This article was first published on AUT's Briefing Papers series. It is here with permission.

By Ryan Greenaway-McGrevy*

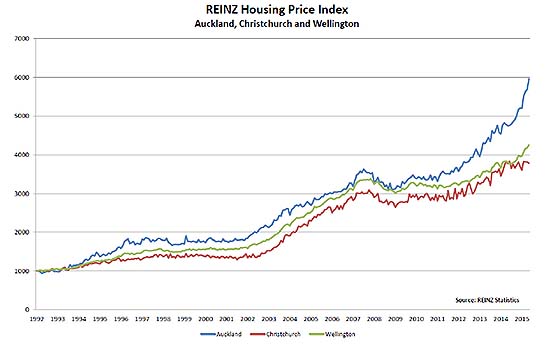

In May 2012, it was only $562,454. That is nearly a 50% increase over only three years.

Can anything justify this incredible growth in prices, or is it all a bubble?

Peter C.B. Phillips and I address this question in a recent article to appear in New Zealand Economic Papers: Hot Property in New Zealand: Empirical Evidence of Housing Bubbles in the Metropolitan Centres. One of our key conclusions is that there is an ongoing bubble in the Auckland real estate market. Interest.co gave this coverage to the paper.

In Hot Property, we try to restore some objectivity to the difficult task of determining whether or not there is a bubble in New Zealand’s real estate markets.

But what exactly is an asset bubble, and how can we spot one?

A bubble describes a situation in which an asset price is substantially inflated relative to the asset’s fundamental value, which is the present value of expected income from the asset. But while we can easily observe asset prices, it is harder to observe expected fundamentals.

Many arguments over the existence of asset bubbles boil down to whether or not high asset prices can be justified by expected incomes. These arguments sometimes persist long after the prices have come crashing down. For example, see this exchange between Eugene Fama and Ivo Welch from 2002 on the famous NASDAQ bubble. Fama is one of the most frequently-cited financial economists, and is known for the efficient markets hypothesis. Arguments over the existence of bubbles lead to a large experimental literature that has established the existence of asset bubbles in the laboratory setting (see, for example, Smith, Suchanek and Williams, 1988). Outside of the lab, however, it is remains difficult to spot a bubble by focusing only on asset prices, because we never really know what market participants’ expectations are.

It may be more productive to focus on the growth rate in prices, rather than the price level, when trying to spot a bubble.

Bubbles occur because sufficient numbers of market participants purchase an asset in anticipation of future price increases. This can generate a self-fulfilling prophecy, in which asset prices spiral upwards simply because market participants think that prices will increase. As more and more buyers enter the market in anticipation of future returns, prices increase, and they increase at an accelerating rate. As I will discuss below in more detail, it is harder to justify this accelerating price growth in terms of changes in expected future income from the asset.

We therefore look for accelerating price growth when trying to spot an asset bubble. This general approach to bubble detection was first proposed in the 1980s (See, e.g., Diba and Grossman, 1988).

The statistical bubble detection tests we employ are designed to establish whether prices are growing and at increasing rate. Peter and his other co-authors provide the theory for these statistical methods in a series of papers (Phillips, Shi and Yu, 2015a; 2015b).

A key feature of the methods is that acceleration in price growth must occur over a sustained period in order for us to identify it with any acceptable degree of statistical precision:

We are not talking about accelerating price growth over a few months, but a few years. The methods provide not only an indicator of whether an asset is currently experiencing a bubble, they also provide date stamping mechanisms for identifying when the bubble begins and ends. In other empirical applications the methods have proved to be very adept at capturing the onset of bubbles in other asset markets, such as stocks and commodities. And importantly, the end of the bubbles always coincides with a fall in the nominal price of the asset in these empirical applications.

Using this method we identify an earlier, broad-based bubble in most of the regional real estate markets of New Zealand. The bubble appears first in Auckland and Wellington in mid- 2003, before spreading to the other main centres. The onset of the bubble suggest that it was part of a broader global bubble in real estate. The bubble burst with the onset of the worldwide recession in 2007, and coincided with about a 10% fall in nominal house prices.

