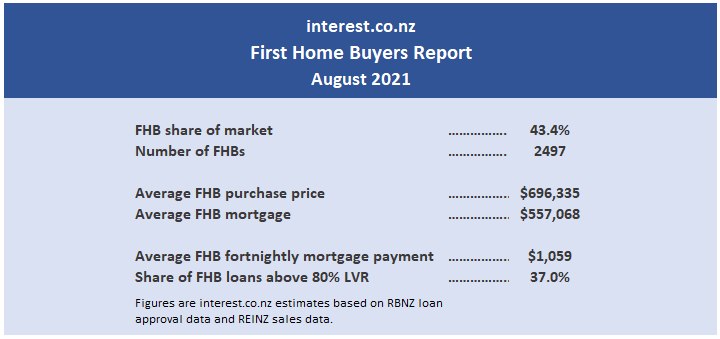

Fewer first home buyers purchased a home in August although their share of the housing market increased.

The latest Reserve Bank figures show that mortgages were issued to 2497 first home buyers in August, down by 14.6% from July.

That decline was not surprising given the severe restrictions imposed on real estate activity in August due to the COVID-19 lockdown in place in the second half of the month.

However the figures suggest that first home buyers more than held their own in the market, with the Real Estate Institute of New Zealand reporting residential sales in August were down 26.5% compared to July. That means first home buyers accounted for an estimated 43.4% of residential sales in August, up from 37.4% in July.

That puts first home buyers' share of the market at its highest level since June last year.

However while the number of first home buyers who got into their own homes declined in August, the average amounts they paid for a home and borrowed from a bank, continued to increase.

The average mortgage issued to first home buyers throughout the country in August was $557,068, which suggests an average purchase price of almost $700,000. That takes their average mortgage payment to $1059 a fortnight (at 2.82% with a 30 year term).

Unfortunately, the number of first home buyers purchasing properties with low equity loans (less than a 20% deposit) is also continuing to rise.

In August, 37% of the loans approved for first home buyers had loan-to-value ratios (LVR) greater than 80%.

That figure has been steadily increasing since March when it was at 31.9% and is heading back towards the high of 40.3% achieved in May last year.

However first home buyers' access to low equity loans is likely to be crimped by new LVR restrictions being imposed by the Reserve Bank, which may also have a chilling effect on the amount they are able to pay for a property.

The comment stream on this story is now closed.

65 Comments

A lot of FHBs in Auckland are buying new builds, the LVR restrictions don't apply to new builds right?

Oh well hope they understand the meaning of caveat emptor .

It would be interesting seeing a breakdown per city. For example average mortgage size for FHB in Auckland & % of deposit. Sure it would paint a much more dire picture...

The idea that housing is unaffordable and FHBs being locked out of the housing market is becoming increasingly debatable. FHB should set realistic expectations for themselves to avoid disconnects with realities.

Average FHB property purchase price = $696,335 (refer above)

Average household income, p.a. = $107,196

Median multiple = 6.5 ← seems unaffordable by median multiple ratios

However,

Average FHB mortgage payments, fortnightly = $1,059 (refer above)

Average household income (6/2020), p.a. = $107,196

Implied interest rate = 2.82% ← ie. the current average interest rates on FHB loans

Percentage of mortgage payments to household income = 25.7% ← $27,534 ÷ 107,196

That is absolutely affordable.

This chart shows you why it is pertinent of FHB & FHD to understand cheering for a interest rate hike is the equivalent of singing at their own requiem and have a dire consequence on the economy.

Another beautiful Saturday to brainstorm with grandkids on some math.

Have a great weekend!

Looking at the income data via your link - the 2021 correction shows that average household gross income is about $88K, not $107K (but happy to be corrected if I'm looking at the wrong data set).

Yes, I'm using the uncorrected data for the math game with the kids.

However, the point remains the same- cheer leading a hike in interest rates is destructive to everyone, including all FHBs.

That simply isn't true.

