The housing market perked up a bit last month, sort of.

The Real Estate Institute of New Zealand (REINZ) recorded 5752 residential sales nationally in May, up 30% compared to April.

The increase in sales was not much of a surprise because sales usually shoot up in May compared to April but they were still down slightly (-0.4%) compared to May last year.

However April's sales were particularly low and were the lowest for the month of April in 31 years (excluding the 2020 lockdown).

May's sales were only the lowest for the month of May in 12 years (excluding the 2020 lockdown), so that was an improvement of sorts.

May's sales also remain down by almost a quarter (-23%) compared to pre-pandemic levels in May 2019, suggesting the housing market remains in a significant slump at the start of winter.

Prices also continued to decline in May, with the REINZ National House Price Index (HPI) declining in all regions of the country last month except for Manawatu/Whanganui where it was up 1.5%.

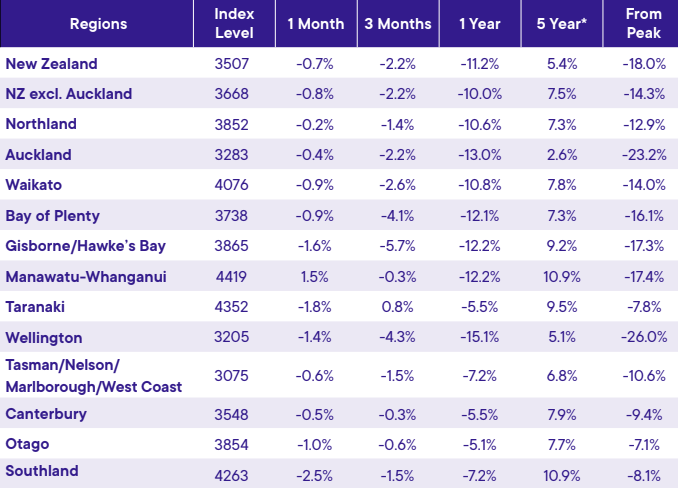

The HPI declined nationally by 0.7% in May compared to April and has now declined by 11.2% compared to May last year and is down 18.0% from its post-pandemic peak (the table below shows the full regional figures), while the REINZ's national median price was unchanged between April and May at $780,000.

The fact that the HPI, which is adjusted to allow for changes in the mix of properties sold each month, was down, while the median price was unchanged, suggests that prices in the top half of the market may be holding up slightly better than the bottom half, although the difference is likely to be marginal.

Properties are also taking longer to sell, with the national median number of days required to achieve a sale increasing to 49 in May, up six days compared to May last year.

REINZ chief executive Jen Baird said there were glimpses of positivity in the market, especially in the regions, following the Reserve Bank's announcement of a slight easing of loan-to-valuation restrictions on new mortgage lending.

However, she also said high mortgage interest rates continued to weigh on the market.

"It's clear that current high interest rates combined with a tight economy, are still influencing the market as buyers continue to act with caution while economic headwinds play out," she said.

The comment stream on this story is now closed.

REINZ House Price Index - May 2023

Volumes sold - REINZ

Select chart tabs

Median price - REINZ

Select chart tabs

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

201 Comments

NZ property correction. It won't happen overnight, but it will happen.

Lv Rach xx

"REINZ chief executive Jen Baird said there were glimpses of positivity in the market"

"Its life" Jim, but not as we know it"

"REINZ chief executive Jen Baird said there were glimpses of positivity in the market"

Glimpses like twitches from a dying rodent after being whacked on the head

LOL! 🐀🔨

The dead cat bounce

Dead rat bounce???

Nice. She's pointing out the shiny bits on the turd for us.

Slump or correction? Take your pick.

Not too many green shoots there then..........

Still enough for a few on this site to keep smoking!

Nah, mate, this is the big one, prices to plummet and stay low. Pick your leafy green central suburb of choice and pick up a nice recently Reno'd 5 beddie for a hundred K, or half a butt-coin.

Capitalism will self regulate and give you exactly what you want!

Exhausted Pa1nter has now capitulated. More here are destined to follow as all those incoming Health, engineering, IT, professionals fail to rescue the housing market!

Anyone who thinks the value of an asset can't go down is kidding themselves.

Unless you're day trading, it's better to be looking at where longer term trajectories are going. For housing, it doesn't look like we'll be generating them significantly cheaper anytime soon.

Or, we're heading for financial Armageddon, in which case house pricing will be the least of most people's concerns.

Wow, so many comments on this article in such a short duration. We are an RE obsessed country for sure.

Mad mad place to buy.. Small sheeple island at the bum end of the world. Who in right mind really pays so much for shabby shacks in here.

There is really no corporate culture or growth for the young in this country.

So people shouldn't be sheeple

But instead flock somewhere with strong corporate culture

Hmmmm

The lack of corporate culture is precisely why I'm here.

Financial Armageddon is really an issue for those with to much debt and not enough income, and a job in a discretionary service. If you are not exposed to that your going to be fine. The creep of inflation being fueled to bail out risky lending is much more insidious.

Is anyone surprised?

And as I have said previously, HPI will keep falling more than median. In this respect, something that Greg omits is the significant impact on the data that a slump in sales of townhouses will have, given these are typically around lower quartile in price.

In fact we may even see the median rise slightly while the HPI continues to fall.

Good morning HM. Where do you get the data that breaks sales down by property type? I've never come across this, and as you suggest, it would be a valuable addition to our data resources.

I have developed my own system that I use for clients in the development sector.

