It has been a tumultuous 12 months for first home buyers since house prices peaked in November last year, with soaring interest rates, plunging property prices, a cooling housing market and economic uncertainties at every turn.

So how have aspiring first home buyers fared over the 12 months to November, is it easier or more difficult for them to get into a home of their own now than it was at last year's market peak?

According to interest.co.nz's Home Loan Affordability Report, the two biggest drivers of changes in affordability are mortgage interest rates and house prices, and to a lesser extent household incomes.

In November last year, mortgage rates were already rising and the average of the two year fixed rates charged by the major banks had increased from its record low of 2.52% in May 2021, to 4.08% in November.

By November this year that had increased to 6.09%.

The low interest rate environment of 2020/21 had seen spectacular house price increases with the Real Estate Institute of New Zealand's national lower quartile dwelling price peaking at $670,000 in November last year.

But it was downhill from there. And by November this year the national lower quartile price had shed $69,000 and was sitting at $601,000.

The lower quartile is the price point at which 75% of sales are above and 25% are below each month, representing the bottom end of the market where first home buyers are likely to be most active.

Some regions, most notably Auckland and Wellington had even bigger falls in lower quartile prices over that period.

In Auckland it dropped from $966,000 in November last year to $829,000 in November this year. In Wellington it dropped from $775,000 to $655,101.

There were three regions - Taranaki, Canterbury and Southland - where lower quartile prices were higher in November this year than November last year. But for everyone else, it was cheaper to buy a lower quartile-priced home in November this year than it was a year ago. And in places like Auckland and Wellington it was considerably cheaper.

The immediate implication for first home buyers is they would need a smaller deposit and would need to borrow less to buy a home at the lower quartile price.

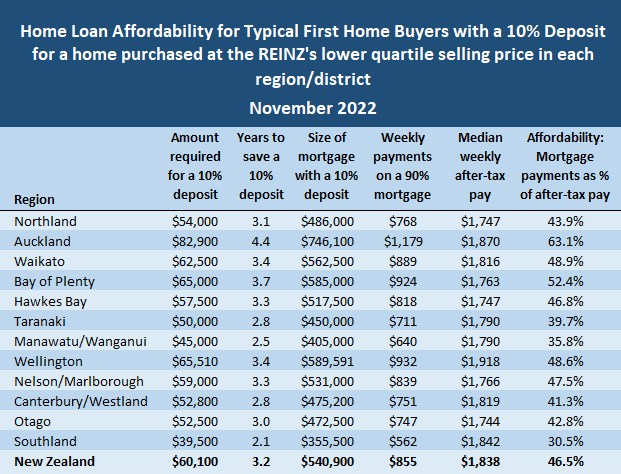

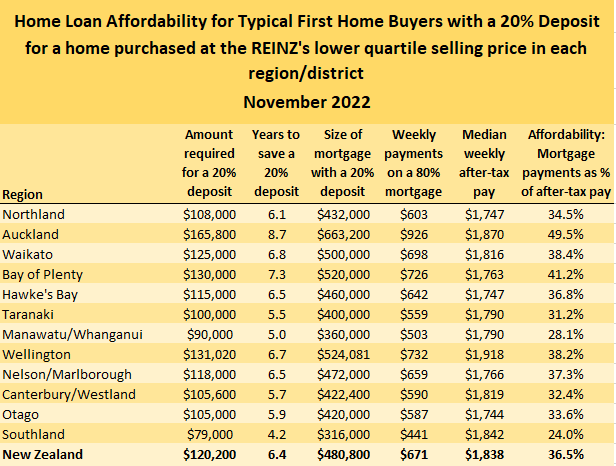

With the national lower quartile price dropping from $670,000 to $601,000 over the year to November, the amount needed for a 10% deposit dropped from $67,000 to $60,100. A 20% deposit dropped from $134,000 to $120,200.

The Home Loan Affordability Report also tracks how long it would take a couple earning median rates of pay for 25-29 year olds, to save a deposit if they put aside 20% of their after-tax pay each week.

