It became slightly easier for aspiring first home buyers to be able to afford a home of their own in several parts of the country in September, as prices dipped at the bottom of the market.

According to the Real Estate Institute of New Zealand, the national lower quartile selling price dropped $14,000 from $619,000 in August to $605,000 in September.

The lower quartile price is the price point at which 25% of sales are below and 75% are above, representing the most affordable part of the market.

The biggest lower quartile price decline was in Auckland where it dropped by $30,000, from $880,000 in August to $850,000 in September. This was followed by falls in Taranaki of $23,785, Manawatu/Whanganui of $15,870, a Northland drop of $15,000 and a fall in Wellington of $10,000.

The lower quartile price was unchanged in Otago, while all other regions posted an increase in the lower quartile price in September.

However not all of the benefit of lower prices flowed through to buyers because it was partially offset by an increase in mortgage interest rates. The average of the two year fixed rates offered by the major banks rose from 2.82% in August to 3.02% in September, which was the first time it has been above 3% since April last year.

For buyers with less than a 20% deposit the impact of higher rates was even worse. That's because banks charge higher rates of interest for low equity loans, and the average rates for those loans jumped from 4.02% in August to 4.22% in September.

The rise in interest rates took most of the shine off the drop in prices and the resulting reduction in mortgage payments on a lower quartile-priced home was less than $10 a week.

But outside of Northland, Auckland, Manawatu/Whanganui, Taranaki and Wellington, first home buyers received no relief at all as ongoing rises in lower quartile prices (apart from Otago), combined with higher mortgage rates to push home ownership further out of reach.

The big unknown for first home buyers at the moment is what effect further interest rates rises will have on house prices compared to mortgage payments.

Average mortgage interest rates have risen in every month since June and those rises are about to get steeper.

The country's largest mortgage lender ANZ on Thursday announced a 45 basis points increase to all its fixed-term mortgage rate terms from six-months to five-years. Other banks are likely to follow the hikes, and most economists are expecting rates to keep rising next year.

Higher mortgage rates affect house prices because they increase mortgage payments which in turn, reduces the amount people can borrow to buy a home, unless the increase mortgage payments is matched by an increase in income.

So the latest round of mortgage increases may well put downward pressure on prices.

However, it is the balance between the effect rising rates have on prices and the effect they have on mortgage payments that determines whether first home buyers will be better or worse off.

Either way, the latest rate rises suggest the market could be in for a bit of shake up.

