By David Hargreaves

Rent increases of about a third would be needed in Auckland to bring the city's house price-to-rents ratio back into line with the rest of the country.

This is according to new research from the University of Auckland, which analyses house price and rent data from 1993 up to the end of last year.

The research concludes that a rebalancing of Auckland's skewed house price-to-rents ratio would be more likely to occur through a correction in house prices than a substantial boosting of rents.

"Hot Property in New Zealand: Empirical Evidence of Housing Bubbles in Metropolitan Centres" has been authored by University of Auckland senior lecturer Ryan Greenaway-McGrevy and Professor Peter CB Phillips of Yale and University of Auckland. The paper is also available here.

The research in the paper uses recently developed statistical methods for testing and dating "exuberant" behaviour in asset prices, and it documents "episodic bubbles" in the New Zealand property market in the past two decades. New methods of analysing "market contagion" have also been developed in the research and are used to examine what Greenaway-McGrevy and Phillips describe as "spillovers from the Auckland market to the other metropolitan centres".

In carrying out the research, house price data from QV spanning the beginning of 1993 to the end of 2014 has been used, along with rent data covering the same period from MBIE.

The two academics have concluded that the whole of New Zealand was in a housing bubble from 2003, before collapsing in 2007-2008, but that Auckland returned to bubble status in late 2013 and has stayed there since.

"One of our primary conclusions is that the expensive nature of New Zealand real estate relative to potential earnings in rents is partly due to the sustained market exuberance that produced the broad based bubble in house prices during the last decade and that has continued through the most recent bubble experienced in the Auckland region since 2013," they say.

They say that the Auckland bubble appears across the four main territorial authorities in the Auckland metro area, "showing that the new bubble is quite broadly based". They also use the term "pervasive".

Prime Minister John Key denied last week that the Auckland housing market is currently in a bubble, though the Reserve Bank is expressing increasing concern.

The research has found that while the early 2000s nationwide bubble was initially led by Auckland and then flowed on to the rest of the country, there is no indication this time around - so far - that the Auckland "contagion" is spreading again.

Greenaway-McGrevy and Phillips say that their findings show that relative to rent fundamentals, current Auckland house prices are "irrational".

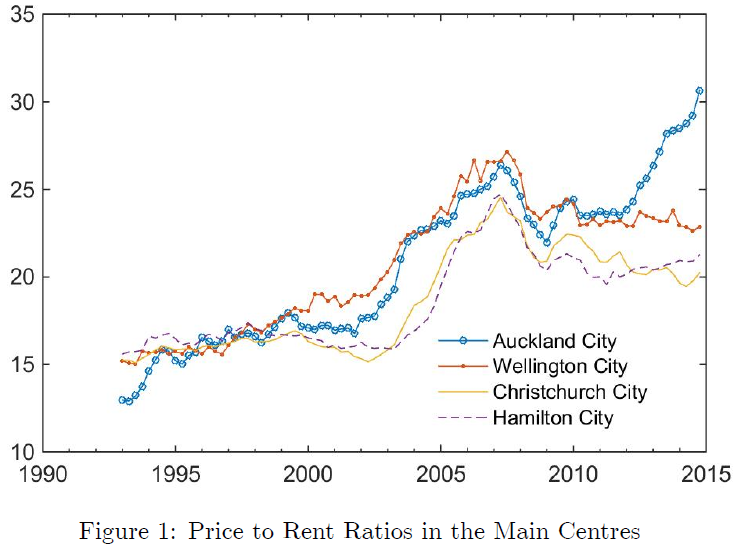

They say that house prices have currently blown out to about 35-times annual rent costs in Auckland, "which corresponds to a rental return of about 2.8% before depreciation".

On the other hand, rental expenditures as a proportion of income have remained "remarkably constant" over the past decade in the main centres of Auckland, Wellington and Canterbury.

"Thus, if a market correction were to come through an increase in rents, this would involve an unprecedented increase in rental expenditure shares. In our view, therefore, any correction is more likely to come through an adjustment in prices driven by a demand or supply side shock or combination of the two."

But the academics say that the "findings of exuberance in a real estate market such as Auckland" do not necessarily imply a house price correction is on the horizon.

"The findings show only that relative to rent fundamentals, house prices are irrational. A return to market normality in the price/rent ratio does not necessarily imply a future correction in house prices. There is also the possibility that rents in Auckland will catch up to prices, thereby bringing the price/rent ratio back to normalcy."

How feasible?

However, they then examine how feasible a market correction based on only a rent increase in Auckland would actually be.

