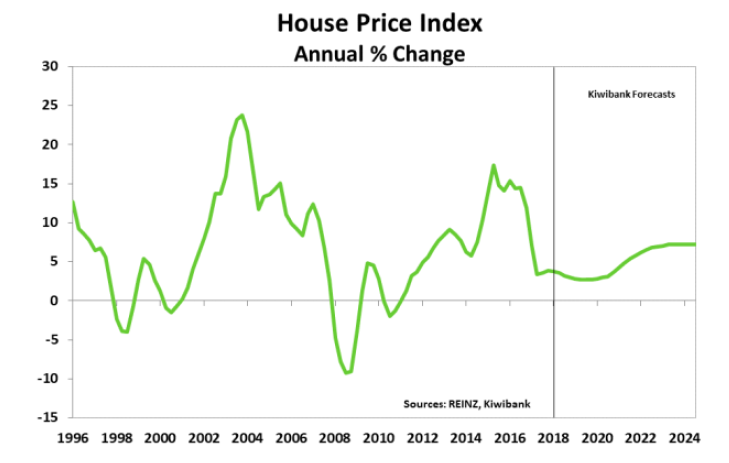

Kiwibank economists are forecasting a "meaningful" rise in the house prices into the mid 2020s on the back of continued under-supply of housing that they estimate is about 100,000 nationwide.

They are also forecasting that the Reserve Bank, which eased its restrictions on high loan to value ratio (LVR) lending at the start of the year, will not be in any hurry to further relax the restrictions.

In a 'Property Insights' publication, Kiwibank's chief economist Jarrod Kerr and senior economist Jeremy Couchman say they don’t expect a major correction in housing. "Because the fundamentals are solid, and there are no signs of any sinkholes."

They say the current supply response to the housing shortage, including the Government’s KiwiBuild programme, will eventually eat into NZ’s shortage. Until then though, excess demand for housing is likely to keep house prices from falling sharply.

"The housing market is undersupplied and mortgage rates are low. And unemployment is likely to fall, not rise sharply. Housing corrections are often driven by haemorrhaging households suddenly unemployed or lumped with rampantly rising interest rates. Neither is expected. The jobs market should remain tight. And the RBNZ will keep interest rates low. Mortgage rates will rise eventually, however.

"When gazing into the property crystal ball, you must conjure up the three Ps: Population, Preference, and Policy. And we see a Kiwi property market far from the precipice. We forecast a period of consolidation due to investor restraint, rising interest rates, and a lift in supply into the 2020s. Auckland house prices are consolidating; and the risk is they fall, but not far. A small fall would be a slight correction from past excesses. We forecast a meaningful lift in prices, nationally, into the mid-2020s," the economists say.

They note that the big surge in inbound migration - which has led to much of the housing pressure and shortfall - is now abating.

But they say even with the forecast pull back in migrant intake, it will take some time before the rate of construction matches demand.

"Even if, or when, construction catches up with increased demand, there is still the cumulative housing shortage to address.

"Our analysis shows a national housing shortfall of over 100,000 homes. And the shortage will to get worse before it gets better.

"At current rates of construction, it could take several years to alleviate the housing shortage. Despite what happens around the edges of the market, including tax changes, there is plenty of work for the foreseeable future. The mighty KiwiBuild will help, even if there is some crowding out (economist speak for ‘some of it was going to be done anyway’)."

On the LVR restrictions, the economists say while they expect household income growth to improve, as wages are poised to lift, its may be sometime before the RBNZ’s criteria under which they would relax the LVR restrictions would be met.

The economists say Loosening macroprudential policy may work against future tightening of monetary policy, as the central Bank moves to tame rising inflation.

Moreover, the RBNZ outlined three criteria that would need to be satisfied if it was to loosen LVRs, these include:

- Evidence that house price and credit growth have fallen to around the rate of household income growth.

- A low risk of housing market resurgence once LVR restrictions are eased.

- Confidence that an easing in policy will not undermine the resilience of the financial system.

The economists say it could be argued that all three criteria have been met, "but it’s certainly not definitive".

