The housing market may be at a turning point for first home buyers as mortgage interest rates take a breather from recent rises and prices at the bottom of the market continue to fall.

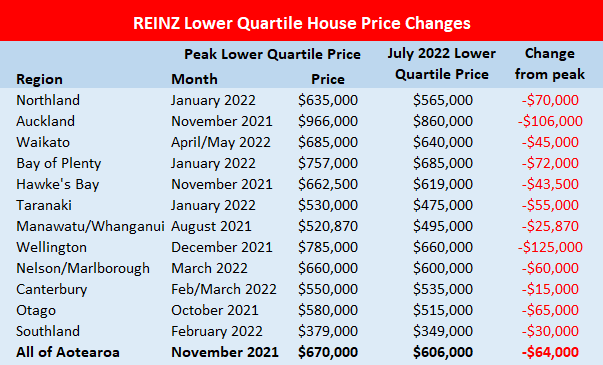

According to interest.co.nz's Home Loan Affordability Report, the Real Estate Institute of New Zealand's national lower quartile selling price, the price point at which 25% of sales are below each month and 75% are above, peaked at $670,000 in November last year. By July this year it had dropped back to $606,000, a decline of $64,000 (-9.6%).

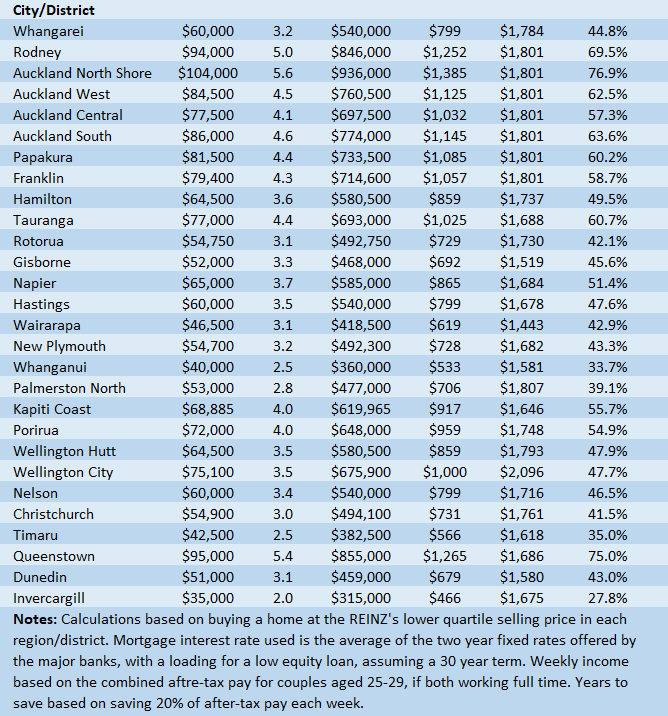

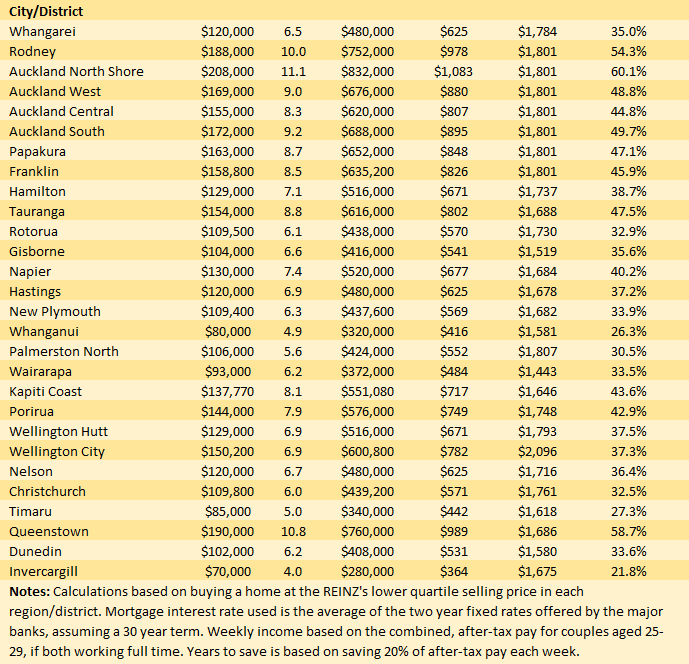

The table below shows how much lower quartile prices have declined from their peaks in each region. The biggest decline of $125,000 was in Wellington, and the smallest of $15,000 in Canterbury.

