By Greg Ninness

The urgent need for the Government to rein in rampant house prices has been reinforced by interest.co.nz’s latest Home Loan Affordability figures.

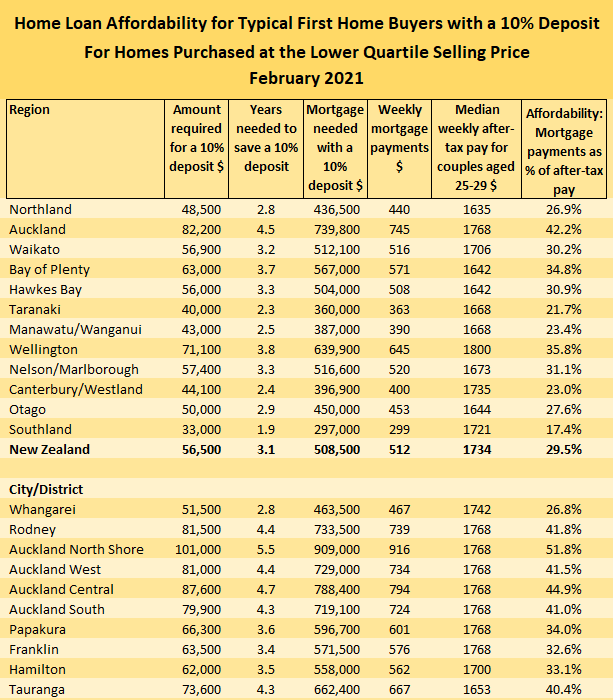

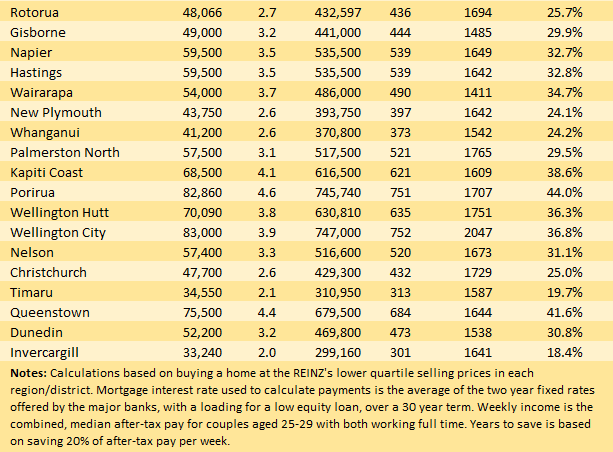

These show the Real Estate Institute of New Zealand’s national lower quartile selling price increased by $40,000 (+7.6%) during February, rising from $525,000 in January to a record $565,000.

Over the 12 months to the end of February the national lower quartile price increased by $106,500, up 23.2% for the year.

In the Auckland region the lower quartile selling price increased by $122,000 in the 12 months to February. But the biggest increase of $160,000 for the year was in Hawke’s Bay, followed by Wellington +$151,000, Bay of Plenty +$110,000 and Waikato +109,000.

The smallest increases were in Canterbury +$66,000 and Northland +$70,000.

Those extraordinary rises mean lower quartile selling prices around New Zealand have increased by an average of $2048 a week over the last 12 months.

The lower quartile selling price is the price point at which 25% of sales are below and 75% are above, representing the lower end of the property market that is most within reach for typical first home buyers.

However price increases of the magnitude of those over the last 12 months will have almost certainly kept the goal of home ownership out of reach of most first home buyers on average incomes, because the amount required for a deposit has likely increased faster than their ability to save it.

Even the amount needed for just a 10% deposit on a home at the national lower quartile price would have increased by $10,650 over the last 12 months, rising from $45,850 in February last year to $56,500 in February this year.

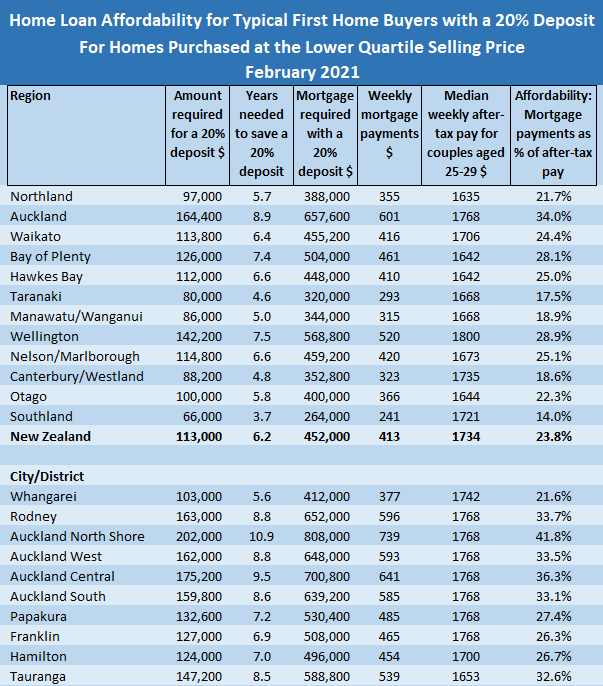

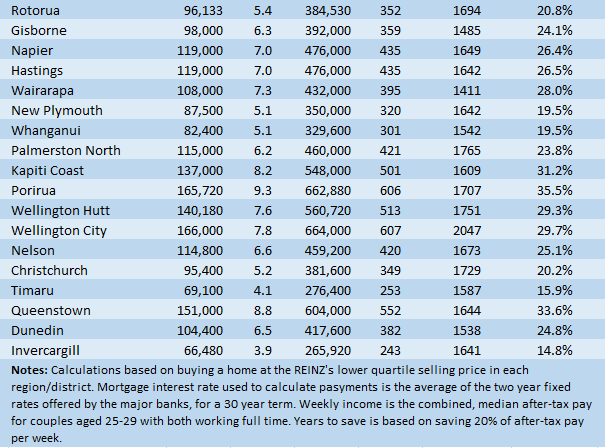

In Auckland, the country’s most expensive housing region, the amount needed for a 10% deposit on a lower quartile-priced home increased by $12,200 over the same period, from $70,000 in February last year to $82,200 in February this year. You can double those numbers for a standard 20% deposit.

Unfortunately the bad news for first home buyers doesn’t end there.

Mortgage interest rates continue to hit record lows, with the average of the two year fixed rates offered by the major banks sinking to 2.53% in February, down from 3.52% in February last year and 4.26% in February 2019.

You would think that a slide in mortgage interest rates would have benefited aspiring first home buyers but that’s not the case, because house prices have risen faster than interest rates have fallen.

The amount of money needed for the mortgage payments on a home purchased at the national lower quartile price with a 10% deposit hit a record high in February. Think about that for a moment. Mortgage interest rates are at a record low, but the mortgage payments for a home at the bottom end of the market are at a record high.

In Auckland the situation is even worse. Not only are mortgage payments on a lower quartile-priced Auckland home at a record high, they have been pushed squarely into unaffordable territory.

Interest.co.nz’s Home Loan Affordability Reports have long considered that mortgage payments start to become unaffordable when they chew up more than 40% of the homeowner’s after-tax income. The median after-tax pay for couples aged 25-29 in Auckland, if they both work full time, is $1768 a week.

The mortgage payments on an Auckland home purchased with a 10% deposit at February’s lower quartile price of $822,000 would be around $745 a week, or just over 42% of the median take home pay for couples aged 25-29 (the monthly breakdown of affordability figures with both 10% and 20% deposits in all of the main housing districts, is set out in the tables below).

That means they would likely already be finding things tight while interest rates are at record lows. But if they suffered a drop in income or if interest rates started to rise, they could find themselves in financial doo-doo.

If both of those things happened at once, the doo-doo could get very deep indeed and that could have implications not just for affected homeowners but for the legacy of Prime Minister Jacinda Ardern. Almost certainly, the greatest achievements of her terms in office so far have been steering the country successfully through the COVID pandemic and avoiding the worst of its potential health and economic impacts.

