This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

One of my favourite charts. pic.twitter.com/XYVd71c20p

— Sharon Zollner (@sharon_zollner) May 20, 2022

1) Container shipping beats tech FANGs.

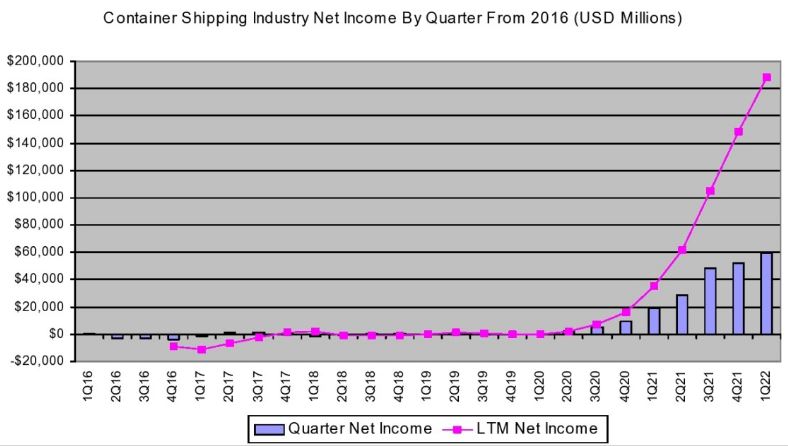

In a Top 5 last year I featured a LinkedIn article on container shipping profits from John McCown, founder of New York-based Blue Alpha Capital. One of the big beneficiaries of the Covid-19 pandemic and able to ramp up prices due to related supply chain woes, I thought the container shipping industry was doing mind boggling well then. Well, McCowan's latest article shows things have got even better for the industry.

McCowan reports the industry's first quarter net income was US$59.3 billion, up $40.2 billion from the first quarter of 2021. It was the sixth straight quarter of record earnings. He compares the container shipping sector to the profitability of the so-called FANG technology behemoths. And guess who's doing better?

2) The oligopoly of giant container ships.

Staying with the container shipping theme, this article from US publisher FreightWaves argues megaships are a key reason for the shipping crisis along with a lack of competition, noting the Biden Administration complaining about "the cartel of shipping companies" controlling global trade.

What's going on with global shipping is of huge importance to New Zealand. According to the Ministry of Transport, 99% of NZ’s imports and exports travel along global shipping routes to reach consumers.

In the 1970s, there were so many ocean carriers that no single company controlled the industry. Since then, the market has consolidated into just a few large firms.

Up to 60 of the 100 largest ocean carriers have vanished from the 2000s to today, thanks to a wave of bankruptcies and acquisitions. The top 10 largest ocean carriers in 2000 commanded 51% of the market; today, they dominate 80% of it, according to a White House fact sheet. All of these companies are based outside the U.S.

Smaller ocean carriers began forming alliances with each other in order to compete with larger carriers, said Campbell University professor Sal Mercogliano. Megashippers decided to copy the strategy. Today, the largest ocean carriers are organized into three major container shipping alliances: 2M, The Alliance and Ocean Alliance.

To ship something from, say, China to Los Angeles, you book space on a container ship operated by one of these alliances. Each company shares space on the container ship with other members of the alliance. But these alliances may cancel — or have “blank sailings” — if demand has slumped.

This system has been great for the carriers’ own financial performance. Some claim this consolidation and the alliance system lead to inflated rates.

The Loadstar, a global logistics publication, reported on April 22 that the 2M alliance was blanking at least three Asia-North Europe sailings. New Chinese COVID lockdowns were one reason for the cancellation, but Loadstar also pointed to 2M’s desire to “halt the slide in rates” amid a slump in volume from China. More canceled sailings mean less capacity for cargo, and likely higher rates.

3) Argentina's lithium riches.

Argentina, sadly, has largely been known as an economic basket case in modern times. It hasn't always been that way. In the early twentieth century Argentina was one of the world's wealthier countries. It's still rich in terms of natural resources.

A Bloomberg article describes how a recent lavish lunch in Buenos Aires featured 400 mining executives, many foreign ones by the sounds, and government officials. What are they excited about? Argentina has more lithium projects in the pipeline than any other country. Lithium, of course, is a key raw material in the batteries used in electric vehicles.

The world needs lithium supplies to grow fivefold by the end of the decade to meet projected demand as the electric-vehicle revolution gets into full swing, according to BloombergNEF. It could be Argentina's last shot at moving beyond its traditional offerings of soybeans, grains and beef to emerge as a global heavyweight in a new sector.

The country has 19 million metric tons of lithium resources that haven't yet been mined, twice as much as Chile. But Argentina has long struggled to lure the consistent, hefty international capital flows needed for mass development of oil, natural gas, gold and silver locked underground.

