By Bernard Hickey

After years of being flat as a pancake, the outlook for interest rates appears to be turning.

There's great hope by some that this could the year of the 'great recovery' after the Global Financial Crisis (GFC), which would see economic growth surge and interest rates rise.

Yet, as in previous years, others point out many of the problems exposed in the GFC have not been solved and growth is unlikely to surge.

The year appeared to begin well with signs of a strong recovery in business confidence in New Zealand and relatively calm financial markets in America and Europe.

If this followed through into a burst of investment, employment and economic activity that would put upward pressure on interest rates, making fixing more attractive.

However, the New Zealand dollar remains persistently high, which is dragging down on inflationary pressures and there's still plenty of potential for hiccups overseas to stall our rebound.

Europe is in recession with few signs of life and America is sputtering along with periodic political and fiscal crises that have handicapped investment plans.

The net result of all this is the Official Cash Rate (OCR) is not expected to rise until late in 2013 or early 2014 and has been at a record low 2.5% for most of the last 5 years.

In previous years I was firmly in the floating camp because I saw interest rates staying low or even falling further because of the stubbornly weak global economy and very low inflation. However, in recent months my views have started to shift towards fixing. This largely followed the appointment of new Reserve Bank Governor Graeme Wheeler in September last year and the surge in the Auckland housing market through 2012 and into 2013.

The new Reserve Bank Governor seems to be taking an orthodox approach to policy and interest rates, which means he is less likely to cut. He is also starting to look at the surge in the housing market and appears reluctant to use alternative tools to control house price inflation (such as a limit on loan to value ratios) other than the blunt instrument of the OCR. This hawkishness on inflation and orthodoxy on monetary policy makes a rate hike late in 2013 more and more likely.

The Reserve Bank has a big dilemma at the moment. The economy is subdued and inflation is below the Reserve Bank's 1-3% target range. All other things being equal, there'd be a good case for the Reserve Bank to cut the OCR, which should in turn drag floating rates lower and make floating more attractive than fixing. But house prices are taking off again and any OCR cut risks pouring yet more petrol on the fire of record low interest rates under house prices, particularly in Auckland and Christchurch.

One way for the Reserve Bank to get around this dilemma would be to use other tools to try to control the housing market, incluing limits on Loan to Value Ratios (LVRs). Other central banks and bank regulators in Israel, Canada, Hong Kong and Singapore have used such LVR limits, but Wheeler said early in November and again in December he would not use a LVR limit yet, even if he had it. See the full article and video here.

That means Wheeler is more likely to use the blunt instrument of the OCR to try to keep inflation around the 2% mark he has agreed to target in his own Policy Targets Agreement. If he worries about the housing market getting too hot then the one way (in his view) to knock it on the head is to hike the OCR. That's why I would tend towards floating half and fixing half of my mortgage in coming months, rather than floating it all. (I have actually sold my house and cleared my mortgage, but that's another story).

This is far from specific financial advice and everyone is different, so it's worth running through the pros and cons of fixing vs floating and looking in depth at the various factors at play. It's also worth spending some time on it. Don't blindly follow my or anyone else's view. This article is aimed at providing useful information in an accessible way to help you make a big decision. As I'll show lower down, it's a decision that could save (or cost) you thousands of dollars over the next couple of years. Here's our Fixed vs Floating calculator to help.

Also, there are many different views, and I've included those views of other economists below.

What the economy is doing and what the RBNZ is saying

Firstly, let's look at what the 'ref' at the Reserve Bank has said recently and what the latest economic and financial signals are saying.

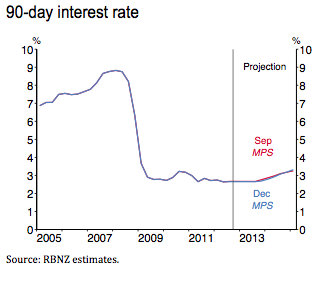

The Reserve Bank's chart below is from its December 2012 Monetary Policy Statement of its forecast track for the 90 day bill rate, which is typically around 30 basis points above the Official Cash Rate (OCR), tells the story.

The blue line shown is its December forecast with the OCR peaking at around 3%. The red line shown is its September forecast. These forecasts have been dropping for at least a year.

