By Bernard Hickey

The times they are 'a changin' in the world of interest rates and that could shift your view on fixing vs floating. So let's have a look at the factors at play and how to think about them.

Wholesale interest rates are rising and so are the fixed mortgage rates that are connected to them, albeit indirectly and with a lag.

The big news in recent months has come from a man far away with a beard, and he's not Father Christmas. US Federal Reserve Chairman Ben Bernanke began signalling in late May that the world's largest central bank would 'taper' down its current programme of Quantitative Easing or money printing to buy government bonds, possibly as soon as later this year. This surprised some in the markets who had been expecting the money printing support from the Fed to go on and on into the foreseeable future, given America's stubbornly high unemployment rate and equally stubbornly low inflation rate. These 'tapering' comments helped the US 10 year Treasury bond yield jump almost 1% to 2.6% in the last couple of months.

That bounce in longer term interest rates has spread around the world, given US Treasuries are seen as the base for all interest rates.

Also, closer to home, expectations about New Zealand's own economic growth rate have improved in the last couple of months. Economists are now expecting the Christchurch rebuild and the house price boom in Auckland will drive economic growth of between 3-4% over the next year or two. Financial markets are beginning to price in expectations the Reserve Bank of New Zealand will have to put up the Official Cash Rate (OCR) by around 0.75% over the next year to keep inflation within its 1-3% target band.

However, the Reserve Bank itself has said as recently as June 13 that it won't be increasing the OCR this year. It even forecast the 90 day bill rate would not start rising until the middle of 2014, which implies the OCR and therefore floating mortgage rates will stay on hold until then. That's because inflation appears dead and buried. It has actually been running below the 1% lower bound of the 1-3% target range for much of the last year, thanks largely to the very strong New Zealand dollar.

Economists are sitting between the Reserve Bank and the markets on the outlook for interest rates. Most expect the first hike will be in the March quarter of next year and then the OCR will rise from 2.5% to around 4.5% over the following year to 18 months. That would lift floating mortgage rates to around 7.5% by the middle of 2015.

In previous years I was firmly in the floating camp because I saw interest rates staying low or even falling further because of the stubbornly weak global economy and very low inflation. However, in recent months my views have started to shift towards fixing. This largely followed the appointment of new Reserve Bank Governor Graeme Wheeler in September last year and the surge in the Auckland housing market through 2012 and into 2013.

The new Reserve Bank Governor seems to be taking an orthodox approach to policy and interest rates, which means he is less likely to cut. He is also worried about the surge in the housing market. In recent months the bank has signalled it is now much keener to use other tools to control the housing market such as a 'speed limit' on growth of low deposit or high LVR (loan to value ratio) mortgages.

That may have some impact, but ultimately the impetus from stronger growth is likely to force the bank to put up interest rates, possibly as early as March next year. Also, fixed mortgage rates have been competed signficantly lower in the last year, making them better value in some cases than floating. One reason for that is a fall in the cost of foreign wholesale funding for the banks. They are passing some of that on in the form of lower fixed mortgage rates and there has been a fresh surge of competition since early 2012 as the banks geared up to fight for market share as ANZ merged with National/

That's why I would tend towards floating half and fixing half of my mortgage in coming months, rather than floating it all. (I have actually sold my house and cleared my mortgage, but that's another story).

This is far from specific financial advice and everyone is different, so it's worth running through the pros and cons of fixing vs floating and looking in depth at the various factors at play. It's also worth spending some time on it. Don't blindly follow my or anyone else's view. This article is aimed at providing useful information in an accessible way to help you make a big decision. As I'll show lower down, it's a decision that could save (or cost) you thousands of dollars over the next couple of years. Here's our Fixed vs Floating calculator to help.

Also, there are many different views, and I've included the views of other economists below.