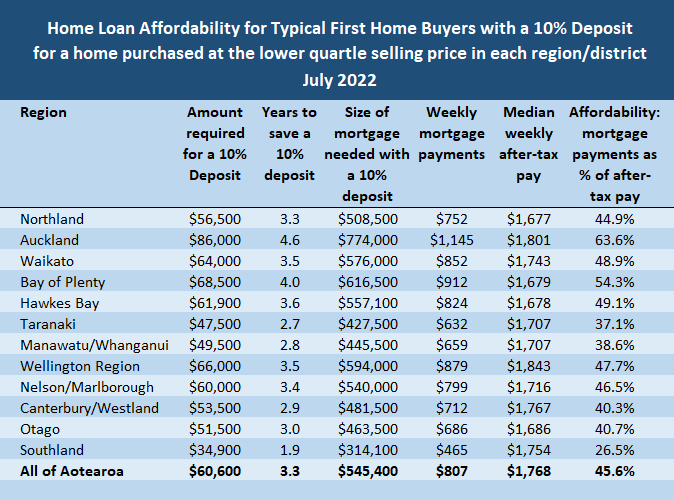

Lower prices should make it easier for first home buyers to get into a home of their own because they reduce the amount of money they need for a deposit, and the amount of debt they need to take on for the mortgage.

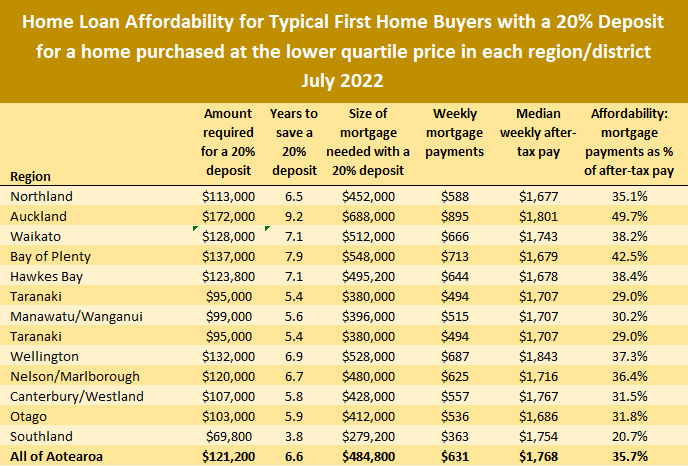

The amount needed for a 20% deposit on a home at the national lower quartile price has declined from its peak of $134,000 in November last year to $121,200 in July this year (down $12,800), while the size of the corresponding 80% mortgage has declined from $536,000 to $484,800 over the same period (down $51,200).

In Auckland, the country's most expensive region for housing, the amount needed for a 20% deposit on a lower quartile-priced home declined from its peak of $193,200 in November last year to $172,000 in July. That's down $21,200. The amount needed for an 80% mortgage declined from $772,800 to $688,000, down $84,800, over the same period.

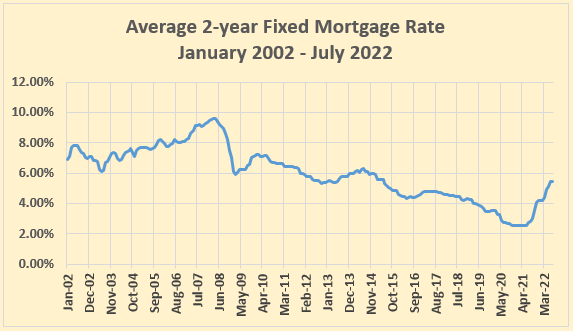

Normally, a decline of that magnitude in the amount being borrowed would also result in a reduction in mortgage payments, however the rise in mortgage interest rates over the same period has been so steep that mortgage payments on a lower quartile-priced home have actually increased even though the amount being borrowed has declined. The graph below shows the movement in the average two year fixed rate since 2002.

The Home Loan Affordability Report estimates that the payments on an 80% mortgage, $536,000 for a home purchased at the national lower quartile price when prices peaked last November, would have been about $596 a week.

In July this year, the amount needed for an 80% mortgage to purchase a lower quartile-priced home would have reduced to $484,800. But the payments on that would be about $631 a week, an extra $35, even though the size of the mortgage had reduced by $51,200. That's because interest rates have risen so sharply over the same period.

In November last year the average of the two year fixed mortgage rates charged by the major banks was 4.08%. By July this year that had risen to 5.44%.

Essentially that means over that time, buyers at the lower end of the market had benefited by needing less for a deposit and would have had to borrow less. But they would have faced increasing mortgage payment costs, which would in turn restricts their ability to make a purchase.

So what they have been gaining from falling house prices they have been losing to higher mortgage interest rates.

However July may have marked a turning point in that trend with rises in the average of the two year fixed rates almost coming to a standstill at 5.44%, compared to 5.43% in June.

At the same time lower quartile prices continued to decline, with the national lower quartile price declining by another $24,000, from $630,000 in June to $606,000 in July.

If that trend continues, first home buyers will be in the money with a winning hand of lower prices, lower deposits, smaller mortgages and lower mortgage payments.

So what are the chances?

The graph below shows the monthly movement in the average two year fixed mortgage rates charged by the major banks from January 2002 until July 2022.

While the steepness of the increase since the middle of last year is unusual, matching the decline that followed the Global Financial Crisis in 2008, there is nothing unusual about the level of current rates.

In fact the graph suggests they have just been heading back to longer term norms.

However even if interest rates stabilise around current levels, house prices would have to keep declining for first home buyers to start receiving any meaningful benefit in terms of affordability.

The comment stream on this story has now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

124 Comments

Unfortunately with recent movements in swaps, that slight dip in mortgage rates will likely be short lived.