Wheeler said in the Reserve Bank's December 6 New Zealand's economic growth outlook had slowed, but was still expected to recover to around 2.5-3%. He said he was watching inflation closely, particularly the housing market in Auckland, but saw no need to change the OCR from 2.5%. On January 31 he repeated that it was appropriate to keep the OCR at 2.5%.

So the Reserve Bank is forecasting a rise (the blue line), but it's very slow and not much at all. If the Reserve Bank's forecast now actually turns out to be fact, then floating mortgage customers would see their advertised floating rates of around 5.7% rise very slowly to a peak of around 6.2% by the end of 2014. Although it's worth remembering that those customers with plenty of equity and good repayment records can push their banks for better deals at the moment of around 5% to 5.2%.

Those in competitive situations would see their floating rates rise to around 5.7% by the end of 2014 in this scenario. Currently advertised 18 month-2 year rates are around 5% to 5.5%, which would mean you'd pay more for the first 6-12 months or so and then less in the second 12 months.

Fixed rates tend to be more closely linked to wholesale 'swap' rates than the OCR. Swaps rates fell broadly through 2012 on increasing fears about a global slowdown and a slow rebuild in Christchurch, but they have risen around half a percentage point in early 2013 on hopes for recovery and relative stability on global markets. Luckily for borrowers though, banks' funding costs on international markets have dropped so the net effect is fixed mortgage rates haven't risen.

There is a way to test the various scenarios and work out which option is cheaper (although cheapness is not the only factor worth thinking about for many people).

There is a calculator

We have a calculator here that allows you to test which rate is cheaper, depending on three different interest rate scenarios. Click here to go to the calculator.

There are three different rate scenarios. A is the high one with an OCR peak of almost 3.5%, B is the medium one, which is in line with market expectations for flat rates and then a rise to 3% by mid 2014, and C is the low one, which implies flat rates through to mid 2014.

Try it out to see which option is cheaper for you, depending on your rates view.

A simple money calculation isn't everything though. Some people put a high value on knowing exactly what their mortgage payments are going to be for the next two years because, perhaps, they have a fixed income or are very nervous about a sharp rise in rates. They may see paying slightly more for a fixed mortgage as a bit like an insurance payment that helps them sleep at night.

Others may want to stay floating because they really believe interest rates will be cut again or not rise, and because they don't want to be stuck fixing and have to pay an exit fee if rates do fall. The most recent memories for some people are having to break their mortgages and pay big break fees (or finding it unaffordable to do so) during 2009 and 2010. Others have longer memories of being stung with big increases in floating mortgage rates as the OCR was hiked from 5% to 8.25% between early 2004 and mid 2007. Really old people remember the 20% plus rates of the mid 1980s. I'm not that old. ;)

Everyone has different appetites for those sorts of risks about paying more or missing out on paying less, and different views about where interest rates will go. Those are the main things to consider when fixing or floating.

More than 50% of New Zealand's mortgage lending is now on floating rates, which is just below a record high and a complete turn-around from before 2008. Although there has been a slight move back to fixing in recent months. See Gareth Vaughan's article here. The decision for many now is when to fix.

What house prices are doing

House prices are rising quite quickly, particularly in Auckland and Christchurch, where chronic shortages of non-leaky and non-damaged buildings are being squeezed by demand from immigrants (both internal and from overseas) and those with insurance payouts. Record low interest rates with little prospect of fast rises is also fueling activity.

REINZ figures showed the national median house price was 4.3% higher in January from a year ago, while Auckland prices were up over 8%.

The Reserve Bank has said it is watching it closely, but has said so far it does not think the Auckland inflation is spreading in a way that would boost Consumer Price inflation beyond its current target band of 1-3%. It has also signalled its reluctance to use unorthodox alternative tools such as Loan to Value Ratio limits to slow the market. Although Governor Wheeler did mention in passing in a speech in late February that the housing market was 'over-heated', particularly in Auckland.

New house building is increasing, but remains less than needed in Auckland to keep up with demand. All those factors together suggest continued house price inflation in Auckland and Christchurch at least, however a weakening economic outlook and any rise in interest rates would take away some of that upward pressure.

What economists are saying

Westpac's Dominick Stephens expects the Reserve Bank to start hiking interest rates from September 2013 and eventually rise to 5.25% by 2016 as the Reserve Bank is forced to react to rising inflation pressures, particularly from the construction sector and the Christchurch rebuild. He thinks fixing is better than floating. Westpac forecasts house price inflation of 9% and 4% respectively over 2013 and 2014.

