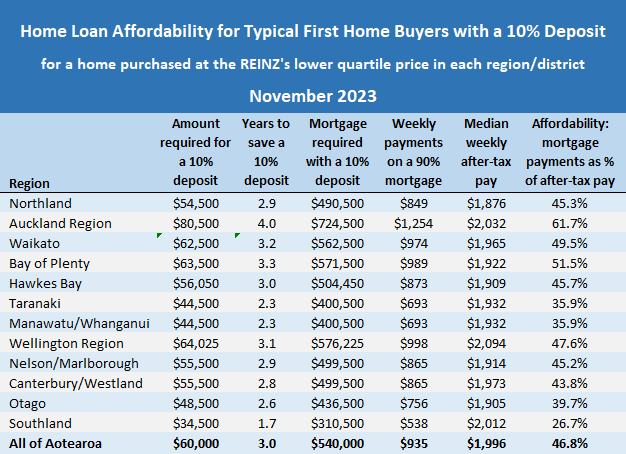

There was no meaningful movement in the main measures of housing affordability in November as the bottom end of the housing market moved sideways in quiet trade and interest rate rises all but stalled.

According to the Real Estate Institute of NZ, the national lower quartile selling price was $600,000 in November. That's up $1000 compared to October, putting it back to exactly where it was in November last year, but still down $70,000 from its November 2021 peak.

The lower quartile price is the price point at which 75% of sales are above and 25% are below, representing the most affordable end of the housing market that's of most interest to potential first home buyers.

Around the country, November's lower quartile price declined in six regions compared to October - Auckland, Bay of Plenty, Hawke's Bay, Nelson/Marlborough, Otago and Southland, and increased in six regions - Northland, Waikato, Manawatu/Whanganui, Taranaki, Wellington and Canterbury.

At the same time there was a minuscule increase in mortgage interest rates, with the average of the two year fixed rates offered by the major banks increasing from 7.01% at the end of October to 7.04% at the end of November.

Those tiny movements in prices and mortgage rates would have pushed up the mortgage payments on a home purchased at the national lower quartile price by about $4 a week.

That was less than the average increase in after-tax pay which typical first home buyers are likely to have been receiving lately. Interest.co.nz estimates this has been increasing at the rate of about $6 a week over the last few months.

So overall, affordability for typical first home buyers improved by about $2 a week in November. Or put another way, there was no meaningful change but at least it didn't get any worse.

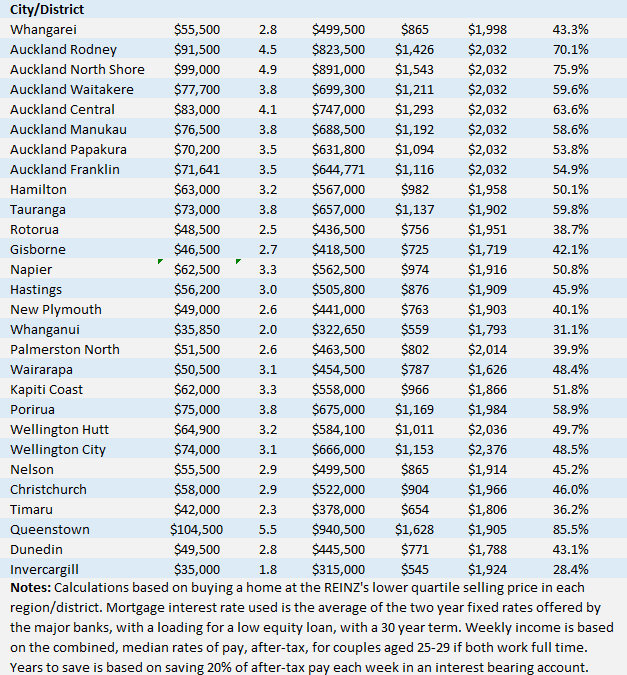

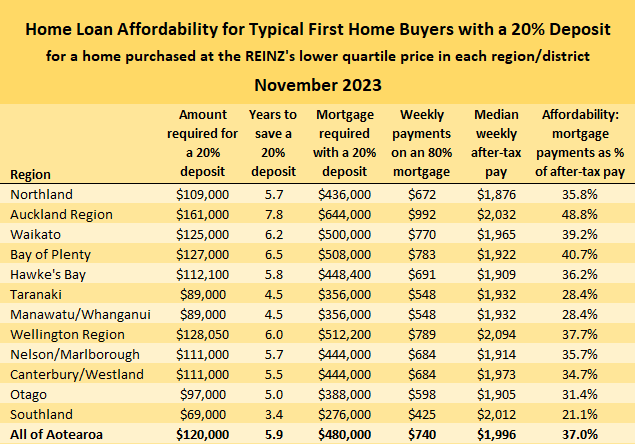

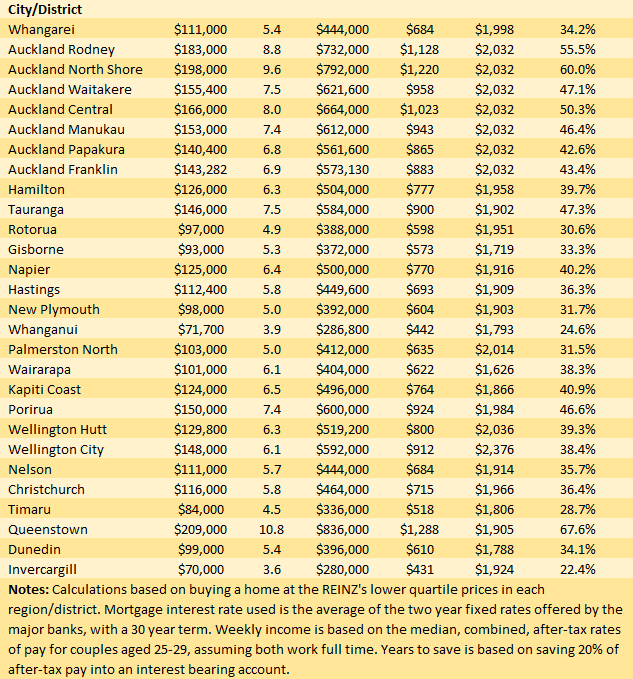

The tables below give the main affordability measures for typical first home buyers with either a 10% or 20% deposit for a home purchased at the lower quartile prices in all of the country's main urban areas.

This is our final Home Loan Affordability Report for 2023 and we wish all of our readers a Merry Christmas and Happy New Year.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

81 Comments

I cannot imagine what it is like for 60% of my salary to go towards mortgage repayments. the monthly repayment on my first home was $900. That was only 2011. It is surreal how feudalistic the country has become in such a short space of time.