Markets conviction that central banks will soon start dropping rates seems be fading.

All eyes on Jackson Hole I guess, but I’m seeing increasing acknowledgments that inflation could be stickier, more structural, than many assumed.

.....in other words no one has any idea what is going on.

FHBs ought to make hay while the sun shines. Price discounting doesn’t happen too often.

TTP

Never make hay while you expect rain!

hahaha, TTP I love it. you put a smile a face with comments like that. hahahaha

Fortunately, FHB's are not as greater fools as you would hope.

I wonder if the fhb’s got bargains during the chaos of the global financial crises are regretting it now.

They did the right thing, at that time.

What is your point?

That now is not different than then?

My opinion is that now is very different (mostly because the interest rates are going in the inverse direction, but not only because of that).

Would you say that now is a good time to buy an house? Would you buy an house?

I agree TTP - I give it 12-18 months and rates will start dropping again

Not that I rate him, but on banking matters he must know a thing or two - TA reckons mortgage rates won’t go much higher at all, at least for fixed rates. Even if the OCR rises a further 1% to 4%.

Regarding OCR going another 1% yes but not another 4%. 4% increase would have the OCR at 7% and there is no way 1 year mortgages would be 4% then. Another 1% is priced into fixed rates already which makes sense.

What could easily happen though is that inflation is more sticky than expected, and also the oil market is very tight and could go way higher. TA's call is using what the market is pricing currently, but the future can easily play out quite differently.

I think you misinterpreted what I said. i am talking about the OCR increasing a further 1%, from its current setting of 3%, up to 4%.

About 10 years ago TA implored everyone to fix their mortgages now because rates were definitely going up. They went down, and people that followed his advice paid dearly for it.

Haha - anyone from the president of the USA, to JA to TA who says they KNOW what the OCR will do. Is lying. Their opinion is all they can offer based on current events AND likely their bias...

TA may well offer his honest opinion. But if my salary and business rested on keeping mortgage brokers happy - for sure i wouldnt write that the OCR and mortgage rates might well go stratospheric in a year.. lol. Hi ]s customers would leave in droves.

Also important to note is that just last year we were told reliably by all the worlds reserve banks that inflation was transitory. Eventually they capitulated (did not apologise) and admitted it was a serious issue and started raising rates to stop it. So if they or TA is wrong again.. dont expect their help.

Earlier in 2022 (pre march) common opinion from governments was that Putin was posturing in Ukraine. We are now in a full blown war with no end in sight and massive energy spikes.

A couple years ago Germany rebuffed trump when he pushed very hard for them to become less reliant on Russia for Gas. They knew best.

So - who knows what the future offers. However certain facts we cant ignore. Things are more risky now, not more stable. Our housing market is overinflated, China is far more likely to invade Taiwaan than a month ago, inflation now may well be structural and take a year or more to bring back down. our OCR (and with it the mortgage rates) may well go up to 5%, 6% or more, and our house price may well fall 50% or more in the next few years.

The probablilty of a 'black swan event' has risen for sure. So FHB should be sure to understand what they are getting into. It might all be good... but owning a house at half what you paid for it, losing your job and living on baked beans is a pretty full on outcome if it goes bad.

I remember it well having fixed 1m for 4 years. Thanks Tony hahaha. But at least I was able to write off the interest which is not allowed now

Between 2011 and around 2020 a lot of expect commentators incl. bank economists and talking heads said rates were going to imminently rise. They rarely did and even then only temporarily.

I ignored them and always fixed short.

I can only conclude either 1. They are terrible forecasters or 2. They aren't terrible forecasters, but then why would they get it so wrong?

Yup you're right I misread that.

as long as governments keep throwing more cash into the system, inflation will be "stickier" than expected...

He's generally optimistic so is widely disliked on here

What a silly comment

Yes its like calling people doom gloom merchants. Its offensive these days to be the bearer of any bad news, or even mention the possibility of bad news.

Why? Because it threatens the status quo, and the status quo is good for some people and it scares them that things might change. For example, people who have become wealthy by doing nothing by buying property, are terrified that if house prices fall, that their empire will collapse around them. So it is very important to control the narrative so that people don't believe it could be true that house prices might fall.

Hence all of the desperate attempts of the likes of TTP, P8, CWBC etc to silence and humiliate anyone who thought house prices could fall by labelling them DGM's - it was essentially a tactic to publicly shun people who threatened their selfish empires.

Honestly I don't think it's malicious as that. There might be some genuine malice from some but for most they were just following the crowd and the easy money. I tried to tell friends and family last year about how we're in a middle of a property bubble and they looked at me sympathetically.... feeling sorry for me because I'm scared of taking the leap into property ownership or something.

I'm happy to admit I'm outside of normal, but pretty much every "normal" person believed the narrative that house prices always go up. Even our leaders. Even now today people believe that in the long term house prices always go up. Whether it's true or not, their shared belief is what creates the market bubble, it's so obvious to me but for some reason most people just can't wrap their heads around this simple idea. Is it our natural desire to fit in and socialise with our neighbors, combined with our lack of financial literacy, that blinds us to what we're collectively doing? I don't know.