"Currently the price-to [annual] rent ratio in Auckland City and the North Shore is around 35 while the price-to-rent ratios in Wellington, Christchurch and Hamilton are between 22 and 24.

"If prices in all regions were held constant, rents in Auckland City and North Shore would have to increase by more than a third in order to bring the Auckland City and North Shore price-rent ratios in line with the levels of the other centres.

"The corresponding rental increase needed to bring the price-to-rent ratio in Manukau and Waitakere in line with the other main centres is about 12%, given that the price-to-rent ratios in these regions is currently around 26."

The academics say any real estate market correction that is based on an increase in rents entails a commensurate increase in the share of household incomes devoted to rent - if incomes are held constant.

They therefore looked at the current proportion of household income devoted to housing costs, and whether there has been "any such steep rise in rents in the past".

Incomes

They said that in 2014, based on Statistics New Zealand figures, the mean annual household income in the broader Auckland region (including Auckland City, Manukau, Waitakere, North Shore, Franklin, Rodney, and Papakura) was $95,784 ( = $1,842 x 52).

The population-weighted annualised rents in the Auckland region were approximately $25,115 in Q4 2014, which corresponded to just over a quarter, or 25%, of the household budget.

Going back to the fourth quarter of 2000, the mean annualised rent was $14,008, and the mean household income was $57,304 (= $1,102 x 52) - so that the mean rent was again about 25% of incomes.

And as at the fourth quarter of 2010, the mean annualised rent was $21,252, and the mean household income was $81,588, so that mean rent was yet again about 25% of mean income.

These results show broad stability in the ratio of rents to incomes over a 15 year period and demonstrate that the average rental expenditure has stayed relatively constant in the broader Auckland region at around 25% of income, Greenaway-McGrevy and Phillips say.

"Rents are therefore by no means low relative to incomes. But it is certainly feasible that rents could increase substantially, thereby bringing house prices more in line with rent fundamentals.

'Unprecedented increase'

"But such an increase in the budget share of rents would clearly be unprecedented at least in the data currently available to us over the last two decades.

"We therefore conclude that to return the Auckland market to normalcy in terms of its price-to-rent ratio a more likely outcome is a housing price correction. Such corrections have occurred in many other countries that have experienced house price inflation in recent years."

The two academics say the New Zealand real estate market has "very largely been spared such major corrections" over the past two decades.

"International factors may now be playing a role in the New Zealand market, providing some degree of insulation from downturns as 'new money' drivers from foreigners, immigrants and ex-patriots assist in sustaining demand side market pressure on prices and, in the process, bringing the prices of desirable real estate, particularly in Auckland, coastal and island locations, in line with prices of similar real estate overseas."

92 Comments

Once again the academics are being left behind by reality.

Clearly the business model that is in play is not about "buying house to live in, renting out the house as a service". This has been said time and time again on this site - clearly the houses have extra value to the purchasers which is not related to the "living residence"/"rent" model.

You could say the same about every single bubble in history. As they turned out, fundamentals were all that mattered.

2.8% return on assets, lol hard to find a worse investment in NZ. To bring that back to reality would require median prices of about 550k. We'll hit that before we hit 1m. Even with values at 22xrents and interest rates at 5.39 you can't afford to pay a 30y mortgage, let alone rates, insurance, R&M, agency fees, so I'd call that at the high end of value with more room to go down then up.

"We therefore conclude that to return the Auckland market to normalcy in terms of its price-to-rent ratio a more likely outcome is a housing price correction. Such corrections have occurred in many other countries that have experienced house price inflation in recent years."

or maybe more persons per area of land/rental, increasing returns, maintaining prop values, whilst keeping rent per head stable?

Would that be what happened in Tokyo?

..sth awkland

Note that Christchurch had massive rent increases but these have tracked with prices unlike in Auckland.

A lot of those rent increases were because of the EQC. If you had to relocate, you received a rent subsidy, and once you were on the gravy train landlords were obliged to hike the rents. For some it went from 250 up to 300 a mere 20% increase, but for others rent went from 400 up to 800 a 100% increase.

That's because in Chch there was actually a shortage of houses. Rent prices are a more accurate way of measuring offer and demand than house prices.

In Auckland the offer is not large, but there is not such a shortage as the media constantly mentions, otherwise rents would have increased in a similar way as in Chch.

Yes the rent increases in Chch were a localised phenomena, from three sources.

Subsidisation, which allowed rents to increase so average people could bid for properties normally out of their reach, and

Private credit -in the form of promised wage increases to stay in the area or emergency premiums- or because people were securing that credit against incoming insurance claims, and

Legislation. By FORCING some landlords to re-house tenants that were in poor properties, the paying landlord had to liquidate some of their equity, the lack of choice in the matter meant demand was extreme so either bankruptcy or liquidation was the only choice. Paying landlords were often adversely affected hampering recovery further.