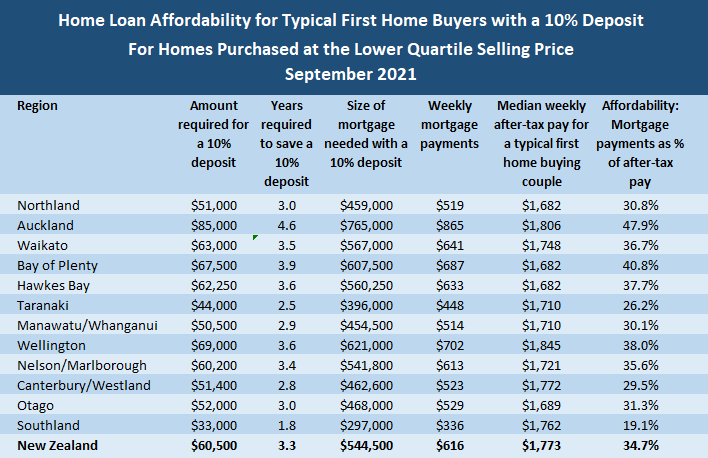

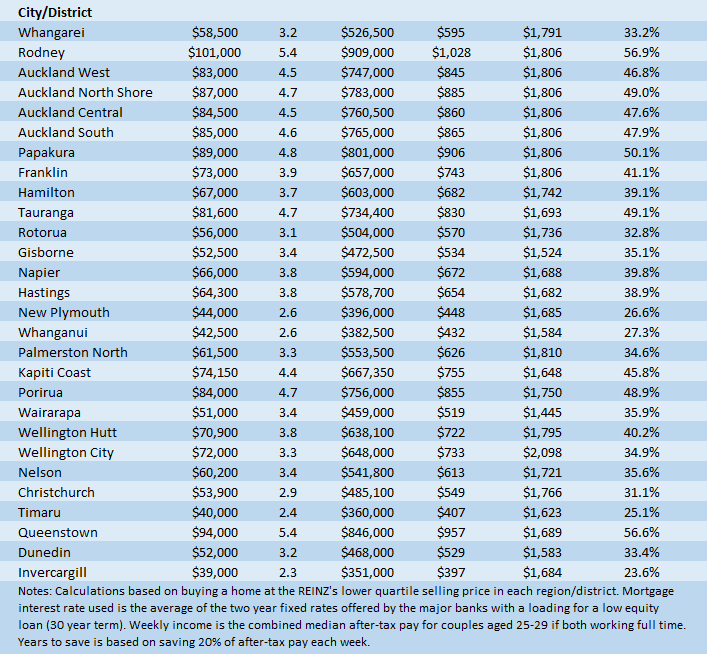

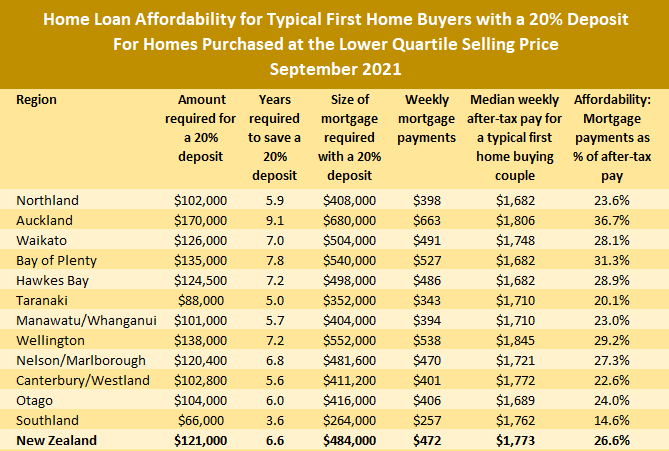

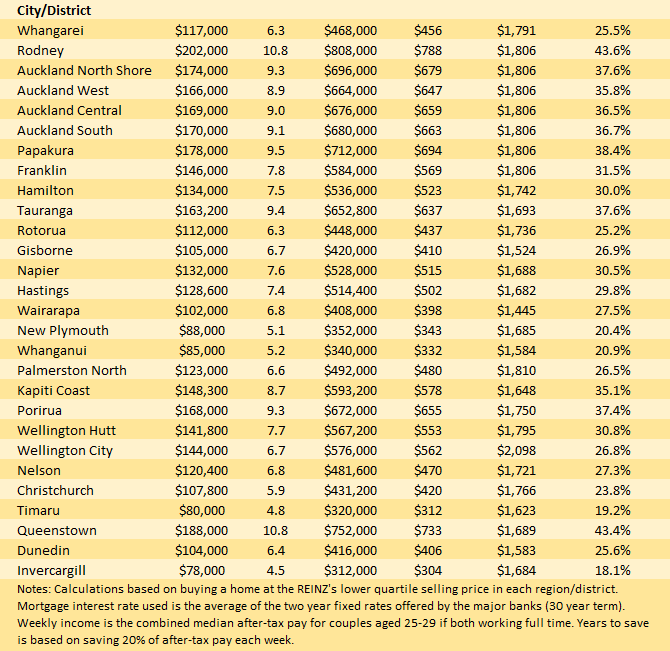

The tables below show the main affordability measures for buying a home at the lower quartile price in all of the country's main urban districts.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

43 Comments

Basically FHB are now left waiting for some apocalyptic event to be able to afford a house.

That would be their home-owning parents dying, I guess.

"Interest rates are like gravity to asset prices"

This is a known-known for a long time right?

It's only a theory.

Good to see that first-home buyers and lower income people are getting a bit more of a chance to get into their own homes.

Long may it last.

I suggest prospective home buyers (at all price levels) hold off from buying through the rest of spring and summer - to see whether house prices can be forced down further........

TTP

Interest rates are definitely a very important factor in the housing market, possibly the most important factor, but definitely not the only factor.

The relationship is not linear and it is also affected by other elements, including taxation regimes, population flows, demographic changes such as population ageing and family composition, unemployment levels, even cultural factors and subjective perceptions.

Correct, and as is often the case in 'real life' we sometimes take for granted just how important to us gravity actually is!