That dropped from 3.7 years to 3.2 years for a 10% deposit, and from 7.3 years to 6.4 years for a 20% deposit.

And of course the size of the mortgage they would be taking on was also reduced, dropping from $603,000 for a home purchased at the national lower quartile price with a 10% deposit in November last year, to $540,900 in November this year.

If the home buyer had a 20% deposit the size of the mortgage would have reduced from $536,000 to $480,800.

So there were three ways in which aspiring first home buyers looking to buy a lower quartile-priced home were better off in November this year than they were in November last year; they would need a smaller deposit, it would take less time to save a deposit and they would need a smaller mortgage.

But of course not everything has gone their way, with rising mortgage rates spoiling the party.

Although first home buyers would need to borrow less to purchase a home at the national lower quartile price in November this year than they would if they had purchased in November last year, rising interest rates mean their mortgage payments would have gone up.

If they had a 10% deposit, the amount they would need to set aside each week for mortgage payments would have increased from $770 a week in November last year to $855 in November this year, up an extra $85 a week.

If they had a 20% deposit those amounts would have increased from $596 a week to $671 a week, up an extra $75 a week.

The pain of finding that extra money each week would have been eased slightly by the fact that incomes have been rising at a reasonable clip this year.

The Home Loan Affordability Report estimates the combined, after-tax pay of couples aged 25-29, at the median rate of pay if both were working full time, would have increased from $1801 a week in November last year to $1838 in November this year, giving them an extra $37 a week.

Mortgage payments are considered unaffordable if they eat up more than 40% of after-tax household income. In the examples above, the mortgage payments for a first home buyer with a 10% deposit would have eaten up 43% of after-tax pay in November last year. That would've risen to 47% in November this year, putting it squarely into unaffordable territory for couples on average wages.

If they had a 20% deposit, the amount of their household income they would need to set aside for mortgage payments would have increased from 33% to 37%.

While that's still considered affordable, interest rates wouldn't need to rise much further to push mortgage payments into unaffordable territory.

So overall, while there has been some good news for first home buyers since the housing market has come back from its peak, the financial obstacles they face remain so high that most will still struggle to get into a home of their own and in places like Auckland, Waikato, Bay of Plenty and Wellington. Home ownership is probably still out of reach for those on average wages.

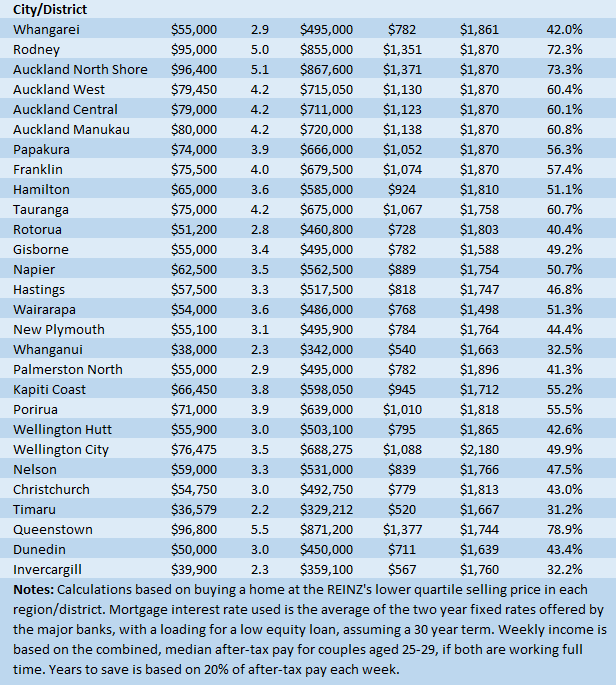

The tables below give the main home loan affordability measures with either a 10% or 20% deposit, in all main urban districts throughout the country.

The comment stream on this article is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

59 Comments

Prices may look cheaper Today Compared To Yesterday.

But Prices next year will look much cheaper than this year.

The wise will just sit back, open a very big bag of popcorn and wait wait wait !