"Credit growth is slowing, but household income growth has yet to lift materially. The need to guard against excessive leverage building in parts of the system remains. But credit quality has improved materially since 2016. We believe the 2nd and 3rd requirements are easier to argue, now that the housing market has cooled, with Auckland’s lead. The 1st is a matter of judgement.

"...And if the RBNZ deems the criteria to be met in the next year, we would only expect a modest adjustment akin to the last [announced] in November 2017 – shaving the LVR by 5%, and allowing a 35% deposit (down from 40%). Not a big move at all."

In terms of making up the shortfall of houses, the economists say It is all fine and good to want to build. It’s even better that we’re prepared to pay to build. "But it’s hopeless if we don’t have the capacity to build.

"The RBNZ estimate there is a 9,000 shortage of residential construction workers in Auckland alone. Auckland building consents are finally closing in on the highs recorded over a decade ago. In the year to May there were 12,300 dwelling consents issued. A most welcome development. But it remains to be seen whether Auckland can maintain the burgeoning pipeline, given the capacity constraints already felt.

"And housing supply concerns are no longer just an Auckland issue. A number of the regions around the country have seen growth in demand outstrip construction, including Waikato, Wellington, and the Hawke’s Bay.

"So in terms of undersupply becoming oversupply and fuelling a housing market correction, we don’t see it. Not in the next 10 years at least. This is neither good nor bad news. It’s a source of continued frustration. Only significant investment, and some creative policies (on migration) to alleviate labour shortages will address imbalances, over the long term."

100 Comments

All sounds a bit like wishful thinking to me.

Could all be famous last words.....

I hope someone’s keeping track of these statements

http://quotesfromthebubble.blogspot.com

One of my favourites:

“...the fundamentals that have been driving the Irish housing market for many years now are completely unique and cannot be compared to other economies. No other country can boast the levels of economic growth that have been witnessed in Ireland in the last decade; no other country has generated the level of employment generation that Ireland has seen; no other country has seen the phenomenal population growth and levels of immigration that Ireland has witnessed and no other economy can match the decline in the average household size that has materialised in Ireland in recent years. It is simply technically incorrect to assume that that Irish house prices will decline significantly simply on the basis that this has occurred in other economies where the fundamentals were so different.”

CBRE July 2009. Sounds like something Eco Bird would say. In fact, I am sure he has already said it. Bless...

Those were Interesting times Bobster.. I see Robert Kiyosaki ( the property gamblers messiah, is now predicting a doozy of a downturn) - I reckon we've probably got a few commentators here who started and finished their financial education with 'Rich Dad, Poor Dad' so that won't be good reading for a few.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

If this does get like Ireland did and people realise that the fall will be hard and be followed by a multi year slump, then there are quite a few people who may be better off just giving the keys back to the bank, letting them deal with it and take the bankruptcy penalty. Which in 'time' terms is less, actually far less, than the mortgage pain and would then give you a chance to start again in a few years time at the bottom, rather than carrying on in blind faith.. Maybe that's why we're seeing the receivers being invited into the development companies already?

After all, If you had a 25 year mortgage, repayment schedule means that you've likely paid 10% off capital after 5 years so if prices drop and don't recover (as they are going to in Australia) you'd be better off re-assigning the issue to the bank... Kiwibank must really be sweating to have produced that ludicrous statement today.

Of course Kiwibank will conjure up anything as were past the top. Aren't they the most leveraged major bank?

Yup

I saw NZH had that article on kiyosaki, I wasn’t sure if I was reading business or the entertainment section. Total garbage

I went to the Rich Dad Education promotion evening in Rotorua a couple of weeks ago. The object being to sign people up for 3day training. No intention of me signing up I just wanted to go to the free session and hear what was happening. The big push was on property investment. They said they had 200 registered, I counted over 120 there, I would suspect from what I could see a lot more than half signed up for the weekend training. This interest in property is not going to go away. These people are going to go to these sessions and come back pumped up at the idea of buying investment property. In Rotorua we only have around 250 houses for sale on TradeMe at the moment. Gather you own conclusions from this.

My conclusions:

1. You need only read one Kiyosaki book because they're all the same, and they all say: to get rich, be in business or property.

