First home buyers' share of the housing market declined for the second month in a row in October, as they face a perfect storm that's turning the market against them.

Rising prices at the bottom end of the market and higher mortgage interest rates are combining to make it harder for first home buyers to get into their own home. Their situation is likely to get worse as banks tighten their lending criteria, making it harder to get low equity loans.

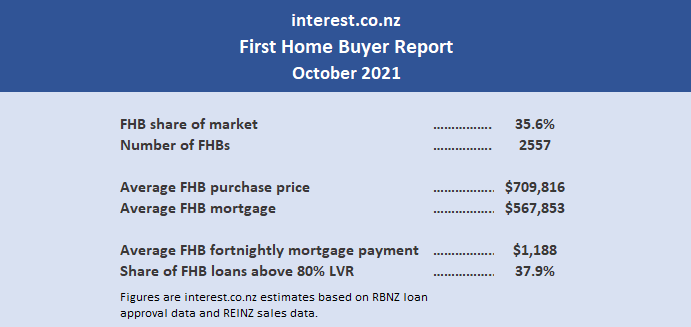

Based on the latest data from the Reserve Bank and the Real Estate Institute of NZ, Interest.co.nz estimates first home buyers' share of the housing market has dropped from 43.4% in August to 39.7% in September and 35.6% in October.

The decline in market share has been caused by the number of mortgage approvals to first home buyers failing to keep up with the increase in housing sales that has occurred over the last few months, with other types of buyers such as existing home owners taking a bigger market share.

You don't need to look far to find the reasons for first home buyers' declining market share.

In October the estimated national average price paid by first home buyers pushed past $700,000 for the first time to hit $709,816.

A year ago in October 2020 it was just under $600,000, meaning that on average first home buyers are having to fork out just over $100,000 more to get into their own home than they did a year ago.

That has also pushed up the amount of debt they are taking on to buy their home.

In October last year the average size of mortgages approved for first home buyers was $479,396. But by October this year that had increased to $567,853.

Those are national averages and the figures would undoubtedly be significantly higher in major centres such as Auckland and Wellington.

Unfortunately the outlook for first home buyers is likely to get worse with mortgage rates also on the rise.

The average of the two year fixed rates offered by the major banks has risen for the last five consecutive months, from 2.52% in May to 3.58% in October, and they seem almost certain to keep rising.

According to interest.co.nz's latest Home Loan Affordability Report, the combination of rapidly escalating house prices and rising interest rates has already put home ownership out of reach for couples on average wages in Auckland, with other regions such as Waikato, Bay of Plenty, Wellington and Nelson/Marlborough not far behind

The comment stream on this story is now closed.

• You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register (it's free) and when approved you can select any of our free email newsletters.

65 Comments

NZ godfather Adriano de Ponzi fed the rich and closed the gate; now the poor should be happy they can enjoy having a job, so that they can pay rent to the rich..

The irony being, many of The Rich aren't actually rich! It's all paper richness - that 'wealth' can evaporate at the stroke of a key.

They are rich in a RBNZ tokens.

Having enough to be comfortable is all that most people worry about. But how much is that? Because people in Africa and Asia are poor but the surveys say that they are also happier than us kiwis.

lol, rich? Rich in what? If I am having a $800,000 mortgage, in a 30 years term, I will have to pay $1,502,280 in total by today's 3 years interest rate 4.75%. That's double of what I've borrowed.

Paying off the 800k is the capital amount. The difference of 702k is the interest cost. Have you considered how much rent that you would likely pay over a 30 year period at an inflation rate of 5 percent. I would say that 700k is pretty cheap and works out to 450pw fixed for 30 years

There is reason that Government and RBNZ wouldn't allow that high inflation rate. Can you image when inflation rate is 5% year on year through 30 year period and how you need to pay both your mortgage and living cost? I can assure you that once inflation rate stays 5% for a period of time and without any action taken, it will continue to go up.

Another perfect storm. I wish Sebastian Junger had never written that book.

First-home buyers will do well over time.

Housing market is destined to make a soft-landing, after 3 years solid price growth……

Most house owners/investors will land with their bums in the butter. ✅

TTP

We actually had a Soft Landing on the go in 2012. It was all doable back then and wasn't going to hurt as much - if at all. So I don't share your confidence that we can do it in today's environment. I'm sure many of us have seen what happens when someone yells "Fire!" (Is that a translation of Adrian's' words yesterday?)

Even in 2018 the market got jittery. Talk of a capital gains caused this.

