New Zealand's housing market "remains comatose" after the excesses of the Covid era, according to the latest Economic Bulletin by Westpac Chief Economist Kelly Eckhold.

House prices have remained flat so far this year even as interest rates have been aggressively cut, and they are expected to remain stable for the rest of this year, the report says.

However, Eckhold is predicting 5.4% house price growth next year.

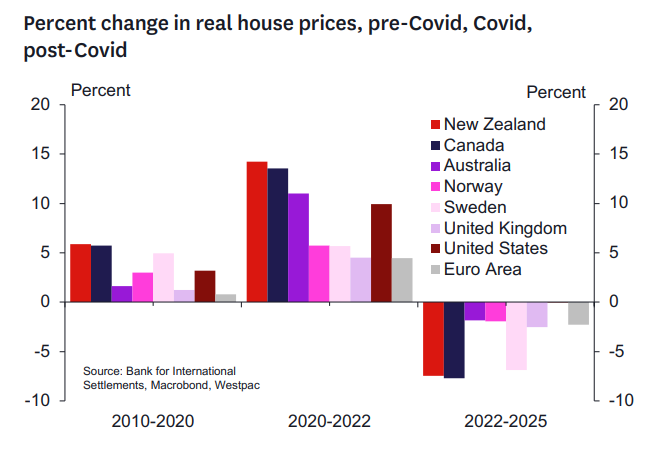

The report says house prices rose at a rapid clip through most of the period between the Global Financial Crisis and the onset of the Covid-19 pandemic.

"Real house prices rose at an astonishing 6% annual rate that decade," it says.

"Few other developed markets achieved such growth. Steadily lower interest rates combined with strong migrant-driven population growth to generate the uptrend in house prices," Eckhold says.

"Pre-Covid, the Official Cash Rate was cut by 75 basis points to 1.0% - during Covid, the OCR was cut by a further 75 basis points to 0.25%."

"In addition, the Reserve Bank undertook considerable quantitative easing, removed macroprudential restrictions on housing lending and issued forward guidance implying a long period of very low interest rates," the report says.

"These accommodative policy settings supercharged a housing market that already had significant momentum," Eckhold says.

During the Covid period New Zealanders plunged into mortgage debt boots and all, with the value of new mortgages taken out peaking at an annual rate of about $100 billion as banks shoveled money out the door. In February 2021 Shayne Elliott, CEO of Australia's ANZ Group, parent of NZ's biggest bank ANZ NZ, highlighted record volumes in ANZ's NZ home loans business saying; "we’ve been really run off our feet there in terms of supporting Kiwis into homes."

Westpac is NZ's third biggest home lender with total loans of $69.6 billion at June 30.

Eckhold says NZ continued to outperform other markets in real terms through Covid, resulting in very high house prices.

"Investors saw value in housing at such low interest rates and behaved as if interest rates would be very low for a very long time."

"The result was a severe and unsustainable spike in house prices in both real and nominal terms, but the fundamentals underlying these price rises were not sustainable, as ultimately, inflation and interest rates rose and house prices fell," the report says.

"Countries that were most overvalued - New Zealand and Canada especially - fell by the most, so that much of the increase in real prices that occurred over the 2020-21 period was eventually unwound," it says.

"Since 2023 house prices in New Zealand have been stable on a nominal basis and falling further on a real basis."

"This year to date we have seen no growth in prices at the national level, albeit with some variation across the country... the weakness in house prices is more prevalent in the largest urban areas which are not directly exposed to improvements in export returns driven by strong commodity prices," says Eckhold.

"While house sales have increased over the past year and the median time to sell has been stable to falling, new housing demand has been balanced by increasing supply - including that provided by new construction - so that the inventory of unsold homes has remained at around a decade high."

"Given the supply in the market, there has been little need for buyers to bid prices higher," the report says.

Next year Eckhold says Westpac's economists expect a gradual lift in momentum will see house price growth of about 5.4%.