2. Signing up at get rich seminars usually seems more successful in poorer areas than in wealthier areas. For example, I once went to a holiday home seminar in Takapuna...They spoke of having gathered many sign-ups when presenting the previous week in Mangere, but few in Takapuna ended up signing up.

3. The regions will naturally follow Auckland up or down, with some lag. Auckland's flat, some regions are still feverishly pumping away. Suspect even Invercargill's still going well, despite Southland's predicted population decline over the next decades.

Properties around us in Rotorua have been bought by speculators and then turned into AirBnB. They were busy over summer but are pretty dormant at the moment. There is a shortage of rental accommodation because of the AirBnB effect. There are no bargains in Rotorua anymore, house prices have risen significantly. So have rates.

Nicely put Bobster however the Irish situation came about by ending up with massive over building the only people in the excess new places was the polish builders renting them whilel still building more excess. So until we NZ end up with a major over build there is no apples for apples comparison.

Nicely put Bobster however the Irish situation came about by ending up with massive over building the only people in the excess new places was the polish builders renting them whilel still building more excess. So until we NZ end up with a major over build there is no apples for apples comparison.

From the bit Bobster quoted " no other country has seen the phenomenal population growth and levels of immigration that Ireland has witnessed and no other economy can match the decline in the average household size that has materialised in Ireland in recent years."

Massive immigration... hmm, sounds familiar. Them that comes here can also become them that buggers off when things turn to custard.

Hi Nic Johnson,

It's those who yearn for a "major correction" who are into wishful thinking.......

But such people are lessening in number. Even in this blog, there is far less talk of a crash than there was 12 months ago.

As time moves on, people adjust to higher prices.

TTP

TTP, that's just what the "spruikers" once said about Australian property. When Sydney prices were skyrocketing, you argued loudest that Auckland bore the same resemblance as an international city. Suddenly in light of negative events you're the first to argue there is no longer a correlation between trans tasman markets. Were all markets pushed along by flood of cheap money in unison? YES.

Property is becoming a longer and even longer term investment by the day!

My wife's cousin and her husband have just sold their waterfront property in Sydney for just over $5million after several months on the market. They were originally expecting closer to $6million. Talking to the husband today they are going to rent and see what happens. He is of the opinion that Sydney is going to keep dropping further. They have used the words "tanking" and plummeting". Interesting times.

Hi R-P,

Sorry - but you are wrong.

I have always argued that it is naive to assume that what happens overseas will happen In NZ.

Choosing negative scenarios from abroad and suggesting the same is about to happen in NZ lacks credibility.

How about all the other places in the world where markets remain firm/buoyant?? Why do you consistently ignore these markets?

TTP

Deleted

TTP

Bit of advice for when you go out appraising peoples properties over the next couple of years.

1. Check when they bought it.

2. Ask them 'sensitively' what their mortgage level is.

3. If they bought in the last few years and have a big mortgage - don't waste your time, they're trapped and you ain't earning any thing by wasting your time.. There will be a fair few dreamers and a good few agents who will be silly enough to waste their time as the dream turns into a nightmare.. You should let the other agents be busy fools on the stuff that can't be sold.. You should probably stop wasting time here and spend a bit more time on the phone trying to get your stock priced appropriately..Or it'll be beans on toast like the 1000 Barfoot agents who sold nothing last month!

Good luck & very best wishes

Nic

Was anybody credible forecasting nominally flat or falling prices? I think most realise that even if Kiwibuild delivers it will still leave supply very short over almost any forecastable future timeframe.

Well, I guess KiwiBank has crunched the numbers .. clearly they believe people can afford mortgages in excess of $600,000 and renters can afford to pay speculator's mortgages.

Wonderful to hear Kiwi's are so well capitalized - living the dream!

Its not just Kiwibank, its all of them. Had a play with the ASB mortgage calculators last night. It appears 7x income is the lending limit if you can find a 20% deposit. Mortgage repayments + living expenses seems to be capped at 80% of take home pay.

Nothing but a fortune teller.

If anyone could predict at least 6 months ahead with at least 75-80% probability, they would be miraculously rich.