Oh dear, there’re a few little Doom Goblins hanging about here today….. 👿

TTP

Yes and they toast Pollyanna's for smoko

I'm sure you've started Doom in the face over the course of your life. A few words written on a blog, isn't it ☺

It's that time when your vision of the World shrinks to the size of a pinhead. All that is in your vision is the tiny picture of the actions you took that got you to where you find yourself. Doom is seeing experienced professionals frozen at their desks; unable to speak or move; or mature Chartered Surveyors (Real Estate Agents in the UK) gasping and sobbing uncontrollably as they look at their portfolio of 'can't lose' holdings. Doom, you say? We don't know the meaning of the word here, today.

TTP - Why do you think a belief in pending price declines aligns with a doom and gloom attitude?

Cheaper houses mean more people can afford to buy, you can get a better quality house for the same money, mortgages can be paid off quicker, more money is available to invest in business, more discretionary funds for leisure / healthcare / education / children etc. Of course there will be a period of pain for many - but those who don’t study and learn from history and economics have nobody to blame but themselves.

The ever upward price spiral to date has created a society of lazy smug ‘investors’ and diverted resources from production and enterprise which facilitates a prosperous society.

A realignment in the near future is inevitable - and I for one am excited for the future.

Why do you think a belief in pending price declines aligns with a doom and gloom attitude?

Entitlement

Its all gambling TTP. The bulls have had the last 20 years. Will they have the next 10?Place your bets

You can’t taper a ponzi

Its hard to be patient when you're young - but for low deposit FHBs this really is a good time to sit on the sidelines for a bit and just observe

Has it ever paid off to sit on the side lines for NZ Property?

In 2007 it did

I remember price growth slowing to about 2% in 2007. Hardly a crash even though they called it one. The market stalled briefly before soldiering on.

The best time to buy a house has always been yesterday.

Trying to time the market is a mugs game for sure - most of the time. But the current situation is a no brainer against property for the very near future. Not life or death if you have built up plenty of equity - but for vulnerable low deposit / tight servicing first home buyers it’s a very risky time to be exposed with your hard earned savings.

So what do they do...sit back and watch their savings become worthless with inflation?

If your money is in cash for a year, inflation will drop it say 4%… but if you gear up at 90% and the market drops 10% you’ve lost the lot… negative equity is mostly ok if you can keep paying the mortgage - but heaven forbid you lose your job or can’t afford the higher rate.. #toast

All I’m saying is this is a turning point in the market and FOMO is an inappropriate attitude. Don’t wait forever to buy your first home - just be cautious for the next 6-12 months is all - in my view :)

That's question you can probably tell us all the answer to Nifty.

Lets assume like a FHB you can afford a bigger (or another) mortgage.

Are you out househunting at the moment?

Me personally - I'd be sucking up that inflation on my savings for at least the next 3 months.

Where will the money for further house inflation come from?

Household debt already at historic Highs. The rbnz winding backs its money printing spree. Interest rates are following wholesale rates up.

Without further credit expansion, I just don't see this party going much longer.

Hedged either way of course. But I think we are a ticking bomb of an economy. Anyone with half an objective brain see the data.

People have been saying this for years now. They were definitely saying it when I bought my first home in 2018. The truth is, no one really knows.

Agreed, we're so far past the point at which economic cycles and logic say we should be that it's totally without precedent. Conventional economic wisdom is broken, because central banking figured out they could break it. The rest of us are just living with the aftermath.

Nobody really knows who will win a poker tournament either - but the same people keep ending up in the final.. ;)

Little mention of the very recent challenges introduced to lending criteria. More coming on December 1st. The pain for FHB's as well as the wider market is only going to get worse and that's without DTI's being formally introduced or interest rate rises.

I hope the perfect storm hits the market to the tune of a 10-15% drop over the next 12 months. I don't want recent house buyers to come unstuck but somethings got to give or we're going to lose a generation of bright young Kiwi's to other more affordable shores.

I think something most people neglect. Is that a dip of say 30% would in reality only really hurt a few people.

Not that many houses have been bought sold over the last two years, and that would only take us back to 2019. Easy come, easy go.

The vast majority of house owners have not bought at these extravagant prices.

Plenty of room for a downward correction.

The trick is to be well placed regardless of whether it goes up or down.

With full border reopening in May next year I think we will approach housing market apogee for this cycle.

That said it looks like local councils are lobbying government pretty hard to walk back urban densification and the Ministry of Housing is dragging it's feet on using the UDA at scale. All indications the supply side will not be "turbocharged" by measures as central government had intended.

I think the reality of a greens & labour coalition govt and the property taxes that go with this will start to weigh on prices next year. The market won't like it.

House prices are beyond affordability for many Kiwis so they simply cannot afford to buy homes. The house building and land supply are totally corrupt and the cost of new houses are racing away with the ponzie driven price rises. The usually healthy response to a shortage is an increase in production at only a slight price increase and a return to market stability. Is this what we are seeing?