More recently however, the tests show that Auckland once again entered bubble territory in mid 2013. As yet, the bubble in Auckland has not ended, nor has it spread to other parts of the country.

Many readers will disagree with our conclusion and argue that the accelerating price growth in Auckland is entirely justified by the fundamentals. We mitigate these concerns to an extent by normalizing house prices by an indicator of asset income – in the paper we use either rents or incomes – before running our battery of statistical tests. By doing so, we rule out the possibility that asset prices have been growing exponentially because rents and incomes have been growing exponentially.

This leaves open the possibility that price growth reflects exponential growth in expected future fundamentals. But while it is easy to generate a fundamentals-based narrative that results in price growth, it is difficult to construct a narrative that can generate accelerating price growth over a prolonged period of time. This is because asset prices incorporate news relatively quickly, and certainly not over a period of several years. Consider, for example, that the Reserve Bank recently cut interest rates and signaled the beginning of monetary easing in the economy. If this cut was a surprise, and all else being equal, this should lead to an increase in house prices, but not an acceleration in house price growth over the next few years.

Many of the common rationalisations for high prices in Auckland – such as lower interest rates or high migration rates – fall into this category. An unexpected increase in migration, or an unexpected decrease in mortgage rates, is good news for property owners, and should lead to a relatively quick increase in real estate prices. But in order to generate accelerating price growth over a sustained period, we would need a sequence of good news that persists over several years. No one is that lucky.

Do bubbles always collapse?

Nobel Laureate Jean Tirole provided the conditions for a bubble to survive in an economy (Tirole, 1985). These conditions include durability, scarcity, and common beliefs, and housing sure does appear to be scarce right now. Up until this point in time, urban zoning restrictions have tied real estate to land in Auckland: We do not have the same high density planning as many other cities in the world, and so the number of dwellings per unit of land has been more-or-less fixed.

Right now, housing is scarce because land is scarce. If this link between land and real estate persists, then we may just be sitting on a rational bubble. Happily however, the current version of the Auckland Unitary Plan allows for a potentially large increase in the number of dwellings within the city limits. If approved, the land restrictions on dwellings will be significantly relaxed, allowing supply to better respond to the price signal.

Where to from here for Auckland?

Unfortunately, the empirical bubble detection literature currently offers little in terms of predicting the future. It is apparent, however, that it can be a long time between when the bubble is first diagnosed and when it finally collapses: Periods of five years or longer are not uncommon. It would be foolish for me to make any claims regarding when the best time to buy or sell a house is, or whether prices will increase or decrease next month.

But can real estate price growth continue to accelerate indefinitely? I wouldn’t bet the house on it.

References:

Diba, B. and H. Grossman (1988). “Explosive Rational Bubbles in Stock Prices?” American Economic Review 78, pp. 520-30

Greenaway-McGrevy, R., and P.C.B Phillips (2015). Hot Property in New Zealand: Empirical Evidence of Housing Bubbles in the Metropolitan Centres. New Zealand Economic Papers, forthcoming.

Phillips, P. C. B., Shi, S. and J. Yu (2015a). Testing for Multiple Bubbles: Limit Theory of Real Time Detectors, International Economic Review, forthcoming.

Phillips, P. C. B., Shi, S. and J. Yu (2015b). Testing for Multiple Bubbles: Historical Episodes of Exuberance and Collapse in the S&P 500,International Economic Review, forthcoming.

Smith, V. L., Suchanek, G. L., and A.W. Williams. (1988) Bubbles, Crashes and Endogenous Expectations in Experimental Spot Asset Markets.Econometrica 56, 1119-1151.

Tirole, J. (1985). Asset Bubbles and Overlapping Generations Econometrica53, pp. 1499-1528

--------------------

Dr. Ryan Greenaway-McGrevy is a Senior Lecturer in the Department of Economics at the University of Auckland. Prior to joining the department in July 2014, he served as a Research Economist in the Office of the Chief Statistician at the Bureau of Economic Analysis (BEA) in Washington, D.C. . This article was first published on AUT's Briefing Papers series. It is here with permission.