So sayeth the men from the Anglo Irish Bank marketing department. “Strong fundamentals”. We’ve heard this all before. Kiwibank are so knee deep in the residential mortgage market they can hardly say anything else. They are well short of the biggest players in overall scale but last time I looked their proportion of loan book allocated to the residential market was well in excess of their peers.

Are these articles from bank economists copy and pasted?

It could be sinking like the Titanic and they would be mildly optimistic

Yawn

They say prices will be maintained or increased due to demand for accomodation. They assume current elevated prices are due to that excess demand. They say the fundamentals are strong, yet a key fundamental (rental yield) would indicate to me that prices are well in excess of a level that reflects that underlying accomodation demand. I think they have completely missed that today’s prices are predominantly caused by the loose credit conditions facilitated by the banks. Those credit conditions are now tightening, and as they tighten I would expect to see pressure on prices. So all this stuff about “supply and demand” for houses as accomodation supporting current prices seems to me a pretty weak and incomplete analysis. The market for houses is not principally about demand for accomodation, it’s about the state of the mortgage market.

Isn't there a housing glut coming up in Australia with a huge amount of apartments coming to completion in the next year? Did they allow for a mobile young workforce?

Yes there looks to be a large number of apartment completing in Sydney and Melbourne over next couple of years. To date rent increases in those markets have been roughly like auckland, their yields are as abysmal as ours

I'm a Kiwi in Melbourne. Moved just over a couple of months ago (I think Greg's piece on the new brain-drain is spot on). My personal observation from following a few rental listing over the last few months is that rental listing length - thus vacancy - are increasing, and that landlords are starting to take small haircuts on the asking rents.

Interesting times.

Agreed - although I'm not sure about credit conditions now tightening?

In the form of lower income multiples, increased scrutiny of borrowers living costs (ie poverty line subsistence no longer assumed) and reduced IO loans. I think the banks have been applying here what is now happening to a larger extent in Aussie.

Hi thegic,

It's actually the floating of the Titanic that people are becoming mildly optimistic about these days.

Modern technology together with bank financing make just about anything possible........

TTP

Media : One day will come out with gloom and next day with boom.

Nothing new.

More important is affordability, if overseas money is really banned in true spirit by the government - houses at current level are unaffordable to Kiwi unless buying second or thrord property.

Even today houses are being bought by foreigners and are buying in heaps atleast in Auckland as are worried that the ban may come soon.

Last from parliment : https://www.youtube.com/watch?v=Zt_4unRBal0

Tomorrow and may be day after tomorrow Overseas amendement bill should be ready for third reading in the parliment and if government really wants can be a law by next week (IF the government wants)

Also will the intereste rate remian such low forever or will it go up.......Affordibality is bad and if the interest rates goes up by few percentage, God save many who are buying or have bought in desperation beyond their affordability.

Big question is IF the government has the desire...…..

Wait and Watch how they will delay and dilute the bill. Politician's be it National or Labour or others...…….

They've already diluted it so much that its practically useless. Similar to how Australia's foreign buyer "ban" has so many loopholes you can drive a Great Wall truck through it.

Andrew Bayly from National sounds like a hysterical screaming baby. What was his point? that the OIO currently processes 150 applications per year and after the bill passes they will process a larger number.

If only the banks were still handing out money to every povo who wanted to buy a house! There might be 100,000 people needing homes but unless all 100,000 can qualify and service a mortgage, there is no housing shortage and nothing to sustain high house prices. Price will be determined by the number of properties being put on the market and the number of buyers who can get financing (and for what amount).

Plus, the more house prices fall in places like Christchurch due to over supply, the more the exodus of people from Auckland will increase.

Given all the negative economic indicators: Abysmal business confidence, falling growth, lowering pop growth (reduced immigration/rising emigration), rising unemployment and soon highly inflationary rise in min wage as well as regressive industrial relations laws it seems wildly optimistic to anticipate a business-as-usual situation.

