By Bernard Hickey

Now that the Reserve Bank has issued its half yearly Financial Stability Report and the European crisis has kicked off again it's worth revisiting the decision about whether to stay floating or to fix your mortgage. A fresh round of short term fixed mortgage rate cuts by the banks has also prompted a fresh look.

The short story is some bank economists have said in recent months now is a good time to fix because 2-3 year fixed mortgage rates offer good value compared to rises they see in floating mortgage rates over the next couple of years. Although in late April and early May those same economists backed off their 'fix now' calls because the European crisis worsened and the prospects for an Official Cash Rate cut increased.

Some economists and the Reserve Bank's own forecasts suggest, that floating may be the marginally cheaper option and allows any borrower to take advantage of any possible (and now more likely) cuts in official interest rates. My view, for what it's worth, is that rates stay lower for longer and floating makes marginally more sense.

Everyone is different though, so it's worth running through the pros and cons of fixing vs floating and look in depth at the various factors at play. It's also worth spending some time on it. As I'll show lower down, it's a decision that could save (or cost) you thousands of dollars over the next couple of years. Here's our Fixed vs Floating calculator to help.

Firstly, let's look at what the 'ref' at the Reserve Bank has said recently and what the latest economic and financial signals are saying.

The Reserve Bank substantially revised down its forecast track for interest rates in its March 8 statement, which was widely interpreted by economists and the financial markets as being 'dovish', which means more emphasised on keeping interest rates lower for longer. See our news report here. It didn't update that forecast in its April 26 statement, but suggested again it is no hurry to raise rates while the New Zealand dollar is so strong.

On March 8 the Reserve Bank held the Official Cash Rate (OCR) at a record-low 2.5% and forecast the 90 day bill rate would peak at around 3.6% by the first quarter of 2015, which implies a peak for the OCR of around 3.25% to 3.5%. This is a reduction of 0.4% or 40 basis points in the Reserve Bank's forecast peak from its December quarter forecast. At some points in the forecast track (early to mid 2013), it represents a 0.7% or 70 basis point fall in the bank's forecast in just three months.

This substantial lowering of the forecast track surprised a few people and triggered a slight (if shortlived) fall in wholesale interest rates and the New Zealand dollar. Reserve Bank Governor Alan Bollard was highly critical of the high New Zealand dollar, given recent falls in commodity prices, but that's another story. He even suggested he might cut the OCR if the currency kept rising.

There's a couple of reasons for the Reserve Bank's more dovish view, which is important because the OCR sets the base for all interest rates and is closely connected to floating mortgage rates. The central bank said the high New Zealand dollar was holding down inflation and the recessionary forces of the last four years were keeping inflationary expectations down too.

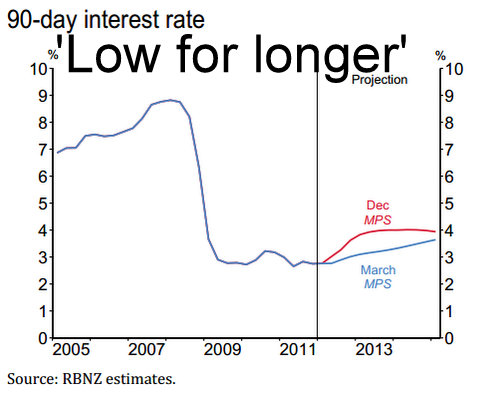

The Reserve Bank's chart here of its forecast track for the 90 day bill rate, which is typically around 30 basis points above the OCR, tells the story.

So the Reserve Bank is forecasting a rise (the blue line), but it's very slow and not much at all. If the Reserve Bank's forecast now actually turns out to be fact, then floating mortgage customers would see their rates rise very slowly to a peak of around 6.5% by 2015 from around 5.7% now. Given 3 year fixed mortgage rates are currently around 6.1%, it's not obvious that fixing is a better deal, assuming the Reserve Bank is right. See our bank mortgage rate comparison page here.