You confuse what is going to be bad for you with what might be bad for FHBs - then use that as a threat to push for the status quo in order to further benefit yourself.

Assuming discounted cash flow models are true, then higher r values will see lower asset prices.

Central banks can pretend that we don't have inflation for a while, but eventually people will wake up to the fact that they can no longer feed the children on the amount of money they are getting paid - see what is happening around the country with the support required by food banks. Its happening, but we pretend that it is not, because any action by central banks will cause the asset bubbles to implode.

Not all asset prices fall on rising rates, many rises with rising rates as well.

Knowing a little can be a dangerous thing.

Name three.

Not your financial advisor nor helping you to make a quick buck.

Regretting not buying Fletcher because of a 200 day high the last time?

What was that comment you just made about "knowing a little"?

Surely one as expert as yourself could whip up 3 examples in a second.

Also - very soon - there are going to be a lot of mortgage free retired boomers and young people locked out of the housing market, who will want interest rates to rise. Boomers because they want return on their savings, and young people because they also want return on their savings for a house, and because of the destructive impact it will have on real house prices (perhaps not nominal, but real).

So suddenly there could be significant political pressure to reverse the policies for the last 40 years, where boomers, the largest demographic, have wanted falling interest rates so they can exploit everything for their own best interests - pretending that its all about 'inflation targeting' (when clearly it is not based upon recent central bank behaviours) - will be cheering on central banks to raise rates and pushing pressure on governments to do so.

The mean age of the baby boomer generation is already over 65.

Many will be sadly deceased and of course you will happily tell us that all of the rest have made a fortune on real estate.

So why would they wait to retire at 65?

If your hypothesis has any merit then it will be observable right now.

Many have made a fortune from real estate 'on paper'. But most are asset rich and cash poor.

The average NZ home, at nearly a million dollars, is worthless if you can't afford to pay your rates or power bill based upon superannuation payments or interest on whatever savings they have.

If inflation is really here, which it appears to be, and the reserve bank want to pretend its not, its going to be eroding away at the quality of the boomers retirement lifestyle. That won't sit well with them at all.

The longer the central banks keep the OCR below the actual level of rises in the costs of living that people are experiencing on a daily basis, we are all becoming poorer.

This will take a few years to play out of course as people start to figure out what is going on - right now people are focused on COVID and can't see the forest for the trees. But the past 40 years its been in boomers interests for rates to fall so they can clear their mortgages - that has changed now. Its now in their interests for rates to rise.

If you cant pay for power there is a winter energy support payment. If you cant pay your rates ask the council for a low income rebate. Lots of handouts are available for the needy so why save, just spend and have a good time.

Think more of the system in total, not of individual groups, and how one intervention will cause another problem somewhere else in the system.

If more government support is required in the future from where we are now, that will require greater deficit spending. Higher deficient spending is generally inflationary which will make the cost of goods and services even more expensive. Power bills, food etc more expensive. That will then require more money from tax payers to pay for old peoples superannuation. So that is a zero sum game. Could be even worse than zero sum. It could be very recessionary. It won't make things any better for people.

What we need are lower asset prices and higher general interest rates to make the system stable and sustainable. At present we're trying our very best to avoid the pain, only to make the pain far worse at a point in the future.

Who cares about all that, certainly this govt does not care too much. They just make bigger promises to suck in gullible voters. I doubt there will be much left after the current old people have stripped the cupboards, mind you they were the ones who built the cupboards (infrastructure) for the next generations of woke idiots that oppose water storage and hydro power schemes etc

Boomers built very little of our infrastructure, it was their parents' and grandparents' generation. How many major projects in the 50s, 60s, 70s (pre-Boomers in charge) compared to the following decades?

Boomers were all about selling infrastructure off for a quick buck in the hope of lower tax rates.

Boomers inherited a prosperous, egalitarian nation with a strong welfare state and world-leading health and education system.

Now our city centres are clogged with the homeless and mentally ill. Boomers broke our country. They thought you could maintain a highly functional state while also treating carefully husbanded collective resources as a personal piggy bank. Well, you can't.