House building rates (35000/yr+) seem likely to be outstripping pop growth in near future, taking pressure of supply side. I'd be surprised to see house prices fall a lot due to sky high build + regulatory costs, but there is nothing to keep them rising other than build-price inflation. And interest rates are more likely than not going to go up from current historic lows pushing house prices down further.

My simple take on housing at present. Housing turnover or sales is a lead indicator of house price. House sales in Auckland and nationally have fallen in the past year (REINZ data). Nationally sales at 75527 are down from 81352 the prior and some 42000 lower than the same (peak ) period 2003/4. Auckland sales at 21956 are down from 24459 the previous and 44 percent or 20,000 lower than the 2003/4 period. In terms of housing turnover/stock , nationally has fallen to 4 percent, Auckland on annual basis has fallen below 4 to 3.8 percent, in recent years this has approached 10 percent. The only time, that housing turnover has been at these low levels in a generation was 2008/9 , when the OCR started its inexorable descent. Auckland house prices will continue to fall, nationally ex Auckland will follow. There is no shortage just unaffordable homes for many, the decline in house prices will be prolonged. Cutting the OCR may have limited effect on a short term basis.

The graph is Interesting. That spike in 2002/03 is, IMHO, at least partly due to the stoopid Welcome Home Loan policy which, as a classic Unintended Consequence, slid a floor under hoose prices. A Universal Pricing Signal, in fact.

The current Gubmint is repeating the same mistake in KB, by setting a universal buy price for the shacks. That pricing will bleed sideways into all sorts of markets and areas - yet another price floor slid under vendor expectations.

Heck, even the price of an Awkland serviced section is not far short of that....if Trademe is anything to go by.

Kiwibank have clearly not read the comments section of Interest.co.nz

I think the comments section is somewhat more independent than Kiwibank ever will be when it comes to the mortgage market

A colleague of mine, single income, stay at home mum with 4 kids is wanting to buy a house, he's got a budget of early $300's

On the other hand, Brother in law is building a house, 3 bedroom, nothing special which will be advertised as a "the perfect home for a young family" will be marketed at $800k

I'm not saying my colleague should be aiming for a new house but something has to give...

Mark my words - Auckland’s housing market upswing to begin 2021/2022

Translated "National are going to win in 2020 and they will make house prices go up again"

They are just biting at the bit to reverse Kiwibuild, Ring Fencing, foreign based buyers ban and shorten Brightline back to two years, if re-elected. (sarcasm)

My prediction stands regardless of who wins the election. I’ll buy a hat and eat it if upswing hasn’t happened by 2023.

Small chance that ringfencing will seriously screw the market up, but if that happens we’ll be looking at skyrocketing rents instead.

I’ve never voted National in my life by the way. If the left keeps on down the loony SJW path I may do.

BuyLowSellHigh, I guess I was hoping you'd provide some insight beyond your own letterbox. You need to provide us with more than that!

I had to google SJW. You learn something new everyday. I added dogpile to my vocab as well.

I had to google dogpile.

There’s a lot of dogpiling done on this site.

BuyLowSellHigh.

I see that in the space of a couple of comments you've extended your upswing from 2021/2022 to 2023. Why the sudden pessimism? Or are you going to extend that out out further tomorrow? From what new 'base' will the upswing begin? 20% off? 30% off? 40 % off? If the upswing has another year before it starts that could see a lot more off the average price level.. I'm keen to here what the Kiyosaki/ Andrew King followers get told over the next few months to stop them selling en masse and causing issues for the NZPIF and their main sponsor ANZ....

What? You’re clutching at straws sunshine. I said that the upswing will be in 2021/22, and that I’d eat my hat if it hadn’t happened by 2023. I was then asked how much the YoY gain would be in Feb 2023, so I answered. Market will be pretty much flat until then, with no more than 5% drop next year absolute worst case scenario, probably 0% - 1% gains. So that will be the starting point for the upswing.

I’m talking Auckland here, not wherever the heck out in the whops that ‘cottage’ of yours is.

'Sunshine' Really BLSH

Can make you sweat though when the temperature gets too high though, hey?

What makes me sweat? Temperature of what? Ramblings of a madman.

