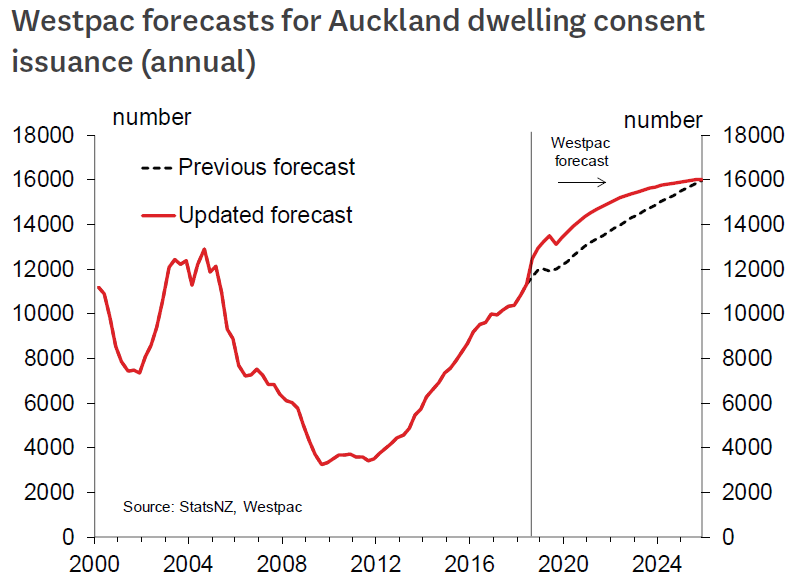

The recent strong surge in Auckland building consents has prompted Westpac economists to substantially lift their forecasts of near-term residential building activity in the country's largest city.

In a new Construction Bulletin issued by Westpac, senior economist Satish Ranchhod says Auckland's now entering a "new phase" of the construction cycle due to the combination of increasing construction and now slowing population growth.

"The shortage of houses in Auckland that has been growing for years has now started to flatten off, and rental inflation has also cooled," he says.

"Looking ahead, we expect that Auckland will soon be consenting enough homes to start gradually eating into its housing shortage.

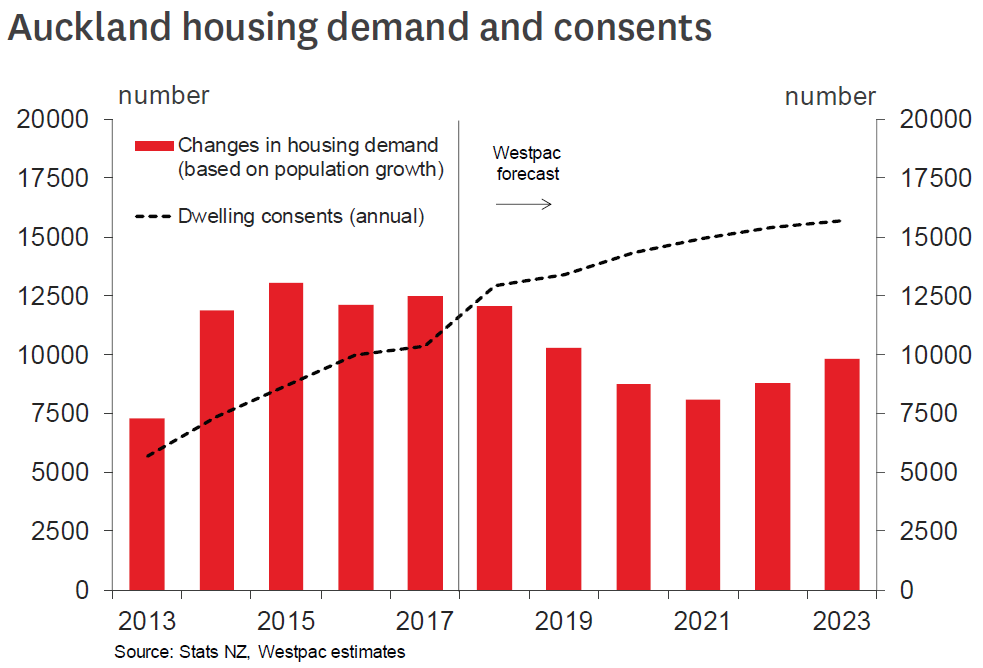

"We estimate that Auckland needs to build an average of 14,000 houses a year. And while we’re not there just yet, the underlying monthly trend in consents is getting close and should reach the required level over the coming year."