There is a way to test the various scenarios and work out which option is cheaper (although cheapness is not the only factor worth thinking about for many people).

There is a calculator

We have a calculator here that allows you to test which rate is cheaper, depending on three different interest rate scenarios. Click here to go to the calculator.

There are three different rate scenarios. A is the high one with an OCR peak of almost 4%, B is the medium one, which is in line with the Reserve Bank's latest forecast track above, and C is the low one, which implies no hikes until early 2014.

Try it out to see which option is cheaper for you, depending on your rates view. My view is that the OCR stays lower for longer, which means my bank floating rate of 5.4% (I hammered my bank down via a broker) is better than my bank's 2 year fixed mortgage offer of 5.8% using option C (low) to the tune of NZ$1,161 on a NZ$200,000 mortgage. I would be NZ$1072 worse off off fixing if rates rose on the high track (option A). I'd be NZ$1,117worse off with the middle option B.

A simple money calculation isn't everything though. Some people put a high value on knowing exactly what their mortgage payments are going to be for the next two years because, perhaps, they have a fixed income or are very nervous about a sharp rise in rates. They may see paying slightly more for a fixed mortgage as a bit like an insurance payment.

Others may want to stay floating because they really believe interest rates will be cut again and because they don't want to be stuck fixing and have to pay an exit fee if rates do fall. The most recent memories for some people are having to break their mortgages and pay big break fees (or finding it unaffordable to do so) during 2009 and 2010. Others have longer memories of being stung with big increases in floating mortgage rates as the OCR was hiked from 5% to 8.25% between early 2004 and mid 2007. Really old people remember the 20% plus rates of the mid 1980s. I'm not that old. ;)

Everyone has different appetites for those sorts of risks about paying more or missing out on paying less, and different views about where interest rates will go. Those are the main things to consider when fixing or floating.

More than 60% of New Zealand's mortgage lending is now on floating rates, which is a record high and a complete turn-around from before 2008. The decision for many now is when to fix.

The bank economists' views

Westpac's Dominick Stephens changed his view on fixed vs floating in late April, saying that floating now looked more attractive than fixing. See Gareth Vaughan's April 27 article here.

Back in early March he pointed to the risk of quite fast and steep increases in the Official Cash Rate through 2013 and said fixed rates looked good value.

But by late April after the worsening of the local and global economic outlook and a change in the outlook for the OCR he switched back.

Here's his latest comment on the OCR outlook in his April 26 note:

Markets are now pricing in a 40% chance of an OCR cut before the end of RBNZ Governor Bollard’s term in September. We broadly agree with the market’s assessment of risks; while we don’t believe that a rate cut would be eff ective or appropriate, it has to be regarded as a meaningful risk in the near term. Whether the OCR is cut this year or not, our expectation is for an extensive series of OCR hikes over the 2013-2015 period. Interest rates remain well below neutral levels, and the impending construction boom is likely to be more infl ationary than the RBNZ is conceding (this will be more of a driving force in later years than it will be this year).

ASB's economists now expect the Reserve Bank to wait until March next year before increasing interest rates and Jane Turner said in a May 16 note is that "some fixed rates are now below or similar to floating rates, offering a window of opportunity (to fix)"

The economic recovery remains gradual and inflation pressures are currently subdued. Recent economic developments highlight the downside risks that remain to the outlook in the near term, and we expect the RBNZ to leave to OCR unchanged at 2.5% until March 2013. Nonetheless, we continue to expect the economy to recover which, along with the Canterbury rebuild, will underpin a swift pick up in inflation pressures. As a result, we expect the RBNZ will need to steadily increase the OCR over 2013 and 2014, returning the OCR to 4% by mid-2014.