Patagonian shale formation Vaca Muerta is perhaps the best example. A decade ago, it was all buzz and promise. There was a special exemption from capital controls that attracted Chevron Corp. But the trickle never became a flood: Argentina's broader woes and interventions in fuel markets kept development in check.

Now, the world’s largest lithium producer, Albemarle Corp., plans to restart exploration in the Salar de Antofalla in Argentina, a more remote and less developed area than Australia and Chile, where the company has been mining so far.

4) The Brazilianization of the World.

Back before Covid-19 changed the world, much was written and spoken about how other developed economies, including ours and that of the United States, were following a Japanese path. This was primarily due to ongoing low interest rates, which Japan had experienced - alongside a deflationary environment - for decades.

But now that we have an inflation problem and rising interest rates, a new country comparison is being made for the US at least. It's Brazil. I stumbled across this via the twitter thread below.

So just to get it on the record again and elaborate a bit:

— Paulo Macro (@PauloMacro) May 6, 2022

The US is speaking Portuguese and doesn’t even know it.

The US is approx 2-3 qtrs behind Brazil in terms of stagflationary roadmap. Today’s window of US vulnerability/soft patch is where Bz was back in the fall.

1/15

In response to Paulo Macro's tweets, someone posted a link to an American Affairs article, The Brazilianization of the World. It's a bit long winded but makes an interesting, albeit not upbeat, argument.

The reality is that the twentieth century—with its confident state machines, forged in war, applying themselves to determine social outcomes—is over. So are its other features: organized political conflict between Left and Right, or between social democracy and Christian democracy; competition between universalist and secular forces leading to cultural modernization; the integration of the laboring masses into the nation through formal, reasonably paid employment; and rapid and shared growth.

We now find ourselves at the End of the End of History. Unlike in the 1990s and 2000s, today many are keenly aware that things aren’t well. We are weighed down, as the late cultural theorist Mark Fisher wrote, by “the slow cancellation of the future,” of a future promised but not delivered, of involution in the place of progression.

The West’s involution finds its mirror image in the original country of the future, the nation doomed forever to remain the country of the future, the one that never reaches its destination: Brazil. The Brazilianization of the world is our encounter with a future denied, and in which this frustration has become constitutive of our social reality. While the closing of historical horizons has often been a leftist, indeed Marxist, concern, the sense that things don’t work as they should is now widely shared across the political spectrum.

Welcome to Brazil. Here the only people satisfied with their situation are financial elites and venal politicians. Everyone complains, but everyone shrugs their shoulders. This slow degradation of society is not so much a runaway train, but more of a jittery rollercoaster, occasionally holding out promise of ascent, yet never breaking free from the tracks. We always come back to where we started, shaken and disoriented, haunted by what might have been.

5) QE versus 'a special case of helicopter money.'

It may seem a long time ago now, but in 2020 and 2021 we had an Official Cash Rate of just 0.25%, and a Reserve Bank (RBNZ) Large Scale Asset Purchase Programme. Through this quantitative easing (QE) the central bank bought $53.5 billion worth of NZ government and local government bonds.

The RBNZ embarked on QE, buying the bonds off banks in the secondary market, to keep borrowing costs to households and businesses low. It said QE would encourage the bank sellers of the bonds to use the money they received from the RBNZ to switch into other financial assets like company shares, bonds, or new lending, thus helping to inject money into the economy.

However, even before the RBNZ launched QE, overseas central banks who had pursued the policy were being criticised for driving up asset prices and worsening wealth and income inequality.

Should the worm turn and we end up back in a world where interest rates are at or near zero, their effective lower bound (ELB), with central banks striving to kick some life into the economies they preside over, an International Monetary Fund working paper offers an alternative to QE. Economist Sascha Buetzer, the paper's author, argues outright transfers (OT) would be a better option than QE. Buetzer refers to OT as "a special case of helicopter money."

In an economy at the ELB with spare capacity, outright transfers (OT) from the central bank to private households would allow for a much more direct monetary policy transmission on prices and the real economy without creating undesirable financial stability risks such as asset price inflation or unsustainable credit growth. Moreover, in contrast to quantitative easing (QE), OT would not contribute to greater wealth inequality and reduce, rather than increase, risks of fiscal dominance. It would also allow for a faster and less disruptive liftoff from the ELB. OT could be implemented within the existing payments infrastructure although the emergence of central bank issued digital currencies (CBDC) could facilitate its use and allow for a more structural integration in central banks’ monetary policy toolkits.

