed a jekyll and hyde personality til meeting him. It was disturbing to watch how extreme the two personalities were.

I had that experience too. There are quite a few of them around surprisingly. Their behavior clashes so much with normal decent behavior that at first it is hard to believe what you are seeing. However having seen it in one it is surprising where else you see it. Some are far more subtle, charming, charismatic and hard to spot than the one you describe. They are far more dangerous. Key was a classic example and looks like Adern may be another.

Yeah that sort of narcissistic personality seems to be more common in New Zealand & somewhat encouraged. Some workplaces seem to see it as desirable trait - especially for management positions. Yet these same workplaces struggle with high turn over of staff and wonder why...

Common in Human Resources.

.

Careful, JA is taking notes

Greg... have been waiting for an article like this, which examines things from the perspective of somebody trying to get on the property ladder. For them, it is a horrible situation and we need to take every possible step to fix it for them. Well written.

Horrible for buyers forever after. Enjoy folding your beds up against the wall Japan style, peoples, and showering over the toilet. Unless you have $5million to spend on something 'spacious'

This site is classic. Pre-election at least 80% of those on here were Labour supporters. Pretty obvious to spot noting the number of thumbs up ticks here and there. My how things have suddenly changed. At the end of the day did you seriously expect any government to have a major impact on improving your life ? Its all talk to get elected and then no action. Your in deep shit if your sitting round waiting to be saved by politicians.

Pre-election at least 80% of those on here were Labour supporters

You're either a warlock or Mike Hosking if you know the political stance of the commentators of interest dot co without running a representative survey at the very least. People like you are active commentators around the water coolers of NZ.

Carlos67... all public servants (especially local and central Govt ones) are, almost without exception, worthless, waste of space academics, with nothing positive to offer to society. No politician has EVER received my vote as none of them have ever earned it.

Fairly sure a few of us said be careful what you wish for after that election result, and it has gone pretty much as I thought. Could'nt deliver first term, have'nt got a Sh** show of doing anything in the next three years, but the pain of their policies will be around for decades.

It is the pain of National's policies and the smelly muck is from all of their chickens that have come home to roost. They did NOTHING, actually worse than nothing

To be fair I've been slagging off Jacinda as useless for a very long time now.

Does anyone have the stats on homeownership by generation? In our family its the GenXers that have more than one home.

Houses are the fuel.

Restrictions to supply are the ignition.

Everything else like interest rates etc. is an accelerant, which only works because the fuel has been ignited.

Accerlants won't cause the fuel to burn at a higher rate (increases in prices) unless the supply is less than demand (ignition).

Other jurisdictions, have as low or lower interest rates, high immigration, flat land, etc. but because they have legislation (or lack thereof) that allows supply to equal demand, then they have far more affordable housing, eg 3x median household income.

We have got what we have got because we have legislated for that.

Dale.. well said

And the majority of kiwis are doing well from the status quo.

Is real change ever likely if the majority are swell?

I am not advocating that view btw, but I do think it's a reality.

Politics shouldn't be a popularity contest - but it usually is.

However, if the issue is pronounced enough for the minority(especially if it is a large minority), then it should be the government's role to address that. After all, the government has a poverty agenda even though well less than 50% of the population are experiencing true poverty.

But as I said the other day, maybe we should look at our collective selves rather than the government...

Fritz.. Yes I think as the number of homeowners decreases the chances of major (possibly violent) problems increases. Could be years yet but if we do not change direction.....

Without immigration is the percentage of home owners still going down? I don't think we've got good enough stats on that yet.

Yes, and it takes a rational mind that when one moves from renter to owner to acknowledge that the problem for society has a whole is still there, even if it has been removed for you as an individual.

As you have purchased recently, did you 'feel' any different in how you viewed the data, even though the data had not changed?

Dale.... no difference. Still unhappy (about the housing situation) as I was in the late 80s. I did buy a few houses in Akld back then and held them all till a few years ago but will always rail against the unfair system that made me rich. Bought a nice home in NZ for my family but that has not changed my opinion that as a country we are really messing up. What am I gunna do with the $1000+ a day profit (on paper) on my house? I have not owned a watch or telephone for 3 years and drive a $4500 car. I just need enough money so that I never have to sell another minute of my time. And on the positive side, the unfair, divisive inhumane situation that is our housing crisis allowed me to stop selling my time a long long time ago. Good luck.

BTW: I rented overseas, mainly in Thailand for over 20 years so have experienced both sides first hand.

