ANZ's economists see "growth headwinds" intensifying for the supply of new Auckland dwellings as escalating costs and capital constraints start to squeeze the market.

"The supply side is responding to considerable housing pressures in Auckland, but barely sufficiently to keep up with demand," the economists say in their weekly Market Focus publication.

They say the twin challenges of cost escalation and capital constraints (especially in the multi-dwelling space) "risk curtailing the supply side response further".

"It all points to growth headwinds intensifying for dwelling supply. In fact, there is a risk that the above pressures actually result in a slower rate of dwelling construction over coming months.

"...Finding skilled labour is an additional issue. While there are some natural ways the ‘market’ could offset demand-side strength (increased inter-regional migration and larger household sizes), headwinds to supply growth reinforce how correcting Auckland’s housing imbalances and affordability challenges is a multi-decade undertaking."

The economists say that while Auckland house prices have cooled over recent months, with the REINZ Stratified House Price Index actually falling 6.2% month-on-month in January, this can all be seen in the context of recent LVR restrictions, lifts in mortgage rates, affordability headwinds and possibly the impact of stricter Chinese capital controls.

'Hard to see Auckland price weakness extending'

"However, it is hard to see weakness, especially in prices, extending too far, when the demand/supply picture doesn’t look set to normalise any time soon."

Another complicating factor for the supply of new housing is the difficulties the construction sector is having in finding skilled staff at present, which is also constraining its ability to respond to demand, the economists say.

"At a time when net migration inflows are showing few signs of turning, a weaker supply story certainly doesn’t paint a picture of Auckland housing imbalances and affordability challenges being corrected any time soon. We’ve already seen some construction cost inflation. However, in the words of Bachman-Turner Overdrive, 'You ain’t seen nothing yet'."

The economists say current annual net international migrant inflows into Auckland are equivalent to 2½% of the resident population. That compares with 1½% for the country as a whole.

"Statistics NZ project that under its “medium” assumptions for fertility, mortality and net migration, Auckland’s population will grow by a further 600k people (37%) by 2043.

"Right now, the region’s population is not only tracking north of that projection, but is actually north of Statistics NZ’s “high” scenario (where the population is projected to grow by a further 50%)."

The economists say there is "little denying" the strong fundamental outlook for Auckland housing demand. "And that is before you even consider whether or not there is a shortage of dwellings to begin with (we believe there is, perhaps around 20k, but the exact figure is open to plenty of conjecture)."

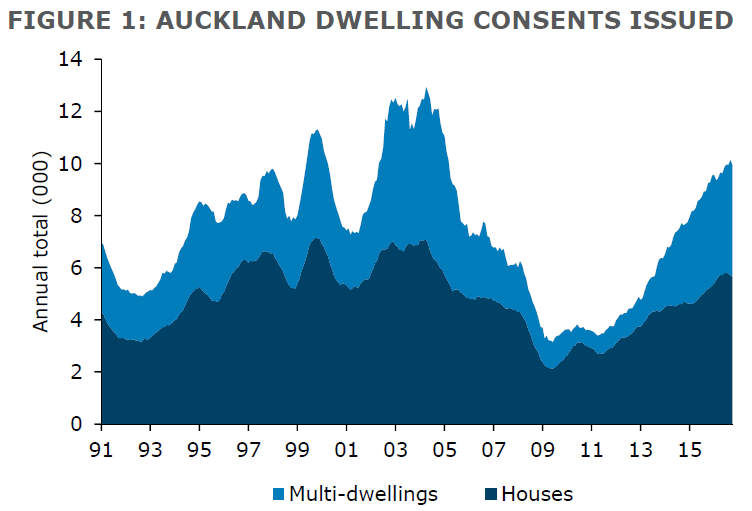

They note that the supply side is responding, with Auckland dwelling consents totalling close to 10k in 2016, which is the highest since 2004. Consents for multi-dwelling units made up 43% of that (the highest share since 2005), so there is increased evidence of intensification, "which is what the region needs to see, although we are yet to reach prior peaks". (NOTE: All the graphs in this article are sourced from ANZ/Statistics New Zealand information)

"But of course, part of this growth just reflects catch-up after a material period of underinvestment since around the middle of last decade."

Given the growth picture, chinks in the supply response is the "last thing needed right now, but that’s precisely what is happening", the economists say.

"There are increasing reports of residential development projects being delayed or canned. In fact, you can see this in the data to some extent, with our estimates of seasonally adjusted Auckland consent issuance actually falling in four of the past six months, to be down around 20% since June 2016. That’s a big drop."

The economists say some of this will be "noise versus signal", with regional monthly consents figures volatile and requiring plenty of caution about making strong conclusions. Moreover, the reasons for project cancellations can be numerous and in many cases unrelated.