So easy to save so much. Do Nothing.

Lucky that we had the Prophet warning us last year of what was to come.

By repeatedly spamming these forums with claims of 30% house price drops, He will have saved some first home buyers from otherwise being in a negative equity position now.

We should petition the government to erect a statue in his honour.

John Bolton from Squirrel Mortgages has gone very quiet I have been told. People are telling me they cannot contact him. Not sure Why ?

"A slower economy will also take the pressure off interest rates. For a long while now we’ve been saying peak mortgage rates will be between 5.50% and 6.00%, and I’ve yet to see anything to change my mind on that."

https://www.squirrel.co.nz/blogs/housing-market/down-but-not-out-making…

Oh Dear.

I have now realised what the raison d’être for people like him and TA is - they are like opiates for the ‘property people’.

I overheard a conversation the other day between some consultants and a troubled developer, one of the consultants was saying ‘Mate, I’ll send you Tony Alexander’s latest report, he sees things picking up soon’. And then the conversation started to turn more positive….

If you want to remain positive about property, follow williams corps directors on instagram.

I think an induced coma for 18-24months might be the best alternative

Around the same time he was trying to get people to invest in squirrel's essentially subprime mortgages. If I were an investor there I'd be feeling pretty nervous right now

Father Fitzgerald - Ferocious Fighter For Financial Freedoms Of Families.

May he RIP.

I don't know what happened to this Great Man. But The Prophet would be Proud !

A True Fighter of the Faith to the very End.

A certain Hall Monitor will be interviewed First. I don,t think he will be so Forthcoming this time.

You're intending to question DC and GN. Good luck to you.

No they will not be any cheaper in the long run, interest rates are offsetting any price drops. You will be buying on the hope that interest rates fall again and you bought the dip. As for the numbers in the tables above, good luck finding a house you want to live in for $585K in Tauranga.

Interest rates will rise and fall over the course of a loan - you're always better off with a smaller debt.

100% this ^^

After the initial period of higher interest, you should end up on roughly the same rates as someone who bought at the peak of the market on a lower interest rates (many of whom will end up refixing to higher rates in the next 6-12 months anyway, but you're carrying a lower principal.

Trick comment. For most people of sound mind, no amount of money could convince them to want to live in Tauranga.

Genuinely feel a bit sorry for you Brock, having to go bush in Australia to find a house you can afford and all that.

Oh there's no need for any of that faux sympathy Carlos. Buying houses in New Zealand is currently a bit like buying red onions at Countdown. You can afford to pay for them, but only idiots would pay nosebleed prices for glorified turds.

Besides... living in the sunshine in a first world country sounds like a much better life for the time being.

I just like them in my sammich, alright :(

Once the panic selling sets in next year, prices will overshoot on the downside so will be cheaper, even accounting for higher mortgage rates.

Not long now - I think we have finally moved past the last 6 months of Denial. By the end of January, I think we can expect everyone to have moved into full-blown Disbelief. Then I'm guessing that July / Aug should have seen Panic well and truly entrenched (floating rates nearing 10%). Too early to tell when we will enter, what will be a significant, Bust period.

Housing bubble cycle:

1. Rising prices

2. FOMO

3. Euphoria

4. Denial

5. Disbelief

6. Panic

7. Bust

Yes, let the reality set in when the smug turn up to BBQ's over Christmas with nothing to gloat about property wise this year.

- "How's that reno going Darren? Has it sold yet?"

- "......nah well you know I've....uhhhh...well we had a couple of offers but they were way too low....so about the cricket aye?"

- "What's it listed for?"

- "Ahh well we started at BEO $820k in October, dropped it to $750k beginning of December"

- "Didn't you pay $720k for it and leverage the deposit from your home? How much was the new kitchen, bathroom and deck?"

- "Did you hear Williamson has stepped down as test captain?"

Yeh it's much cheaper to buy something when it is over priced rather than on discount. Tauranga is just a big carpark now anyways, just sit in traffic watching the crack head behind you sucking on a pipe twitching around.