But a consequence of that has been the debt fuelled, speculative housing bubble, which is now so serious that it risks the PM and her Government being remembered as major contributors to a new class system based on property ownership, and for burdening the economy with a growing mortgage debt millstone.

This week’s housing policy announcements by the Government showed that it is prepared to act decisively to address those problems. The changes made to the way residential investment property will be taxed are probably the most significant changes to impact the property market in a lifetime.

Although it will be several years for them to be fully implemented, they will likely have an immediate cooling effect on the market. And with that will come hope for aspiring first home buyers. The changes should put a stop to prices spiralling out of control and put the dream of home ownership more within their grasp, turning their mood from hopeless to hopeful.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

217 Comments

I agree that something had to be done... but not with the proposals. The arend administration is making a hash of housing

They've given 'hopium.' Give the serfs something, even if it's the promise of extra turnips they can call their own.

"Hope" doesn't help FHB to own a property. Sound judgement and proactive planning does; not knee-jerk reactive responses.

First they blamed the Overseas buyers (aka Asian buyers) for the housing crisis..... They banned them from buying.... Prices still went up.

Then they blamed the RBNZ & the Banks for the housing crisis..... Banks proactively reacted and lifted the LVR for investors even before the Govt said anything..... Prices still went up....

Now they are blaming LOCAL investors for the housing crisis..... So they add all these deterrents....... I wonder what will happen now? (*Sarcasm*)

Not once have I heard the Government point the fingers to themselves and say "hey, we are the problem. we need to fix ourselves first." It's always easy to point the blame at someone, but hard to point it at yourself.

Two major reasons for house price increases:

1. Lifting the LVR, this should have never happened

2. Record low interest rates

The latter means people just can’t put money into term deposits for a decent return and hence the money directed straight into property

I am glad the tax deductible part has been removed. At least this somewhat evens the playing field.

Please add interest only loan to it specially when interest rates are so low.

This interest only tool is not for such low interest environment as is bound to trigger speculation.

This NEEDS to happen. Prices are at a point where a serious correction at some point is a near certainty. The more investors you have on interest only terms the higher the risk of a disorderly collapse, as IO terms will not be viable in a falling market. Going from IO to P&I doubles monthly payments.

This isn't about house prices, its about financial stability.

Yeah hopefully you are still glad when you are see The tax is being added into rent for next few years.

There needs to be a correction at some point. This is highly unsustainable. Rent rises will be calculated in the CPI so here is me hoping that will kick off the “inflation” that Orr needs to see to start increasing the interest rates. People won’t just keep paying for whatever a landlord asks. I’m hoping in May they make it so that investors cannot have interest only loans and be made to pay fair share of principal back just like FHB or owner occupiers and let’s see how the house of greed falls. It all has to start somewhere. We cannot accept and be okay with never ending greed.

Rent makes up around 9% of the CPI so if rents increase by 5% on average that would only impact the CPI by less that 0.5%

Jack...don't worry. next change will be that rent increases are pegged to wage increases ie about 1.5% PA. The Govt are well aware that too many investors will try to pas the costs off onto renters who can least afford it so they will have to peg rent rises.

This is indeed badly needed after all outrageous threats from investors in the past couple of days, if their investment becomes non profitable after the latest changes they should get ready to sell which will leave more homes available for owner occupiers. We do not need investors, we really do not need them in the current environment.

Really? Can Labour provide all rental property for all renters in New Zealand? Tell all renters now move out to make sure their landlord does not make any money . Let’s see how everything goes.

Let me tell you how everything would go. Less investors means less demand hence less competition to buy a home, some of those renting would be able to buy their own home which now they can thanks to the greed of a few. Nobody will need to provide anything to anybody, we just need to push out usury from our housing market.

Haha. You are still live in a your dream.the fact is Only small part of renter can a house. Can the govt give free money to all renters to buy a house? Answer is “no”People need to borrow money to a house. Where can they borrow ? The bank or other Finance company.People need to meet a lot of requirements to borrow money to buy a house.Less investors, does not mean they will lend to anyone.Another question is Why property owner have to sell their house for a cheaper price? Just because less competition?Some people have good saving history, good job and credit history will get loan from the bank and buy their house. However it is going to be small part of renters. A lot of people still need to rent house to live.

So we need more usury to mitigate the very issues usury already created? Exorbitant prices need to go down and your argument is just confirming how unsustainable this is not just for prospective buyers but also for landlords.

You clearly have no idea what your talking about. Investors take a multi year approach when buying a property for rental purposes and thus like most business want certainty - this latest knee jerk response to a basically Auckland problem will not encourage anyone to invest now as Labour has broken election promises and is thus an unreliable government. If you cant trust them to leave common business rules ie interest rate deductions you have to wonder what sector is next

The NZ needs economy and society need more housing investors like a bullet in the head.

There is ONE reason for why house prices have gone up - and no one seems to mention it.

The NZ population has increased at a rate greater than expected.

So what are you suggestions? Prices in Auckland (where most of the foreign speculation occurred) actually were flat from 2017 until recently. Was that because of the FBB? Who knows, but we can’t say decisively that it didn’t have a material effect.

I'm confused by your comments Albert. "Prices in Auckland (where most of the foreign speculation occurred) actually were flat from 2017 until recently." have you got some data somewhere that backs this up? Have all the news stories of late with skyrocketing house prices been wrong? I'm struggling to make any sense from this statement.

Auckland was flat from mid 2016 until late 2019. Accounting for inflation, they fell. Same for mid 2007 until 2011.

https://www.interest.co.nz/charts/real-estate/median-price-reinz

See comment above

ALL of those factors can have some portion of blame laid squarely at their feet, all of them, including successive governments allowing it to culminate in this. Now we have a government trying to fix this while not crashing the market. Unfortunately, for so many traumatized people out there unable to afford any sort of home, including a rented one a massive change is required.

Just building more overpriced houses will NOT solve this, they will still be unaffordable and they just be further fodder for the economic cannibals to exploit the need for people to be housed.

The ONLY solution that may achieve a softer landing is a massive state house build, start with housing those at the very bottom and work your way up till affordability meets supply. Prices might eventually still come down, but it would be a bit slower.

For now, investors are screaming, something must be right about the new steps the govt has taken.

I am surprised. Do couples in Wanganui earn only 13% less than couples in Auckland? Why isn't half of Auckland moving to Wanganui?

Heaps already have. Flight runs daily to and from Whanganui so many can still commute

I’ve considered it. But-

1. My job (fairly specialised), my family, my wife’s family and my friends are in Auckland;

2. I wouldn’t feel great about buying a property in Whanganui by outbidding a local. We’re just exporting Auckland’s lunacy.

Because perhaps it’s Whanganui? Auckland for of its traffic and housing woes is a brilliant city in a great setting, and with a nice climate. International airport, excellent healthcare, beaches, top restaurants, Hauraki Gulf destinations like Matakana, Sandspit/Kawau, Great Barrier and the other gulf islands. Then there’s the Manukau Harbour, west Auckland’s vineyards, weird, wonderful places like the Kaipara, South Head, Leigh, lots of great golf courses....

You mean those beaches that you can't swim at due to toxic algae?

People kid themselves with this all the time. A lot of what you've mentioned isn't unique.

However the weather is decent and there are some okay views from a few spots.

This is the crux of why all the regions have gone mental over the past few years. Big city wage premium not enough to offset big city living costs = people not moving to big city/young people moving to smaller centres to buy a house = big supply/demand imbalance in smaller centres = big price increases.

"But the biggest increase of $160,000 for the year was in Hawke’s Bay . . "

Much to do because they still haven't addressed the supply problem where over 1% of the resident population is living in motel units.

https://i.stuff.co.nz/national/124624124/napiers-long-social-housing-wa…

It is more about availability rather than affordability.

Exactly. With 2000+ people in Motels and holiday parks in Hawkes Bay and no new affordable rental housing supply in sight there is only one direction rental price pressure will move things. Rents were $350pw for a 3 bed 2yrs ago and the same house is now $470+. It is a little hopeful that it wont be pushed further by these changes. I don't agree with it but simple supply and demand. Christchurch is a perfect example of what happens when you have over supply. Essentially flat prices and flat rents for 9 of the last 10yrs. Unless there is an immediate and huge supply response from central government there are no downward pressures on rents I can see and this has just added another upward pressure...