A small improvement in affordability - but, nonetheless, well fought for.

TTP

I used to be on just the average wage and paying the mortgage on a single income. Yes I was paying it down faster than I needed to but wanted to kill it in 15 years or less so at one point 80% of my pay was going on the mortgage. Priorities I guess, you just suck it up and do it.

Yeah, "suck it up and do it" doesn't really work anymore in a world where they are printing trillions at will, effectively enslaving vast majority of the populous and its offspring without them noticing... but here we are, just bi*ching about how everything is property speculators' and the immigrants fault :P

I'd love to see you buy a house in today's market on a single income and with average wages, LOL.

Well, it's tough, but you certainly can, it just depends where. Look at the charts provided, there are many localities where this is feasible.

Hi Yvil, malamah kindly crunched the numbers a bit further down. Had you worked out the maths before making your comment, you'd have seen that by spending 80% of the average wage (on a single income), you'd be able to get a loan of about "$265k" (assuming you managed to scrape together a 10% deposit - or perhaps you could get your parents to pitch in as Zwifter's allegedly did).

Now, have a look at the charts provided and please point out where you can buy a house for that loan amount?

(Hint, the closest you'll find is Invercargill at $315K. I, for one, will find it hard commuting the hundreds of kilometres to work from there.)

But, it's OK. NZ's smug, 'savvy' landlords are not typically 'math' guys/gals.

Sounds great for those that wish to live in the great hustle-bustle metropolis that is Gore...

I did exactly this, in November 2023, by buying my first home in a small town in the North Island (population <3000). I got a 1000 m² section and 4 bedrooms to boot. It's not where I imagined I'd live, but I can actually afford it. I paid less than $400K.

Do you think if out of towners did that for all small towns, then people who live there will have to move, as their houses will become too expensive. Not to mention what a poor business model for NZ inc.

"Do you think if out of towners did that for all small towns, then people who live there will have to move, as their houses will become too expensive"

It has been happening for quite a period of time.

Property investors living in Auckland, bought out of Auckland when Auckland property had low rental yields. They were buying in Hamilton, which then drove up house prices in that area. Then this continued throughout the country. Eventually it got to small towns such as Kawerau, Invercargill, Hastings. That is how out of towners can bid up house prices that are too expensive for local residents. At some point these local residents are unable to afford buying and can only afford to rent. The lowest income earners may need a rental subsidy from the government, or even need social housing (which costs government money and tax payer money)

https://i.stuff.co.nz/life-style/homed/real-estate/117317608/how-a-town…

Now who are the own of towners who come into Auckland and buy? Here are some:

1) NZ expats working overseas e.g US, UK, Asia, etc. There was one person who reportedly bought over 25 investment properties throughout NZ in a short period.

2) local residents who have spouses working overseas (e.g wife and kids in NZ whilst income earner is fly in fly out) and sends money to NZ - e.g income earner works in Asia

3) non residents of NZ who are in the loophole of the ban on foreign buyers of existing houses in NZ - Australia, Singapore

4) NZ expats return to live in NZ from working overseas buy in Auckland. These people have been on higher salaries, have higher savings.

This was the reason for banning buying existing houses by many non resident non New Zealanders. They bid up house prices which made house prices unaffordable for local residents to buy.

Everything Zwifter says affordability should be taken with a scoop of salt. His parents gave him the deposit. The most deluded individual on this forum.

Yes, it's also delusional thinking that "August to October this year was the only window of opportunity to buy" This is despite a steadily rising mountain if listings, unemployment and debt stress and of course a flat market that's going nowhere. Someone whom is saving while receiving 6% interest on their growing deposit is making real progress here. Its one of the fastest ways to accumulate equity on the biggest purchase of ones lifetime.

I think Autumn 2024 will be the beginning of a period of real "buying opportunities".

Hi Retired-Poppy,

I think Autumn 2024 will be the beginning of a period of real "buying opportunities".

You repeat this message continuously but, alas, the crash (and "real buying opportunities") never eventuate.

Spare a thought for anyone who's taken your advice over all the years that you've been mouthing-off here...... Your followers are growing older but remain without the many benefits of home ownership. They'll be wringing their hands with despair. Certainly a lot of rent money down the drain. 😤

TTP

....speaking of mouthing off 😂

Spare a thought for anyone who's taken your advice over all the years that you've been mouthing-off here...... Your followers are growing older but remain without the many benefits of home ownership. They'll be wringing their hands with despair. Certainly a lot of rent money down the drain.

Everyone I know who 'missed out' on buying a house in 2021 and is still renting is delighted and relieved with how it all played out. I'd rather spare a moment for the poor bag holders who have horribly overpaid in recent years and are now up to their necks in mortgage payments.

What has been the financial cost of following that advice that those commentators don't tell you about?

Here are some financial calculations for owner occupier buyers to think about. The Peaker and Buyer Today.

How does this compare with a Peaker and a Buyer Today (BT) in NZ? (Assuming that the Peaker can hold on and is not under cashflow stress to sell.)

1) Peaker

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

2) Buyer Today ("BT")

In 2021, the buyer who waited, deposited the same $260,000 equity into a bank deposit earning interest. Also BT would rent an equivalent house and have still saved money due to the rental being below the monthly P&I mortgage payments of Peaker - in 2 years the savings would have been about $20,000 annually. So a Buyer Today would have an amount of $319,349 to use as a deposit.

The current median house price for Auckland is $1,040,000

Equity deposit of $319,349

The mortgage at this purchase price would be $720,651 (an LVR of 69%)

The Peaker has a mortgage which is higher by $319,349 (mortgage of $1,040,000 for Peaker vs $720,651 for BT)

Assuming BT, pays the same exact dollar amount each year that Peaker pays for their mortgage, as a result of that additional borrowing, Peaker is paying $856,632 more over the 30 years than BT (This is due to higher borrowing amount of $319,349, and total interest on this of $537,283 over 30 years). BT is mortgage free by the year 2042, whilst Peaker continues to pay their mortgage until 2051 (9 years later) - so after the year 2042, BT can save all that money that Peaker continues to pay on the P&I mortgage.

Assuming same incomes, and same living costs (food, travel, etc except mortgage) , BT can save the $856,632 in payments that Peaker is paying.

Remember that at the end of 30 years, the house price will be EXACTLY THE SAME for Peaker and BT.

BT will have more money available for retirement than Peaker. Conversely, Peaker will have less money than BT at retirement.

That single decision to buy in November 2021 would have cost $856,632 extra to buy the exact same house for Peaker compared to a Buyer Today.

Note that the median house price today of 1,040,000.

If Peaker was on an interest only loan - then all of Peaker's equity has evaporated in 2 years.