"Demand for both owner-occupier and investor housing should strengthen as the broadening economic recovery, and crucially an upturn in the labour market, encourages the formation of new households, including migrant households. Over time, this should eat into the current stock of unsold inventory and so reduce the current downward pressure on real house prices."

The comment stream on this article is now closed.

You can read Eckhold's full report here.

17 Comments

Graph shows we lead the stupidity up and close second on the way down. Sad.

And how stable the Euro zone. Perhaps they think there is a real economy beyond property.

I tend to agree, prices probably will increase next year. Its a tough call though, lots of factors pushing in both directions.

Westpac's copy and paste from this time last year.

More total BS, from the selfishly interested Banking industry!

With all their recent mortgages all dangerously under water.....THEY NEED HOUSIING TO TURN POSITIVE!

Not happening, maybe a stabilisation of the NZ Housing crash, come 2027 2028.

Guy who has called gains every year, once again calls for gains...

I am assuming most in NZ have smartened up by now and ignore bank economist house price forecasts.

Hard to call gains while we are still dropping, try calling the bottom first perhaps?

Indeed. Business Model of lending to oblivion requires capital gains to make it all stack up. We need outer bonuses back!!!

Westpac's disclaimer on this stuff is rambling. Much to get through before the final sentence - which is all you need to know.

This material contains general commentary, and market colour. The material does not constitute investment advice. We recommend that you seek your own independent legal or financial advice before proceeding with any investment decision. This information has been prepared without taking account of your objectives, financial situation or needs. This material may contain material provided by third parties. While such material is published with the necessary permission none of Westpac or its related entities accepts any responsibility for the accuracy or completeness of any such material. Although we have made every effort to ensure the information is free from error, none of Westpac or its related entities warrants the accuracy, adequacy or completeness of the information, or otherwise endorses it in any way. Except where contrary to law, Westpac and its related entities intend by this notice to exclude liability for the information. The information is subject to change without notice and none of Westpac or its related entities is under any obligation to update the information or correct any inaccuracy which may become apparent at a later date. The information contained in this material does not constitute an offer, a solicitation of an offer, or an inducement to subscribe for, purchase or sell any financial instrument or to enter a legally binding contract. Past performance is not a reliable indicator of future performance. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The ultimate outcomes may differ substantially from these forecasts.

From where do you keep pulling these numbers Kelly? Is it a random roll of the dice or working backward from profits they hope to make?

I wonder if they have the revision figures already on standby, up in peak summertime then way down again as winter nears.

Economic models are like sausages, if you saw what when into them, you would not consume them.

Westpac economists - spring into life end of 2024... sorry early 2025... sorry mid 2025... sorry late 2025, ... sorry 2026. They'll get it right eventually

WGTN down 30% Auckland down 20% and not one bank economist has yet called a drop anywhere.

FFS sheeple they (bank economists) are never going to tell you (the public). Westpac interest rate trading desk will not be positioned for rates going up anytime soon on the back of a booming housing market in 2026.

Part of investing is knowing who to ignore. These guys are as biased as Property apprentice and OneRoof

100% ITG!

Pay attention to bankster economists (yes economic with truth) at your peril.

Agreed. The prop funded media have done their best to paper of the cracks of crashing truth. When its a vast chasm, the paper and bog of misdirection collapses with house prices.

Popcorn.

NZME totally biased due to RE advertising revenue, we have in the last month even Liam calls crash and the honest situation is becoming apparent to all, prices are dropping as we move to Depression, about prices lost opportunities negitive equity realities and the loss of Ponzi credit creation killing our construction industry and associated manufacturing.

Due to the massive over allocation of property to most NZers investment portfolio i think Acceptance is a late 2026/27 emotion....

We are all Depressed that things are so bad right now.

Another milk-aging prediction. How many economists even talk about the elephant in the room (tariffs largest in almost a century) and the tsunami of layoffs and debt defaults coming with them? Bet they will discover these "unexpected shocks" after the fact.

One must not underestimate the power of positive thought

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.