Right, good luck finding anything worth living in at lower-decile numbers.

Yep something down here you would actually want to live in would start in the $700's. Factor in how much money a week that would cost you would make it a real struggle. You still want about a million for what I would call a "Nice" house in Tauranga.

Tauranga house price’s are falling fast what was a million last November will be 650k in a years time. I had friends living there in March they left for Aussie more money better prospects for children

✈️✅

The prices are just ridiculous. This is not a sane market. The greed of some is cancer for the society and we are creating a slow death of the way of kiwi life.

This cancer of greed to make more and more from a non moveable asset will kill what ever is left of kiwis way of living. Mark my words, the generation of future.

Sit back and grab the popcorn. Panic will ensue, recession will bite hard and the govt will fail to intervne, or if they're smart, won't do aything and let the market find it's natural equilibrium. We will see prices become more reasonable and some will struggle hard to make ends meet. Property specu-vestors will start shedding houses at around 8% upwards to keep hold of the rest of their portfolio as they will clearly not have read the prophets scrolls, FHB's will be happy to be able to buy a house and move on with life, hell maybe even afford to have kids as well (insane thought i know). We will all do what we can to truck on and squeze the good times where we can, and before you know it in a couple of years time, the egos will start inflating again in the property world, acting as if nothing ever happened and to 'buy now before prices keep rising'. This is when they'll get the most scrutiny, more than when they were desperately trying to keep positive in the last 6months amongst all the telltale signs of an imminent collapse.

A million bucks in debt, is still a million bucks in debt. I had this conversation with a few people during the halcyon daze - money is cheap faze

Sure maybe 500k costs you more right now in interest, its still 500k less in principal, no matter how you spin it.

Yes, and every extra one dollar you contribute at $500k has the same effect as contributing an extra two dollars at $1m.

Entering the market during a brief record low interest period is lose lose. A seriously unfortunate turn of events for FHB from about 2016 onward. Many will be fine, some won’t.

The tragedy for First Home Buyers in our distorted Property Sector isn't Price - it's Time.

FHBers are at that stage in life where they are supposed to be creating a family and family life, independent of their parents. And that has been denied them by the abomination we cheerily call The Property Market.

How many young women do we all know who are well into their 30's, who are still aspiring FHBers, who have seen a decade or more of prime family establishment time denied to them because of the uncertainty of home ownership - let alone the sheer cost of being able to do it and having anything left over to support a family life with.

Yes, times change. But what we have done to our next generation hasn't been for the better, and we are still a long way off from correcting that mistake.

Sad thing is I know of many young aspiring FHB couples, some with a child, who are renting a whole house to themselves. These people are middle class income earners that would normally be in their own homes by now, but are consigned to renting.

If you put the rental property title in their name, it would be ZERO net change to rental stock. These people don't need Landlords to provide them a house, they need amateur "mom and pop" investors to stop bidding up the market for entry level homes using leveraged equity, interest only lending and tax advantages.

Precisely.

And your example is of a lucky couple. There are those less lucky who've given up on the possibility of home ownership, and they are trying to establish a family in a shared accommodation; trying to raise a baby/children, in the confines of shared facilities. And these aren't 'poor' people.

The rent for our family home costs literally the ENTIRE after tax wage of an average earner.

Rents are ridiculously high. They are driving people into poverty. I can't even imagine how other families are coping.

This is why we didn’t return to NZ after my ex pat placement. Once you get a walk in wardrobe and an ensuite, it’s impossible to go back to sharing a bathroom with the kids.

We rent a modernish 4bed home 20km from Melbourne city centre for 600pw. All my opportunities were shaping up in Auckland but we decided to start again here.

zero regrets.

edit: we’re now in a position to buy after liquidating our NZ property. Waiting on the right place at the right price.

Has Fitzgerald been Deleted ?

His comment was as was mine that commented on the comment.that was deleted. Its like China... but we all know what he said..... he maybe deleted, i suspect on stand down

they need amateur "mom and pop" investors to stop bidding up the market for entry level homes using leveraged equity, interest only lending and tax advantages.