Median House price: 1,040,000

Mortgage balance: 1,040,000

Equity is ZERO

Loss of 100% of equity deposit which may have been their entire lifetime savings.

Thank you very much, CN. I much appreciate your comprehensive and information-rich posts. It combines facts from various sources and blends them into some fascinating insights.

"Each new generation of new investors learns the same lessons learnt by previous generations of new investors"

"What we learn, is that people don't learn from history."

"Those who fail to learn the lessons of history are doomed to repeat them"

Narrative < numbers

Nice explainer for those of us who struggle with the numbers and promote narrative based decision making over the cold numbers

In case you don't know, here are residential property price falls in other countries around the world

https://www.interest.co.nz/property/125605/david-cunningham-looks-wild-…

"spare a moment for the poor bag holders who have horribly overpaid in recent years and are now up to their necks in mortgage payments."

Here are some reported examples.

1) May 2022 - https://www.nzherald.co.nz/nz/waiting-for-the-guillotine-to-fall-how-in…

2) July 2022 - https://www.oneroof.co.nz/news/homeowners-scramble-for-interest-only-li…

3) Nov 2022 - https://www.stuff.co.nz/business/130353910/no-money-in-negative-equity-…

4) Jan 2023 - https://www.nzherald.co.nz/bay-of-plenty-times/news/homeowners-scared-a…

5) Feb 2023 - https://www.nzherald.co.nz/business/mortgage-shock-900fortnight-rise-fo…

6) May 2023 - https://www.nzherald.co.nz/kahu/peak-ocr-pain-auckland-couple-working-f…

7) May 2023 - https://www.oneroof.co.nz/news/latest-news/interest-rate-pain-banks-urg…

😎 July 2023 - https://www.oneroof.co.nz/news/they-dont-know-how-theyll-afford-it-home…

9) July 2023 https://www.oneroof.co.nz/news/desperate-homeowners-turning-to-third-ti…

10) July 2023 - https://www.stuff.co.nz/business/property/132483897/mortgage-rate-pain-…

11) Nov 2023 - https://www.oneroof.co.nz/news/refix-terror-homeowner-has-to-stump-up-a…

Many will simply be unable to maintain their higher mortgage payments as they renew their mortgage interest rate. Those that followed the advice of some commenters and bought in the 2021 - 2022 period using high amounts of leverage are going to lose a significant chunk of their equity, for some it could be their entire life savings. Some will be in negative equity and will owe money to their lender even after the residential property has been sold.

There will also be the non financial costs, the impact on their mental health.

Owners who are in negative equity

https://www.stuff.co.nz/business/129470098/hundreds-of-wellington-first…

I see we hear only crickets from TTP when faced with cold hard logic and reason as well as evidence to the contrary. I guess it is too hard to find facts as a spruiker when the market doesn't suit their narrative.

Average income is around $66k. After tax, ~$52k. 80% of that is about 800pw.

So first of all, "Dear second tier lender, yes I accept 14%p.a."

Second of all, even if this were the case, you'd be looking at ~$100pw rates and insurance (maintenance? wouldn't even bother.)

Leaving $100 for food, power, comms (phone and internet if desired).

This will get you about $265k in loan at that rate, and provided you had some deposit (1 year earnings) you could afford about $330k.

So what you're saying is the very best you could suck up and do is not even half what is expected of young people these days.

Nice one.

Thanks malamah.

Some of the worst posters on this site never use numbers or logic. They prefer hyperbole and/or sweeping statements. Especially if it points out how clever, grand or experienced they are. You know, they're somehow far better at this than everyone else is. And when challenged? They slink off, or change the subject, or resort to personal attacks or whataboutisms.

Ah the old days of 3x your salary ah Zwifter..

I used to be on just the average wage and paying the mortgage on a single income. Yes I was paying it down faster than I needed to but wanted to kill it in 15 years or less so at one point 80% of my pay was going on the mortgage. Priorities I guess, you just suck it up and do it.

Entirely possible before the ponzi became the be-all-and-end-all. What we know now is that h'hold formation is a completely different animal than in the 1950s-80s.

I just looked at my first home purchased in 2009. It was $740k and I was on about $100k (7.4x). That house sold recently at $2.0m and my salary is about $200k (10x)…. So house is up nearly 3 times versus 2 times for salary. Interest rates were about the same.

Crazy. The market is broken.

No amount of “suck it up and do it” can fix that.

Maths edit: thanks CN

"That house sold recently at $2.0m and my salary is about $200k (20x)"

Typo? should be 10x? (i.e. 2.0mn / 200k)

Try having more than 60% of your salary go on rent. At least with a mortgage you're getting some of that money back.

"Try having more than 60% of your salary go on rent."

Yes, that is certainly tough.

"At least with a mortgage you're getting some of that money back. "

Buyers in the 2021 - 2022 period would have been better to rent rather than buy. Many of those buyers have lost a significant chunk of their equity deposit. Some are in negative equity. Many are now in cashflow stress, and may be in mental stress.

Here are some reported examples.

1) May 2022 - https://www.nzherald.co.nz/nz/waiting-for-the-guillotine-to-fall-how-in…

2) July 2022 - https://www.oneroof.co.nz/news/homeowners-scramble-for-interest-only-li…

3) Nov 2022 - https://www.stuff.co.nz/business/130353910/no-money-in-negative-equity-…

4) Jan 2023 - https://www.nzherald.co.nz/bay-of-plenty-times/news/homeowners-scared-a…

5) Feb 2023 - https://www.nzherald.co.nz/business/mortgage-shock-900fortnight-rise-fo…

6) May 2023 - https://www.nzherald.co.nz/kahu/peak-ocr-pain-auckland-couple-working-f…

7) May 2023 - https://www.oneroof.co.nz/news/latest-news/interest-rate-pain-banks-urg…

😎 July 2023 - https://www.oneroof.co.nz/news/they-dont-know-how-theyll-afford-it-home…

9) July 2023 https://www.oneroof.co.nz/news/desperate-homeowners-turning-to-third-ti…

10) July 2023 - https://www.stuff.co.nz/business/property/132483897/mortgage-rate-pain-…

11) Nov 2023 - https://www.oneroof.co.nz/news/refix-terror-homeowner-has-to-stump-up-a…

Many will simply be unable to maintain their higher mortgage payments as they renew their mortgage interest rate. Those that followed the advice of some commenters and bought in the 2021 - 2022 period using high amounts of leverage are going to lose a significant chunk of their equity, for some it could be their entire life savings. Some will be in negative equity and will owe money to their lender even after the residential property has been sold.

There will also be the non financial costs, the impact on their mental health.