The point here is that Chch had a major shortage which caused rents to sharply increase. House prices relative to rents stayed relatively stable (actually dropped slightly relative to rents) - a pricing increase caused by a shortage. In Auckland house prices are rising without rents keeping up - a price bubble.

House prices Vs Rent 'prices' needs a closer look, and if you do it will show there is no possibility of rents jumping a third.

House prices are set by the 1% or less recent house sales to the few people willing to pay those market prices... everyone else sits out and watches their own home skyrocket in value, unable to participate as the prices are now out of their reach.

Rents are not set like this. If say 1% of new tenants this year pay over the top rents (due to shortage or whatever) it does not automatically create a re-rating of all rents of similar properties (i.e current tenants dont get a letter saying their rents have now increased 50% due to 10 local bond submissions in the area!!).

And for rents this cant happen, as unlike house prices, the incumbents dont just sit uneffected by increased price, but would need to actually pay more (met the market themselves) for the 'price' to be accepted.

So basically, rents are what you watch, not house prices, which can be effected by a relatively small % of house sales to a few irrational people...

When academics models don't match reality, academics should be asking themselves "what's wrong with my models". None of them take into account the new ZIRP, QE, accumulated wealth world that we live in.

Okay so 55,000 new migrants , and only 6,000 new houses built .

Its not rocket science , the only thing that can happen is rents and sale prices will go up until the ceiling is reached or migrants give up coming here .

Three things to bear in mind :-

1)The market is usually right

2) Auckland houses are way cheaper than apartments in Hong Kong or Shanghai in terms of selling prices .Rents in Auckland are also way cheaper than Shanghai ( a small one bed apartment in a good part of Shanghai is $2,500 a week to Auckland's $400)

3)We are likely to get more migrants this year than last year

the rent ceiling has been reached which is what the academic research actually says, it's a s curve and it's topping out.

Which means that rents can't go up much more, and so whatever is driving the sale prices -already- is rent related (although rent might be a factor). That is -why- the old model is contra-indicated.

Yes Boatman. The market is always right and when prices plunge as the the bubble pops it will prove that principle.

Hong Kong is five times the size of Auckland and Shanghai is ten times the size. You are comparing massive world cities to a middling city in a tiny country that doesn't have sufficient income to sustain these prices.

It's a bubble and you will keep denying it until it pops, because you're a heavily vested interest.

New Zealand has a housing bubble no matter how much John Key or others deny it.

According to this study:

1-In relation to incomes, rent haven't grown much

2-House prices, however, have increased so much that they would require a 33% drop to be aligned to rents and incomes. Hence they are overpriced and we are seeing a bubble getting out of control.

3-At current prices, there is a 2.8% rental return. So buying a house to rent it out makes little sense as an investment considering that by just putting this money into a savings account you already get 4.3%

So.. my conclusions on this:

1- THERE IS NO SUCH A SHORTAGE OF HOUSES. I don't think there is such a huge shortage of houses as some media constantly mentions to explain the increase of purchase prices. If there was such a big shortage rents would've increased at a similar pace as prices. Rents tend to be a more accurate way of measuring offer and demand than house prices because in house prices there are additional factors such as rate interest loans, speculation and irrational common social beliefs and behaviors.

2- THERE IS, HOWEVER, AN INEFFICIENT APPROACH TO BUILDING. By spreading cities, using productive land to build houses and anti-ecological gardens, building one storey houses and hence requiring more material in asphalt, pipes and general infrastructures.. the house prices increase due to an inefficient usage of limited, and otherwise productive, land instead due to a shortage (lack of offer).

3- IT'S PURELY A SPECULATIVE MARKET. People without assets are simply unable to buy a house in Auckland. Not because they don't want, unfortunately they seem to want to do it, but fortunately there are restrictions such as LVR and the reality of their incomes that prevent them from taking on huge loans to buy overpriced assets. Those first home buyers without assets who still want to buy a house are rejected from the market and have to purchase something on the outskirts in, otherwise, less desired areas. The ones that are able to still buy are mainly speculators and/or already owners than can use their equity to purchase another property. Proof of that is that more than half of buyers in Auckland (I recall it was more than 60%) are already owners/property investors.