"But we do believe the overall message of a weakening in the supply picture is consistent with some key challenges the construction sector is facing right now."

'Credit rationing'

The economists note that credit is now being "rationed".

"That’s prudent at the top of the cycle and also necessary to rein in a bank wide ‘funding gap’, with deposit growth still trailing credit growth. It’s not in New Zealand’s long-term interests to let such a gap persist.

"The current account deficit (and external debt levels) would blow-out, New Zealand’s credit rating would likely get reviewed, and inflation would turn up necessitating tighter monetary policy.

"Credit driven booms invariably end in busts. In playing the long-game though, less credit makes it more difficult for pro-cyclical components of the economy such as housing and construction.

"A net 32% of respondents to our Business Outlook survey reported it being more difficult obtaining credit in December, the highest since we began asking this question in 2009. So it’s having an impact."

The economists said another "canary in the coalmine" is costs, which have "exploded", making the viability of projects (and also obtaining credit) more challenging.

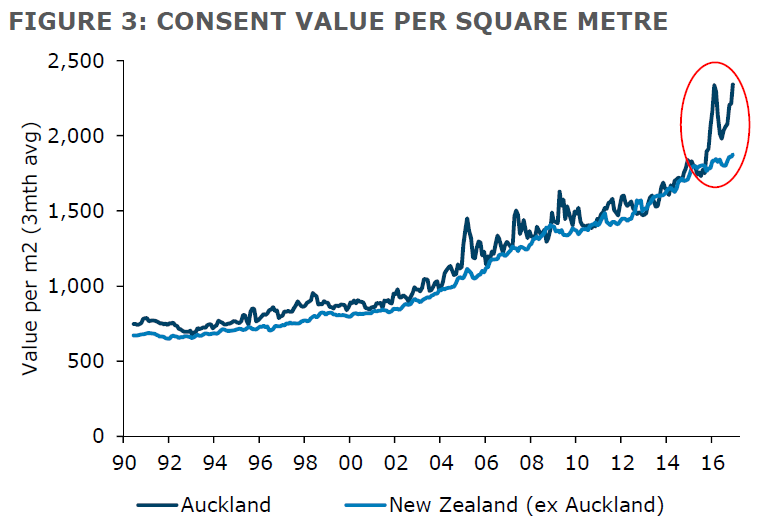

"You can see this in the difference in consent value per square metre in Auckland versus the rest of the country. It has always been a little more expensive to build in Auckland, but the gap is now historically wide, with Auckland around $2,400/m2 and the rest of the country less than $1,900/m2 (note these are consented figures and not actual costs so it is not the final word, but a useful gauge). It certainly fits with the Q4 CPI figures that showed implied construction costs rising 8.2% y/y in Auckland versus 5.5% y/y over the rest of the country.

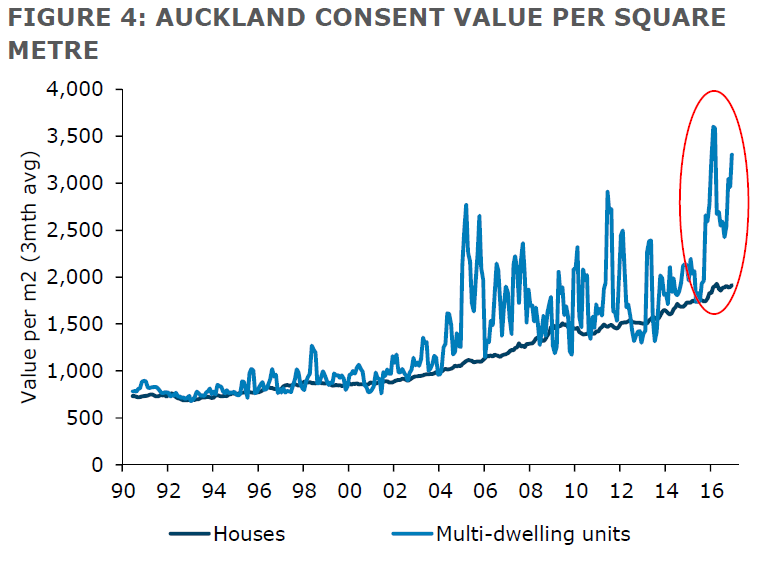

"The majority of this cost escalation is in the multi-dwelling space. Compared with ‘houses’, which have seen costs rise steadily over time in Auckland (to about $1,900/m2), the value of consents per square metre for multi-dwelling units has surged to over $3,500/m2. Now to be fair, with many developments (apartment developments especially) occurring in the CBD or city fringe, elevated land values means it just doesn’t make sense to build low-value dwellings. You need to earn a return somehow. Yet costs still appear to have reached the point where these projects are becoming increasingly difficult to make “work” from a risk-return perspective. And the “spike” in the series of late looks telling."