40 Comments

Rational bubble. Is that the same as distinguishing between EBIT and normalised EBIT, because despite all the unforeseen events we had no strategy to deal with we would like to propose our business was run well for the last reporting period.

Fail to draw any useful conclusion from this paper but thanks for the reference on bubble testing.

What about the effect of money laundering? How does that fuel asset bubbles?

Money laundering is certainly one element of the fuel pyre, and the levers for that as all broader elements are with Govt.

On supply side, it's not just more land (Pokeno anyone, no infrastructure/transport link beyond pushing more people into clogged motorway?), but more effective land use (personally, I'd prefer NYC-style vibrant city apartment living, as in every other big city).

Also demand side. Whether to put any curbs on overseas investment by legitimate investors, eg those who buy solely for capital gains as better than interest returns, or divert into new housing only (boost supply), or distinguish between resident, occupier, etc,

And whether our curbs on illicit investment are sufficient (eg if police can more easily convict the local drug dealer who buys a few rental properties, than the overseas drugs cartel which buys 50 houses. They might 'see' both, if banks/lawyers/agents file STRs, but if they can only prove the predicate offence in one, they're powerless to stop the other. And which one affects prices?

That said, money laundering is just one part of the policy-setting puzzle. But in one sense it should be simplest. For legitimate investors, there are valid competing arguments. But surely no-one's really too keen on the world's criminals having the same rights to invest as they please with the proceeds of serious crime?

Some policy settings are hard, some not so much, perhaps?

http://www.interest.co.nz/opinion/76906/ron-pol-argues-theres-missing-d…

The answer you seek is here

http://www.interest.co.nz/opinion/76847/caroline-courtney-argues-john-k…

Examples include:

• Use of cash, or disproportionate amounts of cash.

• Transactions where the price does not reflect local valuation data/trends.

• Purchasers unusually willing to pay the asking price with lack of concern about price.

and here

Basel Brush July 2012

I was told today of a local Asian RE agent buying on behalf of a China buyer, sight-unseen, a property in Botany area. The price negotiated is $1.6m for a property with a CV of $800k

http://www.interest.co.nz/opinion/60396/thursdays-top-10-10-japanese-pe…

Think that thru and consider how the locals in that suburb are going to respond to the knowledge that the houses in their street have just doubled on the sale of one house, and then try and talk them down

Think about the impact the sale price of JUST one single transaction has on the surrounding neighbourhood, and their subsequent expectations, and then ask yourself was that a money-laundering transaction. Looks like it. And that's the impact of one overseas buyer which then bleeds through into the surrounding area

Re-read the article by Caroline Courtney and the example of one buyer buying multiple properties - and the way it was done - that's not the behaviour of a home-buyer - so what is it?

Nice piece, thanks. Whatever differing views, good to add data and analysis for rational debate.

A bubble describes a situation in which an asset price is substantially inflated relative to the asset’s fundamental value, which is the present value of expected income from the asset.

This definition is incomplete when it comes to land.... Land has unique properties that separate it from other asset classes...

eg... Build a Harbour bridge across to the North Shore... and the value of land sky rockets, which has nothing to do with Net present Value of expected incomes.

It has everything to do with Land values appropriating the benefits of the investment in infrastructure... which results in a greater utility value for people.... etc...etc.

another example is the impact of the coming unitary plan on Land values... and part of that is the impact of policies that have restrictive urban limits...

Maybe much/some of the Capital Gains are in the repricing of land because of zoning changes....

SO... the above definition of a bubble in real estate is not quite right .... in my view.... especially when it comes to residential houses..

You are saying without the bridge, I could rent my house on Northcote point for the same amount that I could rent it with the bridge. Come on. The bridge brings a massive increase in income from the land asset.