Sounds like you are speaking of a fair an equitable system that allows hard working families the ability to own their own home for a secure future in this country and at the same time drive speculative parasites out of the property game and into some of the many other investment options available but do however require hard work and financial intelligence.

Sounds like a good election promise for someone game enough?

Maybe NZDan but many FHB dont like the suburbs where ma and pa own, think Manurewa.

Just appreciate that labour have done something about landlords with the tax rules on interest/bright line. Mr Luxon and Mr Seymour will undo this and attempt to ignite the fire yet again.

I'm not a labour fan, never have been. But National make it hard.

What worries me is Luxon's silence on foreign buyer ban in NZ. Collins and Bridges were both against the ban but this guy rather not bring it up than face backlash from voters.

I also disagree with National's argument that housing is only a supply side problem. Why wouldn't they want us to believe that? It justifies their intention to unleash speculative housing demand to its fullest.

Just appreciate that labour have done something about landlords with the tax rules on interest/bright line. Mr Luxon and Mr Seymour will undo this and attempt to ignite the fire yet again.

I'm not a labour fan, never have been. But National make it hard.

Definitely appreciate what Labour has done in particular deductibility rules. IRD makes a distinction in their Glossary that someone who rents a property out but is not registered for GST is an Individual. Yes, the income is received from "business" but that's describing the activity rather than defining the entity. E.g. my salary is an income from business, same with shares, but I can't deduct my mortgage costs from my income because I am an individual.

I have never voted Labour, I voted National in 08 and then ACT ever since, but minor temptation to vote Labour as a protest.

No mention of Rents under the Types of Business Income page @ IRD. https://www.ird.govt.nz/income-tax/income-tax-for-businesses-and-organi…

https://www.ird.govt.nz/glossary-source

Individual

Customers not registered for GST or PAYE and not belonging to large enterprises (LE) or non-profit organisations (NPO).

Notes

- This includes individual customers receiving income from business (eg, rental property, shares) but not registered for GST or PAYE.

- Where there are overlaps between LE, NPO, SME and individuals, entities are allocated to the group according to the following order of priority. The priorities are:

- large enterprises (LE)

- non-profit organisations (NPO)

- small and medium enterprises (SME)

- individuals.

This is 100% it. There is a lot of anger in my cohort. Those that are 5-10 years younger, it’s palpable.

It would be cool to see a long term chart of the % of take home pay required to pay the mortgage in NZ. Would strip away a lot of noise about prices / wages / costs etc etc etc

Thinking back to when we first bought a house in Auckland. Can’t remember first well, but I can remember our second house. It cost $130,000, we would have had about $30,000 deposit - mostly from proceeds of our first house. We were earning between $15,000 and $20,000 each ( both young professionals). Of the $100,000 mortgage, $80,000 was at 18% the remaining $20,000 was a second mortgage at 22%.

We willingly took this on as there was a housing bubble at the time and we felt we had to buy to avoid higher prices later. But needless to say were very cash strapped to the point of never going out, not buying clothing and living to a very strict weekly budget. The 1987 crash hit Auckland and shortly after we sold and moved to the provinces where living was more reasonable …… although we did experience troubles there with the long recession of the 1990s.

Oh yeah and ……….. “we used to live in paper bag in middle o’ road” ……. “ tell the kids today and they just won’t believe ya, won’t believe ya”.

Looking at the second chart with 20% deposit - doesn't seem overly unaffordable to me? In Wellington at $732 per week you would likely be paying more in rent for a 2 or 3 beddy

Each month price’s are falling why buy now when over the next year house prices will probably tumble another 20%.

A few FHBs and OOs in my circle bought in the last few weeks. Believe or not, people still buy the crap that it doesn't matter what you pay for a house today if you aren't planning to sell in the next 5-10 years.

I probably should make some new friends!

A lot of FHBs are couples, there is a lot of emotion in the decision.