29 Comments

And still the immigrants pour in. When is the government going to face reality? How bad does it have to get?

Clearly the people who need houses cannot afford to build new houses at these prices. The market is completely broken and still they pump in ever increasing demand!!!!

The market is completely broken, and this government is completely broken.

Perhaps we'll look back at this government as the ones who oversaw The Great Sell-out, where younger generations of Kiwis had their city sold out from under them as a government of the boomers, by the boomers and for the boomers sought solely to inflate the portfolios of their investor voters.

It's this that makes the new state house sculpture on Queens Wharf a monument to John Key's fostered housing crisis, not our heritage.

We run the risk of Auckland becoming like Monaco , a city so expensive only the very wealthy can afford to live in

It's heading in that direction. What I noticed this weekend is that most of Auckland is a shambles and the airport badly needs more investment. I'm thinking most businesses would be better off relocating outside of Auckland as everyone is cutting work hours to beat rush hour traffic. How does anyone get any work done and maintain productivity?

J'adore Monaco, c'est une ville fabuleuse, ça serait génial si Auckland devenait le Monaco du sud

Huh?

My French is very rusty but the gist is " I love Monaco it's a fabulous city and I hope Auckland becomes the Monaco of the south". I'm guessing there's some sarcasm involved.

ANZ says that "the average mortgage payment to income in Auckland around 52% for new purchases"

Obviously imprudent lending and reckless borrowing are continuing apace.

In terms of rough calculations that get thrown around say they are at 52% and on the 4.5% fix interest 1 year. Say that goes up to the crippling figure of 6.5% in the next year or two that percentage would increase to: 6.5/4.5 x 52% = 75.1%.

The rule of thumb for housing is 25% of net income but at a stretch up to 33%. Why are banks even approving 52% with interest rates at a record low and starting to climb? It's madness.

It is ok, if banks allow 52%. This is not based on $40k income. They have a tool that calculates that you have about $600-$700 per week on hand for two people after servicing your loan (based on about 6.5% interest rate [not current rate]). In this scenario it is quite safe to lend.

You have a lot more faith in the banks' prudence then I do.

If interest rates go up to 6% plus there'll be a whole lot of people going broke very quickly.

Well, something wrong here. Looks like

Income (x) = 100%. Mortgage = 0.52*x.

Based on my knowledge we leave that poor guy with $600 per week on hands. So, if he is paying 52%, his $600pw is a 48% of income. Income comes to $1250 pw. Repayments are $650pw with current interest rate. This is a $555k loan. Then we go to assumed interest rate of 6.5% which I was told is used by the bank when I applied for my mortgage. It gives $809 pw. The person will have $1250 - 809 = $441pw left. But I was told you must have at least $600 leftover after servicing loan with assumed rate increase to 6.5%.

I think these people who say they pay 52% of income probably went down to one income from two, while when they apply - they provided combined income.

If you are a bank, how you can reject application? If his wife earned $40k, they have combined income of $1250 + $640 = $1890 pw. What is the reason to reject mortgage of $809pw? So, banks go for it. Then people get pregnant...

If I were in that guy situation, I would be unhappy to get declined loan of $555k when my income is $1890pw after tax.

What do you think bank should do? What is right?

In conclusion I would say 52% repayments is an exceptional situation into which anybody can come to (loose job, or get pregnant) way after getting his loan. And this is not a guide line for the bank to give mortgages to every one on this condition. Risk is still high if you lend to young family in their 20th. You say they will make a child next year... But some people get first child after 35, because of loan.. They think ahead...

The conclusion that you are coming to is that there are some loans in a precarious positions due to typical life events. This is very much the case. Many borrow money from other sources and end up locked into other minimum payments for debt servicing. Some may already be at their limit so any increase in mortgage payments may have their finances spiral out of control.

Sorry, just registered on interest.co.nz

I think people might loose my point in my long reply. I agree: a lot will go broke, if interest goes up to 6.5%. But this is not the original condition they got their loan. This is their circumstance changes during loan time. It is bad definitely. We need to promote 'wise spending' on mass media to make people think.

One thing that keeps coming up in research into teaching financial literacy is that the teaching has no effect. People only start taking their personal finances seriously when they are ready to focus and learn. Some propaganda may help, or at least get people to talk about finances.

There are people paying 52% of their income with the current low rates around 4.5%. If their interest rate increases to 6.5% they would be paying 75% of their income. That is not safe as you suggest that is a disaster waiting to happen.

If the RBNZ displays their usual level of stupidity and increase interest rates to 8% then that would have them paying over 92% of their income. How exactly would someone pay their bills and buy food?