I doubt it will be enough to turn the worm significantly downwards, which is what is really required in an environment where we might get higher interest rates in the future and where wages are flat. I am guessing plateau for a while as people wait to see if anything else is added.

2 days ago, if I decided to sell my soul, I could have bought an investment house using the equity in my own house, the rent would roughly cover the mortgage, I wouldn't pay any extra tax, and I could wait for capital gains. Now if I did that I would have to come up with 33% of the rent to pay in tax. What was a no brainer for soulless people in the past no longer sounds that great. This has to make a serious dent in the number of new investors, housing demand, and house prices doesn't it? And there will be some existing PIs that can not afford that tax money that have to sell. Yes rents may go up a bit, but not 33%.

Yes rents are going up at least 30% the next 4 years

Why? Only out of sheer greed.

Supply and demand, a concept that lovely auntie Jacinda and her dumb followers never able to grasp.

Dumb follower never questioned why she never delivered kiwi-build (and never is mentioned again), why did property still had a crazy boom after they banned greedy foreign buyers. Because no one is smart enough to out-wit the market invisible hand. Not even the charming J. And there they are, doing it again, more government intervention which would hurt the lower income even further. Wait and see.

Won't happen, there is just as much that rents can go up, if renters can't pay they won't and investors will be either force to take losses or sell.

Medium salary renter and first-home buyers will be pushed to rent or buy smaller units or apartments, anchoring a 700k price point for such property in Auckland. People in IT industry with 120k+ would continue considering to buy a property with land or rent such properties.

The decision would get everyone housed, but lower the living quality. And it would only be this case if labour could deliver, if another kiwi-home happens again, property would still rise unfortunately.

Oh, the hand is visible alright. It's called the 'ham fisted hand' of poor Govt. policy that has allowed either crony capitalism when National was in power, or crony socialism when Labour is.

The true invisible hand that Adam Smith talked about is the light hand of Govt, where the market operates in a truly competitive market which you think is your free will yet just happens to also be the rules the Govt. would have incidentally prescribed if you hadn't already happily voluntary done so.

Last round they thought introducing kiwi home + banning foreign buyers would do. Turns out they could not deliver the phoney-project and Kiwi investors were just as greedy and speculative as the Chinese :)

The only solution to the housing bubble is to up the supply and boost up economy so that GDP goes up average Kiwi gets more skilled and earns more.

Labour is so good at convincing people in the sinking ship that using a bigger bucket to pour out the water is a killer idea. They blame Nationals for causing the ship to crack, but never works to fix the hole.

The majority of Landlords with say 1 or 2 rental prpoerties are not greedy . They are just looking for some sort of return on capital employed. Remember they are the ones who take all the financial risk that tenants pay.

I know from doing the numbers last night , my 600k rental which has a current debt of 60 K will lose money once the no interest rule comes in. So i take all the risks yet get no return on my 540K . Please explain how im greedy

Uhhh. So your rental will now lose money because you cannot deduct the $30 per week of interest on the $60k? Maybe being a Landlord is not for you, stick the $540k in the bank and earn $50 per week.

'Please explain how I'm greedy': well, you have an asset worth 600k, and given your low mortgage, I assume you bought that a while ago. A large part of the value of your asset - the benefits of which will flow directly to you - has been built on the backs of, and to the detriment of, hard working younger New Zealanders. Now, this isn't your fault - but where the greed comes in is that you seem to think that you not paying a very small amount more in taxes is more important than younger generations of kiwis being able to have a shot at a stable home and a decent retirement.

Also, if youre right that you get 'no return' on your 540k (unless you bought very recently, id bet youve received a significant return on your initial investment), then sell it. Its also not clear why you think that taking 'the risk' should guarantee a return. Part of what it means to take the risk is to run the risk of not getting a return on your investment. Youre experiencing the downside of risk investment. Your options are to stay in the game, or to bow out. Simple as that.

Why did I suddenly remember that oft quoted line from the character Darryl Kerrigan from the movie The Castle when I read the previous comment?

Good luck with that prediction - rent is set by the market not landlords.

Say you increase your rent from $500 to $600. Tenant A can no longer afford it so he moves out. Tenant B who just left a house where the rent went from $600 to $700 discovers that he is now in your price bracket and so occupies the house that tenant A used to occupy. Tennant C occupies the house Tennant B used to occupy (paying the $700 rent), etc. when the whole market moves due to government pricing signals what the market can bear changes. Neither tenant B nor tenant C are willing to be homeless so they take the lower quality accomodation which is all that they can now afford. Let’s say 70% of tenants in each price band end up having to move to lower quality accomodation, the only landlords who need to worry are those renting out houses in the very top band, but their clients are the tenants who are the most likely to be able to absorb the increase.

Your market tolerance logic only works if a significant portion of tenants would prefer to be homeless over moving to lower quality accomodation (ie. they need to have the ability to go without)

People 'go without' all the time by living in arrangements they otherwise would not like to - flatting/living with family.

If landlords need to keep properties full, they will need to meet the market.

Or hope that there is a housing shortage severe enough that demand for rentals persists regardless. Perhaps a friendly Prime minister who will disincentivize the construction of new investment (rental) property by removing the deductibility of interest so as to keep supply short and demand high? The new build exclusion will either not be enough to incentivise new builds (be for too short a duration preventing the builder from recovering costs, which can take 20-50 years to recover) or a mechanism to Rort the system whilst being to little to incentives new builds ( if a new build is tax deductible for so long as you hold it, you shift it to interest only and pay down principle only on the rest of the portfolio~ forever.

Many landlords won’t want or need to increase rents eg those with low debt levels. Their houses will be readily tenanted. Landlords who try to increase rents beyond market norms will probably find their properties remain untennanted for longer periods. Also, there doesn’t seem to be a shortage of rentals in Auckland. Yesterday there were over 5500 Auckland rental properties advertised on Trademe. More than 3500 of those were identified as ‘ available now’.

I agree, and with the latest covid case highlighting that the vaccine doesn’t actually stop transmission theres every likelihood that our borders will be severely shuttered for the next couple of years.

The "market" has pushed rents up 6.8% in Hastings in the last 12 months and 44% in the last 5 years. With 2000+ people in Motels in Hawkes Bay rents will continue to rise without a massive supply side response. How much they will rise can be argued.. but there are only upward pressures as we sit here today. Every region is different, but ChCh is the only place currently with close to a supply/demand balance.

Is income increasing by 30%.

I guess that will just compensate for the big drop in rents that occurred as interest rates went through the floor. Oh, wait....

Did rents go down when interest rates dropped by ~50%?

You're right, JJ.

There are enough greedy landlords out there for us to say with certainty that there isn't a 33% slack in national rental prices.

Even if these changes force a handful of existing investors out of the market while making future investments less attractive, that would leave more new and existing stock available for FHBs.

Yes, you've nailed it. Leveraged money is out of the market now for existing residential stock - what were previously positive or neutral cash yielding properties are now negative cash yielding. Completely unattractive to own even if you can jack rents a bit. And good luck in the short term with emigration likely to restart before immigration as northern hemisphere opens up. Delayed OEs etc. Slow foreign student ramp up.

Residential prices in the FHB zone will drop back rapidly to erase their post-Covid bump, more buyers will get on the ladder. Happy days.

Investor money will flow into commercial property syndicates and the like which now have a tax edge.

That's right. Yesterday an MIQ worker who had received her second vaccine 5 days ago tested positive for COVID.

Various vaccine candidates ranging from testing to delivery stages are effective in eliminating the symptoms from the infection but not so much the infection itself.

Which means mandatory quarantining is here to stay for a while and will hinder tourism and migration with all the added costs and logistical issues of travelling.

Bruts..I hope you are right. People investing in commercial property does not destroy the dreams of young kiwis like property investment does. NZ has just begun its journey to a (far) better place.