Owners who are in negative equity

https://www.stuff.co.nz/business/129470098/hundreds-of-wellington-first…

Many of these buyers may prefer to have rented instead of buying.

The price needs to be kept stable, only rising by the general rate of inflation if at all.

To prevent price rises, non-value added costs need to be removed, ie remove restrictions that cause speculative, monopolistic costs that result in demand and supply imbalance and an increase in price without any extra amenity value. That's what new Govt. regulation and deregulation need to focus on.

This reduction in non-value-added costs is more than enough to counter any increase in value-added costs like upgrades in building regulations.

To prevent price rises, non-value added costs need to be removed, ie remove restrictions that cause speculative, monopolistic costs that result in demand and supply imbalance and an increase in price without any extra amenity value. That's what new Govt. regulation and deregulation need to focus on.

Can't disagree with that. Problem is the purchasing power of the currency has been decimated. That's a far bigger issue to contend with. And the boomers wear the pants. They're not going down without a fight. Problem is that the younger generations can no longer feed the monster they've created.

It's not so much the loss of purchasing power, in as much as what we have been unnecessarily spending the money on.

Approx. 1/3 of the cost of housing is non-value added costs, which represent up to 80% of a person's mortgage in extra debt they have taken on, and the interest required to pay that. All for no extra amenity value.

If you still had that money in your hands, that would easily cover any loss of purchasing power.

And because they can't remove enough of the non-valu added costs immediately least they cause too many economic problems, the best they can do is strive to prevent any increase and let increasing wage inflation restore order over time to a more affordable median income multiple.

It's not so much the loss of purchasing power

It's exactly what it is

For owner occupier buyers, something to think about;

Rent vs buy in Auckland

Can get this lifestyle with renting and at much cheaper cost (for an equivalent house, estimated to be $36,816 to rent vs $73,800 payment for 80% LVR on a 30 year P&I with rates, insurance, maintenance etc.)

Here is a house in Auckland near the median house price in Auckland currently for sale:

https://homes.co.nz/address/auckland/panmure/32-domain-road/QjbYx

Can keep saving the difference of renting over buying (this is almost $37,000 in year one) to increase their savings. Savings can be deposited in bank earning interest, thereby increasing the size of savings.

Every owner occupier buyer should do their own rent vs buy calculation - one of the key assumptions is the future house price growth over their expected holding period.

And if it helps prospective buyers I can say (with statistical evidence to back it up if given permission to reproduce it) that roughly 19 out of 20 houses selling now are getting no better than between a 3% to 4% annualized nominal return from the original date of purchase without spending considerable sums on significant upgrades or extensions, and/or major renovation.

The 'house prices double every ten years' nonsense requires a rate of 7.2%. Very, very few are getting that at this time and those that do are either lucky, or buy with specific attributes firmly established at purchase time.

The 'house prices double every ten years' nonsense requires a rate of 7.2%. Very, very few are getting that at this time and those that do are either lucky, or buy with specific attributes firmly established at purchase time.

The 7-10 year theory should be consistent with growth in credit creation - more or less created out of thin air. Ashley Church never talks about his baby in these terms.

Have you extrapolated that rent vs buy calculation when factoring in rent increases? Using your numbers provided, let's work on a round $1m property, $200k deposit. I've assumed:

- Rent will increase by 5% p.a.

- The owner's rates/insurance increase 10% p.a. for the full 15 years (very unrealistic but gives renting a bit of a handicap).

- A current mortgage rate of 7.35% on $800k = $66k per year, leaving an initial $8k for rates/insurance/maintenance.

Invest the $200k deposit and the savings between rent/owning ($37k year 1), compounded return 7% gross. By year 15 the renter will have around $1.1m net savings and be down $800k. If the house increases by just 3% p.a. it's worth $1.6m and the home owner is down $1.2m.

"Have you extrapolated that rent vs buy calculation when factoring in rent increases?"

The calculation has been extended out to 30 years and factored in rent and home ownership cost increases.

Owner occupier buyers will have their own assumptions for the above variables.

The idea is that a home buyer at the current median price and current interest rates, and ownership costs spends a total $1.2mn over the next 15 years to own and maintain their home - P&I mortgage, rates, insurance, maintenance, etc.

The non buyer can spend that same $1.2mn over the next 15 years in rent for a similar dwelling and save the differential to invest. Or they could rent a smaller place and save more.

So the question becomes how to get the highest probability adjusted future value for the same $1.2mn that the owner occupier spends over the next 15 years (the expected holding period of the property)

There are 2 key assumptions:

1) due to the impact of leverage, the output is highly sensitive to the assumption of house price growth for the holding period

2) investment returns for the holding period

Both assumptions are very difficult to forecast with much accuracy.

There are other scenarios not examined above. For example - rent, save and buy later if house prices become more attractive and house price growth increases.

Will house prices offer higher house price growth in the future than that currently available?

1) If owner occupier buyers believe that house price growth is inadequate and they could rise, then renting may be a better alternative.

2) If owner occupier buyers believe that house price growth are at or near peak levels or sufficiently attractive, then buying may be a better alternative.

Note higher house price growth is a result of lower prices.

Yes the figures are very difficult to extrapolate over a long term. What if rents triple, house prices halve, mortgage rates go negative. So many unknowns. The best we can do is work with constants.

I might have been a little unclear on expenses. The non buyer over 15 years is spending: $800k on rent and $443k on investing + $200k initial deposit invested = $1.43m. The home owner has spent $200k on the deposit, and will pay $1.02m in mortgage/rates/insurance where R&I increase at 10% p.a. = $1.22m.

The reason the renter spends more, is that 5% increases p.a. in rent, in dollar terms, exceed the 10% increases in R&I for the home owner.

In the later years, when the rent is higher than the costs for the owner occupier's ownership costs (mortgage, rates, insurance, maintenance, etc), the renter pays for the shortfall from withdrawals from their savings / investments. (so previously the renter was saving the surplus, now they're withdrawing the shortfall)

This makes the annual cashflow payments of the renter from their annual income from their employment equivalent to that of the owner occupier buyer. (& totals $1.2mn over 15 years, including deposit from your example)

All that investing to withdraw the shortfall when they could have just bought a home. Their $1.2m investment stalls as they're now drawing down the returns, and the capital starts going backwards with inflation?

We haven't touched on wage inflation. While rents will increase, so will wages. The owner can increase their repayments each year. This would null out the scaling down of the savings the renter puts away, instead the owner shortens the loan term. Taking the dollar amount from the 5% rent increases, and adding to the owner's repayments, they'll be mortgage free in about 15 years.

"The owner can increase their repayments each year."

Assuming wage increases, if the owner chooses to increase their repayments, the non buyer will also increase their savings by the same dollar amount.