Fixing is likely to prove better value than floating over the next few years. Fixed-term rates out to two years are currently well below floating rates, while three-year and longer fixed rates are only slightly higher. Staying on floating would only be the better option if the RBNZ actually cut the OCR, and we regard that as fairly unlikely. Our view is that the OCR will stay on hold for now, and increase steadily from late 2013.

BNZ's Tony Alexander thinks interest rates are on hold this year, but sees house price inflation in Auckland accelerating and spreading to other centres. He prefers to sit floating, or to fix for one year.

The upturn in the housing cycle underway in New Zealand has only just started and it will probably run for another three years. It bears greatest resemblance to the 1990s cycle which was also led by Auckland, rather than the 2000s cycle which came out of the regions.In case you had not noticed there is the sniff of a fixed rate discounting war in the air. I’d be keeping an eye out for a nice low long term fixed rate and locking half of my mortgage into it while placing the other half in a mixture of floating and fixed rates out to two years. I’d not be doing this with the goal of minimising my interest rate cost because doing that requires faith in interest rate forecasts which have all been wrong for about five years. Instead I’d look at it from a near pure risk management perspective of giving myself time to adjust should interest rate surprise on the upside.

ASB's Nick Tuffley sees the Reserve Bank waiting until the March quarter of 2014 before raising interest rates. He also sees house prices continuing to rise.

Mortgage rates remain competitive, in part due to a reduction in bank funding costs. As such, many shorter-term rates are still below the floating rate, which allows borrowers to secure a lower interest rate despite the reduced prospect of an OCR cut. Medium-term fixed rates also offer excellent value, providing a good hedge against interest rate increases in the future.

ANZ's Cameron Bagrie sees interest rates on hold for some time and only limited house price rises. ANZ suggests a mix of shorter term fixed mortgages while waiting for a clearer view on rates.

The withdrawal of specials has also coincided with a rise in wholesale interest rates after the Reserve Bank’s December Monetary Policy Statement, which made it clear that rate cuts are off the agenda. With monetary policy likely to remain on hold for an extended period, and cuts unlikely, a mix of 6 month, 1 year and 2 year terms with a view to re-fixing them when they expire offers a good “rolling” balance of cost and certainty.

(Housing) activity metrics are continuing to recover from cyclical troughs, as historically low mortgage interest rates start to impact. This is now flowing through into prices, although the reasonably modest pick-up in borrowing and retail spending suggests no immediate signs of a widespread impact on consumer spending. There remain regional nuances, with the shortage of listings more acute in Auckland and Canterbury, which is contributing to faster price rises in Auckland in particular. While the supply response will help, we expect the high household debt overhang and subdued labour market backdrop to limit the uplift in property values over the next few years. If they don’t, and consumer spending picks up, higher interest rates and likely prudential policy changes look set to materialise.

Repeated undershooting of inflation will inflame the debate more as to whether we’ve seen a structural shift in the evolution of inflation. Inflation suppressants in the form of deleveraging (think credit growth below GDP) and a high NZD look set to be around for a while yet. Absent a city rebuild and perkiness across the housing market, the case for a lower OCR would be solid. However, both present risks to the medium-term outlook for inflation which carries the implication that the odds remain tilted towards the next move being up as opposed to down. However, we continue articulate the timing as being well down the track.

(Updated with economists' views on fixed vs floating, the OCR and house prices)

--------------------------------------------------------------------------------------------------------------------------

Mortgage choices involve making a significant financial decision so it often pays to get professional personalised advice. A Roost mortgage broker can be contacted by following this link »

--------------------------------------------------------------------------------------------------------------------------

No chart with that title exists.

20 Comments

Ah, Bernard, you always come round to my way of thinking in the end...

As I said some months back I would fix half long term (5 years) for the late 5s while you still can, and then leave the rest floating unless your bank offers a cheaper rate fixed for 6mths or 1 year.

So if you get 5.95% for 5 years, plus a 4.95% for 1 year, you're only paying 5.45% average which is better than most floating rates. Chances of missing out on long term rates going lower are slim, and if they do go lower in a year of two (highly unlikely) you can always fix the other half anyway.

But Bernard, with your new purchase, are you leading by example and building a new house rather than just creating more demand in Wellington?