If they can't buy then, they can't buy now and they wouldn't be able to buy tomorrow.

Perhaps prices need to come down more then.

No according to JA and GR we just need moderation of house prices which is code for we don’t want house prices to fall but also don’t want 20% per annum inflation.

JA and GR can't be seen to say they want prices to fall.

But prices can and probably will fall.

Without uttering the actual words (which would be a political no-no) JA gave the impression on RNZ this morning she would like a drop to take us back where we were only a few months ago.

JC was interviewed on the same topic and was truly awful. If she is still in charge next election National will lose again.

Lately I have been a National voter. I voted for Collins last election, but I wasnt happy about it at the time. If Act gets through the next 3 years and those newbies show some intelligence I will dump National with gusto. JC is not clear in her thoughts. She says some stupid stuff. And all those religious folk in National scare me. Muller should have gone. In other words its still a hot mess.

National needs to find a way to get David Seymour to lead them. Collins is hopeless, and there’s no one else at the moment. Come back Bill English.

Lol, yeah the one rather religious dude I was keen to see carry on in charge. Judith has been good at times but too frequently she just talks rubbish. Her smart mouth gets carried away, and she becomes petty. Its a shame.

Seymour has been excellent. He's the only credible opposition currently.

.. and last I heard, he doesn't even own the home he lives in!

He's of the rich, by the rich, for the rich. Let's not pretend otherwise.

No he’s certainly not I actually went to school with him.

Very sharp and an astute communicator who took an minor party to some significant standing. More in touch than Jacinda who incidentally I voted for.

This narrative is fine that do not want house price to fall, when house prices goes up from 100 to 140 and than fall may be to 120 but still not fallen on an annual basis, in fact gain of 20%.

This politicians have changed and play on the fear that is thrown at them by bureaucrats and politicans fall for it.

The problem is still one of affordability. Unless your DTI is around maximum five then a house is still not affordable if you want to have a life..

But if you reduce competition from those leveraging capital gains to capture a record portion of purchases, then suddenly prices will need to meet what FHB CAN afford. Sounds like a good outcome for FHB, no?

I guess time will tell how much competition from investors has been removed... perhaps a few more measures can be added (DTI and IO restrictions) if they haven't gone far enough already.

I suspect desirable property will still be a good investment, by and large. The new settings, ie a de facto CGT and not being able to offset interest payments are pretty standard, and prices are still going up in desirable cities worldwide. All the good locations have gone. Pokeno isn’t Devonport and never will be. Best plan is to buy the best house in the best place you can. That capital gain will never be taxed, and you can always trade down at a later date.

"The new settings, ie a de facto CGT and not being able to offset interest payments are pretty standard" - perhaps I am missing something ..

Please give examples ( other than the UK , where tax deduction at 20% is / will still be allowed ) of places where it is not possible to offset rental property interest payments for tax purposes.

So is it going to make a difference to prices or not? What do you even mean? That only superior beings such as yourself will ever own property regardless of price?

Sorry but banks will need to lend to someone, and with investors prepared to borrow heavily about to dive off a cliff, who else is going to borrow? Some FHB will be in a position to buy, but some won't. There may be cash buyers still out there but they might want to hold off on buying as they are not desperate to buy, want to see if market drops. Overall the demand has SHRUNK, maybe the supply of homes for sale will increase too as some try to cash in

dago

Property speculators will “dive off the cliff” as extension of brightline test and removal of tax on interest will hit them.

Property investors will likely not.

For property investors it should be about long term and yield. While interest rates remain low around the 2% and net yields around 3 or 4% (but 5 or 6% on equity) the loss of tax provisions will be a negative but not a ground breaker. Never bought a rental that wasn’t cash flow positive. The reality is that most investors - whether the Mum and Dad for retirement or the large portfolio holders - the extension of the brightline test is irrelevant - and for most if there is need to sell under 10 years , well then most would be happy for a CG bonus and wouldn’t be concerned about a 33% tax on that.

These changes are going to affect speculators - not investors significantly.

Yes expecting some drop in number of investors - that happened back in 2015/16 with introduction of brightline test and LVRs and perception that the market was overpriced/peaking but according to RBNZ data it fell only from around 18 to 19% of all sales to 14 to 15% but hardly reminiscent of “falling off a cliff”.

For a number of reasons, for many older people, a rental property will remain to be seen as an important part of a retirement portfolio. And certainly a capital gains (BLT) and tax was not a consideration.

A look in one of the facebook property investor groups and it sure looks like most of these so called investors are what you call speculators going by the amount of toy-throwing and victim card playing from the announcements yesterday.

The non FHB aspect is going to decline dramatically, I believe. Whether there are many investors out there who can buy properties without taking on a decent bank loan, now would seem a crazy time to buy - there's not exactly any good deals going. Not a very good return likely compared to previous years. Older people tend to be much more conservative than someone would was playing spacy games or skateboarding through the GFC. So a big shift in buyer demand could be on the cards

The government has basically created a special class of investment property with greater yields than everything else (ie. if you sell a property you bought before the 27th of March you’ll never get the same yield again). Investors will hold property acquired prior to the 27th of match until FY 2026 when they lost their special privileges.

They did not create a special class of investment, they have put in place a plan to remove that special treatment by FY 2026?

Exactly, until FY2026 property bought before 27 March 2021 has an advantage not accorded to property purchased after 27 March 2021. Your reasoning would be correct if property purchased after March 27 also only had the interest deductibility phased out gradually up to FY 2026 (ie. if new purchases also phased out their interest deductibility slowly instead of the hard stop on the 27th of March there would be no special asset class).

So what you are saying is actually they did not create a special class of investment, they are gradually putting a stop to a special class of investment over a 4 year period?

Regardless of semantics a class of property that no new entrants can get, which is beneficial to hold until FY2026 now exists. The incentive to leave this special class is reduced.

Accommodation subsidy is going to go up. Many think renting is normal, just like getting handouts and not working is normal. Many don’t even care about owning their own home.

$800k for a "lower quartile" shitbox.

Absolute madness.

Are banks even lending to FHB with a 10% deposit these days in such a frothy market?

I suspect that depends what they expect the market to do over the next couple of years.

I'll bet they are relibrating those models and projections as we speak.

But the reality is if investors become net sellers due to the changes announced, prices are going to have to meet what FHB can afford, rather than FHB attempting to bid more than they can afford to compete with investors leveraging equity, lending and tax advantages to outbid them.

FHB might even start holding out, low-balling, and days to sell increases

Investors are incentivised to hold as long as possible (up to FY 2026) due to bright line and special tax treatment of property bought before 27 March they they will never be able to get again. Also there is a chance a future government will reverse these changes, which when added to the existing incentives to hold will likely really really thin the volumes of property coming to market.

sadr...any future Govt who reversed this would go down in history the same way as members of the Supreme Court would have gone down if they had overturned the election result. Surely no PM would ever want that to be associated with their name, let alone live with it on their conscience. We have turned a corner and are finally starting to move in the right direction.

We are the only country in the world with this complete non deductibility of interest policy.

My prediction is that investors stop building rentals ( because if their circumstances change and they need to sell they immediately have to take a loss - assuming that there is an exception for new builds to allow those to retain interest deductibility for so long as the buyer of the new build does not sell, the loss will arise because the future buyer can’t get the same interest deductibility and as such has to use a lower yield to calculate value). Also increased costs and reduced demand makes building rentals less attractive. In order to get building activity up again after it drops off in about 2-3 years (once everything already in the pipeline comes through), the government will reverse this rule and be hailed as heroes for doing so.