4- IF FINANCIALLY IT MAKES LITTLE SENSE TO BUY AND RENT IT OUT, WHY PEOPLE KEEP BUYING? At 2.8% rental returns buying a property to rent it out doesn't make any sense. It makes sense, however, to buy a house to sell it afterwards as we live in a country where there are no capital gain taxes and the bubble is still growing. This reinforces the idea that this is a purely speculative market where the number of players will decrease until some of them loose it all if they are too greedy or too slow to exit the market.

Also, those who decide to enter the market with no intentions of investment but with the feeling that they are "joining the property ladder" or that "if we don't buy today tomorrow will be more expensive" are being fooled by such dogmas, encourages to do so by families and by a society where ownership means "success" and where renting, or paying for a service, means "making someone else rich when I could be that one that gets rich".

5- IF IT'S TRUE MONEY COMES FROM OUTSIDE, THEN WE ALL ARE LUCKY. People tend to blame rich Chinese and other foreign investors that get cheap loans outside NZ and buy properties in NZ driving up the prices. I don't have statistics on this (is there any?) but if that's the case I would be happy to know that the balances affected by a decrease in assets' prices would be foreign banks' balances and not NZ's financial economy. The main risk of a bubble bursting is the exposure of the whole financial system to this bubble. The less exposure, the more chances NZ has to continue with low unemployment and relatively good productive investment which is, at the end, the ONLY source of wealth.

Keysian Economic Logic dictates that it's only a " bubble " if it bursts .... until then , it's just market forces at work ...

.... and after it bursts , we hope the other lot are in power to clean up the bloody mess we left behind ....

But because it hasn't popped and deflated at any time in the past 45 years , it's not a " bubble " anyway ... so go away , and get a proper career re-stocking the shelves at the Warehouse , and stop bothering important luminaries such as moi , your P.M. ....

... impeccable political reasoning , dontcha think ?

Indeed it's just market forces at work.

As long as only 30% of my income goes into accommodation (rent) I personally wouldn't have any problem with such market forces.

The problem is that:

-not having capital gain taxes creates relative poverty, hence it creates inequality in society that eventually affects us all.

-not having capital gain taxes while there are taxes on employment income creates a feeling of injustice that eventually leads people to try to avoid taxes or, worse, to try to join the speculation party because it seems to be the quickest and easier way to accumulate wealth.

-having things such as government allowing to use Kiwisaver to pay a deposit for a mortgage only helps banks and property owners, encourages debt and makes the whole society participate on that.

-having a financial system exposed to an irrational housing market puts us all at risk (especially those that will have to pay the after-party)

Houses are expensive? Market is irrational? Simply don't buy. But unfortunately it's not enough to run away from bad decisions, and that's what concerns me. If only the speculators and fools were to suffer the consequences..

CGT just makes " inequality " in society even worse ... the rich folks can afford the smart taxation advisors and accountants to run rings around and through it .... at the moment , houses are not expensive , not at all .... but the land beneath them is , that is the problem , land at extraordinary over-inflated prices ..

.... a land tax , however , is as unavoidable as rates are ... easy to implement , raises lots of money every year , and allows the reduction of tax on personal income and company profits ...

If you don't believe me , ask Bernard Hickey .... he's been a long time proponent of the land tax .

It's not "land" it's "goodwill". If it was just land then other places in NZ would show similar behaviour but they aren't so it isn't. There is some factor about that location that is providing an intangible asset of value (the intangible is why all the "bubble" noise happens). Part of that intangible is that they are price stable areas, with reasonable value protection, in a moderately stable country, all in places where a bigger fool is likely to be easily found. Those are not "land" qualities, they are intangibles qualities that you could find on any business balance sheet.

Rentals tend to be at the bottom of the market so your average rental figures are made up primarily of entry level south Auckland properties, i.e. a low number. Your Auckland average price figure is made up of the whole market, which includes houses selling for 10m plus. Common sense should tell you that the upper end of the market typically doesn't get rented out so you're essentially trying to draw parallels between purchasing a 1m + house V renting a 400k 3 beddy in South Auckland. Your analysis would only start to make sense if you compared renting a 400k 3 beddy in South Auckland V buying the same 400k 3 beddy in South Auckland and factored in the opportunity cost of a 80% LVR.

"I don't think there's a shortage of house..." WTF... are you town planner? Work at Auckland council? There are reputable sources that have categorically confirmed there is a supply shortage.

Your second point cancels out your first.

3 and 4 are just your confused opinion and lacking facts.

5. finally you get something partially right. In my experience foreign investors borrow here.

I rent a $1m+ house. Most houses round my way are $1m+ including the rentals

I paid $400pw for a house that got sold last year for $975000. It's just been sold again for $1.25mil. But no, theres no bubble.....