A good example of the townhouse market in WGN;

https://www.realestate.co.nz/42379261/residential/sale/5-jean-caldwell-…

That $1.84m "sale" in 2017 is listed on homes.co.nz as;

ASR - Agent Sales Record. This record has been supplied to us by the Real Estate Agent(s) involved in the transaction. This is where the purchase agreement has gone unconditional but has not necessarily settled. Once the public record has been received by us from the relevant Council, the price and sale type will be updated. (The ASR code will change so S11 or other Council Sale Type)

So whether it went through or not - who knows - but will be interesting to see if it can sell for $1.2m in today's market. Might need to come back to the $920K price paid in 2017, I suspect (and even then....?). The rental market could free up considerably with a flood of these secondary sales falling through for relatively new townhouses. I wonder whether we seeing an oversupply of that type of housing?

Interesting to note in the property history - that the property sold twice on the same date - 16 Sept 2017 - for 2 different prices

One for $920,000 and the next for $1,840,000 (this is exactly double the $920,000 price)

Could the higher number be a contemporaneous purchase, or failed settlement, or other?

Or two for the price of two... I would say this is a data issue. I doubt it sold for $1.84 as there are too may directly comparable properties on both sides.

Data issue - that makes sense. But look at the weird "two" revaluations on 1 September 2021. And a check of the WCC rates database - sees them paying rates based on a $1.54m CV. And the neighbours got the same inflated valuation. So, QV might well have plugged that $1.8m sale in its revaluation algorithm. I hope owners haven't upped their borrowings on the house relative to the inflated figure!

FYI, QV.co.nz current valuation is $1,200,000

https://www.qv.co.nz/property-search/property-details/3218660/

I agree the $1.8 is an odd value. However, it is not unusual for a property to be contracted to be 'bought off the plans', then on-sold at a higher price on completion. Two sales on the same day is one mechanism for this.

Available on REINZ site but not published

Greg Ninness,

Does the asterix on the (5 Year*) stand for an annualised growth rate or something else?

I assume you mean asterisk rather than the comic book character Asterix. According the REINZ the asterisk denotes a compound growth rate. However inserting Asterix into the REINZ reports may be a worthwhile feature for some readers.

Haha. Reminds me of recently overhearing an adolescent refer to a musical sharp symbol, "Beethoven's Violin Concerto in D-hashtag Major"

Lol yes my error and showing my age as an avid comic reader in the 1960's :-)

yes corrected to rate per annum

Steady as she goes downwards.... WGTN at -26% getting close to the biblical geezers magic -30%

Remember we only had 9% drop post GFC in 2009 and took 7years to recover. WGTN will drop further 10-20% and will take10-20years to recover to 2021 levels..

probably wellington will stabilise where it is at the moment - but auckland will continue to fall. In Wellington the prices have been accepted and the rate of sales is back to where it was while in Auckland people haven't accepted the new market levels. There are 28 weeks of inventory in Auckland and it is climbing while in Wellington it is 14 weeks of inventory and falling.

And actually the regions will settle but I could see Auckland falling a few more percentage points.

Don't forget that a change in government could push house prices in Wellington down a cliff, perhaps back to pre-2017 levels. House prices in Wellington first took off in the aftermath of the 2016 earthquake when many people were locked out of apartments blocks.

A year later, the Labour-led coalition took office and bumped up public service headcount, with the hiring frenzy really picking up during Covid. Public service headcount has gone up 34% (18k) since 2017.

As per PSC data, nearly came from back-office roles (managers, HR, admin workers, etc.)

Consulting spending is also up 66% since Labour took office, despite promising a big reduction from lifting FTE caps on public service and hiring more instead of outsourcing work.

Cue mass culling of hopeless roles and middle management come November 2023, or January 2023, increased job competition halting the increases in wages/salaries and increases in retention for those leftover. Then we'll start seeing a rise in productivity as this becomes the key focus for employers as they'll have a greater talent pool to choose from.

Auckland looks to be crashing nicely.

Pretty soon Labour will be able to say that they have presided over a very stable real estate market. If you exclude everything that happened in between 2017 and 2023 they will be able to say that house prices are the same when they leave office, as they were at the start.

Auckland's average price appears to be only 100K above 2017 prices, and with 6 months to go to the election and house prices falling 13k a month, it is going to be pretty close to that 2017 level.

Yes, they will and it is their excellent housing policies that have supported getting the craziness back under control.

Yes which National want to reverse so that the craziness continues. They have no chance of getting my vote because of this.

They don't care about much except to continue excessive tax free capital gains (and any criticism about it is just "tall poppy syndrome and wingeing")

Labour is setting the bar so low in terms of competence and performance that one would be forgiven for thinking it should be easy for National to top them. Alas! National seems determined to undo the incredibly modest progress Labour has achieved, especially in terms of housing affordability - which is clearly one of NZ's most pressing issues.

I would say it's our most important issue because it affects nearly everything. To think people should just "have more babies" is very out of touch. National's policies will mean less babies and more immigrants instead.

Don't let the facts intrude into your argument.

Labour has generated a boom/bust in housing.

Labour has ensured rental prices continue to march upwards.

Labour has increased immigration.

And you criticise National? Seriously WTF.

Labour's not great, but NACT plan to reinstate negative gearing, reinstate interest deductibility, reduce Brightline back to 2 year and "look at" allowing foreign buyers into the market again. Plus take off what restrictions there are on migration at the moment.

If Labour's policies stick they will completely change the landscape around residential property being the default investment option for NZ.