"adding to the owner's repayments, they'll be mortgage free in about 15 years"

The owner will be able to make principal reductions

The key assumption is future house price growth - it has a magnified impact (both on the upside and downside)

Each person has their own assumptions for the key variables and do their own calculations for their situation.

There are other scenarios that also need to be considered - such as rent, save and buy later as mentioned above.

But the non buyer is not increasing their savings. The non-buyer is subject to 5% rent increases. What I'm saying, is the home owner could increase their principal repayments by the same dollar amounts that the rents are going up by, so both are neck and neck.

That would mean the renter would continue investing the difference between rent and owning without the amount they invest diminishing over time as rents go up while the mortgage payments would not normally increase (aside from interest rate fluctuations).

As you say, key variables could change but I think the variables I've used, despite giving renting a bit of a handicap (10% p.a. rates/insurance increases for the home owner), are quite realistic. Thing is, if interest rates stayed in the 5 - 7% range, but wage inflation was 3% p.a., it would be fairly safe to assume that house prices might similarly track wage increases.

" The non-buyer is subject to 5% rent increases"

I don't know if savings from renter are unchanged in your calculations.

In my calculations, if the owner's costs remain unchanged, then renter savings are reducing every year due to the 5% rent increase.

Remember the key point is that renter spends exactly the same amount out of their regular household income as owner - that way the output is directly comparable. (FYI, that is how the calculation of Peaker vs Buyer Today is calculated to arrive at the comparable amount in year 30)

Let me explain, using an example assuming

a) no cost increases for the buyer / owner and

b) 5% rent increases for the non buyer

1) Year 1:

Owner pays: $66,000 per year for P&I payments on mortgage, rates, insurance, maintenance, etc

Renter spends same total amount of $66,000. This is spent in the following way:

- pays rent of $29,000

- saves $37,000

2) Year 2

Owner pays: $66,000 per year for P&I payments on mortgage, rates, insurance, maintenance, etc (no change in costs)

Renter spends same total amount of $66,000. This is spent in the following way:

- pays rent of $30,450 ($29,000 rent of previous year increased by 5%)

- saves $35,550 (reducing saving in year 2 compared to year 1 due to rise in rent)

3) Year 3

Owner pays: $66,000 per year for P&I payments on mortgage, rates, insurance, maintenance, etc

Renter spends same total amount of $66,000. This is spent in the following way:

- pays rent of $31,972 ($30,450 rent of previous year increased by 5%)

- saves $34,028 (reducing saving in year 3 compared to year 2 due to rise in rent)

So you can see that the renter is saving less due to rent rises ( year 1 - $37,000; year 2 - $35,550; year 3 - $34,028).

Now owner also decides to pay a lump sum of $5,000 in year 3 to reduce his mortgage (due to pay rise, bonus, unexpected gift, lottery win, etc)

To keep the exact same cashflows of the 2 choices, renter also saves this amount $5,000

"Thing is, if interest rates stayed in the 5 - 7% range, but wage inflation was 3% p.a., it would be fairly safe to assume that house prices might similarly track wage increases. "

Each person has to make their own assumptions based on their own set of circumstances. A young couple starting out might have higher wage inflation due to rise in experience and positional authority compared to an employee who has been in the work force for 25 years.

"it would be fairly safe to assume that house prices might similarly track wage increases."

House prices have exceeded household income increases for quite a few years now. That is how house prices became unaffordable for local residents. Previously could afford to buy a house on one single income. Now it might require 2-4 incomes or the bank of mum and dad - is this sustainable?

Also note since Nov 2021, on a countrywide level, house prices and household income increases have moved in opposite directions - slightly improving housing affordability in NZ.

Also, you'll see I mentioned in my workings, using 3% annual house price growth the $1m house should be worth $1.6m in 15 years.

Meanwhile the renter has $1.1m. Assuming all rates of increase remain static, it's by about year 29 that the renter's investment reaches $2.4m and that house increasing at 3% p.a. is $2.36m. But that's also based on the renter investing the difference between renting and ownership when the home owner's rates/insurance increase at 10% p.a. which over 29 years would stack the numbers heavily in the renter's favor.

If I dial that back to 6% increases, by year 19-20 the renter is paying more in rent than the home owner and they still only have $1.1m (due to lesser differences to invest).

Again, extrapolating 20 - 30 years is fruitless but I think I've used some fairly balanced numbers?

Shame it doesn't actually work like that mate, just about all the renters end up with nothing because they are spending everything on rent with no other option or are not prepared to compromise. Yeah so looking at the history of buying a house, there were 2 years recently that were bad timing, that's a couple of bad years in the last 50 so that's pretty good odds, otherwise its just DGM's cherry picking. Chances of picking other "Investments" that have paid off big over the last 50 years ? pretty low.

" just about all the renters end up with nothing because they are spending everything on rent with no other option or are not prepared to compromise."

That is entirely their choice. Some are financially illiterate and are blissfully ignorant of being financially illiterate.

Some are low income earners and not in a position to save - the most financially disadvantaged person is the low income single parent with children.

Not all renters are in that position, there will be quite a few potential owner occupier buyers that have the chosen to rent, and save to buy an owner occupier house in the future.

"Yeah so looking at the history of buying a house, there were 2 years recently that were bad timing, that's a couple of bad years in the last 50 so that's pretty good odds"

People who were knowledgeable could see the signs of extremely elevated house price risks.

Most people are unable to see the signs of extremely elevated house price risks and blissfully unaware of such extremely elevated house price risks.

There were warnings to the public by the RBNZ as early as Feb 2021 that people may have chosen to ignore, dismiss or perhaps were missed. The odds had increased significantly but most people couldn't see it.

Some people bet 500% of their net worth (80% LVR mortgage to buy a house) in 2021 - 2022, to potentially lose 50-250% of their net worth and entire lifetime of savings. There is going to be some real pain - both financial & mental. Unfortunately some will choose to resort to self harm.

"that house increasing at 3% p.a. is $2.36m"

I refer you to the Japan example of the dangers of using historical house price growth rates as the basis for future house price growth expectations.

Let's take a look at the leveraged buyer in 1991.

From 1955 to 1991, the house price index has grown at a rate of 13.0% p.a for 36 years.