So all the punters claiming there will be a correction are renters... sounds like just a bunch of vested interests hoping the market will crash so they can swoop in and buy at others expense.

Or they are people who see the risk and do not participate in the market, instead choosing to put their money to good use elsewhere.

I have owned 4 properties including 2 rentals in the past (not in Auckland) but would not be taking on that risk now

I rent 1/2 a $1m+ house as well ($420 per week for the last year), a good amount of my neighbourhood is rented as well, prices would be nearing $1.8m + if not more for the average villa.

What percentage of Auckland rentals are in 1m+ areas...

I once owned and occupied a house in Hillcrest on the North Shore for 15 years. ACC valuation now $1 million. All the neighbours kept their places neat-n-tidy, lawns always mown, everything spick and span. Went back for a look-see, to revisit old memories. Now, most of the street looks like a street of rentals. Scruffy, tired, run-down, unkempt. Wouldn't live there now. And that used to be 10 minutes from the city in off-peak hour

If Auckland had such a shortage, rents would have grown more and many more companies would have relocated, like it happened in Chch.

Probably there is a shortage of GOOD properties (insulated, modern, desirable location) and that might explain why rents grow a bit, but as a whole what makes you think offer cannot follow demand?

Also, increasing the offer, when talking about housing in the middle of a bubble doesn't necessarily drive prices down (see Spain or Ireland examples of oversupply despite an increase of prices fueled by foreign capital).

As I said before there are many irrational factors when talking about buying properties so building more would only have an effect on prices once the bubble burst creating a further decrease of prices, but not before.

I believe by keeping offer low (not building much more) we are protecting the system and council is keeping things under control.

I rent. Believe me if I say I would like rents to decrease. But I rather pay what I still consider "normal" rent (~30% of income) and keep my job expectations in the future than having to suffer a big contraction in the whole economy like Ireland or Spain once the correction happens and the offer has to meet the demand.

In other words, I believe the only thing the government can and should do is to build firewalls so when there is a correction the collapse does not affect the whole NZ's economy.

Right now there is no way to stop it, it doesn't matter how much they build.

Example of firewalls:

-LVR

-Controls on the exposure of public institutions and banks to the housing market

-Not a single cent of public money to encourage debt or "development". Prevent kiwisavers from using the money to take on expensive mortgages.

-Increasing interest rates if possible to make saving a more attractive thing

-End the "property ladder" dogma, protect first home buyers from making the biggest mistake of their lives.

What the government and Len Brown can do , is get out of the way of house builders !

... they are impeding construction .... cities must grow upwards and outwards ... we need more apartments in the CBD ... and less wastage of valuable land in green leafy suburbs for the old gentrified Nimbys who want to retain their prized camellia beds , and bugger anyone else ...

Well there is the OBR and just listen to the whining on that one. Besides that I dont think we can put up walls as such as everything is so inter-dependant.

Rent is increasing, at a rapid rate, it's following prices up.

Spain and Ireland are completely different situations to Auckland, they both had a dramatic over supply, in Spain they built whole towns at a time but without the demand. Again, you're not comparing apples with apples.

Just because you say irrational factors and bubble doesn't make it so, the factors driving people to buy in Auckland are very rational and in my opinion the current prices are not over-inflated, in fact there is a long way to go.

You say you're renting and glad that works for you, but ask yourself, is what you say what you think will happen or what you want to happen? Some could call you a vested interest, if the market drops you could buy in at others expense...

I disagree on rents rising rapidly ...will be interesting to see the next set of data out, last ones showing small increase overall. Unless you have some fresh info?

Interest.co.nz in March 2015... "Weekly median rents in Manukau and Waitakere rose by 8.43% and 7.90% over the year to February 28"

the last part of sentence was cut off?.. " while the national median only increased by 4.29%."

Who cares about the rest of the country; the article is about Auckland.

Really? , the Title of the report is

"Hot Property in New Zealand: Empirical Evidence of Housing Bubbles in the Metropolitan Centres"

NZ is not just Auckland

Metropolitan areas... I.e. Auckland and Christchurch. And the article talks almost exclusively about Auckland.

In any event what's your point?

If rent was higher and leading prices I would say yes, but it isnt. Sure rents in some parts of Auckland is going up, but nationwide? not really.

"very rational" indeed its known as greed. "long way to go" when the current ratio has not got past 9 to 1 without bankers commenting there was a bubble and we are at 6~8 to 1, I cant see if as "far". Unless you think somehow NZ is unique in the world and will defy gravity like no other country has been able to, cant see why.

Does it matter if rents rise faster than prices or vice versa? You still have a rising market, one eventually catches the other. I've stated before why the old metrics are antiquated; economists have been getting it wrong for years because they rely on them. If you are interested in getting it right you need new models.