The boom was initiated a long time before Labour got in power. The most recent spike can be partially blamed on the RBNZ actions (but personally I think it was more due to personal greed and spruiker narrative from people like TA and AC and organisations like NZ Herald, REINZ and real estate lobby). The bust has come about due to increased interest rates which are globally driven. Labour's policies would have probably brought prices down but in a gentler way.

I'm not sure how you blame Labour for rental prices increasing. They have been increasing but by less than CPI?

Labour has increased immigration. Yes but National we're going to increase it too. In some ways Labour increased it to cut National's point of difference from under them. If Labour win the election you will see them start closing the floodgates, National/Act will blow the whole dam up.

I'm no fan of Labour's recent performance but on housing in particular they smash National out of the park

Ok let me look at your "facts":

"Labour has generated a boom/bust in housing"

This is not a fact - it's your opinion. My opinion is that it was the reserve bank that did this. Remember it was Orr saying "they wanted to have the least regrets" when dropping rates during covid. You could also blame the US federal reserve for leading all central banks that way. Then inflation hit the world everywhere at the same time. The same would have happened if National were in power.

"Labour has ensured rental prices continue to march upwards."

Rents have always gone up and there isn't any evidence that Labour has made this happen more. It's much better to be in Auckland than Sydney regarding rental growth.

"Labour has increased immigration"

We had low immigration the last couple of years and now we are catching up and need workers. National would probably be bringing in more to put more pressure on the housing market.

Poor Labour, in power for 6 years and had no control over any of those issues..

They are all Nationals fault...

No Rodger, I didn't say they were National's fault, I said you were wrong that they were Labour's fault which is different. Might be a bit difficult for you to understand the rules of logic as you seem to be blinkered by ideology.

I don't think you even read my response or care to, so I'm not going to continue this discussion.

House prices boomed worldwide as countries tried to soften the blow from the Covid lockdowns. The RBNZ basically did what everyone else was doing when they caused the boom. Feel free to blame Labour if you're small-minded enough to miss such details.

Labour then had the guts to put policies in place to encourage investors to buy new builds rather than competing with - and hogging - existing houses. With Jacinda "No-CGT-On-My-Watch" Ardern out of the picture, Labour might even be considering a proper CGT.

Meanwhile, all is National is considering is how to get the disaster that is NZ House Market capital gains into the stratospheric zone again. Pitiful.

Meanwhile, all is National is considering is how to get the disaster that is NZ House Market capital gains into the stratospheric zone again. Pitiful.

Clearly you are displaying traditional polar thinking. Perhaps try reflect and change from reacting to Labour criticism by shooting back with something around National, to a more broad based analysis of political parties and the potential solutions they offer NZ

Greens and Top both offer some positive housing policies.

Perhaps try reflect and change ... to a more broad based analysis of political parties and the potential solutions they offer NZ

Thanks, it is good advice to look at the smaller parties. Too bad we can't vote for different policies (on the big issues such as immigration, housing, health and education) in addition to a political party - with the winning party then being responsible for implementing the winning policies.

I like it - reimagining democracy. Great thought. It's a bit like California's Initiative and Referendum process.

NZ property will never get as expensive compared to incomes as it was in Nov 2021. To regain Peak Madness would be an astonishing feat as a new wave of automation washes over the world in the next couple of years, and NZ will not be driving it. And our balance of payments is negative.

Nov 2021 is going to sit there now on Web pages and memories as an infamous high tide mark, when we just managed to slide the very last blocks on a teetering pile, before gravity reasserted itself, and a bottomless pit of need swallowed it up. And we were here, we few, we lucky few, to witness it. Some of us even helped to pop a block or two near the top. Hold on to those memories - it's over now, finally.

.

probably wellington will stabilise where it is at the moment - but auckland will continue to fall. In Wellington the prices have been accepted and the rate of sales is back to where it was while in Auckland people haven't accepted the new market levels. There are 28 weeks of inventory in Auckland and it is climbing while in Wellington it is 14 weeks of inventory and falling.

And actually the regions will settle but I could see Auckland falling a few more percentage points.

Wellington had the biggest drop of 4.5% in last 3months compared to 2.5% in Auckland. Rate of decrease in wellington has increased. 14weeks of inventory heading into winter is like years worth of inventory. It will go down further 10-20% within next year. 26% drop has never happened in New Zealand for the past 100years.. worst was 9% in 2009.

Suspect some of the Wellington drop relates to the Wellington regions. Many of the bigger drops ( median house price) this time were in Wairarapa, not Wellington City or the Hutt. Very small sales volume in these areas though

bernard hickey was first to predict the 30% fall. He called it all the way back in 2008! 15 years too early but got to give it to him he's on the money!

Have you seen what Hickeys been saying lately, basically the complete opposite...

I moved on from reading the guy a lonnnngggggg time ago

Sure, but he claimed price falls were almost over back in April … 2022, when prices had fallen 5%~

He was still claiming inflation was “transitory” and saying inflation was about to “fall off a cliff” as late as early 2023.

He repeatedly claimed interest rates had “peaked” when they were still around 5%.

I don’t think he has been right about anything in the last 2 years, so I’m not sure why you think that will change now.

Say it often enough and you will be right one day.

some people just love to validate with anything even a dead horse

For every Buyer, there is s Seller.

And any transaction at the moment suggest the Vendors see the current price deteriorating further. And they are probably right, as we are continually assured that it is the Seller that controls the price of the market.

Some are selling because mortgage rate increases and lack of deductibility are forcing them to, regardless of where they think prices are going. That is why I'm having to find a new place to rent.