Ranchhod says Auckland may be close to building enough houses to keep pace with population growth.

"However, the region will still need a protracted period of rapid home building to address the shortage of houses that has built up in recent years. Auckland currently has a shortfall of close to 30,000 houses. And even allowing for a slowdown in net migration, the population is set to grow by around 300,000 people over the coming decade.

"To address the existing shortfall and meet the needs of its growing population, Auckland will need around a decade of strong construction activity."

Ranchhod says, however, that even then, the Westpac economists would not expect that the availability of homes to return to the sorts of levels seen in the past decade.

"It’s normal for larger centres to have higher levels of population density than other regions. The employment, educational and social opportunities that larger centres tend to offer attracts large numbers of people. And Auckland is no exception. However, with limits on land supply, the resulting pressure on rents and house prices means that many people end up living in larger households, be that with flatmates or extended family."

Ranchhod says that the recent 30% increase in ‘multiple’ consents (which includes apartments and medium density houses) has been supported by regulatory changes, including 2016’s Unitary Plan, which allow for a significant increase in housing density in Auckland.

"It has taken some time for projects under the new regulations to come to market. However, we are now seeing a substantial lift in new housing developments, including a significant increase in ‘brown fields’ construction. In addition, with a shift to higher density dwellings, the size of homes that are now being consented has been trending downwards. Over time, this could help to improve housing affordability."

Ranchhod points out that consents are often issued in ‘lumps.’ That’s because a single housing development can include a large number of units.

"With this in mind, it wouldn’t be surprising to see a bit of a pullback in consent numbers over the next few months.

"However, smoothing through such month-to-month volatility, we expect that most of the recent increase in medium-density consent numbers will be sustained.

"In light of the uptick in consents, we have revised up our forecasts for Auckland home building over the coming year. We also expect that the underlying trend in consents will continue to grind higher over the coming years. However, with limits on capacity, further increases will likely be gradual. Construction firms are continuing to highlight significant challenges sourcing skilled labour and rising costs. In addition, many building firms are reporting difficulties accessing finance."

Ranchhod says that with a faster pick up in construction activity, the Westpac economists will be watching for related changes on "some other important fronts".

"First is the labour market. As noted above, shortages of skilled labour are already a key challenge for the building industry. Further increases in activity are likely to add to the competition for labour, and that could spill over to other sectors of the economy or regions outside of Auckland.

"This could also see associated pressure on wages in some sectors. We could also see important changes in inflation.

"Construction plays a key role in determining the level of domestic inflation, and we were already assuming firm levels of construction activity over the coming years.

"A stronger construction outlook would imply even more pressure on costs. As a comparison, the last time we saw the sort of pace in home building that is now needed was in the late 1990s / early 2000s. Even though that was a much shorter building cycle than we now require, it was associated with large increases in building costs."

37 Comments

Excellent news! I hope in ten years time we remember this as the beginnings of the greatest construction Tsunami.

There's far more chance nobody will remember it and those who do will remember it as yet another forecast that was wrong

That is if they actually get built.

If the economy tanks so does the numbers.

Credit is very tight at the moment. You don't need bank finance to consent a development, but you do to actually build it.

that said, remove access to easy credit and this "too big to fail" house of cards fails and many dreams and aspirations along with it.

i like your positiveness

… and I like your positivity, mate!

And isn't this exactly where kiwiBuildBuy kicks in? Assuming you want to build the sort of places that qualify of course.

Finance will happen, whether the banks want to issue it or the government wants to issue it.

If the big 4 don't want or have the means of lending to Kiwibuild buyers then what's stopping the government from directing borrowers to Kiwibank? Just get the Reserve Bank to print the money, and lend it to Kiwibank for the purpose of Kiwibuild. The houses will have already been built, it's just a transfer of title to the purchaser and then provisioning of sums back into the Kiwibuild purse so they can continue with the building.

Will also mean that tens of millions of dollars in interest will go back to the government instead of capital heading offshore.

Print money? Preferential/Government back financial institution to simulate lending?

What could possibly go wrong lol...

in all fairness - KiwiBuild will be providing an underwrite for a lot of developments - and means that builders can directly contract for an underwrite without the need for developers as middle-men

I see a recent uptick in RE desperation. You ask for a price indication, and the reply includes the LIM, title, and a blank S&P form! Also the words "Put in an offer, you might get lucky"

That does sound desperate, what area/ areas is that happening?