And;

Rather than relying on an increase of private and non-central bank public sector debt, OT would simultaneously expand base and broad money without creating new liabilities for firms, households, and governments. OT would raise the real net private wealth of the private sector, thereby setting in motion a virtuous cycle of increased consumption and investment, higher capacity utilization, and greater confidence.

Plus;

As households in regions that are hardest hit by a crisis are likely to have higher MPCs [marginal propensity to consume], e.g. due to an increase in unemployment or other cash constraints, one can expect a larger share of the transfer to be spent in such regions, boosting regional demand. In regions that are relatively less affected by an economic downturn, more of the transfer will be saved. Moreover, the part that is being spent would have a greater impact on nominal price and wage growth relative to regions with a larger negative output gap.

26 Comments

Grant Robertson is increasing government spending by almost $ 40 billion over the next 3 years ....

... Adrian Orr is raising the OCR to crush down inflation ....

Wouldnt it be easier & a whole heap cheaper if we just gloved them up , popped them into a boxing ring , and let them punch each other senseless .... 'cos they're diametrically opposed in what they're each trying to achieve for the NZ economy ...

Robertson should stop fighting Orr and start fighting the unproductive landed gentry. If he immediately taxed land at a rate of 0.25 or 0.5 % he could challenge Orr to slow down his interest rate increases because he has already hit property owners. Once the government deficit is covered he could give a PAYE tax cut to the bottom income bracket. Or a tax cut to productive businesses. Or reform local government so capital value rates can be slashed - thus supporting the construction industry.

I would support that. Turn unproductive land into productive land. Tax cuts or for active businesses rather than passive at both company and sole trader level.

More tenant taxes doesn't help anyone

Should take all taxes away, right?

The solution always seems to be pile extra taxes or costs onto landlords.

Then people wonder why rents keep rising?

Rents are a function of supply and demand and are not necessarily related to landlord's short-term input costs. A land tax would reduce demand for speculative property investment, especially those where property in untenanted sitting idle or as an AirBnB. Less property sitting untenanted would reduce rent. Reduced housing demand means lower house prices, thereby making housing more affordable for first home buyers.

I enjoyed this from the attached QEII article that you linked in your post...

"First, it is more expensive to buy assets (e.g. housing) which will prevent some people from purchasing them over time. Second, when QE is unwound and asset prices move back to their underlying value, those who purchased assets at the higher price will lose out. And third, pre-existing owners of assets are able to sell them at the higher price and realise a higher level of consumption," the paper says.

--

Wondering where exactly the underlying values are and where they will settle.

Generally it is the present value of future revenues.

Point 5: QE versus a special case of helicopter money.

The Labour-led Government, the Reserve Bank and Treasury in early 2020 had plenty of warning from TOP, The Opportunities Party, about the QE folly they were embarking on, and how the non-inflationary recipe was helicopter money and a universal basic income for all. Here's a press statement (one of many, a voice crying in the wilderness):

TOP Calls for UBI Stimulus in Response to COVID-19

Posted by Geoff Simmons on March 10, 2020

Yesterday Labour and National released their responses to COVID-19. Both are clearly out of fresh ideas.

National is calling for a regulation bonfire, but it isn’t clear what will be different from their failed Rules Reduction Taskforce in 2015. When we are on the brink of a pandemic of a respiratory disease, their regulation bonfire scored an own goal by cutting back on the need to ensure homes are warm and dry.

Meanwhile Labour are looking at handing wage subsidies to employers. This response appears to overlook growing numbers of contractors. TOP asks why give money to businesses when it is the people that need it?

“Why not just give the money directly to the people and cut out the middle-man?” asks TOP Leader and economist Geoff Simmons. “This could still be targeted at regions or industries as the Government is exploring, but TOP’s preference would be to give $1,000 to all residents aged 18-65.”

This approach, known internationally as a Unconditional Basic Income (UBI) Stimulus, was used in Australia by the Labor Government as a response to the Global Financial Crisis. Australia avoided recession and the popular stimulus package is credited with achieving that. COVID-19 has precipitated the biggest crisis since then.

There are many reasons why this is a better solution for the economy than wage subsidies. Giving people money would encourage people to spend, and stimulate local economies. It would allow people to stay home if they need to while ill. And finally a UBI Stimulus is infinitely more flexible than wage subsidies.

“While COVID-19 is a big threat, we still have a tight labour market. Wage subsidies will simply keep people in jobs where there is nothing to do. Giving people money directly allows them to move around the labour market, and ensure that their skills are used to their best advantage during this crisis. COVID-19 doesn’t mean downing tools and sitting on our hands. There is plenty to do, and people want to be useful.”

Some worry that giving people money means they will stop working, but this isn’t borne out by the evidence. Unless people need to not work (e.g. they are sick or have loved ones that are sick), a UBI doesn’t impact employment.