Yes there are herds and group behaviours/narratives but then you have to watch out for the wolves in sheeps clothing who take advantage of those who don't know any better (i.e. those who you refer to above).

Having lived through a property bubble in the US its all much more obvious the second time round as you have seen the signs before - and you've experience the pain in the aftermath. I've also read quite a bit about behavioural financial/economics/bubbles/asses pricing, psychology etc.

I decided to challenge those who were behaving like wolves in sheeps clothing the last few years because on this forum because I could see what they were doing - that is they were trying tp spruik prices for their own financial gain with no care for those who they were potentially harming in the process. I was also meeting similar people within society.

So to you it may not appear malicious....but just remember that about 5% of the human population are narcissistic psychopaths...they don't care about you or anyone else except for themselves. They happily try to manipulate others in order to better their own position. I've got a pretty good handle of who that 5% would be on this forum over the past 5 years and hence I've continued to challenge their position. Some have no gone because people can see through their intentions...but there are still one or two who are trying to mislead/deceive people for their own benefit. And i think those who can see it for what it is, have a social responsibility to continue to call them out.

You are right - but to be fair its their job.

If you are a Real estate agent your job to sell houses, mortgage broker to get people to take big loans, TA is a mortgage broker marketer really.

Same as all investments its vital to form your own opinion before jumping in . By all means read the opinion of TA, of Mr Orr or Jacinda. But also talk to people who have experienced a crash, investors who have got through the GFC, read up on finance, understand the economic boom-bust cycles... you can bet anyone who got rich the hard way either read up on how money works, or pays someone they trust who does.

Too many peeps these days seem to only read mainstream media and put too great a percentage of their money into houses...

Its nobody's job to push unethical investing on others....we each have the capacity to think and act with morals.

Yawn how boring

And one of the 5% joins the conversation.

Sarcastic wit. Maybe you really are not so empathetic as you would have us believe.

I have read enough of your earlier posts that you present yourself as capitalistic and capricious. Now suddenly you found a conscience and got preachy.

Keep going HW2, you're proving the point of my post above. I must be shunned, belittle and silenced by those with vested interests - because I can see through them and risk changing the narrative against their unethical investment rort (property investment during a housing affordability crisis). Gotcha.

Enjoy your evening, I'm off for a beer.

Tell me what exactly are you doing to put your money (either literal or other) where your mouth is

IO doesn’t come across as capitalistic and capricious at all. Rather he comes across as very fair minded, balanced, socially conscious and intelligent.

That's ok. You misread the comment

?

My concern is that people are not told why house prices are increasing. As was recently reported one of the reasons was decreasing interest rates. Don't forget that many column inches were written about why interest rates would remain low - then something changed. Without understanding why something has happened and can that something continue to happen people end up making assumptions that are wrong.

The path we have chosen over the last several decades has lead us to this. It's all about the individual finding ways to benefit themselves through whatever means possible and property simply turned into the ultimate vehicle for that. And like any other tradable commodity there is a lot of BS that goes around to spin the narrative for a positive outcome.

No different than walking the aisles of a supermarket or a car yard, property was just something to be manipulated and the people in the game will do whatever they can to keep the party going. Ethics, morality and fairness were never part of it, just like the breakfast cereal that claims its healthy and full of fibre but is just pure sugar , or the Ford salesman that swears black and blue that Fords are the best vehicles ever made.......until he changes jobs and works for Toyota. If you just drink the cool aide and believe every word you hear or read, then you will likely end up overweight, driving a crappy car and in negative equity, but you can't blame the salesman.

... I was a DGM when house prices were rising rising to wildly giddying speculative prices ...

Very happy now , joy that the bubble has burst , the aura of tax free gains has evaporated ....

... one day , we may get back to that hallowed point where regular Kiwis , friends & families , can afford a home ....

Indeed GBH, it feels good for society to have this happen. I have said before how I fear for the FHB's who have made the leap and will now suffer significant hardship, possible bankruptcy (sooner the better if they are smart) etc, but society in general will be better if more people feel invested in it.

Optimistic about what? High house prices? If we were talking about petrol prices would crazy high unaffordable prices be considered optimism?

It's crazy how people calling for a lower cost of living are often seen as 'negative'.

I guess the equivalent would be discussing food prices in an environment where most Politicians and people crafting the media narrative are supermarket owners. High food prices are a good problem to have! It shows people want to come here and eat our food!

Optimistic prices will drop and house prices will become affordable for first home buyers and future generations. Is TA the same hope he cares about future thats optimistic.

Think we can see now that all these economists are taking guesses. I personally feel that TA with his real estate agents sampling is basically flawed. Do we think that it's impossible the bosses of agencies aren't telling their employees what to write? It's in their interests to fudge.

He certainly gets referenced a lot in their increasingly deranged emails explaining why now, is the time to buy. I feel that TA extrapolation from that, on interest rates and their future, should be taken with a grain of salt. Especially when we are starting to see double digits overseas.

TA reckons, huh? Kiwibank 1yr special currently still 4.95. I reckon if OCR reaches 4%, that special rate will be setting a floor around 5.95% at minimum. Also have to factor in the end to the FLP which is an interesting one. But that's probably enough reckons for one day.