What the economy is doing and what the RBNZ is saying

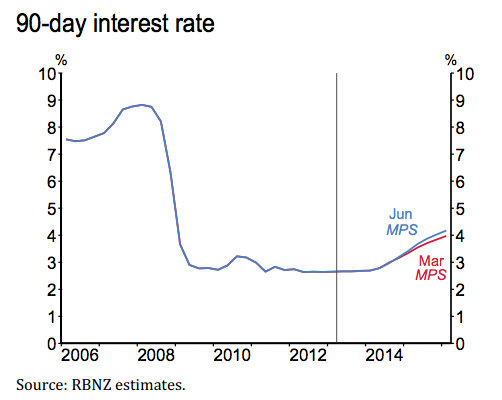

The Reserve Bank's chart below is from its June 2013 Monetary Policy Statement of its forecast track for the 90 day bill rate, which is typically around 30 basis points above the Official Cash Rate (OCR). It tells the story of what the bank is thinking. It sees economic growth accelerating to 3.5% by the second half of next year and it expects inflation to rise from under 1% to around the mid point of its 1-3% target range over the next couple years.

The blue line shown is its June forecast and the red line its March forecast, which shows it is slightly more worried about inflation, but not that much. It shows the OCR only rising to just below 4% by early 2016, which suggests floating mortgage rates only rising as high as 7% within the next 3 years. Three year fixed mortgage rates are currently around 5.9%.

Those in competitive situations and with plenty of equity can get floating rtaes of around 5.3% at the moment and would see their floating rates rise to around 5.7% by the end of 2014 in this scenario painted by the Reserve Bank..

Currently advertised 18 month-2 year rates are around 5.4% to 5.5%, which would mean you'd pay slightly more for the first 6-12 months or so and then slightly less in the second 12 months if you were to switch from floating to fix..

Fixed rates tend to be more closely linked to wholesale 'swap' rates than the OCR. Swaps rates fell broadly through 2012 on increasing fears about a global slowdown and a slow rebuild in Christchurch, but they have risen around 40 to 80 basis points through the first six months of 2013 on hopes for recovery and the rise in international rates.

Luckily for borrowers though, banks' funding costs on international markets have dropped so the net effect is fixed mortgage rates haven't risen as much. Two to five year swap rates have risen from 40 to 70 basis points over the last two months, but fixed mortgage rates are up on average by only 15-20 basis points in the last month or so.

There is a way to test the various scenarios and work out which option is cheaper (although cheapness is not the only factor worth thinking about for many people).

There is a calculator

We have a calculator here that allows you to test which rate is cheaper, depending on three different interest rate scenarios. Click here to go to the calculator.

There are three different rate scenarios. A is the high one with an OCR peak of over 4.6%, B is the medium one, which is in line with market expectations for a rise to 3.6% by late 2014, and C is the low one, which implies flat rates through to mid 2015.

Try it out to see which option is cheaper for you, depending on your rates view.

A simple money calculation isn't everything though. Some people put a high value on knowing exactly what their mortgage payments are going to be for the next two years because, perhaps, they have a fixed income or are very nervous about a sharp rise in rates. They may see paying slightly more for a fixed mortgage as a bit like an insurance payment that helps them sleep at night.

Others may want to stay floating because they really believe interest rates will be cut again or not rise, and because they don't want to be stuck fixing and have to pay an exit fee if rates do fall. The most recent memories for some people are having to break their mortgages and pay big break fees (or finding it unaffordable to do so) during 2009 and 2010. Others have longer memories of being stung with big increases in floating mortgage rates as the OCR was hiked from 5% to 8.25% between early 2004 and mid 2007. Really old people remember the 20% plus rates of the mid 1980s. I'm not that old. ;)

Everyone has different appetites for those sorts of risks of paying more or missing out on paying less, and different views about where interest rates will go. Those are the main things to consider when fixing or floating.

Less than 50% of New Zealand's mortgage lending is now on floating rates and there has been a significant move back to fixing in the last year. The decision for many now is when to fix.

What house prices are doing

House prices are rising quite quickly, particularly in Auckland and Christchurch, where chronic shortages of non-leaky and non-damaged buildings are being squeezed by demand from immigrants (both internal and from overseas) and those with insurance payouts. Record low interest rates with little prospect of fast rises are also fueling activity.

REINZ figures showed Auckland house prices were up 19.8% in year to June, while Christchurch prices were up 10.6% and prices nationwide were up 8.4%.

New house building is increasing, but remains less than needed in Auckland to keep up with demand. All those factors together suggest continued house price inflation in Auckland and Christchurch at least, however a weakening economic outlook and any rise in interest rates would take away some of that upward pressure.