Note there were a few people here saying only 2-3 years ago that house prices would never crash.

Whoops.

Hardly a crash when the median is still up $150k +/- on 2020...

For now Nifty.

For those who purchased near the peak (in the areas where price falls have been the greatest) it will be feeling like a crash.

Does it feel like a crash if you don't obsess over your house value daily? I'd say most don't even think about it until they come to sell...

Friends in this position are off that exact volition. Worrying about your house price is only valid if you can't service the mortgage, or you have a vested interest in property perpetually increasing in value.

Obsess! I know quite a few who are starting to realise they are going to be stuck in the same first home s##box in the gang creep suburb with no end in site. They cant take a job out of town or country etc because they will end up with a mortgage to pay off and rent.

It's an absolute disaster out there for so many of the younger generation. They were raised and invested in by NZ inc to be the next generation of wealth creators. Now...they are in either in mortgage chains or are on the plane to Aus.

A replacement generation of our best are moving on if they can. Another one of mine about to go.....NZ outlook for her just looks bleak.

It's never a good time to buy a 'first home s##box in the gang creep suburb'... I suspect they got caught up in the FOMO over the last couple of years?

Hard call as it could have been the case, but can you really fault the basic drive to want to have a secure home of your own to raise a family in? This runs deeper than FOMO, as the FOMO will have been fueled even further who had planned on having a family after securing a house then had this dangled in front of them as potentially getting out of reach in a matter of weeks or months as the prices skyrocketed.

While yes, we can bag on the FOMO, but underneath it all is the simple wish to live the kiwi dream we were sold as possible if we worked and saved hard enough. The death of this dream for many will have been the last straw and they;ll pack up and leave, but the potential realisation that many new homeowners dreams of starting a family is financially impossible with the cost of servicing their mortgage, this is what is wrong with the notion of accumulating wealth through never ending capital gains

"Hard call as it could have been the case, but can you really fault the basic drive to want to have a secure home of your own to raise a family in?"

FYI, here is an example of owner occupier collateral damage from falling house prices elsewhere around the world:

I dont get it - the obsession of those who bought will this and that.

What ? so you can laugh and say I told you so?

How about checking back in 10 or so years, they same will regret of not taking any action be it a calculated one

"Hardly a crash when the median is still up $150k +/- on 2020..."

That is not going to provide any reassurance to the owner occupier buyers in 2020 - 2021, who have a large unrealised loss on a large proportion of their equity (which took many years to save, they might have used all their KiwiSaver as deposit, or they might have gone to the bank of mum and dad). Remember there are hardworking people and families who are affected here.

Some owner occupiers may now be in negative equity.

Many might now also be facing cashflow stress, mental stress and some may ultimately be forced to realise those losses.

Some may need to apply for social housing (or government subsidy in the private housing market).

The losses may cause long term mental health issues and unfortunately a few may resort to self harm.

FYI, median house prices are back to Feb 2021 levels.

Since Feb 2021, there have been over 167,000 transactions throughout the whole of NZ.

That is not going to provide any reassurance to the owner occupier buyers in 2020 - 2021, who have a large unrealised loss on a large proportion of their equity (which took many years to save, they might have used all their KiwiSaver as deposit, or they might have gone to the bank of mum and dad). Remember there are hardworking people and families who are affected here.

The key word here is unrealised. Just as peak prices were unrealised unless a house was sold and money changed hands, unrealised losses mean nothing unless there is a sale. Owner occupiers only need worry about ensuring they can service the mortgage moving forwards, the specuvestors on the other hand can take a long awaited bath for the betterment of society at large.

Actually unrealised losses become a big problem in a divorce. Instead of arguing over who gets to keep the house (and mortgage) the argument becomes how much one partner will have to pay the other partner to keep the house and mortgage. A friend from the US was in this situation post GFC, it cost her $45k to walk away from the house. It was that, or both partners had to declare bankruptcy as neither could afford to pay back the bank due to the drop in market value.

So, a reminder ... "happy wife, happy life"

I thought they had no recourse loans in the US and you just left your keys in the front door and called the bank to take over?

Edit - Apologies the friend from the US had this happen in NZ?

Only a few states have no-recourse loans. Jingle-mail is not universal in the US.

Definitely stresses the importance of maintaining relationships. Mantra for all: You're never too busy to work on yourself, you can't escape your own company! :-)

sexist nonsense

If you feel it is sexist to ensure your life partner is fulfilled and happy, then you may need to rethink your perspective

it's the phrase really - a bit grating, too patriarchal, a cliche - i do get the drift though

Buyers of off the plan in 2020 - 2021 might have issues at settlement date financing their purchase.

The market value of the property has fallen from their purchase price, and the purchaser may now borrow 25-35% less under current bank lending criteria, leaving a potential financing shortfall that needs to be filled.

Already seen a few of these listed for sale before settlement date.

Yep. Exact thing happened to my friend and his mrs. FHB in Welly- off the plans in late 21. Just settled. had to cough up 70k for the drop in value. Back foot for two great 27 year old kiwis, sucked into the fomo.

That’s such an absurd argument.

It's one of those moving goalpost type things. In 6 months time it'll be "Hardly a crash when the median is still up $75k +/- on 2017...".

Do a search on the REINZ report after the word "fall". You won't find it. You'll find "ease", you might even find "soften", but you won't find "fall".

Language is a powerful way to spin things; either by avoiding the most accurate terms for what's happening, or by trying to redefine them to suit.

"Do a search on the REINZ report after the word "fall". You won't find it. You'll find "ease", you might even find "soften", but you won't find "fall".