Speaking of things specuvestors are never going to get again - the current sales prices!! Woweee what a windfall! Interest rates are going up at some point (watch the U.S) Interest-only may end. And do you really think Labour is going to be shy about doing a rent cap or rent freeze ? I think they've made it pretty clear they aren't specuvestors friends now. Not hard to see they will act in time, even if it does try everyone's patience a bit. However alot of specuvestors will hang on and drag this out, and find themselves feeling the sharp pang of regret. Unlike some long term investors we have noticed who have jumped ship - so much for the theory that all long term investors are not interested in cashing in on capital gains. People can change their approach, cash in whey they feel it's worthwhile - the same as in the share market. Going long in a market does not mean someone never ever sells. They can opt to dip out while new entrants are still buying near the top, late to the party as they say

I can't see your average specuvestor who has purchased many properties over the last few years, hanging on any longer than a day-trader on Sharesies

By phasing the interest deductibility out over many years till FY2026 and giving clear forward guidance as to the profitability of rentals I reckon you’ll find that build to rent construction activity drops of before the tax advantage now accorded to property purchased before 27 March runs out. Net effect should be a reduction is supply coming on stream (in about 2 years, once everything already contracted is delivered) which should eventually push prices up? Prices being sticky on the way down (until a crash) should mean trading volumes just drop for the next couple of years between now and the supply squeeze.

Reducing supply rarely ever leads to lower prices. In Malaysia to increase supply and lower prices they made being a landlord more desirable by halving tax from rental income, the net effect was a massive oversupply of housing after a decade. This in turn dropped rents and house prices. The beauty of their solution is that the rich paid for it all and were happy to do so.

Banks will start being a whole lot friendlier to FHB.. Who else is going to borrow to buy houses?

The odds that this new hope gives you - hang on to it.

While Kiwibuild was a failure overall, it had some good outcomes. I got my first home through it, a 3 bed townhouse for 650 that's probably worth over 800k now.

On similar lines, the Homesart amendments are great. FHBs will be able to buy a 3 bed 700k apartment or townhouse. With a 30 year 660k mortgage at 2.3%, that's about $600 pw, achievable for a middle income household.

The only thing missing now is a bigger commitment to shared equity home ownership, which will open up more opportunity for lower-middle income households. Hopefully that is a key part of the Budget.

Fritz, can you explain how shared equity would work. Does it mean a lifetime of debt repayments to only own some of your house? Because that would be a good way of increasing house prices even more.

The usual way these are set up (e.g. Housing Foundation NZ) is you put in a deposit, the funding vehicle pays the balance, and you buy their equity off them over the life of the scheme.

Why would it increase prices more?

Also as someone else explains below, you have chance to buy out full equity over time.

Furthermore, the mortgage payments on say 60% equity of a 3 bedroom 800k home are way lower than equivalent rent. Plus you are getting a new house built to current code, and all the security and stability you don't get with renting.

People need to get over the 'freehold detached housing dream'. It will never again be an option other than for high income earners. Move on.

How will it increase prices?...well using your own example above someone who could only afford to bid for a 480k house can now roll up and bid up to 800k.

You don't explain what return is in it for the other entity holding the other 40% equity. If that part is subsidized so it is effectively "interest free" then anyone can see prices will be bid higher.

And then what - communal living, with shared toilets.

Look at the trend, none of this solves the long-term problem, it only helps reinforce it.

Oh come on Dale, that's trite and unfair.

Yes, it is unfair, but that is where the trend is pushing many. No one in the middle class should need Govt. support, via Govt. home starter grants, etc.

The fact that it has pushed up into this cohort should not be encouraged or accepted as the new norm.

Accept it as triage, but don't encourage it plus its worsening variants like shared equity as the long-term solution.

If I had asked you 10/15 years ago would you have thought you would need Govt, assistance to buy a house, I'm sure you would have said no, as I would have. And chances are you would have also envisaged yourself in a different type of house.

Look at the trend.

But the thing is nothing will turn this around fundamentally.

Things have fundamentally changed, for the worse of course. It's a real shame. But shit happens.

In my opinion we need to move on and accept this, and find ways of mitigating this disaster. In my opinion, shared equity has to be one of those ways.

There is plenty left to turn this around, and only some of it in the Govts. control.

It all depends on which way the prices go, both in the short term and the long term. Shared equity increases are equally shared on the way up, but only the purchaser on any loss first on the way down.

We used to live in a democracy, the way this government rush through ideas shows no regard for the very people who supply funds to this sinking ship.

Landlords don't supply funds, they extract them from working people.

I think the problem is this government doesn’t do enough rushing

My business is paying around 300k in tax on the profits this year. It has absolutely nothing to do with property and doesnt own any houses. I think you'll find the tax take from SME's is relatively huge. From what I read on property investor forums, and facebook groups, the main thrust of property investment is to avoid tax at all costs, particularly when it comes to unearned profits like CG's.

At the time of John Key, house became unaffordable which was a crime but the bigger crime was / is under Jacinda Arden, when she snatched away even the dream from a FHB to own a home and NOW as per below if Jacinda has again given hope to dream and does not deliver by taking other corrective measures like DTI and Interest Only Loan ( which has already promised) , will be commiting the greats sin of all time.

When parity of interest only is removed from speculators ( Though will be auctioned by rbnz) Jacinda Arden will redeem herself.

The prospect of home ownership has been increasingly hopeless for people on average wages but the Government's new housing policies should give them hope

Does the tax deductions really matter that much for investors? Record low interest rates are here to stay for at least the next few years...

So what if an investor can't deduct the 2.29% of interest off their mortgage? The capital gains on it will far exceed that deduction in a matter of months. Also, most smart landlords would just mark their rent up from $600 a week to $650-700 a week to minimize the impact.

I currently do not own an investment property (because property prices are too expensive), however if houses do drop in price, I will for sure buy an investment property. Where else am I going to put my savings? I can't travel outside of NZ...... I don't want to spend my money on useless items...... my savings account interest is less than 1%......

The only options I have are to "gamble" with the stock market, or buy a property to get yield. I think I would take the latter.

You make a good point about where will people go to invest their savings. But if residential property prices start falling it wont be there.

I would be interested on others opinions of where these maturing term deposits are going to be invested.

One I recently heard was carbon credits, but I don't know enough about them to comment.

Buying carbon credits would be simple speculation on the price of carbon rising - probably not a mainstream investment. As an aside, you can buy carbon credits and surrender them, and in doing so have a genuine impact on reducing NZs carbon emissions.

Share market is an obvious target, either locally or overseas through ETFs, managed funds, kiwisaver etc.

With a little luck, current property investors who consider themselves businesspeople will actually start some real businesses and maybe benefit the economy.

I've been saying the same thing for awhile now. I have a TD maturing shortly and there ARE NO options apart from an investment property. I cashed out of stocks awhile ago (so I could sleep at night) and bonds as well as TD returns are hopeless. It appears that the young and the elderly have been screwed .

No options? You can buy shares in almost any market or indexed fund around the world, some don't even require a broker, just an app, and there's an international crypto currency market finding on the rise. It has literally never been easier to invest in anything. It's just not as risk-free as the NZ government as artificially made property, until recently.

I bought a boat. Plan is to sail away from this madness.

Depending on the size of your TDs this may not get you far, but how about investing in your home? I'm switching my downlights to LEDs, improving my insulation, and adding timers to my hot water cylinder, spa etc to take advantage of cheaper power times. Then there's the option of adding solar panels of some kind.

Some of these have rates of return well into the double figures, and as they are savings rather than income you don't pay tax on them. Not to mention the wider benefits of lower/off peak power usage.

Have you done DD with Bitcoin? The hardest money in existence, and the best performing asset for the past 10 years, averaging 200% returns per annum. Houses are costing more in fiat every month, but getting cheaper in BTC.

Bitcoin too risky for most older savers. Just look at the chart of historical prices. It will likely keep going even more exponential until it will suddenly crash.

Stock markets also look overvalued to anyone who has seen a few crashes, they are only where they are because of artificially cheap money.

Buying a property is a gamble too - much more risky as you can lose more than 100% of what you put in. Say you buy a property with a 20% deposit and then watch the market fall by 25% - your savings are not only wiped out, but you're in debt for more than the house is worth.

With my share portfolio, the most I can possibly lose if 100% of my money. As it's spread over many investments, I'm very unlikely to lose anything close to that. I'd suggest it's at least as likely the property market could fall 10% (wiping out half a 20% deposit) as my portfolio falling 50%.

