The number of first home buyers getting into a home of their own appears to be stabilising after an extended period of decline.

The latest mortgage lending figures from the Reserve Bank show 1883 mortgages were approved for first home buyers in April, up 6.6% compared to April last year.

That was the second month in a row that the number of mortgages approved to first home buyers has been higher than it was in the same month of the previous year, bringing an end to a 20 month run in which approvals to first home buyers were lower than they were a year earlier.

That decline in mortgage approvals for first home buyers should not be a surprise because the housing market has been in a slump, which has seen the number of residential sales recorded by the Real Estate Institute of New Zealand (REINZ) decline by 43% between April 2021 and April 2023.

However although first home buyer mortgage approvals also declined over that period, they did so at a lower rate than the overall market, down by 35% in April 2023 compared to April 2021.

That suggests they are gaining an increasing share of the housing market, with sales to other types of buyers such as investors and owner-occupiers, dropping away more strongly.

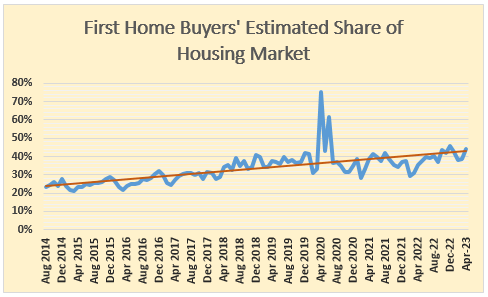

The first graph below shows the trend in monthly mortgage approvals to first home buyers expressed as a percentage of total housing sales.

The blip in the middle was during the period of strict pandemic lockdowns when the numbers went a bit haywire, but the overall trend for first home buyers is clear, rising steadily from a market share of less than a quarter in 2014 to 44% in April this year.

The other sign of a possible recovery in first home buyer activity is an increase in the estimated prices they are paying for properties.

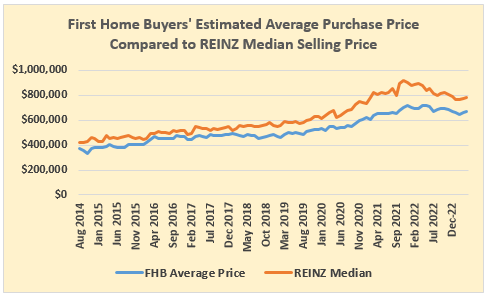

Interest.co.nz estimates the average price paid by first home buyers peaked at $717,724 in April last year, then declined steadily to $645,925 in February 2023, before rising again to $661,326 in March and $671,505 in April.

The second graph below shows the relationship between the REINZ's monthly median selling price and the estimated average price paid by first home buyers.

Overall, the figures show while first home buyers have been affected by factors such as rising interest rates and tougher lending conditions, which have impacted the entire market, they have proved to be more resilient than other types of buyers.

The latest moves by the Reserve Bank to slightly ease loan-to-value ratio restrictions and signal an end to increases in the Official Cash Rate, should also help a few more of them into a home of their own, all other things being equal.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

58 Comments

Sometimes I wonder if the changing demographic of the FHB, ie, likely to be older and further into their career, makes some of these historical comparisons misleading.

Misleading!??... not as much as the REINZ , and the so callled " INDEPENDENT " body that governs their behavior

https://www.nzherald.co.nz/nz/realtor-allegedly-tried-to-convince-buyer…

Name suppression for a multiple offender.🙄

Time for the REINZ and thier governing body to be CC audited.

As a FHB, I ain't buying a home at current prices. Call me when they drop ~20-30% more and I can afford them.

The return of FHB to the market to catch the falling knife of property prices, as well as the active promotion that young people should buy houses now is vile. These people will be drained through usurious prices for these properties into immense debt slavery.

Attempts by the State and the private Economy Planners to bailout all these insolvent speculators, home builders and co are morally repugnant. Markets should be illiquid when the price does not reflect the underlying value, and only return to liquidity when the price is reasonable.

this comment is a vibe.

-SMG.

Best post today. Although I don't like your chances of another 30% drop. The reserve Bank keep talking about sustainable house prices from an investing/return perspective. The powers don't care about affordability. It's all about investment and return. What we need is a cultural shift where people disincentivised to invest in houses for profit purposes. This has to come from the government to save people like you. It's a giant mess.