It's your opportunity to increase housing supply and stimulate the economy all in one go...

Chris J

Interesting idea. Struggling to find some flat and unbuilt-on land close to the city.

In theory, though, our buying an existing home lifts the demand for housing and lifts prices above the level that makes home building economic for someone.

However, the main reluctance to build is all the work involved with designing and project managing etc. Just makes me tired thinking about it.

Curious though. Made me think

cheers

Bernard

Unfortunately you're in the wrong city if you want flat land close to town...

Wellington has a lot of very cheap land (old never built on titles) close in, however few are brave enough to take the sites on.

In theory a $60k section, plus a $150k budget build makes sense, but in reality the cost of getting driveway access to these types of sites make them unviable for any typical construction. (They could suit goat herders and mountain climbing hermits though?).

Still given there are not many decent houses on the market in Wellington Central under $600k and close in suburban sections (buildable ones) in Churton Park, Newlands or Johnsonville are available at $200k ish or maybe below, then a new build is probably economically viable, however most people find it all too hard, hence NZ's lack of new homes and the current "crisis"...

"5.45% average which is better than most floating rates"

5% float is not unheard of these days...

I think Bernard you miss the point and the point is that when our reserve bank prints $1:00 of physical currency, that when that $1:00 is deposited in a bank the bank can then print about $9:00 on to their balance sheet in the form of a loan.

At 5% interest per annum over tweenty years the loan returns $14:00 to the bank creating a $5:00 or about a 500% profit and return to the bank on the $1:00 deposite, all from the 'mirical' of accounting and slight of hand.

Now not only is there not the physical money in the ecconomy to repay the loan at the time the loan is created but the 'system' requires that the reserve bank must increase physical supply of the currency inline with the bank lending rate - so this means NZ will increase money supply by 500% over 20 years - this is garanteed.

Not printing money at the same or greater lavels than the bank lending rate = US, England, France, Portugal, Ireland, Spain all those currencies where the maths has currently run dry and the banking system has either failed or been bailed out.

So now that interest rates are what some would say 'artificially low', they can never sugnificantly increase because the money isn't there to pay the borrowings back at higher rates and the reserve bank will be forced to continue the spiral of credit expansion to keep our flawed financial system running badly at the current interest rates.

Spacific to NZ here we have a low income to house price value so with the credit expansion required to keep Banks afloat which is definatly going to happen and lack of return for each dollar - interms of export and wage growth, we're screwed.

Infact Bernard with your experience you could easily plot a historical/future graph which shows factually how the more money the reserve bank prints the more insustainable (or risky), our ecconomy becomes and plot this against time to estimate in the future when the debt load becomes completly unstable and the ecconomy and property market crashes.

It is good to see the bank economists give a more realistic view this time than they did a couple of years back when i criticized them. Well done, i hope they keep it up.

The Reserve Bank Govenor, Wheeler, must either be trying some kind of psychological tactic in which he is the only one who understands it, or he is fumbling about. I can't work him out as he makes no sense to me.

As to the GFC and the "are we nearly over it or not" question. Well the more i look into the economy the more unreliable the data becomes. First we have those that try to "Talk the economy up" and so distort the data to do so. Then we have the distorted data that is reported as fact. Recently i tried to make sense of GDP by following it through the GFC and it did'nt add up. Acording to the data there was hardly a blip in GDP and now, acording to the data everyones GDP is higher now than before the crash when we were all booming. In other words we should all be booming now. Take the unemployment data. You are only unemployed if you are "actively looking for a job" so that data is crap. An so it goes on. Trying to use this data to look ahead is useless.

As we have no reliable data we have to turn to our own assumptions, so i will give mine.

GDP grew to a point where it became unsustainable and crashed. This crash caused high unemployment. GDP would have fallen because the unemployed had less money to spend and those that had jobs started to pay back debt. When a significant portion of your work force stops spending you expect a significant fall in GDP. Did you see any data that indicated a significant fall in GDP? If you did then show us the data (note i am talking GDP's throughout the Western world). Now we see rubbish growth data, since the crash, telling us that we have been getting very small increase in growth and "Hey Presto" GDP is above crash levels.

A point to mention here is government spending and the multiplyer effect. If GDP has reached pre crash levels then the multiplyer effect either didn't work or only had a minor impact. I also believe inflation is not a factor at this point in time.