What economists are saying

BNZ's Tony Alexander says in his latest commentary interest rates will start rising in the March quarter of next year and could rise by as much as 3% by the end of 2015. He sees house prices continuing to rise.

Our current forecast is that the rate rise cycle for floating rates starts in the first half of next year, takes the official cash rate from the current 2.5% to 4.5% come late-2015 and after that it depends very much upon how Kiwis react to rising rates this particular economic cycle. History tells us that we will largely ignore the RB for a long time therefore the risk is that the cash rate rises to 5.5% and not 4.5% and that floating mortgage rates therefore reach 8.5%

House prices will rise higher given that migration flows now appear headed for boom territory thus adding to already high buying pressures and a deepening dearth of listings made worse by the low ability of house construction to rise quickly given a shortage of builders.

Here's his summary of what he'd do as of July 11.

If you think taking out an 18 month or even two year term is fixing and giving you some certainty through the interest rate cycle – you’re dreaming. Three years and beyond is true risk management. Anything shorter is largely opportunistic grabbing of a low rate simply because it is less than the floating rate.

Personally, having really sat down and given it thought this week, were I truly borrowing at the moment I would have half at the five year fixed rate of 6.35%, one quarter fixed 3 years at 5.9%, 15% fixed at one year for 5.25%, and 10% floating at 5.74%. If you are in a position where you recognise the risk management benefits of this structure but can’t do it and instead take one of the low short-term fixed rates out there because otherwise you could not afford your house – then don’t borrow the money in the first place.

You could well be forced to sell when rates rise 3% even though your equity will be greater because you won’t be able to afford the cash outflows – especially if at the moment you are a couple, both working, but plan having one partner quit within three years to raise children. Work out your cash flows assuming an 8.5% mortgage rate come 2016 and see how you would be left.

ASB's Nick Tuffley sees the RBNZ holding the OCR at 2.5% until March of 2014, before increasing it gradually over the following two years to 4%. But he reckons low fixed rates provided a good hedge. Here's ASB's latest home loan rate report.

Mortgage rates remain competitive, in part due to a reduction in bank funding costs. As such, many shorter-term rates are still below the floating rate, which allows borrowers to secure a lower interest rate despite the reduced prospect of an OCR cut. Medium-term fixed rates also offer excellent value, providing a good hedge against interest rate increases in the future.

Borrowers should keep in mind that large uncertainties remain around the economic outlook. Given the risks to the economic outlook, it is equally conceivable borrowing rates could end up either lower or higher than average. Faced with uncertainty the best strategy for borrowers is to weigh up what their priorities are and make the choice that looks the best aligned with them.

Westpac's Dominick Stephens says in his July 'Home Truths' research note that New Zealand's housing landscape is now split into three distinct markets -- Auckland, Christchurch and the rest. He sees genuine short term supply problems driving up house prices and rents in Christchurch, but he questions whether supply is the only expanation for the fast inflation in Auckland house prices, given rents there are flat.

If physical shortages are not the main explanation for the behaviour of Auckland’s housing market, then building more houses will not necessarily change the market. I seriously doubt that the supply measures recently enacted by the Government will really change much. Prices are being driven by buyer expectations of future capital gain - we know this because prices have become divorced from rents.

Westpac sees the OCR rising from the first quarter of 2014 to 3.5% by the end of 2014 and 5.5% by the beginning of 2017. Here's Westpac's July 8 commentary on fixed vs floating:

We favour fixing over floating. Fixed-term rates out to two years are currently below floating rates, while three-year and longer fixed rates are only slightly higher. Staying on floating would only be the lower-cost option if the RBNZ actually cut the OCR, which we regard as unlikely.

In fact, we expect the floating mortgage rate to rise significantly over the 2014 to 2016 period. There may be value in fixing sooner rather than later. Wholesale interest rates have risen sharply in recent weeks, and fixed mortgage rates are already rising in response. We think fixed mortgage rates may rise further in the near term.

ANZ's economics team releases its monthly property focus here. It sees the OCR rising from early 2014 and says there is merit in fixing.