And this is not even mentioning interest rate risks, or the risk of your rental property leaking or needing structural work...

Jacinda has promised that under her, house price will never fall....not sure if she understand, What she is talking or its implication as coming from prime mi ister.

Agreed, those people who call investing in stock market "gambling" probably don't know much about investment. One of the golden rules of investment is not to put all your eggs in one basket. Investing into property not only requires you to put all your money into property, you will likely also take on a huge amount of debt. It looks less risky at the moment, that's because the price is going up. If it goes down, you might not be able to recover from your bankruptcy for the rest of your life.

Except with residential property, you have a captive audience once you have priced them out of the market. Having somewhere to live is nothing like saying "On let's not eat out this week, money's a bit short" and for that reason the playing field here, MUST be flattened and the whole business of "people farming" needs kicking in the guts.

I look forward to further measures against this culture that has risen in our country

Only takes one person to start a revolution.

If investors think they can force rents up to cover costs they can’t afford in the first place, don’t be surprised if it backfires.

I was thinking about this yesterday. Living in Wellington, where rents are the highest in NZ: if one is on minimum wage or close to it, then there must come a point where you just up sticks and move somewhere else where rent is more bearable. I'm not sure how many people are willing to sleep 3 to a room - and dare I say it, with immigration at an extreme low (and will stay that way for some time) there aren't going to be people coming in that will......assuming landlords are fine with that (most are not).

Infact there was a net loss of 127k in the last 12 months across our borders. That must account for some rental demand surely. It's now running at about +/- 0 net loss/gain. Also 3k FHBers and about 5K investors are taking out mortgages each month, so we're now relying on the homeless and the school leavers to fill the rentals.

Alot of the perceived shortage is some specuvestors just letting property sit unoccupied or under-rented because it's so cheap to do that with current interest rates and interest only deals going, and rising prices justify the lack of revenue vs interest paid

Say you increase your rent from $500 to $600. Tenant A can no longer afford it so he moves out. Tenant B who just left a house where the rent went from $600 to $700 discovers that he is now in your price bracket and so occupies the house that tenant A used to occupy. Tennant C occupies the house Tennant B used to occupy (paying the $700 rent), etc. when the whole market moves due to government pricing signals what the market can bear changes. Neither tenant B nor tenant C are willing to be homeless so they take the lower quality accomodation which is all that they can now afford. Let’s say 70% of tenants in each price band end up having to move to lower quality accomodation, the only landlords who need to worry are those renting out houses in the very top band, but their clients are the tenants who are the most likely to be able to absorb the increase.

Your market tolerance logic only works if a significant portion of tenants would prefer to be homeless over moving to lower quality accomodation (ie. they need to have the ability to go without)

Tenant A buys their first home. There are now 3 rentals but only 2 Tenants.

If they could buy why haven't they already? The increased rent will reduce their ability to save a deposit (unless they move to lower quality housing).

Also if we have a shortage of 100,000 houses as claimed by Andrew Little in the lead up to the previous election that would imply that 100,000 tenants need to buy houses before landlords start to be short of tenants. Add to that the fact that tenanted houses have a higher density/occupancy rate and the fact that 100,000 houses don’t transact to FHB in a typical year...

There comes a point when every FHBer transitions to that stage of being ready to buy. It doesn't need to be Tenant A strictly speaking, but Tenant D or Tenant E?

If we have a shortage of 100,000 houses, and according to Customs 127k additional people have departed vs arrived into the country in the last 12 months, 5000 per month FHBers, 5000 per month Investor purchases (RBNZ C32). What does that 100k shortage look like today?

Based on 2.7 people per house that still leaves us 63,000 houses short?

Sure, Tenant A can buy..... probably in the middle of god-knows where. The problem is, Tenant A wants to be in a "good school zone" for their kids, and they can't afford to buy Remuera properties, or Buckland Beach properties for the school zone.

Therefore Tenant A buys some random home in the middle of nowhere (because that's all they can afford) to rent it out. But then they will probably go back to renting good school zone areas to give their kids a decent education at a higher weekly rent rate (which btw should be universally consistent across all schools, but clearly the quality is not - separate topic which govt hasn't really fixed either).

What are you even talking about? Some very weird assumptions you've stitched together. Sounds like wishful thinking from someone who is hurting from the recent news. 3k per month First Home Buyers (RBNZ C31) aren't all buying in Remuera or Buckland Beach. Open your eyes at all the construction going on around you.

Not wishful thinking. I think you need to open your eyes up to the reality of the situation. Sure, construction is happening, especially further and further from the core city. Either that or you live in a high-rise/townhouse block which the "NZ way" is to own a house, a piece of land, and maybe a little backyard. If you really think FHB are happy to just buy "any home", then good on ya and keep wearing those rosy sunglasses.

I know how this all ends. I've lived in countries and cities that have gone through this process years ago. NZ is just finally catching up to the rest of the world. Wait until the borders open up.

Not hurting myself. Not a property investor, but after this news, I do hope prices fall, because I have been looking at ways of buying a 2nd investment property but the prices were too expensive. Super excited about what's to come!

“Not a property investor but looking at ways to buy my 2nd investment property” *facepalm

I choose the former (the stock market) every time. The yields have been generally superior to property, even more so now. The capital gains not as much thanks to the cultural obsession that NZers have with real estate, but the latest action has effectively changed that. No CGT or outright capital tax? Fine by me.

My Milford KiwiSaver returned 33% last year.

What's the settings? Mostly growth or balanced?

Wise decision, nothing beats brick and mortar when it comes to secure investments besides bonds.

You mean the bonds that aren’t even keeping up with CPI? Don’t get me started on real world inflation.

Houses need to return to being regarded for what they were intended to be, HOMES for people, not a never losing casino for greedy land leeches bleeding other dry.

There's still the issue of cash flow. Capital gains only materialise upon sale. Tax has to be paid every year and if you don't have the cash flow, you need to sell.

Investment in property is all about cash flow. When your cash flow is not looking good, that investment wont look attractive anymore. So debt level, expense, interest rate they all matter.

An example will show how much of an impact this change can have.

Ms X owns her home. She uses the equity in her home to buy a rental property for $1m. The property rents for $800/wk ($41,600 pa). Expenses are mortgage interest of $23k ($1m at 2.3%) and others expenses (e.g. rates, insurance and maintenance) $10k.

Ms X's taxable income is $41,600 - $33,000 = $8,600 = tax bill of $2,838 (assuming Ms X earns of $70k from salary income so 33% rate applies to rental profit).

If the interest was not able to be claimed as a deduction Ms X's tax bill from the rental would be $41,600 - $10.000 = $31,600 = tax bill of $10,428.

Increase in tax bill is $7,590 pa. That's gonna hurt cash flow, decision to buy another rental, house prices and therefore future potential capital gains.

Yes, going from a very modest income to a negative return. If you had several properties it would be quite painful. It's a pity we no longer have The Man2 to chime in and comment on this.

Ain't going to change anything. Investors will just stop eating smashed avo and buying iphones...

By way of an introduction I am a reluctant landlord / manager of two houses close to where I live in addition to working full time. I've been saddened to read many posts and comments blaming "souless" investors that are being held up as the root cause of the current problems. I have been frustrated by serial Governments in NZ that have produced a financial landscape (by accident or design) that has funnelled a river of dollars of those lucky enough to have some savings away from almost all vehicles of investment into property. If there were alternatives as, or nearly as effective I would have avoided the responsibility and work involved with tenancy management opting for a more passive investment model. This landscape has been compounded by a falling OCR driving investment money away from term deposits leaving us with a mess. The new measures will help FHB's which I applaud but it is also leaving a powerful financial tool unused - where to invest savings that can appreciate while helping out society not hurting it. I wonder how many suggestions may follow on this topic, but I'd have liked to see potential investors help out producing new housing stocks not just driven away from the market entirely. The new measures could have done this but don't in any meaningful way. The interest offset being removed will simply deter those who were considering property as an investment entirely. That in itself is not a bad thing, but I can't help feel an opportunity has been lost too.