My pick is that GDP fell about 25% or more and that since the crash we have had, about 5% or 6% compounded growth, MAX. That means we are, or should be, about 80% of GDP levels pre crash, at best.

I feel the economy will continue to grow very slowly, maybe 1 or 2% compounded, and at this rate will take about another 12 years to get back to pre crash GDP. At which point it will have reached another unsustainable level.

Of course growth will not be uniform, it will start off very slowly and increase over time. It is that "over time" that is the most difficult to predict. At some point, i expect about 2 years away, we will see a pick up in growth figures and a small rise in inflation. This inflation will be temporary as supply lags demand. Once retailers catch up and re-stock, supply and demand will find equalibrium and no inflation. During this temporary inflation Central bankers will panic and push up interest rates and stuff things up as they usually do.

In light of what i have said i believe that what the bank economist have said above is worth taking on board.

If mortgage interest rates rise, that means deposit rates will also rise, drawing an influx of foreign investors making the most of those deposit rates (which will be some of the highest around the world). This in turn will cause the exchange rate to rise which would be very bad for our exporters who are already struggling and surely the Governor will be wanting to avoid that? I do think that foreign lending is about to get much more expensive for NZ/Oz banks which may force rates up anyway but I think the exchange rate pressure is more pressing especially against up all of these money printing countries who are doing everything to lower their exchange rates. Any thoughts?

http://www.telegraph.co.uk/finance/financialcrisis/9807092/Europe-drawn…

Also, can someone tell me what the Telegraph's Ambrose Evans-Pritchard means with this sentence in a recent article:

"The ECB has so far refused to take action to curb euro strength, standing aloof as Japan, the US, Britain, Switzerland, Norway, New Zealand and Korea itself, among others, try to steer their currencies lower."

Question: how has NZ tried to steer it's currency lower?

Thanks

While this is all very interesting, academically, etc. It's codswallup (sp?). NZ is one big sub-prime mortgage and the growth in M3, since the 1970s shows how we bought into the whole non-Gold standard lie. We will pay dearly and house prices will be the least of our worries. Fixed/floating, how about none, it isn't about a lack of affordability, not buying is a rational choice made by people who think that mortgaging yourself up to the eyeballs for a motley house is madness. Sure there are some winners, but mostly people who bought years and years ago whose savings are worthless in any case. Bring the axe down hard, especially on those that have benefited from and engineered the mess, that's the only honest way to govern these days.

Stay Floating. Research has shown that over the life of a 15 or 20 year mortgage, that floating is cheaper over the entire term.

Is the GFC really over? The unpredictable, & overly complex financial products that even the merchant banks don't understand are still spread throughout the global system. This means various time-bombs will keep going off in various zones. Unpredictable rallies (like this week) surges, then sudden unexplained drops in financial markets will keep everyone on their toes for the next 3 years or so.

Why risk paying break fees if you want to sell your house? 20-40k to the RE Agent, & 12-16k to the bank for the privilege of repaying your mortgage!

If floating hikes for a while - just tough it out, disconnect Sky & whatever.

Do you think the Pillars of 4 can now hike dramatically when they have 50,000 new home buyers with $350-450k mortgages on 75k incomes? They are stuck now with all the new mortgagebelt who bought over the last 3 years.

Pillars of 4 - do you really think its the banks who decide to hike. Be careful about working on averages. Even if the floating rate did average the same or better than fixed rates over a long period (probably about the same but we can't test that in NZ because we've had many interest rate mechanisms over the years - strict regulation, MCI etc), if you can't survive the higher point of the cycle, someone else will get to own your house and enjoy the latter low rates that creates the average.

Exactly, people need to consider the relative benefit/cost of the upside or downside given their ability to pay. For most you cannot minimise the cost by guessing. Ask yourself what you can live with, avoid the greater fear.

It is interesting everyone moans about our current account and debt growth yet they never consider a credit event effecting rates in this country. Really??!!

The reality for a quality proposition is that it will allow you to fix lower than most current discounted floating rates available and you can get the best of both worlds as floating rates are sticky for good reason. The herd does not ask for a discount or settles on .25% and think they are special.

Current min. I have seem are 4.75 1 year around 5% for 3 years and 5.6 for five years. Stagger that lot with a mix of floating around 5.1-5.2 currently means you should have an average of 5.2-5.3 average over 3-5 years.