Supply shortages and the lowest mortgage interest rates in almost 50 years are underpinning a rising trajectory for house prices, but we question the durability of a nationwide housing market lift given stretched affordability and debt metrics. Given the high NZD, the RBNZ will shy away from OCR hikes as long as possible, and will deploy macro-prudential tools to try to cool the housing market directly.

Rising residential investment activity and an additional 39,000 houses for Auckland over the next three years will eventually help reduce pressure on prices, but a nervous wait lies ahead. The RBNZ will be hoping that pending restrictions on high-LVR lending will help cap the housing market. If not, the OCR will be brought into play. We expect the first OCR hike to occur in early 2014.

Looking ahead, given the likelihood that rates will continue to rise, borrowers would do well to consider fixing. Fixing now means paying more, but it may work out cheaper in the long run. Selecting a term depends on how quickly you believe interest rates might rise versus one’s appetite for the extra cost. We have long favoured a spread of terms, with an emphasis on 1-2 year terms. However, for the first time in some time, we believe there is now some merit in for fixing for longer than 2 years.

--------------------------------------------------------------------------------------------------------------------------

Mortgage choices involve making a significant financial decision so it often pays to get professional personalised advice. A Roost mortgage broker can be contacted by following this link »

--------------------------------------------------------------------------------------------------------------------------

No chart with that title exists.

30 Comments

Good Day. I'm a fan of this particular article. But i could not really comprehend why BH decided to release this today. There are some sort of back down today from the Chairman of the US Fed Reserve, BB from the so called Tapering or shall we call it Taper Gate now.

I'm really keen to wait for the views of everyone from this forum with this regard. Have a Nice Day All.

One really has to wonder whether the NZ/world economies can cope with higher interest rates.

Just three weeks after he talked of tapering Bernanke now says that “highly accommodative monetary policy for the foreseeable future is what’s needed” and now it looks like the whole of southern Europe is about to go down the gurgler:

http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/10172…

China too??

In light of all of this could the recent increases in swap rates in itself be a "bubble" that will burst. Perhaps we will see much lower rates in a years time - fixing say 3 or 5 years could be a mistake - who really knows in these volatile times?

Is there any breakdown available that indicates of the 50% of mortgages that are fixed how many are fixed for 1,2,3,4 or 5 years? I suspect that a large portion of the fixed mortgages are only for 6 or 12 months.

Currency wars.....everyone trying to drive their currency below competitors. I notice now the Americans want access to Chinese companies, to exchange worthless no cost currency for real assets.....no wonder the Chinese are reticent.

The "taper" was never really going to happen, it's just jawboning. We have solid centrally planned money and interest rates. Infinite fiddling with markets, employment, inflation.

When the gold window was closed in 1971 all bets were off......we can have deficits with no tears.

Savers be damned.

Agreed big blue. Nothing has changed. Too much private debt. See Keen's spiel: http://t.co/qVvtJ5EOEp

We've got years of this. Take the 1-year specials from the banks I reckon, too much uncertainty for anything else.

Muppet - page 30 of that document very interesting

"Inflation dead and buried"....but will this matter with the property prices rising a fat % every year...so much so that the stability of the economy is clearly at serious risk...and so the stability of the banks that are pumping out the credit to blow the bubble?

Clearly something has to explode...either the RBNZ acts to cause mortgage rates to rise, be it ocr leaps and bounds upward, or some other action,,,,,or we face the damage caused by not acting.

There are only these two options.

The cost of mortgage credit can be raised without the ocr going up to bash exporters....the RBNZ can increase the amount of local deposits from residents, the banks must hold.

The real question then....why is Wheeler not being allowed to do this?

Wolly - you've confused the hell out of me with that last comment. Are you suggesting that if the banks are legislated in some manner by the RBNZ such that they are foreced to put up deposit rates to high levels, which will obviously negatively impact mortgage rates, but because the OCR might stay down that some how exporters will be able to fund at the same rate as currently ?

Agree... take the 1 year specials at 4.8% etc and enjoy. 3 or 4 year fixes are not exactly long-term insurance anyway. We don't have the choice of the length-of-loan fixes as the US & UK do.

Our fragile economy will not bear much in the way of interest rate rises..... watch the effect of the first (if any) rate rise.