Rodney. Listings on trade me hit an all time high in May (2491), and even with the seasonal drop are still up 16% vs LY. Drive around Kumeu/Huapai and see all new builds with sale signs, while they are steaming ahead with more high density housing. Don't forget Millwater/Orewa area also still expanding.

These are developers that NEEDS to sell in order to stay solvent. I reiterate my previous predictions that these new builds will drag the market down. As can be seen by this report, more and more low cost terraced houses will be built which will attract FHB's. That will reduce demand for existing entry level houses, which in turn will lead to smaller deposits for the up-graders looking for those Mil+ properties.

Not sure i follow your logic

developers of $1M+ homes are catering for about 50% of buyers in Auckland today ... should they sell and change to develop smaller units then the shortage of new bigger houses will push their prices UP, and that will happen at some stage when Millwater, LongBay, Orewa, Riverhead, and Kumue reach to saturation stages and developer need to build further afield.

Building materials prices are not letting up, traders and building costs are mounting by the hour - try developing or renovating a small or medium project today.... costs are eye watering.

We will soon see a different housing market ... Average / Median prices will no longer be meaningful, each market segment has its own buyers, developers, areas/ pockets, and its own price brackets - a micro market of its own which cannot be compared with standalone freehold new built $1m+, could neither be compared with old 60s, and 70s house values.

Disagree Ecobird. Banks will soon want significant equity to allow people to trade up. The second home buyers of the future are largely mortgaged up already on their first home purchase so there won't be very many of them able to trade to the $1,000,000 market. But as rates go up, there will be many more $1,000,000 sellers who may subsequently become $900,000 sellers then $800,000 etc etc. Those that can afford to trade will continue to do so as people always need to sell and will have to meet the market, those that can't sell because of debt (there are already hundreds of these languishing on the market), get trapped or worse. It'll be a slow bleed but a big top-down correction is inevitable.

We have to agree to disagree ... not that it affects me in any way, but I see desperate ( need to sell people) all the time - and we should not expect a blanket crash or depreciation of the housing market in Auckland... generalisation is a big trap.

A beautiful fully renovated Home and income was sold 2 weeks ago for 17.5% discount below CV and over 25% of its market value .. why? not sure. But that was a epic bargain sold in auction not to be repeated. In fact even the buyer did not believe his luck!

Surprisingly, there are a lot of people on 2 incomes which can now afford updating to $1M - $1.7M range ( like buying new build as I mentioned) which are being sold like hot cake. When we all thought last year as where will the buyers of these new 1M+ houses come from after the market has peaked?.... Today, we are experiencing further sprawling towards the outer Auckland skirts and a lot of folks are updating to new.

As i said, the market is not orbiting around the affordability of FHBs who are only 21% of buyers. there are others who want the expensive spect products and apparently they can afford them.

Time will tell, but ATM, I cannot see quality house prices dropping at all in the next 12 -24 months.

However, as I said repeatedly here, What will become cheaper is the old, tired, and do ups ( anything that needs work done) .. especially those who are next to new areas or houses built around them ... in fact anything that even is in need of a bit of TLC is getting cheaper because of costs involved.

Some of these run down ( uneconomical to repair houses) need to become cheaper than its bare section value to justify buying them and erect a new dwelling on .

the foreign buyer ban has not hit yet and the Australian banking debacle is just beginning!

People get conditioned to always go up..... and sometimes they do it on 7 -8 times combined income... The brainwashing on the way up has been relentless..... I think it will be lacking any consideration on the way down..... @But the owners paid £1,000,000 for it...... 'So what, they can't afford it and I', prepared to pay $600,000...' -- we'll see what the banks twill ake I guess, there will be lots of them?

The other thing to take into consideration is:

Sure, the banks could be lending responsibly and people with $800k mortgages likely can afford to service them if interest rates hit 8% - 10%. As far as the banks and the regulators are concerned there’s no issue.

But let’s be realistic here, people will drive halfway across town to save 10 cents a litre on petrol. What’s the reaction going to be when interest costs on a mortgage go up by $100 - $200 per week?