There is no benefit of buying in this crazy market. In NZ we do not fix interest rates for 30 years, only yearly. So when interest rates are very low, prices of assets tend to go higher because everything becomes so affordable not because people have money but banks are ready to lend them more. So more money in the market means people spend more and then comes the inflation. So now interest rates rise, asset prices will come to a reasonable level and if you have saved cash. You buy it. Although you pay high interest but you pay on less amount borrowed and you bought an asset at low price too. Overall you own the asset at a reasonabally low total cost of ownership. And this is good if you plan to keep the asset and not be one of those greedy leeches who want to buy to make money from others misery at a later date.

People were saying wait for the pullback in 2017 before buying... looked what happened since. Ultimately no one knows what’s going to happen to house prices. For all we know rates could be dropping this time next year. If you have just brought a house and want more certainty then interest rate average your mortgage structure

Yes true nothing is for sure in this universe.

But it helps to have a brain and make grounded decesions and not run with FOMO. Also buy with intention to keep it not with an intention that will sell in few years when prices go up and dream about becoming a millionaire. If everyone is a millionaire, then it means one chicken costs a million too. (Hyperinflation) and that's not going to be good in anyway.

This is true. All we can do is estimate probabilities based on the evidence at hand.

Prices could go up, down, sideways, backwards and inside out for all we know.

But the evidence strongly indicates that we now have reached peak bubble.

Totally agree with 'Notagreedykiwi' on this one. So things have changed a lot in a few generations. The modesty in which our grandparents lived post WW2 has all but vanished and the hardships forgotten. We now live in a world where extreme wealth is the single goal of many, and this comes with a heavy price to communities and families with a more selfish attitude (ie flipping houses to make your fortune).

No we don't know what the future holds but we can all make decisions to set our own path. I choose to live in my one and only (first) home mortgage free, with no interest in participating in the NZ housing investment feeding frenzy so that I can look my kids in the eye in years to come and say I didn't participate in this monumental disaster that is NZ housing.

This world can barely cope with the swarms of humans now let alone if we all become millionaires and consume even more! I feel the future will have to be a more modest one, we just don't know it yet. Greed is our No.1 enemy and may well be our undoing if we aren't careful.

All these jargon numbers can't mean house prices go DOWN. Supply & demand

Immigration is 0 and we're building at record levels.

Tax changes making property a less attractive investment.

Interest rates going up. Banks tightening up.

Where is this demand coming from?

"Where is this demand coming from?"

- The monumental backlog of unfulfilled demand

- The extra 165k people granted an immediate path to residency, that previously were ineligible to buy.

I think he means demand in the financial sense. We won't buy if we can't afford to, or if it doesn't make economic sense to.

If it was this simple, we'd never have gotten to this point - demand would have tapered off long before 11x incomes or whatever the hell we're up to now. It's simply not just a case of 'economics' - you're trying to future-proof years of stability, a place to start a family, etc. House prices haven't made economic since since the mid 2000s.

I think we are underestimating the role of the bank of Mum and dad. They are drawing down on some of their massive gains over the past year to contribute to a large deposit or even buy the house

I'll take your word for that.

But job insecurity (who wants more debt if the job/income ends?), taxation issues (with M&D taking equity stakes in a purchase) and loan serviceability criteria (3% over carded rate of %?) might make drawing down any free equity a little less attractive than what it was until recently.

But as you imply - it's all about access to debt - one way or another. Demand, by and large, remains Desire without it.

The bank of mum and dad is sub-prime v2.0 in the making.

Those 165,000 people are here already and mostly renting a home as they are not allowed to purchase. When they do eventually buy a home, that will will free up an existing home. I also understand ability to get residency is some time away - end of 2022 from memory.

We have been through this before. The immigration has slowed down long time ago and it had little to no effect on the house prices.

The very slight decrease that we see in prices is mainly from Covid, the small increase in the intrest rates has little to do with it.

If you notice the drop is mainly in Auckland and surroundings where covid has been most active. Further more, the cash rate can not be raised significantly as inflation is already at crazy levels.

As I mentioned 5 years ago, buy when you are financially able to, there is a big difference today in property value compared 5 years ago.

10,000 new doctors, teachers, engineers each with a partner means demand for houses increases by 10,000. Tax revenue increases.

10,000 extra pump attendants, checkout operators, fast food workers means no increased demand for houses but more living in existing houses. Tax revenue increases modestly but balanced by increased demand for benefits.