For borrowers, this means that floating mortgage rates are likely to remain at very low levels for the rest of the year, although borrowers do need to be prepared for rising interest rates from 2013. A combination of domestic and offshore events has seen the market start to price in interest cuts. This has reduced domestic wholesale funding costs, and lowered some fixed-term mortgage rates. In some cases these are lower or at similar levels as the floating mortgage rate. Our view is these declines may not be sustained unless the RBNZ follows through, and provides a window of opportunity for those borrowers that prefer certainty to protect themselves against further interest rate increases.

ANZ National's Cameron Bagrie sees the economy in a 'grumpy growth' mode that means the Reserve Bank is likely to hold the OCR for some time and may even cut rates before the end of the year. He leans towards staying floating.

Here is ANZ National's latest comment on May 3 on where the OCR might go:

This is the third “major data” downward surprise for the RBNZ since the March MPS. While the hurdle remains high, it is now easier to articulate scenarios involving rate cuts. The probability of a rate cut is low, but rising, and ultimately depends crucially on global events and their impact on New Zealand.

Here's ANZ National's latest views on borrowing strategy in its May 11 note:

The big picture remains one of interest rates remaining lower for longer, and we still remain of the view that borrowers have time on their side. Some say interest rates have moved to price in too much easing, and there could be some truth to that. But with no catalyst for a sustained move higher in sight, we prefer to go with the flow, taking relief from lower rates. Broadly speaking, we still prefer to be more exposed to floating than fixed, but with rate cuts a possibility rather than the central scenario, given they are priced in, it makes sense to “average in” to fixed by gradually adding to fixed cover at current levels.

BNZ Chief Economist Tony Alexander said on February 16 that it was time to fix. Here's his view as of May 10:

Stay floating or fix three years at 6.15%. It all depends upon one’s risk tolerance. Thankfully, on February 16 when I wrote here that I would move from floating to fixed the justification was not an expectation of a rise in interest rates but simply the small gap between floating and fixing.

To whit...“The gap between floating and fixing for three years has declined to only 0.41% from 1.4% three months ago and is now the lowest since March 2009. Personally I would take the three year rate because I like certainty and the 0.41% cost is very small. Most people however seem to be very comfortable sitting floating so if they change will probably only jump to the two year rate. The chances are however that with little discussion in the media regarding interest rate rises and picking low points, very few people will in fact shift away from floating. This will likely happen even though it is a complete gimmee because the chances of either the two year rate or floating rates falling again this year are low (though not zero given Europe uncertainty) and our official view is that the Reserve Bank will start tightening monetary policy before the end of the year."

The only change I would make in the February 16 statement would be to note more explicitly the always high probability that monetary policy tightens in 2013 and not anytime this year.

Bernard Hickey's view

For what it's worth, I think the Reserve Bank is likely to keep the OCR low for longer and I'm closer to the RBNZ's view than the economists' views. I still think there is a risk (now increasing) of a blow-up in Europe's financial markets that could even force the Reserve Bank to cut interest rates again.

There are plenty of structural deflationary risks in the global economy as consumers in the big economies struggle to find well paid jobs and companies look to outsource work in both manufacturing and services to lower paid emerging economies such as India and China. This tends to suppress wages and prices, which in turn encourages savings and keeps interest rates low.

At the same time, there is a mountain of debt that has to be worked off (or restructured). Studies of previous financial crises show that these mountains of debt tend to suppress growth rates and inflation rates (and therefore interest rates) for many, many years after a crisis.

That means I'm personally staying floating, even though the two and three year fixed rates appear reasonably attractive if interest rates rise in the same way they have in previous recoveries. I think some structural things have changed in the global economy that mean interest rates are likely to be suppressed for some time to come.

But my view is just one view and there are plenty of others, including the views of the financial markets (which are often different to those of economists).

Those views are often expressed in Wholesale interest rates known as 'Swap rates'. Check out our interactive chart below. They rose quite sharply in the second half of February as markets calmed down about the problems in Europe, but have dropped again through April and early May as the Greek crisis reappeared and election results endangered Europe's austerity strategy.