The reserve Bank keep talking about sustainable house prices from an investing/return perspective.

Jawboning from central bankers, govt, media, water cooler exchanges is important in the decision making of the sheeple.

The RBNZ said (in 2016) they're not there to bail out homeowners. Then bailed out homeowners

To be fair during Covid they bailed out everyone

HW2, here you go. In Dec 2017 (not 2016), the RBNZ did warn: 'It's not our job to protect you from the housing market'

https://www.stuff.co.nz/business/99408539/reserve-bank-warns-its-not-ou…

Their job is wider financial stability. Right now, they're using naive FHB's in order to achieve this. Can you explain how RBNZ actions either bails out or protects FHB's?

HW2, here's a bit of de-ja-vu. On the subject of LVR relaxation, in Dec 2017 they also said this "When the Reserve Bank announced it was relaxing mortgage lending restrictions on Wednesday, it was not a message that buying a house was becoming less risky"

No-one should get their hopes up that a massive broad based and sustainable recovery is imminent - not even you :)

"What we need is a cultural shift where people disincentivised to invest in houses for profit purposes. "

It requires a change in government priorities and policy.

Look at Singapore government policy on housing, where the priority is for owner occupier resident buyers and lower priority for non owner occupier buyers.

Some people will always game the system and the rules in place.

If the residents of NZ want to encourage more residential housing ownership by residential owner occupiers then it comes down to government priorities and government policies.

Singapore focuses on encouraging resident owner occupiers and less on owners of multiple houses, non resident owners with their tax policies.

1) Property taxes (which we call rates)

i) note that they differentiate between owner occupied and non owner occupied,

ii) and they are on progressive rates - the higher the inputed rent, the higher the rate to determine property taxes (which we call them rates in NZ)

https://www.gov.sg/article/property-tax-on-residential-property

https://www.iras.gov.sg/taxes/property-tax/property-owners/property-tax-rates

Imagine bringing in a progressive rate system in NZ to calculate rates.

2) Stamp duty is differentiated between

1) citizens vs residents vs non resident buyers

2) first, or any property beyond their first property

https://www.propertyguru.com.sg/mortgage/calculators/stamp-duty

https://twitter.com/GRomePow/status/1643083095376285698?s=20

I totally agree, is there any political party that has the courage to do this? Words cannot begin to express how deeply toxic I see our current housing market. The way we are treating each other is simply sub-human, I’m far from a financial expert, I still am not clear where this mess started, can it be turned around, or have we gone too far down a particularly nasty path?

#renterforlife

The addition of the word 'usurious' to this comment is outstanding. For those who don't know what it means - I'll save you Googlising on the Interwebs. 'Extortionate' - that's the similar meaning. When you also throw in the words, 'vile', 'repugnant' and 'slavery' - what you have here my dear Boomer friends, is an absolute dressing down. Von my squire - you win www.interest.co.nz today.

As you were.

- Chubbs.

The big question is... How many FHBs are immigrants!?

FHBs are 23% of buyers.

Immigrants are what?

“As a FHB” then proceeds to dream of 20-30% drops. So you’re not actually a “buyer”…

Waiting on the sidelines as prices continue to fall. Why move now and take a huge L as the prices continue to fall?

This is the bottom or very close to it. Many have failed trying to time the bottom to buy.

When volume of sales increases for three consecutive months, I'll believe that.

I wish house prices can be lower, but it won't.

How much do you think it would cost to build a new house nowadays? Building costs is not easy to drop, unless builders willing to build at their loss.

On top of building cost, you will need to add on the land costs. getting the land ready also costs a lot.

My little house in Petone is a dated small 3 bedroom house, when I did a estimation on the rebuild costs, which came as 538k. and land costs in that area is about 500k to 700k. There is a new home on my street is selling 1.3mil. It's not cheap, but definitely not unreasonable as the builder won't have much profits selling at 1.3 mil.

for many people, Houses are always expensive to buy, sadly.

""There are early signs that first home buyer activity could be starting to stabilise"" ........so here are the figures of an even beginning to ""STABILISE"" Auckland Market .....