Wait till the mortgagee sales start. They will set a new valuation data point for the true market, devoid of cheap debt, and tax avoidance speculation sweetener. The banks will then base lending off those sales and vola - the real market.

Just met a couple yesterday whose landlord had given them 90 day's notice as wanting to present house for vacant possession, and has already listed the house. Said landlord was unaware that part of that specific notice requirement is that the property may not be listed until the tenant's have moved out - making their action in listing it illegal. (They may list and have the purchaser decide vacant possession, however).

I wonder how many people are going to be caught out on that one - wanting/needing to list now, but forced to wait potentially another 90 days? How long till we see cases at the tenancy services where clued up tenants take on said landlords?

Maybe true but seems like a ridiculous rule, I get 90 days, I get the tenants shouldn't have to let prospective buyers through their house, but they should be able to agree, and if you have a good relationship with the landlord why not. Why should the landlord have to wait while not getting rent.

It actually sounds like good loophole to get tenants out, I am "planning" to sell my home, once the tenants are out "oh I changed my mind".

Could be a good opportunity for a compromise - you let me show a bunch of randoms through your home and in return you only pay 50% rent while the property is listed. Or maybe I give you $100 per showing?

No idea if the regulations allow for this though.

It's exactly that loophole it's intended to deter. The tenants have a contract on the property, and the landlord wants to end the contract. Part of that change potentially costs the tenant money. So this shares the pain a little bit in order to discourage that behaviour - though I personally think a better solution would have been that landlords who sell out from under tenants are required to pay their existing, contracted tenant's relocation costs. Especially over the last decade where landlords have been selling up to crystallize capital gains.

I agree, and in the one case I needed to do this, this is exactly what we did (plus the post move clean etc).

Renting has certainly got a lot better for the tenant recently and feels more equal now as it should be.

The problem is that 'being able to agree' would very quickly turn into 'having to agree.' If your landlord has given you a 90-day notice, you need to find somewhere else to live. How many tenants are in the position where they can risk not getting a good reference from their current landlord, given how difficult it's been to get a rental for a very long time now? So it puts people in the stressful position of having to find a new place, while keeping the current place spotless and frequently having to leave the house while random prospective buyers walk through. And if they say no to this they seriously impact their chances of finding a new place to live. Why should the landlord have to wait? Because the tenant has paid them for quiet enjoyment of the property. The landlord can't decide not to provide that anymore because it's not convenient to them while the tenant is still paying for that.

It’s a DGM crap-fest here today……

But before you know it, they’ll be whinging and moaning that they didn’t buy a house in 2022 - when prices were cheap.

TTP

Many or most of us own homes…,

There's a particular kind of poster who doesn't believe anyone who owns a home could think that lower house prices are a good thing. Apparently we should always pursue our own narrow financial self-interest without any consideration for the rest of society.

Some of them even think we assume the price falls we want won't apply to our own homes...

The tenants are well within their rights to refuse any marketing photography while they live there. I certainly would.

These landlords who want all the benefit of being a lord of the land, but have no sense of noblesse oblige.

(3) With the prior consent of the tenant, the landlord may enter the premises at any reasonable time for the purpose of showing the premises—

(a) to prospective tenants; or

(b) to prospective purchasers; or

(c) to a registered valuer engaged in the preparation of a report on the premises; or

(d) to a real estate agent engaged in appraising, evaluating, or selling or otherwise disposing of the premises; or

(e) to an expert engaged in appraising or evaluating the premises; or

(f) to a person who is authorised to inspect the premises under any enactment.

(3A)

For the purposes of subsection (3), the tenant—

(a) may not withhold his or her consent unreasonably; and

(b) may make the consent subject to any reasonable conditions.

https://www.legislation.govt.nz/act/public/1986/0120/latest/DLM95504.ht…

So not really, according to our legislation.

Practically speaking there is normally an arrangement agreed between the parties to show the property at a time and in a manner not to disturb the tenant.

Hi, I can't be bothered looking up the legislation right now, but there is most definitely a clause in there that says tenants can withhold permission for marketing photos. And they don't have to be "reasonable" or even give a reason.

I'm sure it's in there, was looking at that legislation just a few months ago.

... actually back at that time I also looked into old Tenancy Tribunal decisions, to get an idea of what "unreasonably" withholding consent for viewings means.

The Tribunal ruled in one case that it was "reasonable" for the tenant to only allow viewings on Tuesday evenings, between 4pm and 5pm (or something like that). The Tribunal thought that the tenant was being reasonable to limit viewings in this way.

The problem, of course, is that most tenants need a reference to get a new rental, and so very few are in a position to actually assert their legal rights.

Fitz were you trying out your bush lawyering skills

When we bought our first home in 2017, the tenant in the place was only allowing viewings at weird times such as Tuesday mornings between 10 and 12. Fortunately my wife was on maternity leave, and the accidental landlord was looking for a quick sale. I signed the S&P agreement sight unseen.