BLSH - Please give me something to think about, or a fact based argument, preferably with some evidence, or just stop, you're so far out of your depth now... is it time to switch to Stuff?

To quote you

'Mark my words - Auckland’s housing market upswing to begin 2021/2022'

Do you know that you're the only person on the entire thread of comments here who has had to make a very unsubstantiated comment in emboldened writing? Madman? You could turn it to lower case but I reckon the time change on the comment would probably give you away.

Riposte?

They wont win with that guy Simon ??? what's his name as leader and they wont win when Judith Collins rolls him - who else have they got? certainly have no MMP partners and Winston ain't retiring yet!

Well, you can scratch Judith Collins after today's little effort, clearly she is an aficionado of the fakest of fake news, expecting Ardern to berate France for allowing children to consent to sex. What an absolute stupid nonce, surely you would check on the veracity of any "news" like that before getting on your high horse.

You'll have to be a bit more precise than that Nostradamus. What is the minimum YoY median increase we will see Feb '23 over Feb 22? 4%? 8%?

Auckland YoY gain Feb 2023 minimum 5%, probably 7%, REINZ stratified index.

BuyLowSellHigh, is this based on more than the fallacy "it will because it always has in the past...."? Do you have any supporting arguments other than you just mortgaged the family home to buy in Papamoa?

I understand that "DGM's make you feel sad and you can only reason with positive percentages, but seriously, what's your reasoning? Your forecast runs more optimistic to the likes of Ollie Newland for starters......

First of all, thank goodness for sunny Papamoa - with Auckland being flat, it’s delivering all my capital gains!

The absolute best way to be informed about the future is to learn from the past. Would’ve thought you’ve been around long enough to know that trends are a thing and the economy is cyclical. The cycle is going to keep on rolling as it has done since records began. Ups and downs, but overall direction is positive. The peak of this cycle was 2016. Lots of factors will start the upswing in 2021/22 - growing population and increased availability of credit for a start.

Papamoa

Most overly leveraged market of Auckland specu-vestors... have you seen how slow that market is now that volumes are declining in Auckland... Papamoa is an investors graveyard as the banks continue to tighten.... looked good on paper for a year made 5% on the 4.39% mortgage.... Not so good when you lose 10-25% capital..

Good luck kiddo...

Yours

Sunshine..

Papamoa house prices will tank 50% within the next 5 years. The current growth in BOP is unsustainable.

It’d be great if house prices continue upwards trajectory in 2021. I’m just curious though, why do you think there’s going to be “increased credit availability” in 2021?

At some point in the next 5-6 years I think we will see a 10-20% correction, off the back of an international crisis. I doubt in 10 years time prices will be higher than now

To get from Peak to Trough in these housing declines, it probably averages about 5 years. IF we are in a housing decline and houses do start to increase in value in 2022 - my question would be; what price do you expect houses to be, coming into 2022, preceding your 'upswing' prediction?

I’m picking the market will be pretty much flat until 2021/22, with no more than 5% drop next year absolute worst case scenario, probably 0% - 1% gains. Peak was about 2016. So that will be the starting point for the upswing I think.

Historically Auckland tends to plateau in between upswings, with a couple of exceptions like 1975.

How are people going to afford these sky rocketing rents you speak of? Especially with sluggish wage growth. People are already maxed which is why we have record household debt and negative household savings. These factors are already taking a toll on the economy and things will get worse if rents or prices go any higher as people stop spending on things and all the money just goes back to the banks, most of which will go off shore.

They forgot to mention the record levels of NZ Household debt, negative household savings, rising risks of global shocks to the economy, troubles brewing over the Tasman and everything else going on. In Auckland we currently have a flat Real Estate market and flat rental market and this is happening while we are meant to be having a so called housing shortage, record low interest rates and high migration. Imagine what its going to be like when some of those fundamentals change. These guys have based their scenario on a dream run. Classic bank economist talk the market up kinda stuff.

Exactly. At the very least they should caveat in these uncertain times (in their bubble they seem to think we are in fairly stable times). Lightweight stuff

Yeah it was pretty lightweight, but what do you expect from the Kiwibank marketing department. The more I look at Kiwibank the more they look like a one trick banking pony whom are a prime future candidate for a bailout.