Many people should look at the rates rebate, its well worth your time. I received the full $635 or so this year for filling in a couple of pages and taking it into the local council office where it was processed on the spot now in under 2 minutes.

Yes its more like $88K as the last I heard it was $78K, are you guys remembering to take the tax out of that ? I think you will find that the mortgage repayment will rapidly get closer to 40% in no time and that's if rates stay this low.

I was far too kind on CWBW. Yes there's many flaws in his workings, scary to think he's heavily involved in property.

You are right he hasn't taken tax off that.

So if you apply the correct income, take tax off that, apply penalty interest for low deposits then yeah it will be getting towards 45%. That's not good.

With the correctly weighted numbers the,

Median household gross income is $87,607 and the median household disposable income is $74,533

Therefore the mortgage payments as a percentage of gross income is 31.43% and disposable income is 36.94%.

Not even close to the 45% you claimed.

Math is clearly not your strength. I hope you have a good accountant.

It's even worse than 45%. That was back of the envelope from me.

Assuming 700k purchase price.

10% deposit = 70 k

Mortgage = 630k

A 30 year mortgage paying interest of 3.5% = $650 per week.

Median household income, let's say 90k. Assuming one salary of 50k, and one salary of 40k, and both paying Kiwisaver = $1345 net per week.

650 ÷ 1345 = 48%

You're merely moving a goal post to change an argument in your own favour.

The average FHB purchase price is 696K and the average FHB mortgage is 557K.

The average LVR is 80%.

Suddenly your counter argument uses a LVR of 90%, how dishonest!

You are the one changing the goalposts. You used 90% in your first example.

Acknowledge it, you are out of your depth.

So let's say average is 85% for FHBs. That's still somewhere between 40 and 45%.

The fact is the average is LVR 80%.

85% is a simulated exercise on your part.

I had been consistent with the LVR 80% throughout my examples.

The average FHB mortgage payment of $1,059 per fortnight is the repayment based on average FHB purchase price of $696K and an average FHB mortgage of $557K which has an LVR of 80%.

Therefore,

- Mortgage payment to uncorrected annual household income ($107.1K) is 25.7%;

- Mortgage payment to corrected annual household income ($87.6K) is 31.43%; and

- Mortgage payment to corrected annual household disposable income ($74.5K) is 36.94%

The best you can do is to stop digging at this point- it'll just make it worse for yourself trying to blame your integrity compromises by claiming someone else is incompetent.

Pack it in grandpa.

You are the one who is all over the place.

First of all you said it was 25% of the median income, and now you are claiming 37%. Wow!

That's a massive error. With no admittance of error on your part- it's always about trolling others.

Your credibility is shot. Good night.

The use of uncorrected data was already being highlighted in the reference to Stats NZ on my very first example and I'd been straight with it. Even a revised computation using Stats NZ revised data is nowhere close to your 45% claim.

Your persistence in blaming others for your own misunderstanding is appalling, I was expecting better.

That $696k is purely a GUESS by the author of the article, ASSUMING an 80% LVR. The only thing known from the RBNZ stats is the $557k.

Anyone that knows the FHB segment profile will understand that the average LVR will be higher, given 37% of them are known to be over 80%, and that will be as high as 90%. Most other FHBs will be hanging around 75-80% LVR, so weighted will be somewhere in early 80's.... which then makes the assumed interest rate unlikely, and therefore the assumed repayments higher and affordability lower, esp. after tax. It's dominos.

If you want to take the tax out in calculating housing matrices, you have to take tax out of all of them to have a fair comparison.

That also mean taking tax out of median multiples for a fair comparison, that is not the norm in the industry.

Anyway, it's 36.94% after tax which I personally think it's still reasonable.

Bullshit that is reasonable. 30% is the traditional number.

Fretting over a 6 or 7%? How do you justify 30% besides it's a 'traditional' number?

Christ you are lame. You are also very wrong. See above, it's more like 48%.