Where does it state that - Looking the Tenancy Services website, you can still list a property with the tenants living there.

https://www.tenancy.govt.nz/ending-a-tenancy/change-of-landlord-or-tena…

Prices have a way to fall yet imo. The momentum is downwards, affordability is still atrocious in most regions and economic activity is slowing.

The tide is not out, its an approaching Tsunami of forced sellors.....

Normally, a decline of that magnitude in the amount being borrowed would also result in a reduction in mortgage payments, however the rise in mortgage interest rates over the same period has been so steep that mortgage payments on a lower quartile-priced home have actually increased even though the amount being borrowed has declined.

This is what many here either don't understand or choose to ignore... it's simply not easier for FHB's...

True, it is actually still very difficult for FHB... and without new blood in the system the pressure will need to go much more down.

... if an average 3 brm house in NZ has dropped in price from $ 1 million , to $ 840 000 ... does that make it affordable , will the FHB's be lining up ?

I'm calling BS on Tony Alexander , Ashley Church , Mike Hosking , & all the other property spruikers

... house prices are still double where they ought to be , if we had proper functioning councils & governments ...

... and reserve banks...

Don’t forget the cost of building

This will be affected by reduced demand to a degree but the base materials and the cost of labour will still carry our current inflation into their pricing I would say, thereby keeping the price of new build elevated from past times.

Trade off interest deductibility vs higher prices due to labour and materials. Yield on new builds may still prove to be higher than existing properties, for those who can afford to attend the dance.

Correct the math needs to look at what you pay in TOTAL over the life of the loan, not just what you are paying off per week. What you are saving now due to price falls is not offsetting the rate rises.

That's why smart kiwis aren't getting involved in the market, especially FHB's.

You won't time the absolute bottom, but you can score a MASSIVE discount.

Simply do nothing or go overseas.

Yes and no, it does however mean you can save for a home, Higher saving interest rates, house prices are not going up but down. Wait a while build up a bigger deposit, so if you manage to get a 40% deposit then you probably are saving. Previously getting a deposit for a first home was a moving target.

The math also should include things like lump sum payments. And of course, pay rises.

If someone receives a pay rise of 5% and puts that all towards higher mortgage payments that increase comes straight off the principal. An extra $50 per week against a $800k vs $500k loan is a big difference.

Just to annoy you Nifty I'll reply....

A few FHB's I know who had a 20% deposit ready last year on a house price at $750,000, decided not to buy (so a deposit of $150,000). If they did they would have required a $600,000 mortgage.

The price of the house (or similar house) is now only worth $600,000 and their deposit, after another year of saving, is $170,000. So to buy the same house/standard of house, they now have 30% equity instead of 20% equity. The size of the mortgage required has dropped from $600,000 to $430,000 with the possibility of falling interest rates next year as recession bites.

For these FHB if/when the chose to buy it has got easier as the size of the mortgage they require to buy the standard of house they want has reduced by nearly 30% in a year with the possibility that they will get to re-fix onto lower rates in a year or two. But even if that doesn't play out, their mortgage is 30% less than the people who purchased the same standard of house as them the last year, and both will have to experience the same mortgage rate environment for the next 25-30 years. But one group has a starting mortgage that is 30% less than the other.

Hi all, long time reader first time writer.

I'm a potential FHB who is grateful that I didn't buy at/near the peak. Right around when the banks were required to tighten their lending, I was verbally quoted over the phone as qualifying for a $700,000+ mortgage with a 20% deposit. However when my application went to the creditor it was reduced to ~$450,000 (too much avo toast in my purchase history). I haven't tried getting pre-approved since then because there's a lot of risk out there at the moment, but in my experience banks are very careful about loaning to FHBs even with a 20% deposit, and I really do hope modest houses get back down to $600k.

That said, with prices decreasing things are getting easier for FHB in that I'll need to borrow less to buy a home, but the high interest rates and reduced lending, inflation, and increased housing rates still make it somewhat daunting. I always factored my own stress test of anticipating interest rates would eventually get back up to pre-GFC levels with annual 0.5% rises as a conservative estimate, but this quick of a rise was unexpected for me at the time. The FOMO was strong with this one, but I'm in a better head space now. I think I'll wait this one out.

The clown bankers had me approved for over a million in debt last year. I'm a single income household with two young kids.

I had to both laugh and cry at the stupidity of it all.

Happy Medium - It sounds like you can't get an approval to buy anyway? That's the problem, cheaper house prices but harder to obtain finance to buy what you want. Not much of a win if you're still stuck on the sidelines and for the foreseeable future.

It’s why I have been imploring FHBs to wait.

by this time next year house prices are quite likely to be down another 10-15%, and it’s likely that interest rates will be starting to fall.

This is good advice, prices will come down but as soon as interest rates start to fall, that is the time to buy.

That could be happening right now, looking at the fixed rates:

https://www.interest.co.nz/charts/interest-rates/fixed-mortgage-rates

It's always tricky picking turning points, rates could easily start marching higher again - only hindsight will tell us if that was the top. I also wouldn't be surprised to see a lag of a few months between rates topping out and prices bottoming out which could easily see another 5-10% off prices.