I now am going to withdraw from being a landlord over the next couple of years, and I'm not sad. I'm not sure where I will invest savings from here on in, shares most likely. I now need to break the news to my lovely tenants that they will need to find a new home. They need more rentals not less to give them choice and rent competition. I can't see either of those two things precipitating out from the new legislation sadly - that's another problem.

Most of these new policies have exemptions for new builds.

How long does a new build stay a new build? If indefinitely then using interest only loans allows you to have this as a perpetual interest expensing machine fo ether rest of your portfolio. If the exemption is only for 5 years, what kind of build to rent scheme has an ROI of 5 years? No one would build any more. Even if the new build exemption is forever, the ability to on sell your new build is significantly decreased (an asset worth a million to you based on yield, may only be worth $700k to the next investor who picks it up). This dramatically reduces the incentive to build investment property. It will be interesting to see how the government plans to get around these issues.

But this is typical Labor of course - announce first , think later , maybe . . we have seen it all before.

Pity the people with contracts to buy new builds on their hands now - they literally do not know what the implications for them are.

Looking at this a as whole I am pretty sure that interest deduction changes will be watered down very significantly before they become law .. possibly scrapped altogether although it is less likely.

The announcement is just designed to scare the living lights out of any protentional purchaser right now .. they have not thought of the future at all.

Build and sell new.

Anyone who buys that new house will have their ability to on sell it severely curtailed. Also if you build and the market isn’t conducive to a sale you could previously hold until it was, now you have a year to sell or the value of your product drops massively. Might not disincentivize all building, but maybe 20-30% (after the builds already contracted to happen prior to 27 March are completed)?

So you build and hold on to it forever. Seems like a good outcome

Works if you can do it. What if your circumstances change and you find yourself needing to exit due to unforeseen circumstances out of your control? You essentially attach a loss to any possible exit strategy, this makes building new less attractive.

Older investors may not anticipate being alive for the 30-50 years it takes to recover your capital on a new build. Their children losing the ability to expense the interest reduces the value of the legacy that they are leaving behind.

"where to invest savings that can appreciate while helping out society not hurting it..."

Which cuts to the guts of it. Welcome to Nowhere.

Savings/Money/Wealth are a call on future output. All Debt is. And future output cant possibly deliver under the call. We have plundered & leveraged the resource base to oblivion... And now Net energy is kicking back.

Its becoming apparent our income streams are rapidly drying up

This is a really good comment I read which explains why we are approaching the end of the cul de sac...

"Imagine you are an oil company. You have the wells drilled, the technologies for extraction, purification and refining all mature and in place, and you have access to the pipelines, railway cars, or trucks that will deliver the oil products to the many, many sites where they can be burned to perform useful work.

If your company consumes one gallon of oil as part of its ongoing business, how many gallons can it extract and process? That is EROEI, and it is pleasingly high.

In money terms, that is a “going concern” calculation: your company earns, month by month, more in revenue than it spends to generate that revenue, and that calculation works for oil as well as for money. But all is not well.

The honest calculation is “life cycle cost”, which includes all the capital, and of course all the oil, that was needed to create that huge infrastructure. Plus the reserves of both money and oil that will be needed to decommission it and restore the empty wells and closed factories to their pristine state. And that is never fully costed.

The key fallacy behind Keynesian economics, and hence behind Modern Monetary Theory, is the decoupling of “going concern” from “life cycle” costing, and this is what is destroying our monetary economy. There are many companies that seem to turn a profit month by month, but behind the scenes they are zombie companies, because they are carrying a burden of debt that cannot be repaid.

This will end in the way it has always ended: with default. Which is easy enough if the zombies are few and small; but when, as now, the economy is full of zombies, it can be ruinous. As one domino falls, it will take down the slightly larger domino, and then the next larger, until it takes down governments, countries, and the currencies that underpin world trade. Which is where we are now.

BUT this will not work for energy, because we cannot borrow energy from the future with a fraudulent promise to repay. Energy consumed today must be extracted today, so the only useful calculation is indeed life cycle cost. And when you do that calculation for wind, you find that the cost of mining the raw materials, fabricating the windmills, building the infrastructure to erect them, to access them for maintenance, and to connect them to the grid … this takes more energy than the windmill will generate. It is an energy sink, and one parasitic on an existing fossil fuel infrastructure. Again, it is a delusion.

That is the basis of our predicament, because an energy deficit cannot be solved by default; it can be solved only by collapse"

Note that the houses won't disappear, they can be bought by the tenants, or another PI or a FHB. We wouldn't need more rentals if house prices were sensible.

Agree, consecutive governments have completely ignored all other investment types for years, actively discouraged investment in the productive economy through an outdated and outmoded tax system.

The incentive to build new houses to rent out will reduce so fewer additional houses will become available whilst something like 0.75% of the national housing stock gets torn down every year (assuming most houses survive 150+ years)

The incentive to build new houses to rent out has gone up

Please explain. I have personally put 2 new builds on hold (one is just about ready for the consenting stage and the other is at the technical drawings commissioned stage). My reasoning is that the exemption for new builds may not cover my costs (say I plan to recover my costs over 30-50 years and have to pay interest on the money I borrowed to build over the last 20 years of that time (new build exemption lasts 10-30 years), if that interest can not be expensed my yield proposition takes a dive).

If after 10 years my circumstance change (say I get massive medical bills), I may not be able to sell the properties for as much as it cost to build them because any investor I sell to will have a lower yield (due to them being unable to expense the interest), limiting my pool of available buyers and raising the odds of me losing money on the build.

If I pass away after 15 years and the new build has yet to pay for itself will my children still be able to expense the interest? If not it lowers the value of the legacy I leave behind.

What are the incentives to build new that make it more attractive to build relative to prior to the announcement on the 27th of March?

Are you expecting zero risk or something?

Some risk is acceptable but how risky is an asset class that the government is hell bent on slamming into the ground?

My personal plan is to just wait and see what happens. I suspect that is the same for most people who were planning new builds (who aren’t already past the point of no return).

None of this explains how new builds are incentivised relative to prior to the new rules. Near as I can tell they have been disincentivized (they will hold less value in the secondary market)

Sorry, but it needs slamming into the ground

Central Bankers are the root cause of the problem.

> where to invest savings that can appreciate while helping out society not hurting it

Invest in NZ businesses.

There are plenty of startups that need the capital, albiet they are risky. If you want less risk try the NZX top 50 index.

I am thinking we may have a wave of people heading offshore in a year or two anyway. Some of those that came back because of covid will return to their better prospects in the likes of London and New York. The young will chance their arm in Oz. The economy is taking a helluva beating with no tourism and crops not being picked, as soon as borders open people will be off. Whether things are better or worse elsewhere wont matter. They will give it a go. Watch house prices take a kick in the guts then.

More houses, fewer people. Remember Ireland, Spain? Can happen.

I find it really hard to make a call on the final washing up on immigration when the borders fall. I have read that some believe that there is considerable demand building from folk across all developed countries to relocate to a safer haven because of the worries around a Covid .....22? NZ has a good offshore reputation that may be converted into a pulse of migration. As I said hard to know - it's all speculation. I agree with the points you make and recognise the push factors from here - particularly the cost of living especially housing.

I can imagine a lot of people moving here from eg. the US and being extremely disenchanted when they arrive... poor pay, and uninsulated million-dollar houses in suburbs where violent crackheads roam the streets...

I think that will be the case as well, especially among those who hold what is imho, residencies of convenience. They have used that for their own gain, and they will do it again. Much of this is down to our propensity over the last few decades to hand out residencies like a lolly scramble, now they are being used to their best advantage. Immigration needs to be far more selective, something ACT will never do.

End of the day Housing needs a price reset in NZ because its massive debt loading (lower rate but even stupider amounts) is crushing the fabric of NZ. Rents, mortgages and wages needed to support those are all being driven by the debt levels that exploit kiwis need for shelter in favor of endless bank profits. Aka financial exploitation of a basic human need.