Say an average Auckland property $1,000,000 NZD .....(this amount is why this country is broke)

So you have "saved", coerced family, worked for at least 10 years to FINALLY get your 20% or $200,000 together .....while paying overpriced rents, in some cases subsidised by the taxpayer to some greedy landlord, who won't spend a cent on that unhealthy mould in the bathroom ceiling, because he claims you don't open the windows ?

Then the mortgage ...a truly "manageable "$800,000 @ at a "special" rate of 6.65% p.a over 30 years ..... only valid for 1 year, so what happens after that ???

I'll tell you what happens after that - you have to come up with $1,183 per week for the mortgage ......a very average take home pay.

But wait there's more !!! ......we have to eat, pay insurances, run the car, stuff for the kids school, dental bills, Christmas money, maybe a 10 day camping holiday etc etc etc

Right !! ....one income just won't do, have to increase the work hours for the partner/wife/de facto etc

Who's going to look after the kids !! ?? ....they can look after themselves after school, why it's only from 3.15pm to 6.30pm till when the first of us get home, and we just can't afford childcare !

Oooooops ....our 12 yo little Johnny has a friend Stan whose a great kid, but has a nefarious uncle who runs a meth lab about 1km away ....AND THE REST IS HISTORY

Chatting to an acquaintance at a bbq in the weekend, they have just bought their first investment property. He carefully explained to me that the way to get rich was to wait until it shoots up in value enough to leverage into another rental and so on. I was stunned into silence and thought I must have traveled back in time. They are nice people, but it looks like we need a bigger crash to knock this nonsense out once and for all.

Real estate is a poor investment anyway. Doubles every 10 years (fine print 1: only in NZ, fine print 2: only up to 2021)? That's a meagre 7% a year. Even the BTC that many announced dead around a 6 months ago performed +70% since then.

Fine print 3: Doubles every 10 years on the basis that the cost of credit reduces over the same time span i.e. interest rates.

They might double every 10 years going forward, but will need a new driver i.e. wage growth. But even a doubling in nominal price is good enough to inflate away the burden of debt.

Counterpoint to this is that you (hopefully) don’t buy leveraged btc. Real estate is a fine investment imo, just not at the moment.

"Even the BTC that many announced dead around a 6 months ago performed +70% since then"

FYI, throughout history, many people have been willing to speculate on some unusual items. Here are some other items:

1) tulips

2) beanie babies

3) artwork

Chatting to an acquaintance at a bbq in the weekend,

As one does. You can also get an idea of people's liquidity by looking at the meats, seafood, and wines they bring.

Supposedly picking the bottom is impossible for mere mortals , but for a psychologically driven bubble , the bottom will be obvious - coming to a BBQ near you …

Let's put this debate to bed for ever

What drives a housing recession

High OCR✔️

High mortgage rates✔️

Immigration outwards🤔

High supply✔️

Low demand ✔️

High COL ✔️

Banks ability to lend cheaply✔️

Low rental yield✔️

Market confidence in economy✔️.

Q: how much does immigration inwards drive up prices?

Feel free to add

I had exactly the same experience this week, I don't normally go to barbecues for this reason. If someone can't afford to come out for a really expensive dinner paid for in net cash, they shouldn't be risking their shirts on shit deals.

Bless you! Best comments I’ve ever read. Society can’t cope with much more of this getting rich of the backs of others, so sadly a bigger crash must be on its way.

@ Beanie ..... deluded .

Good to see Chris Bishop acknowledging that an LVR of 4 is about right for the average New Zealander- FHBer included I assume. So at $670k median purchase price, and with a 10% ~$65k in their Kiwisaver accounts etc, let's hope the average FHBer has a household income of $150k.

Median incomes are $30 per hour, annual household income x 4 is 480k ahem ahem.

Chris and Chris will leave taxpayers with more in their pockets too

HW2 ....are you really serious ? ....where are those households with 4 people earning $120 each, under the same roof ?

This is why we are turning into a 3rd world country mate ....have you ever travelled outside NZ ?

You've miscalculated Crazy

But to avoid confusion this is the breakdown. My numbers were based on a couple and each earning the median wage.

An affordable 4 times multiple home as per chris bishop is 480k

I time-travelled once, from the 90s to the year 2000 just to make sure the world hadn't ended. Does that count.