Yes, I can see where people like yourself make that acknowledgment, but I also see that others think that the present situation is some immutable law of the universe, to be followed innately.

These are also the type of people, that given any situation of the day, would take full advantage of that situation, even though it might be reprehensible.

They make Golem look like Father Christmas.

The question might have been directed to me?

Well, I think you can see by the concern I express regularly on this website that I am still very concerned, even though I now own.

If I am honest though I was glad for some post-purchase rise in prices, as I was fearful my timing was awful and prices would plunge with covid.

But to be honest it wouldn't bother me now if prices plunged 20% and wiped out my paper gains.

I have kids whom I would like to hope had some reasonable chance of home ownership. I am unlikely to be able to help them into home ownership very much.

I also think this crisis is a disaster for the country in terms of the bigger picture.

Same here. I own a house (no mortgage), but worry that my children and their hard-working friends will never be able to do the same. House prices are out of control.

Yes, it was, only because you shared that you recently purchased, but as we can see your feelings about being on the 'other side' are shared by others, although I would say it is not by the majority of homeowners.

The point is that it takes a very fair person to say they don't mind the price dropping, although it might not extend to negative equity :-)

Dale... TBH I blame the system far more than the people taking advantage of it. Most people will always put the personal financial gains of themselves (and their children) above all else. The system needs to put kiwis looking to get on the property ladder and/or paying astronomical and ever increasing rent first: before immigrants, before landlords, before employers seeking cheap and easy options. Anything that even might make a difference should be at least tried.

What annoys me (about some posters on here) more than their greed is that many of them think they got where they did solely through hard work and being smart and financially savvy and they seem to genuinely believe things are not much different for a young person today. If you were born between about 1955 and 1970 you have been fishing in a marine reserve. The young today are fishing in the Hauraki Gulf without a boat.

Agree.

I wonder if those people genuinely think it was as hard back in the day, or they are just trolling.

I think most of them genuinely think that...it's BS!!!

I think they really believe it, which shows how lucky and financially lacking they really are. Anyone with even some idea would see things are so much harder now, impossible for many.

Yes, agree 100%, and great analogy.

The trouble with any systems is that if you stay in them long enough you become institutionalized which means in our present housing system it really becomes the lunatics running the asylum, or the classic scene in 'One flew over the Cuckoos Nest' where the patients were able to pass themselves off as professionals with their 'Mad Scientist' look.

Hot housing market. I'd say...

• Property is the fuel

• No return on savings is the ignition

• Cheap credit is the oxygen

• FOMO is the accelerant

As I said, everything else like 'No return on savings,' 'Cheap credit', 'FOMO,' are accelerants.

If supply can equal demand, there is no FOMO, there are no rentier capital gains to be made for the 'No return on savings' money as it is invested in the productive economy eg new business start-ups, and if 'Cheap credit' makes housing easier to buy, then the supply expands to meet that extra demand, so no price increase can happen by a demand shortage.

This is how it works in jurisdictions with truly affordable housing.

Without the demand shortage, which is an artificial constraint caused by Govt. legislation, then none of these other things will cause house prices to increase as they have.

Just wait it out. No one takes their houses with them into the grave. The young of today will be the older generation in a few years. The wealth of older generations will invariably get into the hands of the younger generations over time.

What wealth?

The ageing of today are going to have to sell whatever they have to live from.

That's what virtually 0% interest rates does. First it collapses interest income; then is eats away the principal. Then whatever asset are left (the house?) is sold to put food on the table, so to speak. And the more elderly we have, the more sellers there'll be.

Message? There ain't going to be much wealth left to 'pass on'.

The quiet ones ....

Don't see any statistics on the total of reverse mortgages

The money they use to put food on the table goes to someone. The house they sell to get that money goes to someone. Their wealth stays in the economy long after they have passed on.

Yep, it goes to banks in the form of interest payments and then the equity is released to them in the form of reverse mortgages.

I totally agree. As a retiree (home paid off), I figured I would at least be able to leave my children a house LOL. I was hoping that I could supplement my retirement with interest income. At the rate I'm going, I won't have much left to 'pass on'. (Yes - still LOL as the joke is on me).

The wealth of the older generation is going to the likes of Bupa and Rymans

Lovely, a caste system in the making

We are becoming just like Britain, from which many of our ancestors escaped with it's entrenched class systems.

Having lived in Britain, I would say that New Zealand is far worse.

Yeah worse now. Didn't use to be.