Language is a powerful way to spin things; either by avoiding the most accurate terms for what's happening, or by trying to redefine them to suit."

The commonly used positive spin phrase is "negative growth"

House prices are currently unrising.

'Negative growth' is my favourite

"Negative sideways movement"

Positive retreat

Double plus good

Exactly

"Hardly a crash when the median is still up $150k +/- on 2020..."

Using the nationwide fall from the peak of -18.0% for the REINZ house price index, the total market value of housing in NZ has fallen by an estimated NZ$321 billion (or approximately 84% of GDP)

Now try again in inflation-adjusted terms. Less than 50k off being a wash I'd say.

"Note there were a few people here saying only 2-3 years ago that house prices would never crash."

Professor Robert Shiller on the housing bubbles in the US and Ireland:

"There hadn't been, in the US or Ireland or other countries, any major drop in home prices within modern memory, and so it just didn't seem real to people, and they believed it couldn't happen"

The Auckland property median price chart is starting to look like the current Bitcoin price chart...

During post GFC prices were down 9% in 2009 and took 7 years to recover. We are down 27% in 18months in wellington and still dropping at a un-imaginable rate. Great depression in 1930s will look mild compared to this..

Geez get real. It’s a long overdue house price decline not the Great Depression!

I wonder what the one woof spin will make of this.

LOLZZ

FYI, here's the headline from the REINZ press release

REINZ May data: Early signs of returning confidence as sales volumes rise in the regions

https://www.reinz.co.nz/Web/Web/News/News-Articles/Market-updates/reinz…

I'm not so sure. I think it is just as likely that we've witnessed the end of the beginning as it is that we are getting close to a bottom/green shoots/prices stabalising.

I think that the reason regions are having a few more sales is just that we are seeing capitulation from some vendors. Some signs of vendors with pressure here also.

Breaking Neŵs.

Market has bottomed. Visible signs of green shoots as price drops reduce for one month.

Time to buy is now , coming into spring price rises, lowering inflation, STRONG GOVERNMENT spending AND COL advancements means the market is hot.

Huge immigration will put pressure on market as banks mortgages remain competitive.

"Early signs of a House Price turnaround, momentum building in Wanganui"

🤣↗️

FYI, the REINZ house price index value for Wanganui has experienced negative growth of 22.3% from its peak.

e's takin the Pzzz

While I get the sarc, you sound just like a friend of mine who has rental properties XD Trying to convince them that things are not on the up and up anytime soon is like trying to make a brick wall transform into liquid by having a conversation with it

"I wonder what the one woof spin will make of this."

Oneroof.co.nz has chosen to not report on the REINZ data release.

FYI, here are some other reports on the REINZ data releases.

1) Stuff.co.nz

House sales jumped 30% between April and May: Real Estate Institute

https://www.stuff.co.nz/life-style/homed/real-estate/132321884/house-sa…

2) landlords.co.nz

Confidence returning to the housing market slowly

https://www.landlords.co.nz/article/976521861/confidence-returning-to-t…

Regions have a lot more in the way of price falls to come.

Nah fhb's provide support around the govt mandated "price floor" where all the subsidies etc kick in around the 550-600k mark in the regions of decent size.

Tiny towns down at 400k mark.

Auckland 875k I think. But I'd imagine servicability would bite fhb's in Auckland before reaching 875k unless they've got a very large deposit and income (kiwisaver balances and incomes have only grown last few years as prices come back).

Could somebody please explain this to me - say a property sold in BOP for 1M five years ago, and that was considered fair market value then. Does that mean we could apply the 5 yr BOP HPI of 7.3% and conclude it's now worth 1.073M? Or is it not that simple?

Yes, an index is that simple.

Edit: hang on a minute, there is an asterisk which Greg explains above that they have converted it to a compound growth rate. So 7.3% per year?

Reports such as the HPI provide a very broad overview of market movements, but probably shouldn't be used to determine things like prices of individual properties because their characteristics can vary greatly.

I agree it means 7.3% per year. So in this example, if a $1m house moved at the average for the region, it would go up 7.3% per year, to be $1.42m after 5 years, a 42% increase

Where I live there is so much on the market and not much is selling. Especially those over a million. It sure is going to be a tough winter for many vendors. Come spring zillions more houses will hit the market and buyers will have even more choice.

It's easy for people on here to forget that while we all take an interest in things financial and property related, there are probably a ton of people out there who don't share the same interests and are oblivious to what's actually happening in the property market. The real estate agent will have lead them down the garden path, hoping that the vendor will just accept whatever offer they get because they're "too far down the track".

I think the 1.5+ markets may see bigger % falls then the under 1 mil

Zillions of houses will not hit the market because everyone needs a place to live. If you sell what are you going to do, take a big hit and rent with a massive debt still to pay ? Probably not after all everyone here was saying it was only "on paper money" on the way up so its only on paper money on the way down. If you can stay employed then you just tough it out for the next few years.

“If you can stay employed…”

I’d say this may be a huge factor on the horizon. I’m seeing for-lease signs and other early signs of retrenchment everywhere.

Well this is hardly news is it ? Anyone with a mortgage regardless of the size of it needs to stay employed. Yes it looks like unemployment is set to rise, that's by design apparently which only goes to show the madness of the world we live in.

If you are struggling with mortgage payments you can downsize. Your house may have fallen in value but so have the smaller houses. You may take a hit on equity but you might still be better off.

I've just bought a block of land on the outskirts of Auckland. I reckon I got a terrific deal on it.