The point on capital gains being due to re-zoning is a fair call. But apply the logic of the article. The first versions of the AUP came out a few years ago now. That should have been priced into the market soon after it came out. If anything, since the first version of the AUP, the density restrictions have been tightened again, which would cool the market. That hasn't happened. And if you don't find that convincing: if you still think it is all about zoning, look up the properties that get reported as selling for ridiculous amounts of cash in the AUP geographical viewer. More often than not the are zoned for one dwelling.

I agree with Roelof. Buying a house is not the same as buying shares. Most of the market is from owner-occupiers whose decisions are based on where they work and how much they can afford. Then the rest of the market is investors, and the majority of those, if not all, are buying based on price speculation as opposed to the rent they can get (plus the investors who just need to get their money into a legitimate investment). So that leaves rent as irrelevant.

Equity on property is increasing rapidly and the flow on effect is that homeowners use that equity to purchase more property. There is no CGT so its a "safe" place to leave your money. If investment property is taxed on the capital gain annually as interest on term deposits are, that will make people think twice about investing. 20% capital gain in Auckland ($1mill house) generates 200k equity....what do I do with this equity? Exactly what I plan to do in the coming months.....buy another house

Lac have you thought about just selling one or two of your properties and thereby locking in some profits or do you think the values will continue to just keep going up in the foreseeable future. The economy is hardly rock star of late and there is the risk of rising unemployment and/or stagnant wage increases.

I just don't see it happening in the next 3-4 years....demand is too high. I went to have a look at a property that I thought was fair value at 700k but was willing to go 730-760, the house sold for $935 with way too many interested buyers. Once that cools down I will look at selling. My issue Gordon, is that once I sell a property, what do I do with the profits? Returns are just too good at the moment on property investment with no tax on my gains.....

Spot on Lac and the way to do it.

There appear to be a lot of people on this site that ask questions like will property prices continue to rise in the foreseeable future?

The answer is at the rate they currently are rising, no.

A more appropriate question to ask Lac is with his property worth 1m today (and the 600k property he is buying with his released equity) given the scenario that he does not need to sell either property and can afford to finance the mortgages does he believe that at some point in the future their combined value will be greater that $1.6m? I'm sure his answer is yes.

Property prices will always rise in the long term but people seem obsessed with the here and now and calling it all speculation. A more appropriate question is you tell me a time in NZ history when property prices were lower than they were 5 years ago, if you can, tell me 10 years, or 20 years and so on.

If you live by that belief you position yourself to ride out the crashes because you know, and actually want them to happen because that's when you get a bargain.

It is unfortunate that the FHB have now been left out and honestly have no options but to ask parents etc. who have EQUITY.....that is the problem, the more property u own the easier to buy more. At some point that will change but the cashflow and ROI (IMO) will have outstripped the losses if property was to dip. Even with losses of 10% I will still be in the black.....

How do cycles or trends often end is the question that is important. If a cycle ends-up being supported by those already participating ( "I've got (whatever it is) and I'm going to buy more because others can't afford to etc) then unless another end-user emerges, where is there to go? Price becomes secondary to liquidity. It's like a share issue, where only those who have the share, buy and sell the stock to each other, hoping to attract an outside source of capital to 'take them out'. It's fine if that happens, but can be disastrous if not. History is littered with "Show me where it's happened before" etc as the reason for it not to happen at all. But there's a first time for everything...No?

NZ history, you ask for? Queenstown - 1993 to 2003. (From personal experience, of course!). I arrived in March 1993 and set about buying a residence, and was surprised by two things (1) the prices of what was on the market ( it was so cheap! compared to where I had come from) and (2) the amount of choice there was. I asked the agent (Locations) "How long would it take me to buy one of these?" His answer was "We could get it done this afternoon, if you like". My next question was "And when I want to sell it, how long do you think it would take?" The response should have been a warning "18 months, if you want to get your price". Now as it turned out, I did buy, (but not that afternoon!) and my ex ended up with the property as part of her share. It took her until March 2003 for her to just get back what we'd paid 10 years earlier.

That....is what liquidity is all about. "But that won't happen in Auckland! It's too big" It could, you know....