The rise in swap rates in late February and early March encouraged some to think the worst was over and that interest rates were about to rise sharply again, and therefore now was the time to fix. Some reversed that view in early May though because of the renewed European fears and higher New Zealand unemployment rates.

* There was caveat to all of this. As Dominick Stephens has pointed out to me, if Europe were to go horribly, horribly pear shaped and that signficantly increased the foreign debt funding costs for New Zealand's banks, those banks may pass on those costs to floating mortgage borrowers in the form of higher rates. That is possible in the worst possible scenario. The Reserve Bank has said in the past though that it would help out by cutting the OCR in case that happened, to offset those higher funding costs. We'll see.

The ultimate worst case scenario would be if foreign investors completely lost confidence in New Zealand and started treating us like Greece, slashing our credit rating and pushing up our interest rates dramatically. I think this is very, very unlikely.

(Updated on May 16 with latest from Reserve Bank and markets action, also ASB's view to fix now)

No chart with that title exists.

40 Comments

You can ignore the big banks published fixed rates as they are all ultra hungry to do deals for example published fixed rate 6.1% - offered rate 5.7% and that's the 3 year term.

They are even doing deals on their published variable rates as low as 5.2%

I find Dr Bollard's comments that the high exchange rate is holding down inflation interesting....the reality is it isnt........its more of a cushion.....or a hedge......effect.

Im trying to get my head around my thought here so bear with me.....If you accept Peak oil then the price of oil is going up because of scarcity v demand....this isnt inflation strictly speaking, its an extra cost or a tax on production.

The problem is the its dampening our already lack luster economy and threatening to put us into a recession. So Dr Bollard doesnt need to raise the OCR to dampen a boom which is how inflation normally raises its ugly head....today raising the OCR would be a double whammy.....and lowering it I think almost immaterial.....ie the cost of energy as a % of our economy now significantly outweighs anything Dr B can do with monetary policy IMHO.....he and the RBs around the world are now effectively powerless....By this I mean every time there is a wiff of the ned to raise the OCR the cost of energy will do his work for him.....ie slow the economy down...

Hence my view is floating today is the right way to go......or fix for a short term......I dont think the OCR will ever rise much again......there has been a paradym shift....

regards

Steven, you're right about oil and other factors stemming the NZ and world economies. Lowering the OCR would help for sure but the effects of oil and other commodity price rises quickly erode the cash injection making a sustained rebound difficult.Such inflationary drag-weights only add to the recovery woes as they impact directly in peoples everday lives.In light of NZ and every other country having to get their sovereign debt issues in order a consumer led rebound from within is still unlikely.

cheers Naive

I've been expecting another GFC (or whatever the next financial disaster scenario is called) for the last few years (even locked in my mortgage for 5 years) The fact is, as long central bankers worldwide can man-handle rates lower it's business as usual. That leaves time to pay down debt asap. I don't think anyone can predict when is a good time to lock in rates because "the market can remain irrational longer than you can stay solvent"

The GOV doesn't want a lower NZD because that would = higher living costs and a percieved lower standard of living. As long as they can borrow overseas with good credit rating, run budget deficits, and continue to rein over "good times" they will.

John key doesn't care that he's using NZ's platinum mastercard because he gets to enjoy the benefits now and the next PM can worry about the shocking bill that arrives when interest rates are throught the roof and the NZD is worth half as much.

Whatever the RBNZ says it is prudent to do the opposite. While they are slightly more accurate that the treasury they are still less accurate than most fortune tellers.

Also take note that the RBA is looking at cutting their rates. Unfortunately, the future ins't rosy for this part of the world !

look at Greece

Jacob

As I live in Greece I can tell you that what is happening here is insane.

The economy choked by taxation.