It's been a great few years and with St. Jacinda, Patron Saint of Property Investors, leading the charge I'm sure we can push interest rates even lower and quantitative easing even higher.

People used to talk about "Generation Rent" but now it's half the country. Nothing rises as fast as house prices: https://www.nzherald.co.nz/business/house-prices-twenty-years-of-housin…

Great article. Somehow should hold this graph up to Jacinda at a news conference and ask "can you tell me in how many decades it would take my wage inflation to appreciate to a point of an unaffordable DTI assuming house price inflation stays stagnant?"

Good article. He touches on something I mentioned the other day - the really negative impact on discretionary spending that comes from a lot of people paying far too much rent (or too much mortgage).

He also touches on something I raise higher up, about the politics of it all, when 65% of the population own houses....

I see many times how the argument is between homeowners and non-homeowners. This should not be the case.

The argument/question should be, 'what should be the real cost to rent or own?'

There are many good arguments why at certain points of your life it is better to rent. Not many people go from living with parents (free or subsidized rent) to owning their first home. For example, research has shown that because rentiers can move more easily than homeowners, for that time they are rentiers they can take advantage of better work opportunities and put themselves in a better future financial position for when they are ready to buy a home. Interestingly because most of our money goes into housing, then there are fewer business opportunities in NZ so many then rent overseas to get that opportunity.

The benefits, (non-financial) of homeownership are well understood, although many jurisdictions overseas offer almost those same benefits to long term renters.

So the real question is, if you are going to rent or buy, what price do you want to pay? Would you prefer to buy at 3x your median income, or rent such property at its relative yield, or would you prefer to pay twice or more than that multiple and the corresponding higher rent in NZ?

Would you like a mortgage that is over half the amount you pay presently? What would you like to do with all that extra money?

Or does it not concern homeowners that approx. 1/2 the value of their property is what is known as non-value-added costs? That is, only exists because of monopolistic advantage.

Al Capone is credited with the quote where he said he could get more money from people with a kind word and a gun, than a kind word alone.

Many of the commentators on this site do not seem to realize the gun that is pointed at their heads every time they rent or buy.

But at least, for those benefitting from holding the gun, in the words of both Al Capone and Jacinda Ardern - be kind.

Boomers are clueless

So says the comments

Auckland sales 2020 up 17% on 2019

Lifestyle blocks: 54%

Apartments: 7%

Sections: 10%

Pretty clear people are fleeing for space

Space and land banking?

As a homeowner, I feel no pleasure at all watching house prices go up. I am happy in the house I have and would not worry if the price of houses halved from where they are. In fact I would prefer if they fell as it would give more of my fellow citizens the chance to own their own home. There needs to be a more sensible approach to immigration/population if we are to hope to become a fairer society.

Same here. I realise that if house prices go down, I would be able to purchase a new house for less.

It's so depressing its almost funny. The least likely people to be affect by Covid are the ones paying the price.

It's so depressing its almost funny. The least likely people to be affect by Covid are the ones paying the price.

This will all end in tears.

Yes this will end in tears. Too many people rely on 2 incomes to pay exorbinant mortgages and the correction date is nearing. We need to put a tax on unrented or empty houses so as of today people are buying and sitting knowing that prices will go up. Greed how about starting a business that adds financially to the economy.

I have said for the last couple of years that an international credit crunch will strike in 2022 and that will crash NZ house prices by circa 20%.

I feel less confident in that now - I reckon it's a 30% chance - but I am going to stick with it, for fun.

If the bottom falls out of the USD all bets are off. Times almost up too, tick tock, tick tock, MF. https://i.imgur.com/bag3sKl.jpg

{kind=link}

Nice graphic.

I hope the next reserve currency is not a spiked club.

Great article

OPINION: The prime minister has not just failed to dampen down, but has actually poured petrol on the pyrotechnic panic-buying that has seen housing prices spiral out of control.

Thats the reason why I gapped it to Aussie... no way in hell could I get on the property ladder. Shit wages and nose bleed prices for shit houses in NZ. Watch as soon as the boarders open... all young people will come to Aust so they can at least make a go of life. Who's gonna pay for the boomers rentals, or pay the taxes for the boomers health system, or at least make their avo toasts?!

The problem is for every kiwi that leaves to Perth there are 20 immigrants to replace you. There are millions of people who would sell their soul to live in NZ especially after 2020. So it won’t matter.