A) 1991 - at time of purchase

House price: 1,827,882 (index value multiplied by 10,000)

House purchase price: 1,827,882

80% LVR mortgage: 1,462,308

Equity: 365,577

So given the house price growth average of 13.0% p.a over the previous 36 years, we will use 10% p.a to be conservative. This means in 32 years (in 2023), the house price would estimated to be: 38,593,556

Estimated house price in 2023: 38,593,556

Mortgage: 1,462,308 (assumed to be interest only for illustration purposes)

Equity value expected: 37,131,248

This represents a 15.5% p.a return on the initial equity of 365,577

B) 2023 - today

Market value of house: 1,352,113 (that is an annual growth rate of NEGATIVE 0.9% p.a for 32 years - vastly different than the "conservative" 10% p.a. used back in 1991)

Mortgage: 1,462,308 (assumed to be interest only for illustration purposes)

Equity: NEGATIVE 110,195

Total equity loss of 475,772

That is a loss of 130% of the initial equity - after 32 years

That one single decision to purchase in 1991 has had a significant impact on that person's standard of living in retirement, compared to if they had rented and saved the money in the bank and earned interest.

Ireland

A) From 1970 to 1Q2007, house prices rose at a rate of 11.59% p.a for 37 years. So a buyer in 1Q 2007 may have considered 8% p.a growth as being "conservative."

At an 8% p.a growth, a 1,539,735 Euro house in 2007 (index value x 10,000) might be worth 5,275,044 Euro in 2023 (16 years time)

B) How did it actually work out?

House price grew from 1,539,735 Euro in 2007 to 1,569,180 Euro over 16 years

From 2007 to 2023, house prices rose at a rate of 0.12% p.a for 16 years (FAR BELOW the "conservative" 8.0% p.a growth rate used back in 2007)

Remember the above is all unleveraged and before inflation.

https://fred.stlouisfed.org/series/QIEN628BIS

This is the same methodology that many property promoters in NZ are using in their long term capital growth forecasts.

NZ is much closer to hitting the Ireland 2007-2023 metric rather than the magical "prices double every 10 year metric"

NZ is much closer to hitting the Ireland 2007-2023 metric rather than the magical "prices double every 10 year metric"

FYI, some recent comments seen on house price forecasts:

1) seen in a property investment calculation on a Hamilton property done 2 days ago by a property accountant - 4.52% p.a house price growth in 10 years. He stated that this is "conservative"

2) "NZ likely to continue money printing in the next 12/24 months, asset prices like housing are set to double by 2030 as a base case and triple as a bull case is in our big cities" - made 3 days ago

Thanks Greg for one of most valuable reports on housing in NZ. Have great break.

Looking forward, if interest rates start coming down next year then FHB might finally get a break. But only if homes in their price bracket don't start rising again as 'investors' compete for the same properties. Both factors are in the hands of the RBNZ. i.e. dropping the OCR before NZ Inc tanks and getting the DTI installed with a sensibly restrictive DTI ratio.

Is this when the NZ first government poor cold water on the restart of the housing Ponzi.

One thing we all need to be grateful for in 2023.

It won't get any better to sort this out than now.

They came in on that mandate, and in my opinion are making the right policy statements on housing, although parts are still deficient and there will be some bad faith vested interest actors that will try to disrail it.

But some of the excess in price has been lost with house price falls in the last year, plus the higher wage inflation can help restore parity if they can keep house prices stable.

However having said that, there is no Govt. in the world that has, without pain, managed to successfully unwind a housing ponzi.

The housing market is way over valued it has crashed 20% in many areas but still it is unaffordable for one person buyer. People just need to wake up the next phase of crash will continue next year anyone who buys a property today will be sitting in negative equity in 18 months just like the people who purchased at end of 2021. Also inflation was up 15% in same period and NZD down 12% don’t listen to nonsense from many who post on here just look at facts and see crash has a long way to go.

A reminder for all potential owner occupier buyers - choose your scenario and act accordingly.

Which will the owner occupier regret most:

1) missing out on future potential gains in equity?

2) potential loss of their savings invested as the initial deposit for purchase of the house or even potential negative equity?

For owner occupiers, a reminder of the impact of leverage (it amplifies property price changes both on the up and down):

Scenarios of financial impact of leverage on equity, assuming an 80% LVR for owner occupier, for a recent $1,000,000 property purchase, $200,000 initial deposit, mortgage $800,000. (simple round numbers used for illustration purposes)

A) Scenario - property price rise:

1) property price rises 5% to $1,050,000, mortgage $800,000, equity $250,000, so 25% gain in equity value from $200,000.

2) property price rises 10% to $1,100,000, mortgage $800,000, equity $300,000, so 50% gain in equity value from $200,000.

3) property price rises 15% to $1,150,000, mortgage $800,000, equity $350,000, so 75% gain in equity value from $200,000.

4) property price rises 20% to $1,200,000, mortgage $800,000, equity $400,000, so 100% gain in equity value from $200,000.

5) property price rises 25% to $1,250,000, mortgage $800,000, equity $450,000, so 125% gain in equity value from $200,000.

6) property price rises 30% to $1,300,000, mortgage $800,000, equity $500,000, so 150% gain in equity value from $200,000.

7) property price rises 35% to $1,350,000, mortgage $800,000, equity $550,000, so 175% gain in equity value from $200,000.

8) property price rises 40% to $1,400,000, mortgage $800,000, equity $600,000, so 200% gain in equity value from $200,000.

9) property price rises 50% to $1,500,000, mortgage $800,000, equity $700,000, so 250% gain in equity value from $200,000.

10) property price rises 100% to $2,000,000, mortgage $800,000, equity $1,200,000, so 500% gain in equity value from $200,000. (i.e if they believe that the property price doubles every 10 years)

Remember, the owner occupier must be able to hold on under ALL economic environments (including any mortgage interest rate rises and potential significant reduction in household income).

Scenario - property price falls:

1) property price falls 5% to $950,000, mortgage $800,000, equity $150,000, so 25% loss in equity value from $200,000.

2) property price falls 10% to $900,000, mortgage $800,000, equity $100,000, so 50% loss in equity value from $200,000.

3) property price falls 15% to $850,000, mortgage $800,000, equity $50,000, so 75% loss in equity value from $200,000.

4) property price falls 20% to $800,000, mortgage $800,000, equity is ZERO, so 100% loss in equity value from $200,000.

5) property price falls 25% to $750,000, mortgage $800,000, equity is NEGATIVE $50,000, so 125% loss in equity value from $200,000.

6) property price falls 30% to $700,000, mortgage $800,000, equity is NEGATIVE $100,000, so 150% loss in equity value from $200,000.

7) property price falls 35% to $650,000, mortgage $800,000, equity is NEGATIVE $150,000, so 175% loss in equity value from $200,000.

8) property price falls 40% to $600,000, mortgage $800,000, equity is NEGATIVE $200,000, so 200% loss in equity value from $200,000.