Rents cannot keep pace with house prices without destroying the whole economy due to a lack of spare cash after paying accommodation. Salaries are the natural limit to rent increases: no salary increase, no rent increase.

House prices is another story.. (again, due to another irrational factors, but it has its limit as well)

I used to pay in Kingsland $400 a week for a small 2-bedroom house. Our household income was by then around $1200, so exactly we were paying a third of our income in rent, which is acceptable.

That house was sold for $1.1 million when we moved out.

The rents would have to grow 30% to keep pace with house prices. If we had to pay $520 for the same house we would probably go somewhere else unless our salaries also grew 30%. If we stayed, we'd probably spend 20% or 30% less in groceries, restaurants, cinema, bars, trips...

How long until the demand decrease in productive economy starts destroying jobs and hence punishing even further demand? Again, salaries are the limit to rent increases.

Now lets think that NZ has had good tourism results and record of immigration. Lets also think that the Chch rebuilding has boosted economy (more construction materials, more workers spending money, etc.). What would happen to the overall demand once those things change if rents kept growing?

Rents can't simply keep pace with house prices. House prices might keep increasing for a while, until people recover the common sense, until panic spreads or until external shocks in the global economy make us go back to earth. Eventually both rents and house prices will be aligned, yes, but by correcting the deviated one downwards.

About wishing the house market to collapse.. yes, I must admit I'm looking forward to it :).

It's creating inequalities, it's favoring those who simply were here first, those who inherited wealth and encouraging growth through debt rather than through productivity, work and society development. It encourages parasitism. It discourages productivity investment.

It's something that must stop. Houses should be something were people live, not a tool to make profit at the expenses of others AND at the expense of future generations as the houses are purchased with future wealth represented by money brought to the present as a number in a digital balance: debt

I rent, and I do that because I want to believe I am a rational thinker. Would I like to own a house in the future? Sure, who wouldn't settle down in a place called home and see the trees growing and have long term projects.. but not at any price!. Certainly not at this price.

So yes, a housing price collapse for many of us means hope and return to common sense.

Looking forward to a collapse you say... If you plan on profiting at others expense you'll need to stop preaching about future generations, etc. I trust that after YOU buy you do not want the market to crash...

Not everybody thinks like you.

Who is planing to profit at other expense? I'm talking about not buying a house UNTIL prices are rational (i.e: 3 times the household annual income).

I'm talking about buying a house to live in that house, not as a step in the so called "property ladder" or similar, not as a investment opportunity, not as a speculation good.

So when I buy a house, I don't care if the market value of that house is increased or decreased. That only matters when you sell your house (until then it's just not cash) or when you use your house to back a loan.

Can't wait to see it collapse. And I hope nobody leveraged cries later saying "they didn't know". Facts are there.

I'm with jaqi on this one. I will buy a house when I can afford to live in it. For me, this means being able to pay off the mortgage in a maximum of 10 years (i.e. I can afford double the 30-year payment).

Salaries are increasing too and you ignore accumulated wealth.

If those were the only factors in the market sure.

But since clearly they are not the only factors, as cash stashing and capital gain speculation and property banking are all in play it is very important to local _New Zealanders_ just who owns the houses, lest their Lordships have the nice houses while the workers in their huts work the plantations.

Gee happy, you and boatman talk out of both sides. Trying to compare Auckland to Shanghai and Hong Kong and then accuse others of not comparing apples with apples. Sub 3/4% yields??? At the very least you need to be considering the opportunity cost of having cash locked up in that type of investment. Quite happy being cashed up at the moment, sitting on a couple of us / UK properties and waiting for the opportunity to get a bargain when this goes bang.

In a ZIRP and QE world all returns are being stretched, especially returns from high quality assets that hold their value (like Auckland houses). What return do you get from a web saver account these days...

You people have been scratching your heads for years now saying "why are Auckland prices going up?". All I'm trying to do is tell you why they're going up, why they'll continue to keep going up and why the old models are antiquated.

You get 4.5% for an online saver from Heartland. Or buy a defensive, safe share like Meridian which is yielding 7.2% (and you get a tax credit)

I rent my house for 26% of income. To but the same would cost 46% not including ongoing maintenance.

5 - Clearly it's not true.

Otherwise third world villages with multinational countries sniffing at them, would all be wealthy.

Money comes from inside - in the form of debt, especially forgiven debt.

wealth comes from assets that are still creating return (suc as a beef or sheep farm) that still gives return after the loans are paid off. It money is where the resources exceed the cost. Not just "outside" - in fact in the case of fonterra, having to push product at below real production cost just to move volume destroys money and wealth.

interesting to see wellington as well as auck actually lead the last up cycle from 2001 ish.