I'm sorry to hear that but was it worth more in 2013 than 1993? If the answer is yes then in the long term prices have increased. If someone thinks long term and does not need to sell his property at some point in the future it will undoubtedly be worth more than the value they paid for it. Sorry if anyone disagrees with that it is just a simple fact sorry.

As I wrote, the same price in and out! ( and was lower in between) No change in value at all. And as for long term? Maybe. IF you don't get squeezed out. I had a friend who bought a nice flat in Bondi for... tada...$48,000 in 1988 and even though today it's worth $ $600k, ( I guess) the hike in mortgage rates from the 10% she'd bought at to 22% forced her to sell a few years after purchase. No one, no one.... saw that rate rise coming. That's the issue with a fixed asset. It can take time to sell if push comes to shove, and holding might not be an option for any one of a number of reason -( interest rates and separations being but two!) History isn't a guide to what's coming. It's a record of what's happened so far....

Sorry about your friend and your split but as I wrote if you don't need to sell....

Your friends Bondi place is a prime example its 12 times the value it was 25 years ago if she hadn't needed to sell cause of the interest rates shed be having a great time. But ultimately regardless of what happens in the short term, bubbles burst, interest rates rise, etc, the long term shows property prices rise

You'll be aware, I'm sure, of that Dutch analysis of the sales on the same unaltered house going back to 1700 ? ( Google it if your not - I'm grasping for a date here). 'Prices always rise' can be looked at in a variety of ways. The most profound one is : Over what time-frame? ( That Bondi case above). In the Dutch case there have been time when prices on that same house have fallen continuously for 70 years or more - more than a lifetime for most property owners, and , sure, the price of that house is higher today than back in 1700. But what would you say to the owner in (say ) 1750 who saw the price fall until his death in 1820? "Hang on! You'll be right!". The human brain has evolved to search for, or to interpret, information in a way that confirms its preconceived notions. In prehistoric times, this confirmation bias kept man out of harm’s way by encouraging preferences for things known to be safe ( property in Auckland today?). Today, that instinct is wreaking havoc across the globe, and I believe that process has only just started.

Indeed there is another that tracks house price inflation from the 1600s? Almost none until the fossil fuel age, is a grandson could buy his grandfather's house for about the same amount of $s. Enter the fossil fuel age and then we get inflated values. The Q is what will house prices be after the oil age has ended in 2050 or so? back to the equivalent of pre 1850s prices?

Here's that old chestnut from Holland showing that house prices can fall for decades after decade ( modern day Japan?) before retaining their previous highs point.

https://www.bogleheads.org/forum/viewtopic.php?t=8445

bw, it can and will happen in Auckland.

It happened in ChCh 1993 to 2003 many properties were worth about the same despite being higher in 1997.

In fact a property we sold in Northcote Chch for $119,500 in late 1997 which was resold for $80,000 in 2002 (same agent both times and both open market sales). The new owner had put in a new kitchen and done other renovations costing perhaps $7-10,000. With agents' fees and other selling costs the loss was well over 40%.

That is far from the worst case as there were many sales at below 50% of the previous open market sale price (including ones we bought).

Overall the market stats don't show these types of gyrations as when the market falls, better houses sell so the median is not reflective of the actual fall.

The biggest NZ asset bubble I know of has to be the mid 90s Phonecard boom where prices rose hundreds of percent on assets of no real value and then almost instantaneously collapsed to near zero. Cards that had sold for $2000, 20 years on are still virtually worthless - the bubble never and never will reinflate.

If theoretical (environmental not real ) capital gain is taxed where will the income come from to pay for that tax??

What do you mean? The same way your term deposit or the dairy from around the corner pays its taxes... from the income it receives..... If I want to reap the rewards for a 20%pa property gain, then I should pay for that value because all other income in the country is taxed accordingly. I will either sell the property if its too much or I was take up rents to increase my income. If that fails then it will discourage people like me from investing in an over inflated property market.