The safest way for young Kiwis to navigate the future is to get out of New Zealand.

Let's calculate how much an average kiwi on a average salary will save over their life time.

I take a positive view of average salary at 70000. Take home after tax will be 55k.

If they have some expense or good forbid they eat food, then spend 10k on food per year. Which is $200 per week. So now they have 45k in hand. If they drive a car, than 3k per year for gas and car maintenance. Now they have 42k in hand.

Utilities bills of 3k per year. And now they have 39k left for them to spend.

Now if they own a house for average house in NZ costing 850k. Let's imagine they made 20%deposit of 160 k and now they have a mortgage of 690k. At 3.5 % their yearly interest on this mortgage is around 24k. This is only interest, no principal payments. They are left with 15k now. I am sure they have to pay rates on the house. Even in cheap towns, it's around 4k a year. So they have 11k left with them now. Lets add house insurance. 10k now. If they pay 5k principal on the home mortgage, they have 5k left to save for their retirement per year. And i haven't calculated kiwi saver or any discretionary spending anyone has.

And this is a single person. If they are a couple, we can have some synergies and save but god forbid if they have any kids.

So is this a sustainable economy or a country where any one can live a decent life?

You tell me..

Does the kind of person who spends 3k a year on gas to pollute the environment really deserve to own a house? Especially if they also manage to spend 10k a year on food for an individual!

Gas, maintenance, tyres, registration etc etc. 3k is conservative for most living in Auckland having to commute.

If we weren't smack bang in the middle of the mother of all housing bubbles they could probably afford a Tesla.

So I take it you are against the disabled having access to hospitals, community and medical care as well as often the only transport option is petrol. The whole if they have to use petrol they don't deserve to live argument does not bode well for your moral compass, It may have rusted completely to dust and you will kill many people with that attitude. But it's ok I hear you say it is only the disabled and elderly dying without homes, access to medical care and basic living necessities, not me yet. Also protip the staples shopping budget also likely includes other staples like basic soap, replacement for a minimal amount of clothing e.g. 1 pair shoes, warm blanket, towel, jacket, pants, underpants for a wash day, shirt, cleaning products, bandages to mop up the blood and bleach to clean after it etc etc.

It is what it is mate you just have to get on with life with the cards you got dealt. Its simply a fact that not everyone will live in a million dollar house, that's just the way it is. I opted to stay single and not have any kids so why can't you ? Don't want to do that then you have to pay the price somewhere else, not many people in life get to "Have it all" and even then some of them are still as miserable as hell.

A million dollar house is the average in Auckland. I don't think having a roof over your head is wanting to 'have it all'. Christ.

"I opted to stay single and not have any kids so why can't you?"

This isn't even a good troll.

Hey, there's the answer to happiness! Stay single, don't have children, eat baked beans every day, don't eat avocado on toast, and you too can own a crappy townhouse on no land and be happy and successful!

As opposed to get married have a couple of kids have everyone eating baked beans while your trying to pay the rent for the rest of your life ? Chances are your better off single if the wife decides she doesn't want to work. Basically you now need a bloody high paying job in this country to enable you to live the the lifestyle that most people feel they are entitled to these days. The days that I managed on $60K with a flatmate are long gone and there is no way any of the work I was doing is now paying $150K, in fact its probably got worse looking at the immigrants in one place.

It's a very sad state of affairs here.

That's why I'm taking my lovely wife, my kids, my high paying job and my business to Australia.

We will be living a vastly bigger and nicer place we will be mortgage free in our early 40s.

The wife can go back to work when it suits her and it will be an amazing lifestyle upgrade compared to Auckland.

Plenty more will flee in our footsteps.

Spot on, don't waste time going to open homes in Auck, you will be disappointed.

Better to put energy in a place where you grow rather than in a place that will push you toward deprivation. I know people who are very serious to move to Aus and never come back. After Orr's latest statements now we have to accept this is new normal, as soon people accept it and leave hope of market correction will be good for them.

I see many people hoping for 10% 20% or 30% correction from 2018 but see where we are. Better to leave NZ and go for a secure and happier life, NZ can only give false hope and pain.

Been to quite a few open homes in Auckland it's a tragi-comedy.

No prices of course. Just lies from real estate agents underquoting even the reserve price.

Pretty sure RE are legally not allowed to disclose the reserve price. I believe there are some other quirks that I came across with my current house purchased at action in that if you disclose to the RE what your prepared to pay for the house they are obligated to pass that information to the vendor.

RE agents are lower than cockroaches.