Investors don't see this, and many based on the comment here in the last ten years, many appear to not care either. That said some do, and unfortunately the behavior of the speculators is now impacting the true investors. This behaviour has a) brought this Govt in, and b) lead to the changes yesterday.

I would prefer to see less promotion, govt sponsorship, of endless debt as a retirement strategy.

The government policy only Serves to send a market wide signal to increase rents and stop new builds.

Say you increase your rent from $500 to $600. Tenant A can no longer afford it so he moves out. Tenant B who just left a house where the rent went from $600 to $700 discovers that he is now in your price bracket and so occupies the house that tenant A used to occupy. Tennant C occupies the house Tennant B used to occupy (paying the $700 rent), etc. when the whole market moves due to government pricing signals what the market can bear changes. Neither tenant B nor tenant C are willing to be homeless so they take the lower quality accomodation which is all that they can now afford. Let’s say 70% of tenants in each price band end up having to move to lower quality accomodation, the only landlords who need to worry are those renting out houses in the very top band, but their clients are the tenants who are the most likely to be able to absorb the increase.

Market tolerance logic only works if a significant portion of tenants would prefer to be homeless over moving to lower quality accomodation (ie. they need to have the ability to go without).

The new build exemptions still mean that if you buy a new build your ability to o sell it will be significantly diminished ( your yield will be higher than the buyer’s because your interest is deductible but theirs is not ) this means that the liquidity of the asset is basically non existent (net result being significantly reduced incentive to build new). We have put on hold our plans for 2 new builds in this coming year pending more information as to how the new build exemption will work. I can not think of a sensible exception that would allow new builds to still be viable investments.

But by increasing your rent your increasing your taxable income?

Yep, you would need to gross up the increased rent to account for the increased tax.

Example: No longer able to claim $10,000 interest costs, tax bill increased by $3,300. Increased rent would be subject to 33% tax so the increased rent to cover all new taxes would be $3,300/67% = $4,925.

$4,925 tax is $1,625 = $3,300 (to pay new tax due to loss of interest deductions).

The big issue is how much (if any) of the $100/wk required to pay the new tax can be squeezed out of the tenant.

Not to lose an opportunity, now business brokers are active. Just got this email from a business broker :

The Government has announced its new housing policy which has removed the tax deductibility for interest costs associated with residential property investment. This new policy will further reduce the commercial benefits of residential property investment along with the extension of the bright-line test from 5 years to 10 years.

Business ownership continues to be exempt from any capital gains tax and all interest costs continue to be 100% tax-deductible. This is a clear message from the Government they are wanting to encourage more of New Zealand’s investment dollars into the business sector and away from the residential property market. The Government has a strong view that business investment is better for the economy and creates more jobs than residential property investments.

----------------------------------------

One line of thought for property investors caught on the wrong side of this new legislation is to consider business ownership as a tax-efficient asset for any bank debt required for property ownership. New ownership structures for property investments will be encouraged to diversify into business assets so they can still claim all their interest costs for the annual tax return. Experts and accountants have already commented that all new investment structures should move debt out of investment properties and leverage up business assets that continue to offer tax deductibility for interest costs.

We expect this new tax policy to increase interest in business ownership and this will have a positive flow-on effect for the future New Zealand economy.

I have spoken to a couple of brokers to get a valuation, the multiples they are talking now are wild, I always worked on 2 - 3 times net, these guys are talking 4 - 5 or more, particularly if someone can come in and park their money and dont need to actually work in it.

Old News but may be the reason that RBNZ is giving hard time for DTO and Interest Only Loan as easier for them with perception that everything is fine which is created by housing bubble and also divert attention from many other problems in the economy and also in housing ponzi, the blame stops with government

https://www.abc.net.au/news/2021-03-15/why-the-rba-and-the-government-d…

Hope, yes. Solution, no.

https://www.newshub.co.nz/home/politics/2021/03/government-housing-poli…

Dr Edwards said that shows how "frightened" the Government is of the pressure it's under over the housing affordability crisis.

It seems that speculators and their supporters in guise of experts, economist, politicians are more frightened and making more noise to try and stop government from taking further action that is in pipeline - Interest Only Loan and DTI.

Lobbying to pressurised government is full on.

The appetite for property investing or speculating, it's just not going to be the same anymore. There are always people who want to buy a house to live in - some are restricted by LVR and Kainga Ora limits. What gives??

I reckon the housing shortage will get worse because the government has just removed the incentive to build new investment housing. Even the new build exception is not enough.

How long does a new build stay a new build? If indefinitely then using interest only loans allows you to have this as a perpetual interest expensing machine fo ether rest of your portfolio. If the exemption is only for 5 years, what kind of build to rent scheme has an ROI of 5 years? No one would build any more. Even if the new build exemption is forever, the ability to on sell your new build is significantly decreased (an asset worth a million to you based on yield, may only be worth $700k to the next investor who picks it up, because whilst you can expense your interest they can not). This dramatically reduces the incentive to build investment property. It will be interesting to see how the government plans to get around these issues.

Property investment gurus will have to amend their sales pitch. No longer it's 'gain a 10% capital gain every year and with the deductions of your interest etc the taxman (ie taxpayers) will fund it for you' - even if you make loss you can offset this against your PAYE income.'

There is a lot I dislike about this Govt but I actually think this is a good move. Housing should never have been a subsidised free ride to capital gain. How about invest in real businesses instead? We may have a real economy if that was the case.

Quite like the idea that my kids may be able to afford a house in 10 years time with some of these changes.

Is there any Govt anywhere that has successfully reduced the price of houses with their policies ?

Obviously Dictators and Lunatics not included.

The US, Japan, and Ireland all spring to mind.

None of this was done consciously. Places like Texas have prevented booms or busts from happening in the first place and have low stable affordable housing where capital growth is no higher than rate of inflation and income is made on yield only.

Both National and ACT have confirmed today they would roll back the bright line test and reverse interest deductibility changes.

This is like a mini cultural revolution. Demonizing and penalizing one group of small business people, landlords, one of the "Five Black Categories". These modern Red Guards will eventually be overthrown.

Zach..it is not about penalizing anybody. It is about ensuring investors do not have an unfair advantage over first home buyers and shut them out of the market. Do you demonize meth dealers? If so then why? Because of the damage they do to NZ society. And calling investors business people is an insult to real business people.

B-b-b-but landlords provide an essential service. Just don't ask them if they pay GST, don't expect them to meet health and safety regulations like businesses/PCBUs must adhere to. Don't expect them to pay back the principle on their loans. But it's cool if they claim deductions like other businesses.

Are they completely barking mad? With the growing voter base not being landlording classes (not to mention the perpetrator of this mess JK still fresh in most voters minds) i'd suggest they get used to a very long time in opposition.

So what are the solutions that National and ACT are proposing then? They aim to do absolutely nothing? I won't be voting for any party that is in favour of continuing the housing Ponzi, so may have to abstain from voting at the next election. That's another vote the right of centre will be losing. I'm not a fan of government and central bank run asset bubbles, which are very dangerous IMO.

Maybe some real solutions - like building a statue of each property investor in a public place to say thank you for their contribution to society. This will encourage investors and thus increase supply, solving the problem once and for all.

ld...after finally turning a corner and starting to head in the right direction no leader would ever reverse it. Imagine if that was your legacy. Reversing something that assisted young FHBs with buying their own homes and protected them from greedy investors. You would never be able to sleep at night knowing the damage to NZ that you had done.

I expect house prices in most regions to continue rising steadily until an economic crisis hits, where by rising unemployment and interest rates force a sell off. This government is nowhere near organised or determined enough to build enough houses to catch up with demand.

I think they've proven they can't implement promises very well... kiwibuild was a flop -

but apparently kiwibuild 2 is supposed to be better..?

In terms of market drivers there is mounting pressure on the housing market including

* interest deductibility being removed, this is going to hurt highly geared investors

* low to no immigration due to COVID

* LVR and bank restrictions

* increased tenancy law compliance costs (insulation/ termination limitations etc)

* bright line testing re capital gains at normail income tax rates... (sheesh...)