You just stated the obvious, quality vs quantity. Just wait until your health failing you, then don't complaint about standard this & that, subsidy this & that, eligibility this & that.. just go sit on NZ waiting list be it public or private. 20..phsst of money launderer, crims, drug agents, NZ is not the place for young dentist, pharmacist, nurses, doctors, specialist - all just use it as back door to OZ

My comment was from a Govt perspective not mine. But I do agree with some of what you said re medical.

But I lived in Australia for many years and I can tell you NZ is far preferable in many ways.

Totally disagree. Aust is a significantly better place to raise children. Double the wages half the cost. Best beaches in the world. Just finished filling up my vehicle... $38. How much again, is it in NZ. Best thing for Maori families...No racism.

I dont disagree... the government will replenish its population. However, good luck selling the million dollar houses to immigrants that don't have 2 cents to rub together...plus once citizenship is achieved, a nice flight to Aust to live is usually on the cards!

Australia is going to be in deep trouble with climate change. More and more of it is becoming uninhabitable. Wouldn't even consider moving to Australia.

Theres this new contraption called air con. Most buildings have them in Aust. The poverty issues in NZ... I have never seen that level of poverty like I saw in NZ. So uninhabitable for the majority that don't have a spare $170k deposit for a house. I saw a shit 3 bedroom house in rural NZ for $490 rent per week..... ffs. The average wage was $38k per year in that place. Watch every s young person scramble to get over here. NZ has cut off its nose to spite its face.

Great, stuck indoors for your entire life as you'll fry if you step outside.

Nothing to do with just the outside temperature really, its when you turn on your tap and no water comes out your in trouble. Australia is drying up, has been since I can remember. Uninhabitable is when the water is gone, not when your heatpump breaks down.

I think you missed the point mate. No one can afford to live in NZ. I have lived in both countries and can tell you with absolute certainty, Aussie is a much better country to live in. They have desalination plants in WA to ensure water supply. You are trying to place negative narrative to support your reality... but in all honesty its already happening. Flocks of kiwis are coming...because they can afford a $800 per week rent on $45k salary per year. Simple maths really.

I think you missed the point mate. No one can afford to live in NZ. I have lived in both countries and can tell you with absolute certainty, Aussie is a much better country to live in. They have desalination plants in WA to ensure water supply. You are trying to place negative narrative to support your reality... but in all honesty its already happening. Flocks of kiwis are coming...because they can afford a $800 per week rent on $45k salary per year. Simple maths really.

at least we can afford an 'indoors'. Not like in NZ... because of gready slumlords. Currently rent a 4 x 2 less than one year house, 15 mins to the centre of Perth. $320 per week!!! I make more than DOUBLE what I made in NZ, because of the mining sector. My wife is also able to find awesome paying work...couldn't in NZ. We will be looking at a mortgage soon... the payments $490 per week. BTW govt will give us a financial incentives to build... bye bye younger NZ generation!!!

...

In terms of relative valuation to international housing markets, New Zealand home price to income ratio aren't that too exorbitant- try Luxembourg, Portugal and Spain.

There's still room for an upward valuation on New Zealand properties.

Got a link to any of that?

No need for it Dale, all you have to do is just keep on promoting it.. until the OD result take over. The binge must continue without the limit (just don't tell the patrons).. then observe.

An opinion without evidence is just an opinion. As someone that knows more about the median multiple than most, the three examples you give may be correct, but when you look behind the data don't prove your point, unless your point is because some other places are basket cases, then that is justification for NZ becoming one too.

The 2021 Demographia report will be out any day, which will give the latest on median multiples.

CWBW... Portugal and Spain? As Tony Montana said (in Scarface), "don't get high on your own supply". (pun intended)

Lol, all of this is purely academic. Once the Ponzi housing bubble burst, all statistics and the identities of the winners and losers are going to be dramatically different. It is not an if, it is only a when. One just needs to look at history.

Believing that economic fundamentals apply only to the rest of the world and, for magical reasons, not to NZ, is utterly delusional. Believing that, in international terms, the NZ housing market is not grossly overpriced is wildly optimistic to say the least, as it is believing that the only asset class not subject to natural cycles (and bubbles) is residential housing.

Guess its all relative, my girlfriend (30) has nearly paid off a 3 bedroom house in central auckland when she bought there in 2013 while i'm (28) saving up for my first house (or whatever). We go around to look at places that could be good for me. I save a decent amount and go without, doesn't really bother you if you just want to make a go of it. But there does feel sometimes that a lot of people just give up and go on a holiday, not hard to see why.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.