Banks love lending against property.

New data out from the Reserve Bank reveals just how hooked on property they (and we) really are.

Assuming all rural lending is secured on property, more than 80% of all bank lending has property as its base.

The RBNZ data series S31 has now been extended to show how much business lending is, for "commercial property".

This series already disclosed how much was being lent for housing, split between owner-occupiers and residential property investors.

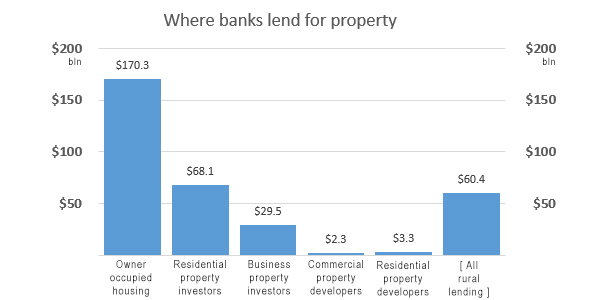

All up, banks have lent $422.7 billion to Kiwi borrowers as at the end of September.

40.3% of that lending is to households for their housing,

16.1% of that is to residential property investors,

7.0% is for business property investment,

0.5% is to commercial property developers,

0.8% is to residential property developers, and

14.3% is to rural borrowers.

All this is supposedly long-term lending, except for loans to property developers who will roll over their facilities by project every two or three years.

This data is only what banks lend. There is likely more lending going on via the non-bank sector although it is likely to be quite small.

The total of these bank loans for property is $273.5 bln excluding the rural component, and $340 bln including it.

That means banks are only lending $82.6 bln for purposes that don't have property at its base.

Real estate as security gets significant encouragement in the way the RBNZ regulates capital adequacy. Banks have responded to those signals, loading up their balance sheets with loans backed by these types of assets.

Our banks are not "trading banks"; rather they are overwhelmingly "mortgage banks". There are substantial risks in permitting this structure, the main one being it enables excessive financial leverage. But banks will never argue against leverage - they themselves are leveraged at an even more extreme level.

13 Comments

Scrambled.

A chunk of that 40.3% secured against housing assets would be used for business purposes. Is there any data on the ppn ?

Real estate as security gets significant encouragement in the way the RBNZ regulates capital adequacy. Banks have responded to those signals, loading up their balance sheets with loans backed by these types of assets.

Exactly

RBNZ officially condones capital leverage in the residential mortgage bank asset class - especially for the four pillar Australian banks. Reduced loss absorbing bank shareholder capital contributions commits OBR exposed depositors to take responsibilty for possible insolvency related balance sheet deficiencies.

The problem is a property market crash will mean the value of those mortgages is not supported by the value of the property. The banks could easily become the primary property owner in the country in the event of a market collapse and it foreclosing on mortgages. No worries though, they'll still screw the mortgage holder for every last cent, until he goes bankrupt!

This will make you smile!

https://www.westpac.co.nz/home-loans/calculators/property-investment-ca…

Look at line item two!

Estimated Capital Gain - mine defaulted to 3.00% - % of property value. Then refers to:

https://www.westpac.co.nz/home-loans/property-investment-hub/investment…

Too funny!.

The default rate is 6.50%.

Banks ALCO's ( Asset and Liability committees) need to constantly be aware of, and manage, the mismatch , where lending is 20 or 30 years and deposits are almost all under 60 months .

This if they get this wrong it can lead to a "run on the bank'

Which financial institutions don't borrow short to lend long? Flat yield curves are the real instability menace at the moment and capital leverage via global regulatory RWA concessions add to it.

A bank run is impossible - not enough cash ( Assets Line 1) on hand to cause the required instability of the fabricated liability base. Currently, a cabal of NZ cash millionaires with inside knowledge could empty NZ banks' cash vaults in a few minutes.

All banks borrow on short term rates and lend long... they lend 30 years long! What could possibly go wrong?

I'm mortgaged up to the eyeballs on 3 properties - I'm gambling all on black 7 on the roulette wheel. Don't worry, I blew on the dice. Wait, that's a different game...ummmm

Sell.

Sell and put your money into a bank that may possibly fail? What an awful scenario for the investor who is trying to de-leverage as fast as he can, only to find that the bank might just confiscate his proceeds of sale anyway. What options are safe these days? Scary times.

Rock star indeed

We were better off with property prices at a lower level and higher interest rates.

Mortgage interest rates are the only real fluid factor in a bank loan, meaning when rates move up (and they will) the loan cost INCREASES.

RBNZ is took a very big risk with our future for a short term balancing.

Christchurch's earthquake cushioned the GFC, the current "housing shortage" is manufactured, at best over stated, so where do they go from here.

For every 100 earned personal borrowings equal 163 plus. Not much room there to achieve GDP growth via people borrowing to spend.

Immigration has flat lined incomes for all but the likes of Mike Hosking. 1ZB & TV1 could save 75% of Hoskings wages by replacing him with a Middle Eastern Uber driver!

Immigration was Nationals answer - lost them the election

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.