HW2 .....you math whizz ! :) when do your talents ever end .....I was talking about Auckland ...you wouldn't get a converted garage with your figures in Auckland !

You are obviously very "local centric" in your area and yes, this principle applies to every market, anywhere - so why don't you at least state the area ?

Your comments tell me you haven't travelled overseas - that is a bummer, as you could see with what you could get with exactly the same NZ dollars. I think you would very much change your perception, as to what is "value for money".

Remember, I still have Auckland never falling below a median of $900,000 for this year in this crazy market ....everybody who has a mortgage or pays rent will just have to dig a little deeper into their pockets, so much for spending anywhere else - great for banks and landlords, as we descend into the 3rd world - truly marvellous :)

"an LVR of 4"

Just checking for typo here. Do you mean debt to income ratio "DTI" of 4?

Could be either or both!

Chris Bishop, on TVNZ’s Q+A, denied the policy was about winning votes back from the Act Party and said National was serious about solving the housing crisis. He said house prices should be roughly 4 times the median household income—the current national average is more than 7 times

And as for any suggestion "We'll make rising incomes achieve that" is naive. Do you know why we have a ratio of 7 at the moment and not 4? Because Income never keeps up with prices in a Debt soaked/reliant economy. Which is why his 'unacceptable alternative' of a property price Crash is probably all we are left with to resolve the issue.

And as for any suggestion "We'll make rising incomes achieve that" is naive. Do you know why we have a ratio of 7 at the moment and not 4? Because Income never keeps up with prices in a Debt soaked/reliant economy

These people are charlatans. If you track income growth via CPI and house price growth over the past 30 years, income growth has the lowest trajectory. In fact, the theory is that bubble economies is promoted by the ruling elite to compensate for the lack of income growth of the boomers. It also has encouraged them to spend because the house is doing the savings.

National are serious about solving the housing crisis... all you have to do is look back at what John Key did. 7 property Luxon cares too, flip flopping on housing density is just the start.

Honestly Labour & National are the same - they don't give a sh** about making housing more affordable. Please don't be so naive if you think this is the case...

Something to ponder:

Is every politician's vested self serving interest, getting elected into office?

What will these politicians say to get elected into office?

Understand the game that politician's play.

"LVR is 4"

Can you expand the acronym LVR please. I'm not sure if my understanding is correct.

In a lending context, LVR is commonly referred to as the loan to value ratio. (I.e the mortgage amount divided by the market value of the residential dwelling). This ratio is a percentage.

THUMBS UP

Complete this: It won't happen overnight...

It won’t happen overnight, but inflation will continue to climb…

Clown.

Are you porky pig or daffy duck

Thats all folks

Banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%. Thus around 60% of NZ bank lending is dedicated to residential property mortgages owed by one third of already wealthy households

Top tier comment. Post some Michael Hudson too.

How about some Don Brash?

DON BRASH - HOUSE PRICES ARE STILL OUTRAGEOUS: BLAME YOUR LOCAL COUNCIL AND THE GREENS

HAMMER ON NAIL DR BRASH

You put it so well but essentially what I've been saying

Getting into a life of slavery to the bank and their handlers.

Nothing to do with the 217,000 newly minted permanent residents courtesy of Jacinda Ardern's kindness who are now fully fledged legal First Home Buyers, right?

Does the definition of a FHB in these stats mean:

a) the first house someone has bought?

b) the first house someone has bought in NZ?

Or someone that has been renting, has owned houses before, but hasn't owned one for a while? If I am someone that fits that description, and I have $3M in cash in the bank, and buy a muti million dollar house with a 20% mortgage, am I a FHB? You can definitely see how those figures would get badly skewed.

Probably the best place to look for a definition in this context would be the criteria around any sort of government incentive scheme.

e.g. https://kaingaora.govt.nz/home-ownership/first-home-grant/check-you-are…

Under this scheme, for example, previous property owners are only eligible if they do "not have realisable assets worth more than 20% of the house price cap for existing properties for the area you are buying in" so your scenario above probably isn't in the FHB stats.

I mean the definition that Greg is using.

Big difference between a young person/family trying to get their first house and a someone coming in from abroad having sold their house and buying in NZ. It would be good to understand which definition is being used.

I can see house prices continuing to slide down for a few years yet.

Good thing too.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.