OFFTOPIC: but its related to housing/mortgage. Came across this news in stuff. So thought of asking this in this forum. Sorry if its not the right-space to discuss .

https://www.stuff.co.nz/business/106013217/real-estate-agent-guilty-for…

Real estate agent guilty for on-selling three properties

The next property involved in the string of on-selling was on Shirley Avenue in Papakura.

The Shirley Avenue property was listed with an LJ Hooker agent based in Takanini.

The agent's recommended sale price for this was between $745,000 and $780,000, but in an arms-length deal, Narayanaraja bought this property on August 28, 2016, for $820,000.

Taylor then on-sold it the same day to Narayanaraja's brother and the Yadavs for $1.19 million.

This time Narayanaraja profited $370,000 and Taylor again received her $10,000 commission.

The third transaction happened the day after on August 29, 2016, where a property on Artillery Drive in Papakura was sold for $780,000 to Narayanaraja by another real estate agency.

The same day Taylor on-sold the property to his brother and a person called A Narayan for $1.1m.

Narayanaraja made a gain of $320,000 on the purchase and sale of this property, and once again, Taylor received her $10,000 commission.

just wondering how does this mortgage fraud work here ? They sell property to each other at much higher price and then how do they exit ? Do they just default ? OR somekind of money-laundering

I remember something like this up-selling happened with infamous Augustine Lau !

Yes it’s mortgage fraud, they get the banks money, split it and the borrower defaults or disappears or both

Past time for proper regulation of the real estate industry. It starts with the franchises being forced to employ people rather than have them as 'self employed' cowboys. That way the buck stops with the owners of the business and they have to regulate all the mistruths that the fraudsters and 'desperate' use on a day to day basis.

If they default, they will lose the deposit/equity they used for first house??

Well, yeah. They already lost it when they paid the original vendor. Put $120k down, borrow the rest to buy the place. Sell it to on to your mates for a profit, they take out a mortgage and then you all disappear with the mortgage proceeds.

Greg

Have you noticed how few 'talk it up' stories there have been on 'Stuff' recently? They can't because they are running out of positive news. Also did you notice how there was no opportunity to comment on the above article. Why? because a lot of people are now realising that the market was never underpinned by fundamentals.

High immigration of pot cleaners will be buying 1 million dollar properties. Yeah Right.

As much as I want Auckland house prices to get back to 2002 level, I think it will only reach 2007 level in the next 5-10 years.

You will need better bait on your DGM troll hook than that DGZ. Are you trying to get Houses Overpriced back on line?

Rumor has it Houses Overpriced is Boatman's son.

Nic et al. You will never be able to understand the property market as you make the mistake most intelligent people do, that is you project your intelligence onto others. You can't understand human behavior as 80% of humans are not smart analytical thinkers such as many posters are on this forum. To understand the market your need to understand who the average market participant is and how they think. Eg ask 10 random ppl walking down the street if this statement is true or false : property doubles every 10 years or so. It'll be an eye opening exercise for you.

What are you even on about? Are you a Flat Earther?

Been a regular here since 2006 probably while you were still in school... Like to drop in and get a sense of the number of frustrated wannabe home buyers to see how much demand side is still left. Plenty of fuel remaining. Especially outside of Auckland.

Been a regular here since 2006 probably while you were still in school... Like to drop in and get a sense of the number of frustrated wannabe home buyers to see how much demand side is still left. Plenty of fuel remaining. Especially outside of Auckland.

Worse.

He's from Palmerston North.

Hi Simon

I totally agree that the market is governed by the actions of the majority and that many are very easily lead by what the herd does. But what I would put to you is that when the herd of antelope run in one direction towards the water hole, which direction do they all run in when the lion pack appears at the waters edge?

I would summise that they all run the other way. Herds of antelope are not renowned for their intelligence but they are very good at running into and then away from trouble... A few of them get caught and eaten but the victims tend to be the 'slowest' to catch on to the danger. Markets are no different and the 'slowest'/most obstinate are usually the ones that get devoured. This will be no different because already buyers are catching on that the good drink by the waters edge may not be quite as promising as it used to be.