There are lots of lessons littered throughout history if you look. For example, in terms of significant property price falls, there are lessons to be learnt from:

1) 1582 - 1810 Amsterdam property bubbles

2) 1890's NZ land bubble

3) 1880's Melbourne, Australia land bubble

4) 1920's Florida land bubble

5) 1930's US

6) 1980's Netherlands property price fall

7) 1990's UK property price fall,

8) 1990's Swedish property price fall,

9) 1990's Norwegian property price fall,

10) 1980's Finland property price fall

11) 1998 - Hong Kong

12) 1998 - Singapore

13) 1998 - Indonesia

14) 1997 - Thailand

15) 2008 - Ireland

16) 2008 - Spain

17) 2008 - Portugal

18) 2008 - Netherlands

19) 2008 - Italy

20) 2008 - Greece

21) 2008 - Denmark

22) 2008 - Cyprus

23) 2008 - Latvia

24) 2008 - Estonia

25) 2008 - Lithuania

26) 1990's Australia property price fall

27) 1990's central Auckland property price fall

28) 1989- 1990's property price fall in Toronto, Canada

29) 1990's Japanese property price fall

30) 1980- 1990's US savings and loan - California

31) 2005-2006 US

32) 2008 - Perth, Western Australia

33) 2009 - Queensland, Australia

Very astute. Keep up the contributions as they;re much appreciated and interesting :-)

"Each new generation of new investors learns the same lessons learnt by previous generations of new investors"

"What we learn, is that people don't learn from history."

"Those who fail to learn the lessons of history are doomed to repeat them"

Japan

https://fred.stlouisfed.org/series/QJPN628BIS

Some observations to note:

1) Residential property prices peaked in 1Q 1991.

2) Prices bottomed in 2Q 2009 (almost 18 years later) and fell 46.5% from their peak.

3) Prices are currently back at 3Q 2001 levels. - this means that everyone who bought between 1Q 1991 (32 years ago) and 3Q 2001 (22 years ago) and still owns, the market value of their residential property is still below their purchase price. Imagine that - owning for 22 - 32 years and the market value of your owner occupied property is below what you paid for it.

The person who started working in say 1985 (say 20 years old), saved for a deposit and bought in 1991. That person today is aged 58 years old, nearing retirement and the market value of their owner occupied home is still 26% below what they paid for it 32 years ago, after regular mortgage payments for 32 years. How many property buyers would expect that the market value of their property 32 years later would be 26% below their purchase price?

Note:

1) these numbers are before the impact of leverage.

2) back at the peak, some lenders were offering mortgages with terms of 100 years (multi-generational mortgages) - https://money.cnn.com/magazines/fortune/fortune_archive/1990/05/21/7356…

3) a buyer in 1Q1991 would have been better to deposit their money in the bank and rent for 32 years, rather than risk the loss of their entire savings used to buy that residential property.

Let's take a look at the leveraged buyer in 1991.

From 1955 to 1991, the house price index has grown at a rate of 13.0% p.a.

A) 1991 - at time of purchase

House price: 1,827,882 (index value multiplied by 10,000)

House purchase price: 1,827,882

80% LVR mortgage: 1,462,308

Equity: 365,577

So given the house price growth average of 13.0% p.a over the previous 36 years, we will use 10% p.a to be conservative. This means in 32 years (in 2023), the house price would estimated to be: 38,593,556

Estimated house price in 2023: 38,593,556

Mortgage: 1,462,308 (assumed to be interest only for illustration purposes)

Equity value expected: 37,131,248

This represents a 15.5% p.a return on the initial equity of 365,577

B) 2023 - today

Market value of house: 1,352,113 (that is an annual growth rate of NEGATIVE 0.9% p.a for 32 years - vastly different than the "conservative" 10% p.a. used back in 1991)

Mortgage: 1,462,308 (assumed to be interest only for illustration purposes)

Equity: NEGATIVE 110,195

Total equity loss of 475,772

That is a loss of 130% of the initial equity - after 32 years

That one single decision to purchase in 1991 has had a significant impact on that person's standard of living in retirement, compared to if they had rented and saved the money in the bank and earned interest.

Ireland example of Peakers vs Troughers calculation done in 2020

i) Index peaked at 163.6 in 2008

ii) Index currently at 133.9 in 2020 - 12 years later

After 12 years, the index is still 18% below the peak (and that is before the impact of leverage used by a buyer)

https://tradingeconomics.com/ireland/housing-index

What is the impact on a house owner?

- assuming a 80% LVR, and a 20% deposit, then that initial equity is down 91% - after 12 YEARS

1) The Peakers

A) Purchase in 2008 (interest only financing used as example)

i) House price purchased at 163,600 (index value 163.6 multiplied by 1000)

ii) Mortgage 80% LVR 130,880

iii) Equity deposit 32,720

B) Equity value in 2013

i) House price at 75,000 (index value at say 75 multiplied by 1000)

ii) Mortgage: 130,880 (LVR 174.5%)

iii) Equity value is NEGATIVE 55,880 (a fall of 171% from initial equity deposit of 32,720 after 5 years)

C) Equity value at June 2020

i) House price now at 133,900 (index value 133.9 multiplied by 1000)

ii) Mortgage: 130,880 (LVR 97.7%)

iii) Equity deposit 3,020 (a fall of 91% from initial equity deposit of 32,720 after 12 years)

Remember that the biggest asset for most people is their house. For many, this asset is used as the main source of their funds for retirement.

2) As contrast, what about the The Troughers who purchase in 2014 (after property prices have bottomed out and stabilised)

A) Purchase in 2014

i) House price purchased at 80,000 (index value 80.0 multiplied by 1000)

ii) using the same equity deposit as above: 32,720

iii) Mortgage 47,280 (LVR 59.1%)

B) Equity value at June 2020

i) House price now at 133,900 (index value 133.9 multiplied by 1000)

ii) Mortgage: 47,280 (LVR 35.3%)

iii) Equity deposit 86,620 (an increase of 164% from initial equity deposit of 32,720 - after 6 years - equivalent to a return of 17.6% per annum )

"the housing market ..... has crashed 20% in many areas"

House prices in some areas have met Ashley Church's definition of a property market crash.

Will Ashley tell you this? Will those with vested financial self interests tell you this?

1) From Ashley Church

"But what constitutes a housing market crash? ...... I define a property market crash as a 20% drop in the median sales price from market peak, and which lasts for more than 12 months." - https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

2) REINZ median house price changes from peak as at Nov 2023

Some areas below have now met Ashley's definition of a property market crash.