For many people, their tax bill is above their total income. Fuel is now €1.80 (~$9 USD per gallon). VAT gone to 23%, Road Tax for a big car can be as much as €1700, Property taxes are 2 average monthly salaries. Healthy Business are refused loans and go bust. National insurance for many has doubled, and every 2-3 months there is an “emergency tax bill” usually a whole average salary. Business are taxes 80% of *next* year’s tax bill

All these are causing a MAJOR recession. No one is investing anything as they can hardly buy the essentials (milk and bread), consumption has declined, car sales are 1/8th of some years ago, properties stay vacant..

The EU/ECB/IMF programme is just insane, it is not addressing at all the real problems, a bloated and inefficient public sector, useless public services, but they are attacking the private sector in every possible way.

It will end-up in tears. Argentina is the good scenario. The bad scenario is Libya with Politicians lynched on the streets. Tar and Feathers are coming

http://hat4uk.wordpress.com/

New data released today show that more 16-24 year old Greeks are now unemployed than employed. This stark fact makes a nonsense of the Troika’s EU austerity programme.

A good rule of thumb when considering the advise of your financial expert: Did they see the 2008 crises coming? If not, I'd suggest that you ask why you should be comfortable with their opinion today.

Accross Europe and the US there is a major consumer and banking deleveraging going on. Consumer demand will not and cannot get back to pre 2007 levels. Those days were a bubble, fueled by cheap and easy credit. The concumer demand gap is being filled, accross much of the world, by Government debt and as bond costs go up central banks print. This scenario will last till a crises stops it, maybe Greece, Portugal, Spain maybe a war with Iran.

Its the time to own hard assets that firstly protect your capital and secondly give a better than inflation yeild. Inflation will be around in spades, even through the deleveraging, due to, debased currencies, aprticulary the worlds reserve currency. Own an asset that is driven by a trend that politicians can't interfair with. Laslty you need to buy the asset at the right price, in other words, buy cheap.

Farmland is one of these assets, but buy in a country where land is cheap, Eastern Europe, Africa, parts of Australia. I particularly like this one. http://j.mp/xU0SaK

When you have a bubble fueled by "cheap and easy" credit, what happens when you add "cheaper and easier" credit? That is the solution on offer today.

Definatly buy things that can't be printed, and have a positive yield. Overseas is great if you can speak the language, and feel secure (or if you don't mind the aussies). I've looked overseas, but I always seem to find an equally good deal right here.

What are the taxes like in Lithuainia? That area is inclined to rain and never stop or go dry and never rain, thats just going on my Polish experience. I think you would be better waiting for the wheat market to correct which it always does (no this time is not different) there is 700,000 extra hectares coming into production in the EU, as they have got rid of set aside, France was cheap but then there is the tax man. Alberta is cheap and gas is cheap there, check but i think its about 2.5k a hectare and my friends say its going to fall to 1.7k a hectare. South of Calgary is bloody cold but some areas are Ok, just dont live there.

Id be carefull in the old eastern block its mostly run by Mafia and the return is %50 of net profit and those management boys like to take most of the money. In fact reading again Id run a mile, better to just own tradeable shares in an ag company, I wouldn't put all my eggs in one basket.

My suggestion would be and your getting as good as I give free :-) get a farm in Aussie and lease it to a local farmer as a 50/50 deal like sharefarming here, farmers are eternal optimists and jump at the best possible outcome and bet the farm on it. I suggest the Perth area they get droughts but they come in bunches of 7 so buy at the end of the 7th drought and you should be right mate. %10 of Aussie farmers are broke probably the same as here but we dont know it yet. Go to parts of the world where they play cricket, fair play is such a great thing to your teach kids, and it helps in business too.

Andrewj I really feel for the place, that is the saddest of pictures, given what modern Europe under the protective umbrella of the euro is meant to look like. Reminds me of those dark days when Argentinians were suffucating under a mountain of debt and people would go to buy a loaf of bread with a crate full of peso notes strapped to the back of a bicycle! You're right it's not going to end well, in fact it's going to turn ugly, and could be the spark of the Aegean tinderbox.That young demography inspired by a traditionally riotist socialist student body is going to challenge the austerity measures to breaking point, just a question of when. Just as well the only oil Greece produces comes from olives.

sadly Naive

Is it easy to negotiate my variable rate with my current lender?