Will all the businesses around the country have to find money to pay tax on the theoretical capital gains their businesses have achieved also? I suppose you'd suggest they should they just put their prices up.

i would like all that voted for this clown, he should get back on the big bird and leave NZ for good

Prime Minister John Key says people outside Auckland are telling him they want Chinese buyers in their area because they increase the value of their homes.

Mr Key also said this morning a large proportion of Aucklanders did not want house price inflation to fall because it was making them wealthier.

toss up isnt it.

Can't think of anyone saying anything so dumb...but with the educational/knowledge level of NZers it might be true

On The Panel 5th August. Mike Williams (ex president of the Labour Party) had just got a great price for his house and was going to take a bottle of bubbly to his wife. He said that while we hear a lot about migration "I was talking to Paul Spoonley and he pointed out the Australian Index of Family Formation. So the baby boomers children....?". Anything but holy migration and the academic institutions lead the denialists charge with so much intellectual capital invested.

Mike Williams made me wonder if the Labour party establishment are a bit of a clergy?

All bubbles have rational arguments for why this time it truly is about the fundamentals, and it couldn't possibly be a bubble because X,Y and Z. One of the best I heard was the one about how the world will need much, much more protein in the future, so dairy prices will be going up, up and up, rising middle class in China etc. I actually would agree that the world will want more protein, but how much can you reasonably expect people to pay, is another question entirely. A question that we are now a little closer to answering.

So yes I agree, Orcs is in the blow-off top stage of the bubble, and the snap-back will be viscous.

Shurely a Viscous Bubble will have Thick Walls and thereby be harder to Prick than a Thin-walled one?

We need a Unitarian Plan, and possibly a New Zealand Standard, for Bubble Wall Thickness Assessment to ensure the Awkland Bubble remains within spec.

I hope so mate. There are so many of us 30 something year old Aucklanders that just want to settle down, buy a house, start a family and get on with life. People say just rent, but I've been kicked out of a few rentals due to the owner selling up - generally with only a month's notice. It wears you down after a while. I couldn't imagine doing it with children.

If we don't see a change soon, we're off to Australia.

This is exactly what is missing from the debate. Ridiculous house prices actually inhibit real growth. How many more jobs would be in Auckland if we didn't have this bubble?

I hope you can stay in Nz. But I don't blame you if you leave

Indeed, when 50% of the rent / mortgage is due to a bubble that is hundreds of $dollars each month per household not spent in the economy.

Unfortunately you now have to make some tough decisions, I stayed single and have no kids and now in my 40's I'm sweet. Mortgage is paid off, having to work in the Auckland rat race is now almost optional. Had to put up with some shit jobs and bosses that were ass**holes but made it in the end. Would I do it all over the same in the current market if I was 30 again ? no of course not it simply would not be possible, my mortgage would still have another 30 years to run and I would be 80 before I paid it off ! If I was 30 and could find a great job in Australia I would be gone as well.

anybody would be sweet without kids. We would be extinct in 100 years as well so climate change wouldn't be a problem anymore. Sounds like a plan!

Not really I see wasters in their 40's that are single and still renting and spending all their money on drugs. Its about choices, yep if you and your partner have really good jobs and both keep working, houses are still "Cheap", its all relative but for Joe Average things are now very tough. Anyone with an IQ over 120 has already figured out the planet has too many people on it, probably 3 times what it needs and yes the planet would be better off without all of us on it. I often dream of what it would be like to visit earth without us on it. New Zealand would have been an incredible country as little as a few thousand years ago.

.

We are in the same boat my soon to be Wife and I. In our mid thirties born and bred Aucklander's went to the best schools and Uni's and grew up in good/average areas. Been living in Sydney for many years and have very well paying jobs and an apartment in Rushcutters Bay. Lifestyle is tremendous here but we desperately want to start a family in NZ not Australia as NZ is were the heart is and Family are all still in Auckland. But we would take close to 50% cuts on salaries and have to buy 2 cars (we have never needed to own a car in 8 years of living here) sit in traffic all day everyday and could barely afford a run down bungalow in Panmure.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.