All of these immigrants you talk about are largely to replace the Kiwis that are going to leave for Australia etc because NZ doesn't make sense anymore with the cost of living vs incomes. High immigration is going to be less acceptable going forward and I expect more to leave than before so on balance we could have a falling population for a while.

I firmly believe that young Kiwis should at least move to Australia for at least 5 years. Even if you go to Sydney you can still save a lot more than here. It's what I did.

Split emigration into two groups - those who cause NZ to lose a skill (our GPs and Nurses) and those who go abroad for experience and who may return with greater skills.

You are right - our housing costs push our talent overseas but does not deter immigrants used to very high density living.

https://www.stuff.co.nz/national/126761590/covid19-blamed-for-aucklands…

Wrong Analysis oor why half truth is twisting the facts.

Covid19 reason for population deckine in Auckland but fir two reason

1: High PHouse Price Growth (1.3 milliin - how many people can affird a loan of one millin after managing to pay deposit if say $300000 as million dollar fir FHB is still the same as ore panademic and if anything with inflation has become more hard)

2: Missing Internatiinal student and people on work permit as most people come to Auckland than any other city.

So....

Agree House price and immigration is the biggest factor contributing to population fall in Auckland.

Covid19 has been used by RBNZ and Government to boost the ponzi so for house orice rise cannit blame covid19 as was the excuse used to boost but yes for immigration covid19 is responsible otherwise no government could afford to cut immigrant be it Winston Peter (though for voges can play to the galledy) as NZ is based on immigration.

Rental prices for my North shore house has gone up but the apartment in the city has taken an over 20% decline and I'm happy to have a tenant. So it is not house prices that contribute to population fall in Auckland. Prices do go up but the buyers expect them to remain high in the future. A property purchase is a hedge against inflation.

"Property purchase is a hedge against inflation."

Could be. But isn't that what many purchasers in China were told, though?

Besides. If China does get into some sort of economic and social strife, they'll lower the value of the Yuan - a lot (you can do that when you control your exchange rate and control money issuance - the opposite of what we do); to keep their exports workers at it, and flood the World with cheaper goods.

So, relying on Inflation is not a given.

"Property purchase is a hedge against inflation." - of course it depends on the property. Cycling the Otago railway you pass many adequate but empty houses. If property prices halve in Auckland not every house would decline by the same percentage. A pleasant detached house in a suburb not too far from the city will retain more value than most. My apartment in the city was bought for $180k in 2009; it had been uninhabited for two years since built and originally advertised at $340k. I worry about the FHB buying the >$1m apartments in North Shore - a decline in the market might cripple them.

This strategy is only profitable if the nominal house prices increase faster than CPI inflation.

In this brave new world where central banks are aggressively raising interest rates to suppress CPI inflation all bets are off.

Yvil's prediction looks to be correct. I feel the market has more or less levelled off for the time being.

It had to slow down sometime...alot of people have been predicting this.

Difference is many people who have been predicting a slow down, have been saying so for 10 years plus

It has slowed down many times in the last ten years.

Or are you saying this time it's the big one?

I've seen many people predicting this months ago, including media commentators such as Tony Alexander. Nothing ground breaking here...

They are always right. price will slow down and fall.

Just like Indian rain ritual always lead to a good rain.

If you want to reduce house prices, increase land supply, reduce development contributions, remove bureaucracy.

Make rentals more profitable for landlords - that way more will enter the market.

Supply / demand equation always works.

Reduce credit growth...done, house prices fall

I can't imagine a single reason why more private landlords in the market could be a good thing.

I find Oneroof's constant spotlighting of houses that are selling for millions above CV etc after only 3 days marketing and bought sight unseen (for example) so tone deaf in todays environment, People are losing their livelihoods and no doubt houses soon too but you have these obscene celebrations of greed being flagged day after day by the Oneroof hype merchants. It seems like a total anachronism and time for it to end.

OneRoof is Granny Herald's crown jewel. If that clickbait goes, who knows what will happen.

Was just looking at some interesting historic charts, and there's a pretty strong correlation (as one would expect) between significant movement in the OCR and both house price growth and construction of new houses.

Given this, a lift in the OCR to say 1.25% in the next 6 months is likely to significantly slow both house price growth and new house construction.

And these trends tend to follow each other quite quickly, there's not typically big lags.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.