Perhaps the old adage about property investors having luck and timing much more than brains is very true.

See above.

We'll talk when you learn some honesty in engaging a debate.

30% has always been a traditional yardstick for affordability. Anyone involved in property should be aware of that.

I am starting to think you are merely a troll.

Always?

Meaning it's a hearsay taken as a infallable word of truth?

It's as conventional as 'property always goes up'

Six percent of the average household income number is more than $100 a week. That may be a mere trifle to you, but for most people, $100 a week - $5200 a year - is certainly worth fretting over.

There is disagreement about what a reasonable affordability measure is - this very site uses 40% in theirs, which I personally don't think is reasonable.

But maybe a comparison will be helpful - the average household, withe the average mortgage payment (using the numbers above), with two kids under 14 (assuming the low income expenditure per child listed on the IRD website), end up with less disposable income than two pensioners who own their own house but have no other savings. (74533 - (1059×26)-(147x2x52) = 31711

Pension for a couple after tax = 34955

We are constantly being told the pension is not enough to live on, and needs to be topped up with other savings. If this is true, an average household in NZ can also not afford a house and have more than one child, let alone save the extra they supposedly need for retirement. And I havent even factored in costs of going to work, like commuting costs. Thats a pretty sorry state of affairs I think.

Of course, this doesn't take into account top ups like WFF, Best Start (or the winter energy payment).

Lets assume the best case scenario for those: both kids are under 3, so the household gets besr start and wff = 134 a week (6968 a year). The pensioners get six months of winter energy payment: $827 a year.

Add those to the above: household = 38769, pensioners = 35762

The household is better off - but assume they put the minimum into Kiwisaver- 3% of 87,607 is 2628.21. = 36,140 remaining. Our household with two kids is now just $378 a year better off than the pensioners. Their work commutes better not cost more than $8 a week, or they will not be able to afford a house, kids, and minimum Kiwisaver contributions, even with maximum government top ups (and they really cant afford for their oldest kid to turn three).

"This chart shows you why it is pertinent of FHB & FHD to understand cheering for a interest rate hike is the equivalent of singing at their own requiem and have a dire consequence on the economy"

Its only signing their own requiem if they have already purchased....but I don't see people who have mortgages screaming for rates to rise.

But for those that haven't who are sitting on savings that are being eroded by inflation that is much higher than the measured CPI and the OCR, then for them, rapid rates rises will be nirvana....but of course, you wouldn't look at that side of the equation as for you, this has nothing to do with FHB's, but instead how much money you can personally gain financially from taking advantage of the plight of others.

"Its only signing their own requiem if they have already purchased..."

This is the part you don't get; a higher interest means it's even harder for FHB hopefuls who have marginal deposits- which may be plenty.

Do you understand asset pricing based upon discount rates? The 'r' is the denominator.

A higher r value would be very beneficial to future home buyers.

Leaving interest rates below the real rate of inflation is the dangerous game that central bankers are playing at present, because its going to erode the quality of our lifestyles, but its happening without anyone talking about or directly seeing it.

When I was still in school completing my paper arguing for and against traditional DCF, CAPM and hybrids, you probably haven't even existed. If you want to throw some financial jargon, at least get them right and know the basics. Watching some YouTube videos makes you an embarrassing expert.

A higher interest rate does not benefit future home buyers; on the contrary, it may just do exactly the opposite.

Is Ray Dalio on YouTube again?

"If you want to throw some financial jargon, at least get them right and know the basics."

If you see an error in my comment above around discounting, please correct me. If I've missed something, it sounds like I have an opportunity to learn from an expert (like you?).

Not that I've learned about discounting from Ray Dalio, but do you assume to be superior to him? Is that what you are saying?

Does flipping houses give you better insight into financial theory than a person with Ray's track record?

(can you see how arrogant this sounds?)

Some good analysis.

And in that analysis I would say it's not *so* dire on a national level.

However, the reality is that a good chunk of FHB demand is in Auckland and Wellington, where the story is quite a lot grimmer.