6 out of the 8 parcels have sold for around the $1.5m mark. There's going to be heaps of local development - a Fletchers consortium has acquired enough for 1800 houses and there's a vast 522 unit retirement village approved along with 90 bed hospital and lots of leisure facilities.

Nathan Rothschild ostensively said, "buy when there's blood in the streets".

That blood you're seeing, it's a small wound with only a trickle flowing. Unfortunately, the patient is on warfarin and it won't clot. There will be blood all over the place shortly.

I've been around the property game for a long time and I've never seen a prolonged or catastrophic crash.

Ah, thanks for letting us know. If you've never seen one, then everyone can relax as that surely means it could never happen. Right? (Yep, sarcasm)

Oh .... you never seen a prolonged crash??

We are collapsing, much faster than Ireland's (-60%, 6 year crash) and we only 1/3 into this once in "your lifetime" NZ crash.

ThIS pin prick blood flow, is no time to buy.

You missed the memo??.....everything changed post 2021.

Oh .... you never seen a prolonged crash??

We are collapsing, much faster than Ireland's (-60%, 6 year crash) and we only 1/3 into this once in "your lifetime" NZ crash.

ThIS pin prick blood flow, is no time to buy.

You missed the memo??.....everything changed post 2021.

Only at mid 2021 median prices range, more pain needs to come as houses are still unaffordable and overvalued for upcoming working generations + those 100k immigrants.

$500k new home and land package prices is where we should be heading, not so long ago in 2018-19 you could pick up a brand new home and house package in Papamoa, although small crowded streets, it was a new home that wouldn't put you into a depressive state over the mortgage.

B&T auction at 1pm in Auckland yesterday had a 91% success rate. 10 out of 11 properties sold.

Wow. How did the sell prices look?

At least 7 out of 10 sold for more than the current CV.

Yes, but how much down on peak?

The two I looked up:

sold for $1.4M, 200K down from peak

Sold for $827K down 200K from peak

Here is the link

Great.. Need to find the IQ level of these 10 sheeple. Combined Total reaches 100?

I suspect they are not idiots mate, the market is at the bottom or nearing it so if the right house comes along then you buy it. Idiots don't get mortgage approval for a million bucks.

They are definitely idiots if they got a million mortgage as only 2 of them sold for more than a million.

I checked each sale (and todays and the sales for last month or so) against ...

a) the last sale for the same property

b) the visual state of the property (i.e. whether is was subject to a recent reno)

... and guess what? Sellers are either:

a) getting about 1% above inflation on an annual basis (and many less) on what they paid, and/or,

b) probably not covering reno costs unless they've done it themselves and costed their labor at $0.00 per hour.

So yeah ... Nothing to shout about there.

(Gotta love the HTML DOM. Makes 'screen scaping' easy!)

Total spruiker death is occurring.

They sound like drug addicts when they talk about the market, as if the next high is just round the corner.

Not really the market is bottoming out to 2020 prices and the DGM's are still fizzing at the bung, so yes the next high is just around the corner as soon as prices start rising again. Personally I'm more concerned about the 2024 US election than NZ house prices.

,🤣🤣🤣

When adjusted for population size the figures here are grim. NZ's housing bubble has popped and there are more falls to come.

The housing market as a bubble is a poor analogy. When bubbles pop there's usually little left however that wont happen with housing.

For some people in negative equity they will be left with no house and a debt. Is that what you mean?

If they hang on they will likely be fine.

ouch!

Not the "Breaking News" I expected...

NZ IS IN RECESSION!

Good news!

NZ is in a MILD recession. Good news!

Mr Orr has fixed the property market in the most unconventional way.

Credit where credit is due ....

Mr Orr and the rest of the Monetary Policy Committee created the boom between 20 and 22. (For this they should be shot!)

The actual credit for ongoing falls - and increases in supply - started with Auckland Council's Unitary Plan of 2016 and ramped up with Central government's bipartisan (National and Labour) support for the MDRS and cross party support for the NPS-UD.

In all this the RBNZ has done nothing useful whatsoever! Absolutely NOTHING!

Is this tongue in cheek satire from you chris. I cant tell

Just facts. Presented in the shortest possible way. If you disagree then by all means present your reasoning.

(Saying the MPC should be shot might be satire, though. That's probably a tad harsh. I'd settle for them being whipped naked through the streets ala Game of Thrones.)

Not sure who in the MPC you'd want to see naked in the streets, but each to their own fetishes I guess?

The one with the biggest .... nose

Each month more people who fixed mortgage rates at super low emergency levels are now refinancing at much higher rate, many will be under huge financial pressure as this play’s out, house’s prices losing 25% of purchased value will create more of a downward spiral and will hit bottom when average wage couples can buy a house and still afford to live. A number of naive people and experts have said this would not happen but as a few of us predicted we are now see this unfold at a accelerating pace.

Lots of grumpy looking REAs around at the moment, the swagger has definetly gone out of their step.

So great buying time then. What would Buffett do buy when people are selling sell when people are buying. If you can add value beats sitting complaining at a screen all day. How's the kiwi savers going just as bad if not worst. I don't know as I wouldn't put my money with someone else.

Buffet knows price is what you pay and value is what you get..... price is still too high for crappy shiteboxes... there is no value in site.

Oh yes there is. Just doing subdivision as we speak total cost is 28k for lawyer council contributions and surveyor. Means I got a building site on the back of the house I own at front. To build a new 4brd new build including the subdivision cost around 250k. Which will rent out for 480 a week plus tax deductions along with 400 aweek I am getting for house in front paid 328k for which won't drop in price for cutting back off. What will the new build value at. Who cares

That explains clearly why property developers can outbid an owner occupier buyer and a buy and hold long term rental property investor who does not want to undertake development.