If you draw a line up at 2003-2004 and zoom in you'll see a similar disconnect between welly and auck and hamilton-chch prices. We are only 2.5 years into this thing. Adjustment to lower global (and local as NZ becomes 'safer') interest rates make cash generating assets worth more using a lower discount rate on the future earnings... but yes at 2.8% yields in auckland I think this has been fully played out at least in the auckland market

It's a bubble. What is it with third term governments. Can't hear the drumbeats.

as long as foreign money pours in, and foreign trading markets exist, it's not a bubble.

Ahh Academia - life in the ivory tower:) Hard to see the value in this research

The average house hold incomes is "askew" to base a report on our society, in this day and age living as couples and both earning is unbalanced.

"The two academics have concluded that the whole of New Zealand was in a housing bubble from 2003, before collapsing in 2007-2008, but that Auckland returned to bubble status in late 2013 and has stayed there since"

There was definitely no collapse of the bubble in 2007-2008, if one recalls there was a Mexican Stand Off - then interest rates fell to the lowest they've ever been.

Interesting. Anecdotally the properties I own in Auckland, based on current value-guesstimates, all have multiples of between 22 and 25. Based on actual purchase prices they are all 22 or well below. As recently as January I bought a 3 bedroom house, with land in a good area at a multiple of 22.

My own home on a full quarter acre in an SHA which has seen rocketing price increases for land would have a ratio of 25-26.

So what's going on?

The 35 times ratio represents rent of $500 p/wk on a $900,000 house. Property Investors are not working to these figures!

I don't think proper investors are buying these low yield homes. It's mom and pop who want to keep up with the Jones' and yap about their "investments" at the coffee roastery.

Yes.. but anybody who believes things like "there is a property ladder" or "house prices always go up" considers himself an "investor".

That's why restrictions to get mortgages should be even higher imo.

It is property investors, just not _local_ property investors (all jokes about "A local shop for _local_ people" aside :) )

Moms and Pops normally can't afford such high prices (the poor yield makes the leverage unserviceable)

the low yield comes from the same affect that works on low yield bonds, it's the increase in the price while the return stays the same. As they buy in at higher and higher rates , the yield which is through rent & costs has an upper bound set by a different feature (available disposable income in the form of wages). It takes an across the board move to force the price setters to move, so that the others can pass on the cost and increase the yield.

A multiple of 22 gives a (gross?) yield of 4.5%, so I guess you'd have to read the report to find out what other costs have been added in. Or it could be that median rents as a ratio of median house prices is the constant. You can do that without actually saying that the median rental has a yield of 4.5%. In other words you don't actually know the median cost of a rental property, all you know is median house price and you assume that there is a stable relationship between median house price and median rental property price and use the median house price as a proxy to measure the change over time.

Gee - My son settles in a couple of weeks on a 1993, 3 bed (83m2) Jennian home in Palmerston North that has a price ($185K) to annual rent ($270 pw) ratio of 13.2 - and I'm pretty sure I calculated it right.

It really is a different world here in the provinces :-).

nice score. Kelvin grove?

Takaro - it's on a subdivided site, but not cross-lease - own title. Nice, quiet street.

Don't get me started on the merits of p.n real estate! With 11% population students its second only to Dunedin (15% students) on that front. Add army airforce foodhq fonterra nzta ird ministry education it's classic under the radar no frills value. Obviously a free house (paid by tenants) is less attractive than gambling on ponzi schemes

Ps my last pn buy in march this year had pe ratio of 11.4... i.e 11.4 years rent pays for the house.

.. and the hospital and the councils, both city and regional.

I go for 16 years ratio because I'm a soft hearted sucker that wants people to get ahead in life. which is why I always do the doubleglaze etc. Better health for less power bill, almost no maintenance investment, got to be good.

Today's Herald has, of course, an article about this in the opinions section. One comment there is about a colleagues father who owns 53 properties not all rented, which now qualifies him investor plus residency status. Now, I reckon he is the embodiment of what has done the biggest damage in Auckland and allowing people qualify for residency via buying up houses was borderline criminal.