Locations where median house prices are down 20% or more from their peak:

1) Franklin: -21.4%

2) North Shore: -20.3%

3) Papakura: -29.8%

4) Waitakere: -21.1%

5) Hauraki: -20.7%

6) Otorohanga: -37.1%

7) South Waikato: -21.2%

8) Thames - Coromandel: -28.0%

9) Opotiki: :-21.8%

10) Rotorua: -24.0%

11) Tauranga City:-20.5%

12) Whakatane: -22.6%

13) Gisborne: -21.7%

14) Central Hawkes Bay: -27.6%

15) Hastings: -23.2%

16) Horowhenua: -24.3%

17) Rangiteki: -29.4%

18) Ruapehu: -32.3%

19) Whanganui: -23.1%

20) Kapiti Coast: -20.6%

21) Lower Hutt: -25.5%

22) South Wairarapa: -51.5%

23) Upper Hutt: -22.5%

24) Wellington City: -24.2%

25) Nelson: -21.7%

26) Buller: -33.7%

27) Westland: -33.4%

28) Hurunui: -22.3%

29) Clutha: -35.3%

31) Southland district: -25.4%

Remember that for most owner occupiers, the equity deposit is 20%, so for those who bought at or near the peak, most of their equity (which could be their entire lifetime savings) has evaporated in just 2 years. In some cases, property owners are now in negative equity.

The purchase of a owner occupied residential property is likely to be the largest purchase for most households and the source of funds for retirement.

Also remember, that the above are nominal prices and not yet adjusted for inflation.

What the property promoters with vested financial self interests are unlikely to tell you.

Another common line of reasoning is buy property as the mortgage erodes with inflation.

https://www.oneroof.co.nz/news/can-rising-inflation-magic-away-your-mor…

So how has that worked out as at November 2023 for a property owner who bought a median priced house in Auckland at the peak using an 80% LVR?

1) Median house price in Auckland has fallen 19.1% in nominal terms

A) November 2021

House price: 1,300,000

Mortgage (at 80% LVR): 1,040,000

Equity: 260,000

B) November 2023

i) Nominal terms

House price: 1,052,000 (-19.1%)

Mortgage: 1,040,000 (deemed to be interest only for simplicity and comparison)

Equity: 12,000 (-95.4%)

2) Inflation adjusted values using a deflator or 1.12 as per RBNZ for corresponding period

https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/inflatio…

House price: 939,286 (-27.7% from original price)

Mortgage: 928,571 (-10.7%)

Equity: 10,714 (-95.9% from original equity)

That fall in inflation adjusted equity value is a significant erosion of purchasing power.

Which would a person prefer?

1) pay 10-20% higher rent or

2) lose 95% of their equity used as a deposit

Also note: an owner who owned their property mortgage free experienced a 27.7% erosion of their purchasing power due to the inflation adjusted change in the market price of their property.

I just love how the "vested interest" spruikers are all running around saying interest rates will drop next year ......well, have they ever thought that would be worse for the FHB, as they will be competing even more with established investors, who are now getting those rental increases and have access to more credit than the average FHB....so we are now back to the FHB's getting pipped at the auction by the investor.

Truly marvellous !! - while what the "vested interest" spruikers don't realise, if interest rates do go down, NZ is in the economic crap, as not enough money being borrowed from the banksters, while the NZD will devalue vs. other currencies, imports will increase in $ terms creating more inflation.....talk about a country living beyond its means, just for the sake of a few "astute" property investors......

Crazy says the "CRAZY HORSE" !

"while what the "vested interest" spruikers don't realise"

There will ALWAYS be someone telling people that now is the best time to buy.

Why?

Because these people need to earn income to put food on the table to feed their families, pay for the roof over their heads (either rent or mortgage). More property transaction volume and transaction values financially benefit the following groups of people:

1) real estate agents

2) mortgage brokers

3) property mentors

4) property developers

There are others.

Positive spin leads to increased confidence to persuade people to buy.

Always remember the vested financial self interests involved.

Insane

61.5% of after tax pay in Auckland

That to me is not a market

It rep a market for 2 professionals on top dollar

How to at other expenses or have a life?

Don’t forget the 4 years saving for a deposit while paying rent. Young people are being ripped off, I have adult children who have no hope of buying until we die. I have never seen this before I managed to buy my first place on my own it wasn’t easy, these days young couples still can’t get on the ladder. This would be why the next phase of housing price crash will happen.

Tony Alexander in the NZH today: "My current pick for price gains in 2024 is the same as it has been since just before the middle of this year. About 10%. For 2025 there will be extra momentum in the housing market, FOMO is likely to be much higher, and I’d expect gains nationwide averaging closer to 15% then than 10%."

Clearly he's given up economics and now believes crystal balls with lashings of alcohol work much better.

So he is picking the Coalition Govt. to not meet any of its housing policy targets?

Does the coalition govt. have any housing policy targets?

He's picking that the only target is property price growth, ie the drug fuelled rockstar economy. He almost looks like a wannabe Keith Richards.

I think he is assumming that the coaltion are going to do exactly the same as Labour, and National before them. ie are well meaning in making housing more affordable, but their polices will either be poorly thought out and/or poorly implimented, and in many cases just make a bad thing worse.

The solutions are complicated in their simplicity.

the only potential negative that he mentioned was rising unemployment. Here are some factors that he has missed:

1) brightline test shortened to 2 years from July 2024 - how many property investors with negative cashflow properties are going to list their residential property for sale?

2) low deposit off the plan purchases that are unable to be settled

Here's how it might play out.

A) Real estate agent (to owner occupier / trader vendor with residential property in location / market with many property investors who is considering selling): the brightline test has been shortened to 2 years, effective July 2024. There is potential for negative cashflow properties to be listed for sale.

B) Owner occupier lists property for sale in New Year - rush of owner occupier listings for sale, hoping to sell before the potential increase in listings in May - June 2024 (hoping to sign S&P agreement before May - June 2024)

C) Property traders speed up their project and lists property for sale as soon as possible - hoping to sell before the potential increase in listings in May - June 2024

D) May - June 2024 - Negative cashflow property investors list their residential property for sale

E) July 1 2024 onwards - sale and purchase agreement signed - avoid brightline test on capital gain

Will there be a significant increase in listings for sale in those locations where there are a large number of non owner occupiers? (all property investors who purchased before June 30, 2022, will not be subject to tax on the capital gain under the brightline test)

First home buyers were better off by $2 a week in November as the market drifted sideways

To summarise... If we want to see a resurrection of real affordability in home prices (not loan affordability), the "market" needs to either:- heavily increase reverse acceleration or drive off the cliff.

It might be the economic driving lesson we need.

Mwahhh

Anyone feel like getting rich......or richer? Lots of people would like to, but even when led by the nose they won't.

Buy property in Riverhead, I've already bought land there so, yes, I've got a vested interest. I've done the homework and I've owned lots of properties. Prices there are up since the election.

Can't miss....get rich...automatically.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.