If there is profit, that is sufficient motivation for developers for adding more underlying supply of housing.

My estimate is that would be a gross rental yield of 7.9% on your cost (purchase price plus construction cost)

Strange this property Sat for three months no FHB can build on the back so will be adding to the rental pool. Give you 3 examples not including this one. You may have read these before. I bring these up as FHBs could not buy them. 1st brought an as is 3brm damaged by earthquake for 140k cannot get a mortgage or insurance because it's an as is. Cost me 75k to bring back to code but also fully insulated got rid of asbestos roof so new roof new dble glazing new bathroom new kitchen newly painted. Now rented no FHB could do that. 2nd was a mortgagee sale banks don't like loaning on those luckily I didn't need a mortgagee brought that for 268k spent 25k on new kitchen new paint inside out fully insulate and new dble glazing Now rented. 3rd just after first lockdown remeber the sky was going to fall in well that was what the media etc said was going to happen. Brought a 3brm on a quarter acre rented the front built 4 bedroom on the back also rented. Cause the way everything was looking FHBs wouldn't have been able to buy it let alone do what I do. We need rentals. Got a lady with her children I'm a rental shifted in with her then partner and two kids. Said it was only temp till they buy their own. Well partner shot thru after a little while. Few months later new partner was there yep all looking good yes they want to buy a house together etc etc 18 mths later he is gone. She been in that house coming up 5 yrs great tenant but people don't realise even if houses were 100k there will always be tenants due to life circumstances. So don't knock the guy like me for getting the work done so a family can have a home. I either lived in these house as I gutted them 1st one with no hot water/shower for 6 weeks middle of a christchurch winter with no windows in. Actually it was warmer under the floor putting pink batts insulation in than above floor. And take the risks all my houses are warm dry clean. Pity some tenants don't look after them as well

I'd pay WAAY more for a house with a backyard rather than house squeezed where one used to be. Just saying. I like land, veggies and things like that. Sun and some trees, room for a trampoline for the kids and a dog to run around.

You may want that but very few do now. As they are ever so busy on their ph or ordering Uber eats. Alot of my tenants don't even pick up bits of rubbish off the yard yet are so concerned about climate change. I have properties with half sections and still got trampolines kids play ground etc. And again most young ones wouldn't know the top to the bottom of a carrot let alone growing one.

As I've said before ...

1. Auckland will go back to the flatline between 2016-2020 that was created by the massive increase in potential housing supply created by the new high intensities allowed under the Council's Unitary Plan introduced in 2016.

2. The rest of the main metro centers will continue to fall until a new equilibrium is found that accounts for:

a) New local government planning rules, e.g. Wellington

b) The MDRS (Medium Density Residential Standards)

c) the NPS-UD (National Policy Statement - Urban Development).

If you disagree - prove me wrong.

Caturbury hasn't fallen. And at the moment am doing a subdivision figures above. Suggest you get out and drive the country a bit. I regularly drive from Invercargill to Taupo and you see things differently. Why are two of the wealthiest NZs buying up. Alan Pye, Gary Rooney are buying land property left right and centre but you won't see that looking at a screen

Uhhhhh The median price in Canterbury decreased 5.4% to $650,000 in May...

Over a yr it hasn't monthly it might.

Did you look at the REINZ graph for Median prices in Canterbury on this page (above) before saying "Canturbury hasn't fallen"?

Please also re-read what I said ... This bit especially: "The rest of the main metro centers will continue to fall until a new equilibrium is found that accounts for ..."

So in fact Canterbury is falling. Where it stops is anybody's guess. But, looking at the graph, Canterbury's price growth between 2014 and 2020 also went kind-of flat - maybe rises equal to inflation? Would that be down to new zoning rules post the Earthquake? Probably. If I'm right, and your comments do nothing to disprove it, then Canterbury still has a way to fall.

Your anecdotal evidence about what rich people are doing only means that they expect to make their desired ROI on the investment. (Probably based upon a new National Government.) It does not imply house prices will be going up in value. Prices can still fall and their ROI can be still be met. The same goes for your subdivision. But if you're planning on houses returning to price growth above inflation you may want to rethink the maths to establish what that would mean for you if I am correct (and as Auckland has shown, and Canterbury seems to show too).

By the way, where are Alan Pye, Gary Rooney, etc buying up land? Would it be inner city where they can build apartment buildings in line with the NPS-UD?

People say New Zealand is not Ireland when it comes to housing. "There were different factors at play" etc. Almost like they're insinuating these differences mean we'll have a better outcome than they did, Ireland being the benchmark for worst case.

Yet our falls continue to outpace theirs and from a much higher price point. I hope whatever magical force that sets the absolute price floor kicks in pretty soon.

Just a reminder that the first lot of 5 year Brightline trapped investors and holiday home owners are free to sell up from April this year. All those desperate owners hanging on by their fingernails waiting for the Brightline to tick over will start relieving a sigh of relief as they are finally free to realise their tax free capital gains. Just in time for that 5 year interest only mortgage to be refinanced. Listings should improve dramatically come spring.

Good point. Completely forgotten about that. Most will hang on using what fingernails they have left until the election.

Talking of waiting ...

A neighbor who is going to Oz has decided not to sell until prices recover. They'll be caught by Oz's Capital Gains Tax won't they?

Yes.

How pervasive is mortgage fraud in NZ?