There will be buyers all the way down. But the shear number of sellers will swamp them.

Agreed, the emotions and just the way people react quickly to things when they like Something.

Everyone acts like kids in a toyshop and impulse buying just happens. One needs to realize, house is a big investment and its a lot and lot of money.

Paying debt for 30-35 years is no joke. Half life is gone paying the debt and rest of the half your are dependent on others for your everything. Life done. Did you enjoy it the way its meant to be enjoyed in the question.

The Real Estate agents pull all the strings, its not a house its a HOME. its your Future together.... its 3 houses away from the school... its .........

In 1-2 years time at the flat bottom, the house will be more affordable and you will have the extra money to take your kids on international holiday EACH YEAR.

I think the agents love it even more if one of the couple is pregnant.

My wife and I saw a place we loved a month ago, RE agent wanted offers within 3 days. I told them to contact me if it didn't sell, the hell I'd be rushed into anything given the downward trajectory of the market, told the wife there will always be another house and likely at a cheaper price next year. Good to go through the rollercoaster of emotions, reflect and harness that lesson for the next time somewhere comes up we really like. You are right, there's a lot of emotions, and I sincerely feel for those who had 0 time to process these and think rationally last year who jumped in and bought due to the heat of the market, that would be insane for such a life altering decision. It takes time and effort to collate all the info, and think rationally through all the hype and BS you get from RE agents etc. Answer? Lowball everything 20% under RV or lower, go fishing and see what comes back, or simply wait if you can. And it may be early, but Merry Christmas everybody!!!

I agree Nguturoa, I was shocked at buyers rushing into multibids with no due diligence and not much care for the value they were receiving for the price they paid. I felt like they were fairly inexperienced with property and had just jumped in because they felt regardless of what they bought they couldn’t lose It was like everyone had gone mad in the previous two years.

No wonder dating apps are so popular these days; you can't afford to buy a house in this country, or almost even rent one, on a single income anymore.

This idea that Tinder users are just looking for a quick root is a misconception. They're looking for long-term commitment.

Not having much luck? Lose the duckface selfie profile pics (✌️😉), and start posting degrees!

It's Friday afternoon, have you started Happy Hour early?

What matters is convincing the boomers to accept the L of selling their house for only 2-3x rather than 10x.

This bubble has seriously harmed the family formation of an entire generation and is having huge downstream effects in births, simply to prop up the gerontocracy. Boomers will be the most hated generation for a long time for robbing the future to ensure their luxuries never run dry.

Runaway house prices have attracted more capital being funnelled into unproductive assets and forced young Kiwi workers to leave for greener pastures, which in turn has put a dampener on economic productivity in NZ.

So, boomers retiring in droves and not having enough workers either paying into the system to fund their retirement or looking after them have themselves to blame to an extent.

As much as we can bash the boomers, they were a product of their environment. Back in the days NZ had more resources, forests to rip down, bigger fisheries, cleaner waterways etc so it was cheaper to build housing, there was ample land to develop close to centres etc. They didn;t get the opportunities technology has afforded the younger generations, they had resources and affordable housing at ther disposal, so of course they took advantage of that. That was their primary way to get the golden ticket to cushy retirement. Given the same circumstances im sure all of us would as well. The downside of course is where we are now as there's a bbig difference between owning a second house as an investment to owning 10-30homes for investment and doing this as a living. On the flipside many of them are popping off early with health issues in their 50's and 60's. Now we are stuck with less resources available, less land near centres, and specu-vestors with more than they could ever need.

Boomers will eventually have to accept whatever price the market demands, it will find it's own equilibrium as time goes on. We may well see price drops for the next 18months or more to affordable levels, and the boomers will end up competing for rest home beds as they age and there aren;t enough available. All I know for sure is there's goin to be one hell of a lot of good deals on campervans in around 10-15years time

Meanwhile, Realies are still in the denial phase. If they don't put a sale price on, how do they expect to garner any interest. Most financial markets oF which housing haS become an also-ran, mark to market in real time. No excuses.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.