If someone is serious about buying a house and can afford it, then it wouldn't be a bad idea to start getting things in order just in case.

Yeah wait a little bit longer for that 5%-10% decrease, then try get back into the market when everyone else has...?if you can get finance - rates will have dropped, FOMO's hot again, auctions are back in favour and you can spend $ on due diligence only to get outbid...

It’s a fair point. It’s not easy but if you keep your eyes open it shouldn’t be too hard to see when the bottom has been reached, or early signs of a tick up.

Another option is to look to buy a little earlier, perhaps just before the market bottoms out. That could be around April / May next year. It shouldn’t be a big deal if prices fall only a further 5% after buying.

what I do know is that the downside risks are far greater than the upside risks at this point.

Good advice Nifty and HM. Will be interesting to see where things are a year from now.

That wasn't my advice Happy Medium...

True, that was a separate thought. Still will be interesting where things are at a year from now. Lots of predictions and timelines in these comments, time will tell how everything unfolds.

It's just an itsy bitsy gully.

FOMO to be back in FULL FORCE.

Be quick!

At the time I tried to get approval for $500k and the bank said to try again in 3 months if I can show that I’m eating less avo toast. I can probably get pre-approved for what they’re comfortable with (ie $450k), but houses haven’t dropped that far yet.

Agreed. Its not that people don't want to buy, they simply cannot qualify under today's banking rules vs price.

If banks though prices were going to continue to lift they would be more relaxed about lending. I watched the speculative run around like crazy people try to dump their student rentals in 1997 on the back of the Asian Banking Crisis. It was panic. If China has a banking problem, and it sure looks like they are or are about to, then its all on for the exit doors. The amount of speculative debt in China with no income is too great for the IMF to absorb. In addition, I cannot see the CCP allowing the IMF to set financial policy in China to pay of the bailout as they did to the Asian Tigers in the late 90s.

Books will be written on this speculative mess in years to come, and filed under the "Finance - how not to".

it's a bit absurd to read your words. Even if the Chinese debt problem gets out of control and become a real financial crisis in China, it doesn't mean China will have a foreign debt problem, let alone get IMF involved. IMF got involved back 1997 to countries like Thailand or South Korea was because they ran out of foreign reserve and cannot fulfil international payments. But China has the world largest foreign reserve, and has had, and still has the world largest trade surplus. In short, they have more money available to pay for the foreign debt.

The problems China facing at the moment is internal debt, and a tanking economy, mostly resulted from very bad COVID policies. You could also blame a geopolitical conflicts with US. None of those has damaged the Strength of Chinese economy yet. there are still plenty of tools available to the Chinese policy makers. The biggest challenge they are facing, in my opinion, is the risk of making wrong decisions in the pressured environment.

FHB should just wait price’s are falling at record speed. In Auckland price’s are dropping $1000 a day if downturn gets worse these drops will accelerate. That 20% deposit which took 10 years to save could end up being a 40% deposit or more.

had a quick look on trademe, I still wouldn't go near property if i was a FHB. The folk buying now are still going to get burned. At ~10 x earnings for FHB, it is still irrational. No wonder they are all moving across the ditch.

Speaking to my physio yesterday. She was telling me how she bought her first house in late 2021 and how much cheaper she could buy it for today. I changed the subject pretty quickly. No shortage of uncomfortable stories out there.

Just had a look at homes.co.nz and values are still very high, maybe 50% higher than what I would call slightly reasonable. A lot of houses in our neighbourhood are valued close to $2 million and it’s not a flash neighbourhood or flash houses. I would say they should be closer to $700k.

Must be a lot of 'progressive people' gentrifying the 'hood.

So what they have been gaining from falling house prices they have been losing to higher mortgage interest rates.

Takes like that just make my head hurt.

It's absolutely true, if you are looking at affordability in-the-moment or over the next year or two.

Taking a view over a decade or two it's very clear the lower price is the important thing that still has an impact years after current rates are forgotten.

Get on the sorted.co.nz mortgage rate calculator and have a play with the rates vs the amount borrowed. Doesn't take much of a rate increase to offset any "apparent savings" made from house price falls. The real gamble is long term interest rates and zero ability to lock in something fixed for the life of the loan.

Many on here, see China's current property bubble bursting as the big event to accelerate our econmic downward spiral.

I'm not sure, I think it's Europe's energy crises this winter (our summer) that's really going to stir things up, especially if Putin is still breathing.

How about both at the same time?

Neither will

China has plenty of money in the bank to keep priming the bubble for a year or two yet and I am predicting that the energy crisis in Europe will pan out to be less impactful than forecast and has already forced many to look hard at how they meet their needs with big moves away from Putin already happening

Yip it will all be sweet as!

https://pbs.twimg.com/media/FbAn1yeXEAAvHhX?format=jpg&name=large

https://pbs.twimg.com/media/FakXiGKXEAAFdFt?format=jpg&name=medium

(Note that these are the types of charts that are looked at 100 years later with shock and horror as to how such things could unfold)

Along these lines...the last time the US 2/10 was this inverted was just prior to the dotcom bubble bursting.

https://pbs.twimg.com/media/Fac4ndYUUAY7f3k?format=jpg&name=medium

More concerned about other possible issues

Israel bombing Iran's nuclear facilities

China blockading Taiwan and the resultant reaction

and a little for the impact of the slow burn drought in the northern hemisphere

Yes good idea so use some other possible bad news to make other bad news appear more palatable (50% sarcasm)

China might do that with Taiwan

For me it was more a catastrophic risk assessment process - good and bad. Struggling to see any good impacts at the moment and to the bad can probably add Putin using nuclear weapons

I am not even sure if the EURO will make it...