Even on a 600-800k loan level the difference of a .2 or .3 further discount change is minimal and use your energy to make more income than worry about interest rates for a while..

It's interesting times Bernard, Christchurch has seen such a decline in inventory - probably a bigger decline than in 2003!

My gut feeling is that with replacement costs escalating, insurance money still to flow through and supply of houses second hand houses (ie houses which have depreciated and are affordable) plunging by the day as dozens are crushed each week, that we will see like for like costs of housing rising at least 60-80% in ChCh between September 2010 and the end of next year.

Already a house that would have cost $300k in 2010 sells for $420-450k if you can get it (at a recent auction for a house next to one of ours, there were at least 10 active (and ferocious) bidders and the sale price was over $430k with a GV of $260k!

With current activity $300k in 2010 going to $540k in 2014 is not at all unlikely.

It's like another world - in so many ways. More bureaucrats as a percentage of population than Wellington I suspect.

yes Kate.... makes my skin crawl...they are even out local celebrities....

Have you been active in the market as well Chris, wondered... with you also being soo quiet.

Been buying below 400k where able and also in the projected lower 600k market as so many buyers unable to find anything in the middle market as well in the right area. The 600s seem to be an affordability threshold for many in the middle.

A few good deals in December/Jan while people were distracted however with the clearance rates now at auction being so high it is wasted eneregy. With central land in the semi- right area now having escalated in price it is difficult to build a town house in Christchurch for less than 800k and you have a 12-14 month lead time given the CCC.

Still can build south and north of the city in right areas for 500k with 6 month lead time so will still build to order with a 80k surplus for now expected to be squeezed with buiding inflation this year. The key will be the end of the red zone March-July flowing through but.

I wonder which key project the government will start for election year and how that will effect the market given the school restructure did not have the effect I was expecting to local property prices. They wimped out...so what.

'Speckles - went to one home last Saturday, has a GV of $460 and it's going to auction and the agent is expecting over $600 - $650k. House is on a 1000m section with good garaging and parking. House is only 147sq m, no double glazing, doesn't lie well for the sun despite agent trying to tell me it has a northerly aspect. very close to the quarry on Waimakariri Rd, house looked pretty dusty on outside despite just being repainted. Blocked drains under large sealed parking area need addressing which will also mean a reseal of the area.

4 Bedroom, 2 bathroom, sep lounge.

Interest at open home on Sat was very high with people lingering for much longer than usual, so I'm thinking the agent will probably get to her higher figure of $650k givin what you have said above about the threshold and the people I saw viewing it.

That quarry north of Waimakariri Rd is possibly about to get rezoned business (industrial) too.

You would be joking to think that will go under $650k given recent auction results. I haven't been through, but looking at the photos my pick is a sale price at $785,000, which may seem obscene but is in line with what houses other similar condition properties are going for.

Can I congratulate myself? The sale price was $780,000. That's within 1% of my estimate, sight unseen! Not bad if I do say so myself, especially since trying to pin a price on an unique property in a hot market is not easy...

Actually you're right, too busy at the moment to make many comments... I have projects coming out my ears...

We have been buying but are getting outbid on many. Auctions have just become frenzies for some properties - one in Courtenay St a week or so ago blew me away at $575k for a small but tidy bungalow on a full site. I expected late $450-475k max on that street with the road widening issues etc. Similar although unrenovated next door went for $250k 6 months ago.

The whole market is wildly topsy turvey and distorted because of earthquake issues.

It seems $500k for a house is pretty average now.

All sorts of stuff is available, I've even ventured buying a couple of blocks in the CBD cordon recently - fun with CERA - I can see why things are moving so slowly with that bunch of bureaucrats...

I am fascinated how much time is spent on this floating vs fixed dilemma. In the US this would make sense. For example, 30 year fixed morgage is currently 3.72%. Good time to fix! Low rate and long term stability

Fixing for a 6 months or a year makes very little sense. Even if you knew what the interest rates are going to do, the difference is peanuts and the term is so short term that it gives you no peace of mind at all. Of course, you never know what the rates will do, so sometimes (often?) you will be doing the wrong thing. On top of that, once or twice in the life of your loan you will have to break the fixed term and pay penalties. When you factor all these things in, there is really no point in fixing.

Why not spend time worrying about something else? Italian elections for example ;-)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.