One common method that I've heard mentioned was claiming rental income from NON EXISTENT borders.

With rising mortgage interest rates, these loans might get exposed.

Caught this story out of Australia - someone clearly overstated her income on the mortgage application (and this is after the Haynes Commission uncovered this behaviour).

In 2021, ANZ confirmed Ms Di Nardo had actually obtained a full-documentation loan, which requires more information than a low-doc loan. It's information Ms Di Nardo said she did not provide the bank or broker.

She said she was unaware that her loan application contained a document that stated she earned an annual income of $128,916.

"I never earned that kind of money in my life,” Ms Di Nardo told The Business.

“I wish I did."

The tax documents submitted in support of the loan application were for 2014-15 and 2015-16, and list tax agents Ms Di Nardo said she has never had any contact with.

The unsigned documents state Ms Di Nardo's net income was $122,481 in 2014-15 and $129,075 in 2015-16.

The ABC cannot name the mortgage broker website, the individual broker, or two people named on the supporting tax documents for legal reasons.

I'm not really liking the new REINZ monthly publication. I can't seem to find regional prices and their comparisons to month and years ago.

Agreed, it also bugs me how they lump Nelson/Tasman/Marlborough together for a load of it unlike any other part of the country when there isn't sound rationale to do so.

... so it's not just me then.

Bugs me that I still have to drag my laptop out to view the reports…. why is it not compatible with phones and iPads anymore?

Retail interest rates have averaged around 6.7% in NZ over the past few decades. So Jen Baird is completely incorrect to refer to interest rates as 'high'. They are about average at the moment.

Many borrowers have been conditioned by the low mortgage interest rates in recent years and many expected mortgage interest rates to remain low . As a result of these expectations and expectations of rising house prices, many chose to borrow large amounts relative to their incomes.

Many highly leveraged borrowers are hoping for lower mortgage interest rates, which may or may not happen.

The key question is how many highly leveraged house owners will be unable to hold on.

With 1 year fixed mortgage interest rates currently around 6.8%, these are levels last seen in Dec 2008 (i.e. almost 15 years ago)

https://www.interest.co.nz/charts/interest-rates/fixed-mortgage-rates

Yes perfectly normal and quite reasonable interest rates right now historically. We will not see 2% or even 4% mortgage rates for years if at all

looking for a two flat property in welly

preferably

1) run down or damaged or rotting or

2) a dwelling able to be converted to flats and

3) with enough land for a an extension &/or a flat in either case

its about the capital gain m8

Cheers

When everyone's so bearish, that's the time to buy. There's parts of Auckland like Riverhead that are going to expand rapidly with big companies acquiring vast tracts of land. Riverhead is right next to Auckland's most expensive suburb - Coatesville.

What's that mean to the trained mind?

$$$$$$?

"What's that mean to the trained mind?"

Sounds like you just bought there and you're trying to get others to also buy into it to increase your land's value.

I have, I've just bought a block.

There's also road widening planned to cope with the increased traffic. I sold a couple of properties 2/3 years ago, now I'm looking to get into an area that's expanding. By the time the doomsayers are convinced the plunge is over they'll have missed the boat.

I did the same thing many years ago in what's now West Harbour when there was nothing there and made a killing.

Most people just want a roof over there head. As such they are not playing in the rarefied atmosphere of land value speculation taking advantage of the larger property rezoning driven by council.

Does that mean you don't approve of my purchase? And the risk I'm taking.

My approval or non is meaningless. Just saying that's a whole different game that most are not involved in.

Anyone who cares to take a punt doesn't have to spend millions, all they have to do is buy a house or section in the area. I still own a house in West Harbour which I built when it was bare land, it cost $140,000 total to build, and I've had years of rent off it. It's made me a fortune.

We're considering purchasing currently, and have looked into Riverhead, but the travel time is just too much of a killer, the road in and out of Kumeu is a disaster, with no fix in site. Join the local community pages and read the daily posts about it.

Coatesville is a completely different market - lifestyle properties with owners who don't need to travel to and from the city, unlike Riverhead. The properties we've seen for sale in Riverhead have been on the market for months. For an investment, there's better out there, but if you're able to work from home or have a business in Silverdale, Albany etc then it probably works fine.

Yes, you are correct, the traffic is a problem, but there aren't too many places in Auckland where it isn't.

The road works that were supposed to fix it were meant to be started years ago but like everything else in this country, nothing's happening. There's billions going to be spent in Riverhead, that's the attraction for me. And I don't commute.

Editor / Greg :

Can you please clarify and help us understand why the comments regarding the most recent auctions were removed?

CN: We do not allow promotional material to be inserted into comments and that includes links to agency websites. If we allowed this to happen we would have dozens of agents cluttering the comment stream by posting links to their listings and that is not something we or most of our readers would want. Commenters who do this repeatedly risk having their commenting rights cancelled. The results of all of the auctions in your link, and many more from around the country, are available for all to see on our Residential Auction Results Page. - Greg.

Thank you for your clarification.

Apologies Greg - I didn’t realise that item I posted had live links to listings - was simply making the point that here is an example of one investor who has just listed half of his South Auckland portfolio.

Investors are in fact cashing up as the loss of interest deductibility starts to bite.

With regard to the sales data the point I was making is that where those 10 from 11 sold at that Barfoot auction session that most were purchased so long ago that there was still a significant capital gain on them albeit lower sale prices than what might have been obtained in 2021 had they sold then.

So when we hear about a sale on here we are no longer allowed to post the previous sale price and date?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.