Let's see - petrol prices rise, food prices rise due to lower dollar, etc feeding into a higher CPI - so let's ramp up the OCR, that will really fix those price rises (which are not stemming from exuberant demand but from currency/commodity price issues).

The last CPI was, what? .2% ? Grounds for a rate rise - not likely.

Banks are just sneaking in a few rate rises while the media have the gullible public fooled that OCR rises might be coming.

Interest rates could well keep falling or flatlining well out into the future ....

If a low OCR has only just kept our economy afloat while we have had quite favourable conditions with Australia & China propping us up over the last 4 years, we will need OCR cuts if Aussie & China falter or we hit some real headwinds .

Are you suggesting Mortgage Belt that interest rates only go up when people can afford them? Have a look at history, its not always the case. And you're right, we'll see what happens, it will hit house prices because some people are clinging to floating, delay looking at fixed rates until they've gone on them, and are then screwed, Its a tough cycle. But don't worry, inflation will set one more, and last low, next week, and therefore OCR hikes are 6-12 months away at least, but I agree, not a long time in the big picture. And by the way, the banks costs to hedge fixed rates (check out wholesale swaps rates if youre aware what they are) have undeniably gone up 40-70 basis points in the past coupe of months, do you not think that might have something to do with the rate rises ?...nah course not, its all about the banks.

Kimy - I appreciate you have a total ignorance in the area of interest rates, and its been a total waste of my time pointing out the basics to you in the past, but one last try. If youre stating"how the swap rates have been manipulated to justify interest rate rises in a low interest rate environment everywhere around the world" do yourself a favour and pull up a chart of US bond rates and have a look and see if you notice some change in the last two months. And while youre at it, because you won't know this, do a bit of research on what is the benchmark rate in the globe that drives the direction of all long term rates, including ours.

As usual you don't answer the question, and hence someone can never have an actual conversation with you on the subject - you just keep rolling out this popularist cr@p that about three of you on here just love to keep convincing yourselves is true, and in this case, irrelevant to the subject....I wonder why you even bother to come here because those here with half a brain ignore you completely, whereas I admittedly occassionly regress.

Can't resist it - Kimy you should apply for the position of Governor of the Reserve Bank. Nice office on The Terrace, Wellington - just across the road from the Beehive.

Kimy - I can tell you that probably for once in your life you are wrong. The Embassy of the People's Republic of China is situated in Wellington, a very good address - right opposite the Botanical Gardens and just around the corner from the Beehive. location, location, location. It is the Chinese Consulate which is situated in Auckland. I'm Wellingtonian born and bred so no argument.

Wldn't be a bad thing if an earthquake hit Wellington and wiped out all the Govt. and the Reserve Bank. Then we could start again! And if it shifts to Auckland, for God's sake don't build another Beehive, there was enough debate the first time around - and it probably leaks now.

Advice for the day Kimy - learn to laugh at yourself.

The service centre is the southern one on GSR, for visas, etc.

Building environment: moderately impressive.

Customer service: what's that? They don't even crack a smile. (Actually it has improved a bit recently).

Ok I admit Kimy, I'm so surprised to hear that the Greens are basing their ideas on your thinking. And shame on them for embarrassingly backing down on the brilliant money printing idea the minute it got a bit of scrutiny - who said its quackery, after all the US are doing it right, admittedly theyre in the cr@p with zero interest rates and nowhere to go. Please dont be put off and keep up the valued contribution to the Greens

Every time you write something my impression that you really have no idea grows.

To start with every other CB that is QEing is up against a zero bound trap, NZ is not.

NZ is considered a risky currency, just look how far we dropped just from Bernankie commenting on starting to taper, let alone actually tapering! Those QEing have a special "status", they are either the reserve currency (USD) or very large (EU), or UK, NZ is neither.

Two reasons we are not worse off right now, a) we have appeared to the overseas ppl who lend to us to be getting out of debt with no great strain and are being fiscally competant in their eyse (perception but there you go). b) we are linked to the OZ and its mineral boom, unjustifiably but thats the way it is... The oz boom is of course wilting, so that leaves us with a) being seen to be acting in a "sensible" manner.