Can you think of Portugal Italy Greece and Spain to start to pay non negative interest on their debts?

Looks to me that the only decision the ECB has is to choose kill the EURO slowly or fast.

It's not just the young sensing that something is very rotten in the state of 'Aotearoa'.

https://www.stuff.co.nz/national/300671648/sir-ray-avery-moving-to-aust…

✈️ ✅

I'm just waiting for the property speculators to jump on you here Brock Landers and argue that despite how bad things are, NZ is still a very attractive place to come to - but only because the value of their property investment portfolios requires the arrival of more foreign immigrants to the country while ignoring the serious financial and social issues that are appearing in our country and aren't being resolved. Any bad news that might make NZ appear less desirable place to move to must be crushed in order to protect their vested interest - even if things are getting quite bad on the streets and in our communities.

The cost of living in Auckland is not commensurate with the standard of living in Auckland, but I can see how it may still appeal as a stepping stone to those from developing countries.

There are a lot of social issues that have been left to fester. Unfortunately our ideologically warped government seems to think that dividing the population by race and gender to see who qualifies for handouts is the solution.

Not only is it the solution but it is also right on and kind to boot. To be fair their total failure to deliver on their promises means increasing handouts is simply keeping people alive now.

The problem was more they sought to protect the status quo, because "people expect the value of their primary asset to keep going up". The major parties' myopic focus on preserving housing wealth has come to a head. Social agencies pointed out that most poverty here is driven by housing, so we're pumping ready recruits for gangs and crime out the bottom of the market. In seeking to preserve our wealth transfers upwards, we're creating social issues.

Most of our recent handouts have gone to those over 65, property investor subsidies, and businesses. Less, in comparison, to those at the bottom of the heap, who - at last figures I saw - were still only supported to about 75% of the level that John Key was when he was a beneficiary.

We are not that fussed IO, we are not talking about people who will be assessing their choices against benchmarks. The 3rd world is still turning out educated people who will see NZ as paradise.

Out of interest, assuming you're a property investor given your response - do you feel a sense of social responsibility for the outcomes of your investment decisions? And you could argue 'look I only own one rental so what's the damage'....which is fine, but when its become part of the country's culture and its clearly doing harm and causing financial and social issues, do you ever say to yourself....'hey is being a property investor an ethical thing to do when its doing harm?' Or does that thought never cross your mind?

For me it would like a few years ago I thought about buying Exxon shares when they were $30 (they are now $100)....but then I thought do I really want to support a company that is profiteering by damaging the environment....I would have tripled my money by now and been tens or hundreds of thousands of dollars better off for making that decision....but at the same time, I'm happy that I haven't supported that company so don't regret my choice to not support that industry/line of investment.

Equally, one could ask, did I really need to buy that rental when by doing so that young FHB can no longer afford a house to raise a family.....and at the same time I've created even more leverage and financial risk to the economy that could in the future cause widespread economic harm?

Or am I the only ethical person who thinks like this?

Yawn how boring

Skip past it then, you aren't the only one on here.

a number of neighbourhoods in Auckland crime is a every day occurrence young adults have no hope organised crime is only way for them to find purpose, homes are overcrowded people living in cars, food banks with queues. Unless society changes and government provides affordable homes for families this will get much worse, you will start to see no go area’s for police some landlords are charging way over the top for rent and these people are struggle to feed family. The last few governments have created a situation where some people are just surviving and others have grown richer, I don’t think it will be long till shit hits the fan.

It's a loss to us but Aus does make more sense.

We are getting back on the immigration horse now, galloping into the sunset, lower wages, less services and more congestion for everyone.

Sounds like he's got the pip because local residents objected to his charity concert at Eden Park.

I'm sure he will enjoy the lower Australian tax rates.

Is this the classic 'used godzone as backdoor entry to the luckier country" play?

... usually its Helen Clark , who wanders around to Eden Park in her night dress , and demonstrates with revellers , pointing a bony finger at them : " Go home you horrible specimens ... dontcha know what time it is ... 9:17 p.m. .... F.O. ! " ...

Lock the gate at Jackson Hole...lets start afresh!

A house sold at auction last night at 45% below its peak price on homes. Exactly the same price as its mid 2019 RV. Interest rates are becoming less significant for buyers at these discounts

Indeed. Show low I terest speculation for what it is. More to come.

Link? Because "peak price on homes" and "2019 RV" are not necessarily significant. We need sales history.

If repayments are now more expensive even with lower prices (and the sleight of hand that made 30 year mortgages the norm instead of 25), that tells you property is still overvalued relative to interest rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.