It is foreign money that has brought us to this

Interesting

One of the Australian media outfits today revealed the Australian government has "quietly" pulled the Significant Investor Visa residency program - no megaphone announcement

And that will make it even worse here, but of course for Key it will look like better. My Opinion-of-the-PM-o-Meter is rapidly heading toward "Detest"

Here it is - Significant Investor Visa cash cow - suspended from this Friday till end of year

Government is going to prescribe where that money has to be invested - ie - not property - but into productive activities that earn profits and pay tax - which will add pressure to move across to NZ tax haven

http://news.domain.com.au/domain/real-estate-news/significant-investor-…

This would be such a simple change for our government to make. The fact that they have not done this shows that they are not taking the housing affordability issue seriously.

Sydney house prices driven by Chinese 'bolthole' buyers

How Asian cash pumps up prices

There are four ways that Asian investment is driving Sydney house prices.

Foreign buyers continue to supercharge the Sydney housing market, accounting for more than 21 per cent of demand in NSW (statewide) so Sydney alone is more than that

http://www.smh.com.au/business/property/sydney-house-prices-driven-by-c…

significantly in that SMH article

NAB Chief economist, Allan Oster subscribes to the view that Sydney property is an attractive way for Chinese investors to move cash out of China.

"It's a bolthole, according to everyone that we talk to" he said.

Significantly, the Chief Economist is saying, everyone they talk to, and they are in the business of talking to people, so they should know

The concept of "moving cash out of China" can have several connotations - one of which is laundering money and here you have the Chief Economist of one of the big 4 banks, making a carefully crafted ambiguous statement

Both sides of the Tasman have been very 'helpful' in this regard, and I imagine if the CPC wants to make an example of one of us, NZ would be first in the firing line;

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11434880

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11400480

Well they seem to find any excuse to bag our products and hold them up at the border anyway. I'm sure once they're done buying all of Auckland's houses, our farmland, and infrastructure they'll say they don't anything to do with Fonterra.

that's why the Chinese are smart enough to buy consumables in order to acquire permanent tangibles.

Why our successive governments have been corrupt (or stupid?) enough to encourage it is beyond reason.

Further down the comment stream was this one in the NZherald

Forget CGT

Foreign house buyers should pay an "infrastructure tax"

A bit of re-arrangement should have such things as rated (for local)

and a simple "foreign ownership contribution" to reflect the infrastructure side that would be lost when non-locals purchase.

Would you like to have your blood run cold

https://soundcloud.com/user697294118/radio-ad-investment-in-nz?utm_sour…

How would you like people in New Zealand to give you around half their weekly wages?

Now if you happen to own an apartment in Auckland New Zealand, the high rent returns, other people’s money around half a week’s pay for most people, could be paid to you as rent every week. Now many people invest in Auckland because of the high demand for rents, there's no stamp duty, no land tax, and within New Zealand, generally no capital gains tax. It's an investors dream, and very affordable.

New apartments in the centre of Auckland can be purchased for as little as three hundred and ninety thousand dollars. That's right, three hundred and ninety thousand dollars, and with as little as two thousand dollars initial deposit, you can secure one today for yourself as an investment.

If the idea of having people in New Zealand going to work for you giving you hundreds of dollar per week, paying for your apartment, appeals to you, and I'm sure it does, call now.

---------------------------------------------------------------------------------------------------------------------------

Bravo National voters, your kids will be proud of you! The brighter future for New Zealand has finally arrived!!!

Don't worry, apparently that isn't happening because JK said so. How he still gets away with that BS is probably his best trick.

well the government thinks I should give them a quarter of my wages, and they don't even give me a house to like in...

Unless you're 'elderly'....

Gotta laugh at these type of articles coming out now, preparing the rest of us for the new subsidy the BB generation is about to enjoy....

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=114…

Hang on, there is no issue according to this.

http://news.domain.com.au/domain/real-estate-news/fears-about-foreign-i…

Nice unbiased view from the property investor community there. His view that your need $4m for a 2 bed in NYC is rubbish. Our old place was great, just across from financial district and similar places in the building sell for about $1.8-2m last I looked.

If foreign investors are making up 20%+ of demand in Sydney with their new property restriction imagine what it is in Auckland! At least 30/40%? who knows - no one has the data

David Hargreaves, the price to rent ratio chart above would be interesting in the context of the changing interest rates environment over time. Perhaps you could add the historical 1/NZ government 10 year bond yield to give a comparison to show how interest rates have impacted the house price to rent ratio over time.

Just eyeballing your chart it looks like in 1993 Auckland house price to rent ratio was about 12.5x vs NZ govt 10 yr yields at about 6.94% in July 1993 (or an equivalent comparison of 1/ NZ govt 10 yr yield of 14.4x)

In 2015, Auckland house price to rent ratio was about 30x vs NZ govt 10 yr yield 3.77% at June 2015 (or equivalent comparison of 1/NZ govt 10 yr yield of 26.5x)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.