This could develop into a perfect storm.

> Banks reduce or stop lending on risky over-priced multi-occupancy developments thus constraining supply

> Red tape continues to constrain supply

> Builders trade- wage charge-out rates stay at over $50 per hour

> Properties remain too expensive for working families to afford

And the whole Ponzi scheme could come apart at the seams

Nick Smith, Steven Joyce and Bill English see the cost blowouts in our construction sector as a sign of success. They talk about this been the biggest building boom ever. What a joke. No wonder John Key jumped ship -not even his considerable spinning ability could convince the public this shemozzle was the promised 'brighter future'....

Everything is so overpriced that developers don't want to touch low yield residential development, the risk of a loss is too great. I warned a select committee in 2003 about this happening. Labour didn't care, but National did. Funny how things changed once they got into power.

Successive governments have been useless on housing. We cannot afford for this to continue. I think that Labour became more serious about genuinely fixing housing when they announced KiwiBuild in 2013 under Shearer. The likes of Phil Twyford realised the party needed to commit to building more houses at scale for cheaper prices. Since then they have worked hard with announcements about eliminating urban growth boundaries to remove land bankers and speculators from the market and allow the private sector to also build more houses and more affordably.

Last year Labour really seem to twig that it was their constituents which were harmed by this housing shemozzle. It was Labour MP Jenny Salesa which helped break the homelessness story and it was this story that changed the debate about housing -it created a moral dimension. Tim Watkin the TV producer believes this was the biggest story last year in NZ because of the way it changed the conversation.

http://pundit.co.nz/content/2016-hero-anti-hero-of-the-year

This wasn't just a one-off accident. Labour backed up the concerns of Jenny Salesa with a cross-party Homeless Inquiry. Unfortunately National and Act refused to participate in the inquiry.....

It aint a building boom right now if you look at dwellings consented per capita.

Its only a boom when u look at the absolute $ figure thats blown out by massive above CPI levels of inflation.

Joyce et al are celebrating our ludicrously expensive construction costs as a sign of success - totally out of touch with reality.

The cynic in me sees some bank spin in this to encourage demand.

"Weakness in prices" means clients with negative equity; not good in an environment of increasing mortgage rates.

"The rule of thumb for housing is 25% of net income but at a stretch up to 33%"

That's much bandied around but at times irrelevant.

25% of income on $40k leaves very little to live on.

50% on $250k income leaves much more room for adjustment.

That said, there are a lot of people will struggle bigtime if rates go to 6.5% or worse still, 9.5%. long term average rates might well be around 8%

It's a rule of thumb, as such is just a first test. 25% is a lot of a $40k income but people are paying that or worse in rent and you're right it leaves them with little.

50% of $250k is a lot of money and if interest rates go up we get paid in dollars, not percentages. Someone paying 75% of $250k is going to suffer a lot.

I think we agree on this much. If someone spends 33% of their income on housing it leaves money for food and other purchases/savings etc. If someone spends 50-75% on their mortgage/rent that leaves them with very little and any changes could plunge them into debt and default. If interest rates double or more than double which percentage of housing costs is going to survive?

Anything over $124,000 houeshold income puts you in the top quintile (ie 80% of households earn less than that). There's maybe 100,000 households in the country over $250,000. Source:

http://www.stats.govt.nz/browse_for_stats/people_and_communities/Househ…

The primary factor, Tony Alexander being the biggest cheerleader for the increase in Auckland home prices has been the shortage of supply memo . Here is ANZ saying 'perhaps' its around 20K, whilst its own stratified index, drops the most since 1999. ANZ stating that there was a lack of building in the middle of last decade does not stack up against population growth at the time . Perhaps

Increased bank lending is seen as A Very Good Thing. Something to do with more money sloshing about supposedly means more money for everyone. Politically, if it is for House Building, then it is a Very Good Thing Indeed as the politicians who happen to be in charge at the time can pat themselves on the back and congratulate each other on how very clever they are and what a jolly good job they are doing.

I can't help thinking the bankers invented all this stuff and hired a bunch of academics to put it into academic long speech to make it look convincing. More bank lending means more money sloshing around for now. It also means more income for banks and therefore more income for the bank's executives, and less disposable folding stuff in the future for those clever types who did the borrowing as the steady grind of making the repayments kicks in (yes, the banks do want the money back too, not just the interest).

"The economists said another "canary in the coalmine" is costs, which have "exploded", making the viability of projects (and also obtaining credit) more challenging."

I think this is one of the most important and under-discussed issue on housing inflation. How can the prices possibly come down when the replacement costs are so high.

If demand drops off material costs, some labour costs and profit margins will drop. If contractors are light on work they will price accordingly. At the moment everyone is busy and puts in high fees to scare people off.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.