Any tips on how to do this?

Tell them you are prepared to take all of your business elsewhere - and mean it. If your business means enough to them, they will budge. We got our floating rate with ASB down to 5.5% without much effort.

I am sceptical about the 5.7% three-year fixed rate offer mentioned above....

Bozeman that could be within the realms of possibility, it depends on how willing one is to hold one's ground in negotiating. Even with hard noses like the BNZ I've managed over the years to get them down to levels they weren't really comfortable with, but rather than lose my accounts they were prepared to bend - of course they never lose, the maths are on their side always - but everyone's motto should be nothing ventured nothing gained. Guess where I'll be going on Monday! Given the mood of the economy as expressed by El Supremo on Thursday I think it's time I tested the mood of my local bank manager again!!

cheers, positively Naive

The money lenders of London have honed there skill over the last 1000 years, fix or float, who cares, they win. Answer, get out of debt, the scales tip in your favor, game over, happy days.

The scales tip...yes but then you become the lender!

Sadly this pathway to a better economy was not taken by any NZ govt and once we became entangled in the benefit pork slicing vote buying party political scam behaviour....that was the end of the road...one recognised by the banks as promising them a fat profits future as stupid NZ tottered like a drunk down the road to greater debt.

Now we have govt after govt determined to protect the banks fat profits...the peasant Kiwi are just fodder in this game....the wealth of the country is stipped away year by year...NZ is the banking farm....fabulous tale to help the next generation understand why they will spend the rest of their lives working for the banks.

Well done all the idiot gutless wonders who parked their fat rear ends in the Beehive for the last 50 years...knighthoods to you all....

Steady on there Wolly, you don't want to blow a fofoo valve, but I must say I am on your side taking shots at the pork slicing shinny suited bankers, that through constant scoffing at the trough are about to turn on each other. Now that will be worth paying a few bob for a front seat, tho it may well turn into a blood sport. Or are they too cunning for that?

No RiF you got the wrong end of the banknote...the pork slicing swine are the liars who buy their way into govt office in NZ...promising whatever they have to...the fools and idiots are the Kiwi who go after the pork....the banks are not in that picture...they simply create credit without any controls...they blow the bubbles with the help of the idiot greedy Kiwi and stupid govts.

There is no escape for the economy from this debt trap and dependence on credit.....the banks know this....Bollard knows it....the fools in the Beehive think they are running the show!...morons.

It is for each individual to wake up and avoid borrowing even if that means going without the goodies the drugs will buy. Some will make it through without becoming serfs...most will not.

Just been offered 5% floating if I change bank and my current bank not able to match it!

That's good. Until now the best I had heard was 5.14. One bank offered 5.25 but at the moment I am asking another bank to come back with a four in front of it... they already knew about the 5.14 before I asked them for less.

Can you disclose your lender? is it one of the big four like my two?

President of Property

POP

Ive been floating at 5% with one of the big 4 since last September. Have recently convinced one of the NZ owned banks to do the same for the business we have with them.

Might take some arm twisting but they will do it. They are awash with cash at the moment.

Ivan

It is safe to say I'm paying off a mortgage. I personally do like lower bank mortgage rates.

But I'd also like banks to pay higher term deposit rates. That means lower profits for the banks.

I've argued for that for some time. One way would be for the RBNZ to force the banks to get more of their funding from term depositors. I've argued for that.

It doesn't make me popular with the banks, despite what our commentators say about bank advertisers.

This site is all about the interests of our readers, who are term depositors and mortgage borrowers. We aim to provide useful information and news for our readers, rather than our advertisers. They do, however, want to be where the crowd of term depositors and borrowers are. We get around 200,000 visitors a month.