We'll see I guess, but like a good David Attenborough documentary it'll be entertaining to watch

That's a good analogy. But last time property price peaked banks had been aggressively ramping up mortgage rates into double digits - that's what you need to do to get the herds attention. The herd doesn't read articles, they chat, talk to mates, get jealous of others capital gains that they hear about at a BBQ, they fear missing out. I still think you're over-estimating the intelligence of the average market participant.

Hi SImon

When average mortgages were $80K double digit interest rates were a challenge. When average mortgages are $400K (which is where 1/3 of the country are positioned) the rates hardly have to move to have a very similar effect. That's where it doesn't matter what the intelligence levels of the market participants are they still feel it when they get choked. Disposable incomes are already running at very tight margins and conditions are very different today. The removal of the 'marginal buyer' with the foreign buyer ban could easily start an avalanche. The tightening of credit availability could do the same. An weakening dollar and price pressure on household incomes. I think things are far more precarious than you realise.

Greed and envy help to fuel extremely high market pricing conditions in all free markets.

https://www.businessinsider.com/warren-buffett-explains-how-bubbles-are…

From the May 2010 FCIC interview with Buffett

MR. BONDI: As I mentioned at the outset, we’re investigating the causes of the financial crisis. And I would like to get your opinion as to whether credit ratings and their apparent failure to predict accurately credit quality of structured finance products, like residential mortgage-backed securities and collateralized debt obligations, did that failure, or apparent failure, cause or contribute to the financial crisis?

MR. BUFFETT: It didn’t cause it, but there were a vast number of things that contributed to it. The basic cause, you know, embedded in psychology –- partly in psychology and partly in reality in a growing and finally pervasive belief that house prices couldn’t go down and everyone succumbed –- virtually everybody succumbed to that. But that’s –- the only way you get a bubble is when basically a very high percentage of the population buys into some originally sound premise and –- it’s quite interesting how that develops –- originally sound premise that becomes distorted as time passes and people forget the original sound premise and start focusing solely on the price action.

So every -– the media, investors, the mortgage bankers, the American public, me, my neighbor, rating agencies, Congress –- you name it -– people overwhelmingly came to believe that house prices could not fall significantly. And since it was biggest asset class in the country and it was the easiest class to borrow against, it created probably the biggest bubble in our history.

.. what I would put to you is that when the herd of antelope run in one direction towards the water hole, which direction do they all run in when the lion pack appears at the waters edge

Nice analogy (y)

But the herd could be forgiven for assuming that lion(s) will NOT appear there, all of a sudden. If at all, they could be caged lions or muzzled lion or some sort ...

Spare some thoughts for those antelopes who do not run to water; they may not be attacked by the lions. but could be starved to death.. slow death though . Also in the meantime they feel uncomfortable seeing the the other antelopes drinking water and staying happy for the timebeing !

Greg

But the healthiest antelopes will be the ones that don't get eaten. The 'economic' winds have changed now and many of the antelopes can smell the lion and are realising that it may not be a sensible time to go to the water hole (overleveraged position).. best to find another place to drink for now and go back when the lions have gone. The lion (bear-market), won't 'spare some thoughts' for the Antelope that didn't smell them on the wind.

Buyer numbers are dwindling, kiwi-saver accounts have been stripped, bank of mum and dad is slowly being put on hold (last months first time buyer numbers dropped massively) and with foreigners excluded there is little left to keep the water hole full.

Aren't you all forgetting about the elephant in the Savannah?

Nicely put Simon

Dp

This analysis is quite laughable, considering what has been said at other times right before severe downturns that economists did not see coming - not to mention what is happening with the Australian property market right now. Let's recall the OECD's bi-annual Economic Outlook, which proclaimed in June of 2007 that "the current economic situation is in many ways better than what we have experienced in years".

From property investor to budding property tutor and mentor in 2 and a half years ...

Built a property portfolio of 11 properties in 2 and a half years ...

Aiming for 100 properties

https://www.eventbrite.co.nz/e/learn-property-investing-with-jonathan-b…

https://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=12…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.