TOP believes that we should expect more upheavals like COVID-19. With climate change and automation, this sort of disruption to the job market will become the norm and our welfare system won’t be able to cope. “The gig economy is here and growing. We see a permanent UBI as part of the response to that and TOP will be pushing hard for that this election.”

UBI aka turning people into permanent beneficiaries?

Well every adult is provided with defence, roads, sewers and medical facilities. We are all beneficiaries of what taxpayers contribute. Any national tax is a redistribution of wealth.

It’s something that those that despise “beneficiaries" always seem to forget. There is not a single person who does not receive some benefit from the state, whether directly or indirectly.

I naively thought that with the massive handouts for covid relief that the fact would be driven home and a light bulb would glow for those who hadn't seen this.

Well I was way wrong on that.

UBI has been trialed. It is expensive and doesn't produce results at least in the short term. But the arguments you make are strong because it is very low admin cost and tricky to rort. Just change the age range from 18-65 to 0-16 and it would be cheaper, concentrates on where most of NZ's poverty lies, less likely to be spent on foreign holidays. Pay it to parents who live with the child and it nudges beneficiaries into relationships not out of them as current policies do. Generous Universal Child Benefit - GUCB.

Singautim - NZ used to have a very generous universal child benefit, paid to the mother, I think. It got less generous and then was canned as being “middle class capture” when neo liberalal economic thinking took hold. Like most universal benefits it was quite popular across all social groups and was supported by a progressive tax system. The benefit could be capitalised to fund the deposit on a house.

Do you think $11.50 per child per week would suffice?

Or whether $9500 would be an adequate house deposit?

Frank- not sure where you got that figure from, but no.

When family benefit ceased it was the grand total of $6 p/w per child and previously it could be capitalised for the 16 (or part thereof) years it was available....subject that to the RBNZ inflation CPI calculator and todays equivalent are the figures I submitted.

My figures would be $150pw for the main parent and $50 for the secondary parent but only if they live with the child. Subsequent children about half. Quite expensive but much would be returned income tax and the reduction in WFF and accommodation allowance. Expensive but how much do tax payers contribute to children over the age 5 via free education and subsidised medicine?

Maybe my figures are not generous enough.

RE: 5) QE versus 'a special case of helicopter money.'

..outright transfers (OT) from the central bank to private households would allow for a much more direct monetary policy transmission on prices and the real economy without creating undesirable financial stability risks such as asset price inflation or unsustainable credit growth.

The mechanics of such an endeavour are sadly missing - the central bank has issued a liability without a counterbalancing asset on its balance sheet and where both may reside is not determined.

Furthermore, current banking practice is not consistent with this approach.

Banks don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source.

Yep agree, big difference between money lending and money giving.

The mechanics are simple: the Reserve Bank would channel the money either through Inland Revenue or the Ministry of Social Development.

I have been following the logistic world for a while now & can remember the shipping companies crying long & loud about not making any money, which was probably one of the reasons they began merging 20 years ago. Even the graph in the article shows a negative period. Looking at the resetting of the global supply chains being talked about, the mega-shippers will be keeping their eye out for a drop-off of global trade & a potential reduction in their business model going forward, & as we've read in the article ''making hay while the sun shines.'' It interests me as NZ Inc is an exporting nation & much of what we have to sell needs shipping to our markets offshore. I have often wondered why we do not have a better local shipping industry, a topic which has popped its head up again just recently, but then I remember reading how the warfies strangled the ports in the 50's & 60's making getting stuff just from the port gate onto the ship more than 20% of the total distribution cost.

NZ Inc should be into shipping. It's a critical ingredient in our survival as a nation in the 21st Century. And will be for a while yet. I know the cloud is good but it can't do everything we need.

Brazilinisation - been going on since the 70’s hasn’t it? Maybe a short lull during lockdown

The most interesting thing I saw this week was the IMF talking about bailing out Pakistan (among others.) Since 1950 Pakistan has had 22 IMF bailouts, will this 23rd be the one that finally ushers in the governance and economic management Pakistan needs? You can probably work out the odds.

In a way what the IMF is now doing is enabling OECD countries to maintain political stability in poor countries by allowing those governments access to credit that they then use to subsidise food and fossil fuels. Unfortunately the outcome has been that the IMF has essentially ended up promoting economic stability at the expense of improving governance and fiscal management. Far from promoting international development the IMF might reasonably be said to now be hindering the development and progress of poorer countries. The cynical might say that is intentional but I would like to believe we can live up to higher ideals.

My view is that, while the IMF remains a valuable instrument, perhaps it should only be allowed to offer a credit deal once per generation and with fixed terms to avoid the cyclical situation we are promoting in Pakistan?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.