Also, as per my question yesterday, surely 10% deposit mortgages are attracting much higher than 2.82%? I would have thought it would be more like 3.5%. Which will be more like 4 to 4.5% within the coming year (assuming China does not turn into a global financial crisis)

Also, you shouldn't use average household income. Use median, which I think is 80-90k? That's quite a big difference to 107k.

That's is why it's a national average. If you want a drill down, of course you can even evaluate and compare between Takapuna and Khandallah. However, variations at those levels does not cause an error in the national average.

The next interesting turn will be border reopening which should push houses up further.

In the longer term though price pressure will be downwards in my view. The good thing for FHBs is that houses will get cheaper, the bad thing for FHBs is that the house they buy will decline in value.

Why will borders opening push prices up? People are leaving this Godforsaken place, not arriving.

Bingo 👍

The people who will be leaving know what it's like here for them.

The people who will be coming are hoping it will match their dreams.

Wrong the world population continues to increase at an exponential rate. Since when have we ever had more people leave this country than arrived ? The population of NZ must have doubled since we arrived in 1974. Your dreaming if you think our population will decrease, the government would have to get serious about immigration and limit the numbers trying to pour in here for a better life and we all already know how they couldn't even manage that.

Hi Carlos. Globally we're long out of the exponential phase of population growth now, it seems likely that peak human population will be around 2050 [link] and the next 30 years will be slow growth of course. New Zealand immigration will also likely slow, by far the largest contingent of the foreign born population are from the UK and China which are also countries with aging populations (in fact Chinas population will start decreasing next year according to state media.) Our replacement rate is about 2.1 children/woman in New Zealand but we are currently at about 1.6 children/woman and falling over time so internally we also are on the same population path.

lol, when is it going to be fully reopen? How many free resident visa are we going to send out in order to push houses up further? What makes you think we are going reopen our border before other countries? Why would they come to New Zealand if other developed countries also get covid under control? Keep dreaming mate.

One scenario to bear in mind is we are building a lot of houses today and have been for a few years now and will continue for at least another year. Immigration almost zero and may not return to pre covid levels and rates will eventually go up as inflation is much worse, like in the building industry than the rb is letting on. That's a cocktail called the bubble busta!

Bollocks

Supply won't bring down prices.

In combination with other drivers it certainly will and this is a huge building boom with zero migration & an inflationary setting. Not to mention the pending implosion of China largest developer.

Why do you assume the average loan is at 80% lvr when 37% of FHB loans are over 80? Given HEAPS will be right on 80, wouldn’t be surprised if average was higher. Your 2.82 percent interest rate estimate also forgets higher interest rates apply for this large segment

37% of FHB loans over LVR 80 doesn't cause the average to be higher- that's why it's called 'average'! Somewhere in the sample cummulatively you'll find the 37% under LVR 80 and that applies to the effective interest rates across those groups.

This is the central limit theorem. Even my grand kids got an idea how that works although I would had hoped that they have a deeper understanding beyond what was taught in their school.

Ps. I didn't respond to your banking stuff on a previous post because my wife told me earlier that day to be a little kinder to strangers.

How much do you know about the FHB segment? They are heavily weighted to the high LVR, given no equity. The average will not come out at 80%

In regards to the weighted rate, 2.82% will also be way off the mark. But DC made that error too. Same logic error as the weighted LVR.

Did you explain to your grand kids how tax works? Because you seemed to have used the payments v gross household income % as the affordability measure, which is off. The key point is also that 2.82% is historically low, what happens when interest rates go to even a reasonably low 4.82%?

FYI - I was asking the article author, not you mate. I dont know where his numbers came from and the premise seems flawed.

Lack of skills due to no immigration

+

Higher wages thanks to Labour's ever increasing minimum wage

+

Covid where people had money they couldn't spend elsewhere

+

Low interest rates so money in the bank means it's going backwards

+

NZ's love affair with property

+

Lack of materials

=

The reality today, and this summer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.