They will happily tell you their "opinion" on where they think the reserve price will be (even though they are working hand in glove with the vendor). "Oh around 1.4 or 1.5 million". When you watch the auction later, it will pass in without even reaching the reserve at 1.8 million. I made a habit of recording their numbers and watching auctions to check up on how much they were lying. Every single time they would unquote by 15-20% just to suck people into bidding. They are vermin.

If there wasn't several thousand dollars worth of due diligence involved in reaching the stage of bidding it would be less of a problem. It should be made law that the reserve price is made public two weeks before auction.

The whole system is rigged here.

Moved to Aus earlier this year. Applying for residency now. I will never return to NZ, period. It's so much better here, I wish I'd never returned.

Hate to remind you mate we need the growing population to pay for your benefit when you get over 65. And we need people to have family medical carers so we as a country can save big bucks on the medical nursing support costs (it is hard to beat free through a child family member when compared to someone we would have to pay to take care of you when you are infirm).

Carlos decision making is very suspect, last week he claimed he was rich aa?

Yes its funny how everyone thinks I'm stupid in life, I have just got used to it now days. The reason I have money is my ability NOT to pay anyone else to do life's jobs. Brock stated he needed to spend "Several thousand" dollars on a house before an auction, well I did the house inspection and all the other work before purchasing my current place and didn't spend a single cent before the auction. From my cars never needing to go into a workshop, to repairing anything electronic to landscaping and fencing I can count on one hand the number of times I have had to pay someone else to do a job. Have a guess at my current net worth Frazz.

Perfect, this is what our society is pushed toward.

Now starting a family is considered a success, which actually is the very basic thing & what you are saying is a reality. I know people who are not going to marry because they cannot afford a house.

For many having a family means life & happiness, without it we cannot imagine living (there is no point).

NZ is no more a country, it's a business.

Hate to remind you mate we need the growing population to pay for your benefit when you get over 65. And we need people to have family medical carers so we as a country can save big bucks on the medical nursing support costs (it is hard to beat free when compared to someone we would have to pay to take care of you when you are infirm).

The reality is that in nz we are shrinking as a population without migration. People making decisions like this is why.

Not exactly what you call a healthy well functioning society if we cannot afford to naturally replace our population.

Money printer goes bbrrrrtt.

Oh look global warming!

"We are going to need a bigger printer"

The main culprit is government and rbnz who went all out to support the ever growing housing market. Who can forget Mr Orrs policy of LEAST REGRET when it come to supporting the ponzi and when the time s to control is WAIT AND WATCH - playing with time, using all tactics SO THE BLAME ENTIRELY IS WITH ROBERTSON AND ORR- Main culprit, who still are not acting in right earnest to control as they have no true intent.

They don't give a shite about the housing market. They just needed to pump dollars into the economy and This is How we do it in nz.

All optics are Staged. This activity has been quite deliberate.

Everything is political. Especially houses. Our boffins are just cut & pasting what the others are doing. It doesn't really matter what colour you are. We are a global village whether we like it or not. Let's be grateful for the fact that we can print our own money & get away with it. Most countries cannot. We underwrite our currency with food, which is good because most people need to eat. Australia does it with coal & iron ore, which is fine if China is booming & you can stay friends with them. America does it with IT, law & education. The Uk does it with education, banking & IT. The French do it with perfume & holiday makers. Germany does it with cars & other engineering expertise. Russia does it with oil & gas to Europe & now to China. We all need to underwrite our relative global value with something. So, the prices of our houses keeps going up. Not forever my friends.

....on the market for Kiwi Pesos NZD 1,449,000

https://www.oneroof.co.nz/24-ruawai-road-auckland-1673635?

......or for the same price in USD

https://www.zillow.com/homedetails/5628-Desert-View-Dr-La-Jolla-CA-9203…

you choose .......... the emperor has no clothes .....kiwis are deluded .......La Jolla, CA v. Mt Wellington ......no contest

No doubts house prices are stretched and today no one is thinking but ....

So does this mean that we can now expect another quick round of panic buying?

First home buyers' share of the housing market declined for the second month in a row in October, as they face a perfect storm that's turning the market against them.

I'll be more optimistic about this.

The above scenario also means that more FHBs will be stuck renting which is good for rents- nothing like a captured demand in the market.

Astute investors should absolutely seize the opportunity before others start smelling it.

Be quick!

CWBW ......have you noticed that the NZD is tumbling right now .....Great exchange rates for those overseas buyers !! ...who gives a stuff about FHB's anyway ....lock them in rental serfdom for life paying your rents ! ......you guys can buy and sell to each other until only a few groups/individuals actually own any property and then retire to Hawaii (like your cohort John Key) ...... what a great way for New Zealand to go :) ......BACKWARDS !!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.