That's when the saying "shit will hit the fan" is so appropriate

Good news for everyone ^^

In other words:

Westpac would like to see the rate of building slow down because they already have lots of silly loans that are in danger of going into negative equity and it appears that rents are sliding as well..... Please stop building!

It'd be even better if we can take away that Fletcher's bottle neck.

If this can be achieved, and I have no doubts that it can short of a recession, then the Auckland property bulls’ assumptions about prices rising forever are going to be proven wrong.

That was the course Australia took, they dodged the recession by pumping money into building new infrastructures, the drawback is the debts they have to carry right now.

More graphs disproving that nothing was going in the housing construction space whilst National was in power. It was clearly during the last Labour government that the problems started. A slow turn around after the GFC was followed by sustained improvement after that. Time to change the record Phil.

Yes, a very inconvenient graph.

Still surprises me that neither National, nor the CoL have moved to remove any of the local govt impediments to housing build (huge regulatory costs and time wastage, out-of-control health and safety, excessive land use restriction....) Relatively easy legislative changes could have a powerful laxative effect on the current house building blockages.

The other graphs relevant to your argument are these ones:

https://www.interest.co.nz/charts/population/net-long-term-migration

https://www.interest.co.nz/charts/population/population

National pumped up the need for housing and the market did not respond sufficiently.

The market did respond, house consent rate rose steadily from around 1000/month in 2011 to around 3000/month in 2017, but it is hard to increase capacity fast. It is a pity that build rate had fallen so far under Clark and didn't come up again under first term Key, but leaky home repairs and devastation of building industry by same, followed by twin impacts of GFC and earthquake repairs absorbing building labour probably have a lot to answer for in that. Plenty of blame to go around.

If build rate increase under Nationals last two terms had maintained that trajectory then new house build rate would soon have exceeded the rate needed for increasing population and would have started to eat into backlog of demand (if that existed, given that demand is very price-sensitive). It certainly would have been boosted massively by cutting $1-200k worth of central and local govt imposed regulatory costs from new builds.

Anecdotally, with the number of people I know leaving Auckland to live elsewhere in NZ it seems likely that the housing problem in Auckland has found an equilibrium and is finding a new balance - NZ borns getting out, and foreign borns and poor prepared to stay living in much higher occupancy or expense houses.

Are you trying to tell me it takes more than 9 years to start building houses?

Your reading comprehension could use some work. Or you need to learn how to build better strawmen.

It takes a lot of time to expand an industry by a factor of 3. Under national there was approx 20% growth in house building per year for last 6 years. That is a huge expansion rate for any industry that needs to find capital and sufficiently skilled labour. Particularly with the incredible slow down in the build process created by onerous regulatory and inspection process over last ~6 years in wake of leaky house issue - house building takes something like twice as long as it used to.

I work in the construction sector, the build rate slowed in NZ during the clark/cullen years because the lbp system cut unqualified 'builders' out of the market, which crimped supply greatly then the gfc basically stopped the industry in its tracks and in desperation a huge swathe of tradies decamped to oz and further afield. All the guys and gals I know have found very lucrative opportunities and haven't come home. The Key administration showed supreme lack of vision by not beginning a kiwibuild style operation to keep those tradies in country knowing full well they would be needed when the country eventually righted itself a few years later.

That only leaves to be accomplished consenting and building affordable houses people really would choose if they weren't priced out of what they really needed.

I wondering when they will start doing that?

Oh FGS, another BS report full of probabilities and assumptions from Westpac .... what is wrong with this team ? all their assumptions have been debunked by other economists .... including the estimation of 10.9% drop in prices when CGT is introduced and similar number when ring fencing is inplace ...!

Fact and numbers cannot lie, We need 16000 homes built in Auckland NOW (not in 2024) to catch up with annual growth. I am pretty sure that this number does not include Homeless people and those on HNZ list.

The other big cockup is assuming that all the consented houses will be built and that all of ones built will be SOLD ! ... Well, that is yet to be seen especially with KB shoeboxes.

By 2024 we have to cater for another 150,000 new arrivals + organic growth ... The 30,000 shortage in Auckland was yesteryear , Today's number is closer to 40000 if not more.... talk about kukuland

These guys must be threatened by redundancy if they don't issue some pleasing juicy reports like these!

So after 10? years of insufficient construction and 1 quarter of adequate construction, Westpac predicts "a new phase of construction starting"… not convinced

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.