That is Interest.co.nz

cheers

Bernard

WHAT.. He's being paid by the banks. Look at interest.co.nz.. it's full of bank ads. may be he's having a feast at the hands that feed

Excellent ..... we'll organise a shin-dig for all those who believe in the master gloomsteriser , and who've profited from his advice ...... now to find a suitable venue for the party .......

..... I wonder if Telecom have a 'phone booth they'll rent out ?

wear black

Dream on - he has been way off the mark on 'deflation' of property.

However I agree - thanks to Bernard for attacking the bank profits via encouraging clients to bargain hard!

Again you seem to be saying oh Ive jumped off a cliff but it isnt hurting....my reply is, sure wait til the bottom.

If you go back to the original posts I think the discusion was around the long term fundimentals, ie with BBs retiring, huge debt etc it is very likely that the housing bubble will deflate. Certainly if you look at the effect of BBs over their lifetime so far they primed up the markets due to a) numbers and b) earnings, c) spending per BB, all of which can never be repeated....due to Peak Oil...

For instance,

1) They have bought shares en mass either directly or through pension schemes pushing demand up....as they sell or draw private pensions this alone reverses.

2) Consumerism, they are a big market segment that will be switching from high earnings and spends to far less, retail then just has to shrink.

3) Housing see 1).

So as always this time its different....

regards

come on steven, if you are going to go on about BB's retiring, you haven't yet twigged that that will be counter-balanced by going out and enticing more immigrants in.

IF NZ was aiming at a sustainable population around 4 million level THEN your argument MIGHT hold water.

As both Labour & National appear wed to the Growth is Good lobby, and AndrewJ's report of DonKey's view that there should be twice as many people in NZ sort of backs that up, I am very doubtful your views on BB's retiring will influence anything.

As Wolly used to say. Got to keep Porking the Property Market

just got off trade me property site

2 houses in same street for sale but completely different prices

house A.rating value 300k asking price 269k

house B rating value 310k askingprice 355k

is there something wrong here ,surely they both can't be right

Its called "value added" puck up a cheap house Due for maintance and a bit of renivation, kitchen bathroom...spend 25 /35K on it turn it over 6 weeks or so later...Around 15% of sales for the last 4 to 6 month at least have been like this.

...and deposit rates would also have to be lower by a similar amount. You continue to present a one-sided view of the market.

Lending margins are larger than they were pre-GFC. Deposit margins are much lower. As an investor I'm quite happy that borrowers are paying for my higher (than they should be relative to wholesale rates) deposit rates.

Yeah right, we are tame as!! We are Kiwis (bird that can't flight and a fragile beek) we aren't exactly Greeks

Bernard very positive about housing in that video clip. Should see sub 5% fixed for 5 years within a matter of months and that can only push house prices in one direction - up!

Hey, I'm not really that old - even though I can remember our first mortgage at 20.5% .... 1987. Makes the discussion over 5 or 6% currenty small potatoes I guess.

Fsacinating feedback and comments. But I am so distracted with the poor level of some of your spelling skills. Surely if you want to be taken seriously you should be able to at least spell properly. Or is it those danged smartphone keyboards causing the problem!

If you are so small minded that a typo or not so hot english means you wont take the info or feedback as credible so make the wrong decision, whos problem is that?

regards

.... more right you is , steven ...... very especially so .......you're English is good enough for us what is here , gooder even ....

yeah don't worry too much there Stevo......I get the fat finger problems too, I mean aside from my obvious dyslexia and complete inability to spell...punctuate...form a proper sentence...the message still gets across......and by Dog I'm KO with that.

If the above swap rate table is correct then the Banks are rorting us - shame the Govt can't (or dont have the balls to)legislate a max margin of 2.75% etc. I wish the Banks were more inventive in their mortgage rates and reward those of us who have worked hard and have paid down debt and have LVR less than 50%!!

Great idea, Keene1...or a sliding scale that starts on day1 of your mortgage, maybe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.