Debt, well last time I looked 10 year Govn bonds were 3.2%, (If you accept BAU as teh future scenario) then given inflation is going to be 2% ish we would be borrowing at next to no cost.

Quite why you think printing 40billion would have no effect on a) is mind boggling...then add the effect to Mortgage rates, they would rise...I cant see how they would not....thats a lot of extra stress in an economy already out of balance.

regards

John Key also said with the stimulation we now have (very low OCR) we should be growing at 6%....and we are going no where and he didnt undertsand why not.

Otherwise I think you are cherry picking...

BTW URL top JK's comment?

I missed that one for sure...

If you meanthis, well

http://www.interest.co.nz/currencies/64264/pm-john-key-says-currency-in…

If thats his take on how things work....oh dear.

regards

Steven - that was going to be exactly my question to him as well, where did Key say that printing $40bln NZDs would have no affect ? - Kimy not only doesn't respond to questions or specfic requests (other than with irrelevant comments) but he just plain makes up stuff. Printing $40bln would knife the little NZD overnight, and then tell me that we would still have sub 2% inflation let alone sub 1% now. Divided USD100 per barrell by 0.6000 rather than 0.8000, citing just one import, and then see how thanked he'd be by the public, especially by home owners when the RBNZ then hikes the OCR and mortgage rates spike head higher and steeper.

Thats said I'm not sure what youre suggesting that Key said in that link that you disagree with ?

I'm not calling you dumb Kimy, I'm sure youre not, and there will be alot of areas where you will know alot more than me, property may well be one of them (wouldn't be hard considering I have less than 10% of my net worth in housing). But there are some areas where you're away with the fairies, and interest rates and basic ecomnomics is one of them, and you will never get better for the reasons below.

My frustration is more around people who won't answer specific questions (which you haven't here again), who don't come to learn from others in areas where they're weaker (there are some very informed people on here with either very specific or very good general knowledge), but rather come here to lecture others despite having less knowledge in that particular area - why do they bother as ultimately most just stop responding to that individual's posts as I note most have with you...Admitedly I'm also a slow learner in that regard compared to those smarter others.

A slow leaner but I have learnt finally.

I think that Grant A and Kimy should meet for coffee... this forum is not all about tall poppies.

"never argue with a fool, people might not tell the difference" Irish proverb.

Truer words never said Dobrydan, not the coffee bit though.

No please....I'd like to vote Green again....hard call with kimy "advising" them...

LOL.

regards

I downloaded all the rates from the RBNZ since the inception of ocr, and concluded that the 6 month fix is the best rate. It out performs all other rate over any long period. You just need to ride out a few lean times. I've been doing this now for about 8 years. However I now found that my bank asb keeps tring to charge me a fixing fee which I refuse to pay, but we have the same argurment every 6 months. Also now I'm getting quoted rates 1 percent higher than the housing rates ( I'm a farmer) my manager says this is normal across the banks. Is this correct or is he tring to screw me again?? This never used to be the case in fact a few years back I was getting rate better than housing.

Westpac will waive the fix fee for hooked in customers...

The 1 year rates are actually the best atm.

The only risk (of the 1 yr) is if rates move upwards in the first half of 2014 then you;re stuck until July/August.

Id shop around....I can only quote for myself but a few months ago I considered fixing and kiwibank for one said no fixing fee.

regards

I got a one year fixed from BNZ for 4.7 about two months back. They wanted to charge me a break fee. I said no way as the money comes from thin air, so why do I have to pay. They gave me a credit anyway, but they insisted I paid for the break fee. WTF? If Bernake is saying they will still print then interest rates will the same. I cant see a way out of this mess unless there is " debt forgiveness " - and that aint gonna happen!

The world has too much debt and can't afford higher interest rates, I am going to continue to enjoy historically low short term interest rates. I just can't see short term rates rising materially in the medium term. That said if you can lock in for 4 or 5 years at under 6% then it's not a big price to pay for certainty if Cashflow is tight.

Bernard, what happened to your brother-in-law to whom you used to offer advice in these articles about fixing vs. floating? Ficticious or real, mortgage or no mortgage, I hope he's doing okay :)

Anyone been offered better than 5.65% for a 3 year fixed mortgage lately?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.